Analysis of ABM Industries Corporate Governance

VerifiedAdded on 2021/04/21

|12

|1173

|26

Presentation

AI Summary

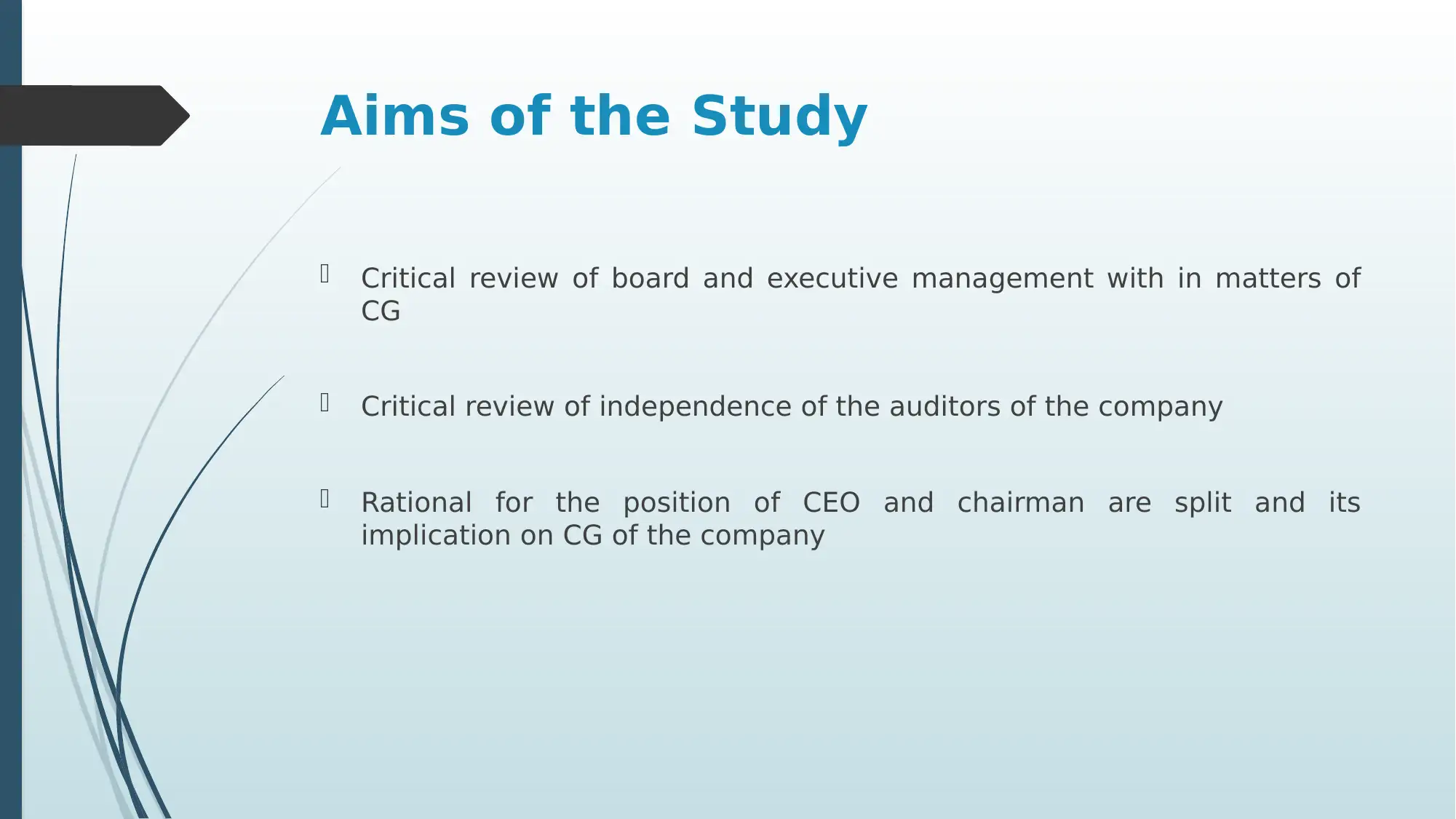

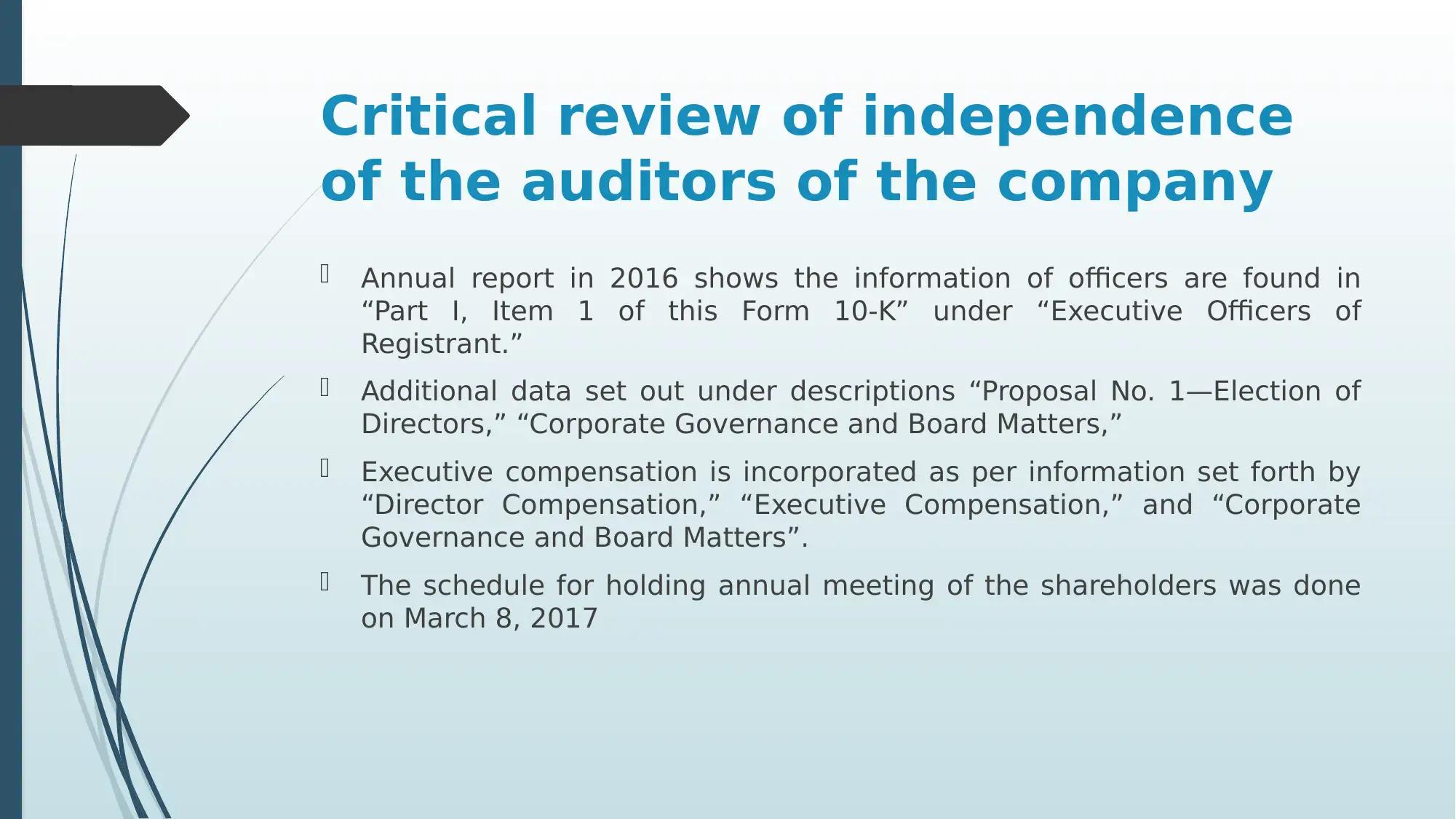

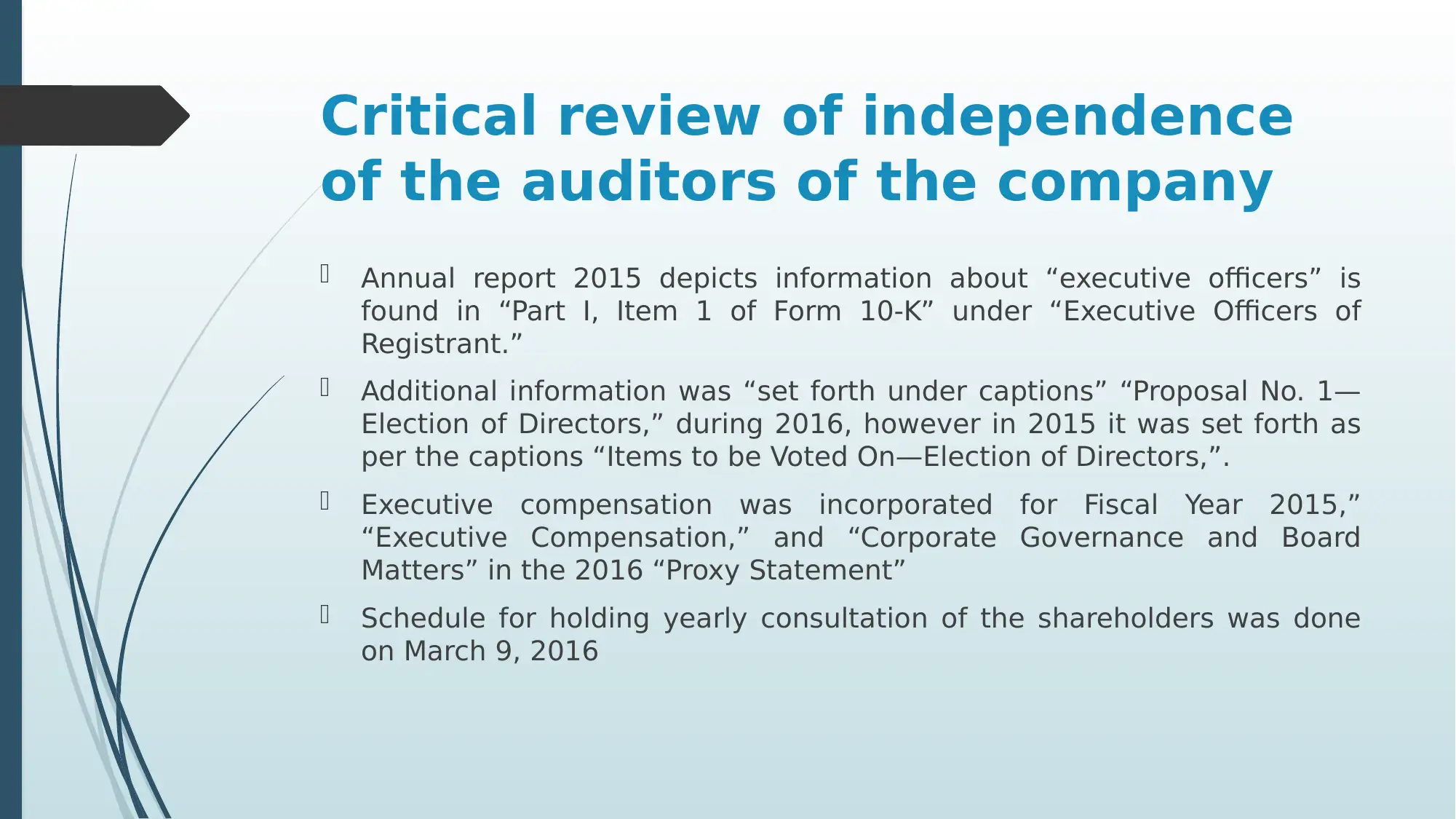

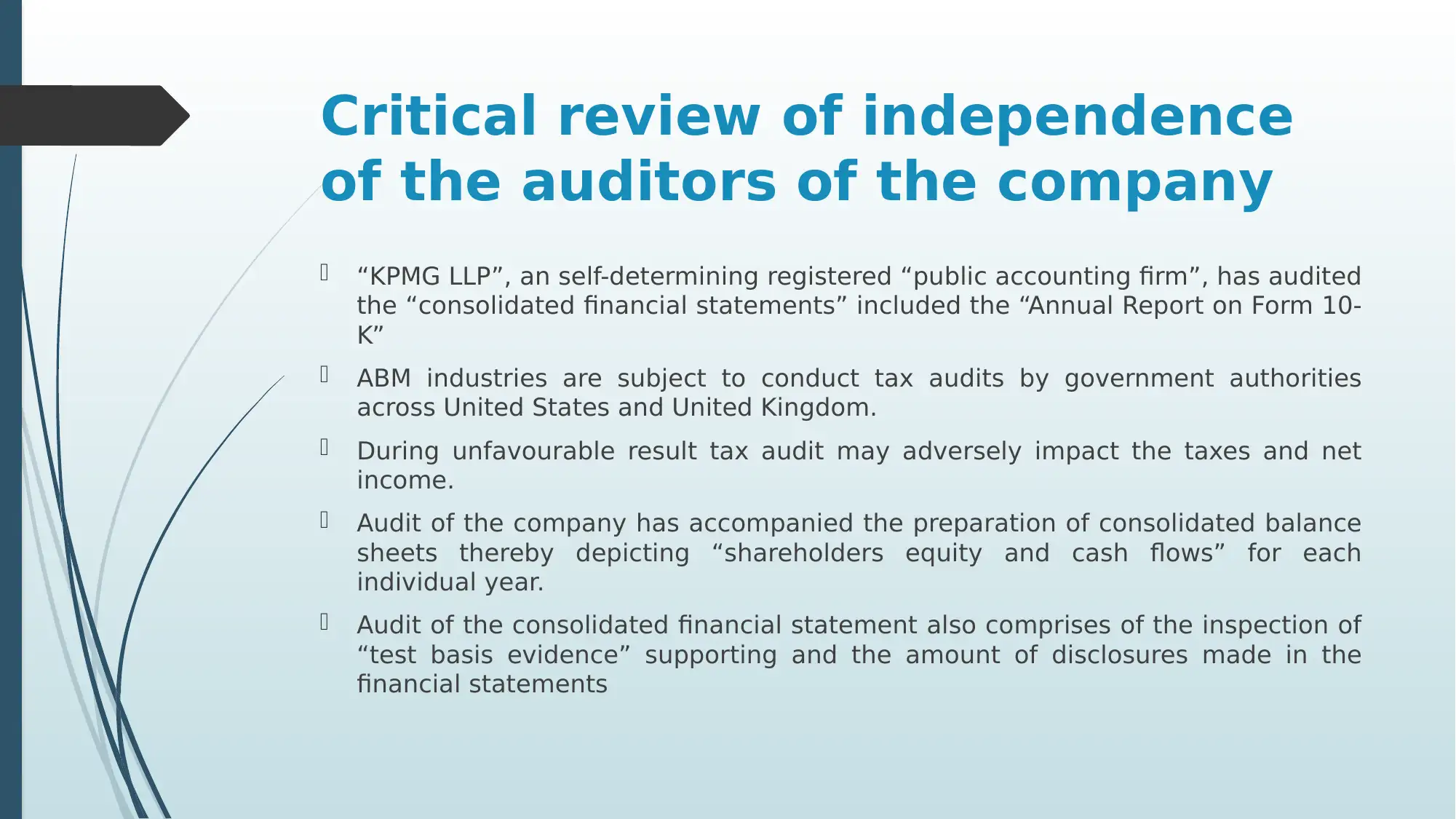

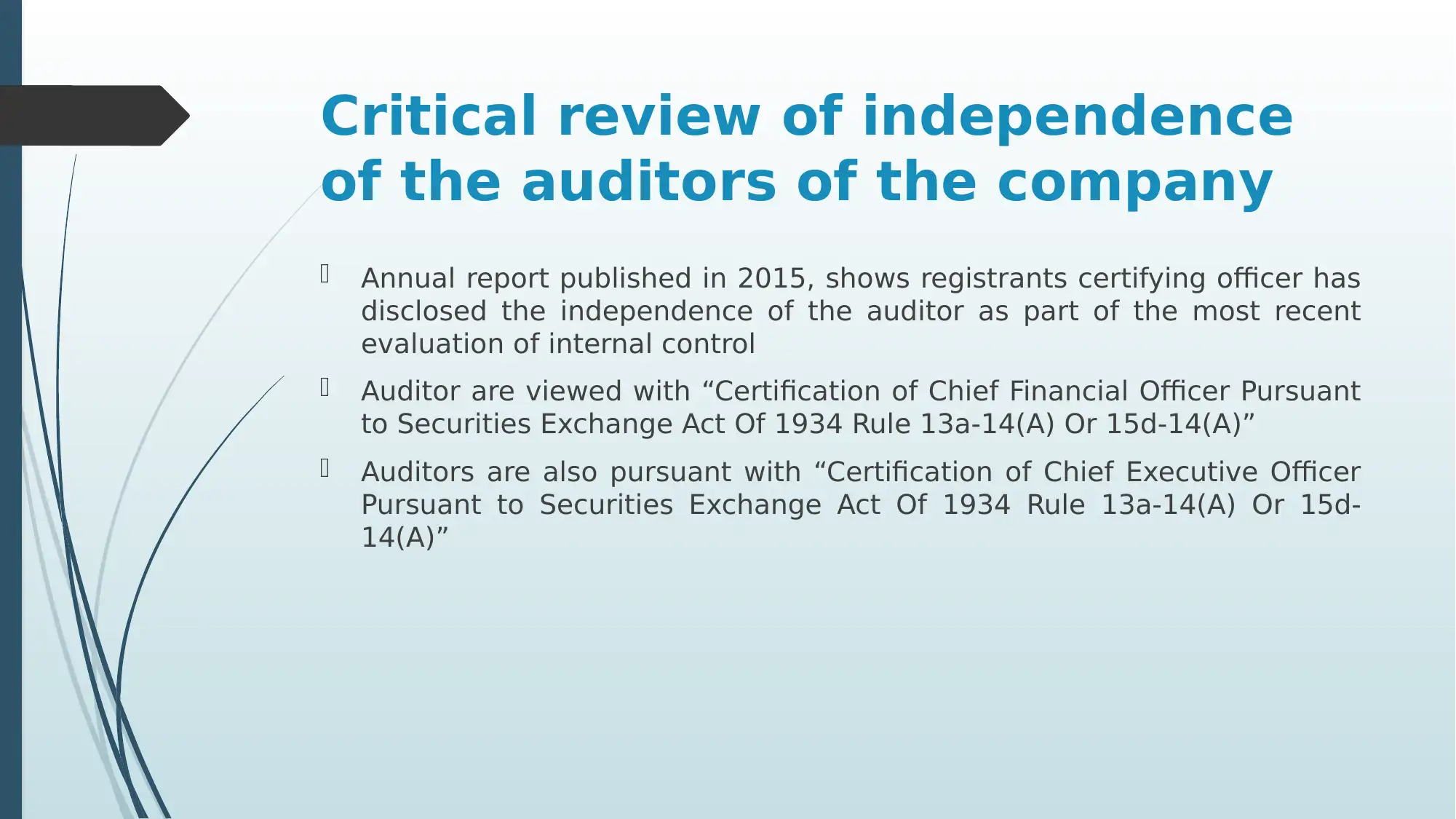

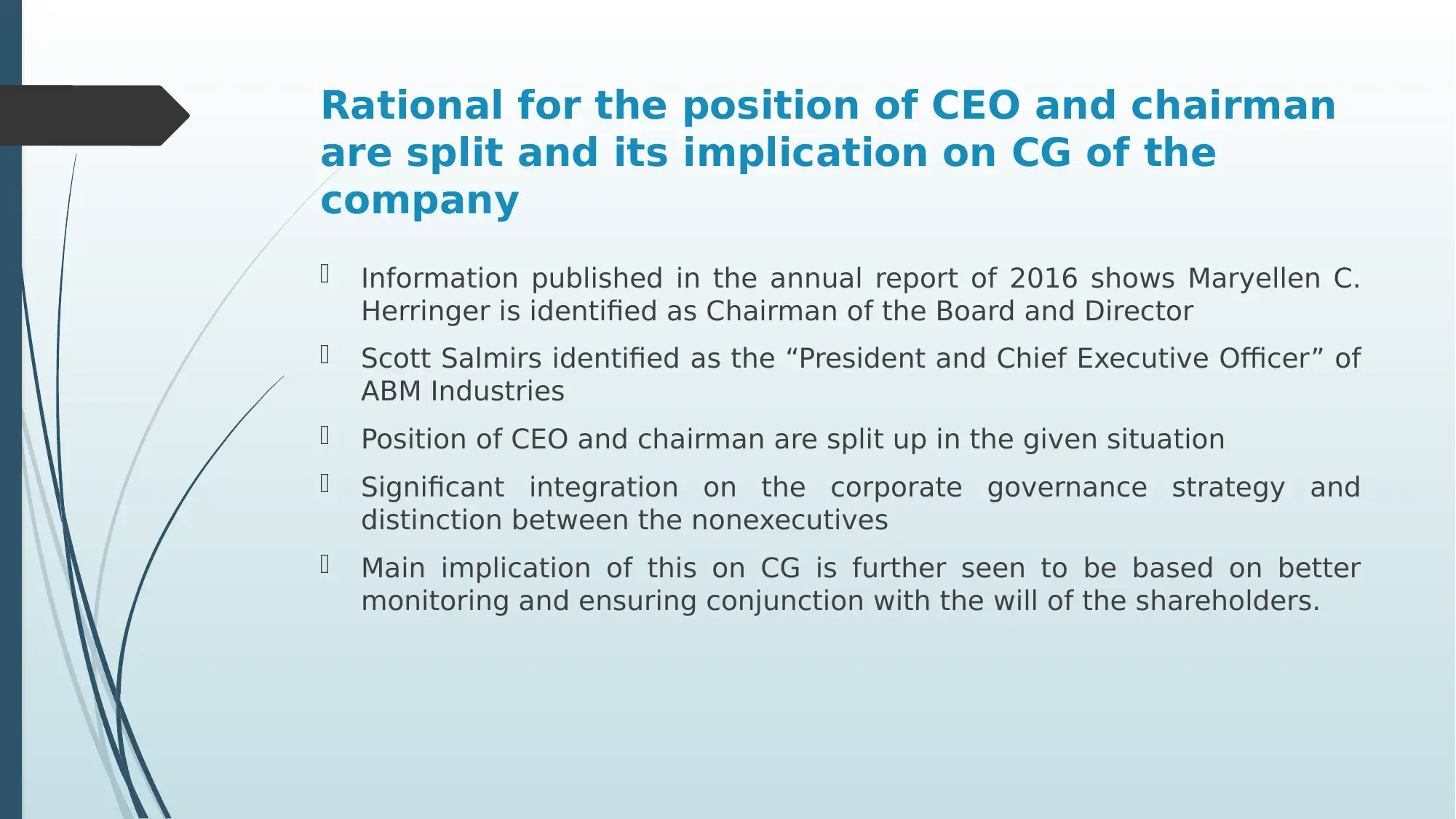

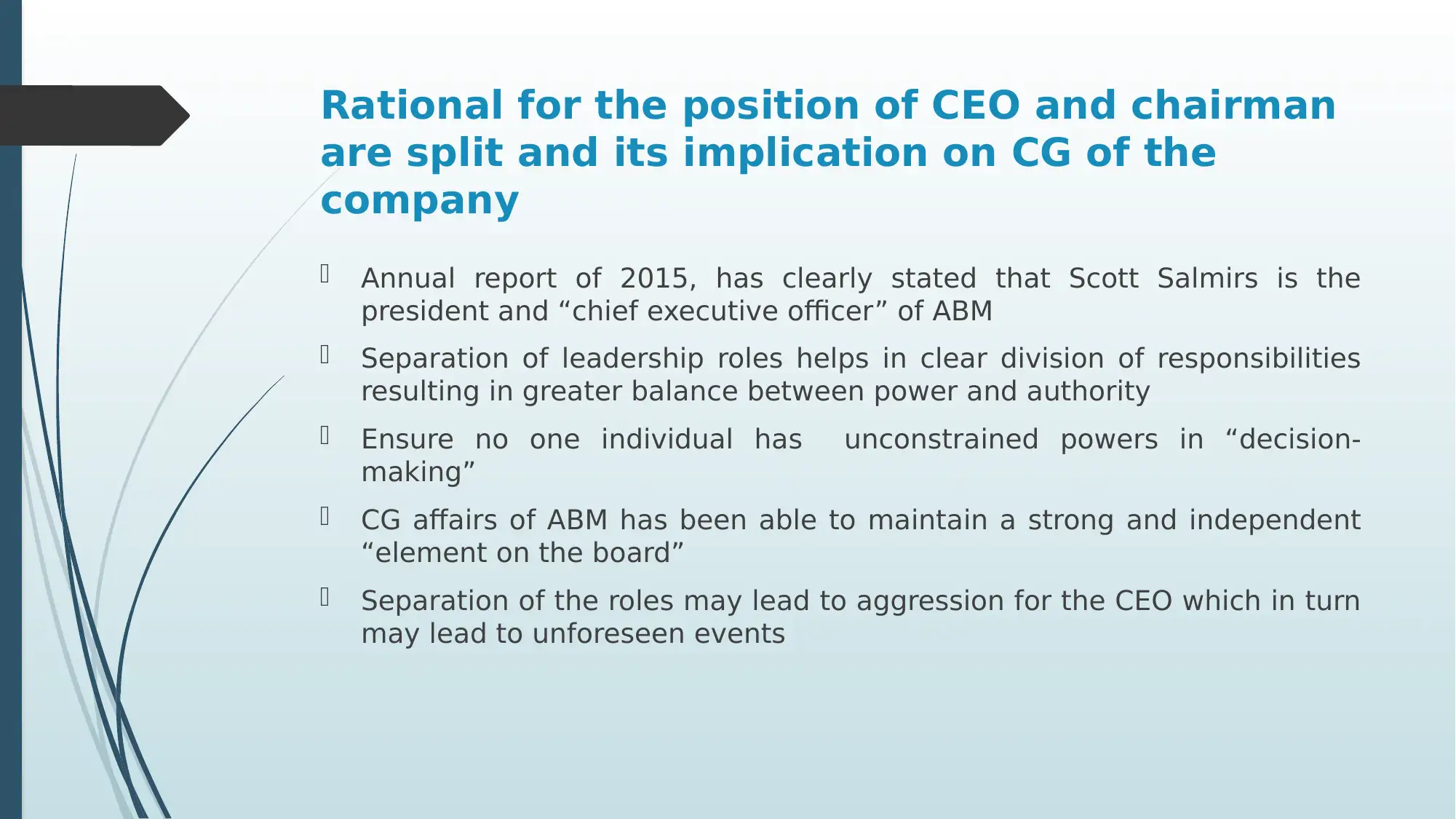

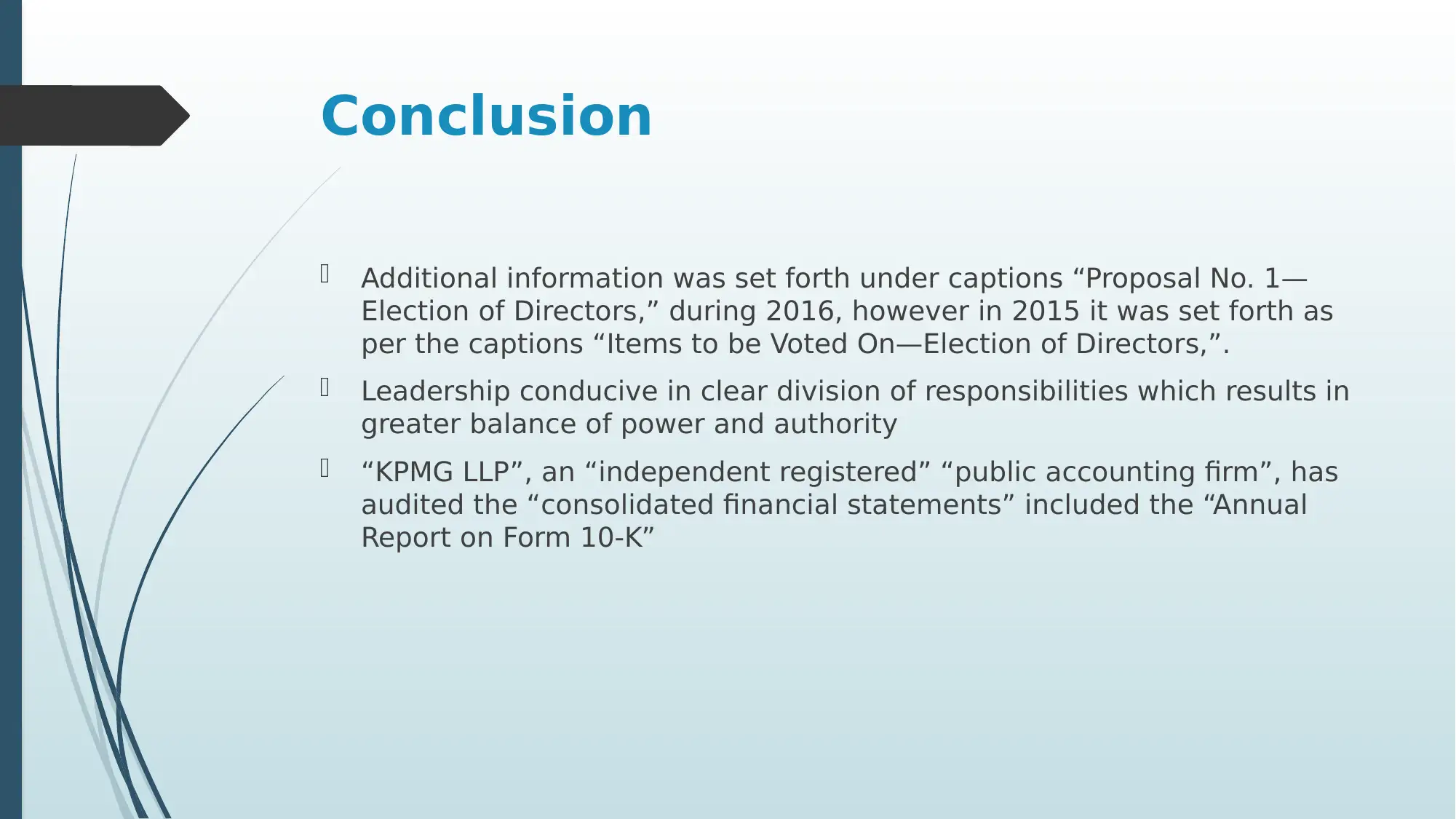

The assignment involves a detailed examination of the corporate governance framework and practices at ABM Industries. It focuses on the separation of the Chief Executive Officer (CEO) and Chairman roles, and explores the implications of this structure on corporate governance. The analysis draws from relevant literature and empirical research to provide insights into the effectiveness of this governance model in promoting accountability and ensuring shareholder interests.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.