Audit Report: Evolution Mining Limited - Financial Statement Analysis

VerifiedAdded on 2023/06/07

|9

|2648

|211

Report

AI Summary

This report presents an audit of Evolution Mining Limited (EVN), focusing on the analysis of its financial statements and ethical compliance. The report's objectives include equipping the audit team with relevant facts and circumstances, emphasizing the importance of materiality, understanding pr...

AUDITING AND ETHICS – EVOLUTION MINING LIMITED -

EVN

Student Name:

Student ID:

EVN

Student Name:

Student ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

An activity of an Audit is very necessary in the current scenario for the companies operating in

the different industries. As the title suggest, the report has been revolved on the audit of the

financial statements of the selected company and the compliance of the ethics thereon. Apart

from the importance of the audit, the report has been framed with four major objectives. First and

major object is to equip the audit team about the facts and the circumstances and the levels which

each of the member of the audit team shall consider while conducting the audit. Second object is

to lay down the importance of the concept of materiality in relation to the audit and compliance

activity. The third object is to understand the need of conducting the preliminary analytical

procedures of the company using the financial ratios of the company and the fourth and the last

object is to lay down the importance of the statements of the cash flows of the company and how

the same shall be considered while conducting the audit. With these objectives and the

considerations, the report is being prepared and presented for the members of the audit team.

The data has been collected from the primary as well as from the secondary sources.

Contents

EXECUTIVE SUMMARY.........................................................................................................................2

INTRODUCTION.......................................................................................................................................3

SECTION 1 – MATERIALITY..................................................................................................................3

SECTION 2 - PRELIMINARY ANALYTICAL REVIEW........................................................................5

SECTION 3 – ANALYSIS OF CASH INFLOWS AND GOING CONCERN...........................................6

CONCLUSION AND RECOMMENDATION...........................................................................................6

REFERENCES............................................................................................................................................7

APPENDICES.............................................................................................................................................8

An activity of an Audit is very necessary in the current scenario for the companies operating in

the different industries. As the title suggest, the report has been revolved on the audit of the

financial statements of the selected company and the compliance of the ethics thereon. Apart

from the importance of the audit, the report has been framed with four major objectives. First and

major object is to equip the audit team about the facts and the circumstances and the levels which

each of the member of the audit team shall consider while conducting the audit. Second object is

to lay down the importance of the concept of materiality in relation to the audit and compliance

activity. The third object is to understand the need of conducting the preliminary analytical

procedures of the company using the financial ratios of the company and the fourth and the last

object is to lay down the importance of the statements of the cash flows of the company and how

the same shall be considered while conducting the audit. With these objectives and the

considerations, the report is being prepared and presented for the members of the audit team.

The data has been collected from the primary as well as from the secondary sources.

Contents

EXECUTIVE SUMMARY.........................................................................................................................2

INTRODUCTION.......................................................................................................................................3

SECTION 1 – MATERIALITY..................................................................................................................3

SECTION 2 - PRELIMINARY ANALYTICAL REVIEW........................................................................5

SECTION 3 – ANALYSIS OF CASH INFLOWS AND GOING CONCERN...........................................6

CONCLUSION AND RECOMMENDATION...........................................................................................6

REFERENCES............................................................................................................................................7

APPENDICES.............................................................................................................................................8

INTRODUCTION

Every company shall get its books of accounts including the financial statements audited by the

competent personnel who shall be the qualified accountant. The need has arisen because of the

consecutive collapses of the companies in the financial as well as the management matters. For

instance – Collapse of the Lehman Brothers, One Tel and others. In this report, the auditing has

been explained with respect to the analysis if the financial statements of the company. For the

purpose of this report the company – Evolution Mining Limited has been selected. The company

is in the sector of the mining and is regarded as the one of the largest company in the industry of

gold miner in Australia and is listed in Australian Stock Exchange. The report has contained the

three major sections. For each of the sections, the annual report of the company for the year 2017

has been considered and for the second section annual reports for the earlier years have also been

considered. In the first section, the concept of the materiality has been discussed in detail with

regard to its meaning and how the different levels of materiality help in the better and efficient

conduct of the audit. It has also highlighted estimate made for the materiality of the company. In

the second section, the preliminary analytical review has been done which has helped the audit

team members to ascertain the areas which require their attention like changes in the major

accounting ratios, risk areas which can affect the opinion of the auditors of the company and so

on. In the third and the last section, the cash flows of the company has been analysed with regard

to the items which have led to the more cash inflows as well as the more cash outflows and along

with the cash flow analysis, the analysis have been done of the going concern risk that the

company has in the future years. The report has then ended up with the appropriate conclusion

and recommendation.

SECTION 1 – MATERIALITY

Anything which has the impact on affecting the decision of the users of results is defined as the

materiality. In terms of the auditing and accounting, the item which can affect the decision of the

users of the financial statements is defined as the materiality (Canning, 2018). The concept of the

materiality has been originated from the world of the accounting rather than the auditing. It’s a

concept of the financial reporting and states that the auditor shall consider the materiality of the

items present in the financial statements of the company while planning as to how the audit shall

be conducted as well as while performing the audit. It is because of the fact that the materiality

Every company shall get its books of accounts including the financial statements audited by the

competent personnel who shall be the qualified accountant. The need has arisen because of the

consecutive collapses of the companies in the financial as well as the management matters. For

instance – Collapse of the Lehman Brothers, One Tel and others. In this report, the auditing has

been explained with respect to the analysis if the financial statements of the company. For the

purpose of this report the company – Evolution Mining Limited has been selected. The company

is in the sector of the mining and is regarded as the one of the largest company in the industry of

gold miner in Australia and is listed in Australian Stock Exchange. The report has contained the

three major sections. For each of the sections, the annual report of the company for the year 2017

has been considered and for the second section annual reports for the earlier years have also been

considered. In the first section, the concept of the materiality has been discussed in detail with

regard to its meaning and how the different levels of materiality help in the better and efficient

conduct of the audit. It has also highlighted estimate made for the materiality of the company. In

the second section, the preliminary analytical review has been done which has helped the audit

team members to ascertain the areas which require their attention like changes in the major

accounting ratios, risk areas which can affect the opinion of the auditors of the company and so

on. In the third and the last section, the cash flows of the company has been analysed with regard

to the items which have led to the more cash inflows as well as the more cash outflows and along

with the cash flow analysis, the analysis have been done of the going concern risk that the

company has in the future years. The report has then ended up with the appropriate conclusion

and recommendation.

SECTION 1 – MATERIALITY

Anything which has the impact on affecting the decision of the users of results is defined as the

materiality. In terms of the auditing and accounting, the item which can affect the decision of the

users of the financial statements is defined as the materiality (Canning, 2018). The concept of the

materiality has been originated from the world of the accounting rather than the auditing. It’s a

concept of the financial reporting and states that the auditor shall consider the materiality of the

items present in the financial statements of the company while planning as to how the audit shall

be conducted as well as while performing the audit. It is because of the fact that the materiality

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

concept in auditing helps the auditor in ascertaining and forming reasonable and justified opinion

as to whether the financial statements of the company are free from any error which have been

materially misstated and which in turn will affect the decision of the user of the financial

statements of the company (Ullah, 2014). The concept states that if the item present in the

financial statement has the material effect then the same shall be disclosed in the financial

statements under the separate head.

The auditors usually before the start of the audit set the levels which are considered as the levels

of materiality in respect of each of the item. The levels of the materiality are made as per the

following criteria:

- Select the benchmark as relevant in the financing industry

- Determination of the level of the benchmark as stated above and Determination of the

level of the benchmark as stated above and

- The level so determined shall be justified enough to enable the audit team to consider it

as the important area for framing opinion (Lai, 2017).

As per the independent auditor report of the company for the year ending 2017 of the company,

as embedded in the annual report of the company, for the purpose of the audit, the level of the

materiality for the overall group has been kept at $18 million which is approximately equals to

the two and a half percent (2.5%) of the amount of the profit before interest, tax, depreciation

and the amount of the amortization of the overall group. The rationale behind choosing the

profit before tax is the key role that it plays in the financial statement and it is the benchmark

against which the performance of the group is generally measured. The 2.5% has been kept as

the materiality level because it is the level of the range which is accepted at the industry level.

As per the annual report of the company, following are the two important matters which are

importance for the audit:

1. Recognition of Deferred Tax Assets – The company has recognized the amount of $

57.744 million as the deferred tax assets and it has been regarded as the material for audit

because of the assessment of the future taxable profits that the company has made in

order to recognize the assets as Australian accounting standard has stated that the

as to whether the financial statements of the company are free from any error which have been

materially misstated and which in turn will affect the decision of the user of the financial

statements of the company (Ullah, 2014). The concept states that if the item present in the

financial statement has the material effect then the same shall be disclosed in the financial

statements under the separate head.

The auditors usually before the start of the audit set the levels which are considered as the levels

of materiality in respect of each of the item. The levels of the materiality are made as per the

following criteria:

- Select the benchmark as relevant in the financing industry

- Determination of the level of the benchmark as stated above and Determination of the

level of the benchmark as stated above and

- The level so determined shall be justified enough to enable the audit team to consider it

as the important area for framing opinion (Lai, 2017).

As per the independent auditor report of the company for the year ending 2017 of the company,

as embedded in the annual report of the company, for the purpose of the audit, the level of the

materiality for the overall group has been kept at $18 million which is approximately equals to

the two and a half percent (2.5%) of the amount of the profit before interest, tax, depreciation

and the amount of the amortization of the overall group. The rationale behind choosing the

profit before tax is the key role that it plays in the financial statement and it is the benchmark

against which the performance of the group is generally measured. The 2.5% has been kept as

the materiality level because it is the level of the range which is accepted at the industry level.

As per the annual report of the company, following are the two important matters which are

importance for the audit:

1. Recognition of Deferred Tax Assets – The company has recognized the amount of $

57.744 million as the deferred tax assets and it has been regarded as the material for audit

because of the assessment of the future taxable profits that the company has made in

order to recognize the assets as Australian accounting standard has stated that the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

deferred tax assets shall be recognized when there is the probable certainty that the future

taxable profits will be there so as to utilize the deferred tax asset.

2. Reversal of Impairment of the Mt Carlton’s NCA – The non - current assets of the Mt

Carlton’s have been revalued by reversing the amount of the impairment charged earlier

because of the non presence of the factors relating to the decrease in the value of the

assets. This has been done due to the increase in the gold prices and the stability in the

market which otherwise have been impaired by the amount of $148.6 million in the year

of 2013. The audit procedures for this matter is to compare the gold prices of today with

the year in which the impairment has been recognized and to compare the forecasts of the

gold prices as of today with the year in which it has been impaired and to analyze the

market trends.

SECTION 2 - PRELIMINARY ANALYTICAL REVIEW

Preliminary analytical review is the act of conducting the analysis from the earlier data available

and the current year draft so as to plan the audit accordingly. It is the first step in the planning for

an audit. Under this step the balance sheet and the statement of income is analysed very closely

with the help of the different accounting ratios (ACCA, 2016). For the purpose of making the

review the financial statements for the four past consecutive years have been considered and the

accounting ratios have been calculated as given in Appendix 1. The analysis of the ratios, the risk

thereon and the audit procedure that should be adopted has been detailed below:

1. From the period of 2014 to 2017, the net profit margin has been fluctuating at the end of

each year with the fluctuating figures of the revenue which states that the company’s sales

are not at par with their requirements (Appelbaum, 2018). The net profit ratio in the year of

2014 was 7.88 and in the year of 2017 it was 14.70. In this way the company has grown but

if the mid two years are also considered then it will be inferred that the company has the

fluctuating income pattern which exhibits that the company will not be able to run in future

(PCAOB, 2017). It means that the company though has been able to generate the higher

amount of the profits but at the same time have left the space to judge what circumstances

taxable profits will be there so as to utilize the deferred tax asset.

2. Reversal of Impairment of the Mt Carlton’s NCA – The non - current assets of the Mt

Carlton’s have been revalued by reversing the amount of the impairment charged earlier

because of the non presence of the factors relating to the decrease in the value of the

assets. This has been done due to the increase in the gold prices and the stability in the

market which otherwise have been impaired by the amount of $148.6 million in the year

of 2013. The audit procedures for this matter is to compare the gold prices of today with

the year in which the impairment has been recognized and to compare the forecasts of the

gold prices as of today with the year in which it has been impaired and to analyze the

market trends.

SECTION 2 - PRELIMINARY ANALYTICAL REVIEW

Preliminary analytical review is the act of conducting the analysis from the earlier data available

and the current year draft so as to plan the audit accordingly. It is the first step in the planning for

an audit. Under this step the balance sheet and the statement of income is analysed very closely

with the help of the different accounting ratios (ACCA, 2016). For the purpose of making the

review the financial statements for the four past consecutive years have been considered and the

accounting ratios have been calculated as given in Appendix 1. The analysis of the ratios, the risk

thereon and the audit procedure that should be adopted has been detailed below:

1. From the period of 2014 to 2017, the net profit margin has been fluctuating at the end of

each year with the fluctuating figures of the revenue which states that the company’s sales

are not at par with their requirements (Appelbaum, 2018). The net profit ratio in the year of

2014 was 7.88 and in the year of 2017 it was 14.70. In this way the company has grown but

if the mid two years are also considered then it will be inferred that the company has the

fluctuating income pattern which exhibits that the company will not be able to run in future

(PCAOB, 2017). It means that the company though has been able to generate the higher

amount of the profits but at the same time have left the space to judge what circumstances

have led the company to generate the profit within one year from the loss of 2.22 % of sales

from 2016 to 14.70 % of sales on 2017.

2. In the same pattern of the net profit margin, the return on the net assets has been flowed in

the analysis. The analysis has to be done in accordance with the procedures for the audit of

the revenue (Jans, 2014).

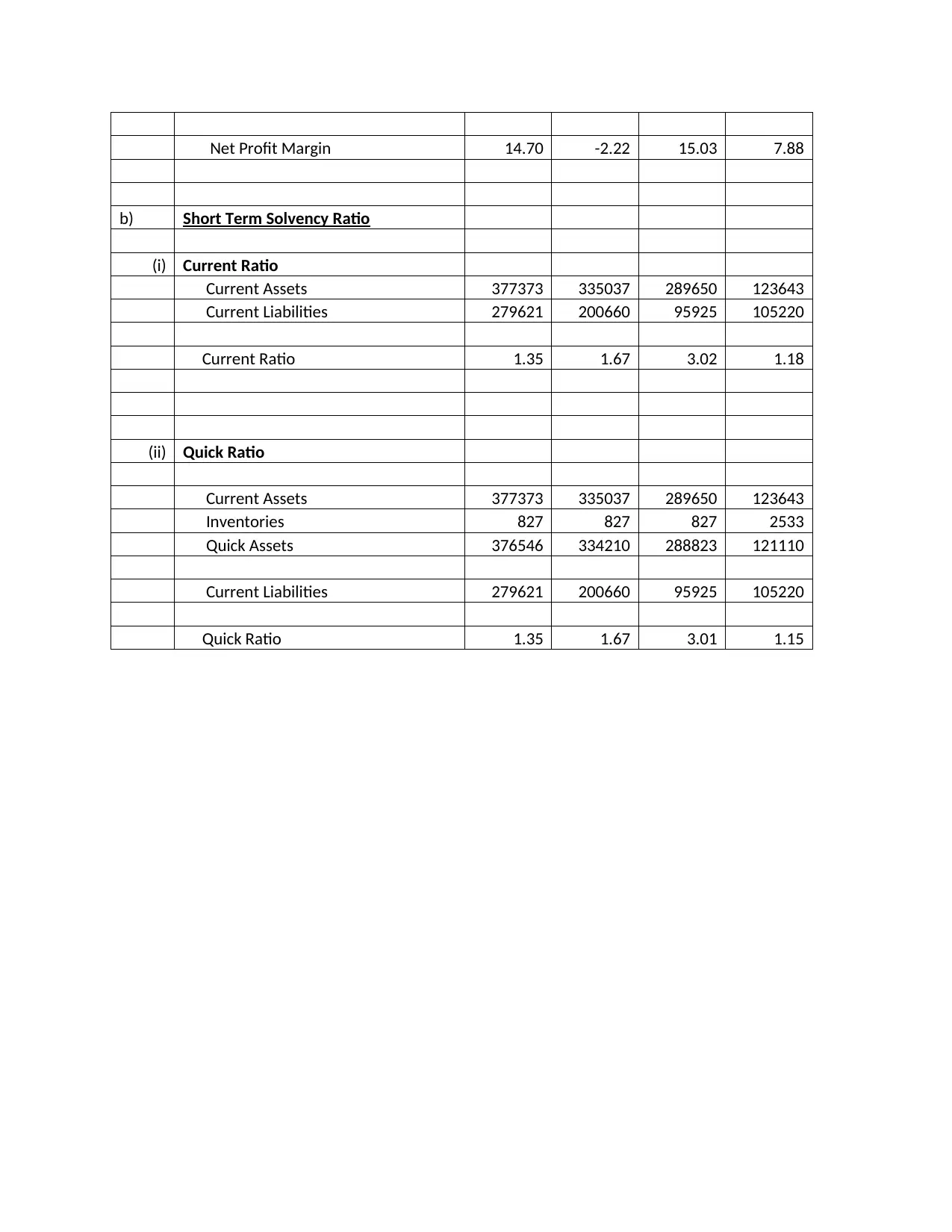

3. From the balance sheet ratio – current ratio and quick asset ratio, it is very clear that the ratio

has been declined from 1.67 in the year of 2016 to 1.35 in the year of 2017 which states that

the company has favorable balance sheet ratios in the year of loss and unfavorable in the

year of profit (Company official Website, 2017).

The major assertion that has been inferred from the above analysis is that the company’s internal

control system is very weak and requires the urgent attention of the management to find out the

areas of risk. One of the major risk areas is the accounting and reporting fraud which can lead to

the higher revenue and profits in one year with lesser current ratio. There might be the chances

that the directors of the company will have the incentive if the sale target is achieved. The audit

procedure involved in this regard is the checking and verifying the each of the sales figure and

assessing the effectiveness and the efficiency of internal control system.

SECTION 3 – ANALYSIS OF CASH INFLOWS AND GOING CONCERN

The majority of the cash inflows have come through the operating activities amounting to

650795 million dollars and that too majorly due to the receipts from sales. Cash flows from

investing activities have higher cash outflows. Primary cash receipts is from the sales amounting

to 1441275 million dollars and primary cash payment is the payment made for economic interest

in Ernest Henry amounting to 884004 million dollars (Anastasia, 2015). There are NIL non cash

financial and investing activities. In accordance with the analysis of the cash inflows, the

company is not at risk in terms of the going concern as there is increase in the cash and cash

equivalents.

CONCLUSION AND RECOMMENDATION

Auditing has the very important role in the financing area which every company shall consider it

as a part of the core objective of the finance function. If this is not present in the core objective,

from 2016 to 14.70 % of sales on 2017.

2. In the same pattern of the net profit margin, the return on the net assets has been flowed in

the analysis. The analysis has to be done in accordance with the procedures for the audit of

the revenue (Jans, 2014).

3. From the balance sheet ratio – current ratio and quick asset ratio, it is very clear that the ratio

has been declined from 1.67 in the year of 2016 to 1.35 in the year of 2017 which states that

the company has favorable balance sheet ratios in the year of loss and unfavorable in the

year of profit (Company official Website, 2017).

The major assertion that has been inferred from the above analysis is that the company’s internal

control system is very weak and requires the urgent attention of the management to find out the

areas of risk. One of the major risk areas is the accounting and reporting fraud which can lead to

the higher revenue and profits in one year with lesser current ratio. There might be the chances

that the directors of the company will have the incentive if the sale target is achieved. The audit

procedure involved in this regard is the checking and verifying the each of the sales figure and

assessing the effectiveness and the efficiency of internal control system.

SECTION 3 – ANALYSIS OF CASH INFLOWS AND GOING CONCERN

The majority of the cash inflows have come through the operating activities amounting to

650795 million dollars and that too majorly due to the receipts from sales. Cash flows from

investing activities have higher cash outflows. Primary cash receipts is from the sales amounting

to 1441275 million dollars and primary cash payment is the payment made for economic interest

in Ernest Henry amounting to 884004 million dollars (Anastasia, 2015). There are NIL non cash

financial and investing activities. In accordance with the analysis of the cash inflows, the

company is not at risk in terms of the going concern as there is increase in the cash and cash

equivalents.

CONCLUSION AND RECOMMENDATION

Auditing has the very important role in the financing area which every company shall consider it

as a part of the core objective of the finance function. If this is not present in the core objective,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

then the overall working of the organization ends up with the improper management and thus

leading to collapses. Through this report the importance of the auditing function has been

detailed in the three different sections. First one has described the levels of the materiality,

second one has described the importance and methods of the conducting the analytical reviews

before start of the audit and the last one has detailed the ways as to how the analysis of the cash

flows shall be made. In the last the analysis of the going concern has also been made keeping in

consideration the analysis of all the financial matters as reported in the annual report of the

company. Thus, in order to conclude the report, it has been very detailed and exhaustive and is

useful to the members of the audit team.

Its recommended to have the sound internal control system embedded with the internal audit

department which can conduct the audit on timely basis and rectify the discrepancies on regular

basis.

REFERENCES

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-

exams -study-resources/p7/technical-articles/analytical-procedures.html accessed on 02-09

-2018.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed

on 02 -09-2018

Appelbaum, D. A. (2018), “Analytical procedures in external auditing: A comprehensive

literature survey and framework for external audit analytics.” Journal of

Accounting Literature, 40, 83-101.

Canning, M., (2018), “Processes of audit ability in sustainability assurance–the case of

materiality construction”. Accounting and Business Research, 1-27.

Company official Website, (2017), “Annual report, 2017” available at

https://evolutionmining.com.au/ accessed on 02-09-2018

leading to collapses. Through this report the importance of the auditing function has been

detailed in the three different sections. First one has described the levels of the materiality,

second one has described the importance and methods of the conducting the analytical reviews

before start of the audit and the last one has detailed the ways as to how the analysis of the cash

flows shall be made. In the last the analysis of the going concern has also been made keeping in

consideration the analysis of all the financial matters as reported in the annual report of the

company. Thus, in order to conclude the report, it has been very detailed and exhaustive and is

useful to the members of the audit team.

Its recommended to have the sound internal control system embedded with the internal audit

department which can conduct the audit on timely basis and rectify the discrepancies on regular

basis.

REFERENCES

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-

exams -study-resources/p7/technical-articles/analytical-procedures.html accessed on 02-09

-2018.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed

on 02 -09-2018

Appelbaum, D. A. (2018), “Analytical procedures in external auditing: A comprehensive

literature survey and framework for external audit analytics.” Journal of

Accounting Literature, 40, 83-101.

Canning, M., (2018), “Processes of audit ability in sustainability assurance–the case of

materiality construction”. Accounting and Business Research, 1-27.

Company official Website, (2017), “Annual report, 2017” available at

https://evolutionmining.com.au/ accessed on 02-09-2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jans, M., (2014), “A field study on the use of process mining of event logs as an analytical

procedure in auditing”, The Accounting Review, 89(5), 1751-1773.

Lai, A., (2017), “What does materiality mean to integrated reporting preparers? An empirical

exploration” Meditari Accountancy Research, 25(4), 533-552.

PCAOB, (2017), “Analytical Procedures” available at

https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx accessed on 02-09-

2018

Ullah A, (2014), “Planning and Audit of Financial Statements” available on

http://leaccountant.com/2014/12/08/asa-300-summary-planning-an-audit-of-

financial -statements/ accessed on 02-09-2018

APPENDICES

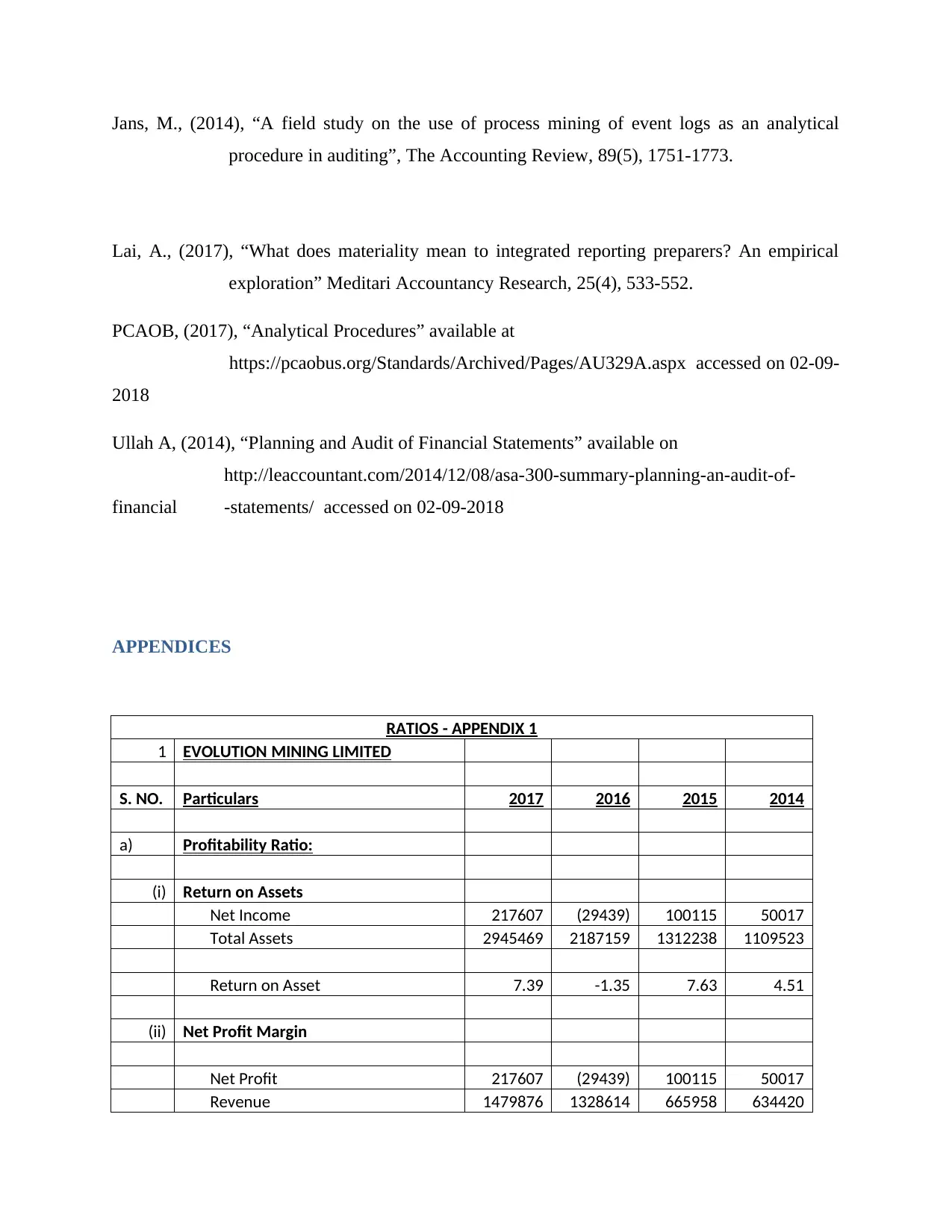

RATIOS - APPENDIX 1

1 EVOLUTION MINING LIMITED

S. NO. Particulars 2017 2016 2015 2014

a) Profitability Ratio:

(i) Return on Assets

Net Income 217607 (29439) 100115 50017

Total Assets 2945469 2187159 1312238 1109523

Return on Asset 7.39 -1.35 7.63 4.51

(ii) Net Profit Margin

Net Profit 217607 (29439) 100115 50017

Revenue 1479876 1328614 665958 634420

procedure in auditing”, The Accounting Review, 89(5), 1751-1773.

Lai, A., (2017), “What does materiality mean to integrated reporting preparers? An empirical

exploration” Meditari Accountancy Research, 25(4), 533-552.

PCAOB, (2017), “Analytical Procedures” available at

https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx accessed on 02-09-

2018

Ullah A, (2014), “Planning and Audit of Financial Statements” available on

http://leaccountant.com/2014/12/08/asa-300-summary-planning-an-audit-of-

financial -statements/ accessed on 02-09-2018

APPENDICES

RATIOS - APPENDIX 1

1 EVOLUTION MINING LIMITED

S. NO. Particulars 2017 2016 2015 2014

a) Profitability Ratio:

(i) Return on Assets

Net Income 217607 (29439) 100115 50017

Total Assets 2945469 2187159 1312238 1109523

Return on Asset 7.39 -1.35 7.63 4.51

(ii) Net Profit Margin

Net Profit 217607 (29439) 100115 50017

Revenue 1479876 1328614 665958 634420

Net Profit Margin 14.70 -2.22 15.03 7.88

b) Short Term Solvency Ratio

(i) Current Ratio

Current Assets 377373 335037 289650 123643

Current Liabilities 279621 200660 95925 105220

Current Ratio 1.35 1.67 3.02 1.18

(ii) Quick Ratio

Current Assets 377373 335037 289650 123643

Inventories 827 827 827 2533

Quick Assets 376546 334210 288823 121110

Current Liabilities 279621 200660 95925 105220

Quick Ratio 1.35 1.67 3.01 1.15

b) Short Term Solvency Ratio

(i) Current Ratio

Current Assets 377373 335037 289650 123643

Current Liabilities 279621 200660 95925 105220

Current Ratio 1.35 1.67 3.02 1.18

(ii) Quick Ratio

Current Assets 377373 335037 289650 123643

Inventories 827 827 827 2533

Quick Assets 376546 334210 288823 121110

Current Liabilities 279621 200660 95925 105220

Quick Ratio 1.35 1.67 3.01 1.15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.