Comprehensive Analysis of Money and Banking in Sri Lanka

VerifiedAdded on 2020/10/22

|16

|2455

|263

Report

AI Summary

This report provides a comprehensive analysis of money and banking in Sri Lanka, examining key economic indicators and the performance of the banking system. The study begins with an introduction to money and banking, followed by a detailed presentation of collected data, including broad money growth rates, inflation rates based on the GDP deflator, and real GDP growth for the period from 1998 to 2017. The report includes graphical representations and calculations of correlation coefficients and real interest rates for deposits and loans. Furthermore, the report explores the structure and performance of Sri Lanka's banking system, regulatory and supervisory measures, the presence of Islamic banking, and the evolution of monetary policy. The analysis extends to discussing the effectiveness of monetary policy in Sri Lanka and its relevance to global banking problems. The report concludes with a summary of key findings and references to relevant literature.

MONEY AND BANKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MONEY AND BANKING 1

INTRODUCTION 3

2. DATA COLLECTION AND DISPLAY 3

3. 3

a. Calculating broad money growth rate YC in percentage terms 3

b. Calculating percentage rate of inflation, π YC based on the CPIYC or the GDP deflator 4

c. Assessing percentage growth rate of real GDP for the sample period 5

d. Plotting the rate of inflation in respect of broad and the narrow money 7

e. Computation of correlation co-efficient 8

f. Plotting the real interest rate of deposit 8

g. Plotting the real interest rate of loan 9

4. 10

4a. Structure and the performance of the banking system. 10

4b. Regulatory and the supervisory measures in the banking system. 11

4c. Presence of the Islamic banking and the financial institution. 11

4d. Reasons and the changes that happened in the monetary policy. 11

4e. Discussion relating to the extent of the successful of the monetary policy. 12

5. Describing the view relating to the use of the monetary policy in solving the banking

problems worldwide. 12

CONCLUSION 12

REFERENCES 13

Books and journal 13

INTRODUCTION 3

2. DATA COLLECTION AND DISPLAY 3

3. 3

a. Calculating broad money growth rate YC in percentage terms 3

b. Calculating percentage rate of inflation, π YC based on the CPIYC or the GDP deflator 4

c. Assessing percentage growth rate of real GDP for the sample period 5

d. Plotting the rate of inflation in respect of broad and the narrow money 7

e. Computation of correlation co-efficient 8

f. Plotting the real interest rate of deposit 8

g. Plotting the real interest rate of loan 9

4. 10

4a. Structure and the performance of the banking system. 10

4b. Regulatory and the supervisory measures in the banking system. 11

4c. Presence of the Islamic banking and the financial institution. 11

4d. Reasons and the changes that happened in the monetary policy. 11

4e. Discussion relating to the extent of the successful of the monetary policy. 12

5. Describing the view relating to the use of the monetary policy in solving the banking

problems worldwide. 12

CONCLUSION 12

REFERENCES 13

Books and journal 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Money and banking is one of the central components in macro-economics. Economic

growth, inflation and the low rate of the unemployment are been assessed through the money and

banking in the overall economy. The present study is based on the evaluation of the money and

banking data of the Srilanka and the description regarding the banking system of Srilanka.

2. DATA COLLECTION AND DISPLAY

Mentioned in appendix.

3.

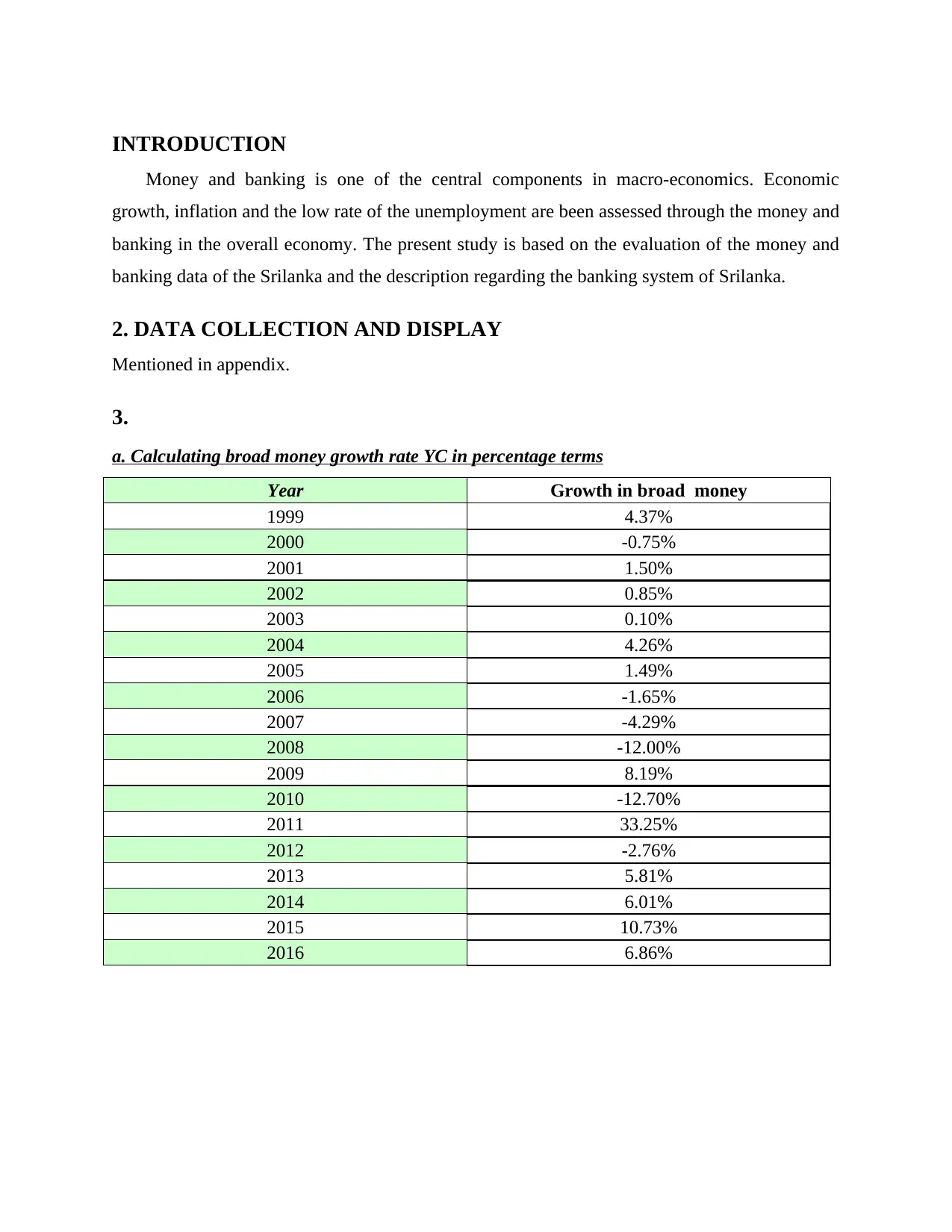

a. Calculating broad money growth rate YC in percentage terms

Year Growth in broad money

1999 4.37%

2000 -0.75%

2001 1.50%

2002 0.85%

2003 0.10%

2004 4.26%

2005 1.49%

2006 -1.65%

2007 -4.29%

2008 -12.00%

2009 8.19%

2010 -12.70%

2011 33.25%

2012 -2.76%

2013 5.81%

2014 6.01%

2015 10.73%

2016 6.86%

Money and banking is one of the central components in macro-economics. Economic

growth, inflation and the low rate of the unemployment are been assessed through the money and

banking in the overall economy. The present study is based on the evaluation of the money and

banking data of the Srilanka and the description regarding the banking system of Srilanka.

2. DATA COLLECTION AND DISPLAY

Mentioned in appendix.

3.

a. Calculating broad money growth rate YC in percentage terms

Year Growth in broad money

1999 4.37%

2000 -0.75%

2001 1.50%

2002 0.85%

2003 0.10%

2004 4.26%

2005 1.49%

2006 -1.65%

2007 -4.29%

2008 -12.00%

2009 8.19%

2010 -12.70%

2011 33.25%

2012 -2.76%

2013 5.81%

2014 6.01%

2015 10.73%

2016 6.86%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

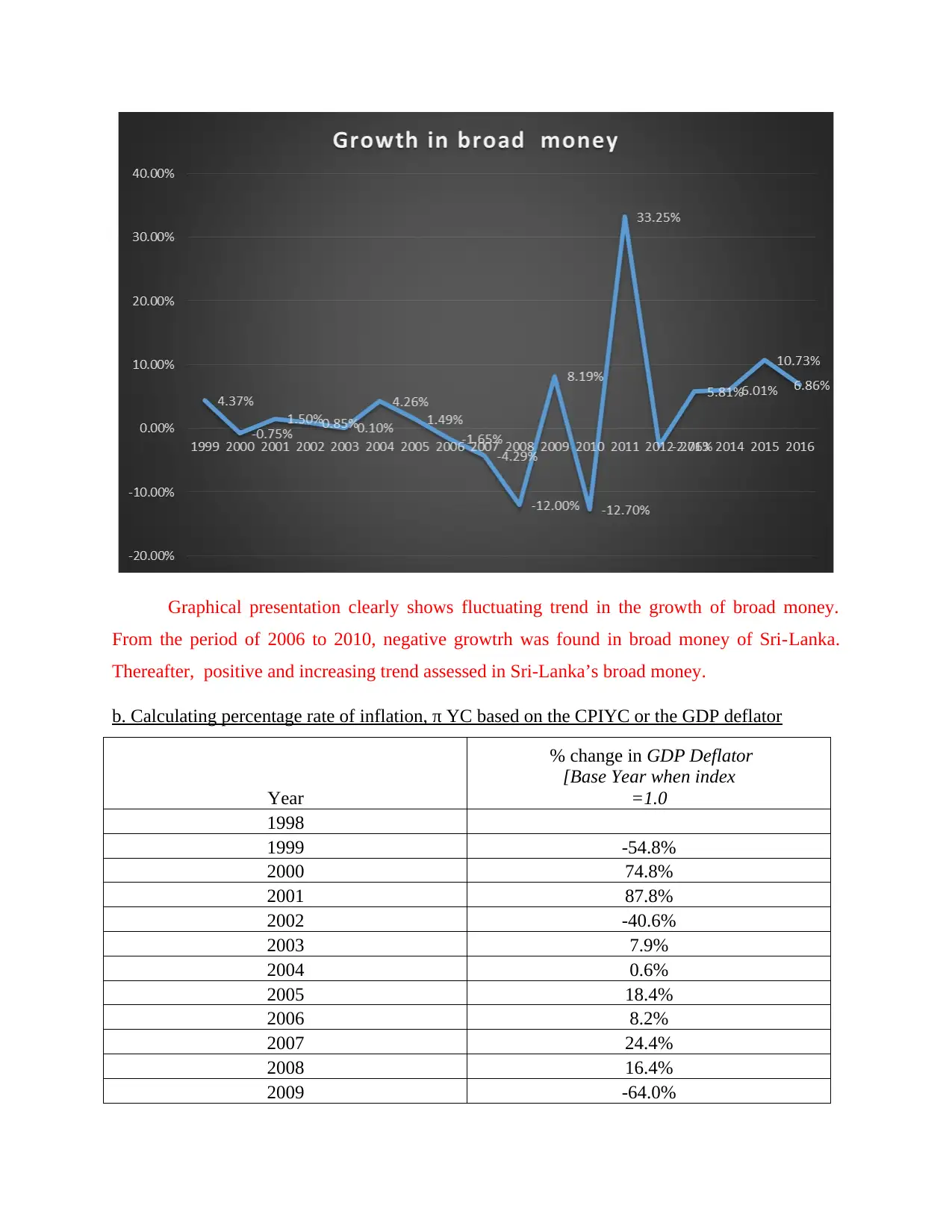

Graphical presentation clearly shows fluctuating trend in the growth of broad money.

From the period of 2006 to 2010, negative growtrh was found in broad money of Sri-Lanka.

Thereafter, positive and increasing trend assessed in Sri-Lanka’s broad money.

b. Calculating percentage rate of inflation, π YC based on the CPIYC or the GDP deflator

Year

% change in GDP Deflator

[Base Year when index

=1.0

1998

1999 -54.8%

2000 74.8%

2001 87.8%

2002 -40.6%

2003 7.9%

2004 0.6%

2005 18.4%

2006 8.2%

2007 24.4%

2008 16.4%

2009 -64.0%

From the period of 2006 to 2010, negative growtrh was found in broad money of Sri-Lanka.

Thereafter, positive and increasing trend assessed in Sri-Lanka’s broad money.

b. Calculating percentage rate of inflation, π YC based on the CPIYC or the GDP deflator

Year

% change in GDP Deflator

[Base Year when index

=1.0

1998

1999 -54.8%

2000 74.8%

2001 87.8%

2002 -40.6%

2003 7.9%

2004 0.6%

2005 18.4%

2006 8.2%

2007 24.4%

2008 16.4%

2009 -64.0%

2010 287.8%

2011 -83.2%

2012 182.6%

2013 -42.4%

2014 -53.3%

2015 -77.7%

2016 528.6%

2017 102.5%

From the above graph and table it can be interpreted that the rate of GDP is having a

fluctuating trend over the time period of last 20 years. The GDP rate is a mixture of both positive

and negative rates ranging from the year 1998 to the year 2017.

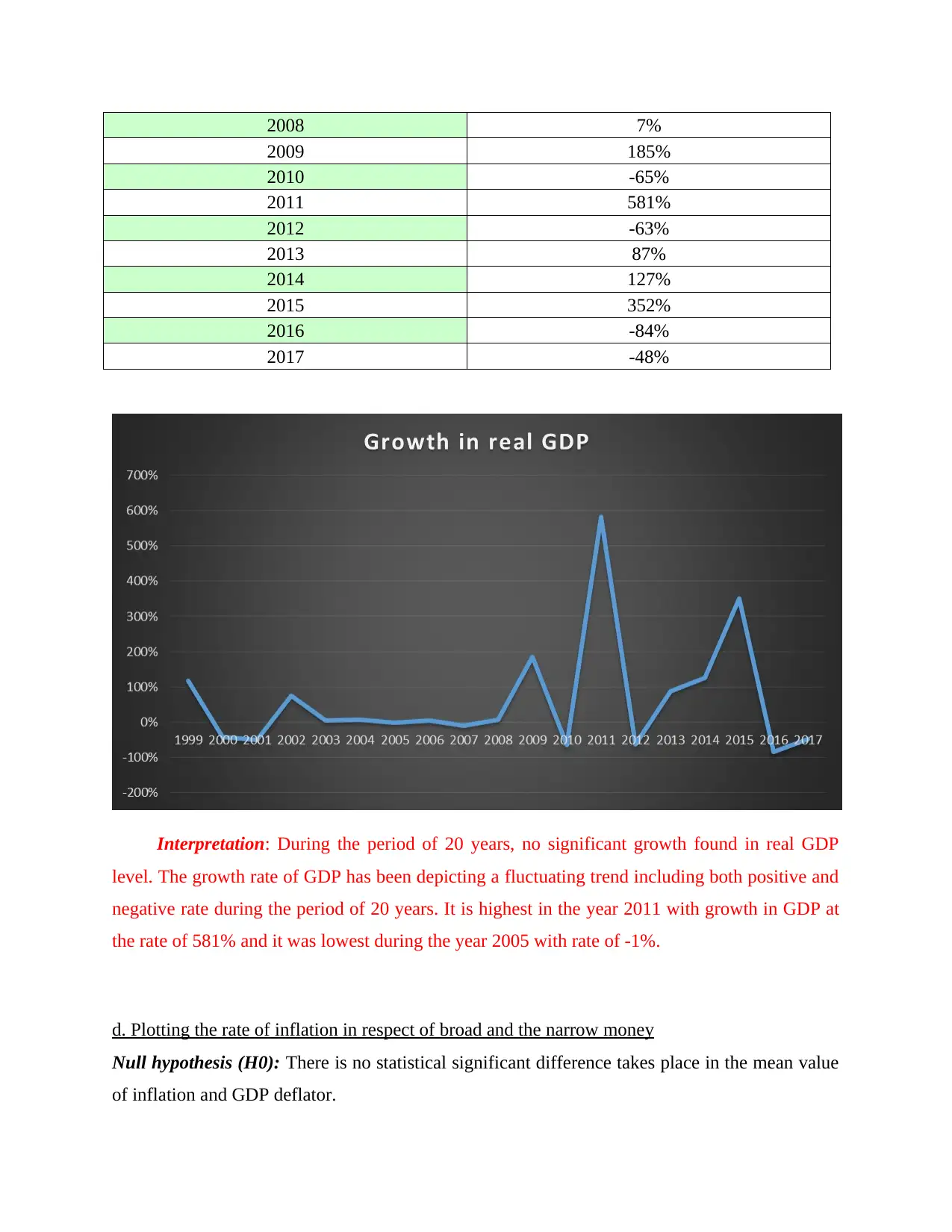

c. Assessing percentage growth rate of real GDP for the sample period

Year Growth in real GDP

1999 118%

2000 -41%

2001 -49%

2002 76%

2003 5%

2004 8%

2005 -1%

2006 6%

2007 -9%

2011 -83.2%

2012 182.6%

2013 -42.4%

2014 -53.3%

2015 -77.7%

2016 528.6%

2017 102.5%

From the above graph and table it can be interpreted that the rate of GDP is having a

fluctuating trend over the time period of last 20 years. The GDP rate is a mixture of both positive

and negative rates ranging from the year 1998 to the year 2017.

c. Assessing percentage growth rate of real GDP for the sample period

Year Growth in real GDP

1999 118%

2000 -41%

2001 -49%

2002 76%

2003 5%

2004 8%

2005 -1%

2006 6%

2007 -9%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2008 7%

2009 185%

2010 -65%

2011 581%

2012 -63%

2013 87%

2014 127%

2015 352%

2016 -84%

2017 -48%

Interpretation: During the period of 20 years, no significant growth found in real GDP

level. The growth rate of GDP has been depicting a fluctuating trend including both positive and

negative rate during the period of 20 years. It is highest in the year 2011 with growth in GDP at

the rate of 581% and it was lowest during the year 2005 with rate of -1%.

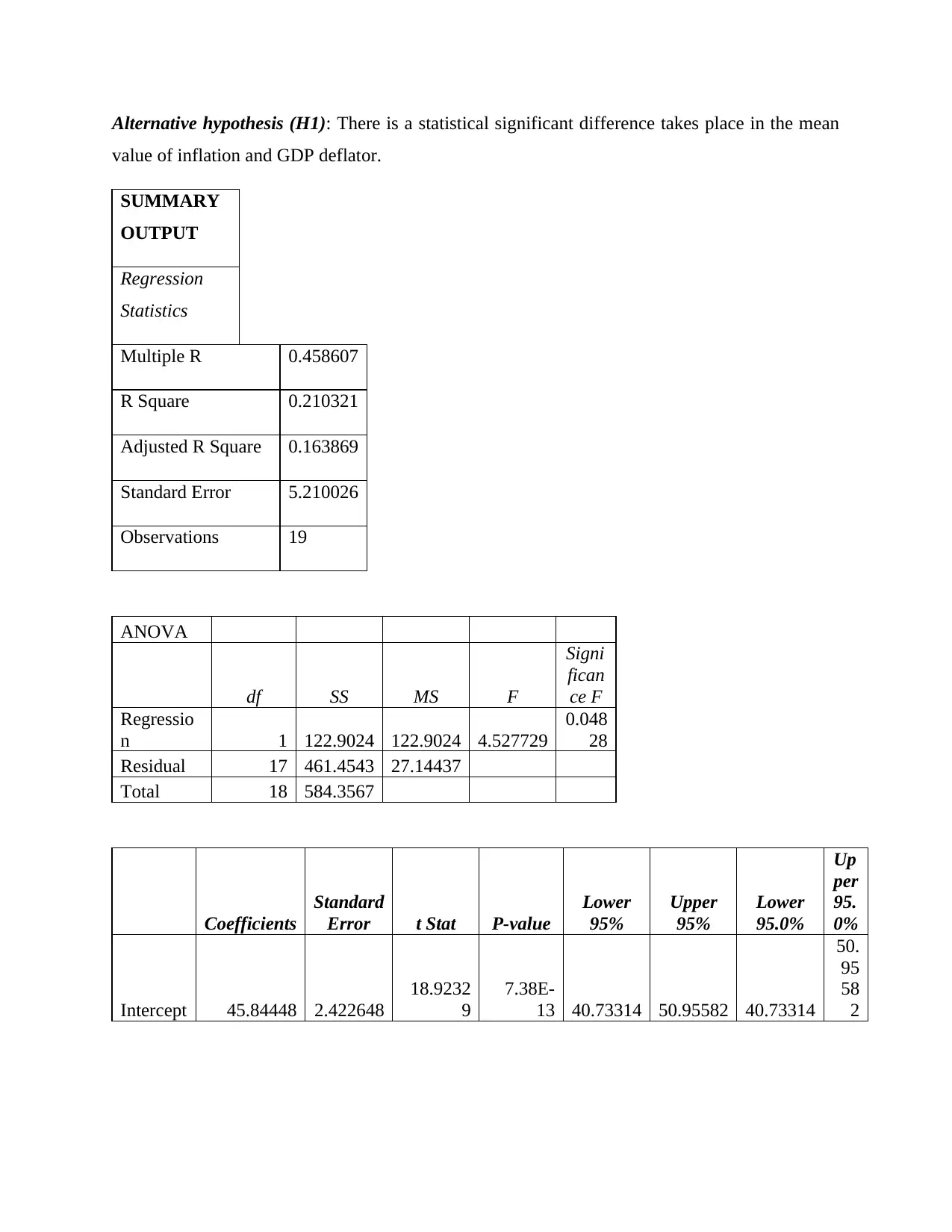

d. Plotting the rate of inflation in respect of broad and the narrow money

Null hypothesis (H0): There is no statistical significant difference takes place in the mean value

of inflation and GDP deflator.

2009 185%

2010 -65%

2011 581%

2012 -63%

2013 87%

2014 127%

2015 352%

2016 -84%

2017 -48%

Interpretation: During the period of 20 years, no significant growth found in real GDP

level. The growth rate of GDP has been depicting a fluctuating trend including both positive and

negative rate during the period of 20 years. It is highest in the year 2011 with growth in GDP at

the rate of 581% and it was lowest during the year 2005 with rate of -1%.

d. Plotting the rate of inflation in respect of broad and the narrow money

Null hypothesis (H0): There is no statistical significant difference takes place in the mean value

of inflation and GDP deflator.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alternative hypothesis (H1): There is a statistical significant difference takes place in the mean

value of inflation and GDP deflator.

SUMMARY

OUTPUT

Regression

Statistics

Multiple R 0.458607

R Square 0.210321

Adjusted R Square 0.163869

Standard Error 5.210026

Observations 19

ANOVA

df SS MS F

Signi

fican

ce F

Regressio

n 1 122.9024 122.9024 4.527729

0.048

28

Residual 17 461.4543 27.14437

Total 18 584.3567

Coefficients

Standard

Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Up

per

95.

0%

Intercept 45.84448 2.422648

18.9232

9

7.38E-

13 40.73314 50.95582 40.73314

50.

95

58

2

value of inflation and GDP deflator.

SUMMARY

OUTPUT

Regression

Statistics

Multiple R 0.458607

R Square 0.210321

Adjusted R Square 0.163869

Standard Error 5.210026

Observations 19

ANOVA

df SS MS F

Signi

fican

ce F

Regressio

n 1 122.9024 122.9024 4.527729

0.048

28

Residual 17 461.4543 27.14437

Total 18 584.3567

Coefficients

Standard

Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Up

per

95.

0%

Intercept 45.84448 2.422648

18.9232

9

7.38E-

13 40.73314 50.95582 40.73314

50.

95

58

2

CPI

[replace

this with

Base

Year

when

index

=1.0] -0.53362 0.250777 -2.12785 0.04828 -1.06271 -0.00452 -1.06271

-

0.0

04

52

e. Computation of correlation co-efficient

Particulars Broad money (growth) Real GDP (growth)

Broad money (growth) 1 .84

Real GDP (growth) .84 1

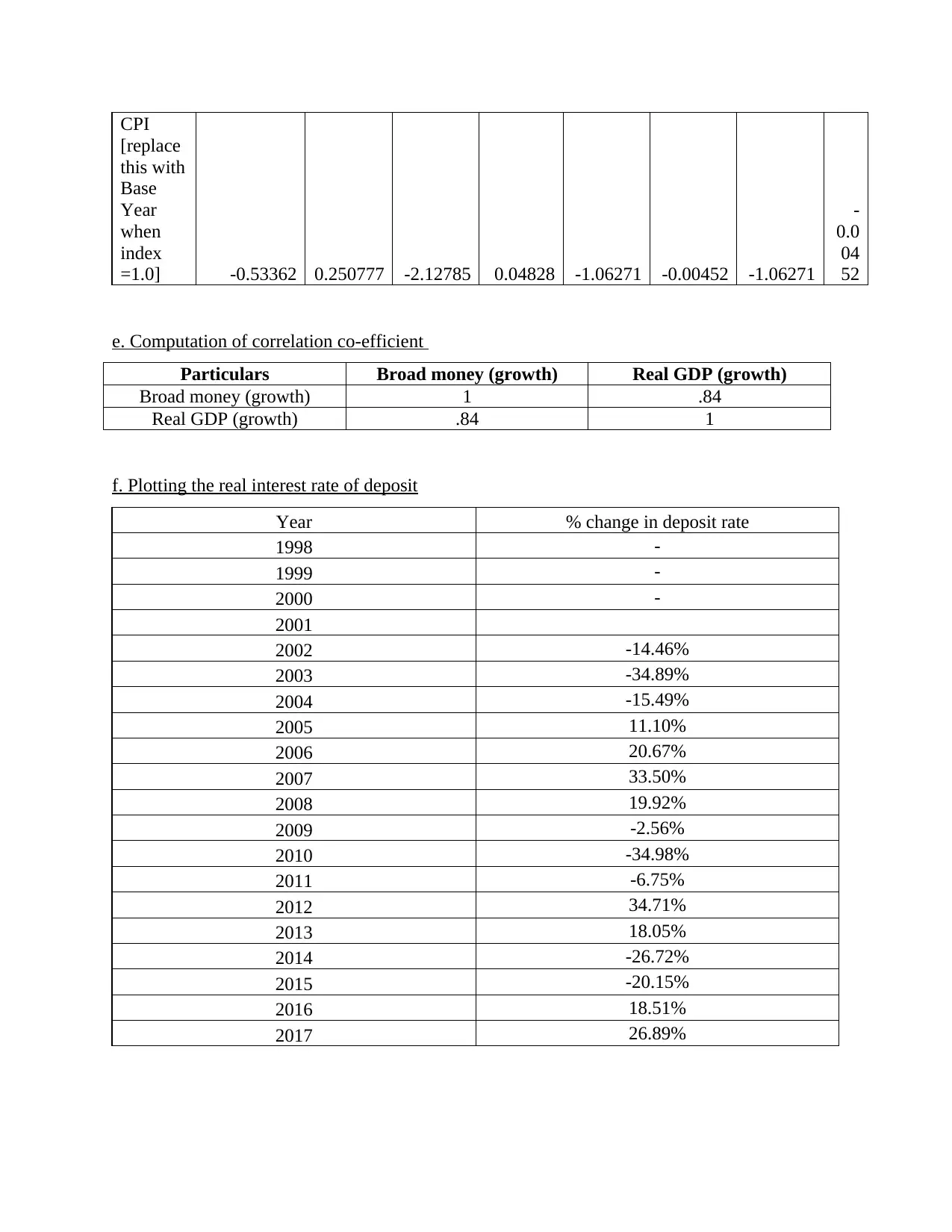

f. Plotting the real interest rate of deposit

Year % change in deposit rate

1998 -

1999 -

2000 -

2001

2002 -14.46%

2003 -34.89%

2004 -15.49%

2005 11.10%

2006 20.67%

2007 33.50%

2008 19.92%

2009 -2.56%

2010 -34.98%

2011 -6.75%

2012 34.71%

2013 18.05%

2014 -26.72%

2015 -20.15%

2016 18.51%

2017 26.89%

[replace

this with

Base

Year

when

index

=1.0] -0.53362 0.250777 -2.12785 0.04828 -1.06271 -0.00452 -1.06271

-

0.0

04

52

e. Computation of correlation co-efficient

Particulars Broad money (growth) Real GDP (growth)

Broad money (growth) 1 .84

Real GDP (growth) .84 1

f. Plotting the real interest rate of deposit

Year % change in deposit rate

1998 -

1999 -

2000 -

2001

2002 -14.46%

2003 -34.89%

2004 -15.49%

2005 11.10%

2006 20.67%

2007 33.50%

2008 19.92%

2009 -2.56%

2010 -34.98%

2011 -6.75%

2012 34.71%

2013 18.05%

2014 -26.72%

2015 -20.15%

2016 18.51%

2017 26.89%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

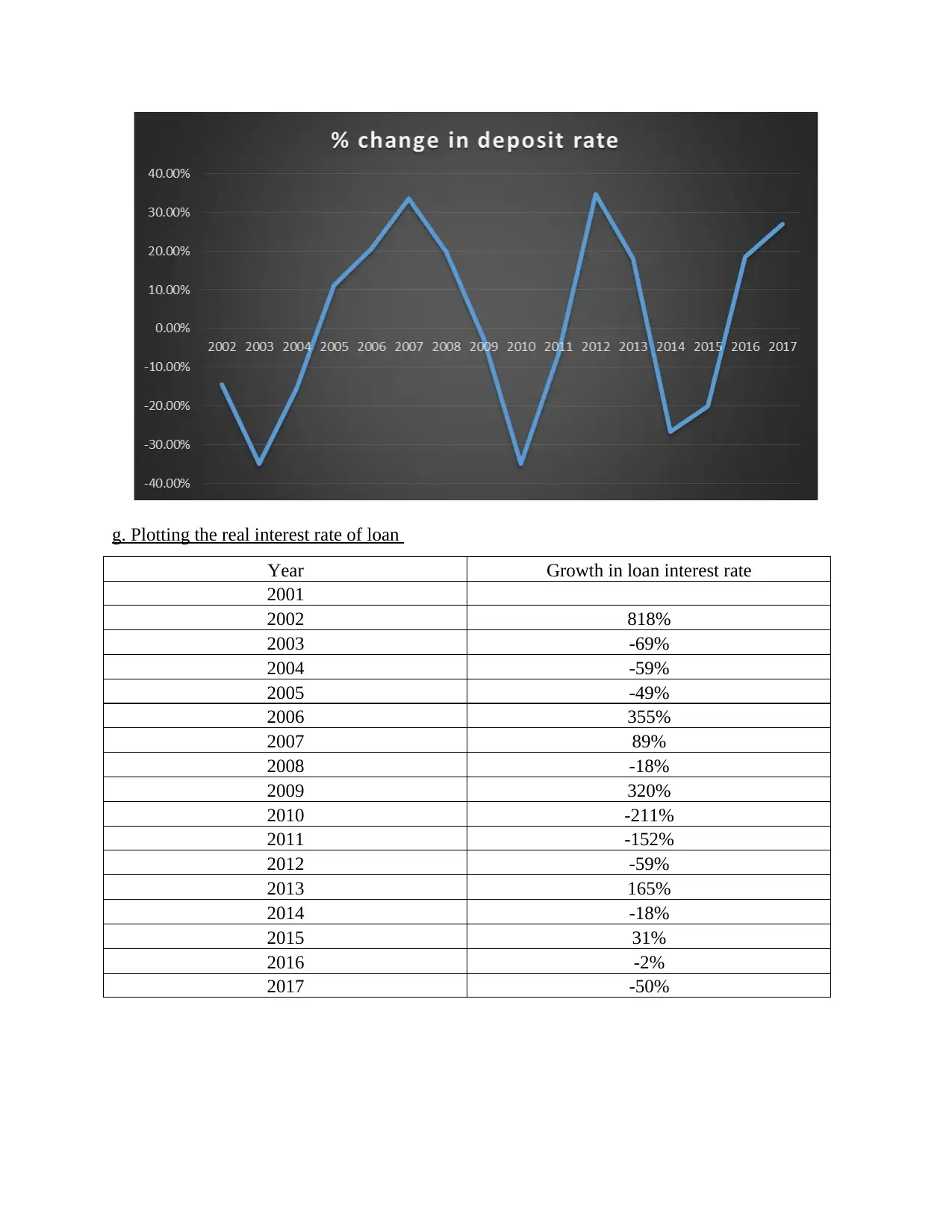

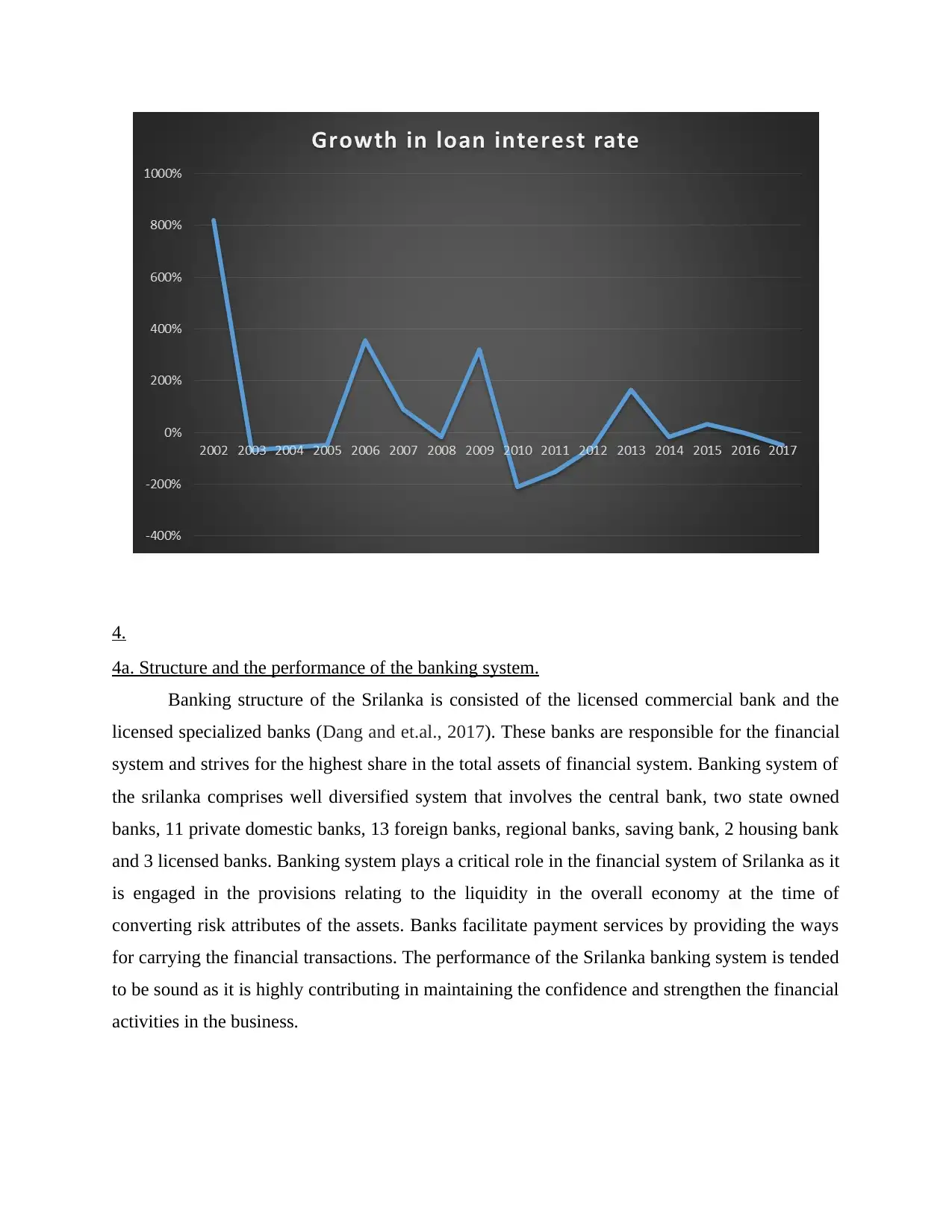

g. Plotting the real interest rate of loan

Year Growth in loan interest rate

2001

2002 818%

2003 -69%

2004 -59%

2005 -49%

2006 355%

2007 89%

2008 -18%

2009 320%

2010 -211%

2011 -152%

2012 -59%

2013 165%

2014 -18%

2015 31%

2016 -2%

2017 -50%

Year Growth in loan interest rate

2001

2002 818%

2003 -69%

2004 -59%

2005 -49%

2006 355%

2007 89%

2008 -18%

2009 320%

2010 -211%

2011 -152%

2012 -59%

2013 165%

2014 -18%

2015 31%

2016 -2%

2017 -50%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.

4a. Structure and the performance of the banking system.

Banking structure of the Srilanka is consisted of the licensed commercial bank and the

licensed specialized banks (Dang and et.al., 2017). These banks are responsible for the financial

system and strives for the highest share in the total assets of financial system. Banking system of

the srilanka comprises well diversified system that involves the central bank, two state owned

banks, 11 private domestic banks, 13 foreign banks, regional banks, saving bank, 2 housing bank

and 3 licensed banks. Banking system plays a critical role in the financial system of Srilanka as it

is engaged in the provisions relating to the liquidity in the overall economy at the time of

converting risk attributes of the assets. Banks facilitate payment services by providing the ways

for carrying the financial transactions. The performance of the Srilanka banking system is tended

to be sound as it is highly contributing in maintaining the confidence and strengthen the financial

activities in the business.

4a. Structure and the performance of the banking system.

Banking structure of the Srilanka is consisted of the licensed commercial bank and the

licensed specialized banks (Dang and et.al., 2017). These banks are responsible for the financial

system and strives for the highest share in the total assets of financial system. Banking system of

the srilanka comprises well diversified system that involves the central bank, two state owned

banks, 11 private domestic banks, 13 foreign banks, regional banks, saving bank, 2 housing bank

and 3 licensed banks. Banking system plays a critical role in the financial system of Srilanka as it

is engaged in the provisions relating to the liquidity in the overall economy at the time of

converting risk attributes of the assets. Banks facilitate payment services by providing the ways

for carrying the financial transactions. The performance of the Srilanka banking system is tended

to be sound as it is highly contributing in maintaining the confidence and strengthen the financial

activities in the business.

4b. Regulatory and the supervisory measures in the banking system.

The regulation and supervision of the banking system in Srilanka is in the hands of the

central bank (Cohen, 2018). Legal framework comprises Monetary law and banking act. Central

bank in Srilanka is has the powers for issuing the detailed directives to commercial bank. During

the 1993, Basel Accord has been adopted for the commercial banks. In accordance with the

Central bank, the capital ratios are been maintained at the comfortable level in the year 2017. At

the time of the global financial crisis banking sector of Srilanka has taken several measures that

includes the establishments of the non-banking sector, innovations in the technology, compliance

risk processes, remuneration practices, improvements in the culture of the corporate and the

customers' relationship management for attaining the survival in the crisis time (Godley and

Lavoie, 2016). These measures enabled the system in mitigating the loss and the risk that

occurred due financial crisis.

4c. Presence of the Islamic banking and the financial institution.

Islamic banking in the Srilanka is been carried out mainly in two forms, on one hand it is

called as the fully-fledged Islamic system while on other side it is known as the co-existence

with the Islamic windows or the conventional banks (Kidwell and et.al., 2016). Particularly

eight banking institution in the Srilanka are carrying out the Islamic banking activities that are

based on the full fledged system. From the 8 banks one of the bank has the license for operating

as the commercial bank on the basis of the Islamic principles provisioned of transactions. The

other banks are been treated as the non banking corporations which are carrying out the Islamic

business in banking. Likewise, there are 38 conventional banks from which 4 are actively

participating in the Islamic business through the Islamic windows.

4d. Reasons and the changes that happened in the monetary policy.

The central of the Srilanka has disposed several ranges of the instruments that includes

direct and the indirect in conducting the monetary policy for the price stability. The indirect

measures such as bank rate, open market operations and the variable ratio. Theses measures

become useful to authorities in quick restoring the order in credit market for bringing desired

results. The monetary policy of the Srilanka keeps on changing over the years as the economy of

the Srilanka has shown the growing success in the past and the current years (Ball, 2017).

Decline in the monetary value of the Srilanka results in lower disposable income and prices has

The regulation and supervision of the banking system in Srilanka is in the hands of the

central bank (Cohen, 2018). Legal framework comprises Monetary law and banking act. Central

bank in Srilanka is has the powers for issuing the detailed directives to commercial bank. During

the 1993, Basel Accord has been adopted for the commercial banks. In accordance with the

Central bank, the capital ratios are been maintained at the comfortable level in the year 2017. At

the time of the global financial crisis banking sector of Srilanka has taken several measures that

includes the establishments of the non-banking sector, innovations in the technology, compliance

risk processes, remuneration practices, improvements in the culture of the corporate and the

customers' relationship management for attaining the survival in the crisis time (Godley and

Lavoie, 2016). These measures enabled the system in mitigating the loss and the risk that

occurred due financial crisis.

4c. Presence of the Islamic banking and the financial institution.

Islamic banking in the Srilanka is been carried out mainly in two forms, on one hand it is

called as the fully-fledged Islamic system while on other side it is known as the co-existence

with the Islamic windows or the conventional banks (Kidwell and et.al., 2016). Particularly

eight banking institution in the Srilanka are carrying out the Islamic banking activities that are

based on the full fledged system. From the 8 banks one of the bank has the license for operating

as the commercial bank on the basis of the Islamic principles provisioned of transactions. The

other banks are been treated as the non banking corporations which are carrying out the Islamic

business in banking. Likewise, there are 38 conventional banks from which 4 are actively

participating in the Islamic business through the Islamic windows.

4d. Reasons and the changes that happened in the monetary policy.

The central of the Srilanka has disposed several ranges of the instruments that includes

direct and the indirect in conducting the monetary policy for the price stability. The indirect

measures such as bank rate, open market operations and the variable ratio. Theses measures

become useful to authorities in quick restoring the order in credit market for bringing desired

results. The monetary policy of the Srilanka keeps on changing over the years as the economy of

the Srilanka has shown the growing success in the past and the current years (Ball, 2017).

Decline in the monetary value of the Srilanka results in lower disposable income and prices has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

been raised which in turn leads to inflation. Higher rate of interest results in depression in the

income but helps in stabilising the level of the prices. The findings depicts that the monetary

policy of Srilanka tended to be effective and the economy has realised the gloomy environment

even in the times of the global crisis.

4e. Discussion relating to the extent of the successful of the monetary policy.

Srilanka uses its monetary policy as the tool for keeping the inflation at lower rate. For

maintaining the inflation rate, Srilanka had opted for changing the intermediate targets or by

using the varying policy. Central bank had announced for the strict supply of the money at the

time when the country faced high inflation or the rate of inflation in the economy of the Srilanka

had been increased with the greater percentage (Berger and Bouwman, 2017). Thus, this country

has always been considered as the high inflation region as compared to the other countries.

5. Describing the view relating to the use of the monetary policy in solving the banking problems

worldwide.

The use of the monetary policy in the Srilanka has not been counted as suitable in resolving

the banking problems across the globe as it impacted the macro economic factors such as

inflation, volatility in the exchange rate had created higher risk. This affects the employment,

savings and the output in the overall economy.

CONCLUSION

From the above report it can be concluded that money and banking plays a major role in

maintaining the stability in the economy of Srilanka. Adoption of the monetary policy the bank

had lead to enhancement in the performance and is the major grounds for the suucess of the

Srilanka in the overall market worldwide.

income but helps in stabilising the level of the prices. The findings depicts that the monetary

policy of Srilanka tended to be effective and the economy has realised the gloomy environment

even in the times of the global crisis.

4e. Discussion relating to the extent of the successful of the monetary policy.

Srilanka uses its monetary policy as the tool for keeping the inflation at lower rate. For

maintaining the inflation rate, Srilanka had opted for changing the intermediate targets or by

using the varying policy. Central bank had announced for the strict supply of the money at the

time when the country faced high inflation or the rate of inflation in the economy of the Srilanka

had been increased with the greater percentage (Berger and Bouwman, 2017). Thus, this country

has always been considered as the high inflation region as compared to the other countries.

5. Describing the view relating to the use of the monetary policy in solving the banking problems

worldwide.

The use of the monetary policy in the Srilanka has not been counted as suitable in resolving

the banking problems across the globe as it impacted the macro economic factors such as

inflation, volatility in the exchange rate had created higher risk. This affects the employment,

savings and the output in the overall economy.

CONCLUSION

From the above report it can be concluded that money and banking plays a major role in

maintaining the stability in the economy of Srilanka. Adoption of the monetary policy the bank

had lead to enhancement in the performance and is the major grounds for the suucess of the

Srilanka in the overall market worldwide.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal

Ball, R. J., 2017. Inflation and the Theory of Money. Routledge.

Berger, A. N. and Bouwman, C. H., 2017. Bank liquidity creation, monetary policy, and

financial crises. Journal of Financial Stability. 30. pp.139-155.

Cohen, B. J., 2018. The geography of money. Cornell University Press.

Dang, T. V., and et.al., 2017. Banks as secret keepers. American Economic Review, 107(4),

pp.1005-29.

Godley, W. and Lavoie, M., 2016. Monetary economics: an integrated approach to credit,

money, income, production and wealth. Springer.

Kidwell, D. S., and et.al., 2016. Financial institutions, markets, and money. John Wiley & Sons.

Books and journal

Ball, R. J., 2017. Inflation and the Theory of Money. Routledge.

Berger, A. N. and Bouwman, C. H., 2017. Bank liquidity creation, monetary policy, and

financial crises. Journal of Financial Stability. 30. pp.139-155.

Cohen, B. J., 2018. The geography of money. Cornell University Press.

Dang, T. V., and et.al., 2017. Banks as secret keepers. American Economic Review, 107(4),

pp.1005-29.

Godley, W. and Lavoie, M., 2016. Monetary economics: an integrated approach to credit,

money, income, production and wealth. Springer.

Kidwell, D. S., and et.al., 2016. Financial institutions, markets, and money. John Wiley & Sons.

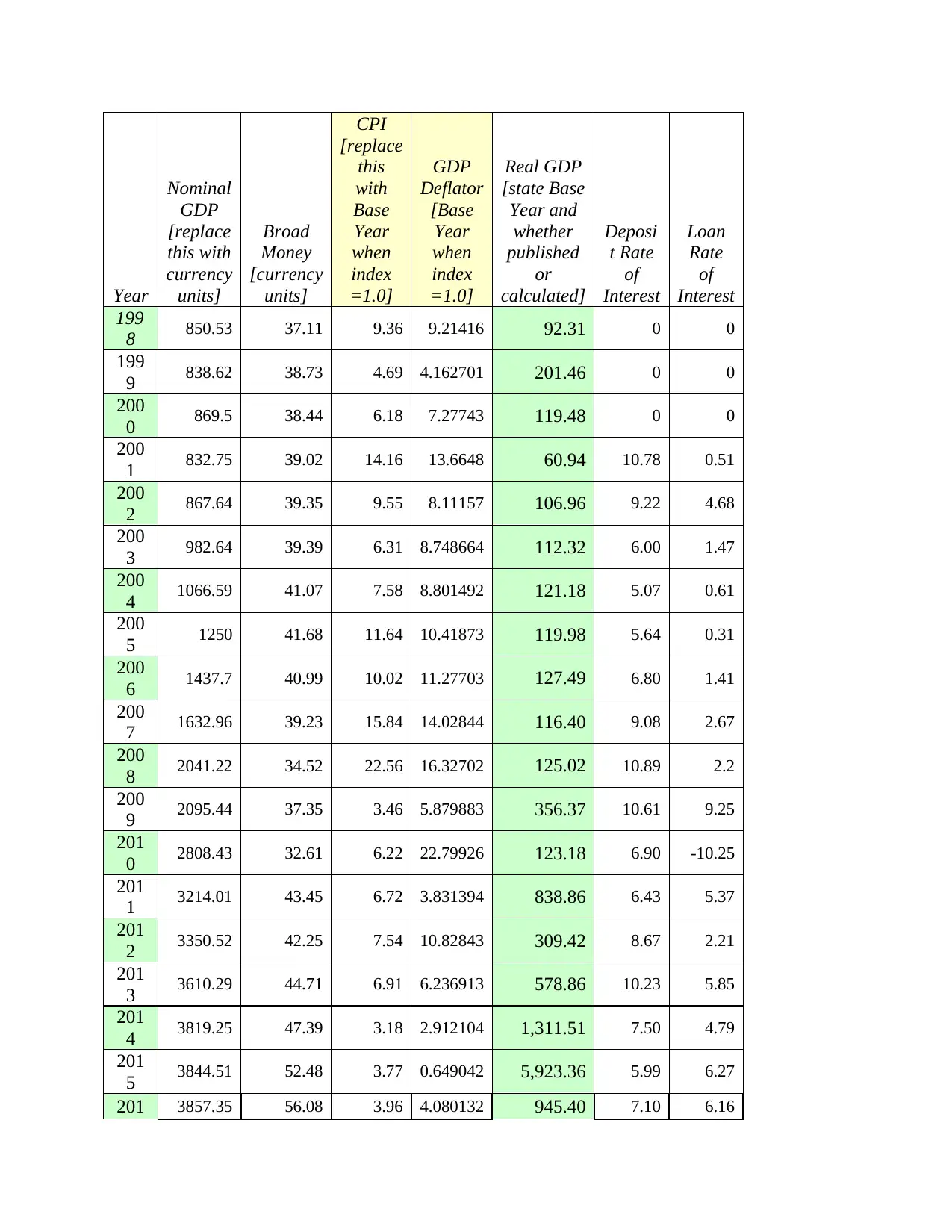

Year

Nominal

GDP

[replace

this with

currency

units]

Broad

Money

[currency

units]

CPI

[replace

this

with

Base

Year

when

index

=1.0]

GDP

Deflator

[Base

Year

when

index

=1.0]

Real GDP

[state Base

Year and

whether

published

or

calculated]

Deposi

t Rate

of

Interest

Loan

Rate

of

Interest

199

8 850.53 37.11 9.36 9.21416 92.31 0 0

199

9 838.62 38.73 4.69 4.162701 201.46 0 0

200

0 869.5 38.44 6.18 7.27743 119.48 0 0

200

1 832.75 39.02 14.16 13.6648 60.94 10.78 0.51

200

2 867.64 39.35 9.55 8.11157 106.96 9.22 4.68

200

3 982.64 39.39 6.31 8.748664 112.32 6.00 1.47

200

4 1066.59 41.07 7.58 8.801492 121.18 5.07 0.61

200

5 1250 41.68 11.64 10.41873 119.98 5.64 0.31

200

6 1437.7 40.99 10.02 11.27703 127.49 6.80 1.41

200

7 1632.96 39.23 15.84 14.02844 116.40 9.08 2.67

200

8 2041.22 34.52 22.56 16.32702 125.02 10.89 2.2

200

9 2095.44 37.35 3.46 5.879883 356.37 10.61 9.25

201

0 2808.43 32.61 6.22 22.79926 123.18 6.90 -10.25

201

1 3214.01 43.45 6.72 3.831394 838.86 6.43 5.37

201

2 3350.52 42.25 7.54 10.82843 309.42 8.67 2.21

201

3 3610.29 44.71 6.91 6.236913 578.86 10.23 5.85

201

4 3819.25 47.39 3.18 2.912104 1,311.51 7.50 4.79

201

5 3844.51 52.48 3.77 0.649042 5,923.36 5.99 6.27

201 3857.35 56.08 3.96 4.080132 945.40 7.10 6.16

Nominal

GDP

[replace

this with

currency

units]

Broad

Money

[currency

units]

CPI

[replace

this

with

Base

Year

when

index

=1.0]

GDP

Deflator

[Base

Year

when

index

=1.0]

Real GDP

[state Base

Year and

whether

published

or

calculated]

Deposi

t Rate

of

Interest

Loan

Rate

of

Interest

199

8 850.53 37.11 9.36 9.21416 92.31 0 0

199

9 838.62 38.73 4.69 4.162701 201.46 0 0

200

0 869.5 38.44 6.18 7.27743 119.48 0 0

200

1 832.75 39.02 14.16 13.6648 60.94 10.78 0.51

200

2 867.64 39.35 9.55 8.11157 106.96 9.22 4.68

200

3 982.64 39.39 6.31 8.748664 112.32 6.00 1.47

200

4 1066.59 41.07 7.58 8.801492 121.18 5.07 0.61

200

5 1250 41.68 11.64 10.41873 119.98 5.64 0.31

200

6 1437.7 40.99 10.02 11.27703 127.49 6.80 1.41

200

7 1632.96 39.23 15.84 14.02844 116.40 9.08 2.67

200

8 2041.22 34.52 22.56 16.32702 125.02 10.89 2.2

200

9 2095.44 37.35 3.46 5.879883 356.37 10.61 9.25

201

0 2808.43 32.61 6.22 22.79926 123.18 6.90 -10.25

201

1 3214.01 43.45 6.72 3.831394 838.86 6.43 5.37

201

2 3350.52 42.25 7.54 10.82843 309.42 8.67 2.21

201

3 3610.29 44.71 6.91 6.236913 578.86 10.23 5.85

201

4 3819.25 47.39 3.18 2.912104 1,311.51 7.50 4.79

201

5 3844.51 52.48 3.77 0.649042 5,923.36 5.99 6.27

201 3857.35 56.08 3.96 4.080132 945.40 7.10 6.16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

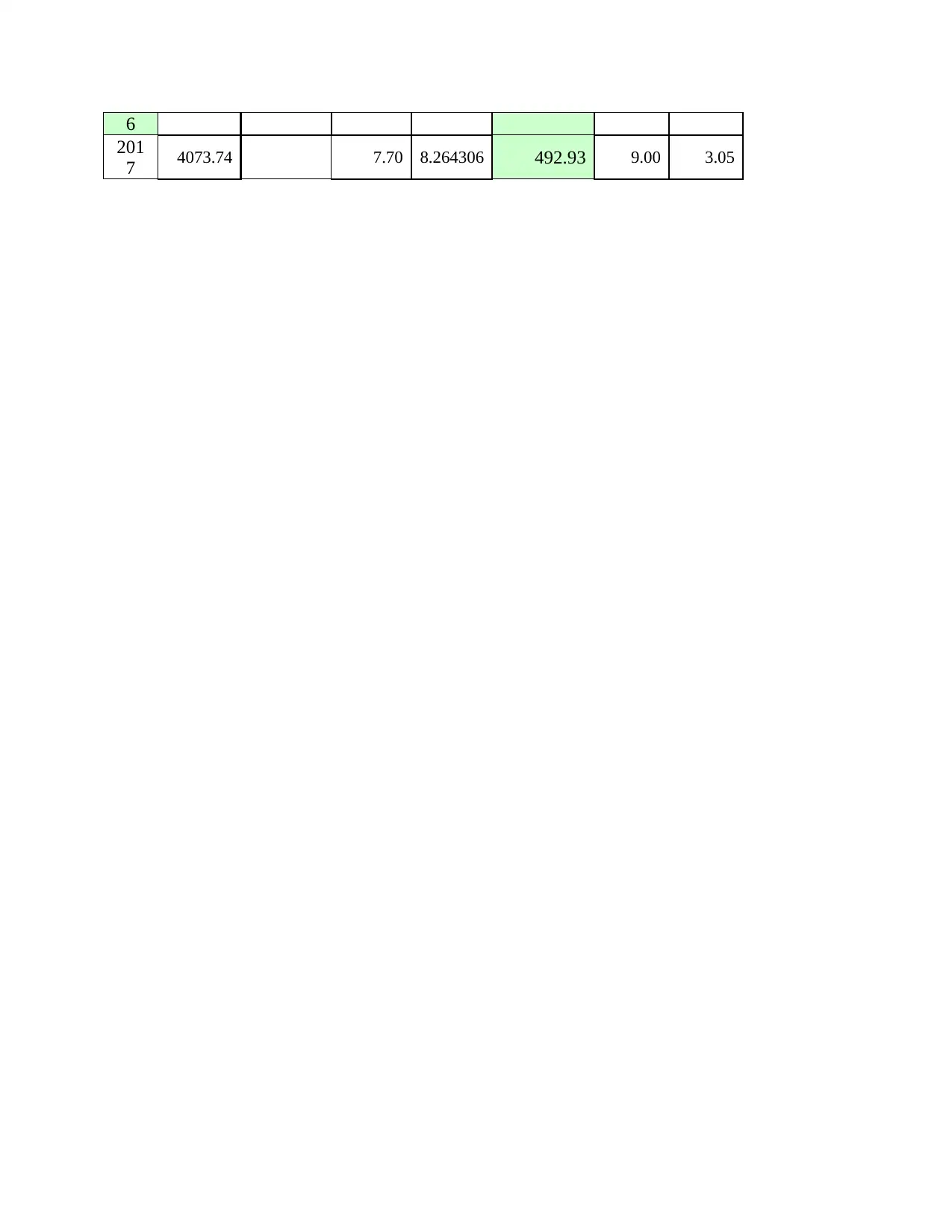

6

201

7 4073.74 7.70 8.264306 492.93 9.00 3.05

201

7 4073.74 7.70 8.264306 492.93 9.00 3.05

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.