ACC00713 Report: Impact of AASB 15 Revenue Recognition Standard

VerifiedAdded on 2022/11/26

|9

|2743

|395

Report

AI Summary

This report analyzes the impact of the new accounting standard AASB 15: Revenue from Contracts with Customers, focusing on changes in financial reporting. It explores the requirements and measurement of revenue under AASB 15, and presents a real-time example using ARB Corporation Limited, an ASX-listed company, to illustrate the standard's effects. The report also discusses the potential impact on inventory recognition and related metrics, noting that the timing of inventory recognition might be affected. The report highlights changes in disclosure requirements, but it finds that the overall impact on revenue and profit for the example company was not significant, although there was a significant increase in income other than sales. The report concludes by summarizing the key changes and implications of AASB 15, emphasizing that the changes were mostly in the form of enhanced disclosures.

Executive summary

This assignment aims to discuss briefly the changes occurred in reporting after the application of

new accounting standard AASB 15: Revenue recognition of contracts with customers. This is

provided along with a real time example of an ASX Listed company to understand the effects of

implementation of such standard in the financial reporting of the company. It also came to notice

during the course of the assignment that the inventory ownership and its recognition be a little

affected due to the change in the timing of recognition of such inventory in the name of the

company. The other standards on accounting will have no impact or less impact with the

introduction of this new accounting standard on revenue, that is AASB 15: revenue from contracts

with customers

This assignment aims to discuss briefly the changes occurred in reporting after the application of

new accounting standard AASB 15: Revenue recognition of contracts with customers. This is

provided along with a real time example of an ASX Listed company to understand the effects of

implementation of such standard in the financial reporting of the company. It also came to notice

during the course of the assignment that the inventory ownership and its recognition be a little

affected due to the change in the timing of recognition of such inventory in the name of the

company. The other standards on accounting will have no impact or less impact with the

introduction of this new accounting standard on revenue, that is AASB 15: revenue from contracts

with customers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction...........................................................................................................................................3

Part A.....................................................................................................................................................3

Revenue Recognition and Requirements as per AASB 15..................................................................3

Measurement of Revenue according to AASB 15..............................................................................4

Part B.....................................................................................................................................................4

Potential impact on adoption of AASB 15 in a Company...................................................................4

Conclusion.............................................................................................................................................6

References.............................................................................................................................................8

Introduction...........................................................................................................................................3

Part A.....................................................................................................................................................3

Revenue Recognition and Requirements as per AASB 15..................................................................3

Measurement of Revenue according to AASB 15..............................................................................4

Part B.....................................................................................................................................................4

Potential impact on adoption of AASB 15 in a Company...................................................................4

Conclusion.............................................................................................................................................6

References.............................................................................................................................................8

Introduction

As revenue recognition is vital for the performance of a company, it is important to have a separate

standard such as AASB 15 for dealing in the recognition of revenue by a company in its financial

statements. AASB 15, which, deal with revenue recognition of contracts with customers, requires a

company to record the revenue in its books of accounts only when the realisation of money from

such transaction is certain. The revenue from such transaction must be readily realisable with

certainty, this standard AASB 15 includes the recognition of only contracts related to customers, but

it does not deal with the recognition of leases, insurance contracts and financial instruments.

Part A

Revenue Recognition and Requirements as per AASB 15

Revenue recognition refers to recording of revenue from contracts or customers in the books of

accounts; this is in accordance with regulatory requirements in form of standards on accounting

issues by AASB. The applicable Accounting standard for recognition of revenue is AASB 15,

Recognition of revenue from contracts with customers (Alexander, 2016). There is a five-stage model

of recognising revenue as per this standard that is as follows:

The contract with the customer must be identified

The performance obligations identified in the contract

The transaction price to be determined (Dichev, 2017)

The transaction price should be allocated to the transaction price

When the obligations related to performance of that contract is satisfied the revenue is

recognised.

The company should assess the customer’s ability and concern to pay for the contract before

recognising such revenue from the contract. The price at which the transaction takes place be

recorded on pro rate to their relative standalone prices; here standalone prices would mean those

prices at which, these products or services sold separately. The AASB 15 requires various disclosures

while reporting revenue in the financial statements of a company.

A company has to disclose all of its particulars with the customers along with any significant

judgements and changes in the judgements, made in incorporating this standard into the company’s

reporting procedures to those contracts. In addition, there is compulsory disclosure of any

capitalised cost that incurred for fulfilling a contract with the customer. This AASB 15 is compulsory

for all the ASX listed entities to incorporate in its accounting process for financial reporting beginning

on or after 1-01-2018 (Mun, 2018).

Measurement of Revenue according to AASB 15

The revenue measured is in accordance with the agreed transaction amount for the sale of such

goods or services to the customers, it excludes any agreed third party payments, which would

normally include tax, transportation cost, etc. Even the estimate of the transaction is changed based

As revenue recognition is vital for the performance of a company, it is important to have a separate

standard such as AASB 15 for dealing in the recognition of revenue by a company in its financial

statements. AASB 15, which, deal with revenue recognition of contracts with customers, requires a

company to record the revenue in its books of accounts only when the realisation of money from

such transaction is certain. The revenue from such transaction must be readily realisable with

certainty, this standard AASB 15 includes the recognition of only contracts related to customers, but

it does not deal with the recognition of leases, insurance contracts and financial instruments.

Part A

Revenue Recognition and Requirements as per AASB 15

Revenue recognition refers to recording of revenue from contracts or customers in the books of

accounts; this is in accordance with regulatory requirements in form of standards on accounting

issues by AASB. The applicable Accounting standard for recognition of revenue is AASB 15,

Recognition of revenue from contracts with customers (Alexander, 2016). There is a five-stage model

of recognising revenue as per this standard that is as follows:

The contract with the customer must be identified

The performance obligations identified in the contract

The transaction price to be determined (Dichev, 2017)

The transaction price should be allocated to the transaction price

When the obligations related to performance of that contract is satisfied the revenue is

recognised.

The company should assess the customer’s ability and concern to pay for the contract before

recognising such revenue from the contract. The price at which the transaction takes place be

recorded on pro rate to their relative standalone prices; here standalone prices would mean those

prices at which, these products or services sold separately. The AASB 15 requires various disclosures

while reporting revenue in the financial statements of a company.

A company has to disclose all of its particulars with the customers along with any significant

judgements and changes in the judgements, made in incorporating this standard into the company’s

reporting procedures to those contracts. In addition, there is compulsory disclosure of any

capitalised cost that incurred for fulfilling a contract with the customer. This AASB 15 is compulsory

for all the ASX listed entities to incorporate in its accounting process for financial reporting beginning

on or after 1-01-2018 (Mun, 2018).

Measurement of Revenue according to AASB 15

The revenue measured is in accordance with the agreed transaction amount for the sale of such

goods or services to the customers, it excludes any agreed third party payments, which would

normally include tax, transportation cost, etc. Even the estimate of the transaction is changed based

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on the nature of such transaction by taking into consideration the timing involved and the amount

agreed for based on that (Arnott, et al., 2017). The consideration can be in any form, such as cash or

kind; the estimate of such revenue is inclusive of all such types of consideration. It may be variable

consideration depending on the product or service, or a fixed consideration irrespective of a certain

aspects of contracts, everything of these are involved in the measurement of revenue from contracts

with customers. If the consideration is a variable type, then the company will further analyse and

assess the amount that gained from such transaction and accordingly the amount recorded. Any

discounts, penalties, etc. considered while making an estimate of such revenue, including the

contingency of any event that is collateral to the happening of this transaction with the customer.

A company will determine a transaction in such a way that the agreed goods or services delivered to

the customer in a way, as it should be in according to the contract with customer. If there are any

changes in the transaction price due to its variable nature, then it is as and when it comes to the

knowledge of company updated regarding such event. If there is any finance component in the

consideration based on the contract then even that is considered while measurement of such

revenue (Smith, 2015). If there is any non-cash consideration from a customer for a contract, then

such consideration recorded at its fair value based on its receipt timing and nature (Jefferson, 2017).

The non-cash consideration recorded only when the right and possession of such non-cash element

transferred in company’s name. Similarly, if there is any consideration payable to a customer then

such amount will recorded as per the consideration measured in accordance with this standard on

accounting AASB 15.

Part B

Potential impact on adoption of AASB 15 in a Company

For purpose of this analysis, and to understand the impact of AASB 15, I have considered an ASX

Listed company “ARB CORPORATION LIMITED “in the latest annual report of this company. In the

annual report of the company, it mentioned at the beginning of disclosure for financial statements

that the financial reports are prepared in accordance with the requirements of Australian

Accounting Standards Board laid AASB standards on financial reporting Framework. Thus complying

with the applicable new accounting standard AASB 15 that deals with recognition of revenue from

contracts with customers (Sithole, et al., 2017). This mentioned under the notes to the financial

statements column that the adoption of AASB 15 on consolidated financial statements of the entity

will have no effect on the revenue recognition of any contracts with customers and there is no

significant change identified from application of this standard AASB 15.

With the adoption of AASB 15, there will be an enhanced disclosures relating to its revenue, provides

guidelines for those that were dealt in the earlier standard including guidelines for multiple level

arrangements. The revenue from sales for this company has grown at an average of 9.5 % over 10

years, based on this view; the adoption of AASB 15 did not affect the change in the average revenue

from sales of this company (Dumay & Baard, 2017). In addition, when we look at the average of 10

years of profit after tax, we can see that it has grown at a constant rate of 10.6 %, even here in this

case, there is no much deviation in the growth of profits that is derived after tax with adoption of

AASB 15. There may be a change in disclosure requirement as the company has mentioned in its

annual report under notes to financial statements but there is no much change in terms of its

revenue nor in terms of its profit after tax comparing last 10 years of operations of the company.

agreed for based on that (Arnott, et al., 2017). The consideration can be in any form, such as cash or

kind; the estimate of such revenue is inclusive of all such types of consideration. It may be variable

consideration depending on the product or service, or a fixed consideration irrespective of a certain

aspects of contracts, everything of these are involved in the measurement of revenue from contracts

with customers. If the consideration is a variable type, then the company will further analyse and

assess the amount that gained from such transaction and accordingly the amount recorded. Any

discounts, penalties, etc. considered while making an estimate of such revenue, including the

contingency of any event that is collateral to the happening of this transaction with the customer.

A company will determine a transaction in such a way that the agreed goods or services delivered to

the customer in a way, as it should be in according to the contract with customer. If there are any

changes in the transaction price due to its variable nature, then it is as and when it comes to the

knowledge of company updated regarding such event. If there is any finance component in the

consideration based on the contract then even that is considered while measurement of such

revenue (Smith, 2015). If there is any non-cash consideration from a customer for a contract, then

such consideration recorded at its fair value based on its receipt timing and nature (Jefferson, 2017).

The non-cash consideration recorded only when the right and possession of such non-cash element

transferred in company’s name. Similarly, if there is any consideration payable to a customer then

such amount will recorded as per the consideration measured in accordance with this standard on

accounting AASB 15.

Part B

Potential impact on adoption of AASB 15 in a Company

For purpose of this analysis, and to understand the impact of AASB 15, I have considered an ASX

Listed company “ARB CORPORATION LIMITED “in the latest annual report of this company. In the

annual report of the company, it mentioned at the beginning of disclosure for financial statements

that the financial reports are prepared in accordance with the requirements of Australian

Accounting Standards Board laid AASB standards on financial reporting Framework. Thus complying

with the applicable new accounting standard AASB 15 that deals with recognition of revenue from

contracts with customers (Sithole, et al., 2017). This mentioned under the notes to the financial

statements column that the adoption of AASB 15 on consolidated financial statements of the entity

will have no effect on the revenue recognition of any contracts with customers and there is no

significant change identified from application of this standard AASB 15.

With the adoption of AASB 15, there will be an enhanced disclosures relating to its revenue, provides

guidelines for those that were dealt in the earlier standard including guidelines for multiple level

arrangements. The revenue from sales for this company has grown at an average of 9.5 % over 10

years, based on this view; the adoption of AASB 15 did not affect the change in the average revenue

from sales of this company (Dumay & Baard, 2017). In addition, when we look at the average of 10

years of profit after tax, we can see that it has grown at a constant rate of 10.6 %, even here in this

case, there is no much deviation in the growth of profits that is derived after tax with adoption of

AASB 15. There may be a change in disclosure requirement as the company has mentioned in its

annual report under notes to financial statements but there is no much change in terms of its

revenue nor in terms of its profit after tax comparing last 10 years of operations of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

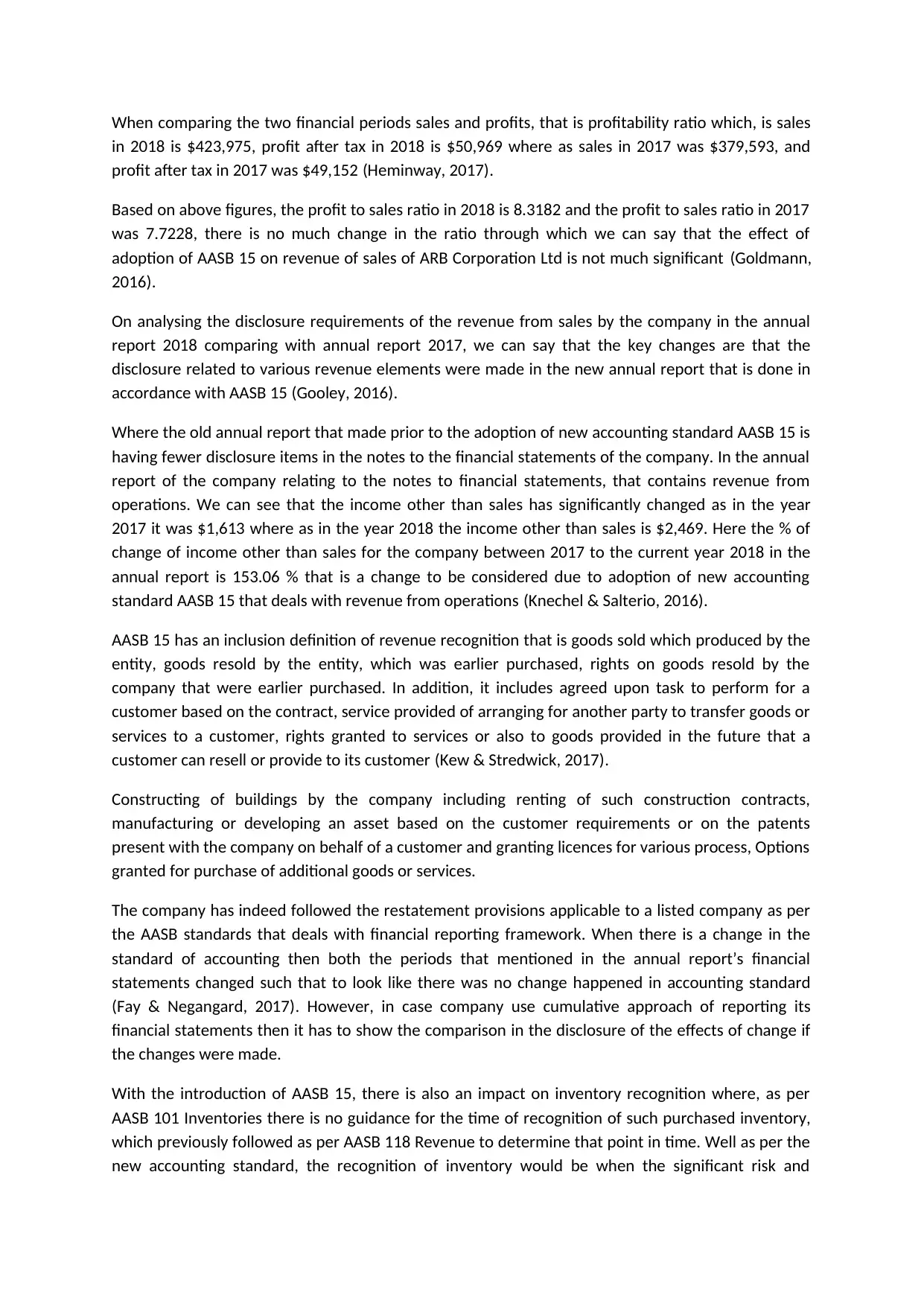

When comparing the two financial periods sales and profits, that is profitability ratio which, is sales

in 2018 is $423,975, profit after tax in 2018 is $50,969 where as sales in 2017 was $379,593, and

profit after tax in 2017 was $49,152 (Heminway, 2017).

Based on above figures, the profit to sales ratio in 2018 is 8.3182 and the profit to sales ratio in 2017

was 7.7228, there is no much change in the ratio through which we can say that the effect of

adoption of AASB 15 on revenue of sales of ARB Corporation Ltd is not much significant (Goldmann,

2016).

On analysing the disclosure requirements of the revenue from sales by the company in the annual

report 2018 comparing with annual report 2017, we can say that the key changes are that the

disclosure related to various revenue elements were made in the new annual report that is done in

accordance with AASB 15 (Gooley, 2016).

Where the old annual report that made prior to the adoption of new accounting standard AASB 15 is

having fewer disclosure items in the notes to the financial statements of the company. In the annual

report of the company relating to the notes to financial statements, that contains revenue from

operations. We can see that the income other than sales has significantly changed as in the year

2017 it was $1,613 where as in the year 2018 the income other than sales is $2,469. Here the % of

change of income other than sales for the company between 2017 to the current year 2018 in the

annual report is 153.06 % that is a change to be considered due to adoption of new accounting

standard AASB 15 that deals with revenue from operations (Knechel & Salterio, 2016).

AASB 15 has an inclusion definition of revenue recognition that is goods sold which produced by the

entity, goods resold by the entity, which was earlier purchased, rights on goods resold by the

company that were earlier purchased. In addition, it includes agreed upon task to perform for a

customer based on the contract, service provided of arranging for another party to transfer goods or

services to a customer, rights granted to services or also to goods provided in the future that a

customer can resell or provide to its customer (Kew & Stredwick, 2017).

Constructing of buildings by the company including renting of such construction contracts,

manufacturing or developing an asset based on the customer requirements or on the patents

present with the company on behalf of a customer and granting licences for various process, Options

granted for purchase of additional goods or services.

The company has indeed followed the restatement provisions applicable to a listed company as per

the AASB standards that deals with financial reporting framework. When there is a change in the

standard of accounting then both the periods that mentioned in the annual report’s financial

statements changed such that to look like there was no change happened in accounting standard

(Fay & Negangard, 2017). However, in case company use cumulative approach of reporting its

financial statements then it has to show the comparison in the disclosure of the effects of change if

the changes were made.

With the introduction of AASB 15, there is also an impact on inventory recognition where, as per

AASB 101 Inventories there is no guidance for the time of recognition of such purchased inventory,

which previously followed as per AASB 118 Revenue to determine that point in time. Well as per the

new accounting standard, the recognition of inventory would be when the significant risk and

in 2018 is $423,975, profit after tax in 2018 is $50,969 where as sales in 2017 was $379,593, and

profit after tax in 2017 was $49,152 (Heminway, 2017).

Based on above figures, the profit to sales ratio in 2018 is 8.3182 and the profit to sales ratio in 2017

was 7.7228, there is no much change in the ratio through which we can say that the effect of

adoption of AASB 15 on revenue of sales of ARB Corporation Ltd is not much significant (Goldmann,

2016).

On analysing the disclosure requirements of the revenue from sales by the company in the annual

report 2018 comparing with annual report 2017, we can say that the key changes are that the

disclosure related to various revenue elements were made in the new annual report that is done in

accordance with AASB 15 (Gooley, 2016).

Where the old annual report that made prior to the adoption of new accounting standard AASB 15 is

having fewer disclosure items in the notes to the financial statements of the company. In the annual

report of the company relating to the notes to financial statements, that contains revenue from

operations. We can see that the income other than sales has significantly changed as in the year

2017 it was $1,613 where as in the year 2018 the income other than sales is $2,469. Here the % of

change of income other than sales for the company between 2017 to the current year 2018 in the

annual report is 153.06 % that is a change to be considered due to adoption of new accounting

standard AASB 15 that deals with revenue from operations (Knechel & Salterio, 2016).

AASB 15 has an inclusion definition of revenue recognition that is goods sold which produced by the

entity, goods resold by the entity, which was earlier purchased, rights on goods resold by the

company that were earlier purchased. In addition, it includes agreed upon task to perform for a

customer based on the contract, service provided of arranging for another party to transfer goods or

services to a customer, rights granted to services or also to goods provided in the future that a

customer can resell or provide to its customer (Kew & Stredwick, 2017).

Constructing of buildings by the company including renting of such construction contracts,

manufacturing or developing an asset based on the customer requirements or on the patents

present with the company on behalf of a customer and granting licences for various process, Options

granted for purchase of additional goods or services.

The company has indeed followed the restatement provisions applicable to a listed company as per

the AASB standards that deals with financial reporting framework. When there is a change in the

standard of accounting then both the periods that mentioned in the annual report’s financial

statements changed such that to look like there was no change happened in accounting standard

(Fay & Negangard, 2017). However, in case company use cumulative approach of reporting its

financial statements then it has to show the comparison in the disclosure of the effects of change if

the changes were made.

With the introduction of AASB 15, there is also an impact on inventory recognition where, as per

AASB 101 Inventories there is no guidance for the time of recognition of such purchased inventory,

which previously followed as per AASB 118 Revenue to determine that point in time. Well as per the

new accounting standard, the recognition of inventory would be when the significant risk and

reward of such inventory transferred to the name of the company. Thus, this change in the timing of

recognition of inventory could influence the inventory management metrics and working capital

ratios of the company (Hepp, 2018).

Conclusion

Based on all the detailed above analysis of the changes caused to a listed company on adoption of a

new standard on accounting, which is AASB 15, there is no much changes in terms of numbers in

revenue from operations as well as income other than revenue. We have seen even the profit after

tax has not changed even after implementation of this standard on accounting,

it is thus noted as per the observation that the change in financial reporting to the company is

basically was in the change of disclosures which is enhanced with further detail on those revenues

that was earlier not part of the notes to the accounts and key changes that happen when reporting

interim financial statements during the period of 2018 – 2019 as the new standard on accounting

came into force only in between of the financial year but not at the beginning of the financial year

(Lavassani & Movahedi, 2017).

The evidences for the above explanation is as below:

recognition of inventory could influence the inventory management metrics and working capital

ratios of the company (Hepp, 2018).

Conclusion

Based on all the detailed above analysis of the changes caused to a listed company on adoption of a

new standard on accounting, which is AASB 15, there is no much changes in terms of numbers in

revenue from operations as well as income other than revenue. We have seen even the profit after

tax has not changed even after implementation of this standard on accounting,

it is thus noted as per the observation that the change in financial reporting to the company is

basically was in the change of disclosures which is enhanced with further detail on those revenues

that was earlier not part of the notes to the accounts and key changes that happen when reporting

interim financial statements during the period of 2018 – 2019 as the new standard on accounting

came into force only in between of the financial year but not at the beginning of the financial year

(Lavassani & Movahedi, 2017).

The evidences for the above explanation is as below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Dumay, J. & Baard, V., 2017. An introduction to interventionist research in accounting.. The

Routledge Companion to Qualitative Accounting Research Methods, 1(1), p. 265.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, Volume 38, pp. 37-49.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

Gooley, J., 2016. Principles of Australian Contract Law. 2 ed. Australia: Lexis Nexis.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Hepp, J., 2018. ASC 606: Challenges in understanding and applying revenue recognition. Journal of

Accounting Education, 42(1), pp. 49-51.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed.

London: Chartered Institute of Personnel and Development.

Knechel, W. & Salterio, S., 2016. Auditing:Assurance and Risk. 4th ed. New York: Routledge.

Lavassani, K. & Movahedi, B., 2017. Applications Driven Information Systems: Beyond Networks

toward Business Ecosystems. International Journal of Innovation in the Digital Economy.

Mun, K. a. S. I., 2018. A close look at the role of regulatory fit in consumers’ responses to unethical

firms.. s.l.:s.n.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Smith, G. S., 2015. The Accountant Stereotype: Positive or Negative?. The Research Gate, 10(3), pp.

1-3.

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Dumay, J. & Baard, V., 2017. An introduction to interventionist research in accounting.. The

Routledge Companion to Qualitative Accounting Research Methods, 1(1), p. 265.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, Volume 38, pp. 37-49.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

Gooley, J., 2016. Principles of Australian Contract Law. 2 ed. Australia: Lexis Nexis.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Hepp, J., 2018. ASC 606: Challenges in understanding and applying revenue recognition. Journal of

Accounting Education, 42(1), pp. 49-51.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed.

London: Chartered Institute of Personnel and Development.

Knechel, W. & Salterio, S., 2016. Auditing:Assurance and Risk. 4th ed. New York: Routledge.

Lavassani, K. & Movahedi, B., 2017. Applications Driven Information Systems: Beyond Networks

toward Business Ecosystems. International Journal of Innovation in the Digital Economy.

Mun, K. a. S. I., 2018. A close look at the role of regulatory fit in consumers’ responses to unethical

firms.. s.l.:s.n.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Smith, G. S., 2015. The Accountant Stereotype: Positive or Negative?. The Research Gate, 10(3), pp.

1-3.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.