EXECUTIVE SUMMARY The main objective of this particular

VerifiedAdded on 2023/03/31

|9

|2601

|489

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

EXECUTIVE SUMMARY

The main objective of this particular assignment is extension of knowledge in the

field of various Australian Accounting Standard Board (AASB) i.e. AASB 3: AASB

3: Business Combinations, AASB 128 Investments in Associates and Joint

Ventures and AASB 10 Consolidated Financial Statements, to AASB 127

Consolidated and Separate Financial Statements and AASB 10 Consolidated

Financial Statements, AASB 127 Consolidated and Separate Financial Statements

and AASB 101 Presentation of Financial Statements and how the accounting is to

be done in the relevant books of accounts of the company.

The main objective of this particular assignment is extension of knowledge in the

field of various Australian Accounting Standard Board (AASB) i.e. AASB 3: AASB

3: Business Combinations, AASB 128 Investments in Associates and Joint

Ventures and AASB 10 Consolidated Financial Statements, to AASB 127

Consolidated and Separate Financial Statements and AASB 10 Consolidated

Financial Statements, AASB 127 Consolidated and Separate Financial Statements

and AASB 101 Presentation of Financial Statements and how the accounting is to

be done in the relevant books of accounts of the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

EXECUTIVE SUMMARY..........................................................................................1

INTRODUCTION....................................................................................................3

PART A.................................................................................................................3

PART B.................................................................................................................4

Calculation of consolidated revenue.......................................................................5

Calculation of Consolidated cost of sales................................................................5

Mutual Set off..........................................................................................................5

Valuation of inventory.............................................................................................5

PART C.................................................................................................................5

Calculation of goodwill/bargain purchase...............................................................6

Calculation of profit attributable to NCI..................................................................7

CONCLUSION........................................................................................................7

References..............................................................................................................8

EXECUTIVE SUMMARY..........................................................................................1

INTRODUCTION....................................................................................................3

PART A.................................................................................................................3

PART B.................................................................................................................4

Calculation of consolidated revenue.......................................................................5

Calculation of Consolidated cost of sales................................................................5

Mutual Set off..........................................................................................................5

Valuation of inventory.............................................................................................5

PART C.................................................................................................................5

Calculation of goodwill/bargain purchase...............................................................6

Calculation of profit attributable to NCI..................................................................7

CONCLUSION........................................................................................................7

References..............................................................................................................8

INTRODUCTION

The assignment deals with accounting under various situations like accounting

under consolidation accounting and Equity accounting, how the intra group

transaction between the two companies should be recorded. The brief description

regarding the non-controlling interest disclosure requirement as a separate part

in the consolidation process. The effect of the various Australian Accounting

Standard on accounting aspect of the entity.

PART A

Business Combination is quite a happening phenomenon in today’s corporate

world. In order to provide it an acceptable accounting sanctity AASB 3: Business

Combinations has been framed which provides that the transfer of control of an

entity to another through a transaction between two parties is the essence of a

business combination. ( Commonwealth of Australia 2015, 2015) However, the

synergies achieved by a business combination have to be brought into books

which is charted out in AASB 10: Consolidated Financial Statement. As per this

standard an entity is said to be having control over another entity if it

participates in its equity-oriented returns.

Now, there are two methods of accounting prescribed for reporting such

transactions - “Consolidation Accounting” and “Equity Accounting”. There is a

major reporting difference between these two methods in the context that while

in consolidation accounting the parent’s financial statements and the subsidiary’s

statements are combined to prepare the results of the entire group but in equity

accounting the investment in the subsidiary is shown as a single line item in the

parent’s financial statements. The choice between the two is mostly entity

specific and at times situation specific as well. For instance, an entity may prefer

to save the trouble of preparing detailed records as required by consolidation

accounting for purchase consideration, non- controlling interest, the goodwill

acquired etc. However, in case of substantial control acquired such detailed

reporting is preferable as the magnitude of the stakes are quite high in that

respect. The equity method of accounting is certainly less cumbersome but it

fails to report the finer details involved in such transactions as aforementioned.

So, in order to resolve this dilemma, the emphasis is placed on the magnitude of

control. Generally, consolidation accounting is preferred for stakes above 50%.

To have a clearer picture of the complex aspects of these two methods, let us

take the following scenario:

Suppose Company A acquired 35% stake in Company B which is worth 1 billion

dollars. So, it incurred an outflow of $350 million from its resources.

Now, going by the equity method the investment of $350 million would be

reported in co. A’s balance sheet as an asset. Company A is entitled to a dividend

of 35% from B which can be reported as an income in its financial statements.

Correspondingly, the value of the investment will also go up due to the income

The assignment deals with accounting under various situations like accounting

under consolidation accounting and Equity accounting, how the intra group

transaction between the two companies should be recorded. The brief description

regarding the non-controlling interest disclosure requirement as a separate part

in the consolidation process. The effect of the various Australian Accounting

Standard on accounting aspect of the entity.

PART A

Business Combination is quite a happening phenomenon in today’s corporate

world. In order to provide it an acceptable accounting sanctity AASB 3: Business

Combinations has been framed which provides that the transfer of control of an

entity to another through a transaction between two parties is the essence of a

business combination. ( Commonwealth of Australia 2015, 2015) However, the

synergies achieved by a business combination have to be brought into books

which is charted out in AASB 10: Consolidated Financial Statement. As per this

standard an entity is said to be having control over another entity if it

participates in its equity-oriented returns.

Now, there are two methods of accounting prescribed for reporting such

transactions - “Consolidation Accounting” and “Equity Accounting”. There is a

major reporting difference between these two methods in the context that while

in consolidation accounting the parent’s financial statements and the subsidiary’s

statements are combined to prepare the results of the entire group but in equity

accounting the investment in the subsidiary is shown as a single line item in the

parent’s financial statements. The choice between the two is mostly entity

specific and at times situation specific as well. For instance, an entity may prefer

to save the trouble of preparing detailed records as required by consolidation

accounting for purchase consideration, non- controlling interest, the goodwill

acquired etc. However, in case of substantial control acquired such detailed

reporting is preferable as the magnitude of the stakes are quite high in that

respect. The equity method of accounting is certainly less cumbersome but it

fails to report the finer details involved in such transactions as aforementioned.

So, in order to resolve this dilemma, the emphasis is placed on the magnitude of

control. Generally, consolidation accounting is preferred for stakes above 50%.

To have a clearer picture of the complex aspects of these two methods, let us

take the following scenario:

Suppose Company A acquired 35% stake in Company B which is worth 1 billion

dollars. So, it incurred an outflow of $350 million from its resources.

Now, going by the equity method the investment of $350 million would be

reported in co. A’s balance sheet as an asset. Company A is entitled to a dividend

of 35% from B which can be reported as an income in its financial statements.

Correspondingly, the value of the investment will also go up due to the income

earned. But in case of losses, vice-versa treatment will be followed thereby

decreasing the value of the investment in the subsidiary.

On the other hand, under the consolidation method separate financial statements

will be prepared by combining the standalone statements of A and B. In that case

line by line addition of the items present in the respective financial statements

will be done. However, certain rules are to be abided by so that ineligible

transactions like intra group transactions do not get reported. In this case, no

separate item is included in the name of investment made in the subsidiary.

So, in a nutshell the choice between the method for accounting of business

combinations is basically a conscious one in which the management must

consider the size as well as financial status of the control position in the acquired

entity.

PART B

Intra group transactions are quite a natural and inherent part of the commercial

relationship between two entities forming part of the same group. These are

transactions which takes place between two entities bound in a control

relationship. Under the accounting standards, these transactions are covered by

AASB 10 Consolidated Financial statement. For example, the sale of goods by a

subsidiary to its parent is an intra group transaction which will be reported as an

ordinary sale in the books of the subsidiary and as an ordinary purchase in the

books of the parent company. However, for consolidation purposes this

transaction is ignored because it is an intra group transaction. (jade.io, 2015)

Similarly, if there is any stock left with the parent which consists of the goods

purchased from the subsidiary then the profit made by the subsidiary on the

transaction will be proportionately reduced from the value of such stock for

consolidation purposes. In fact, AASB 10 also mandates the compulsory

elimination of intra group transactions whether downstream or upstream.

(PricewaterhouseCoopers, 2018)

Proceeding on similar lines the adjustment must be made for mutual set off of

debts owed within the group itself. For example, a debt of $20 million owed by

the subsidiary can be set off with a debt of same or higher amount owed by the

parent to the subsidiary.

In the given case, the parent JKY ltd. has availed certain professional services

from its partially owned subsidiary. This type of transaction gives rise to a

situation where elimination must be made on the lines of AASB 10. By providing

these services the subsidiary must have earned certain revenue in the form of

payments made by the parent for availing these services. So, at the time of

consolidation the income of the subsidiary will be reduced by the amount

received for providing these services and the similarly the expenses will be

reduced in the context of the parent (JKY Ltd.) with the corresponding amount.

Accordingly, entry for mutual set off must also be passed for adjustment of any

balances of owed within the group. The non - controlling interest will also be

reduced as the income of the subsidiary is getting reduced which has a direct

bearing on the profits attributable to non – controlling shareholders.

Secondly, the parent (JKY Ltd.) has also received certain goods from the

subsidiary which gives rise to two types of situations- the entire stock has been

decreasing the value of the investment in the subsidiary.

On the other hand, under the consolidation method separate financial statements

will be prepared by combining the standalone statements of A and B. In that case

line by line addition of the items present in the respective financial statements

will be done. However, certain rules are to be abided by so that ineligible

transactions like intra group transactions do not get reported. In this case, no

separate item is included in the name of investment made in the subsidiary.

So, in a nutshell the choice between the method for accounting of business

combinations is basically a conscious one in which the management must

consider the size as well as financial status of the control position in the acquired

entity.

PART B

Intra group transactions are quite a natural and inherent part of the commercial

relationship between two entities forming part of the same group. These are

transactions which takes place between two entities bound in a control

relationship. Under the accounting standards, these transactions are covered by

AASB 10 Consolidated Financial statement. For example, the sale of goods by a

subsidiary to its parent is an intra group transaction which will be reported as an

ordinary sale in the books of the subsidiary and as an ordinary purchase in the

books of the parent company. However, for consolidation purposes this

transaction is ignored because it is an intra group transaction. (jade.io, 2015)

Similarly, if there is any stock left with the parent which consists of the goods

purchased from the subsidiary then the profit made by the subsidiary on the

transaction will be proportionately reduced from the value of such stock for

consolidation purposes. In fact, AASB 10 also mandates the compulsory

elimination of intra group transactions whether downstream or upstream.

(PricewaterhouseCoopers, 2018)

Proceeding on similar lines the adjustment must be made for mutual set off of

debts owed within the group itself. For example, a debt of $20 million owed by

the subsidiary can be set off with a debt of same or higher amount owed by the

parent to the subsidiary.

In the given case, the parent JKY ltd. has availed certain professional services

from its partially owned subsidiary. This type of transaction gives rise to a

situation where elimination must be made on the lines of AASB 10. By providing

these services the subsidiary must have earned certain revenue in the form of

payments made by the parent for availing these services. So, at the time of

consolidation the income of the subsidiary will be reduced by the amount

received for providing these services and the similarly the expenses will be

reduced in the context of the parent (JKY Ltd.) with the corresponding amount.

Accordingly, entry for mutual set off must also be passed for adjustment of any

balances of owed within the group. The non - controlling interest will also be

reduced as the income of the subsidiary is getting reduced which has a direct

bearing on the profits attributable to non – controlling shareholders.

Secondly, the parent (JKY Ltd.) has also received certain goods from the

subsidiary which gives rise to two types of situations- the entire stock has been

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

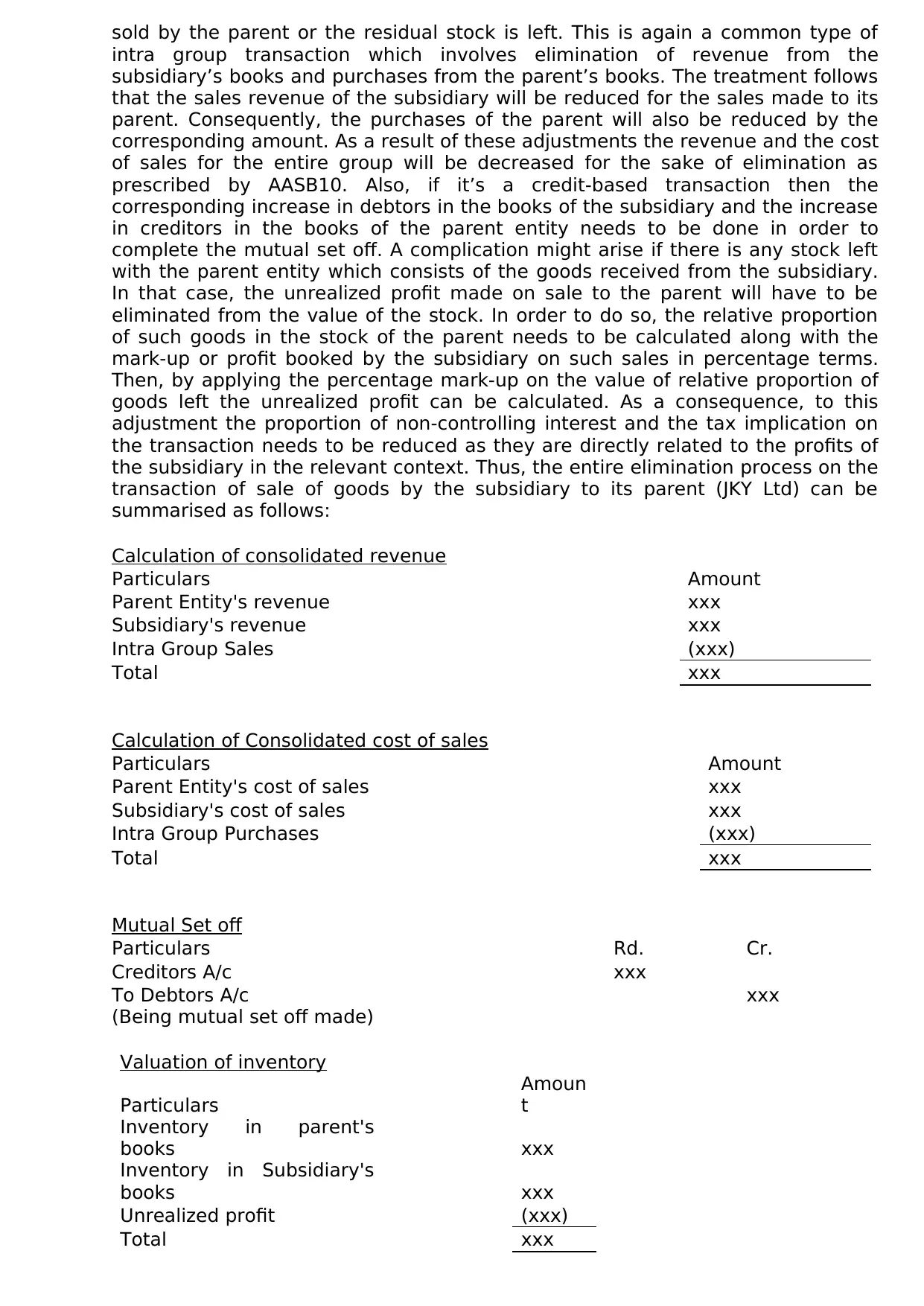

sold by the parent or the residual stock is left. This is again a common type of

intra group transaction which involves elimination of revenue from the

subsidiary’s books and purchases from the parent’s books. The treatment follows

that the sales revenue of the subsidiary will be reduced for the sales made to its

parent. Consequently, the purchases of the parent will also be reduced by the

corresponding amount. As a result of these adjustments the revenue and the cost

of sales for the entire group will be decreased for the sake of elimination as

prescribed by AASB10. Also, if it’s a credit-based transaction then the

corresponding increase in debtors in the books of the subsidiary and the increase

in creditors in the books of the parent entity needs to be done in order to

complete the mutual set off. A complication might arise if there is any stock left

with the parent entity which consists of the goods received from the subsidiary.

In that case, the unrealized profit made on sale to the parent will have to be

eliminated from the value of the stock. In order to do so, the relative proportion

of such goods in the stock of the parent needs to be calculated along with the

mark-up or profit booked by the subsidiary on such sales in percentage terms.

Then, by applying the percentage mark-up on the value of relative proportion of

goods left the unrealized profit can be calculated. As a consequence, to this

adjustment the proportion of non-controlling interest and the tax implication on

the transaction needs to be reduced as they are directly related to the profits of

the subsidiary in the relevant context. Thus, the entire elimination process on the

transaction of sale of goods by the subsidiary to its parent (JKY Ltd) can be

summarised as follows:

Calculation of consolidated revenue

Particulars Amount

Parent Entity's revenue xxx

Subsidiary's revenue xxx

Intra Group Sales (xxx)

Total xxx

Calculation of Consolidated cost of sales

Particulars Amount

Parent Entity's cost of sales xxx

Subsidiary's cost of sales xxx

Intra Group Purchases (xxx)

Total xxx

Mutual Set off

Particulars Rd. Cr.

Creditors A/c xxx

To Debtors A/c xxx

(Being mutual set off made)

Valuation of inventory

Particulars

Amoun

t

Inventory in parent's

books xxx

Inventory in Subsidiary's

books xxx

Unrealized profit (xxx)

Total xxx

intra group transaction which involves elimination of revenue from the

subsidiary’s books and purchases from the parent’s books. The treatment follows

that the sales revenue of the subsidiary will be reduced for the sales made to its

parent. Consequently, the purchases of the parent will also be reduced by the

corresponding amount. As a result of these adjustments the revenue and the cost

of sales for the entire group will be decreased for the sake of elimination as

prescribed by AASB10. Also, if it’s a credit-based transaction then the

corresponding increase in debtors in the books of the subsidiary and the increase

in creditors in the books of the parent entity needs to be done in order to

complete the mutual set off. A complication might arise if there is any stock left

with the parent entity which consists of the goods received from the subsidiary.

In that case, the unrealized profit made on sale to the parent will have to be

eliminated from the value of the stock. In order to do so, the relative proportion

of such goods in the stock of the parent needs to be calculated along with the

mark-up or profit booked by the subsidiary on such sales in percentage terms.

Then, by applying the percentage mark-up on the value of relative proportion of

goods left the unrealized profit can be calculated. As a consequence, to this

adjustment the proportion of non-controlling interest and the tax implication on

the transaction needs to be reduced as they are directly related to the profits of

the subsidiary in the relevant context. Thus, the entire elimination process on the

transaction of sale of goods by the subsidiary to its parent (JKY Ltd) can be

summarised as follows:

Calculation of consolidated revenue

Particulars Amount

Parent Entity's revenue xxx

Subsidiary's revenue xxx

Intra Group Sales (xxx)

Total xxx

Calculation of Consolidated cost of sales

Particulars Amount

Parent Entity's cost of sales xxx

Subsidiary's cost of sales xxx

Intra Group Purchases (xxx)

Total xxx

Mutual Set off

Particulars Rd. Cr.

Creditors A/c xxx

To Debtors A/c xxx

(Being mutual set off made)

Valuation of inventory

Particulars

Amoun

t

Inventory in parent's

books xxx

Inventory in Subsidiary's

books xxx

Unrealized profit (xxx)

Total xxx

PART C

Non-controlling interest represents the interest of those shareholders whose

claim in the total equity of a subsidiary is quite nominal as compared to the

interests of the parent company. In other words, the portion of equity not owned

by the parent in the subsidiary is called non-controlling interest. (CFI Education

Inc., 2019)These investors can be considered as minority investors as their

stakes in the company are marginal, i.e. normally less than 50%. While

preparation of consolidated financial statements for the entire group due

consideration is taken for combining the various items of the financial statements

of the parent and the subsidiary. Basically, the various assets and liabilities are

added on a line by line basis with certain adjustments being undertaken for

elimination of intragroup transactions and reporting the financial results.

However, the investment made in the subsidiary by the parent entity represented

as an asset in the books of the parent is set off against the equity and reserves of

the subsidiary.

As mentioned above, the non-controlling interest (NCI) which represents the

interest of the minority shareholders is quite a significant item in this type of

reporting. AASB 127 ‘Consolidated and Separate Financial Statements’ provides

that the portion of NCI must be shown as a separate item in the Equity portion of

the consolidated balance sheet apart from the parent’s equity. The entire

procedure for reporting of NCI involves diligent consideration of the finer details

of consolidation accounting. To begin with the preliminary step is the

determination of the percentage of the parent’s stake in the subsidiary which

ultimately determines the portion of NCI. For instance, if Company A acquired

6000 shares in Company B (total stock consists of 10000 shares), then by virtue

of its 60% holding in B it acquired a controlling interest in entity B. Thus, the

remaining 40% stake comes within the ambit of NCI as it represents minority

claim in the total pool. It is held that more than 50% stake accords an entity the

status of a parent. However, there can be circumstances when an entity may

decide to subscribe the entire share capital of another entity which gives rise to a

100% subsidiary. In that case, no question of existence of NCI arises.

(Macabacus, LLC., 2019)

The standard provides for consolidated method of accounting for reporting of

majority stake, i.e. controlling interest in the company. The detailed procedure

for reporting of NCI can be understood as follows:

Business combinations involves the transfer of assets and liabilities against a

consideration which is compared with the net assets acquired in order to find the

transactional results. This process gives rise to either goodwill (when net assets

acquired are less than the consideration paid) or gain (when net assets acquired

exceeds the consideration paid). It is calculated as follows:

Calculation of goodwill/bargain purchase

Particulars

Amoun

t

Fair Value of purchase consideration xxx

Add: Non-controlling interest (fair value) xxx

Less: Proportionate share capital of subsidiary xxx

Less: Premium on shares of the subsidiary xxx

Non-controlling interest represents the interest of those shareholders whose

claim in the total equity of a subsidiary is quite nominal as compared to the

interests of the parent company. In other words, the portion of equity not owned

by the parent in the subsidiary is called non-controlling interest. (CFI Education

Inc., 2019)These investors can be considered as minority investors as their

stakes in the company are marginal, i.e. normally less than 50%. While

preparation of consolidated financial statements for the entire group due

consideration is taken for combining the various items of the financial statements

of the parent and the subsidiary. Basically, the various assets and liabilities are

added on a line by line basis with certain adjustments being undertaken for

elimination of intragroup transactions and reporting the financial results.

However, the investment made in the subsidiary by the parent entity represented

as an asset in the books of the parent is set off against the equity and reserves of

the subsidiary.

As mentioned above, the non-controlling interest (NCI) which represents the

interest of the minority shareholders is quite a significant item in this type of

reporting. AASB 127 ‘Consolidated and Separate Financial Statements’ provides

that the portion of NCI must be shown as a separate item in the Equity portion of

the consolidated balance sheet apart from the parent’s equity. The entire

procedure for reporting of NCI involves diligent consideration of the finer details

of consolidation accounting. To begin with the preliminary step is the

determination of the percentage of the parent’s stake in the subsidiary which

ultimately determines the portion of NCI. For instance, if Company A acquired

6000 shares in Company B (total stock consists of 10000 shares), then by virtue

of its 60% holding in B it acquired a controlling interest in entity B. Thus, the

remaining 40% stake comes within the ambit of NCI as it represents minority

claim in the total pool. It is held that more than 50% stake accords an entity the

status of a parent. However, there can be circumstances when an entity may

decide to subscribe the entire share capital of another entity which gives rise to a

100% subsidiary. In that case, no question of existence of NCI arises.

(Macabacus, LLC., 2019)

The standard provides for consolidated method of accounting for reporting of

majority stake, i.e. controlling interest in the company. The detailed procedure

for reporting of NCI can be understood as follows:

Business combinations involves the transfer of assets and liabilities against a

consideration which is compared with the net assets acquired in order to find the

transactional results. This process gives rise to either goodwill (when net assets

acquired are less than the consideration paid) or gain (when net assets acquired

exceeds the consideration paid). It is calculated as follows:

Calculation of goodwill/bargain purchase

Particulars

Amoun

t

Fair Value of purchase consideration xxx

Add: Non-controlling interest (fair value) xxx

Less: Proportionate share capital of subsidiary xxx

Less: Premium on shares of the subsidiary xxx

Less: Fair value adjustments to the assets xxx

Less: Pre-acquisition reserves of the subsidiary xxx

xxx

In the above calculations fair value adjustment has been made to the assets of

the subsidiary in order to eliminate the impact of historical accounting model

followed by the subsidiary. Proceeding on parallel lines adjustment has to be

made to arrive at the fair value of non-controlling interest. In this regard, the net

assets of the subsidiary will have to be calculated accompanied by the respective

fair value adjustment. The fair value of NCI is the product of the resultant figure

of subsidiary’s net assets (adjusted at fair value) and the percentage stake of

shareholders comprising the NCI.

For the purpose of attribution of profit, the profit or loss of the subsidiary will

have to be calculated relevant for the period after acquisition. The calculated

share of profit is attributed to NCI in the proportion of percentage shareholding of

NCI.

Calculation of profit

attributable to NCI

Proportionate Shareholding

of NCI(a) Net profit of subsidiary(b)

Profit

Attributable(axe)

Xxx Xxx Xxx

In the consolidated financial statement for reporting profit or loss, this amount of

profit attributable to NCI is disclosed as a non-operating item with a separate

head- “net income attributable to the minority interest”.

Further, as per the principles enshrined in AASB 127 ‘Consolidated and Separate

Financial statements’ the portion of outstanding cumulative preference shares

held by NCI in the subsidiary which have been classified as equity is also

considered, thereby, following that the parent’s share is computed after

deducting the dividend on those shares irrespective of the dividend being

declared or not. (Deloitte Development LLC. , 2018)In fact, a change in the

parent’s ownership pattern in the subsidiary which does not affect the proportion

of controlling interest is regarded as a transaction between owners. However,

both the controlling and non-controlling interests are adjusted to accommodate

the changes. The difference between the adjustment made to NCI and the fair

value of consideration paid or received is attributed to the parent entity along

with simultaneous recognition in equity.

Perhaps, the most peculiar phenomenon associated with reporting of NCI is the

particular distinction made between controlling interest and NCI. While

controlling interest is accorded priority as a part of an entity’s equity, the

proportion of NCI is viewed as a debt for calculating the magnitude of market

capitalization of the entity. Thus, the portion of NCI is quite significant for

analysing the consolidated financial statements.

Less: Pre-acquisition reserves of the subsidiary xxx

xxx

In the above calculations fair value adjustment has been made to the assets of

the subsidiary in order to eliminate the impact of historical accounting model

followed by the subsidiary. Proceeding on parallel lines adjustment has to be

made to arrive at the fair value of non-controlling interest. In this regard, the net

assets of the subsidiary will have to be calculated accompanied by the respective

fair value adjustment. The fair value of NCI is the product of the resultant figure

of subsidiary’s net assets (adjusted at fair value) and the percentage stake of

shareholders comprising the NCI.

For the purpose of attribution of profit, the profit or loss of the subsidiary will

have to be calculated relevant for the period after acquisition. The calculated

share of profit is attributed to NCI in the proportion of percentage shareholding of

NCI.

Calculation of profit

attributable to NCI

Proportionate Shareholding

of NCI(a) Net profit of subsidiary(b)

Profit

Attributable(axe)

Xxx Xxx Xxx

In the consolidated financial statement for reporting profit or loss, this amount of

profit attributable to NCI is disclosed as a non-operating item with a separate

head- “net income attributable to the minority interest”.

Further, as per the principles enshrined in AASB 127 ‘Consolidated and Separate

Financial statements’ the portion of outstanding cumulative preference shares

held by NCI in the subsidiary which have been classified as equity is also

considered, thereby, following that the parent’s share is computed after

deducting the dividend on those shares irrespective of the dividend being

declared or not. (Deloitte Development LLC. , 2018)In fact, a change in the

parent’s ownership pattern in the subsidiary which does not affect the proportion

of controlling interest is regarded as a transaction between owners. However,

both the controlling and non-controlling interests are adjusted to accommodate

the changes. The difference between the adjustment made to NCI and the fair

value of consideration paid or received is attributed to the parent entity along

with simultaneous recognition in equity.

Perhaps, the most peculiar phenomenon associated with reporting of NCI is the

particular distinction made between controlling interest and NCI. While

controlling interest is accorded priority as a part of an entity’s equity, the

proportion of NCI is viewed as a debt for calculating the magnitude of market

capitalization of the entity. Thus, the portion of NCI is quite significant for

analysing the consolidated financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it is analysed that the various methods of accounting were

introduced and how to do that particular accounting relevant Australian

Accounting Standards were introduced, this relevant accounting standard

provides a guidance and framework to the company .This is also helpful in

reporting purpose so that no part is left unreported in the books of accounts of

the company. The above analysis also shows the computation for consolidation

accounting, Non-controlling interest and intra group transactions.

References

Commonwealth of Australia 2015, 2015. Business Combinations. [Online]

Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf

[Accessed 29 May 2018].

CFI Education Inc., 2019. What is a Non-Controlling Interest?. [Online]

Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/non-

controlling-interest/

[Accessed 29 May 2019].

Deloitte Development LLC. , 2018. A Roadmap to Accounting for Noncontrolling

Interests. [Online]

Available at:

https://www2.deloitte.com/content/dam/Deloitte/us/Documents/audit/ASC/

Roadmaps/us-aers-roadmap-noncontrolling-interest-2018.pdf

[Accessed 29 May 2019].

jade.io, 2015. Consolidated Financial Statements. [Online]

Available at: https://jade.io/j/?a=outline&id=503698

[Accessed 29 May 2019].

Macabacus, LLC., 2019. Noncontrolling (Minority) Interest. [Online]

Available at: http://macabacus.com/accounting/noncontrolling-interest

[Accessed 29 May 2019].

From the above report it is analysed that the various methods of accounting were

introduced and how to do that particular accounting relevant Australian

Accounting Standards were introduced, this relevant accounting standard

provides a guidance and framework to the company .This is also helpful in

reporting purpose so that no part is left unreported in the books of accounts of

the company. The above analysis also shows the computation for consolidation

accounting, Non-controlling interest and intra group transactions.

References

Commonwealth of Australia 2015, 2015. Business Combinations. [Online]

Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf

[Accessed 29 May 2018].

CFI Education Inc., 2019. What is a Non-Controlling Interest?. [Online]

Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/non-

controlling-interest/

[Accessed 29 May 2019].

Deloitte Development LLC. , 2018. A Roadmap to Accounting for Noncontrolling

Interests. [Online]

Available at:

https://www2.deloitte.com/content/dam/Deloitte/us/Documents/audit/ASC/

Roadmaps/us-aers-roadmap-noncontrolling-interest-2018.pdf

[Accessed 29 May 2019].

jade.io, 2015. Consolidated Financial Statements. [Online]

Available at: https://jade.io/j/?a=outline&id=503698

[Accessed 29 May 2019].

Macabacus, LLC., 2019. Noncontrolling (Minority) Interest. [Online]

Available at: http://macabacus.com/accounting/noncontrolling-interest

[Accessed 29 May 2019].

PricewaterhouseCoopers, 2018. Consolidation. [Online]

Available at: https://www.pwc.com.au/assurance/ifrs/assets/consolidation-are-

you-one-big-happy-family.pdf

[Accessed 29 May 2019].

Available at: https://www.pwc.com.au/assurance/ifrs/assets/consolidation-are-

you-one-big-happy-family.pdf

[Accessed 29 May 2019].

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.