FIN80005 Corporate Financial Management: Tastegood Expansion Report

VerifiedAdded on 2023/06/03

|12

|2580

|413

Report

AI Summary

This report assesses Tastegood Limited's expansion proposal involving selling goods under Cheap & Good's private label. It evaluates the project's profitability using Net Present Value (NPV) analysis, considering factors like machinery costs, depreciation, revenue growth, variable costs, and tax implications. Sensitivity analysis is conducted to understand the impact of revenue fluctuations on the project's NPV. Furthermore, the report examines abnormal returns based on the semi-strong form of the market hypothesis, analyzing stock and market returns around the announcement date to determine market efficiency and potential mispricing opportunities. The analysis uses time series and regression to calculate Beta and Weighted Average Cost of Capital (WACC) to determine appropriate discounting factors. Appendices provide detailed calculations and supporting data for the analysis.

EXAPANSION OF BUSINESS & SALE OF GOODS UNDER PRIVATE

LABEL TO CHEAP & GOOD

1

LABEL TO CHEAP & GOOD

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL ASSIGNMENT-INDIVIDUAL

EXECUTIVE SUMMARY

The report details out expansion proposal of Tastegood by selling under the private label of Cheap&

Goods. The report inks out the probable impact of such expansion on other business of the

company. The report further presses on sensitivity analysis form Year 6 and the probable impact of

such announcement on the market value of the shares of the company and any excess earning

earned by the company on account of same in a semi-strong Hypothesis market.

2

EXECUTIVE SUMMARY

The report details out expansion proposal of Tastegood by selling under the private label of Cheap&

Goods. The report inks out the probable impact of such expansion on other business of the

company. The report further presses on sensitivity analysis form Year 6 and the probable impact of

such announcement on the market value of the shares of the company and any excess earning

earned by the company on account of same in a semi-strong Hypothesis market.

2

Table of Content

Contents

EXECUTIVE SUMMARY...........................................................................................................................2

Table of Content....................................................................................................................................3

Purpose of Report.................................................................................................................................4

Net Present Value..................................................................................................................................4

Assumptions involved under the computation..................................................................................4

NPV Analysis......................................................................................................................................4

Sensitivity Analysis.................................................................................................................................5

Assumption........................................................................................................................................5

Abnormal Returns: Semi Strong Form of Market Hypothesis................................................................5

Appendix-1............................................................................................................................................7

Appendix-2..........................................................................................................................................11

3

Contents

EXECUTIVE SUMMARY...........................................................................................................................2

Table of Content....................................................................................................................................3

Purpose of Report.................................................................................................................................4

Net Present Value..................................................................................................................................4

Assumptions involved under the computation..................................................................................4

NPV Analysis......................................................................................................................................4

Sensitivity Analysis.................................................................................................................................5

Assumption........................................................................................................................................5

Abnormal Returns: Semi Strong Form of Market Hypothesis................................................................5

Appendix-1............................................................................................................................................7

Appendix-2..........................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purpose of Report

Tastegood Limited, a public entity, listed on Australian Stock Exchange is contemplating to expand its

operations by selling finished good in a private label to Cheap & Good. Further, under the said terms

the supply shall be made for a period of 10 years. On the basis of above, the Chief Executive Officer

of the company wishes to understand the profitability of the said project. Further, the report deals

with sensitivity analysis of the said project deals with the abnormal returns earned by the company

on account of announcement of said project. The breakup of the content of the report:

(a) Computation of Net Present Value of the project;

(b) Sensitivity Analysis of the project;

(c) Abnormal Returns: Semi Strong Form of Market Hypothesis.

Net Present Value

Under the said tool of Capital Budgeting, the present value of the cash flows of the project by a

particular discount rate usually Weighted Average Cost of Capital of the company is reduced by the

initial outlay of the project. If the computation is positive, then the project is viable otherwise not.

Further, the higher the value, the more lucrative the project is.

Assumptions involved under the computation

(a) The cash flow assumed holds good;

(b) The cost incurred for installation and shipping of machinery has been considered a cost of the

asset in terms of AASB and accordingly the same has been depreciated using Written down

value method over the period of 10 years;

(c) Yield of debentures has not been considered for analysis as bond market value is not required

as debt to equity ratio has been stated in the question.

(d) The maturity period of bond has not been considered for analysis.

NPV Analysis

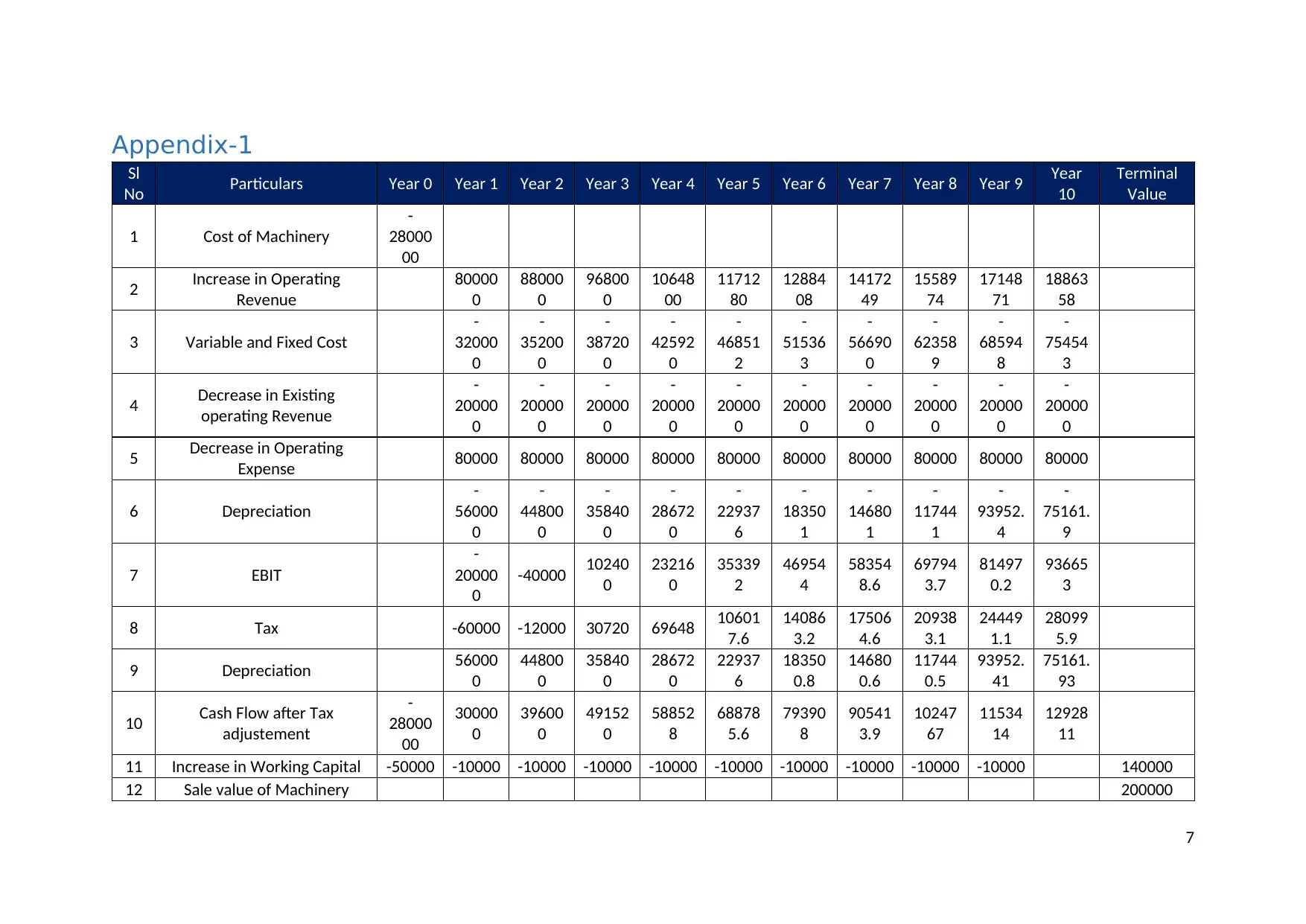

On perusal of the appendix 1, it shall be seen that the proposed project has a positive Net present

value which is significantly beneficial for the company and the company shall execute the same as t

it shall add value to the company. Further, it shall be pertinent to note that the said computation

has been derived in the following manner:

(a) Cost of Machinery has been considered by including shipping and installation cost;

(b) Machinery has been depreciated using declining balance method @20%;

(c) Revenue has been expected to increase @10%;

(d) Variable cost has been considered 40% of expenditure;

(e) Opportunity loss has been considered for computation of net present value;

(f) Tax has been deducted from Operating Cash flow @30%;

(g) There has been adjustment on account of changes in Working Capital on account of execution

of the proposed project ;

(h) Machine has been sold at the end of the period and tax impact on the same has been

considered. For detailed analysis refer Appendix 1;

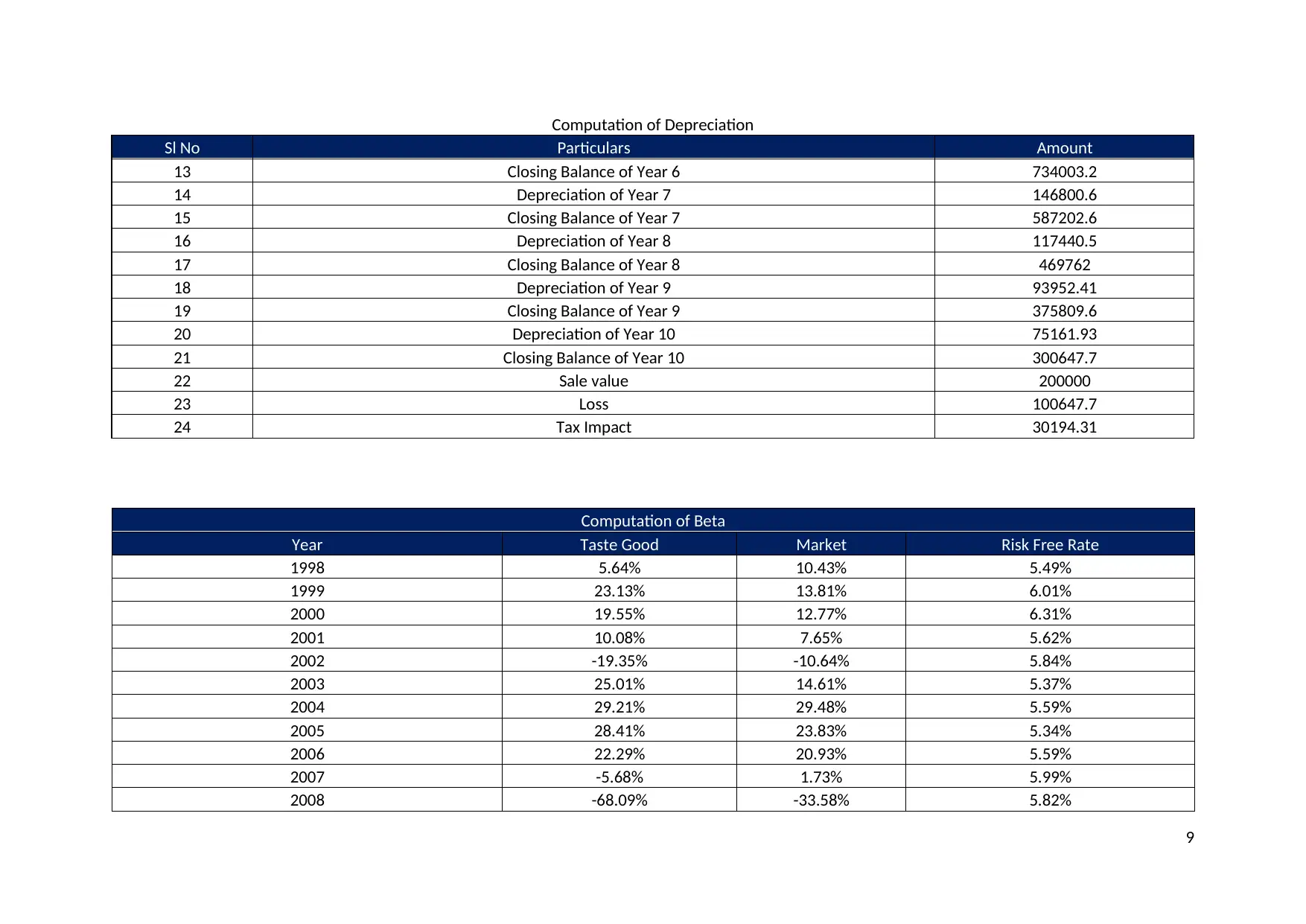

(i) Beta has been computed based on time series and regression analysis;

(j) The discounting factor has been taken at Weighted Average Cost of Capital of the company i.e.

11.54%.

4

Tastegood Limited, a public entity, listed on Australian Stock Exchange is contemplating to expand its

operations by selling finished good in a private label to Cheap & Good. Further, under the said terms

the supply shall be made for a period of 10 years. On the basis of above, the Chief Executive Officer

of the company wishes to understand the profitability of the said project. Further, the report deals

with sensitivity analysis of the said project deals with the abnormal returns earned by the company

on account of announcement of said project. The breakup of the content of the report:

(a) Computation of Net Present Value of the project;

(b) Sensitivity Analysis of the project;

(c) Abnormal Returns: Semi Strong Form of Market Hypothesis.

Net Present Value

Under the said tool of Capital Budgeting, the present value of the cash flows of the project by a

particular discount rate usually Weighted Average Cost of Capital of the company is reduced by the

initial outlay of the project. If the computation is positive, then the project is viable otherwise not.

Further, the higher the value, the more lucrative the project is.

Assumptions involved under the computation

(a) The cash flow assumed holds good;

(b) The cost incurred for installation and shipping of machinery has been considered a cost of the

asset in terms of AASB and accordingly the same has been depreciated using Written down

value method over the period of 10 years;

(c) Yield of debentures has not been considered for analysis as bond market value is not required

as debt to equity ratio has been stated in the question.

(d) The maturity period of bond has not been considered for analysis.

NPV Analysis

On perusal of the appendix 1, it shall be seen that the proposed project has a positive Net present

value which is significantly beneficial for the company and the company shall execute the same as t

it shall add value to the company. Further, it shall be pertinent to note that the said computation

has been derived in the following manner:

(a) Cost of Machinery has been considered by including shipping and installation cost;

(b) Machinery has been depreciated using declining balance method @20%;

(c) Revenue has been expected to increase @10%;

(d) Variable cost has been considered 40% of expenditure;

(e) Opportunity loss has been considered for computation of net present value;

(f) Tax has been deducted from Operating Cash flow @30%;

(g) There has been adjustment on account of changes in Working Capital on account of execution

of the proposed project ;

(h) Machine has been sold at the end of the period and tax impact on the same has been

considered. For detailed analysis refer Appendix 1;

(i) Beta has been computed based on time series and regression analysis;

(j) The discounting factor has been taken at Weighted Average Cost of Capital of the company i.e.

11.54%.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

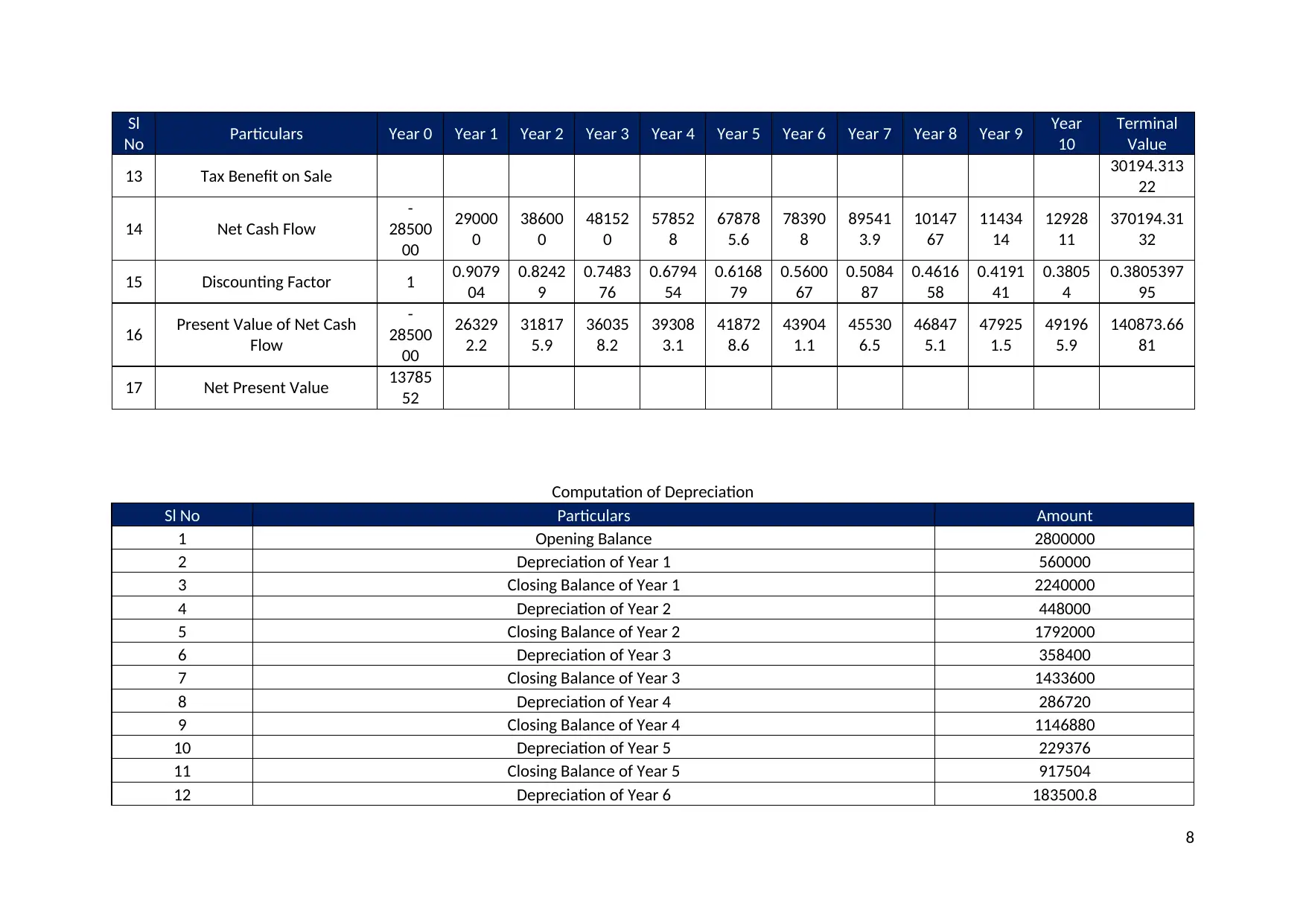

On basis of the above, net present value has been computed at $ 1,378,552.

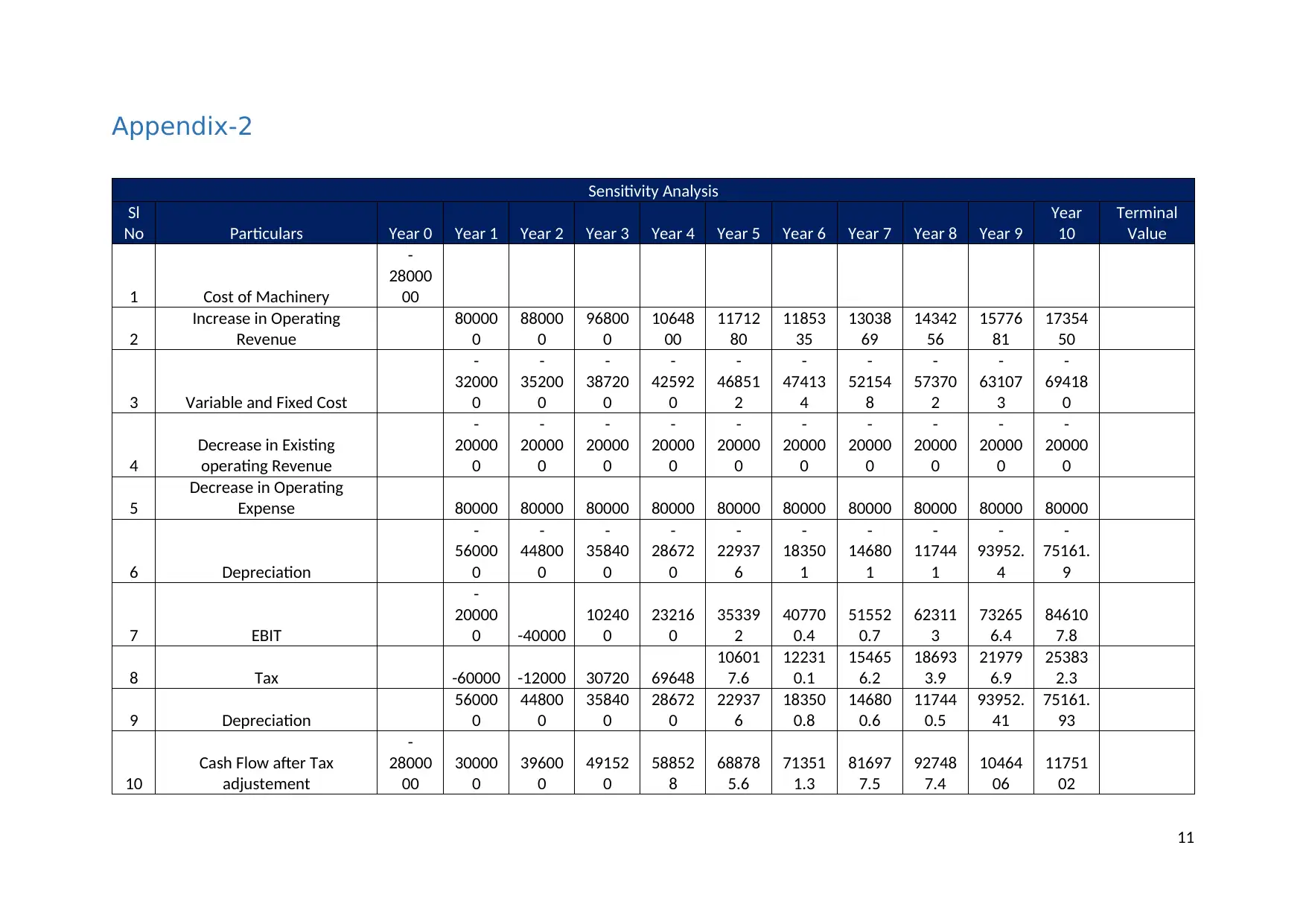

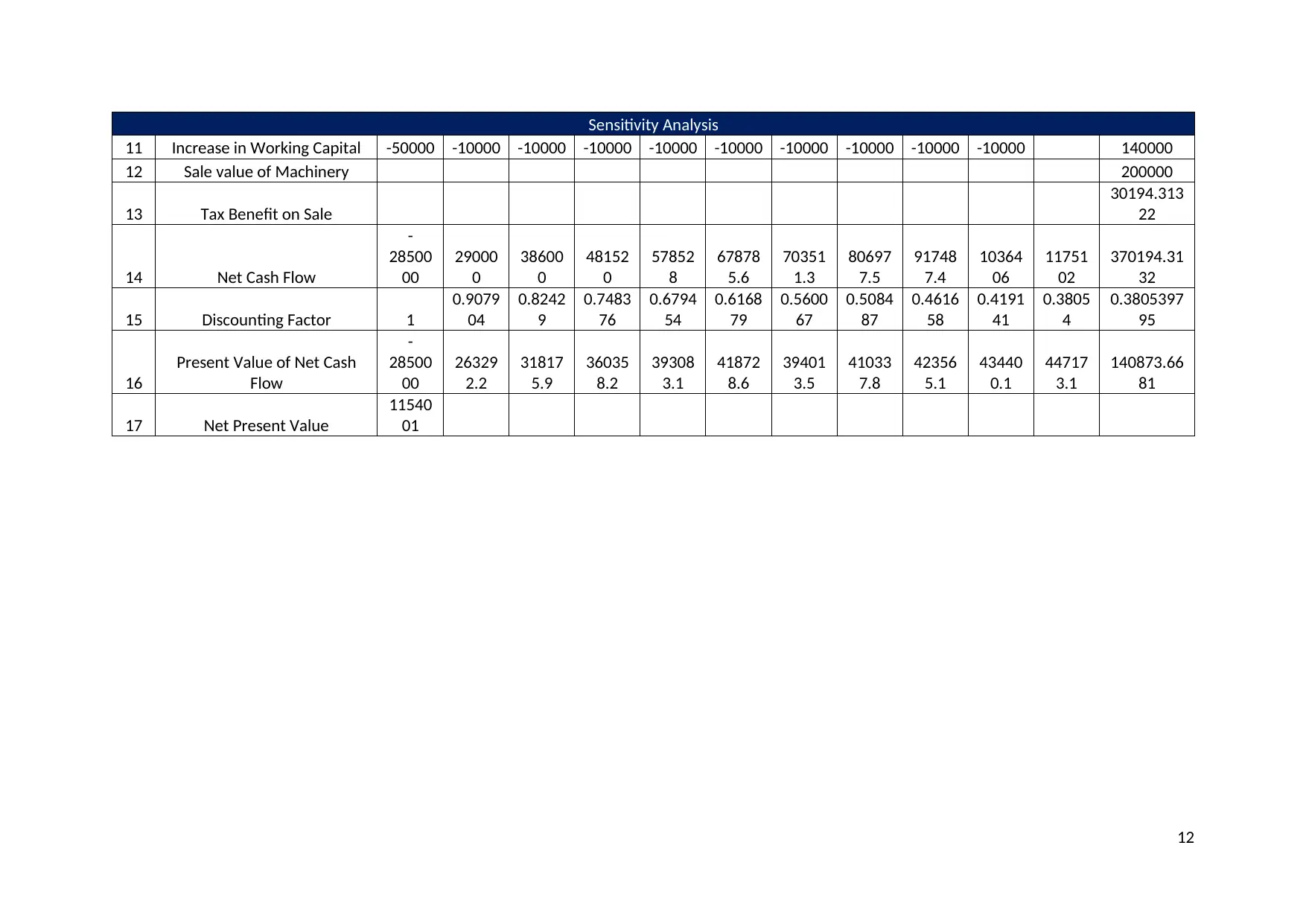

Sensitivity Analysis

Sensitivity Analysis of the project encompasses computation of projected cash flows based on

upward and downward revision and analysing the impact of the same on the net present value of

the project. In the concerned case, the projected revenue from the project has been revised

downward 40% by a probability of 30% and upward by 20% with a probability of 20% and the same

predicted with a probability of 40%,

The computation of the Net Present Value based on such sensitivity has been tabulated in Appendix

2. Further, the predicted cash flow from year 6 has been given here-in-under:

Probability Analysis

Particular Weight Net

773044.8 (40% downward) 30% 231913.4

1546089.6 (20% Upward) 20% 309217.9

1288408 50% 644204

Expected Cash flow (Year 6) 1185335

Further, the net present has been subject to the same analysis as stated above and has been subject

to same assumption as stated above. Accordingly, the Net Present Value is computed at $ 1154001

leading to fall in NPV by 17%.

Assumption

It shall be pertinent to note that the said computation has been based on a understanding that the

22 point stated by the CEO of Tastegood relates to a single sensitivity analysis.

Abnormal Returns: Semi Strong Form of Market

Hypothesis.

The third part of the report deals with computation of abnormal return. The term means return

earned in excess of Expected return. The expected return symbolise the return which shall be earned

by the company in terms of Capital Asset Pricing Model. The CAPM model is an additive model and is

based on risk return trade off considering systematic risk as the only risk.

Further, it shall be noted that the market efficiency has been considered semi strong implying that

all the price sensitivity information of the market has been rapidly factored in the available market

information and no superior gain shall be achieved by the investor by using fundamental or technical

analysis. Further, the security price reflects all market information at a particular period of time.

Based on the above, the analysis of abnormal returns has been reflected here-in-below:

Day Stock Return Market Return Risk-Free Beta Expected Return Abnormal Return

-5 0.30% 0.30% 0.01% 1.56 0.46% -0.16%

-4 0.45% 0.20% 0.01% 1.56 0.31% 0.14%

-3 -0.18% 0.01% 0.01% 1.56 0.01% -0.19%

-2 -0.60% -0.50% 0.01% 1.56 -0.78% 0.18%

-1 1.20% 0.20% 0.01% 1.56 0.31% 0.89%

0 2.50% 0.30% 0.01% 1.56 0.46% 2.04%

5

Sensitivity Analysis

Sensitivity Analysis of the project encompasses computation of projected cash flows based on

upward and downward revision and analysing the impact of the same on the net present value of

the project. In the concerned case, the projected revenue from the project has been revised

downward 40% by a probability of 30% and upward by 20% with a probability of 20% and the same

predicted with a probability of 40%,

The computation of the Net Present Value based on such sensitivity has been tabulated in Appendix

2. Further, the predicted cash flow from year 6 has been given here-in-under:

Probability Analysis

Particular Weight Net

773044.8 (40% downward) 30% 231913.4

1546089.6 (20% Upward) 20% 309217.9

1288408 50% 644204

Expected Cash flow (Year 6) 1185335

Further, the net present has been subject to the same analysis as stated above and has been subject

to same assumption as stated above. Accordingly, the Net Present Value is computed at $ 1154001

leading to fall in NPV by 17%.

Assumption

It shall be pertinent to note that the said computation has been based on a understanding that the

22 point stated by the CEO of Tastegood relates to a single sensitivity analysis.

Abnormal Returns: Semi Strong Form of Market

Hypothesis.

The third part of the report deals with computation of abnormal return. The term means return

earned in excess of Expected return. The expected return symbolise the return which shall be earned

by the company in terms of Capital Asset Pricing Model. The CAPM model is an additive model and is

based on risk return trade off considering systematic risk as the only risk.

Further, it shall be noted that the market efficiency has been considered semi strong implying that

all the price sensitivity information of the market has been rapidly factored in the available market

information and no superior gain shall be achieved by the investor by using fundamental or technical

analysis. Further, the security price reflects all market information at a particular period of time.

Based on the above, the analysis of abnormal returns has been reflected here-in-below:

Day Stock Return Market Return Risk-Free Beta Expected Return Abnormal Return

-5 0.30% 0.30% 0.01% 1.56 0.46% -0.16%

-4 0.45% 0.20% 0.01% 1.56 0.31% 0.14%

-3 -0.18% 0.01% 0.01% 1.56 0.01% -0.19%

-2 -0.60% -0.50% 0.01% 1.56 -0.78% 0.18%

-1 1.20% 0.20% 0.01% 1.56 0.31% 0.89%

0 2.50% 0.30% 0.01% 1.56 0.46% 2.04%

5

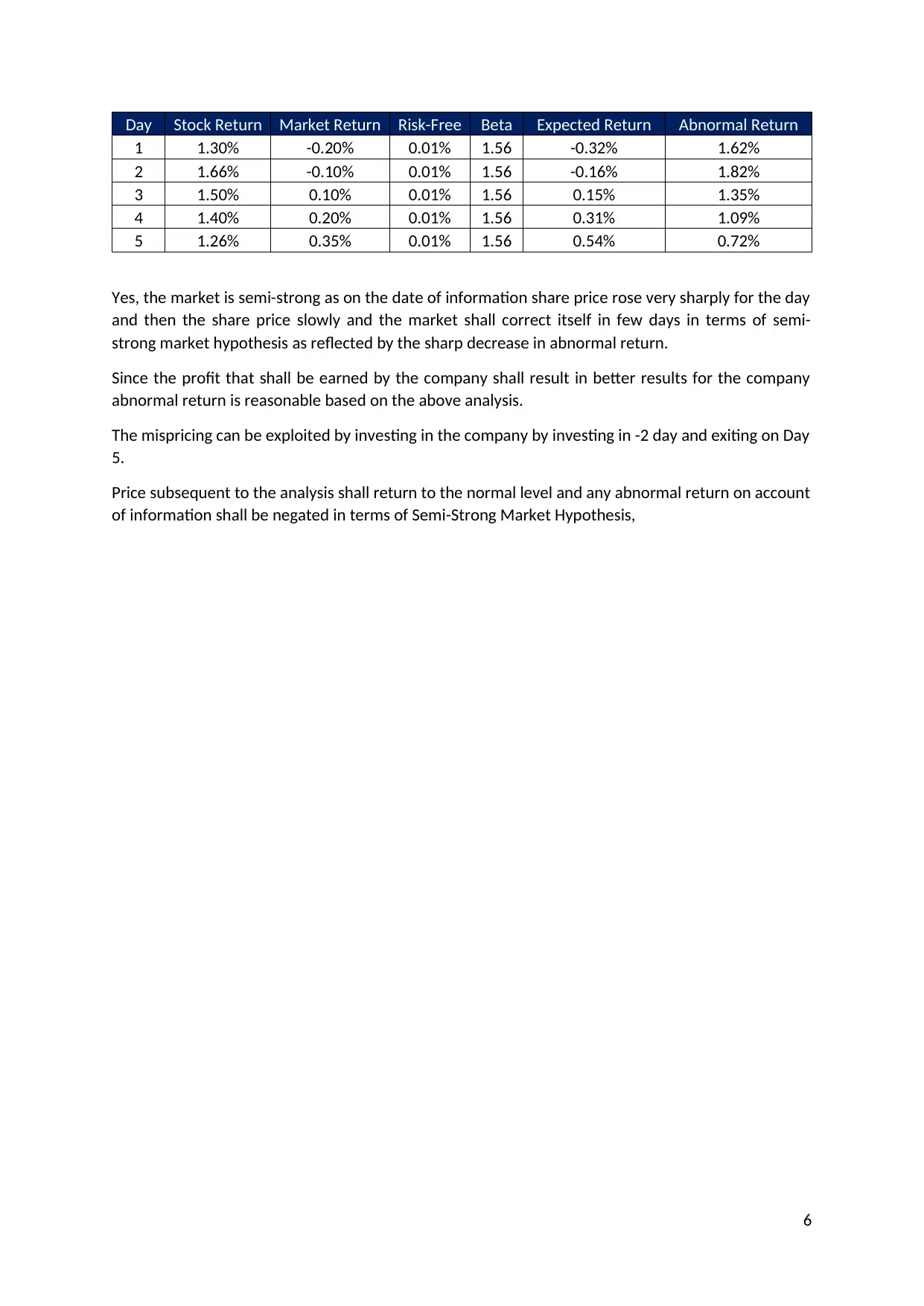

Day Stock Return Market Return Risk-Free Beta Expected Return Abnormal Return

1 1.30% -0.20% 0.01% 1.56 -0.32% 1.62%

2 1.66% -0.10% 0.01% 1.56 -0.16% 1.82%

3 1.50% 0.10% 0.01% 1.56 0.15% 1.35%

4 1.40% 0.20% 0.01% 1.56 0.31% 1.09%

5 1.26% 0.35% 0.01% 1.56 0.54% 0.72%

Yes, the market is semi-strong as on the date of information share price rose very sharply for the day

and then the share price slowly and the market shall correct itself in few days in terms of semi-

strong market hypothesis as reflected by the sharp decrease in abnormal return.

Since the profit that shall be earned by the company shall result in better results for the company

abnormal return is reasonable based on the above analysis.

The mispricing can be exploited by investing in the company by investing in -2 day and exiting on Day

5.

Price subsequent to the analysis shall return to the normal level and any abnormal return on account

of information shall be negated in terms of Semi-Strong Market Hypothesis,

6

1 1.30% -0.20% 0.01% 1.56 -0.32% 1.62%

2 1.66% -0.10% 0.01% 1.56 -0.16% 1.82%

3 1.50% 0.10% 0.01% 1.56 0.15% 1.35%

4 1.40% 0.20% 0.01% 1.56 0.31% 1.09%

5 1.26% 0.35% 0.01% 1.56 0.54% 0.72%

Yes, the market is semi-strong as on the date of information share price rose very sharply for the day

and then the share price slowly and the market shall correct itself in few days in terms of semi-

strong market hypothesis as reflected by the sharp decrease in abnormal return.

Since the profit that shall be earned by the company shall result in better results for the company

abnormal return is reasonable based on the above analysis.

The mispricing can be exploited by investing in the company by investing in -2 day and exiting on Day

5.

Price subsequent to the analysis shall return to the normal level and any abnormal return on account

of information shall be negated in terms of Semi-Strong Market Hypothesis,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appendix-1

Sl

No Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year

10

Terminal

Value

1 Cost of Machinery

-

28000

00

2 Increase in Operating

Revenue

80000

0

88000

0

96800

0

10648

00

11712

80

12884

08

14172

49

15589

74

17148

71

18863

58

3 Variable and Fixed Cost

-

32000

0

-

35200

0

-

38720

0

-

42592

0

-

46851

2

-

51536

3

-

56690

0

-

62358

9

-

68594

8

-

75454

3

4 Decrease in Existing

operating Revenue

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

5 Decrease in Operating

Expense 80000 80000 80000 80000 80000 80000 80000 80000 80000 80000

6 Depreciation

-

56000

0

-

44800

0

-

35840

0

-

28672

0

-

22937

6

-

18350

1

-

14680

1

-

11744

1

-

93952.

4

-

75161.

9

7 EBIT

-

20000

0

-40000 10240

0

23216

0

35339

2

46954

4

58354

8.6

69794

3.7

81497

0.2

93665

3

8 Tax -60000 -12000 30720 69648 10601

7.6

14086

3.2

17506

4.6

20938

3.1

24449

1.1

28099

5.9

9 Depreciation 56000

0

44800

0

35840

0

28672

0

22937

6

18350

0.8

14680

0.6

11744

0.5

93952.

41

75161.

93

10 Cash Flow after Tax

adjustement

-

28000

00

30000

0

39600

0

49152

0

58852

8

68878

5.6

79390

8

90541

3.9

10247

67

11534

14

12928

11

11 Increase in Working Capital -50000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 140000

12 Sale value of Machinery 200000

7

Sl

No Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year

10

Terminal

Value

1 Cost of Machinery

-

28000

00

2 Increase in Operating

Revenue

80000

0

88000

0

96800

0

10648

00

11712

80

12884

08

14172

49

15589

74

17148

71

18863

58

3 Variable and Fixed Cost

-

32000

0

-

35200

0

-

38720

0

-

42592

0

-

46851

2

-

51536

3

-

56690

0

-

62358

9

-

68594

8

-

75454

3

4 Decrease in Existing

operating Revenue

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

5 Decrease in Operating

Expense 80000 80000 80000 80000 80000 80000 80000 80000 80000 80000

6 Depreciation

-

56000

0

-

44800

0

-

35840

0

-

28672

0

-

22937

6

-

18350

1

-

14680

1

-

11744

1

-

93952.

4

-

75161.

9

7 EBIT

-

20000

0

-40000 10240

0

23216

0

35339

2

46954

4

58354

8.6

69794

3.7

81497

0.2

93665

3

8 Tax -60000 -12000 30720 69648 10601

7.6

14086

3.2

17506

4.6

20938

3.1

24449

1.1

28099

5.9

9 Depreciation 56000

0

44800

0

35840

0

28672

0

22937

6

18350

0.8

14680

0.6

11744

0.5

93952.

41

75161.

93

10 Cash Flow after Tax

adjustement

-

28000

00

30000

0

39600

0

49152

0

58852

8

68878

5.6

79390

8

90541

3.9

10247

67

11534

14

12928

11

11 Increase in Working Capital -50000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 140000

12 Sale value of Machinery 200000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sl

No Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year

10

Terminal

Value

13 Tax Benefit on Sale 30194.313

22

14 Net Cash Flow

-

28500

00

29000

0

38600

0

48152

0

57852

8

67878

5.6

78390

8

89541

3.9

10147

67

11434

14

12928

11

370194.31

32

15 Discounting Factor 1 0.9079

04

0.8242

9

0.7483

76

0.6794

54

0.6168

79

0.5600

67

0.5084

87

0.4616

58

0.4191

41

0.3805

4

0.3805397

95

16 Present Value of Net Cash

Flow

-

28500

00

26329

2.2

31817

5.9

36035

8.2

39308

3.1

41872

8.6

43904

1.1

45530

6.5

46847

5.1

47925

1.5

49196

5.9

140873.66

81

17 Net Present Value 13785

52

Computation of Depreciation

Sl No Particulars Amount

1 Opening Balance 2800000

2 Depreciation of Year 1 560000

3 Closing Balance of Year 1 2240000

4 Depreciation of Year 2 448000

5 Closing Balance of Year 2 1792000

6 Depreciation of Year 3 358400

7 Closing Balance of Year 3 1433600

8 Depreciation of Year 4 286720

9 Closing Balance of Year 4 1146880

10 Depreciation of Year 5 229376

11 Closing Balance of Year 5 917504

12 Depreciation of Year 6 183500.8

8

No Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year

10

Terminal

Value

13 Tax Benefit on Sale 30194.313

22

14 Net Cash Flow

-

28500

00

29000

0

38600

0

48152

0

57852

8

67878

5.6

78390

8

89541

3.9

10147

67

11434

14

12928

11

370194.31

32

15 Discounting Factor 1 0.9079

04

0.8242

9

0.7483

76

0.6794

54

0.6168

79

0.5600

67

0.5084

87

0.4616

58

0.4191

41

0.3805

4

0.3805397

95

16 Present Value of Net Cash

Flow

-

28500

00

26329

2.2

31817

5.9

36035

8.2

39308

3.1

41872

8.6

43904

1.1

45530

6.5

46847

5.1

47925

1.5

49196

5.9

140873.66

81

17 Net Present Value 13785

52

Computation of Depreciation

Sl No Particulars Amount

1 Opening Balance 2800000

2 Depreciation of Year 1 560000

3 Closing Balance of Year 1 2240000

4 Depreciation of Year 2 448000

5 Closing Balance of Year 2 1792000

6 Depreciation of Year 3 358400

7 Closing Balance of Year 3 1433600

8 Depreciation of Year 4 286720

9 Closing Balance of Year 4 1146880

10 Depreciation of Year 5 229376

11 Closing Balance of Year 5 917504

12 Depreciation of Year 6 183500.8

8

Computation of Depreciation

Sl No Particulars Amount

13 Closing Balance of Year 6 734003.2

14 Depreciation of Year 7 146800.6

15 Closing Balance of Year 7 587202.6

16 Depreciation of Year 8 117440.5

17 Closing Balance of Year 8 469762

18 Depreciation of Year 9 93952.41

19 Closing Balance of Year 9 375809.6

20 Depreciation of Year 10 75161.93

21 Closing Balance of Year 10 300647.7

22 Sale value 200000

23 Loss 100647.7

24 Tax Impact 30194.31

Computation of Beta

Year Taste Good Market Risk Free Rate

1998 5.64% 10.43% 5.49%

1999 23.13% 13.81% 6.01%

2000 19.55% 12.77% 6.31%

2001 10.08% 7.65% 5.62%

2002 -19.35% -10.64% 5.84%

2003 25.01% 14.61% 5.37%

2004 29.21% 29.48% 5.59%

2005 28.41% 23.83% 5.34%

2006 22.29% 20.93% 5.59%

2007 -5.68% 1.73% 5.99%

2008 -68.09% -33.58% 5.82%

9

Sl No Particulars Amount

13 Closing Balance of Year 6 734003.2

14 Depreciation of Year 7 146800.6

15 Closing Balance of Year 7 587202.6

16 Depreciation of Year 8 117440.5

17 Closing Balance of Year 8 469762

18 Depreciation of Year 9 93952.41

19 Closing Balance of Year 9 375809.6

20 Depreciation of Year 10 75161.93

21 Closing Balance of Year 10 300647.7

22 Sale value 200000

23 Loss 100647.7

24 Tax Impact 30194.31

Computation of Beta

Year Taste Good Market Risk Free Rate

1998 5.64% 10.43% 5.49%

1999 23.13% 13.81% 6.01%

2000 19.55% 12.77% 6.31%

2001 10.08% 7.65% 5.62%

2002 -19.35% -10.64% 5.84%

2003 25.01% 14.61% 5.37%

2004 29.21% 29.48% 5.59%

2005 28.41% 23.83% 5.34%

2006 22.29% 20.93% 5.59%

2007 -5.68% 1.73% 5.99%

2008 -68.09% -33.58% 5.82%

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Computation of Beta

2009 48.21% 33.84% 5.04%

2010 12.39% 8.03% 5.37%

2011 -6.54% -6.43% 4.88%

2012 15.28% 18.56% 3.38%

2013 -1.12% 10.38% 3.70%

2014 17.98% 11.67% 3.66%

2015 -15.44% -6.43% 2.71%

2016 26.23% 16.29% 2.34%

2017 0.20% 5.70% 2.72%

Mean 8.37% 9.13% 4.84%

Standard Deviation 24.58% 15.16% 1.26%

Covariance 3.59%

Beta 1.56

Computation of Weighted Average Cost of Capital

Sl No Particulars Rate Tax Net Rate Weight Net

1 Debentures 12% 30% 8.4% 0.8 6.7%

2 Equity 11.54% 11.54% 1 11.5%

1.80 18.3%

3 WACC 10.14%

Computation of cost of Equity

Sl No Particulars Rate

1 Risk Free rate 4.84%

2 Risk Premium 4.29%

3 Beta 1.56

4 Cost of Equity 11.54%

10

2009 48.21% 33.84% 5.04%

2010 12.39% 8.03% 5.37%

2011 -6.54% -6.43% 4.88%

2012 15.28% 18.56% 3.38%

2013 -1.12% 10.38% 3.70%

2014 17.98% 11.67% 3.66%

2015 -15.44% -6.43% 2.71%

2016 26.23% 16.29% 2.34%

2017 0.20% 5.70% 2.72%

Mean 8.37% 9.13% 4.84%

Standard Deviation 24.58% 15.16% 1.26%

Covariance 3.59%

Beta 1.56

Computation of Weighted Average Cost of Capital

Sl No Particulars Rate Tax Net Rate Weight Net

1 Debentures 12% 30% 8.4% 0.8 6.7%

2 Equity 11.54% 11.54% 1 11.5%

1.80 18.3%

3 WACC 10.14%

Computation of cost of Equity

Sl No Particulars Rate

1 Risk Free rate 4.84%

2 Risk Premium 4.29%

3 Beta 1.56

4 Cost of Equity 11.54%

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix-2

Sensitivity Analysis

Sl

No Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9

Year

10

Terminal

Value

1 Cost of Machinery

-

28000

00

2

Increase in Operating

Revenue

80000

0

88000

0

96800

0

10648

00

11712

80

11853

35

13038

69

14342

56

15776

81

17354

50

3 Variable and Fixed Cost

-

32000

0

-

35200

0

-

38720

0

-

42592

0

-

46851

2

-

47413

4

-

52154

8

-

57370

2

-

63107

3

-

69418

0

4

Decrease in Existing

operating Revenue

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

5

Decrease in Operating

Expense 80000 80000 80000 80000 80000 80000 80000 80000 80000 80000

6 Depreciation

-

56000

0

-

44800

0

-

35840

0

-

28672

0

-

22937

6

-

18350

1

-

14680

1

-

11744

1

-

93952.

4

-

75161.

9

7 EBIT

-

20000

0 -40000

10240

0

23216

0

35339

2

40770

0.4

51552

0.7

62311

3

73265

6.4

84610

7.8

8 Tax -60000 -12000 30720 69648

10601

7.6

12231

0.1

15465

6.2

18693

3.9

21979

6.9

25383

2.3

9 Depreciation

56000

0

44800

0

35840

0

28672

0

22937

6

18350

0.8

14680

0.6

11744

0.5

93952.

41

75161.

93

10

Cash Flow after Tax

adjustement

-

28000

00

30000

0

39600

0

49152

0

58852

8

68878

5.6

71351

1.3

81697

7.5

92748

7.4

10464

06

11751

02

11

Sensitivity Analysis

Sl

No Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9

Year

10

Terminal

Value

1 Cost of Machinery

-

28000

00

2

Increase in Operating

Revenue

80000

0

88000

0

96800

0

10648

00

11712

80

11853

35

13038

69

14342

56

15776

81

17354

50

3 Variable and Fixed Cost

-

32000

0

-

35200

0

-

38720

0

-

42592

0

-

46851

2

-

47413

4

-

52154

8

-

57370

2

-

63107

3

-

69418

0

4

Decrease in Existing

operating Revenue

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

-

20000

0

5

Decrease in Operating

Expense 80000 80000 80000 80000 80000 80000 80000 80000 80000 80000

6 Depreciation

-

56000

0

-

44800

0

-

35840

0

-

28672

0

-

22937

6

-

18350

1

-

14680

1

-

11744

1

-

93952.

4

-

75161.

9

7 EBIT

-

20000

0 -40000

10240

0

23216

0

35339

2

40770

0.4

51552

0.7

62311

3

73265

6.4

84610

7.8

8 Tax -60000 -12000 30720 69648

10601

7.6

12231

0.1

15465

6.2

18693

3.9

21979

6.9

25383

2.3

9 Depreciation

56000

0

44800

0

35840

0

28672

0

22937

6

18350

0.8

14680

0.6

11744

0.5

93952.

41

75161.

93

10

Cash Flow after Tax

adjustement

-

28000

00

30000

0

39600

0

49152

0

58852

8

68878

5.6

71351

1.3

81697

7.5

92748

7.4

10464

06

11751

02

11

Sensitivity Analysis

11 Increase in Working Capital -50000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 140000

12 Sale value of Machinery 200000

13 Tax Benefit on Sale

30194.313

22

14 Net Cash Flow

-

28500

00

29000

0

38600

0

48152

0

57852

8

67878

5.6

70351

1.3

80697

7.5

91748

7.4

10364

06

11751

02

370194.31

32

15 Discounting Factor 1

0.9079

04

0.8242

9

0.7483

76

0.6794

54

0.6168

79

0.5600

67

0.5084

87

0.4616

58

0.4191

41

0.3805

4

0.3805397

95

16

Present Value of Net Cash

Flow

-

28500

00

26329

2.2

31817

5.9

36035

8.2

39308

3.1

41872

8.6

39401

3.5

41033

7.8

42356

5.1

43440

0.1

44717

3.1

140873.66

81

17 Net Present Value

11540

01

12

11 Increase in Working Capital -50000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 -10000 140000

12 Sale value of Machinery 200000

13 Tax Benefit on Sale

30194.313

22

14 Net Cash Flow

-

28500

00

29000

0

38600

0

48152

0

57852

8

67878

5.6

70351

1.3

80697

7.5

91748

7.4

10364

06

11751

02

370194.31

32

15 Discounting Factor 1

0.9079

04

0.8242

9

0.7483

76

0.6794

54

0.6168

79

0.5600

67

0.5084

87

0.4616

58

0.4191

41

0.3805

4

0.3805397

95

16

Present Value of Net Cash

Flow

-

28500

00

26329

2.2

31817

5.9

36035

8.2

39308

3.1

41872

8.6

39401

3.5

41033

7.8

42356

5.1

43440

0.1

44717

3.1

140873.66

81

17 Net Present Value

11540

01

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.