Adam & Co.: An Analysis of the Expenditure Cycle Systems

VerifiedAdded on 2022/10/15

|14

|2896

|320

Report

AI Summary

This report analyzes the expenditure cycle of Adam & Co., a Perth-based industrial supply wholesaler, focusing on its purchase, cash disbursement, and payroll systems. It identifies weaknesses in the current procedures and suggests improvements to strengthen internal controls. The report examines the existing purchasing system, including inventory management and order placement, and highlights areas for optimization such as establishing minimum, maximum, and reordering levels. The cash disbursement system is evaluated for its efficiency in managing payments to vendors, and the payroll system is assessed for its accuracy and security. The report also discusses the importance of job ticket systems and the separation of duties to prevent fraud and ensure accurate financial records. The analysis is based on expert opinions and findings, with recommendations for enhanced inventory control, authorization of payments, and streamlining payroll processes.

1

Running Head: REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Case Study

Expenditure Cycle of Adam and Company

Student’s Name:

ID:

Module:

Instructor:

Date of Submission:

Number of Words:

Running Head: REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Case Study

Expenditure Cycle of Adam and Company

Student’s Name:

ID:

Module:

Instructor:

Date of Submission:

Number of Words:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

EXECUTIVE SUMMARY

Adam and Co is a Perth based industrial supply wholesaler. The managing director of the firm is

concerned about the effectiveness of the current business cycle procedure of the firm, where do

the weaknesses of the system lie, so that necessary actions can be taken to make the internal

control system robust and work better. This report comprises of the present state of efficiency in

the systems, namely cash disbursement system, purchase system, and payroll system of the firm,

discussion about their weaknesses and some corrective actions necessary to make the internal

control system robust. The report is based on review of findings, comments, opinions of subject

experts, and the same has been duly recognized by insertion of references in text, and a full list

of works cited at the end.

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

EXECUTIVE SUMMARY

Adam and Co is a Perth based industrial supply wholesaler. The managing director of the firm is

concerned about the effectiveness of the current business cycle procedure of the firm, where do

the weaknesses of the system lie, so that necessary actions can be taken to make the internal

control system robust and work better. This report comprises of the present state of efficiency in

the systems, namely cash disbursement system, purchase system, and payroll system of the firm,

discussion about their weaknesses and some corrective actions necessary to make the internal

control system robust. The report is based on review of findings, comments, opinions of subject

experts, and the same has been duly recognized by insertion of references in text, and a full list

of works cited at the end.

3

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Introduction

Cash is the life-line of any business organization, hence deserves special attention respected with

its control in flows. The objectives of such control are to plug the leakage in its flow, prevent

unnecessary blockade of cash resulting in opportunity cost, and ensure availability of cash to

avoid cash-dry situations. Achieving these objectives is vital for any business, especially for

retail businesses having multiple cash flow directions, in order to ensure that the scarce resource

is optimally utilized in business. Purchase system involves making purchase requisition on the

basis of stock levels, placing purchase order to the best available vendor, receiving inventory,

and authorization and payment to suppliers. Payroll system comprises of maintaining employee

work records and disbursing salaries. This report is constructed upon the existing expenditure

cycle and the systems in the cycle of Adam and Co. a wholesaler of industrial supplies in Perth.

The audience of this report is the managing director of Adam and Co., on whose behest the

report is prepared by the undersigned to evaluate the expenditure cycle procedure of the firm.

Expenditure Cycle

Expenditure cycle of a business has the objective of converting cash into physical resources like

inventory, and human resources. Human and physical resources are obtained by the business

entries mostly in credit with time lagged cash disbursement. Out-flow of cash to purchase these

resources take place after the resources are availed of by the firms. This makes the expenditure

cycle a two-way traffic; in the first phase resources are procured and in the second phase cash is

disbursed, each phase having different sub-systems (Klamm and Weidenmier, 2004).

Purchasing System of Adam and Co.

The purchasing system of the firm is initiated by a purchase clerk on the basis of information in

his computer terminal about the minimum level and reordering level of respective inventory

items. On the basis of such information the clerk places purchase orders to selected vendors.

After the goods are received, the same is inspected and checked with purchase order for quantity,

quality, and price, and then put in shelves in the stores department. Liability to disburse cash is

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Introduction

Cash is the life-line of any business organization, hence deserves special attention respected with

its control in flows. The objectives of such control are to plug the leakage in its flow, prevent

unnecessary blockade of cash resulting in opportunity cost, and ensure availability of cash to

avoid cash-dry situations. Achieving these objectives is vital for any business, especially for

retail businesses having multiple cash flow directions, in order to ensure that the scarce resource

is optimally utilized in business. Purchase system involves making purchase requisition on the

basis of stock levels, placing purchase order to the best available vendor, receiving inventory,

and authorization and payment to suppliers. Payroll system comprises of maintaining employee

work records and disbursing salaries. This report is constructed upon the existing expenditure

cycle and the systems in the cycle of Adam and Co. a wholesaler of industrial supplies in Perth.

The audience of this report is the managing director of Adam and Co., on whose behest the

report is prepared by the undersigned to evaluate the expenditure cycle procedure of the firm.

Expenditure Cycle

Expenditure cycle of a business has the objective of converting cash into physical resources like

inventory, and human resources. Human and physical resources are obtained by the business

entries mostly in credit with time lagged cash disbursement. Out-flow of cash to purchase these

resources take place after the resources are availed of by the firms. This makes the expenditure

cycle a two-way traffic; in the first phase resources are procured and in the second phase cash is

disbursed, each phase having different sub-systems (Klamm and Weidenmier, 2004).

Purchasing System of Adam and Co.

The purchasing system of the firm is initiated by a purchase clerk on the basis of information in

his computer terminal about the minimum level and reordering level of respective inventory

items. On the basis of such information the clerk places purchase orders to selected vendors.

After the goods are received, the same is inspected and checked with purchase order for quantity,

quality, and price, and then put in shelves in the stores department. Liability to disburse cash is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

recognized when the goods are accepted by the purchasing department (Accounting Tools,

2018).

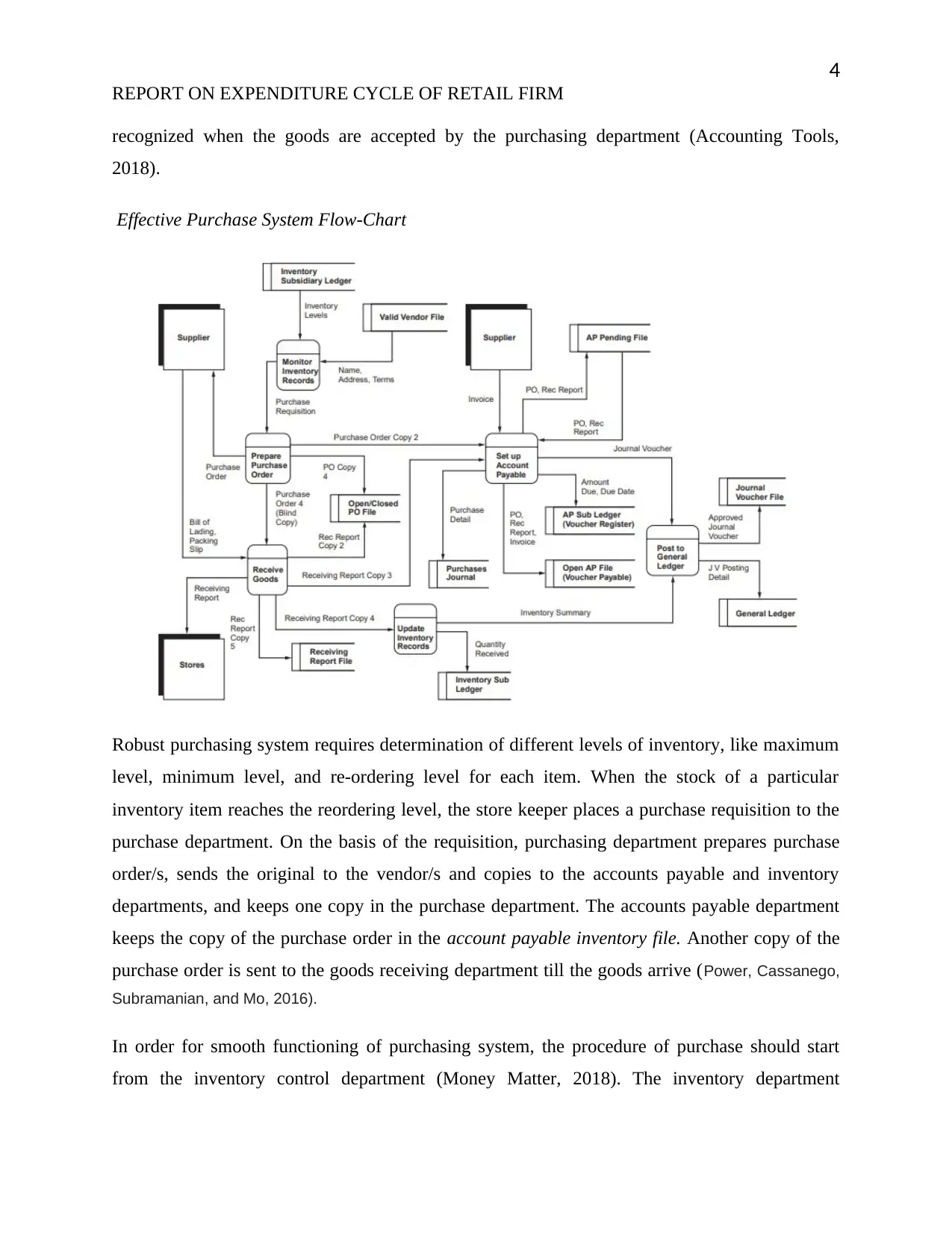

Effective Purchase System Flow-Chart

Robust purchasing system requires determination of different levels of inventory, like maximum

level, minimum level, and re-ordering level for each item. When the stock of a particular

inventory item reaches the reordering level, the store keeper places a purchase requisition to the

purchase department. On the basis of the requisition, purchasing department prepares purchase

order/s, sends the original to the vendor/s and copies to the accounts payable and inventory

departments, and keeps one copy in the purchase department. The accounts payable department

keeps the copy of the purchase order in the account payable inventory file. Another copy of the

purchase order is sent to the goods receiving department till the goods arrive (Power, Cassanego,

Subramanian, and Mo, 2016).

In order for smooth functioning of purchasing system, the procedure of purchase should start

from the inventory control department (Money Matter, 2018). The inventory department

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

recognized when the goods are accepted by the purchasing department (Accounting Tools,

2018).

Effective Purchase System Flow-Chart

Robust purchasing system requires determination of different levels of inventory, like maximum

level, minimum level, and re-ordering level for each item. When the stock of a particular

inventory item reaches the reordering level, the store keeper places a purchase requisition to the

purchase department. On the basis of the requisition, purchasing department prepares purchase

order/s, sends the original to the vendor/s and copies to the accounts payable and inventory

departments, and keeps one copy in the purchase department. The accounts payable department

keeps the copy of the purchase order in the account payable inventory file. Another copy of the

purchase order is sent to the goods receiving department till the goods arrive (Power, Cassanego,

Subramanian, and Mo, 2016).

In order for smooth functioning of purchasing system, the procedure of purchase should start

from the inventory control department (Money Matter, 2018). The inventory department

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

possesses and sends necessary purchasing information like re-ordering quantity re-ordering level,

quality and rates of inventories, and addresses of listed vendors. On the basis of these

information, purchasing department is enabled to make best purchasing decisions.

Review of the purchase system of Adam and Co. reveals certain draw-backs. The purchase

department of the company places purchase orders on the basis of information contained in

inventory subsidiary ledger, instead of on the basis of requisition placed by the inventory clerk.

The inventory subsidiary ledger may not contain updated information about ground situation and

vendor credentials, resulting in either unnecessary purchase or delayed purchase which would

affect business operations of the firm. Adam and Co. should take note of this shortcoming and

reorganize the purchase system of the firm. Secondly inventory control and purchasing system of

the firm need to be managed with the help of established inventory control tools of inventory

levels. Minimum level is the level below which the stock of an inventory should not be allowed

to fall, to ensure smooth operations. Maximum level is the level above which the stock of an

inventory must not rise, to prevent capital blockade in inventory. Re-ordering level lies between

these two levels, at which orders will have to be placed, Re-ordering quantity also termed as

economic order quantity (EOQ) is the quantity to be ordered at a time, so that cost of carrying

plus the cost of ordering is minimum. All these quantities are determined on the basis of annual

demand, cost per unit, ordering cost of placing an order, and carrying or storage cost of

inventories (Trade Gecko, 2018). Establishing these levels and using them in the purchase

system would ensure better inventory control and more efficient utilization of resources by the

purchase department of the company.

The purchase department should send a blind copy of the purchase order to the goods receiving

department, so that the goods receiving clerk can check quantity of material with the purchase

order handed to him by the representative of the vendor carrying in the goods. In busy schedule,

the goods receiving clerk often does not physically check the quantity of inventory carried in,

before making the goods received report. Sending blind copy to the receiving department would

prevent such negligence.

Purchase System Flow-Chart of Adam and Co.

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

possesses and sends necessary purchasing information like re-ordering quantity re-ordering level,

quality and rates of inventories, and addresses of listed vendors. On the basis of these

information, purchasing department is enabled to make best purchasing decisions.

Review of the purchase system of Adam and Co. reveals certain draw-backs. The purchase

department of the company places purchase orders on the basis of information contained in

inventory subsidiary ledger, instead of on the basis of requisition placed by the inventory clerk.

The inventory subsidiary ledger may not contain updated information about ground situation and

vendor credentials, resulting in either unnecessary purchase or delayed purchase which would

affect business operations of the firm. Adam and Co. should take note of this shortcoming and

reorganize the purchase system of the firm. Secondly inventory control and purchasing system of

the firm need to be managed with the help of established inventory control tools of inventory

levels. Minimum level is the level below which the stock of an inventory should not be allowed

to fall, to ensure smooth operations. Maximum level is the level above which the stock of an

inventory must not rise, to prevent capital blockade in inventory. Re-ordering level lies between

these two levels, at which orders will have to be placed, Re-ordering quantity also termed as

economic order quantity (EOQ) is the quantity to be ordered at a time, so that cost of carrying

plus the cost of ordering is minimum. All these quantities are determined on the basis of annual

demand, cost per unit, ordering cost of placing an order, and carrying or storage cost of

inventories (Trade Gecko, 2018). Establishing these levels and using them in the purchase

system would ensure better inventory control and more efficient utilization of resources by the

purchase department of the company.

The purchase department should send a blind copy of the purchase order to the goods receiving

department, so that the goods receiving clerk can check quantity of material with the purchase

order handed to him by the representative of the vendor carrying in the goods. In busy schedule,

the goods receiving clerk often does not physically check the quantity of inventory carried in,

before making the goods received report. Sending blind copy to the receiving department would

prevent such negligence.

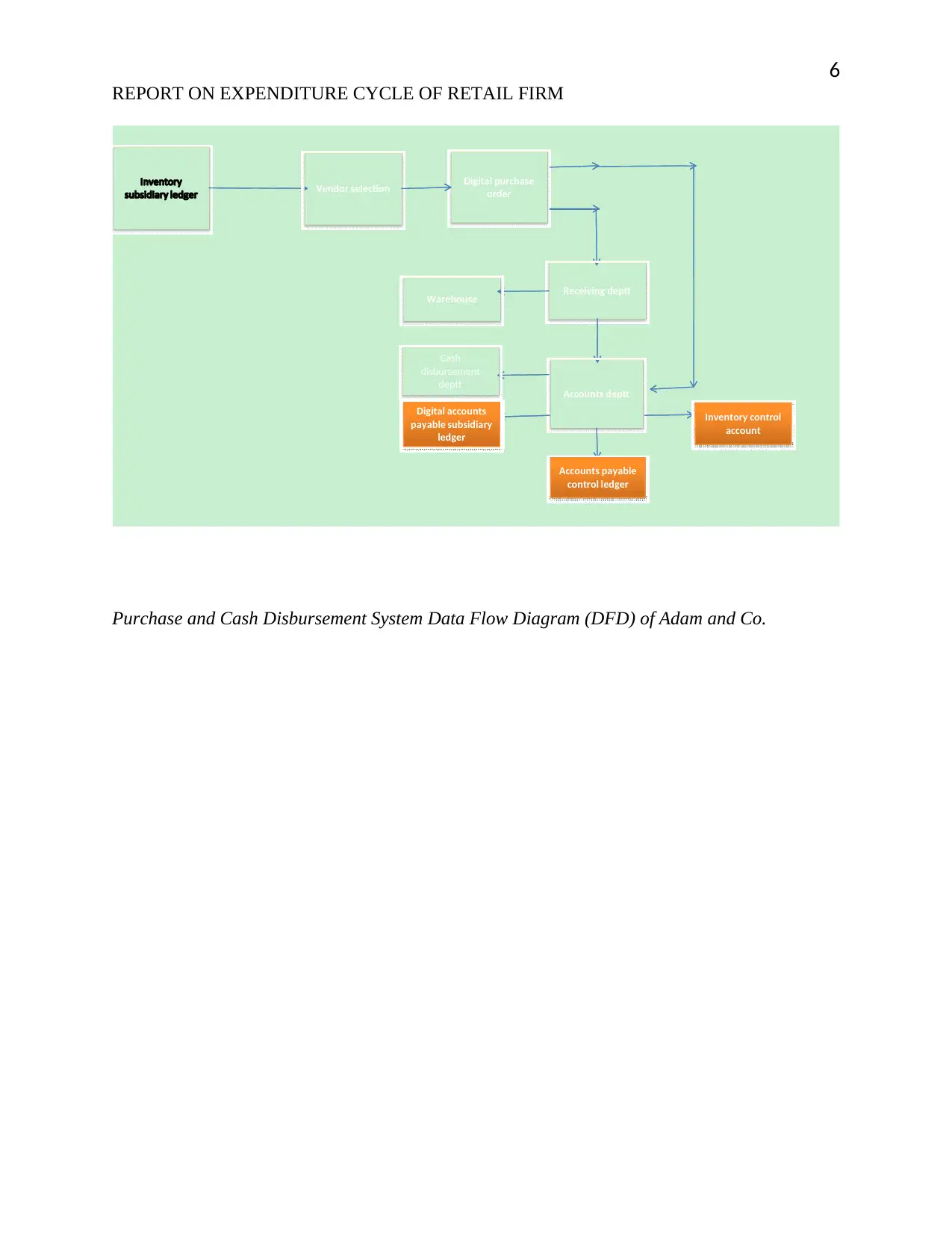

Purchase System Flow-Chart of Adam and Co.

6

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Vendor selection Digital purchase

order

Receiving deptt

Warehouse

Accounts deptt

Cash

disbursement

deptt

Digital accounts

payable subsidiary

ledger

Accounts payable

control ledger

Inventory control

account

Oopen Digital

PO and AP

files

Prepare cash

disbursement

Accounts

Cash

Identify

liabilities Supplier

Purchase and Cash Disbursement System Data Flow Diagram (DFD) of Adam and Co.

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Vendor selection Digital purchase

order

Receiving deptt

Warehouse

Accounts deptt

Cash

disbursement

deptt

Digital accounts

payable subsidiary

ledger

Accounts payable

control ledger

Inventory control

account

Oopen Digital

PO and AP

files

Prepare cash

disbursement

Accounts

Cash

Identify

liabilities Supplier

Purchase and Cash Disbursement System Data Flow Diagram (DFD) of Adam and Co.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

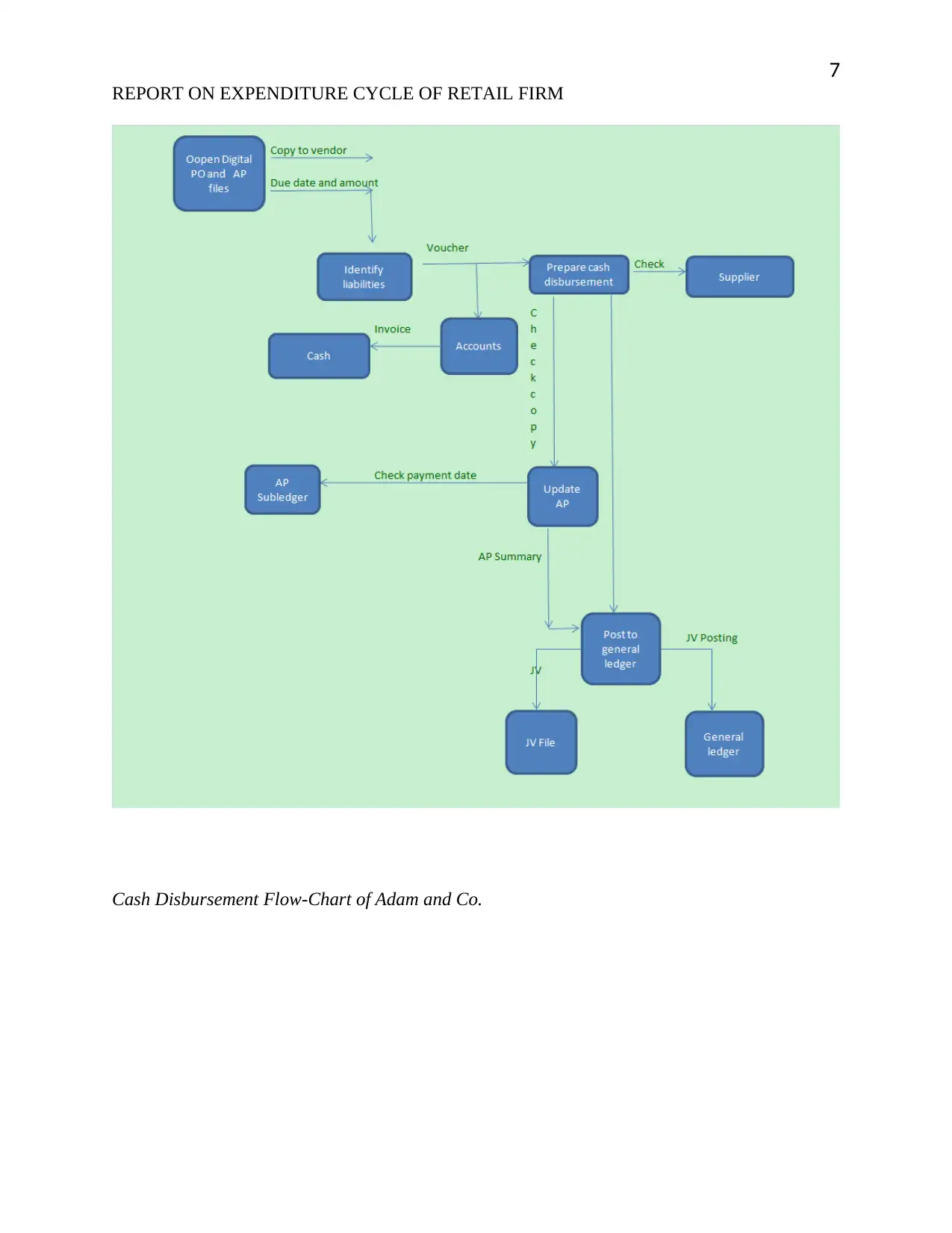

Cash Disbursement Flow-Chart of Adam and Co.

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Cash Disbursement Flow-Chart of Adam and Co.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Accounts

payable

deptt.

Cash deptt. Treasurer

Vendor

Time card Payroll deptt. Digital employee

recirds

Supervisors

Accounts

payable

Bell Studio's

employees Time

card Payroll Supervisors

Disbursement

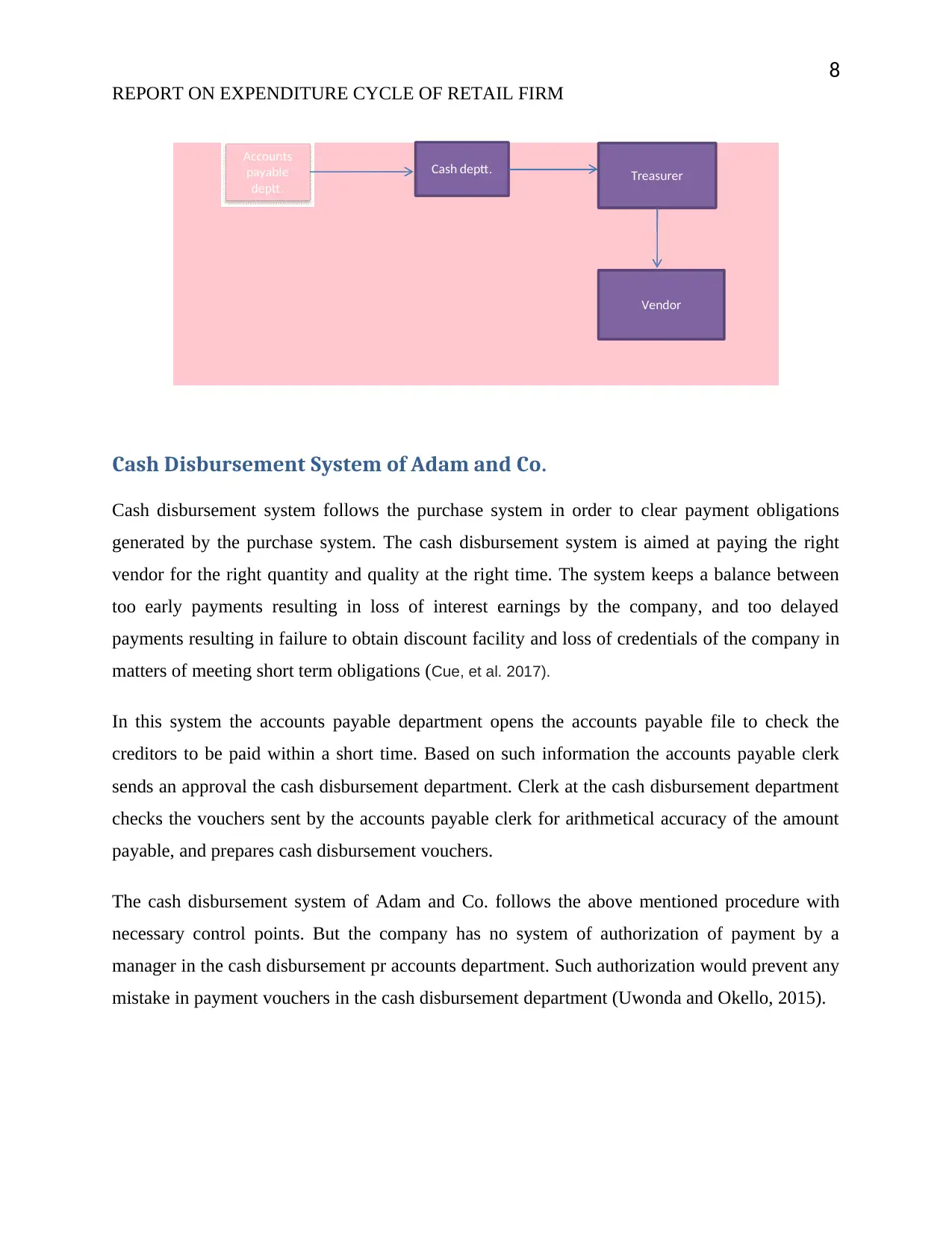

Cash Disbursement System of Adam and Co.

Cash disbursement system follows the purchase system in order to clear payment obligations

generated by the purchase system. The cash disbursement system is aimed at paying the right

vendor for the right quantity and quality at the right time. The system keeps a balance between

too early payments resulting in loss of interest earnings by the company, and too delayed

payments resulting in failure to obtain discount facility and loss of credentials of the company in

matters of meeting short term obligations (Cue, et al. 2017).

In this system the accounts payable department opens the accounts payable file to check the

creditors to be paid within a short time. Based on such information the accounts payable clerk

sends an approval the cash disbursement department. Clerk at the cash disbursement department

checks the vouchers sent by the accounts payable clerk for arithmetical accuracy of the amount

payable, and prepares cash disbursement vouchers.

The cash disbursement system of Adam and Co. follows the above mentioned procedure with

necessary control points. But the company has no system of authorization of payment by a

manager in the cash disbursement pr accounts department. Such authorization would prevent any

mistake in payment vouchers in the cash disbursement department (Uwonda and Okello, 2015).

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Accounts

payable

deptt.

Cash deptt. Treasurer

Vendor

Time card Payroll deptt. Digital employee

recirds

Supervisors

Accounts

payable

Bell Studio's

employees Time

card Payroll Supervisors

Disbursement

Cash Disbursement System of Adam and Co.

Cash disbursement system follows the purchase system in order to clear payment obligations

generated by the purchase system. The cash disbursement system is aimed at paying the right

vendor for the right quantity and quality at the right time. The system keeps a balance between

too early payments resulting in loss of interest earnings by the company, and too delayed

payments resulting in failure to obtain discount facility and loss of credentials of the company in

matters of meeting short term obligations (Cue, et al. 2017).

In this system the accounts payable department opens the accounts payable file to check the

creditors to be paid within a short time. Based on such information the accounts payable clerk

sends an approval the cash disbursement department. Clerk at the cash disbursement department

checks the vouchers sent by the accounts payable clerk for arithmetical accuracy of the amount

payable, and prepares cash disbursement vouchers.

The cash disbursement system of Adam and Co. follows the above mentioned procedure with

necessary control points. But the company has no system of authorization of payment by a

manager in the cash disbursement pr accounts department. Such authorization would prevent any

mistake in payment vouchers in the cash disbursement department (Uwonda and Okello, 2015).

9

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

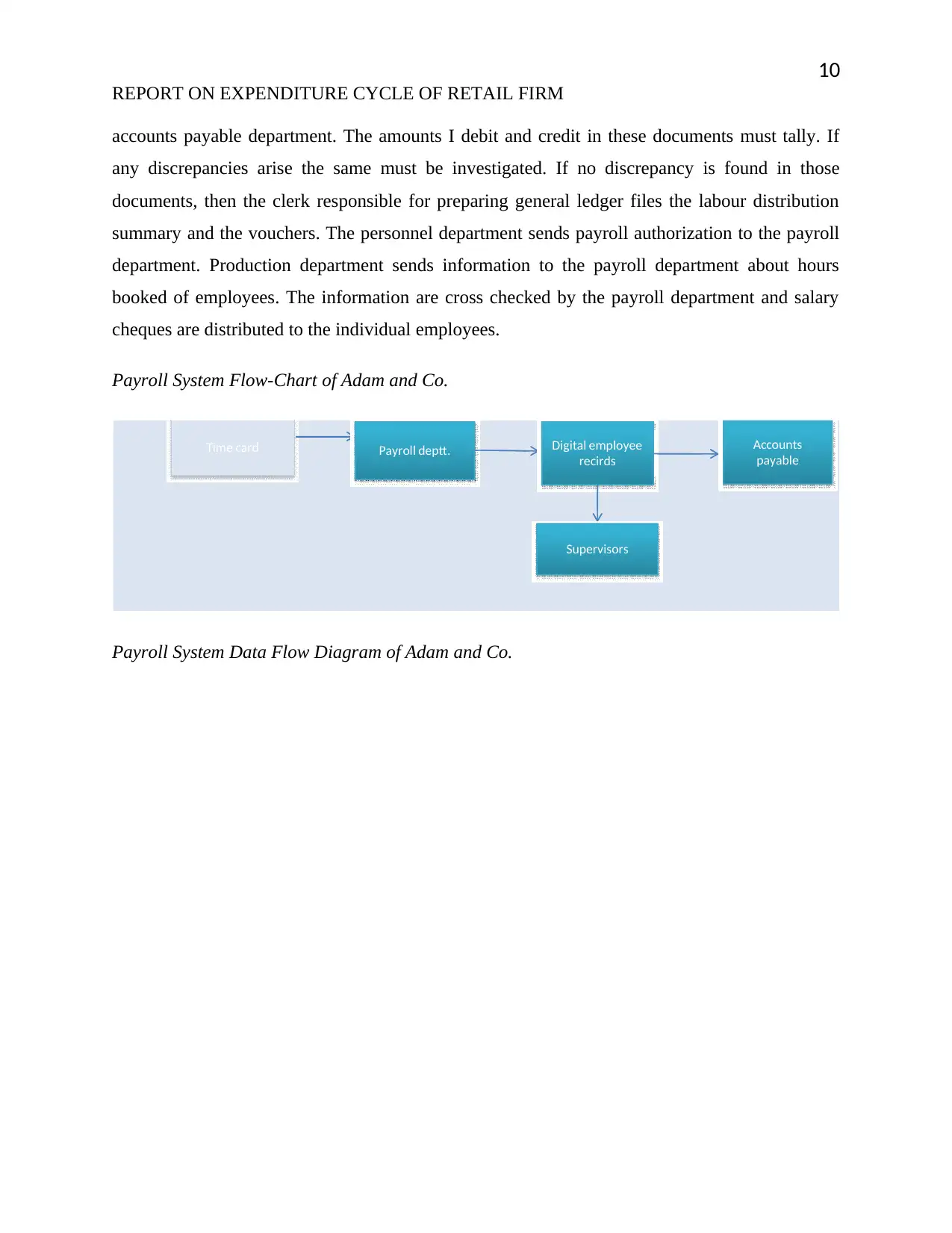

Payroll System of Adam and Co.

Payroll of a firm consists of records of employee compensation including basic salary,

allowances, other payments, bonus, deductions, etc. Correct payroll system ensures payment to

right employee of the right amount and at the right time. Payroll system is a special type of

purchase system as the employers purchase services of the employees in lieu of cash. Purchasing

system has blanket application for all types of industries. But payroll system of firms differ from

one business to another depending upon whether the payment is made weekly, fortnightly, or

monthly (Kondrk, et al. 2016). Payroll system requires detailed and complex calculations to arrive

at the disbursement figures. The personnel department supplies employee compensation details

to the accounts department where salary sheets are prepared. The primary documents used by the

accounts department to prepare the salary sheets are job ticket and time card. Time card shows

the time the employee is present at the work place and the job ticket shows the time employees

spend on a particular job. These documents are sent by the personnel department to the payroll

section of the accounts department. One common fraud committed by employees is to provide

details of non-existent employees to the payroll section. To prevent this fraud, many firms use

paymasters for employee payment. Paymaster prepares salary checks independent of payroll

information. Whenever a paycheck is not claimed by genuine employees of the firm, the same

goes back to the Paymaster, who then returns the check to the payroll department. When this

happens, investigations can be made as to how the check reached unintended person (Khan,

2018).

The payroll registers are checked by the accounts payable department where payment vouchers

are prepared. The accounts payable clerk keeps records of the payment vouchers in the voucher

register and sends vouchers to the cash disbursement department. Copies of these vouchers are

then sent to the general ledger clerk. The cash disbursement department prepares a single check

for the entire amount and places it the company’s payroll imprest account.

Fund from general cash account is then transferred to the imprest account from where individual

cheques to the employees are handed out. A labour distribution summary is prepared by the cost

accounting department for posting in the general ledger. This summary is tallied by the journal

vouchers prepared by cash disbursement department and disbursement vouchers prepared by the

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Payroll System of Adam and Co.

Payroll of a firm consists of records of employee compensation including basic salary,

allowances, other payments, bonus, deductions, etc. Correct payroll system ensures payment to

right employee of the right amount and at the right time. Payroll system is a special type of

purchase system as the employers purchase services of the employees in lieu of cash. Purchasing

system has blanket application for all types of industries. But payroll system of firms differ from

one business to another depending upon whether the payment is made weekly, fortnightly, or

monthly (Kondrk, et al. 2016). Payroll system requires detailed and complex calculations to arrive

at the disbursement figures. The personnel department supplies employee compensation details

to the accounts department where salary sheets are prepared. The primary documents used by the

accounts department to prepare the salary sheets are job ticket and time card. Time card shows

the time the employee is present at the work place and the job ticket shows the time employees

spend on a particular job. These documents are sent by the personnel department to the payroll

section of the accounts department. One common fraud committed by employees is to provide

details of non-existent employees to the payroll section. To prevent this fraud, many firms use

paymasters for employee payment. Paymaster prepares salary checks independent of payroll

information. Whenever a paycheck is not claimed by genuine employees of the firm, the same

goes back to the Paymaster, who then returns the check to the payroll department. When this

happens, investigations can be made as to how the check reached unintended person (Khan,

2018).

The payroll registers are checked by the accounts payable department where payment vouchers

are prepared. The accounts payable clerk keeps records of the payment vouchers in the voucher

register and sends vouchers to the cash disbursement department. Copies of these vouchers are

then sent to the general ledger clerk. The cash disbursement department prepares a single check

for the entire amount and places it the company’s payroll imprest account.

Fund from general cash account is then transferred to the imprest account from where individual

cheques to the employees are handed out. A labour distribution summary is prepared by the cost

accounting department for posting in the general ledger. This summary is tallied by the journal

vouchers prepared by cash disbursement department and disbursement vouchers prepared by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

accounts payable department. The amounts I debit and credit in these documents must tally. If

any discrepancies arise the same must be investigated. If no discrepancy is found in those

documents, then the clerk responsible for preparing general ledger files the labour distribution

summary and the vouchers. The personnel department sends payroll authorization to the payroll

department. Production department sends information to the payroll department about hours

booked of employees. The information are cross checked by the payroll department and salary

cheques are distributed to the individual employees.

Payroll System Flow-Chart of Adam and Co.

Time card Payroll deptt. Digital employee

recirds

Supervisors

Accounts

payable

Employees

bank details Time

card Payroll Supervisors

Calculate pay

Calculate

deductions and

subtractions

Deductions

Employee pay

Depodit

employee

pay

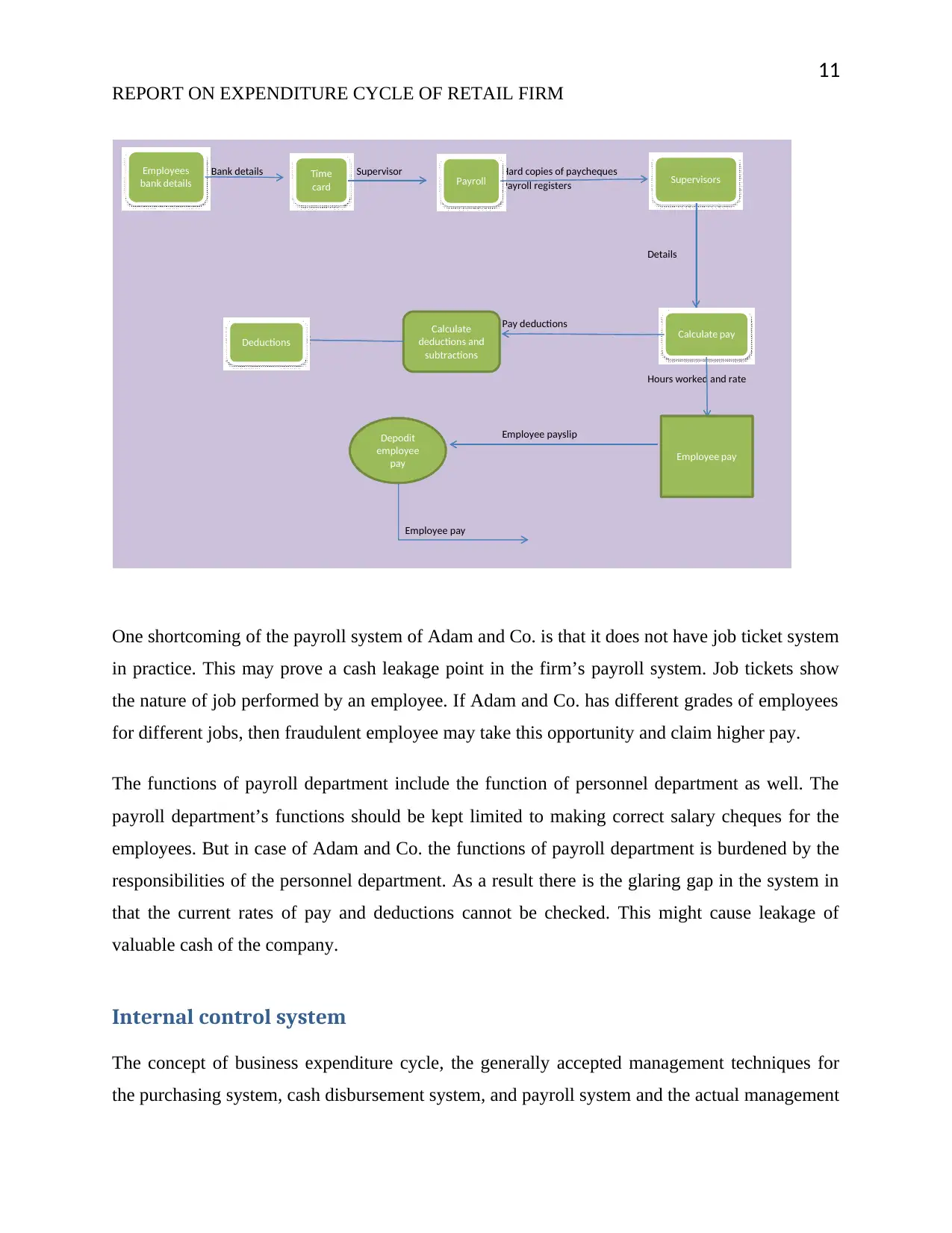

Payroll System Data Flow Diagram of Adam and Co.

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

accounts payable department. The amounts I debit and credit in these documents must tally. If

any discrepancies arise the same must be investigated. If no discrepancy is found in those

documents, then the clerk responsible for preparing general ledger files the labour distribution

summary and the vouchers. The personnel department sends payroll authorization to the payroll

department. Production department sends information to the payroll department about hours

booked of employees. The information are cross checked by the payroll department and salary

cheques are distributed to the individual employees.

Payroll System Flow-Chart of Adam and Co.

Time card Payroll deptt. Digital employee

recirds

Supervisors

Accounts

payable

Employees

bank details Time

card Payroll Supervisors

Calculate pay

Calculate

deductions and

subtractions

Deductions

Employee pay

Depodit

employee

pay

Payroll System Data Flow Diagram of Adam and Co.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Bank details Supervisor Hard copies of paycheques

Payroll registers

Details

Pay deductions

Hours worked and rate

Employee payslip

Employee pay

Employees

bank details Time

card Payroll Supervisors

Calculate pay

Calculate

deductions and

subtractions

Deductions

Employee pay

Depodit

employee

pay

One shortcoming of the payroll system of Adam and Co. is that it does not have job ticket system

in practice. This may prove a cash leakage point in the firm’s payroll system. Job tickets show

the nature of job performed by an employee. If Adam and Co. has different grades of employees

for different jobs, then fraudulent employee may take this opportunity and claim higher pay.

The functions of payroll department include the function of personnel department as well. The

payroll department’s functions should be kept limited to making correct salary cheques for the

employees. But in case of Adam and Co. the functions of payroll department is burdened by the

responsibilities of the personnel department. As a result there is the glaring gap in the system in

that the current rates of pay and deductions cannot be checked. This might cause leakage of

valuable cash of the company.

Internal control system

The concept of business expenditure cycle, the generally accepted management techniques for

the purchasing system, cash disbursement system, and payroll system and the actual management

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

Bank details Supervisor Hard copies of paycheques

Payroll registers

Details

Pay deductions

Hours worked and rate

Employee payslip

Employee pay

Employees

bank details Time

card Payroll Supervisors

Calculate pay

Calculate

deductions and

subtractions

Deductions

Employee pay

Depodit

employee

pay

One shortcoming of the payroll system of Adam and Co. is that it does not have job ticket system

in practice. This may prove a cash leakage point in the firm’s payroll system. Job tickets show

the nature of job performed by an employee. If Adam and Co. has different grades of employees

for different jobs, then fraudulent employee may take this opportunity and claim higher pay.

The functions of payroll department include the function of personnel department as well. The

payroll department’s functions should be kept limited to making correct salary cheques for the

employees. But in case of Adam and Co. the functions of payroll department is burdened by the

responsibilities of the personnel department. As a result there is the glaring gap in the system in

that the current rates of pay and deductions cannot be checked. This might cause leakage of

valuable cash of the company.

Internal control system

The concept of business expenditure cycle, the generally accepted management techniques for

the purchasing system, cash disbursement system, and payroll system and the actual management

12

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

of the said systems of Adam and Co. are discussed in the foregoing sections of this report. A

succinct analysis has been made to get insight of the existing internal control system as reflected

by the purchasing system, payroll system, and cash disbursement system of the company. The

purchasing system needs a revisit in the light of some holes in the system, which has given rise

to risk and may prove costly in future in the form of weak liquidity position of the firm.

Purchasing procedure must be initiated by the inventory department as this gives real time data

to the purchasing department (De Mattei, and Emeth, 2016). For better management of the

purchasing system different quantitative measurements for the items are needed to be

established. The cash disbursement system requires managerial authorization of payment to bring

in greater control as the cash disbursement clerk presently depends upon the information

supplied by the payroll, and AP department to prepare disbursement cheques.

Conclusion

In this report the concept of business expenditure cycle, the best management techniques of the

purchase system, cash disbursement system, and the payroll system and the actual practice of

these systems by the management of Adam and Co. are discussed. Analysis of the actual system

in operation in Adam and Co. reveals certain shortcomings in the said systems. The purchasing

system of the company needs a revisit in order to plug certain loopholes which may result in

leakage of cash or opportunity cost of cash. The purchasing department should reorganize the

system to incorporate certain inventory management tools, tom provide real time data to the

purchase department. The cash disbursement system may be strengthened by introducing a

system of authorization of payment to suppliers by a manager. In the absence of separate

personnel department in Adam and Co., the functions of maintaining employee job and

compensation records and supplying information to the payroll department should be undertaken

by the directors to avoid any ghost payments.

REPORT ON EXPENDITURE CYCLE OF RETAIL FIRM

of the said systems of Adam and Co. are discussed in the foregoing sections of this report. A

succinct analysis has been made to get insight of the existing internal control system as reflected

by the purchasing system, payroll system, and cash disbursement system of the company. The

purchasing system needs a revisit in the light of some holes in the system, which has given rise

to risk and may prove costly in future in the form of weak liquidity position of the firm.

Purchasing procedure must be initiated by the inventory department as this gives real time data

to the purchasing department (De Mattei, and Emeth, 2016). For better management of the

purchasing system different quantitative measurements for the items are needed to be

established. The cash disbursement system requires managerial authorization of payment to bring

in greater control as the cash disbursement clerk presently depends upon the information

supplied by the payroll, and AP department to prepare disbursement cheques.

Conclusion

In this report the concept of business expenditure cycle, the best management techniques of the

purchase system, cash disbursement system, and the payroll system and the actual practice of

these systems by the management of Adam and Co. are discussed. Analysis of the actual system

in operation in Adam and Co. reveals certain shortcomings in the said systems. The purchasing

system of the company needs a revisit in order to plug certain loopholes which may result in

leakage of cash or opportunity cost of cash. The purchasing department should reorganize the

system to incorporate certain inventory management tools, tom provide real time data to the

purchase department. The cash disbursement system may be strengthened by introducing a

system of authorization of payment to suppliers by a manager. In the absence of separate

personnel department in Adam and Co., the functions of maintaining employee job and

compensation records and supplying information to the payroll department should be undertaken

by the directors to avoid any ghost payments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.