Bell Studio Expenditure Cycle: Risks, Controls, and Processes Analysis

VerifiedAdded on 2022/11/24

|15

|3083

|164

Case Study

AI Summary

This case study analyzes the expenditure cycle at Bell Studio, focusing on the strategic information system. The report examines the payroll, cash disbursements, and purchases systems through system flowcharts and data flow diagrams. It identifies internal control weaknesses, associated ri...

Expenditure Cycle

Strategic Information System

Expenditure Cycle at Bell Studio

Student Name

Instructor

Institutional Affiliation

1

Strategic Information System

Expenditure Cycle at Bell Studio

Student Name

Instructor

Institutional Affiliation

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expenditure Cycle

Executive Summary

Strategic Information System is essentially used in the organization to help in making

decisions with regards to the firm activities when compared to the real world. When SIS is used

in a firm, they are known for giving an organization a higher preferred position when compared

with the immediate competitors. It can be used to deliver material or services at cost which are

low and thus separating most of the part as it is focusing on ordering market which in deed is

much creative.

SIS is a basic element in corporate and technology development globally. In additional,

this has been used by many firms as it enhances the organizations to be able to acquire, store, be

able to process information and thus using such received information to create and receive

others. It has also been used in empowering and giving different materials and services that can

be used to help the organization to be able to measure the materials thus enabling them to

perceive the ingenious open doors. This is usually used for development and thus the basic ways

will upgrade the tasks and supply proficiency.

This report has majored on doing an analysis on the procedures, the hazards and the

internal controls that exists in Bell Studio expenditure cycle. The report has been classified in

several parts as stated below. There is the diagram representing the flowcharts and data flow

diagrams of payroll system and disbursement system. The diagrams are used to show how the

processes from one point to another within the given internal controls. The report has also been

used to show how decisions are made with relation to the information movement. It has also

been used to show the associated risks, threats are in the business processes in the Bell Studio

Expenditure cycle scenario. This will help one in understanding the required internal controls in

addressing all the threats.

2

Executive Summary

Strategic Information System is essentially used in the organization to help in making

decisions with regards to the firm activities when compared to the real world. When SIS is used

in a firm, they are known for giving an organization a higher preferred position when compared

with the immediate competitors. It can be used to deliver material or services at cost which are

low and thus separating most of the part as it is focusing on ordering market which in deed is

much creative.

SIS is a basic element in corporate and technology development globally. In additional,

this has been used by many firms as it enhances the organizations to be able to acquire, store, be

able to process information and thus using such received information to create and receive

others. It has also been used in empowering and giving different materials and services that can

be used to help the organization to be able to measure the materials thus enabling them to

perceive the ingenious open doors. This is usually used for development and thus the basic ways

will upgrade the tasks and supply proficiency.

This report has majored on doing an analysis on the procedures, the hazards and the

internal controls that exists in Bell Studio expenditure cycle. The report has been classified in

several parts as stated below. There is the diagram representing the flowcharts and data flow

diagrams of payroll system and disbursement system. The diagrams are used to show how the

processes from one point to another within the given internal controls. The report has also been

used to show how decisions are made with relation to the information movement. It has also

been used to show the associated risks, threats are in the business processes in the Bell Studio

Expenditure cycle scenario. This will help one in understanding the required internal controls in

addressing all the threats.

2

Expenditure Cycle

Table of Contents

Executive Summary.......................................................................................................................2

List of Figures................................................................................................................................3

Introduction....................................................................................................................................4

Structural and Modelling Diagrams............................................................................................5

System flowchart of payroll system..........................................................................................6

Data flow diagram of payroll system........................................................................................6

System flowchart of cash disbursements system.....................................................................7

Data flow diagram of purchases and cash disbursements systems.......................................7

System flowchart of purchases system.....................................................................................8

Description of internal control weakness in each system and risks associated with the

identified weakness........................................................................................................................8

Expenditure Cycle......................................................................................................................8

Business Processes......................................................................................................................9

Risks, Threats and Internal Controls.....................................................................................10

Conclusion....................................................................................................................................13

List of references..........................................................................................................................14

3

Table of Contents

Executive Summary.......................................................................................................................2

List of Figures................................................................................................................................3

Introduction....................................................................................................................................4

Structural and Modelling Diagrams............................................................................................5

System flowchart of payroll system..........................................................................................6

Data flow diagram of payroll system........................................................................................6

System flowchart of cash disbursements system.....................................................................7

Data flow diagram of purchases and cash disbursements systems.......................................7

System flowchart of purchases system.....................................................................................8

Description of internal control weakness in each system and risks associated with the

identified weakness........................................................................................................................8

Expenditure Cycle......................................................................................................................8

Business Processes......................................................................................................................9

Risks, Threats and Internal Controls.....................................................................................10

Conclusion....................................................................................................................................13

List of references..........................................................................................................................14

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expenditure Cycle

List of Figures

Figure 1 System flowchart of the payroll system............................................................................7

Figure 2 DFD for Payroll System of Bell Studio............................................................................7

Figure 3 Flowchart for Cash Disbursements system.......................................................................8

Figure 4 Data flow diagram of purchases and cash disbursements systems...................................9

Figure 5 System Flowchart of Bell Studio Purchases System.........................................................9

Introduction

Strategic Information System is essentially used in the organization to help in making

decisions with regards to the firm activities when compared to the real world. When SIS is used

in a firm, they are known for giving an organization a higher preferred position when compared

with the immediate competitors. It can be used to deliver material or services at cost which are

low and thus separating most of the part as it is focusing on ordering market which in deed is

much creative. SIS is a basic element in corporate and technology development globally. In

additional, this has been used by many firms as it enhances the organizations to be able to

acquire, store, be able to process information and thus using such received information to create

and receive others. It has also been used in empowering and giving different materials and

services that can be used to help the organization to be able to measure the materials thus

enabling them to perceive the ingenious open doors. This is usually used for development and

thus the basic ways will upgrade the tasks and supply proficiency.

In the Strategic information system in this case of Bell Studio, will be explained in terms

of the expenditure cycle. EC can be explained to be the detailed collection of the activities

related to the purchases and payment made to various products and services in a given

organization (Kazak, 2015). In the expenditure cycle, the cycle will start when the firm is in need

of any service or a product for the firm operational functions or for trading. In the concept of

expenditure cycle, the internal controls are defined as the systems which have a relationship with

4

List of Figures

Figure 1 System flowchart of the payroll system............................................................................7

Figure 2 DFD for Payroll System of Bell Studio............................................................................7

Figure 3 Flowchart for Cash Disbursements system.......................................................................8

Figure 4 Data flow diagram of purchases and cash disbursements systems...................................9

Figure 5 System Flowchart of Bell Studio Purchases System.........................................................9

Introduction

Strategic Information System is essentially used in the organization to help in making

decisions with regards to the firm activities when compared to the real world. When SIS is used

in a firm, they are known for giving an organization a higher preferred position when compared

with the immediate competitors. It can be used to deliver material or services at cost which are

low and thus separating most of the part as it is focusing on ordering market which in deed is

much creative. SIS is a basic element in corporate and technology development globally. In

additional, this has been used by many firms as it enhances the organizations to be able to

acquire, store, be able to process information and thus using such received information to create

and receive others. It has also been used in empowering and giving different materials and

services that can be used to help the organization to be able to measure the materials thus

enabling them to perceive the ingenious open doors. This is usually used for development and

thus the basic ways will upgrade the tasks and supply proficiency.

In the Strategic information system in this case of Bell Studio, will be explained in terms

of the expenditure cycle. EC can be explained to be the detailed collection of the activities

related to the purchases and payment made to various products and services in a given

organization (Kazak, 2015). In the expenditure cycle, the cycle will start when the firm is in need

of any service or a product for the firm operational functions or for trading. In the concept of

expenditure cycle, the internal controls are defined as the systems which have a relationship with

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expenditure Cycle

rent practices and processes and it is usually developed by the aimed entities at securing all the

assets, also enhance efficiency, accuracy assurance of the accounting information and measure

the procedure of compliance and management policies.

This report has majored on doing an analysis on the procedures, the hazards and the

internal controls that exists in Bell Studio expenditure cycle. The report has been classified in

several parts as stated below. There is the diagram representing the flowcharts and data flow

diagrams of payroll system and disbursement system. The diagrams are used to show how the

processes from one point to another within the given internal controls. It will also be used to

show the decision making process on how information move, the main risks associated and all

the threats with regards to the expenditure cycle. This will help one in understanding the required

internal controls in addressing all the threats.

Structural and Modelling Diagrams

The figures below shows the drawings for the Data flow diagrams and flowchart

diagrams on the cash disbursements systems, purchases systems, and the payroll system. In this

concept, diagrams have been used in showing how information flow in the expenditure cycle of

the given systems of Bell Studio. This figures are drawn using the Microsoft Vision and are own

drawing.

5

rent practices and processes and it is usually developed by the aimed entities at securing all the

assets, also enhance efficiency, accuracy assurance of the accounting information and measure

the procedure of compliance and management policies.

This report has majored on doing an analysis on the procedures, the hazards and the

internal controls that exists in Bell Studio expenditure cycle. The report has been classified in

several parts as stated below. There is the diagram representing the flowcharts and data flow

diagrams of payroll system and disbursement system. The diagrams are used to show how the

processes from one point to another within the given internal controls. It will also be used to

show the decision making process on how information move, the main risks associated and all

the threats with regards to the expenditure cycle. This will help one in understanding the required

internal controls in addressing all the threats.

Structural and Modelling Diagrams

The figures below shows the drawings for the Data flow diagrams and flowchart

diagrams on the cash disbursements systems, purchases systems, and the payroll system. In this

concept, diagrams have been used in showing how information flow in the expenditure cycle of

the given systems of Bell Studio. This figures are drawn using the Microsoft Vision and are own

drawing.

5

Expenditure Cycle

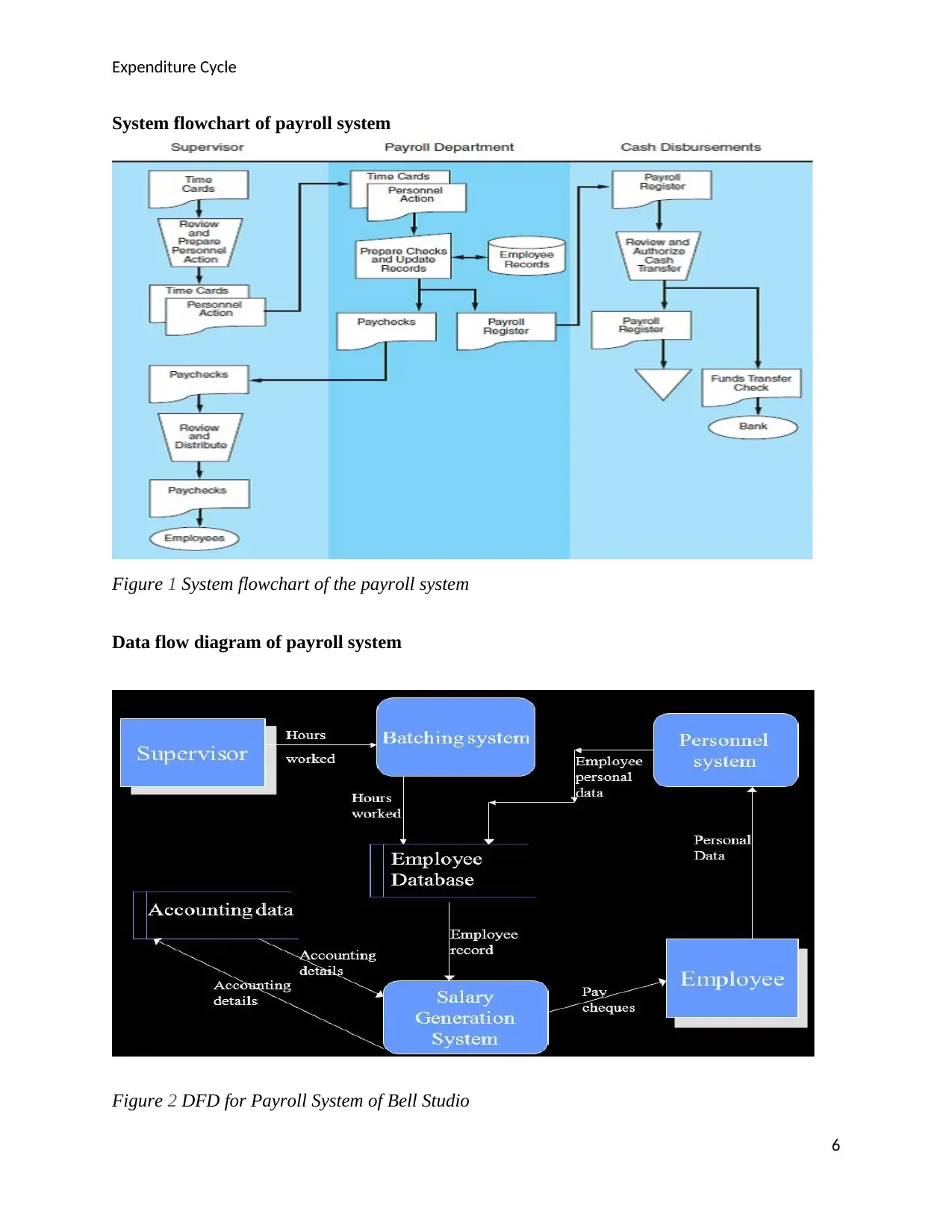

System flowchart of payroll system

Figure 1 System flowchart of the payroll system

Data flow diagram of payroll system

Figure 2 DFD for Payroll System of Bell Studio

6

System flowchart of payroll system

Figure 1 System flowchart of the payroll system

Data flow diagram of payroll system

Figure 2 DFD for Payroll System of Bell Studio

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expenditure Cycle

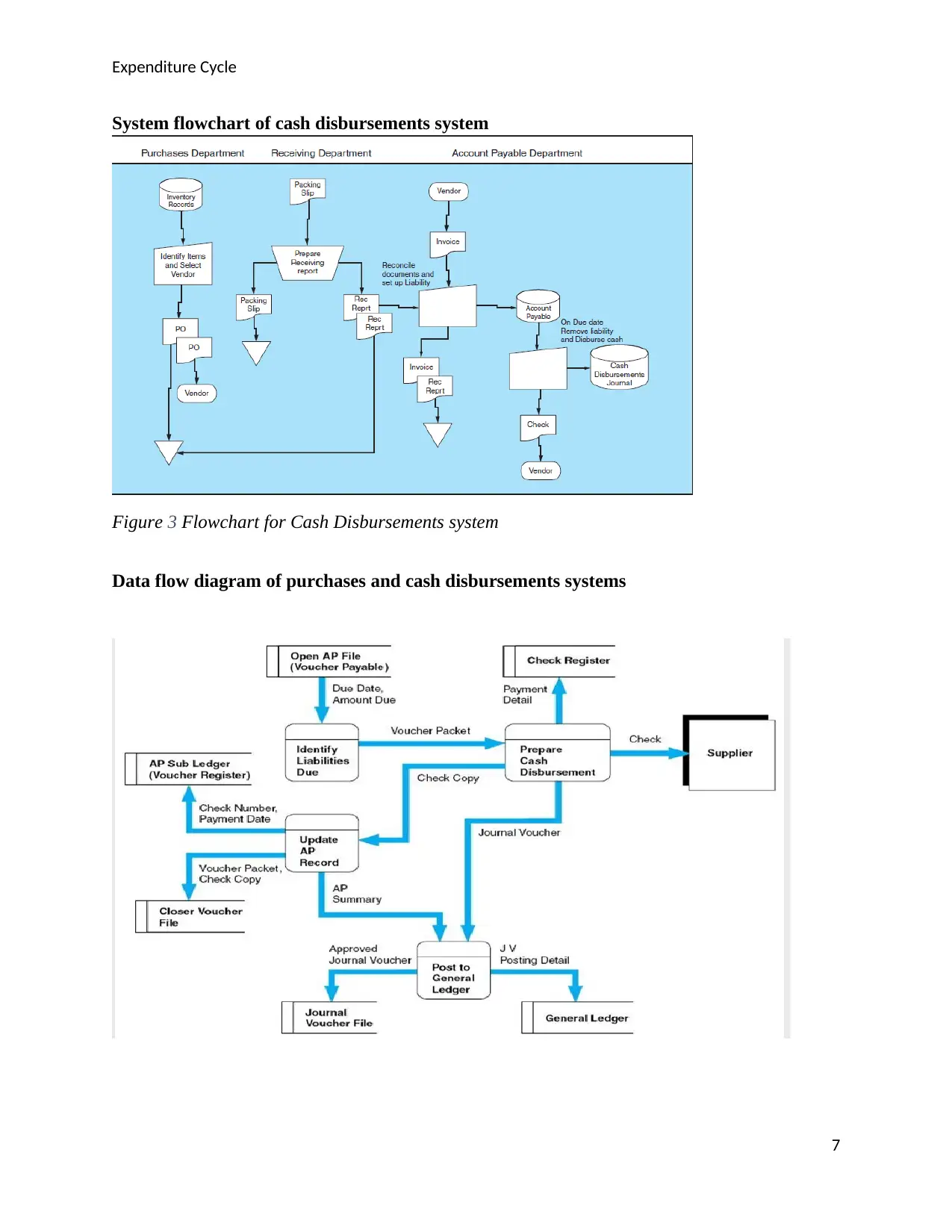

System flowchart of cash disbursements system

Figure 3 Flowchart for Cash Disbursements system

Data flow diagram of purchases and cash disbursements systems

7

System flowchart of cash disbursements system

Figure 3 Flowchart for Cash Disbursements system

Data flow diagram of purchases and cash disbursements systems

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expenditure Cycle

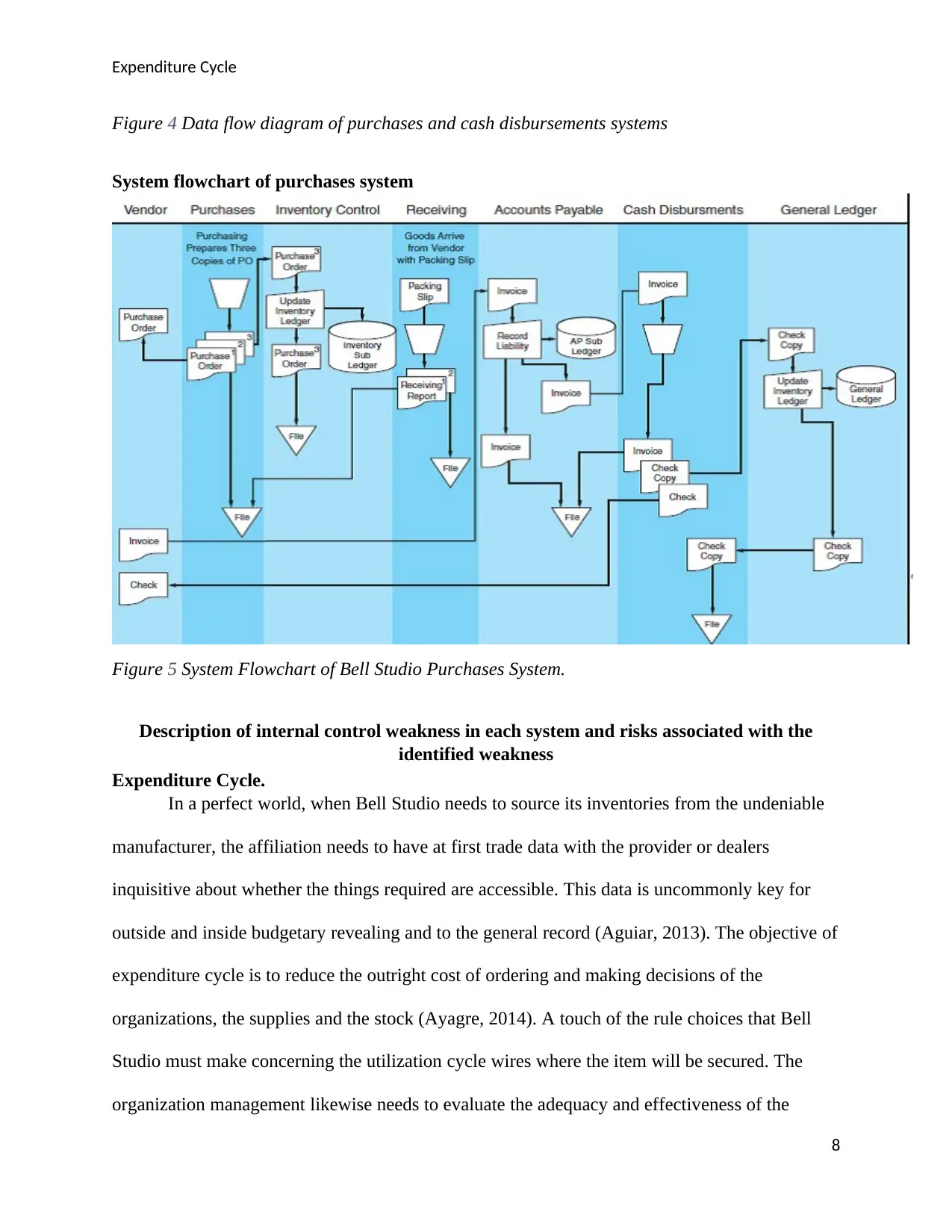

Figure 4 Data flow diagram of purchases and cash disbursements systems

System flowchart of purchases system

Figure 5 System Flowchart of Bell Studio Purchases System.

Description of internal control weakness in each system and risks associated with the

identified weakness

Expenditure Cycle.

In a perfect world, when Bell Studio needs to source its inventories from the undeniable

manufacturer, the affiliation needs to have at first trade data with the provider or dealers

inquisitive about whether the things required are accessible. This data is uncommonly key for

outside and inside budgetary revealing and to the general record (Aguiar, 2013). The objective of

expenditure cycle is to reduce the outright cost of ordering and making decisions of the

organizations, the supplies and the stock (Ayagre, 2014). A touch of the rule choices that Bell

Studio must make concerning the utilization cycle wires where the item will be secured. The

organization management likewise needs to evaluate the adequacy and effectiveness of the

8

Figure 4 Data flow diagram of purchases and cash disbursements systems

System flowchart of purchases system

Figure 5 System Flowchart of Bell Studio Purchases System.

Description of internal control weakness in each system and risks associated with the

identified weakness

Expenditure Cycle.

In a perfect world, when Bell Studio needs to source its inventories from the undeniable

manufacturer, the affiliation needs to have at first trade data with the provider or dealers

inquisitive about whether the things required are accessible. This data is uncommonly key for

outside and inside budgetary revealing and to the general record (Aguiar, 2013). The objective of

expenditure cycle is to reduce the outright cost of ordering and making decisions of the

organizations, the supplies and the stock (Ayagre, 2014). A touch of the rule choices that Bell

Studio must make concerning the utilization cycle wires where the item will be secured. The

organization management likewise needs to evaluate the adequacy and effectiveness of the

8

Expenditure Cycle

procedures associated with the expenditure cycle (Burt, Petcavage and Pinkerton, 2011). The

information utilized in the use cycle should be precise and it ought to contain data about the

operators who are included, the assets influenced, and the occasions that happen (Guillamón,

2013). The information that is used in the expenditure cycle should be accurate and detailed in

giving information of the specialists involved, affected assets and the date it happened.

Business Processes

The first process is when the firm order for goods or the services. This procedure joins on

perceiving what, how much, and when to buy and from which producer. The organization should

put more emphasis on their stock control on the grounds, thus in this case, any shortcoming may

achieve basic issues with this technique. The decision of this strategy for stock control is the

essential believed that affected the referencing technique. There are three unique approaches to

oversee stock control from which Bell Studio can examine: Material Requirements Planning,

Economic Order Quantity, and Just in Time Inventory.

Regardless of the kind of stock control framework, the requesting procedure

fundamentally begins with a buy demand, in this way age of procurement request. There must be

a worker inside Bell Studio who understands the deficiency of a specific material and thus

triggers the buy demand. The buying operator gets the buy order in the buying division. The

obtaining specialist at that point plays out a fundamental choice in choosing a producer

dependent on unwavering quality, and cost. Note: it is essential to always follow the

manufacturer. IT frameworks can be utilized to improve adequacy and productivity of the

obtaining capacity.

Secondly is the receiving and storage of ordered goods and services. This philosophy

fuses the suffering development of materials from the producer. The materials received must be

9

procedures associated with the expenditure cycle (Burt, Petcavage and Pinkerton, 2011). The

information utilized in the use cycle should be precise and it ought to contain data about the

operators who are included, the assets influenced, and the occasions that happen (Guillamón,

2013). The information that is used in the expenditure cycle should be accurate and detailed in

giving information of the specialists involved, affected assets and the date it happened.

Business Processes

The first process is when the firm order for goods or the services. This procedure joins on

perceiving what, how much, and when to buy and from which producer. The organization should

put more emphasis on their stock control on the grounds, thus in this case, any shortcoming may

achieve basic issues with this technique. The decision of this strategy for stock control is the

essential believed that affected the referencing technique. There are three unique approaches to

oversee stock control from which Bell Studio can examine: Material Requirements Planning,

Economic Order Quantity, and Just in Time Inventory.

Regardless of the kind of stock control framework, the requesting procedure

fundamentally begins with a buy demand, in this way age of procurement request. There must be

a worker inside Bell Studio who understands the deficiency of a specific material and thus

triggers the buy demand. The buying operator gets the buy order in the buying division. The

obtaining specialist at that point plays out a fundamental choice in choosing a producer

dependent on unwavering quality, and cost. Note: it is essential to always follow the

manufacturer. IT frameworks can be utilized to improve adequacy and productivity of the

obtaining capacity.

Secondly is the receiving and storage of ordered goods and services. This philosophy

fuses the suffering development of materials from the producer. The materials received must be

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expenditure Cycle

passed on to the stock control so that they can be recorded. The receiving division has two basic

occupations: to check on the received materials and decide if to perceive or dismiss them subject

to the status and nature of the materials. The check technique is basic since it guarantees that the

aggregate and nature of materials to be received is what was referenced.

The third business process is the payment of the received materials and services. This

procedure includes making the installment subsequent to accepting and confirming the materials

requested. Two sub-forms are associated with this procedure: affirming the solicitations of the

producers and making the genuine installment of the solicitations. The records payable office is

in charge of affirming the producer solicitations. The law obliges that installment ought to be

endless supply of the materials, however most organizations make the installment after receipt

and confirmation of both the materials and receipt. The Finance division is in charge of starting

payment for products that the organization requested and were delivered. There are two basic

strategies to handling maker solicitations (Länsiluoto, Jokipii and Eklund, 2016): Bell Studio can

improve the practicality and capability of the installment method by having the producers or

manufacturers present their solicitations through EDI in light of the fact that the system will

facilitate their POs thusly with the getting reports.

Risks, Threats and Internal Controls

Preferably, abundance stock or materials out of stock: the verifying representative may make a

buying interest for the things that are right now in stock. This will incite abundance stock.

Besides, he/she may comparatively surrender in referencing for new supplies required by Bell

Studio, and this may understand conclusion of the operational approach given the nonappearance

of creation materials. This danger can be obliged by utilizing fitting and solid choosing

techniques, and exact stock controls likewise ought to be utilized.

10

passed on to the stock control so that they can be recorded. The receiving division has two basic

occupations: to check on the received materials and decide if to perceive or dismiss them subject

to the status and nature of the materials. The check technique is basic since it guarantees that the

aggregate and nature of materials to be received is what was referenced.

The third business process is the payment of the received materials and services. This

procedure includes making the installment subsequent to accepting and confirming the materials

requested. Two sub-forms are associated with this procedure: affirming the solicitations of the

producers and making the genuine installment of the solicitations. The records payable office is

in charge of affirming the producer solicitations. The law obliges that installment ought to be

endless supply of the materials, however most organizations make the installment after receipt

and confirmation of both the materials and receipt. The Finance division is in charge of starting

payment for products that the organization requested and were delivered. There are two basic

strategies to handling maker solicitations (Länsiluoto, Jokipii and Eklund, 2016): Bell Studio can

improve the practicality and capability of the installment method by having the producers or

manufacturers present their solicitations through EDI in light of the fact that the system will

facilitate their POs thusly with the getting reports.

Risks, Threats and Internal Controls

Preferably, abundance stock or materials out of stock: the verifying representative may make a

buying interest for the things that are right now in stock. This will incite abundance stock.

Besides, he/she may comparatively surrender in referencing for new supplies required by Bell

Studio, and this may understand conclusion of the operational approach given the nonappearance

of creation materials. This danger can be obliged by utilizing fitting and solid choosing

techniques, and exact stock controls likewise ought to be utilized.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expenditure Cycle

Another hazard that may influence the requesting procedure is the referencing of

senseless materials or supplies: the workers at Bell Studio may make a buy enthusiasm for a

thing that isn't essential. Along these lines, the obtaining operator may proceed in referencing the

materials, and this will instigate the affiliation procuring useless things that have little a spurring

power to the relationship of the referencing pro. The internal control of such a risk is through the

use of a database bargain for the various divisions and produce reports that interface portrayal of

the things to part numbers to help request affiliation (Wood, 2014).

Requesting materials at swelled costs: this is a typical hazard confronting numerous

organizations. Bell Studioz is note excellent. In view of the dynamic idea of the economy may

prompt expansion. Therefore, the organization may wind up requesting materials when the costs

are swelled. This hazard can be controlled keeping a rundown of costs for the materials that are

acquired consistently; survey buy orders; use lists for shabby things; execution audit; obligation

bookkeeping; and spending controls (El Mahdy and Thiruvadi, 2014).

Receipt of material that were not requested: this is a conceivable hazard that Bell

Company may be involved. A producer may convey things to the organization that Bell Studio

had not requested. This generally happens when the obtaining representatives makes and request

and later drops it. The provider might not have gotten dropping and proceeds to convey the

items. Such a hazard can be constrained by getting just materials with an endorsed buy request

(Länsiluoto, Jokipii and Eklund, 2016).

Another risk is botches in checking the materials and products received. This hazard

generally happens in the Bell's receiving division where material are tallied physically. The

tallying representatives may miss the numbers and end up giving erroneous qualities (Frank,

2014). The control of this hazard includes utilizing the utilization of standardized identifications

11

Another hazard that may influence the requesting procedure is the referencing of

senseless materials or supplies: the workers at Bell Studio may make a buy enthusiasm for a

thing that isn't essential. Along these lines, the obtaining operator may proceed in referencing the

materials, and this will instigate the affiliation procuring useless things that have little a spurring

power to the relationship of the referencing pro. The internal control of such a risk is through the

use of a database bargain for the various divisions and produce reports that interface portrayal of

the things to part numbers to help request affiliation (Wood, 2014).

Requesting materials at swelled costs: this is a typical hazard confronting numerous

organizations. Bell Studioz is note excellent. In view of the dynamic idea of the economy may

prompt expansion. Therefore, the organization may wind up requesting materials when the costs

are swelled. This hazard can be controlled keeping a rundown of costs for the materials that are

acquired consistently; survey buy orders; use lists for shabby things; execution audit; obligation

bookkeeping; and spending controls (El Mahdy and Thiruvadi, 2014).

Receipt of material that were not requested: this is a conceivable hazard that Bell

Company may be involved. A producer may convey things to the organization that Bell Studio

had not requested. This generally happens when the obtaining representatives makes and request

and later drops it. The provider might not have gotten dropping and proceeds to convey the

items. Such a hazard can be constrained by getting just materials with an endorsed buy request

(Länsiluoto, Jokipii and Eklund, 2016).

Another risk is botches in checking the materials and products received. This hazard

generally happens in the Bell's receiving division where material are tallied physically. The

tallying representatives may miss the numbers and end up giving erroneous qualities (Frank,

2014). The control of this hazard includes utilizing the utilization of standardized identifications

11

Expenditure Cycle

for the material arranged, re-checking the materials for stock control, motivating forces for

distinguishing errors, mark of accepting agent, and amounts blanked out on receiving shapes

(Länsiluoto, Jokipii and Eklund, 2016).

The other risk is failing to give the correct receipts. The finance department

representative may mess around by missing to know the mistake made when receiveing the

materials. Two or three figures may have been adjusted and may look so evident. In that limit,

they may wrap up supporting invalid or off center sales for segment. In any case, this risk can be

tended to by supporting acquisition cards, utilizing an average transporter beyond what many

would consider possible, preparing workers on burden terms, utilizing assessed receipt

settlement, and avow coherent exactness (Pevzner, 2015).

Paying for materials not delivered. This risk may occur when there is some records which

are sent to finance departments even before the materials have been received. Bell Studio may

wrap up paying for the materials that were referenced yet have not been conveyed. This hazard

can be obliged by utilizing limited spending controls and checking the entireties gotten by

looking totals low down against aggregates conveyed (Gaynor, 2015).

Conclusion

Notably, this report has endeavored to isolate the approach, dangers and inside controls

for Expenditure cycle at Bell Studio. The main ideas covered in this paper have been

12

for the material arranged, re-checking the materials for stock control, motivating forces for

distinguishing errors, mark of accepting agent, and amounts blanked out on receiving shapes

(Länsiluoto, Jokipii and Eklund, 2016).

The other risk is failing to give the correct receipts. The finance department

representative may mess around by missing to know the mistake made when receiveing the

materials. Two or three figures may have been adjusted and may look so evident. In that limit,

they may wrap up supporting invalid or off center sales for segment. In any case, this risk can be

tended to by supporting acquisition cards, utilizing an average transporter beyond what many

would consider possible, preparing workers on burden terms, utilizing assessed receipt

settlement, and avow coherent exactness (Pevzner, 2015).

Paying for materials not delivered. This risk may occur when there is some records which

are sent to finance departments even before the materials have been received. Bell Studio may

wrap up paying for the materials that were referenced yet have not been conveyed. This hazard

can be obliged by utilizing limited spending controls and checking the entireties gotten by

looking totals low down against aggregates conveyed (Gaynor, 2015).

Conclusion

Notably, this report has endeavored to isolate the approach, dangers and inside controls

for Expenditure cycle at Bell Studio. The main ideas covered in this paper have been

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expenditure Cycle

summarized below: examining the different exercises and methodologies that are done in the use,

the choices that must be made and the data that is required to settle on these choices, the standard

hazard and dangers in the expenditure cycle, and within controls required to address the dangers.

The essential choices that Bell Studio must make concerning utilization cycle intertwine

where the item will be secured, the part of courses of action and stock to be received, and the

producers who offer the quality materials at reasonable expenses. The decision of the framework

for stock control is the basic imagined that influenced the referencing strategy.

List of references

Aguiar, M. and Hurst, E. (2013). Deconstructing Life Cycle Expenditure. Journal of Political

Economy, 121(3), pp.437-492.

13

summarized below: examining the different exercises and methodologies that are done in the use,

the choices that must be made and the data that is required to settle on these choices, the standard

hazard and dangers in the expenditure cycle, and within controls required to address the dangers.

The essential choices that Bell Studio must make concerning utilization cycle intertwine

where the item will be secured, the part of courses of action and stock to be received, and the

producers who offer the quality materials at reasonable expenses. The decision of the framework

for stock control is the basic imagined that influenced the referencing strategy.

List of references

Aguiar, M. and Hurst, E. (2013). Deconstructing Life Cycle Expenditure. Journal of Political

Economy, 121(3), pp.437-492.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expenditure Cycle

Ayagre, P., Appiah-Gyamerah, I. and Nartey, J. (2014). The Effectiveness of Internal Control

Systems of Banks. International Journal of Accounting and Financial Reporting, 4(2), p.377.

Ayam, J. (2015). An Analysis of Revenue Cycle Internal Controls. Case Studies in Business and

Management, 2(2), p.1.

Burt, D., Petcavage, S. and Pinkerton, R. (2011). Proactive Purchasing in the Supply Chain.

New York: McGraw-Hill Publishing.

Chow, V., Long, D., Wang, R. and Zhang, R. (2018). Joint Inventory, Pricing, and Expenditure

Control. SSRN Electronic Journal.

El Mahdy, D. and Thiruvadi, S. (2014). Antecedents, Characteristics and Consequences of

Internal Control Weaknesses and the COSO (2013) Framework. SSRN Electronic Journal.

Frank, R., Levine, A. and Dijk, O., 2014. Expenditure cascades.

Guillamón, M.D., Bastida, F. and Benito, B., 2013. The electoral budget cycle on municipal

police expenditure. European Journal of Law and Economics, 36(3), pp.447-469.

Hsueh, C. (2011). An inventory control model with consideration of remanufacturing and

product life cycle. International Journal of Production Economics, 133(2), pp.645-652.

Kazak, L., Chouchani, E.T., Jedrychowski, M.P., Erickson, B.K., Shinoda, K., Cohen, P.,

Vetrivelan, R., Lu, G.Z., Laznik-Bogoslavski, D., Hasenfuss, S.C. and Kajimura, S., 2015. A

creatine-driven substrate cycle enhances energy expenditure and thermogenesis in beige

fat. Cell, 163(3), pp.643-655.

Länsiluoto, A., Jokipii, A. and Eklund, T. (2016). Internal control effectiveness – a clustering

approach. Managerial Auditing Journal, 31(1), pp.5-34.

14

Ayagre, P., Appiah-Gyamerah, I. and Nartey, J. (2014). The Effectiveness of Internal Control

Systems of Banks. International Journal of Accounting and Financial Reporting, 4(2), p.377.

Ayam, J. (2015). An Analysis of Revenue Cycle Internal Controls. Case Studies in Business and

Management, 2(2), p.1.

Burt, D., Petcavage, S. and Pinkerton, R. (2011). Proactive Purchasing in the Supply Chain.

New York: McGraw-Hill Publishing.

Chow, V., Long, D., Wang, R. and Zhang, R. (2018). Joint Inventory, Pricing, and Expenditure

Control. SSRN Electronic Journal.

El Mahdy, D. and Thiruvadi, S. (2014). Antecedents, Characteristics and Consequences of

Internal Control Weaknesses and the COSO (2013) Framework. SSRN Electronic Journal.

Frank, R., Levine, A. and Dijk, O., 2014. Expenditure cascades.

Guillamón, M.D., Bastida, F. and Benito, B., 2013. The electoral budget cycle on municipal

police expenditure. European Journal of Law and Economics, 36(3), pp.447-469.

Hsueh, C. (2011). An inventory control model with consideration of remanufacturing and

product life cycle. International Journal of Production Economics, 133(2), pp.645-652.

Kazak, L., Chouchani, E.T., Jedrychowski, M.P., Erickson, B.K., Shinoda, K., Cohen, P.,

Vetrivelan, R., Lu, G.Z., Laznik-Bogoslavski, D., Hasenfuss, S.C. and Kajimura, S., 2015. A

creatine-driven substrate cycle enhances energy expenditure and thermogenesis in beige

fat. Cell, 163(3), pp.643-655.

Länsiluoto, A., Jokipii, A. and Eklund, T. (2016). Internal control effectiveness – a clustering

approach. Managerial Auditing Journal, 31(1), pp.5-34.

14

Expenditure Cycle

Pevzner, M. and Gaynor, G. (2015). The Impact of Internal Control Weaknesses on Firms's Cash

Policies. SSRN Electronic Journal.

Wood, J. (2014). IT Auditing and Application Controls for Small and Mid-Sized Enterprises.

Wiley

15

Pevzner, M. and Gaynor, G. (2015). The Impact of Internal Control Weaknesses on Firms's Cash

Policies. SSRN Electronic Journal.

Wood, J. (2014). IT Auditing and Application Controls for Small and Mid-Sized Enterprises.

Wiley

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.