False Assurance Case Study: D-MERTON Financial Performance Analysis

VerifiedAdded on 2020/09/08

|10

|2520

|77

Report

AI Summary

This report provides a comprehensive financial analysis of D-MERTON, a company examined through the lens of the "False Assurance" case study. It delves into the responsibilities of TYSL accountants in preventing and detecting fraud, exploring ethical considerations that might affect their independence. The report identifies inherent risks, proposes control measures, and assesses the impact of product cancellations on D-MERTON's financial standing. It further evaluates the actions of the audit partner, Sarah Hancock, in fulfilling her duties. The analysis covers aspects like financial risk, competitor analysis, and the effects of cancellations on the company's financial position, providing a detailed overview of the financial dynamics within D-MERTON. The report references auditing standards and highlights the importance of ethical practices within the accounting profession.

FALSE ASSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTIONS...................................................................................................................................1

1. Provide brief introduction for these three persons..................................................................1

2. Responsibilities of TYSL accountants in relation to prevent and detect frauds and errors in

D-MERTON................................................................................................................................2

3. Three ethical which may affect independence of TYSL accountants to conduct audit of D-

MERTON and how to reduce it..................................................................................................2

4. Two inherent risks and how to control in by TYSL accountants to respond each risk in

planning and audit.......................................................................................................................3

5. How cancellation the product and system affect to D-MERTON's financial position...........4

6. Do you believe that Sarah Hancock has exercised her duty as the care audit partner ...........5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

QUESTIONS...................................................................................................................................1

1. Provide brief introduction for these three persons..................................................................1

2. Responsibilities of TYSL accountants in relation to prevent and detect frauds and errors in

D-MERTON................................................................................................................................2

3. Three ethical which may affect independence of TYSL accountants to conduct audit of D-

MERTON and how to reduce it..................................................................................................2

4. Two inherent risks and how to control in by TYSL accountants to respond each risk in

planning and audit.......................................................................................................................3

5. How cancellation the product and system affect to D-MERTON's financial position...........4

6. Do you believe that Sarah Hancock has exercised her duty as the care audit partner ...........5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

False assurance determines film drama which created to facilitate in discussion about

accountants, auditors and company directors. In this aspect, people act when they face difficult

situation (Buchanan, 2014). Present study based on D-MERTON in which different types of

financial performances has been explains with generic themes and setting. For gaining insight

knowledge of the company, it covers responsibilities of TYSL accountants to prevent and detect

frauds.

QUESTIONS

1. Provide brief introduction for these three persons

Perso

n A

He is Alex Frayn who Chief Financial Officer. As the CFO

of D-MERTON, he is responsible for the every activity of

the enterprise which performed in the past, present and

future as well. Furthermore, Alex also taking responsibility

for future financial situation and risk as well. His duty is to

predict best and effective economy strategy that forecasting

to make prediction for successful operations within the

future. In addition to this, he is also responsible towards

stakeholders due to many decisions based on the financial

information which accurate so that it require in accuracy.

Perso

n B

She is Liz Harris who is positioned on Audit Committee

chair. She is responsible in D-MERTON for oversight of

financial reporting and disclose them. Among all board

members, she responsible for making on regular basic

reports.

Perso

n C

She is Sarah Hancock who is audit partner and responsible

for signing and approving the firm audit report. She works

on financial statement of client and manages it. The audit

partners are responsible to all the clients and employees

those admitted and made financial investment.

1

False assurance determines film drama which created to facilitate in discussion about

accountants, auditors and company directors. In this aspect, people act when they face difficult

situation (Buchanan, 2014). Present study based on D-MERTON in which different types of

financial performances has been explains with generic themes and setting. For gaining insight

knowledge of the company, it covers responsibilities of TYSL accountants to prevent and detect

frauds.

QUESTIONS

1. Provide brief introduction for these three persons

Perso

n A

He is Alex Frayn who Chief Financial Officer. As the CFO

of D-MERTON, he is responsible for the every activity of

the enterprise which performed in the past, present and

future as well. Furthermore, Alex also taking responsibility

for future financial situation and risk as well. His duty is to

predict best and effective economy strategy that forecasting

to make prediction for successful operations within the

future. In addition to this, he is also responsible towards

stakeholders due to many decisions based on the financial

information which accurate so that it require in accuracy.

Perso

n B

She is Liz Harris who is positioned on Audit Committee

chair. She is responsible in D-MERTON for oversight of

financial reporting and disclose them. Among all board

members, she responsible for making on regular basic

reports.

Perso

n C

She is Sarah Hancock who is audit partner and responsible

for signing and approving the firm audit report. She works

on financial statement of client and manages it. The audit

partners are responsible to all the clients and employees

those admitted and made financial investment.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Responsibilities of TYSL accountants in relation to prevent and detect frauds and errors in D-

MERTON

The main cause of each issue is requires presenting its origin with identifying errors and

frauds. It makes strong likelihood to start operations within the organisation. In this way, internal

auditors and control managers play important role (Murphy, McAlea and Mullins, 2016). Main

question that arisises to control and help in discharging errors and frauds, there are several

elements considered in TYSL accountants. They are as follows:

Implement and strengthen physical control in the business: Main importance of

implementing physical control within the fraud prevention overlooked with many

physical barriers. Internal fraud takes place due to people who internally do not take any

responsibilities (Ferran and Ho, 2014). In order to prevent fraud, TYSL accountants has

responsibilities in D-MERTON to discover all relevant information at workplace.

Therefore, it will help to solve business issues in significantly.

Develop preventive and detective internal controls: Another responsibility of TYSL

accountant is prevention and control through development of effective functions in D-

MERTON.

Introduce fraud awareness programs in enterprise: Another responsibility of TYSL

accountant is to prevent and control frauds in D-MERTON. Therefore, it will help in

identifying errors that might create big issues in the business (Dai and Vasarhelyi, 2017).

Auditing standards: Following are auditing standards implemented in the D-MERTON'S:

ASA 100: This preamble to AUASB standards

ASA 101: It preamble to the Australian auditing standards

ASA 102: Compliance with ethical requirement to perform audits. In addition to this,

reviews and other Assurance engagement included in D-MERTON'S.

3. Three ethical which may affect independence of TYSL accountants to conduct audit of D-

MERTON and how to reduce it

Ethics defines as the primary field which could be applied in business and also important

part of it, human, study of moral values, judgements towards accountancy. It can be included in

2

MERTON

The main cause of each issue is requires presenting its origin with identifying errors and

frauds. It makes strong likelihood to start operations within the organisation. In this way, internal

auditors and control managers play important role (Murphy, McAlea and Mullins, 2016). Main

question that arisises to control and help in discharging errors and frauds, there are several

elements considered in TYSL accountants. They are as follows:

Implement and strengthen physical control in the business: Main importance of

implementing physical control within the fraud prevention overlooked with many

physical barriers. Internal fraud takes place due to people who internally do not take any

responsibilities (Ferran and Ho, 2014). In order to prevent fraud, TYSL accountants has

responsibilities in D-MERTON to discover all relevant information at workplace.

Therefore, it will help to solve business issues in significantly.

Develop preventive and detective internal controls: Another responsibility of TYSL

accountant is prevention and control through development of effective functions in D-

MERTON.

Introduce fraud awareness programs in enterprise: Another responsibility of TYSL

accountant is to prevent and control frauds in D-MERTON. Therefore, it will help in

identifying errors that might create big issues in the business (Dai and Vasarhelyi, 2017).

Auditing standards: Following are auditing standards implemented in the D-MERTON'S:

ASA 100: This preamble to AUASB standards

ASA 101: It preamble to the Australian auditing standards

ASA 102: Compliance with ethical requirement to perform audits. In addition to this,

reviews and other Assurance engagement included in D-MERTON'S.

3. Three ethical which may affect independence of TYSL accountants to conduct audit of D-

MERTON and how to reduce it

Ethics defines as the primary field which could be applied in business and also important

part of it, human, study of moral values, judgements towards accountancy. It can be included in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

professional ethics which could be expanding government group, professional organisation and

organisations (Harvey and McCrohan, 2017). Ethics are taught in the accounting courses in

higher educational institute and companies training programmes as well. Because of the diverse

range of accountancy services and recent corporate collapse, D-MERTON ethical standards are

accepted in the accounting profession. Government and organisation develop regulations and

remedies for improving ethics in the accounting profession.

Nature of the work carried by the accountant and auditors which requires high level of

ethics. Shareholders and other people of the company use this information to make informed

decision about investment (Peters and Romi, 2014). They rely on the opinion of TYSL

accountants who prepare financial statements. However, it becomes difficult to control

accountants and auditors and ensure that they consider public interest without being biased. to

consists interest of public. Further, because of the accounting scandals in businesses, critics have

been stated which need to be responded.

In order to solve this issue, new regulations need to be made for scandals that include for

corporate law economic reform. Improper leadership and ill-culture create threat and problem to

lack of competence of professional body support (Couture, 2015). In D-MERTON, TYSL

accountant require implementing principles and rules to develop international accounting

standards. They can also report to many stakeholders on several concerns in usage of rules based

accounting. In addition to this, they have to include understandability, relevance, materiality,

reliability and comparability. These practices never make international standards in the world

domain.

Regulatory compliance becoming increasing continuously and it is very complex to reach

of regulators continuous to expand.

Regulatory compliance and reporting:

Regulatory compliance with the financial and non financial reporting requirement.

Risk effectively managed with regulatory risk.

Corporate governance is strong.

3

organisations (Harvey and McCrohan, 2017). Ethics are taught in the accounting courses in

higher educational institute and companies training programmes as well. Because of the diverse

range of accountancy services and recent corporate collapse, D-MERTON ethical standards are

accepted in the accounting profession. Government and organisation develop regulations and

remedies for improving ethics in the accounting profession.

Nature of the work carried by the accountant and auditors which requires high level of

ethics. Shareholders and other people of the company use this information to make informed

decision about investment (Peters and Romi, 2014). They rely on the opinion of TYSL

accountants who prepare financial statements. However, it becomes difficult to control

accountants and auditors and ensure that they consider public interest without being biased. to

consists interest of public. Further, because of the accounting scandals in businesses, critics have

been stated which need to be responded.

In order to solve this issue, new regulations need to be made for scandals that include for

corporate law economic reform. Improper leadership and ill-culture create threat and problem to

lack of competence of professional body support (Couture, 2015). In D-MERTON, TYSL

accountant require implementing principles and rules to develop international accounting

standards. They can also report to many stakeholders on several concerns in usage of rules based

accounting. In addition to this, they have to include understandability, relevance, materiality,

reliability and comparability. These practices never make international standards in the world

domain.

Regulatory compliance becoming increasing continuously and it is very complex to reach

of regulators continuous to expand.

Regulatory compliance and reporting:

Regulatory compliance with the financial and non financial reporting requirement.

Risk effectively managed with regulatory risk.

Corporate governance is strong.

3

Auditing and assurance board of standards: It is the independent, statutory agency who

responsible to enhance standards and guidance for auditors.

Australian accounting standards: It makes standards of accounting for private, public and non

profit sectors. They are also participates in respect to formulate international standards of

accounting.

Australian financial security authority: It provides improved financial outcomes for several

people such as customers, business and community. Security laws, regulations and personal

insolvency develop effectively.

4. Two inherent risks and how to control in by TYSL accountants to respond each risk in

planning and audit

With the help of standards, concept will be develop that the auditor required to

understand of business risk to extent relevant to the financial statements. In audit plan of D-

MERTON, TYSL accountants facing issue in making decisions, programs and procedures.

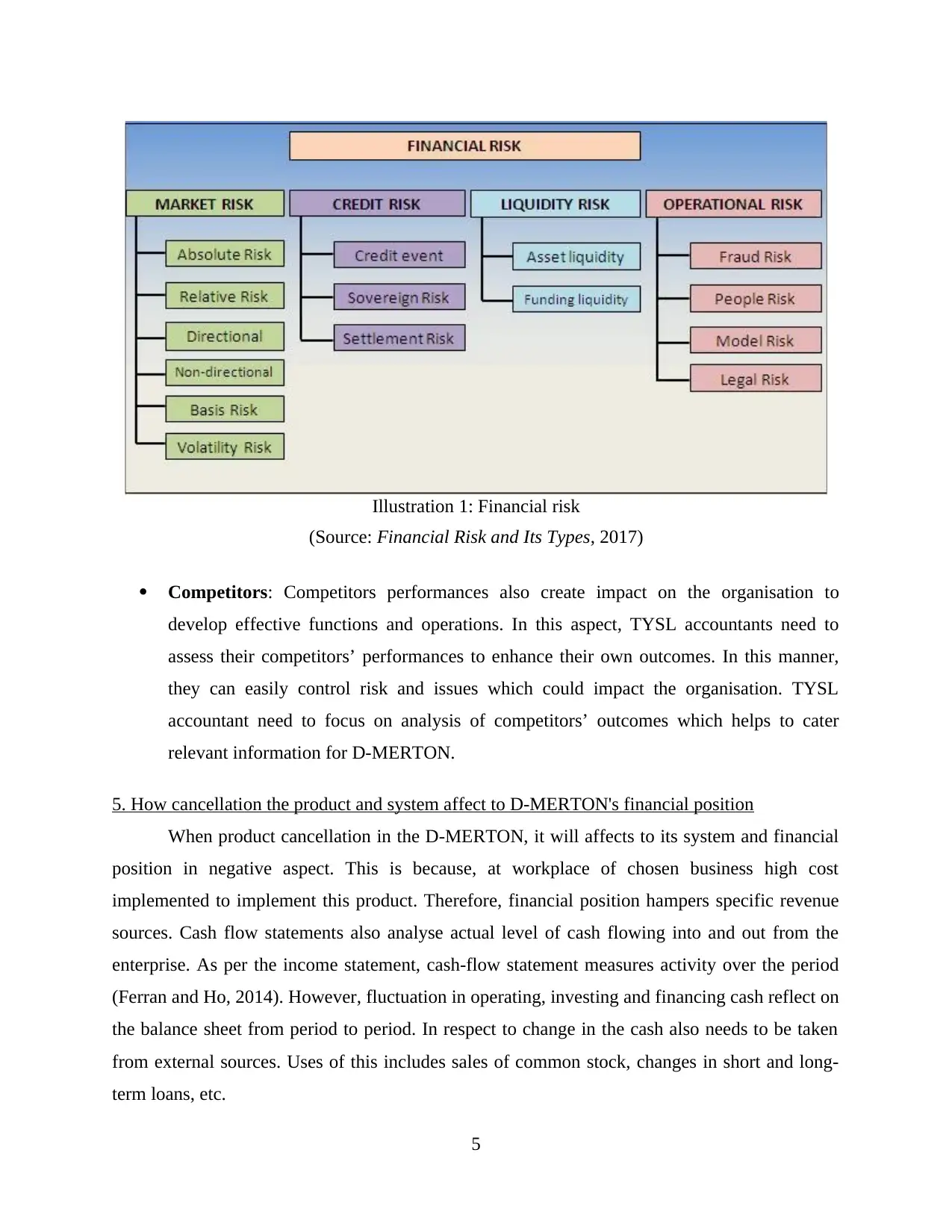

Following are two main risk take place in business:

Financial risk: There is high financial risk because standards are continuously changed

and implementation of IT system also needed high cost (Buchanan, 2014). Therefore, it is

the biggest issue which is faced by TYSL accountants in D-MERTON. In order to solve

this issue, new investment need to be implemented by the company. Therefore, it will

help in making decisions and respond towards problem in systematic way. In this risk,

TYSL accountants need to arrange fund to reduce financial risk from the business unit.

Therefore, it will be profitable to supply relevant things at workplace. There are different

types of financial risks, can be occurs at workplace of chosen business. They are as

follows:

4

responsible to enhance standards and guidance for auditors.

Australian accounting standards: It makes standards of accounting for private, public and non

profit sectors. They are also participates in respect to formulate international standards of

accounting.

Australian financial security authority: It provides improved financial outcomes for several

people such as customers, business and community. Security laws, regulations and personal

insolvency develop effectively.

4. Two inherent risks and how to control in by TYSL accountants to respond each risk in

planning and audit

With the help of standards, concept will be develop that the auditor required to

understand of business risk to extent relevant to the financial statements. In audit plan of D-

MERTON, TYSL accountants facing issue in making decisions, programs and procedures.

Following are two main risk take place in business:

Financial risk: There is high financial risk because standards are continuously changed

and implementation of IT system also needed high cost (Buchanan, 2014). Therefore, it is

the biggest issue which is faced by TYSL accountants in D-MERTON. In order to solve

this issue, new investment need to be implemented by the company. Therefore, it will

help in making decisions and respond towards problem in systematic way. In this risk,

TYSL accountants need to arrange fund to reduce financial risk from the business unit.

Therefore, it will be profitable to supply relevant things at workplace. There are different

types of financial risks, can be occurs at workplace of chosen business. They are as

follows:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Competitors: Competitors performances also create impact on the organisation to

develop effective functions and operations. In this aspect, TYSL accountants need to

assess their competitors’ performances to enhance their own outcomes. In this manner,

they can easily control risk and issues which could impact the organisation. TYSL

accountant need to focus on analysis of competitors’ outcomes which helps to cater

relevant information for D-MERTON.

5. How cancellation the product and system affect to D-MERTON's financial position

When product cancellation in the D-MERTON, it will affects to its system and financial

position in negative aspect. This is because, at workplace of chosen business high cost

implemented to implement this product. Therefore, financial position hampers specific revenue

sources. Cash flow statements also analyse actual level of cash flowing into and out from the

enterprise. As per the income statement, cash-flow statement measures activity over the period

(Ferran and Ho, 2014). However, fluctuation in operating, investing and financing cash reflect on

the balance sheet from period to period. In respect to change in the cash also needs to be taken

from external sources. Uses of this includes sales of common stock, changes in short and long-

term loans, etc.

5

Illustration 1: Financial risk

(Source: Financial Risk and Its Types, 2017)

develop effective functions and operations. In this aspect, TYSL accountants need to

assess their competitors’ performances to enhance their own outcomes. In this manner,

they can easily control risk and issues which could impact the organisation. TYSL

accountant need to focus on analysis of competitors’ outcomes which helps to cater

relevant information for D-MERTON.

5. How cancellation the product and system affect to D-MERTON's financial position

When product cancellation in the D-MERTON, it will affects to its system and financial

position in negative aspect. This is because, at workplace of chosen business high cost

implemented to implement this product. Therefore, financial position hampers specific revenue

sources. Cash flow statements also analyse actual level of cash flowing into and out from the

enterprise. As per the income statement, cash-flow statement measures activity over the period

(Ferran and Ho, 2014). However, fluctuation in operating, investing and financing cash reflect on

the balance sheet from period to period. In respect to change in the cash also needs to be taken

from external sources. Uses of this includes sales of common stock, changes in short and long-

term loans, etc.

5

Illustration 1: Financial risk

(Source: Financial Risk and Its Types, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In addition to this, balance sheet also provide summary that make changes in profits and

revenue due to decreasing or increasing of assets and liabilities. In order to generate more profits,

each product offer to consumers. With regard to supply products, demand and design plans

related and based on the factors of consumer preferences (Harvey and McCrohan, 2017). With

cancellation of products, D-MERTON also loss opportunity for sales. These circumstances have

impact on the group performances and financial position.

6. Do you believe that Sarah Hancock has exercised her duty as the care audit partner

Yes, I believe that Sarah Hancock exercised her responsibility as the care audit partner.

She is responsible for auditing and making financial report to send it to client. She makes

financial statements for clients and managers (Buchanan, 2014). In this way, she performs

several responsibilities and duties which are explained below:

Plan and manage audit engagement: In respect to ascertain effective functions, Sarah

Hancock focusing on plan and managing audit programs in D-MERTON. In this way, she

fulfils her duty in significant manner as care audit partner. It is helpful to attain more

effective results at workplace for audit. In this duty, she exercised continuousl to do work

to meet with client requirement.

Understand client business and provide audit services to meet their expectations:

With the help of understanding client business and providing them audit services, Sarah

Hancock can also work in D-MERTON to meet client expectations. It helps to understand

customer expectations to enhance profitability (Murphy, McAlea and Mullins, 2016).

Maintain up to date knowledge for company standards, policies and regulations:

Sarah Hancock also require maintaining their knowledge for ascertain company

standards, policies and regulations as well. It helps to develop business performances of

D-MERTON.

Develop innovative ideas to extent services for client: Sarah also possess some

innovative ideas through which she can extent services for client. It will help to

understand customer requirement to meet its objectives and goals (Harvey and

McCrohan, 2017). In D-MERTON, innovative ideas help to understand the services

which are required by client.

Attend meeting with clients as per industry trends: According to industry trends, Sarah

Hancock need to arrange meeting with clients. It will help to understand their

6

revenue due to decreasing or increasing of assets and liabilities. In order to generate more profits,

each product offer to consumers. With regard to supply products, demand and design plans

related and based on the factors of consumer preferences (Harvey and McCrohan, 2017). With

cancellation of products, D-MERTON also loss opportunity for sales. These circumstances have

impact on the group performances and financial position.

6. Do you believe that Sarah Hancock has exercised her duty as the care audit partner

Yes, I believe that Sarah Hancock exercised her responsibility as the care audit partner.

She is responsible for auditing and making financial report to send it to client. She makes

financial statements for clients and managers (Buchanan, 2014). In this way, she performs

several responsibilities and duties which are explained below:

Plan and manage audit engagement: In respect to ascertain effective functions, Sarah

Hancock focusing on plan and managing audit programs in D-MERTON. In this way, she

fulfils her duty in significant manner as care audit partner. It is helpful to attain more

effective results at workplace for audit. In this duty, she exercised continuousl to do work

to meet with client requirement.

Understand client business and provide audit services to meet their expectations:

With the help of understanding client business and providing them audit services, Sarah

Hancock can also work in D-MERTON to meet client expectations. It helps to understand

customer expectations to enhance profitability (Murphy, McAlea and Mullins, 2016).

Maintain up to date knowledge for company standards, policies and regulations:

Sarah Hancock also require maintaining their knowledge for ascertain company

standards, policies and regulations as well. It helps to develop business performances of

D-MERTON.

Develop innovative ideas to extent services for client: Sarah also possess some

innovative ideas through which she can extent services for client. It will help to

understand customer requirement to meet its objectives and goals (Harvey and

McCrohan, 2017). In D-MERTON, innovative ideas help to understand the services

which are required by client.

Attend meeting with clients as per industry trends: According to industry trends, Sarah

Hancock need to arrange meeting with clients. It will help to understand their

6

requirement and behaviour towards business products. Hence, she can work effectively in

making their financial data (Audit Partner Responsibilities and Duties, 2017). From the

above duty, it can be stated that Sarah work effectively her duties to make financial

reports and outcomes.

CONCLUSION

From the above report, it can be concluded that in D-MERTON, there are several people

work together for developing results and assess performances at workplace. Furthermore, it

summarized about responsibilities of accountants also explains in the present business to analysis

performances Moreover, it articulated about duty of audit partner to make effective functioning

at workplace.

7

making their financial data (Audit Partner Responsibilities and Duties, 2017). From the

above duty, it can be stated that Sarah work effectively her duties to make financial

reports and outcomes.

CONCLUSION

From the above report, it can be concluded that in D-MERTON, there are several people

work together for developing results and assess performances at workplace. Furthermore, it

summarized about responsibilities of accountants also explains in the present business to analysis

performances Moreover, it articulated about duty of audit partner to make effective functioning

at workplace.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Buchanan, J. M., 2014. Public finance in democratic process: Fiscal institutions and individual

choice. UNC Press Books.

Couture, W. G., 2015. False Statements of Belief as Securities Fraud. Law Review, 43, p.351.

Dai, J. and Vasarhelyi, M. A., 2017. Towards Blockchain-based Accounting and Assurance.

Journal of Information Systems.

Ferran, E. and Ho, L. C., 2014. Principles of corporate finance law. Oxford University Press.

Harvey, J. W. and McCrohan, K. F., 2017. Improving AACSB Assurance of Learning With

Importance-Performance and Learning Growth: A Case Study. Marketing Education

Review. pp.1-15.

Murphy, F., McAlea, E. M. and Mullins, M. eds., 2016. Managing Risk in Nanotechnology:

Topics in Governance, Assurance and Transfer. Springer.

Peters, G. F. and Romi, A. M., 2014. The association between sustainability governance

characteristics and the assurance of corporate sustainability reports. Auditing: A Journal

of Practice & Theory. 34(1). pp.163-198.

Online

Audit Partner Responsibilities and Duties, 2017. [Online] Available through:

<https://www.resumebaking.com/job-responsibilities/audit-partner-responsibilities/>.

[Accessed on 12th September 2017].

Financial Risk and Its Types, 2017. [Online] Available through:

<https://www.simplilearn.com/financial-risk-and-types-rar131-article>. [Accessed on 12th

September 2017].

8

Books and Journals

Buchanan, J. M., 2014. Public finance in democratic process: Fiscal institutions and individual

choice. UNC Press Books.

Couture, W. G., 2015. False Statements of Belief as Securities Fraud. Law Review, 43, p.351.

Dai, J. and Vasarhelyi, M. A., 2017. Towards Blockchain-based Accounting and Assurance.

Journal of Information Systems.

Ferran, E. and Ho, L. C., 2014. Principles of corporate finance law. Oxford University Press.

Harvey, J. W. and McCrohan, K. F., 2017. Improving AACSB Assurance of Learning With

Importance-Performance and Learning Growth: A Case Study. Marketing Education

Review. pp.1-15.

Murphy, F., McAlea, E. M. and Mullins, M. eds., 2016. Managing Risk in Nanotechnology:

Topics in Governance, Assurance and Transfer. Springer.

Peters, G. F. and Romi, A. M., 2014. The association between sustainability governance

characteristics and the assurance of corporate sustainability reports. Auditing: A Journal

of Practice & Theory. 34(1). pp.163-198.

Online

Audit Partner Responsibilities and Duties, 2017. [Online] Available through:

<https://www.resumebaking.com/job-responsibilities/audit-partner-responsibilities/>.

[Accessed on 12th September 2017].

Financial Risk and Its Types, 2017. [Online] Available through:

<https://www.simplilearn.com/financial-risk-and-types-rar131-article>. [Accessed on 12th

September 2017].

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.