Fannie Mae Risk Assessment and Stakeholder Analysis Report

VerifiedAdded on 2023/06/03

|37

|5045

|433

Report

AI Summary

This report provides a comprehensive analysis of Fannie Mae's risk management practices, focusing on its role in the American mortgage market. It begins with an overview of the company, including its business operations, share price performance, and competitive environment. The report then delves into the identification of key stakeholders, categorizing them as internal and external, and assessing their influence and interests. A significant portion of the report is dedicated to a detailed risk assessment, outlining a risk model with twenty identified risks, along with a diagram of the top ten risks and a radar diagram. The risks include changes in government legislation, economic weakening, and data theft, among others. For each risk, the report evaluates its potential impact on the business and proposes possible mitigation actions. The report concludes with an assessment of the company's risk culture and provides recommendations for investors, suggesting a long-term investment strategy. The analysis utilizes various financial data, graphs, and tables to support the findings.

Running head: RISK MANAGEMENT

Risk Management

Name of the Student:

Name of the University:

Author Note:

Risk Management

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

RISK MANAGEMENT

Executive Summary:

The reports that Fannie Mae plays a very important role in ensuring liquidity of the American

mortgage market. It also ensures that the mortgage investors are able to invest in the mortgage

market which in turn boosts the securities market. The study then goes on to show the different

types of risks Fannie Mae encounters. The risk culture of the company is average which means

that investors should invest in the shares only on long term basis.

RISK MANAGEMENT

Executive Summary:

The reports that Fannie Mae plays a very important role in ensuring liquidity of the American

mortgage market. It also ensures that the mortgage investors are able to invest in the mortgage

market which in turn boosts the securities market. The study then goes on to show the different

types of risks Fannie Mae encounters. The risk culture of the company is average which means

that investors should invest in the shares only on long term basis.

2

RISK MANAGEMENT

Table of Contents

1. Company overview:.....................................................................................................................3

Location of business and operation scope:......................................................................................3

Business mix, operating hours:........................................................................................................3

Share price:......................................................................................................................................3

Share price comparison with two similar companies:.....................................................................5

Debt carried by the company:..........................................................................................................6

Key Stakeholders:............................................................................................................................6

Established date:..............................................................................................................................7

Competitive environment-low/medium/high:.................................................................................7

Other relevant information:.............................................................................................................7

2. Key stakeholders:.........................................................................................................................7

3. Finding/Section Result:.............................................................................................................10

Risk model of 20 risks:..................................................................................................................10

Diagram of top ten risks:...........................................................................................................26

Radar Diagram with at least 7 identified criteria relating to analysis:..........................................30

4. Report Conclusion:....................................................................................................................31

References:....................................................................................................................................33

RISK MANAGEMENT

Table of Contents

1. Company overview:.....................................................................................................................3

Location of business and operation scope:......................................................................................3

Business mix, operating hours:........................................................................................................3

Share price:......................................................................................................................................3

Share price comparison with two similar companies:.....................................................................5

Debt carried by the company:..........................................................................................................6

Key Stakeholders:............................................................................................................................6

Established date:..............................................................................................................................7

Competitive environment-low/medium/high:.................................................................................7

Other relevant information:.............................................................................................................7

2. Key stakeholders:.........................................................................................................................7

3. Finding/Section Result:.............................................................................................................10

Risk model of 20 risks:..................................................................................................................10

Diagram of top ten risks:...........................................................................................................26

Radar Diagram with at least 7 identified criteria relating to analysis:..........................................30

4. Report Conclusion:....................................................................................................................31

References:....................................................................................................................................33

You're viewing a preview

Unlock full access by subscribing today!

3

RISK MANAGEMENT

1. Company overview:

The Federal National Mortgage Association, FNMA or Fannie Mae is a publicly

traded American company and sponsored by the Government of the US, which invests in the

secondary mortgage market by pooling different types of mortgage loans. The loans are traded in

the secondary market in the forms of mortgage back securities of different types like shares and

bonds (Fanniemae.com, 2019). The body’s main function is to sell these mortgage backed

securities to a large pool of investors which ensure more inflow of cash in the mortgage markets,

thus curbing the impact of thrift investment companies on the American economy

(Krishnamurthy, 2017).

Location of business and operation scope:

Fannie Mae is headquartered in Washington D.C. and has its branches Virginia, Atlanta,

Chicago, Plano, Maryland, Philadelphia, Los Angeles, Massachusetts, California and New York.

The scope of operation of Fannie Mae consists of two main pillars namely, strengthening

the secondary mortgage market in the US. This ensuring liquidity to the participants in the

securities market backed by mortgage (Adrian & Jones, 2018).

Business mix, operating hours:

The business mix of Fannie Mae consists of mortgage products for households and

companies seeking to mortgage their assets to acquire financial resources. The operating hours of

Fannie Mae range from 8 am to 8 pm on Monday to Friday. The customer care of the company

are open from 9 am to 5 pm.

RISK MANAGEMENT

1. Company overview:

The Federal National Mortgage Association, FNMA or Fannie Mae is a publicly

traded American company and sponsored by the Government of the US, which invests in the

secondary mortgage market by pooling different types of mortgage loans. The loans are traded in

the secondary market in the forms of mortgage back securities of different types like shares and

bonds (Fanniemae.com, 2019). The body’s main function is to sell these mortgage backed

securities to a large pool of investors which ensure more inflow of cash in the mortgage markets,

thus curbing the impact of thrift investment companies on the American economy

(Krishnamurthy, 2017).

Location of business and operation scope:

Fannie Mae is headquartered in Washington D.C. and has its branches Virginia, Atlanta,

Chicago, Plano, Maryland, Philadelphia, Los Angeles, Massachusetts, California and New York.

The scope of operation of Fannie Mae consists of two main pillars namely, strengthening

the secondary mortgage market in the US. This ensuring liquidity to the participants in the

securities market backed by mortgage (Adrian & Jones, 2018).

Business mix, operating hours:

The business mix of Fannie Mae consists of mortgage products for households and

companies seeking to mortgage their assets to acquire financial resources. The operating hours of

Fannie Mae range from 8 am to 8 pm on Monday to Friday. The customer care of the company

are open from 9 am to 5 pm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

RISK MANAGEMENT

Share price:

The share price of as shown in the graph below shows that company enjoys a very

unstable position in the American stock market. The share price of the company reached a high

in 2014 after which it followed a bearish trend intercepted with period rises. The share price of

the company again rose in 2017 after which its performance fell. The unstable trend of the share

price of Fannie Mae continues into 2019 and is showing signs of recovering.

Figure 1. Graoph showing share price of Fannie Mae for 5years

(Source: Bloomberg.com, 2019)

RISK MANAGEMENT

Share price:

The share price of as shown in the graph below shows that company enjoys a very

unstable position in the American stock market. The share price of the company reached a high

in 2014 after which it followed a bearish trend intercepted with period rises. The share price of

the company again rose in 2017 after which its performance fell. The unstable trend of the share

price of Fannie Mae continues into 2019 and is showing signs of recovering.

Figure 1. Graoph showing share price of Fannie Mae for 5years

(Source: Bloomberg.com, 2019)

5

RISK MANAGEMENT

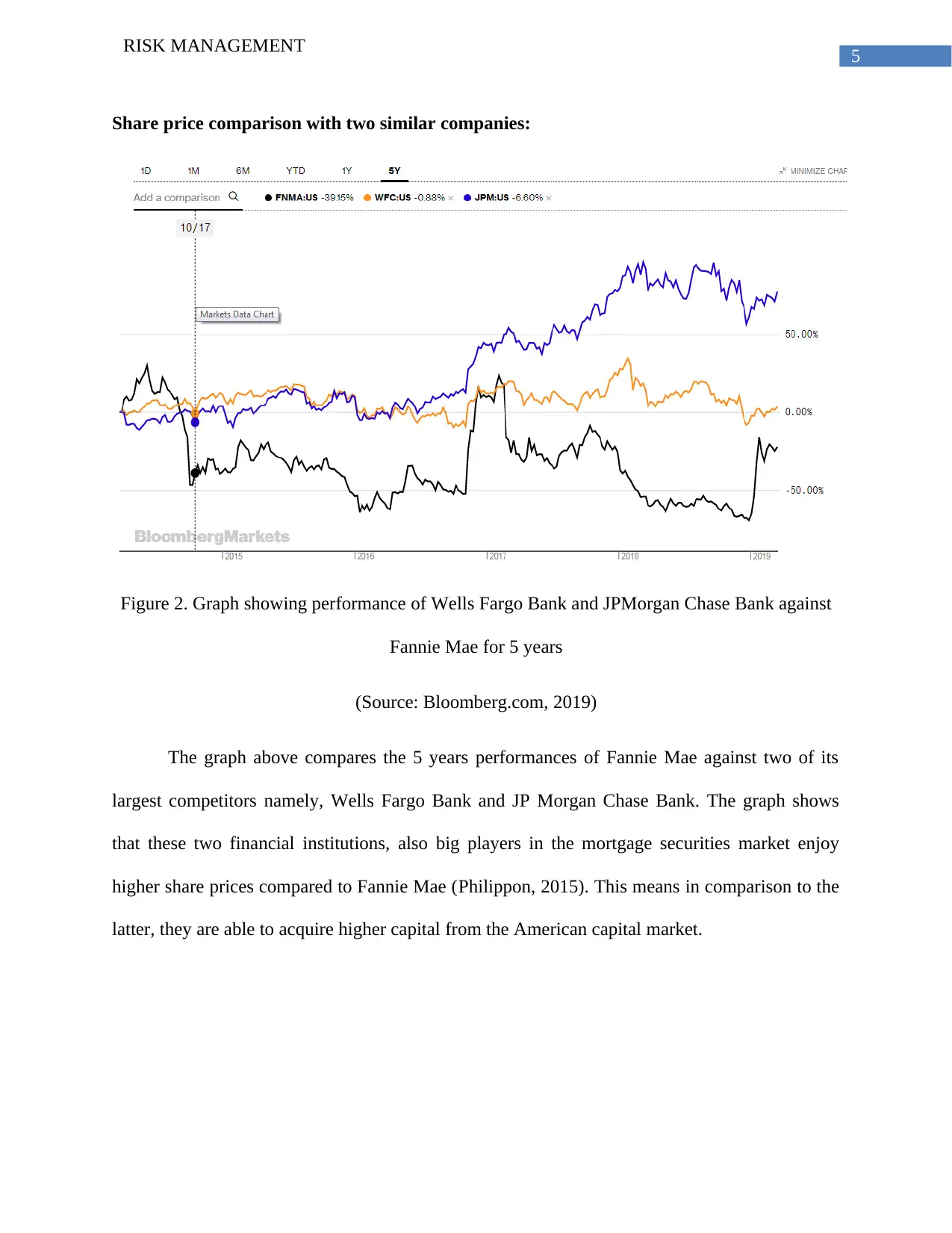

Share price comparison with two similar companies:

Figure 2. Graph showing performance of Wells Fargo Bank and JPMorgan Chase Bank against

Fannie Mae for 5 years

(Source: Bloomberg.com, 2019)

The graph above compares the 5 years performances of Fannie Mae against two of its

largest competitors namely, Wells Fargo Bank and JP Morgan Chase Bank. The graph shows

that these two financial institutions, also big players in the mortgage securities market enjoy

higher share prices compared to Fannie Mae (Philippon, 2015). This means in comparison to the

latter, they are able to acquire higher capital from the American capital market.

RISK MANAGEMENT

Share price comparison with two similar companies:

Figure 2. Graph showing performance of Wells Fargo Bank and JPMorgan Chase Bank against

Fannie Mae for 5 years

(Source: Bloomberg.com, 2019)

The graph above compares the 5 years performances of Fannie Mae against two of its

largest competitors namely, Wells Fargo Bank and JP Morgan Chase Bank. The graph shows

that these two financial institutions, also big players in the mortgage securities market enjoy

higher share prices compared to Fannie Mae (Philippon, 2015). This means in comparison to the

latter, they are able to acquire higher capital from the American capital market.

You're viewing a preview

Unlock full access by subscribing today!

6

RISK MANAGEMENT

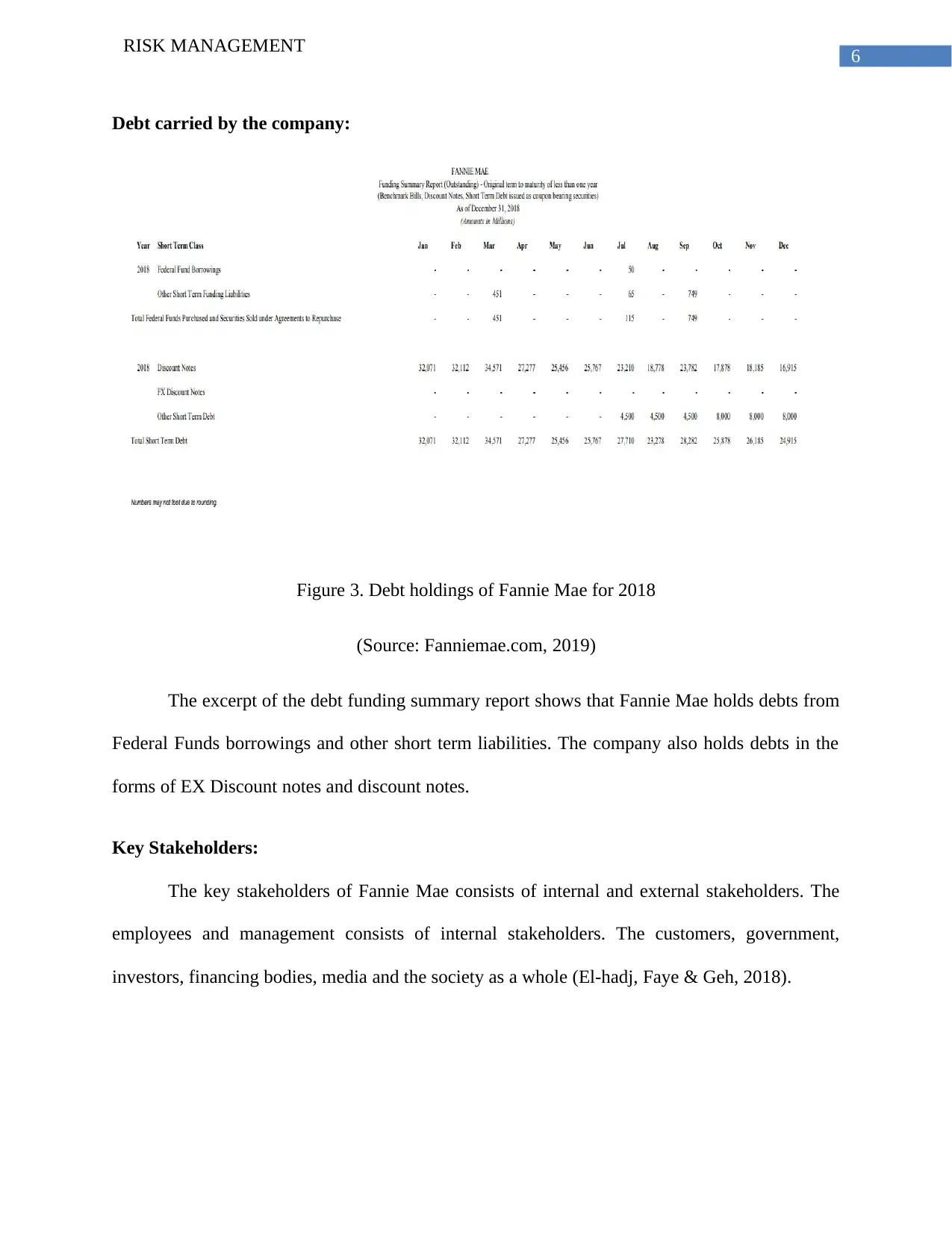

Debt carried by the company:

Figure 3. Debt holdings of Fannie Mae for 2018

(Source: Fanniemae.com, 2019)

The excerpt of the debt funding summary report shows that Fannie Mae holds debts from

Federal Funds borrowings and other short term liabilities. The company also holds debts in the

forms of EX Discount notes and discount notes.

Key Stakeholders:

The key stakeholders of Fannie Mae consists of internal and external stakeholders. The

employees and management consists of internal stakeholders. The customers, government,

investors, financing bodies, media and the society as a whole (El-hadj, Faye & Geh, 2018).

RISK MANAGEMENT

Debt carried by the company:

Figure 3. Debt holdings of Fannie Mae for 2018

(Source: Fanniemae.com, 2019)

The excerpt of the debt funding summary report shows that Fannie Mae holds debts from

Federal Funds borrowings and other short term liabilities. The company also holds debts in the

forms of EX Discount notes and discount notes.

Key Stakeholders:

The key stakeholders of Fannie Mae consists of internal and external stakeholders. The

employees and management consists of internal stakeholders. The customers, government,

investors, financing bodies, media and the society as a whole (El-hadj, Faye & Geh, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

RISK MANAGEMENT

Established date:

The date of establishment of Fannie Mae was 1938 which means that the company is

over 80 years in business till 2019.

Competitive environment-low/medium/high:

The competitive environment of Fannie Mae is highly competitive. This is evident from

that fact the American mortgage market is dominated by organisations like Wells Fargo and JP

Morgan Chase Bank Limited (Jarzabkowski et al. 2018).

Other relevant information:

Fannie Mae ensures liquidity in the American mortgage market by ensure economic

development in the market. This is because by investing the mortgage market, the company

curbs the impact of the small mortgage companies from duping investor (Betts, 2018).

2. Key stakeholders:

Influenc

e

High

KEEP

SATISFIED(Government,

investors, stock

exchanges)

MANAGE

CLOSELY(Management,

employees, customers

Low

MONITOR (minimum

effort)

Financing bodies, banks

KEEP INFORMED(Media,

society)

Low High

Interests

Figure 4. Table showing the main stakeholders of Fannie Mae

(Source: Author)

RISK MANAGEMENT

Established date:

The date of establishment of Fannie Mae was 1938 which means that the company is

over 80 years in business till 2019.

Competitive environment-low/medium/high:

The competitive environment of Fannie Mae is highly competitive. This is evident from

that fact the American mortgage market is dominated by organisations like Wells Fargo and JP

Morgan Chase Bank Limited (Jarzabkowski et al. 2018).

Other relevant information:

Fannie Mae ensures liquidity in the American mortgage market by ensure economic

development in the market. This is because by investing the mortgage market, the company

curbs the impact of the small mortgage companies from duping investor (Betts, 2018).

2. Key stakeholders:

Influenc

e

High

KEEP

SATISFIED(Government,

investors, stock

exchanges)

MANAGE

CLOSELY(Management,

employees, customers

Low

MONITOR (minimum

effort)

Financing bodies, banks

KEEP INFORMED(Media,

society)

Low High

Interests

Figure 4. Table showing the main stakeholders of Fannie Mae

(Source: Author)

8

RISK MANAGEMENT

Fannie Mae being a leading mortgage financing and responsible for ensure liquidity in

the mortgage market by pooling in other types of assets like shares and bonds, comes under

impacts of several groups of stakeholders consisting of groups as well as individuals. It would be

prudent to divide the stakeholders impacting Fannie Mae into two broad groups namely internal

and external stakeholders (Trevino & Nelson, 2016). The internal stakeholders of Fannie Mae

consist of the apex management under the leadership of the CEO and the employees. The

‘Corporate Governance’ page of the body clearly mentions that the board of directors of the

company is constituted by Federal Housing Finance Agency which means that the Government

of the US is also an internal stakeholder in this case (Fhfa.gov, 2019). The responsibility of the

management board is to form strategies under governance of the FHFA. The interests of the

management lies in generating high profits and getting more support from the government. The

next group of stakeholders consist of employees who actually implement the instructions of the

managements. De Silva, Howells and Meyer (2018) mention that the responsibility of the

employees of lie in providing appropriate mortgage products to clients to allow them to invest in

assets. The responsibilities of the employees also pertains to operating in the American financial

market in compliance with legislations and ethics. The interests of the employees lie in gaining

professional developmental opportunities. Khan, Lalitha and Omonaiye (2017) mention that

employees are the internal customers whose interests have to be upheld in order to ensure

seamless service provision to the external customers. Thus, in this respect it can be pointed out

that Fannie Mae should ensure it provides sufficient professional developmental opportunities to

its employees like salary hikes, promotions and paid family trips.

The first external stakeholder group which Fannie has to consider and manage closely are

the investors in the mortgage investors both individuals and institutions. Aalbers (2016)

RISK MANAGEMENT

Fannie Mae being a leading mortgage financing and responsible for ensure liquidity in

the mortgage market by pooling in other types of assets like shares and bonds, comes under

impacts of several groups of stakeholders consisting of groups as well as individuals. It would be

prudent to divide the stakeholders impacting Fannie Mae into two broad groups namely internal

and external stakeholders (Trevino & Nelson, 2016). The internal stakeholders of Fannie Mae

consist of the apex management under the leadership of the CEO and the employees. The

‘Corporate Governance’ page of the body clearly mentions that the board of directors of the

company is constituted by Federal Housing Finance Agency which means that the Government

of the US is also an internal stakeholder in this case (Fhfa.gov, 2019). The responsibility of the

management board is to form strategies under governance of the FHFA. The interests of the

management lies in generating high profits and getting more support from the government. The

next group of stakeholders consist of employees who actually implement the instructions of the

managements. De Silva, Howells and Meyer (2018) mention that the responsibility of the

employees of lie in providing appropriate mortgage products to clients to allow them to invest in

assets. The responsibilities of the employees also pertains to operating in the American financial

market in compliance with legislations and ethics. The interests of the employees lie in gaining

professional developmental opportunities. Khan, Lalitha and Omonaiye (2017) mention that

employees are the internal customers whose interests have to be upheld in order to ensure

seamless service provision to the external customers. Thus, in this respect it can be pointed out

that Fannie Mae should ensure it provides sufficient professional developmental opportunities to

its employees like salary hikes, promotions and paid family trips.

The first external stakeholder group which Fannie has to consider and manage closely are

the investors in the mortgage investors both individuals and institutions. Aalbers (2016)

You're viewing a preview

Unlock full access by subscribing today!

9

RISK MANAGEMENT

mentions that the main function of the mortgage market lies in making capital available to

mortgagers against the property mortgaged. Korschun (2015) in this respect mentions that the

investors who invest in the mortgage and real estate are important external stakeholders. Fannie

Mae has to ensure that it is able to ensure high liquidity to in the mortgage market to ensure high

ROI to these investors. The next group of stakeholders consists of the banks which provide

gateway for the financial transaction, thus actually ensuring the liquidity in the mortgage market.

The responsibility of Fannie Mae is to protect the interests of the banks by investing in their

products, thus generating revenue for the latter (Oatley & Petrova, 2016). The next external

stakeholders which Fannie Mae should consider is the stock exchange. The stock exchanges like

OTC Market provide platform to the company to float its shares and raise capital

(Otcmarkets.com, 2019). Fannie Mae msut protect the interests of the OTC Market by complying

with the policies and directives laid down by the body. The next important group of stakeholders

which Fannie Mae should take into account is investors investing in its shares floated on the

stock exchange. Huang et al.(2016) mention in this respect that companies like Fannie Mae

should protect the interests of the investors by giving them high returns on the investments.

Similarly, the shareholders should encourage important decision making of the board of

directors. The media as mentioned by Cho, Furey and Mohr (2017) constitute an important

stakeholder group since it enables the company spread awareness about its decisions among the

other stakeholders like investors and clients. Thus, it can be inferred from the discussion that

Fannie Mae supports a large group of stakeholders and should operate in order to protect their

interests (Navarro, Moreno and Al-Sumait, 2017).

RISK MANAGEMENT

mentions that the main function of the mortgage market lies in making capital available to

mortgagers against the property mortgaged. Korschun (2015) in this respect mentions that the

investors who invest in the mortgage and real estate are important external stakeholders. Fannie

Mae has to ensure that it is able to ensure high liquidity to in the mortgage market to ensure high

ROI to these investors. The next group of stakeholders consists of the banks which provide

gateway for the financial transaction, thus actually ensuring the liquidity in the mortgage market.

The responsibility of Fannie Mae is to protect the interests of the banks by investing in their

products, thus generating revenue for the latter (Oatley & Petrova, 2016). The next external

stakeholders which Fannie Mae should consider is the stock exchange. The stock exchanges like

OTC Market provide platform to the company to float its shares and raise capital

(Otcmarkets.com, 2019). Fannie Mae msut protect the interests of the OTC Market by complying

with the policies and directives laid down by the body. The next important group of stakeholders

which Fannie Mae should take into account is investors investing in its shares floated on the

stock exchange. Huang et al.(2016) mention in this respect that companies like Fannie Mae

should protect the interests of the investors by giving them high returns on the investments.

Similarly, the shareholders should encourage important decision making of the board of

directors. The media as mentioned by Cho, Furey and Mohr (2017) constitute an important

stakeholder group since it enables the company spread awareness about its decisions among the

other stakeholders like investors and clients. Thus, it can be inferred from the discussion that

Fannie Mae supports a large group of stakeholders and should operate in order to protect their

interests (Navarro, Moreno and Al-Sumait, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

RISK MANAGEMENT

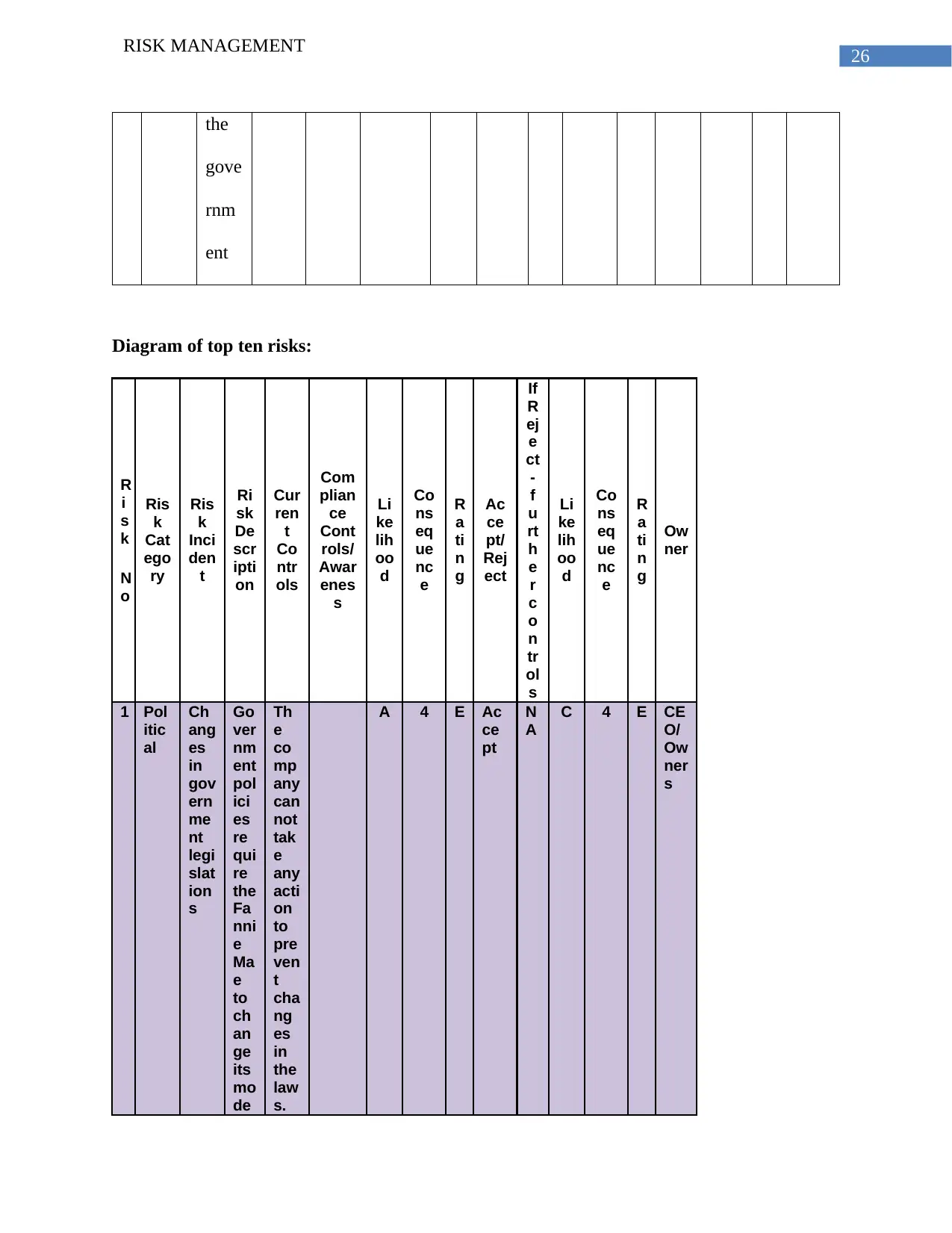

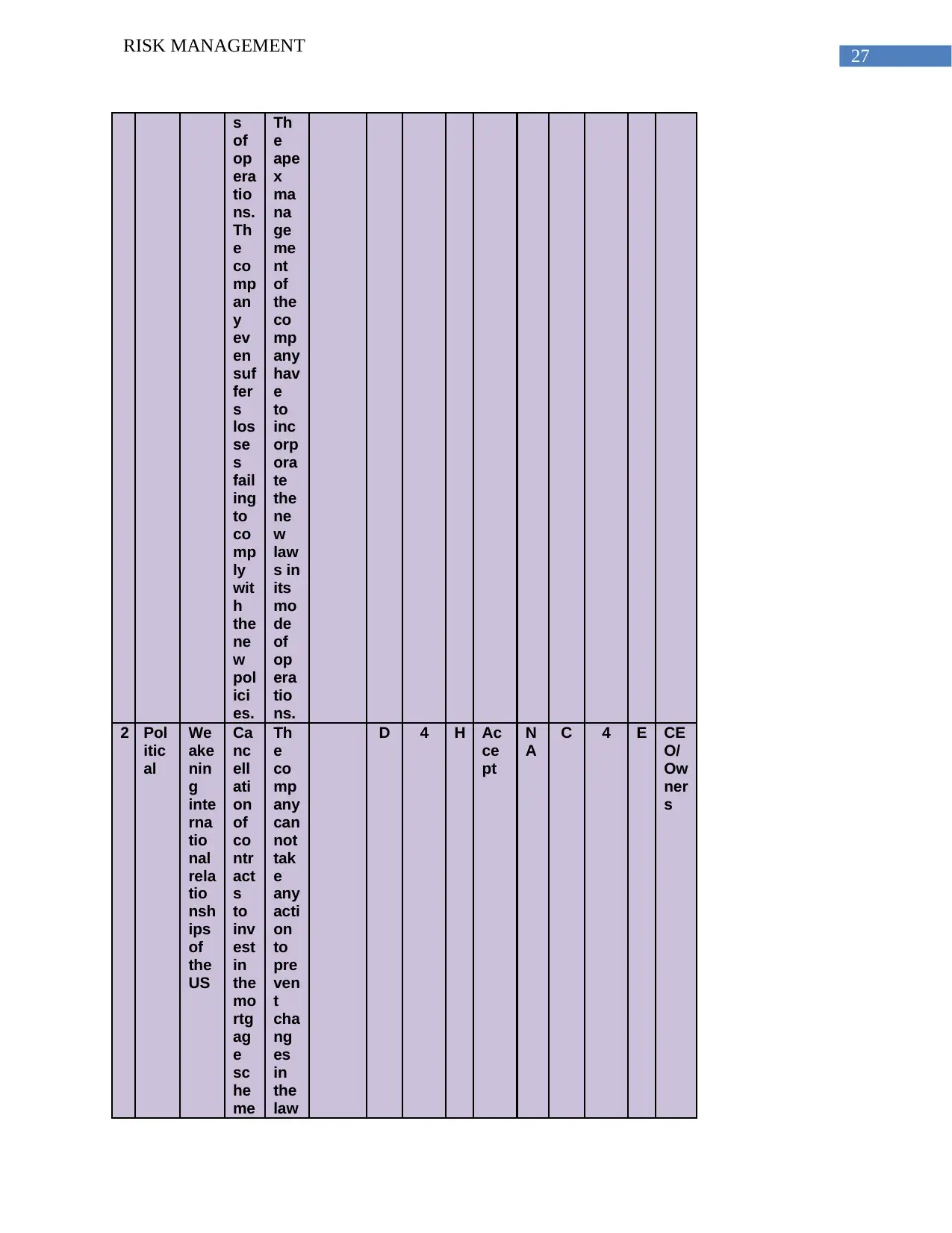

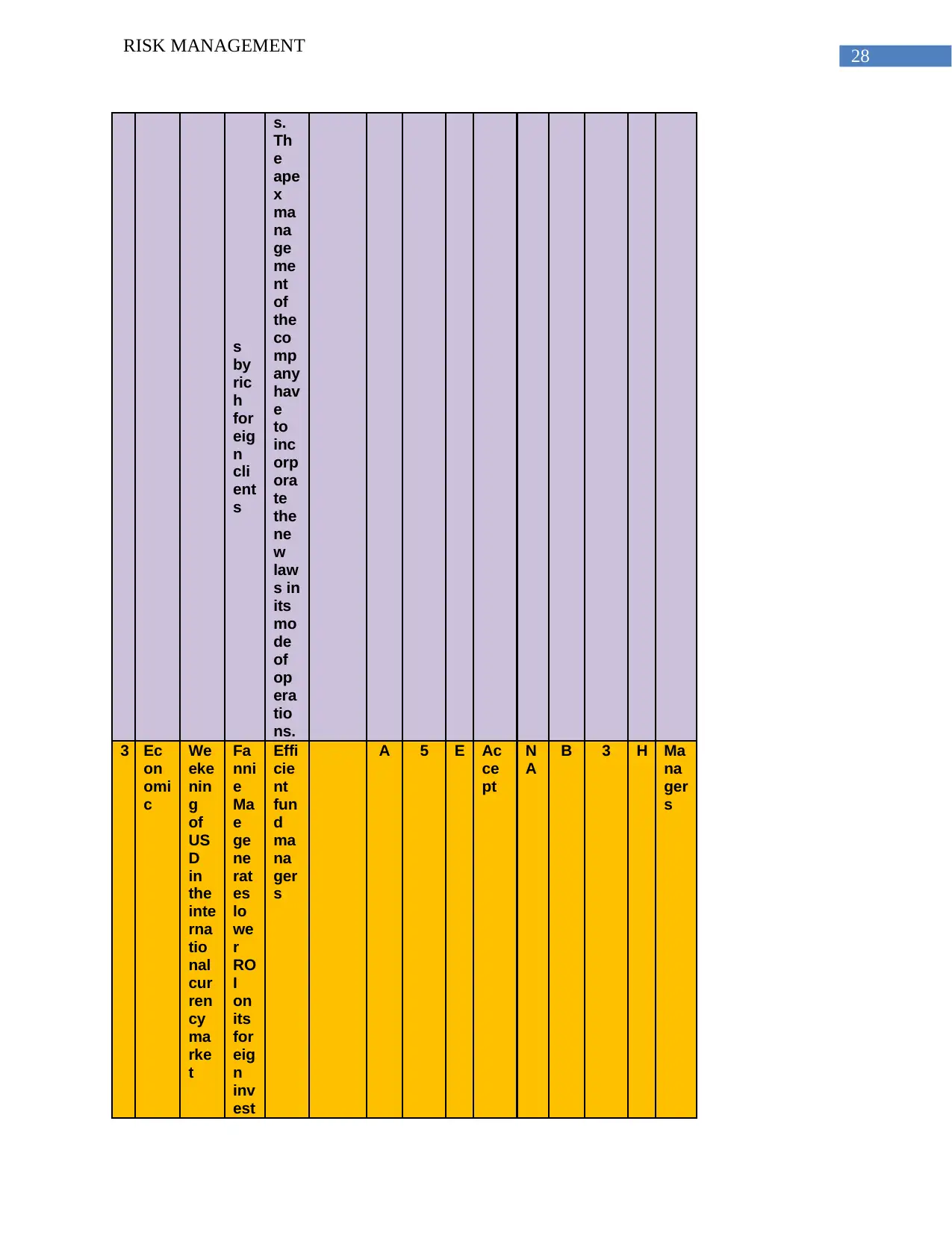

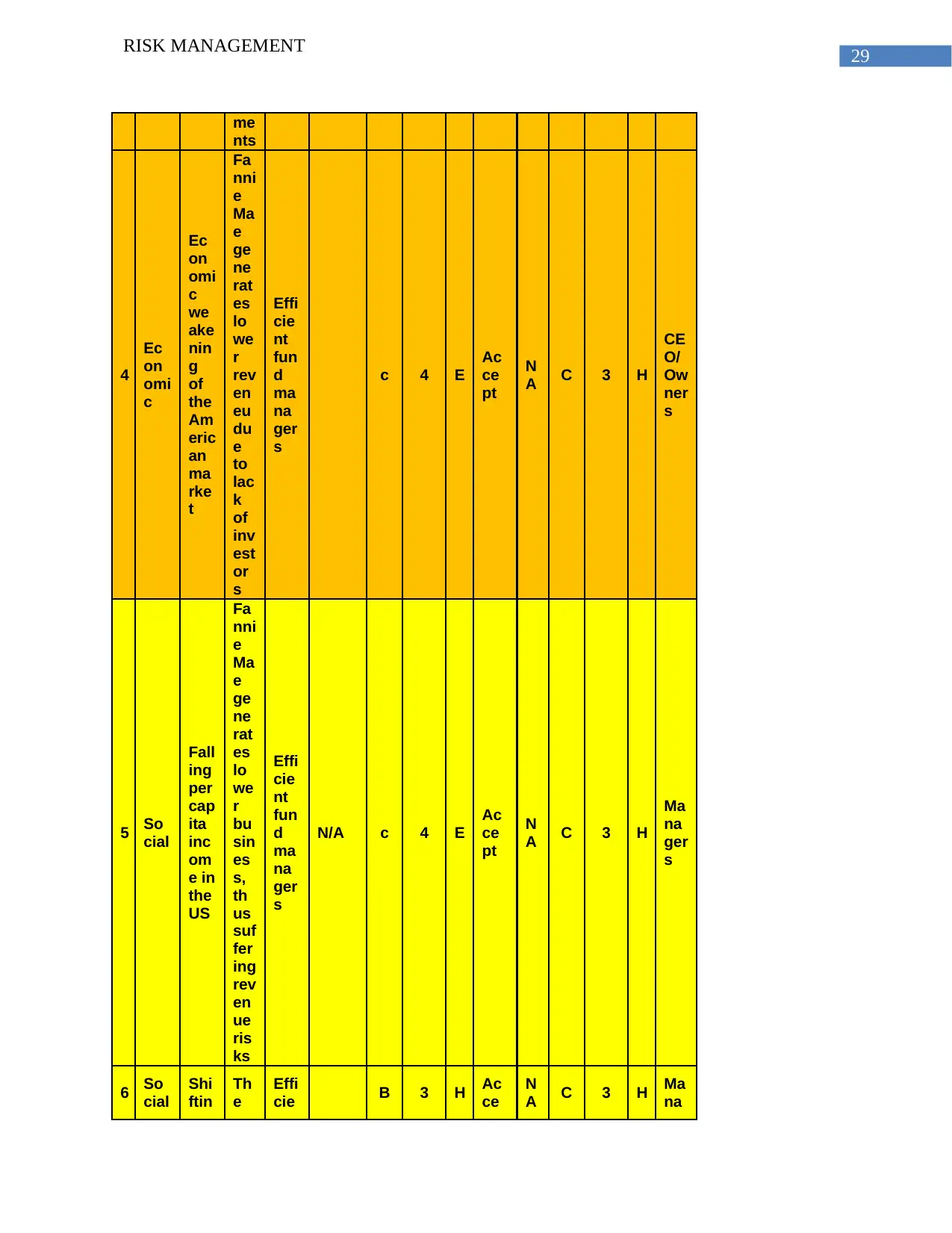

3. Finding/Section Result:

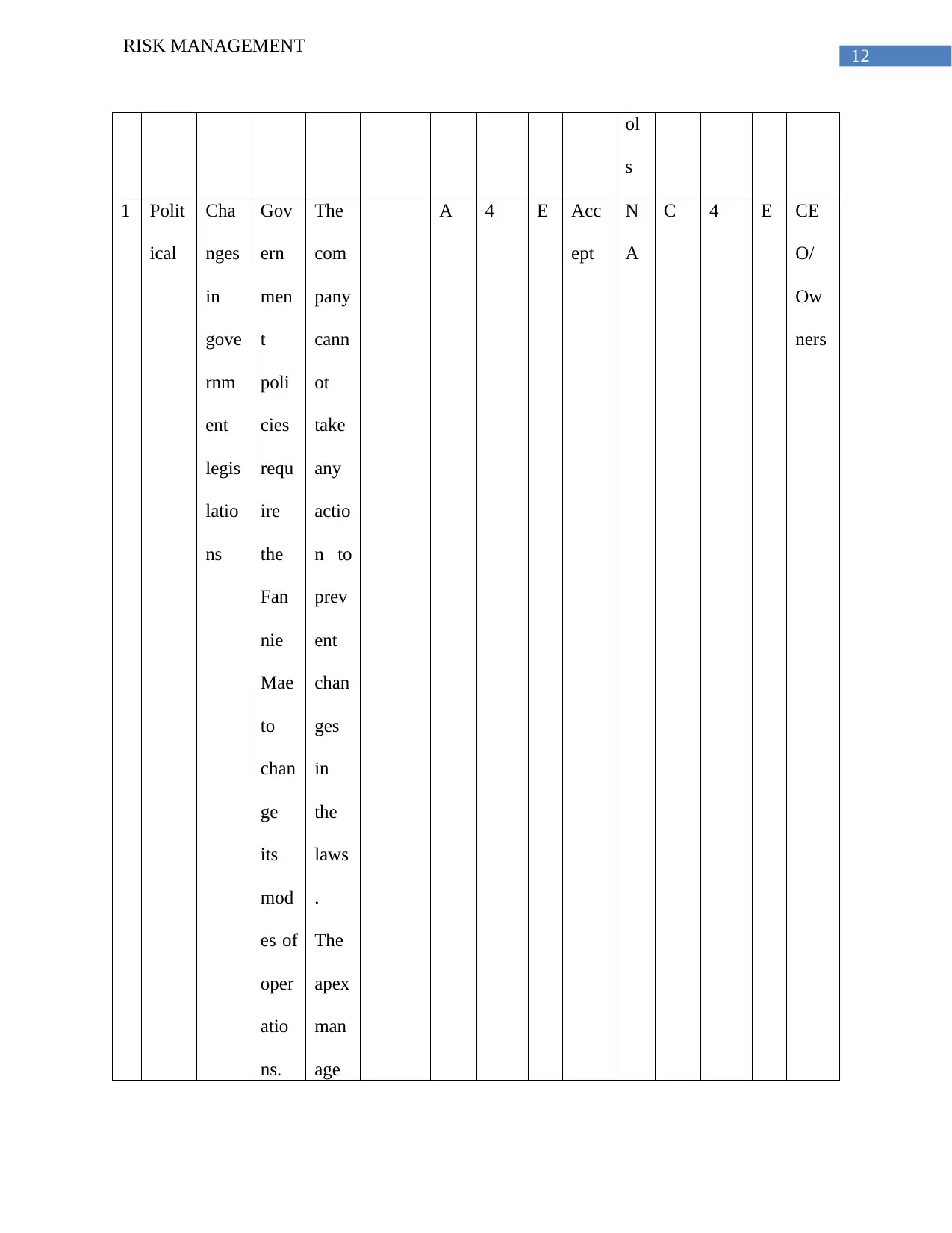

Risk model of 20 risks:

The top 20 risks identified below are changes in government legislations, weakening of

the international relationships of the United States of America, weakening of USD in the

international currency exchange market, economic weakening of the American economy and

falling in the per capita income in the American society. The sixth, seventh, eight, nine and tenth

risks are shifting of investment patterns of investors to more secure modes of investments like

bonds, advanced technology renders existing technology redundant, data thefts, rising frequency

of natural calamities and rising environmental pollution. The eleventh, twelfth, thirteenth,

fourteenth and fifteenth risks are changes in laws, crime, higher turnover of employees,

resistance to changes, investor poaching and falling revenue and threat of newly entering

companies respectively. The other risks are risks of employee theft, fire, WHS risks, risk due to

political corruption and risks due to IPR infringement. The above mentioned risks have been

analysed in terms of aspects like impacts on the business and probable mitigation actions, if

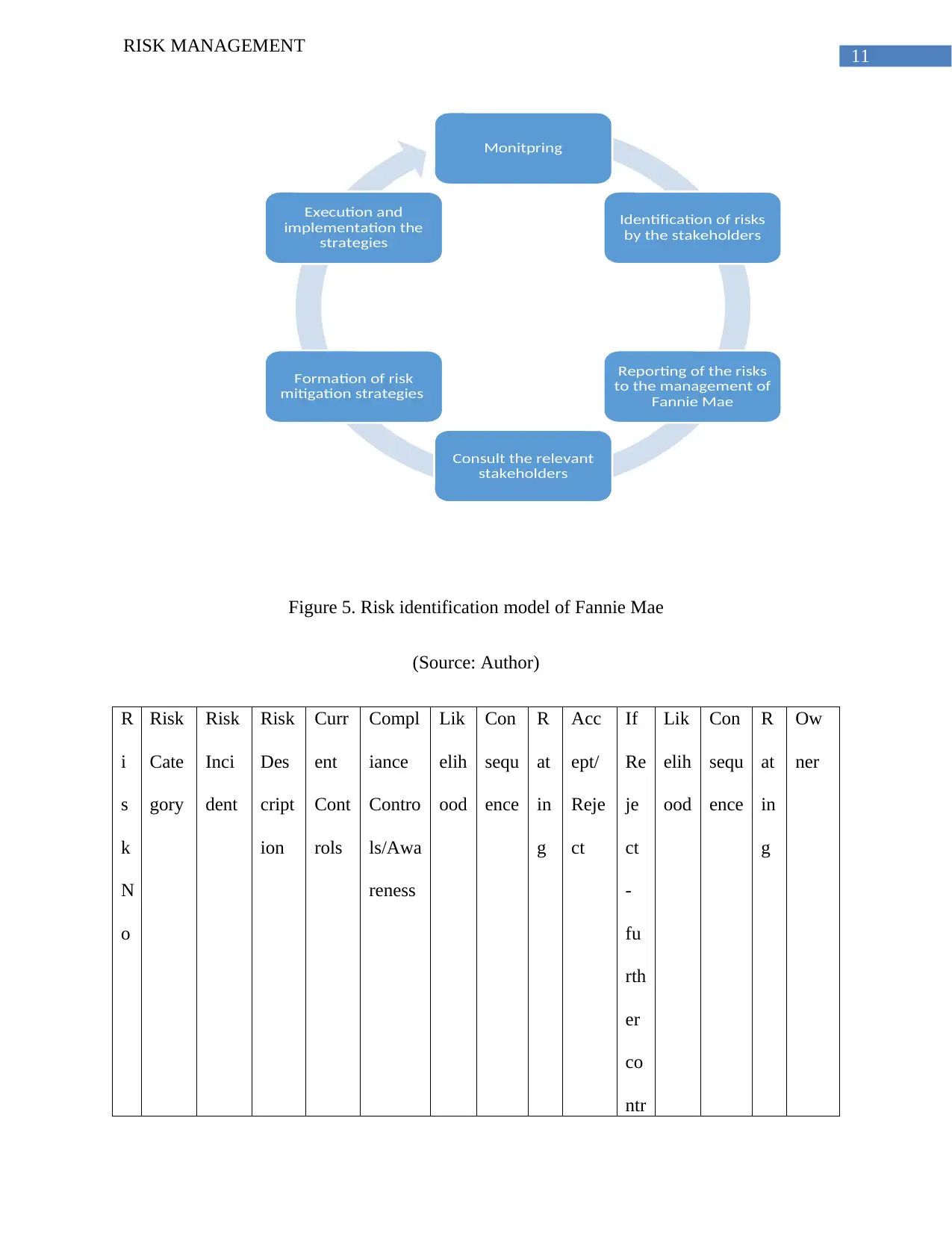

possible. The risk identification model of the risks would consist of the six steps. They are

identification of risks by the stakeholders including management, employees and external

stakeholders followed by reporting of the risks to the management of Fannie Mae. The

management then consult the relevant stakeholders like the government and investors to analyse

the probable mitigation methods (Brustbauer, 2016). The leads to formation of risk mitigation

strategies at the apex level. The subordinates then execute and implement the strategies. The

management of the Fannie Mae monitors the actual performance of the risk mitigation strategies

and amend them according to the requirement of the situation.

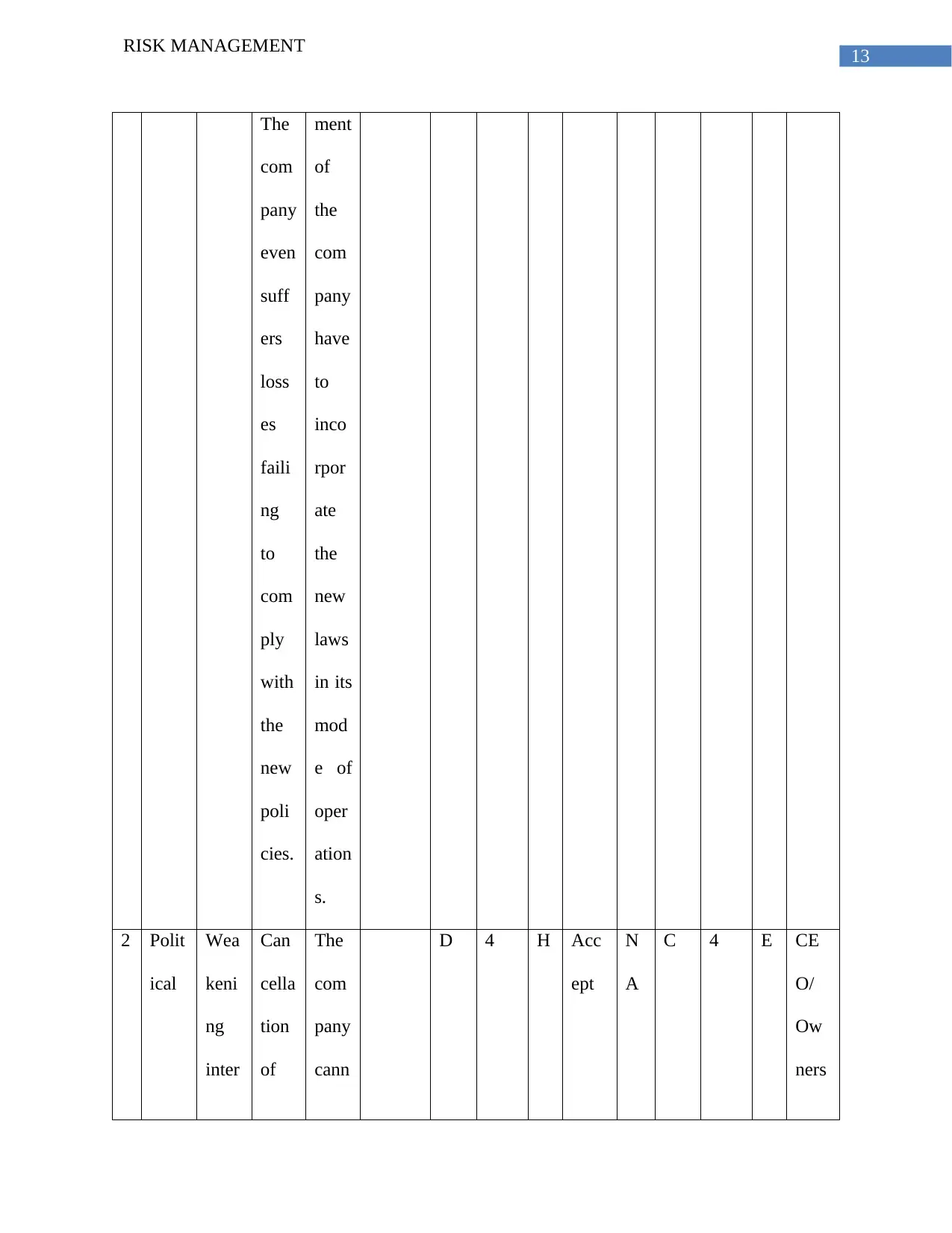

RISK MANAGEMENT

3. Finding/Section Result:

Risk model of 20 risks:

The top 20 risks identified below are changes in government legislations, weakening of

the international relationships of the United States of America, weakening of USD in the

international currency exchange market, economic weakening of the American economy and

falling in the per capita income in the American society. The sixth, seventh, eight, nine and tenth

risks are shifting of investment patterns of investors to more secure modes of investments like

bonds, advanced technology renders existing technology redundant, data thefts, rising frequency

of natural calamities and rising environmental pollution. The eleventh, twelfth, thirteenth,

fourteenth and fifteenth risks are changes in laws, crime, higher turnover of employees,

resistance to changes, investor poaching and falling revenue and threat of newly entering

companies respectively. The other risks are risks of employee theft, fire, WHS risks, risk due to

political corruption and risks due to IPR infringement. The above mentioned risks have been

analysed in terms of aspects like impacts on the business and probable mitigation actions, if

possible. The risk identification model of the risks would consist of the six steps. They are

identification of risks by the stakeholders including management, employees and external

stakeholders followed by reporting of the risks to the management of Fannie Mae. The

management then consult the relevant stakeholders like the government and investors to analyse

the probable mitigation methods (Brustbauer, 2016). The leads to formation of risk mitigation

strategies at the apex level. The subordinates then execute and implement the strategies. The

management of the Fannie Mae monitors the actual performance of the risk mitigation strategies

and amend them according to the requirement of the situation.

11

RISK MANAGEMENT

Figure 5. Risk identification model of Fannie Mae

(Source: Author)

R

i

s

k

N

o

Risk

Cate

gory

Risk

Inci

dent

Risk

Des

cript

ion

Curr

ent

Cont

rols

Compl

iance

Contro

ls/Awa

reness

Lik

elih

ood

Con

sequ

ence

R

at

in

g

Acc

ept/

Reje

ct

If

Re

je

ct

-

fu

rth

er

co

ntr

Lik

elih

ood

Con

sequ

ence

R

at

in

g

Ow

ner

Monitpring

Identification of risks

by the stakeholders

Reporting of the risks

to the management of

Fannie Mae

Consult the relevant

stakeholders

Formation of risk

mitigation strategies

Execution and

implementation the

strategies

RISK MANAGEMENT

Figure 5. Risk identification model of Fannie Mae

(Source: Author)

R

i

s

k

N

o

Risk

Cate

gory

Risk

Inci

dent

Risk

Des

cript

ion

Curr

ent

Cont

rols

Compl

iance

Contro

ls/Awa

reness

Lik

elih

ood

Con

sequ

ence

R

at

in

g

Acc

ept/

Reje

ct

If

Re

je

ct

-

fu

rth

er

co

ntr

Lik

elih

ood

Con

sequ

ence

R

at

in

g

Ow

ner

Monitpring

Identification of risks

by the stakeholders

Reporting of the risks

to the management of

Fannie Mae

Consult the relevant

stakeholders

Formation of risk

mitigation strategies

Execution and

implementation the

strategies

You're viewing a preview

Unlock full access by subscribing today!

12

RISK MANAGEMENT

ol

s

1 Polit

ical

Cha

nges

in

gove

rnm

ent

legis

latio

ns

Gov

ern

men

t

poli

cies

requ

ire

the

Fan

nie

Mae

to

chan

ge

its

mod

es of

oper

atio

ns.

The

com

pany

cann

ot

take

any

actio

n to

prev

ent

chan

ges

in

the

laws

.

The

apex

man

age

A 4 E Acc

ept

N

A

C 4 E CE

O/

Ow

ners

RISK MANAGEMENT

ol

s

1 Polit

ical

Cha

nges

in

gove

rnm

ent

legis

latio

ns

Gov

ern

men

t

poli

cies

requ

ire

the

Fan

nie

Mae

to

chan

ge

its

mod

es of

oper

atio

ns.

The

com

pany

cann

ot

take

any

actio

n to

prev

ent

chan

ges

in

the

laws

.

The

apex

man

age

A 4 E Acc

ept

N

A

C 4 E CE

O/

Ow

ners

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

RISK MANAGEMENT

The

com

pany

even

suff

ers

loss

es

faili

ng

to

com

ply

with

the

new

poli

cies.

ment

of

the

com

pany

have

to

inco

rpor

ate

the

new

laws

in its

mod

e of

oper

ation

s.

2 Polit

ical

Wea

keni

ng

inter

Can

cella

tion

of

The

com

pany

cann

D 4 H Acc

ept

N

A

C 4 E CE

O/

Ow

ners

RISK MANAGEMENT

The

com

pany

even

suff

ers

loss

es

faili

ng

to

com

ply

with

the

new

poli

cies.

ment

of

the

com

pany

have

to

inco

rpor

ate

the

new

laws

in its

mod

e of

oper

ation

s.

2 Polit

ical

Wea

keni

ng

inter

Can

cella

tion

of

The

com

pany

cann

D 4 H Acc

ept

N

A

C 4 E CE

O/

Ow

ners

14

RISK MANAGEMENT

natio

nal

relat

ions

hips

of

the

US

cont

racts

to

inve

st in

the

mort

gage

sche

mes

by

rich

forei

gn

clien

ts

ot

take

any

actio

n to

prev

ent

chan

ges

in

the

laws

.

The

apex

man

age

ment

of

the

com

pany

have

RISK MANAGEMENT

natio

nal

relat

ions

hips

of

the

US

cont

racts

to

inve

st in

the

mort

gage

sche

mes

by

rich

forei

gn

clien

ts

ot

take

any

actio

n to

prev

ent

chan

ges

in

the

laws

.

The

apex

man

age

ment

of

the

com

pany

have

You're viewing a preview

Unlock full access by subscribing today!

15

RISK MANAGEMENT

to

inco

rpor

ate

the

new

laws

in its

mod

e of

oper

ation

s.

3 Econ

omic

Wee

keni

ng

of

USD

in

the

inter

natio

nal

Fan

nie

Mae

gene

rates

lowe

r

ROI

on

its

Effic

ient

fund

man

ager

s

A 5 E Acc

ept

N

A

B 3 H Man

ager

s

RISK MANAGEMENT

to

inco

rpor

ate

the

new

laws

in its

mod

e of

oper

ation

s.

3 Econ

omic

Wee

keni

ng

of

USD

in

the

inter

natio

nal

Fan

nie

Mae

gene

rates

lowe

r

ROI

on

its

Effic

ient

fund

man

ager

s

A 5 E Acc

ept

N

A

B 3 H Man

ager

s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

16

RISK MANAGEMENT

curr

ency

mar

ket

forei

gn

inve

stme

nts

4 Econ

omic

Eco

nom

ic

wea

keni

ng

of

the

Ame

rican

mar

ket

Fan

nie

Mae

gene

rates

lowe

r

reve

neu

due

to

lack

of

inve

stors

Effic

ient

fund

man

ager

s

c 4 E Acc

ept

N

A

C 3 H CE

O/

Ow

ners

5 Soci

al

Falli

ng

per

Fan

nie

Mae

Effic

ient

fund

N/A c 4 E Acc

ept

N

A

C 3 H Man

ager

s

RISK MANAGEMENT

curr

ency

mar

ket

forei

gn

inve

stme

nts

4 Econ

omic

Eco

nom

ic

wea

keni

ng

of

the

Ame

rican

mar

ket

Fan

nie

Mae

gene

rates

lowe

r

reve

neu

due

to

lack

of

inve

stors

Effic

ient

fund

man

ager

s

c 4 E Acc

ept

N

A

C 3 H CE

O/

Ow

ners

5 Soci

al

Falli

ng

per

Fan

nie

Mae

Effic

ient

fund

N/A c 4 E Acc

ept

N

A

C 3 H Man

ager

s

17

RISK MANAGEMENT

capit

a

inco

me

in

the

US

gene

rates

lowe

r

busi

ness,

thus

suff

erin

g

reve

nue

risks

man

ager

s

6 Soci

al

Shift

ing

of

inve

stme

nt

patte

rn of

inve

stors

The

inve

stors

may

shift

to

mor

e

secu

red

Effic

ient

fund

man

ager

s

B 3 H Acc

ept

N

A

C 3 H Man

ager

s

RISK MANAGEMENT

capit

a

inco

me

in

the

US

gene

rates

lowe

r

busi

ness,

thus

suff

erin

g

reve

nue

risks

man

ager

s

6 Soci

al

Shift

ing

of

inve

stme

nt

patte

rn of

inve

stors

The

inve

stors

may

shift

to

mor

e

secu

red

Effic

ient

fund

man

ager

s

B 3 H Acc

ept

N

A

C 3 H Man

ager

s

You're viewing a preview

Unlock full access by subscribing today!

18

RISK MANAGEMENT

mod

e of

inve

stme

nts

like

bon

ds

and

savi

ng

acco

unt

7 Tech

nolo

gical

Adv

ance

d

tech

nolo

gy

rend

ers

curr

ent

The

capit

al

whic

h

Fan

nie

Mae

inve

sts

Effic

ient

fund

man

ager

s

A 4 E Acc

ept

N

A

C 3 H Man

ager

s

RISK MANAGEMENT

mod

e of

inve

stme

nts

like

bon

ds

and

savi

ng

acco

unt

7 Tech

nolo

gical

Adv

ance

d

tech

nolo

gy

rend

ers

curr

ent

The

capit

al

whic

h

Fan

nie

Mae

inve

sts

Effic

ient

fund

man

ager

s

A 4 E Acc

ept

N

A

C 3 H Man

ager

s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

RISK MANAGEMENT

tech

nolo

gy

redu

ndan

t

in

tech

nolg

y

goes

to

wast

e

8 Tech

nolo

gical

Data

theft

s

Loss

of

sens

etive

data

pert

aini

ng

to

inve

stors

incl

udin

g

fina

Tech

nolo

gical

depa

rtme

nt

A 5 E Acc

ept

N

A

A 5 E Man

ager

s

RISK MANAGEMENT

tech

nolo

gy

redu

ndan

t

in

tech

nolg

y

goes

to

wast

e

8 Tech

nolo

gical

Data

theft

s

Loss

of

sens

etive

data

pert

aini

ng

to

inve

stors

incl

udin

g

fina

Tech

nolo

gical

depa

rtme

nt

A 5 E Acc

ept

N

A

A 5 E Man

ager

s

20

RISK MANAGEMENT

ncial

data

9 Envi

ron

ment

al

Risi

ng

natu

ral

cala

miti

es

Loss

of

prop

erty

and

man

pow

er

All

the

depa

rtme

nt

A 5 E Acc

ept

N

A

C 5 E CE

O/

Ow

ners

1

0

Envi

ron

ment

al

Risi

ng

envr

ion

ment

al

poll

utio

n

Insta

llati

on

of

tech

nolo

gy

usin

g

less

elect

ricit

y

All

the

depa

rtme

nt

B 3 H Acc

ept

N

A

C 2 M CE

O/

Ow

ners

RISK MANAGEMENT

ncial

data

9 Envi

ron

ment

al

Risi

ng

natu

ral

cala

miti

es

Loss

of

prop

erty

and

man

pow

er

All

the

depa

rtme

nt

A 5 E Acc

ept

N

A

C 5 E CE

O/

Ow

ners

1

0

Envi

ron

ment

al

Risi

ng

envr

ion

ment

al

poll

utio

n

Insta

llati

on

of

tech

nolo

gy

usin

g

less

elect

ricit

y

All

the

depa

rtme

nt

B 3 H Acc

ept

N

A

C 2 M CE

O/

Ow

ners

You're viewing a preview

Unlock full access by subscribing today!

21

RISK MANAGEMENT

1

1

Lega

l

Cha

nges

in

laws

Cha

nge

of

orga

nisat

iona

l

poli

cies

All

the

depa

rtme

nt

B 3 H Acc

ept

N

A

C 4 E CE

O/

Ow

ners

1

2

Lega

l

Cri

me

legal

char

ges

All

the

depa

rtme

nt

C 3 H Acc

ept

N

A

C 4 E CE

O/

Ow

ners

1

3

Oper

ation

al

High

er

turn

over

of

empl

oyee

s

Disr

upti

on

of

prod

ucti

vity

All

the

depa

rtme

nt

C 3 H Acc

ept

N

A

C 4 E CE

O/

Ow

ners

1 Oper Resi Disr All C 4 E Acc N C 4 E CE

RISK MANAGEMENT

1

1

Lega

l

Cha

nges

in

laws

Cha

nge

of

orga

nisat

iona

l

poli

cies

All

the

depa

rtme

nt

B 3 H Acc

ept

N

A

C 4 E CE

O/

Ow

ners

1

2

Lega

l

Cri

me

legal

char

ges

All

the

depa

rtme

nt

C 3 H Acc

ept

N

A

C 4 E CE

O/

Ow

ners

1

3

Oper

ation

al

High

er

turn

over

of

empl

oyee

s

Disr

upti

on

of

prod

ucti

vity

All

the

depa

rtme

nt

C 3 H Acc

ept

N

A

C 4 E CE

O/

Ow

ners

1 Oper Resi Disr All C 4 E Acc N C 4 E CE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

22

RISK MANAGEMENT

4 ation

al

stan

ce to

chan

ges

upti

on

of

prod

ucti

vity

the

depa

rtme

nt

ept A O/

Ow

ners

1

5

Thre

at of

new

enter

ing

com

pany

Inve

stor

poac

hing

and

falli

ng

reve

nue

Red

ucti

on

of

reve

nue

All

the

depa

rtme

nt

C 4 E Acc

ept

N

A

C 5 E CE

O/

Ow

ners

1

6

Risk

of

empl

oyee

theft

Loss

of

asset

s

inclu

ding

infor

mati

Red

ucti

on

of

reve

nue

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 6 E CE

O/

Ow

ners

RISK MANAGEMENT

4 ation

al

stan

ce to

chan

ges

upti

on

of

prod

ucti

vity

the

depa

rtme

nt

ept A O/

Ow

ners

1

5

Thre

at of

new

enter

ing

com

pany

Inve

stor

poac

hing

and

falli

ng

reve

nue

Red

ucti

on

of

reve

nue

All

the

depa

rtme

nt

C 4 E Acc

ept

N

A

C 5 E CE

O/

Ow

ners

1

6

Risk

of

empl

oyee

theft

Loss

of

asset

s

inclu

ding

infor

mati

Red

ucti

on

of

reve

nue

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 6 E CE

O/

Ow

ners

23

RISK MANAGEMENT

on

1

7

Fire Loss

of

asset

s

inclu

ding

infor

mati

on

Mas

sive

loss

of

reve

nue

and

busi

ness

data

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 7 E CE

O/

Ow

ners

1

8

WH

S

risks

Loss

of

prod

uctiv

ity

due

to

injur

ies/d

eath

of

empl

Leg

al

actio

ns

from

gove

rnm

ents

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 8 E CE

O/

Ow

ners

RISK MANAGEMENT

on

1

7

Fire Loss

of

asset

s

inclu

ding

infor

mati

on

Mas

sive

loss

of

reve

nue

and

busi

ness

data

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 7 E CE

O/

Ow

ners

1

8

WH

S

risks

Loss

of

prod

uctiv

ity

due

to

injur

ies/d

eath

of

empl

Leg

al

actio

ns

from

gove

rnm

ents

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 8 E CE

O/

Ow

ners

You're viewing a preview

Unlock full access by subscribing today!

24

RISK MANAGEMENT

oyee

s

1

9

Risk

due

to

polit

ical

corr

uptio

n

Loss

of

reso

urce

s

and

reve

nue,

inhi

bitio

n in

getti

ng

appr

oval

s

and

sabc

tions

from

the

Busi

ness

opp

ortu

nity

loss

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 9 E CE

O/

Ow

ners

RISK MANAGEMENT

oyee

s

1

9

Risk

due

to

polit

ical

corr

uptio

n

Loss

of

reso

urce

s

and

reve

nue,

inhi

bitio

n in

getti

ng

appr

oval

s

and

sabc

tions

from

the

Busi

ness

opp

ortu

nity

loss

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 9 E CE

O/

Ow

ners

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25

RISK MANAGEMENT

gove

rnm

ent

2

0

Risk

due

to

IPR

infri

ngm

ent

Loss

of

reso

urce

s

and

reve

nue,

inhi

bitio

n in

getti

ng

appr

oval

s

and

sabc

tions

from

Busi

ness

opp

ortu

nity

loss

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 10 E CE

O/

Ow

ners

RISK MANAGEMENT

gove

rnm

ent

2

0

Risk

due

to

IPR

infri

ngm

ent

Loss

of

reso

urce

s

and

reve

nue,

inhi

bitio

n in

getti

ng

appr

oval

s

and

sabc

tions

from

Busi

ness

opp

ortu

nity

loss

All

the

depa

rtme

nt

C E Acc

ept

N

A

C 10 E CE

O/

Ow

ners

26

RISK MANAGEMENT

the

gove

rnm

ent

Diagram of top ten risks:

R

i

s

k

N

o

Ris

k

Cat

ego

ry

Ris

k

Inci

den

t

Ri

sk

De

scr

ipti

on

Cur

ren

t

Co

ntr

ols

Com

plian

ce

Cont

rols/

Awar

enes

s

Li

ke

lih

oo

d

Co

ns

eq

ue

nc

e

R

a

ti

n

g

Ac

ce

pt/

Rej

ect

If

R

ej

e

ct

-

f

u

rt

h

e

r

c

o

n

tr

ol

s

Li

ke

lih

oo

d

Co

ns

eq

ue

nc

e

R

a

ti

n

g

Ow

ner

1 Pol

itic

al

Ch

ang

es

in

gov

ern

me

nt

legi

slat

ion

s

Go

ver

nm

ent

pol

ici

es

re

qui

re

the

Fa

nni

e

Ma

e

to

ch

an

ge

its

mo

de

Th

e

co

mp

any

can

not

tak

e

any

acti

on

to

pre

ven

t

cha

ng

es

in

the

law

s.

A 4 E Ac

ce

pt

N

A

C 4 E CE

O/

Ow

ner

s

RISK MANAGEMENT

the

gove

rnm

ent

Diagram of top ten risks:

R

i

s

k

N

o

Ris

k

Cat

ego

ry

Ris

k

Inci

den

t

Ri

sk

De

scr

ipti

on

Cur

ren

t

Co

ntr

ols

Com

plian

ce

Cont

rols/

Awar

enes

s

Li

ke

lih

oo

d

Co

ns

eq

ue

nc

e

R

a

ti

n

g

Ac

ce

pt/

Rej

ect

If

R

ej

e

ct

-

f

u

rt

h

e

r

c

o

n

tr

ol

s

Li

ke

lih

oo

d

Co

ns

eq

ue

nc

e

R

a

ti

n

g

Ow

ner

1 Pol

itic

al

Ch

ang

es

in

gov

ern

me

nt

legi

slat

ion

s

Go

ver

nm

ent

pol

ici

es

re

qui

re

the

Fa

nni

e

Ma

e

to

ch

an

ge

its

mo

de

Th

e

co

mp

any

can

not

tak

e

any

acti

on

to

pre

ven

t

cha

ng

es

in

the

law

s.

A 4 E Ac

ce

pt

N

A

C 4 E CE

O/

Ow

ner

s

You're viewing a preview

Unlock full access by subscribing today!

27

RISK MANAGEMENT

s

of

op

era

tio

ns.

Th

e

co

mp

an

y

ev

en

suf

fer

s

los

se

s

fail

ing

to

co

mp

ly

wit

h

the

ne

w

pol

ici

es.

Th

e

ape

x

ma

na

ge

me

nt

of

the

co

mp

any

hav

e

to

inc

orp

ora

te

the

ne

w

law

s in

its

mo

de

of

op

era

tio

ns.

2 Pol

itic

al

We

ake

nin

g

inte

rna

tio

nal

rela

tio

nsh

ips

of

the

US

Ca

nc

ell

ati

on

of

co

ntr

act

s

to

inv

est

in

the

mo

rtg

ag

e

sc

he

me

Th

e

co

mp

any

can

not

tak

e

any

acti

on

to

pre

ven

t

cha

ng

es

in

the

law

D 4 H Ac

ce

pt

N

A

C 4 E CE

O/

Ow

ner

s

RISK MANAGEMENT

s

of

op

era

tio

ns.

Th

e

co

mp

an

y

ev

en

suf

fer

s

los

se

s

fail

ing

to

co

mp

ly

wit

h

the

ne

w

pol

ici

es.

Th

e

ape

x

ma

na

ge

me

nt

of

the

co

mp

any

hav

e

to

inc

orp

ora

te

the

ne

w

law

s in

its

mo

de

of

op

era

tio

ns.

2 Pol

itic

al

We

ake

nin

g

inte

rna

tio

nal

rela

tio

nsh

ips

of

the

US

Ca

nc

ell

ati

on

of

co

ntr

act

s

to

inv

est

in

the

mo

rtg

ag

e

sc

he

me

Th

e

co

mp

any

can

not

tak

e

any

acti

on

to

pre

ven

t

cha

ng

es

in

the

law

D 4 H Ac

ce

pt

N

A

C 4 E CE

O/

Ow

ner

s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

28

RISK MANAGEMENT

s

by

ric

h

for

eig

n

cli

ent

s

s.

Th

e

ape

x

ma

na

ge

me

nt

of

the

co

mp

any

hav

e

to

inc

orp

ora

te

the

ne

w

law

s in

its

mo

de

of

op

era

tio

ns.

3 Ec

on

omi

c

We

eke

nin

g

of

US

D

in

the

inte

rna

tio

nal

cur

ren

cy

ma

rke

t

Fa

nni

e

Ma

e

ge

ne

rat

es

lo

we

r

RO

I

on

its

for

eig

n

inv

est

Effi

cie

nt

fun

d

ma

na

ger

s

A 5 E Ac

ce

pt

N

A

B 3 H Ma

na

ger

s

RISK MANAGEMENT

s

by

ric

h

for

eig

n

cli

ent

s

s.

Th

e

ape

x

ma

na

ge

me

nt

of

the

co

mp

any

hav

e

to

inc

orp

ora

te

the

ne

w

law

s in

its

mo

de

of

op

era

tio

ns.

3 Ec

on

omi

c

We

eke

nin

g

of

US

D

in

the

inte

rna

tio

nal

cur

ren

cy

ma

rke

t

Fa

nni

e

Ma

e

ge

ne

rat

es

lo

we

r

RO

I

on

its

for

eig

n

inv

est

Effi

cie

nt

fun

d

ma

na

ger

s

A 5 E Ac

ce

pt

N

A

B 3 H Ma

na

ger

s

29

RISK MANAGEMENT

me

nts

4

Ec

on

omi

c

Ec

on

omi

c

we

ake

nin

g

of

the

Am

eric

an

ma

rke

t

Fa

nni

e

Ma

e

ge

ne

rat

es

lo

we

r

rev

en

eu

du

e

to

lac

k

of

inv

est

or

s

Effi

cie

nt

fun

d

ma

na

ger

s

c 4 E

Ac

ce

pt

N

A C 3 H

CE

O/

Ow

ner

s

5 So

cial

Fall

ing

per

cap

ita

inc

om

e in

the

US

Fa

nni

e

Ma

e

ge

ne

rat

es

lo

we

r

bu

sin

es

s,

th

us

suf

fer

ing

rev

en

ue

ris

ks

Effi

cie

nt

fun

d

ma

na

ger

s

N/A c 4 E

Ac

ce

pt

N

A C 3 H

Ma

na

ger

s

6 So

cial

Shi

ftin

Th

e

Effi

cie B 3 H Ac

ce

N

A C 3 H Ma

na

RISK MANAGEMENT

me

nts

4

Ec

on

omi

c

Ec

on

omi

c

we

ake

nin

g

of

the

Am

eric

an

ma

rke

t

Fa

nni

e

Ma

e

ge

ne

rat

es

lo

we

r

rev

en

eu

du

e

to

lac

k

of

inv

est

or

s

Effi

cie

nt

fun

d

ma

na

ger

s

c 4 E

Ac

ce

pt

N

A C 3 H

CE

O/

Ow

ner

s

5 So

cial

Fall

ing

per

cap

ita

inc

om

e in

the

US

Fa

nni

e

Ma

e

ge

ne

rat

es

lo

we

r

bu

sin

es

s,

th

us

suf

fer

ing

rev

en

ue

ris

ks

Effi

cie

nt

fun

d

ma

na

ger

s

N/A c 4 E

Ac

ce

pt

N

A C 3 H

Ma

na

ger

s

6 So

cial

Shi

ftin

Th

e

Effi

cie B 3 H Ac

ce

N

A C 3 H Ma

na

You're viewing a preview

Unlock full access by subscribing today!

30

RISK MANAGEMENT

g

of

inv

est

me

nt

pat

ter

n

of

inv

est

ors

inv

est

or

s

ma

y

shi

ft

to

mo

re

se

cu

re

d

mo

de

of

inv

est

me

nts

lik

e

bo

nd

s

an

d

sa

vin

g

ac

co

un

t

nt

fun

d

ma

na

ger

s

pt ger

s

7 Tec

hn

olo

gic

al

Ad

van

ced

tec

hn

olo

gy

ren

der

s

cur

ren

t

tec

hn

olo

gy

red

un

dan

Th

e

ca

pit

al

wh

ich

Fa

nni

e

Ma

e

inv

est

s

in

tec

hn

olg

y

Effi

cie

nt

fun

d

ma

na

ger

s

A 4 E Ac

ce

pt

N

A

C 3 H Ma

na

ger

s

RISK MANAGEMENT

g

of

inv

est

me

nt

pat

ter

n

of

inv

est

ors

inv

est

or

s

ma

y

shi

ft

to

mo

re

se

cu

re

d

mo

de

of

inv

est

me

nts

lik

e

bo

nd

s

an

d

sa

vin

g

ac

co

un

t

nt

fun

d

ma

na

ger

s

pt ger

s

7 Tec

hn

olo

gic

al

Ad

van

ced

tec

hn

olo

gy

ren

der

s

cur

ren

t

tec

hn

olo

gy

red

un

dan

Th

e

ca

pit

al

wh

ich

Fa

nni

e

Ma

e

inv

est

s

in

tec

hn

olg

y

Effi

cie

nt

fun

d

ma

na

ger

s

A 4 E Ac

ce

pt

N

A

C 3 H Ma

na

ger

s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31

RISK MANAGEMENT

t

go

es

to

wa

ste

8

Tec

hn

olo

gic

al

Dat

a

the

fts

Lo

ss

of

se

ns

eti

ve

dat

a

pe

rta

ini

ng

to

inv

est

or

s

inc

lud

ing

fin

an

cia

l

dat

a

Tec

hn

olo

gic

al

de

par

tm

ent

A 5 E

Ac

ce

pt

N

A A 5 E

Ma

na

ger

s

9

En

vir

on

me

ntal

Ris

ing

nat

ura

l

cal

ami

ties

Lo

ss

of

pr

op

ert

y

an

d

ma

np

ow

er

All

the

de

par

tm

ent

A 5 E

Ac

ce

pt

N

A C 5 E

CE

O/

Ow

ner

s

1

0

En

vir

on

me

ntal

Ris

ing

env

rio

nm

ent

al

poll

uti

on

Ins

tall

ati

on

of

tec

hn

olo

gy

usi

All

the

de

par

tm

ent

B 3 H Ac

ce

pt

N

A

C 2 M CE

O/

Ow

ner

s

RISK MANAGEMENT

t

go

es

to

wa

ste

8

Tec

hn

olo

gic

al

Dat

a

the

fts

Lo

ss

of

se

ns

eti

ve

dat

a

pe

rta

ini

ng

to

inv

est

or

s

inc

lud

ing

fin

an

cia

l

dat

a

Tec

hn

olo

gic

al

de

par

tm

ent

A 5 E

Ac

ce

pt

N

A A 5 E

Ma

na

ger

s

9

En

vir

on

me

ntal

Ris

ing

nat

ura

l

cal

ami

ties

Lo

ss

of

pr

op

ert

y

an

d

ma

np

ow

er

All

the

de

par

tm

ent

A 5 E

Ac

ce

pt

N

A C 5 E

CE

O/

Ow

ner

s

1

0

En

vir

on

me

ntal

Ris

ing

env

rio

nm

ent

al

poll

uti

on

Ins

tall

ati

on

of

tec

hn

olo

gy

usi

All

the

de

par

tm

ent

B 3 H Ac

ce

pt

N

A

C 2 M CE

O/

Ow

ner

s

32

RISK MANAGEMENT

ng

les

s

ele

ctr

icit

y

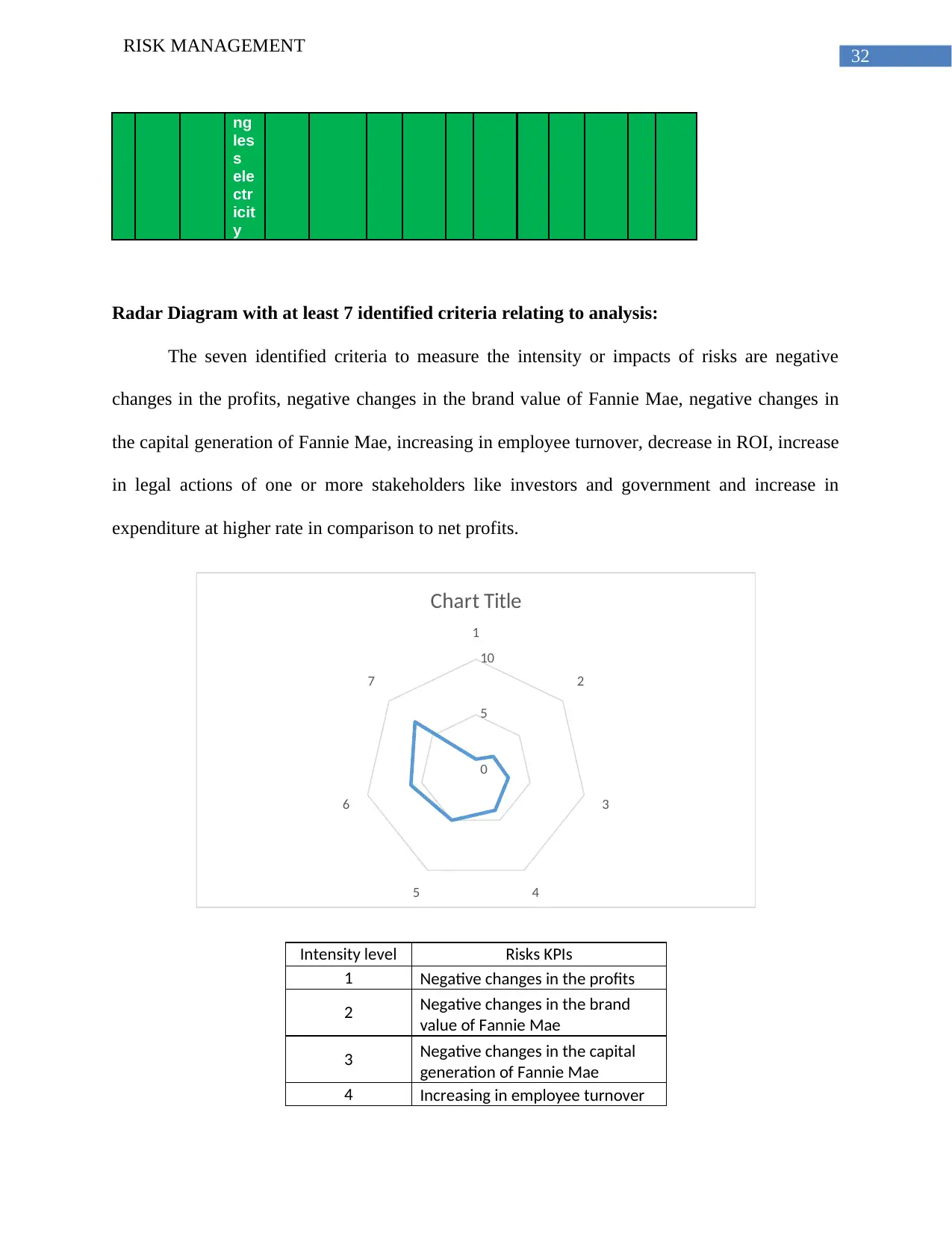

Radar Diagram with at least 7 identified criteria relating to analysis:

The seven identified criteria to measure the intensity or impacts of risks are negative

changes in the profits, negative changes in the brand value of Fannie Mae, negative changes in

the capital generation of Fannie Mae, increasing in employee turnover, decrease in ROI, increase

in legal actions of one or more stakeholders like investors and government and increase in

expenditure at higher rate in comparison to net profits.

1

2

3

45

6

7

0

5

10

Chart Title

Intensity level Risks KPIs

1 Negative changes in the profits

2 Negative changes in the brand

value of Fannie Mae

3 Negative changes in the capital

generation of Fannie Mae

4 Increasing in employee turnover

RISK MANAGEMENT

ng

les

s

ele

ctr

icit

y

Radar Diagram with at least 7 identified criteria relating to analysis:

The seven identified criteria to measure the intensity or impacts of risks are negative

changes in the profits, negative changes in the brand value of Fannie Mae, negative changes in

the capital generation of Fannie Mae, increasing in employee turnover, decrease in ROI, increase

in legal actions of one or more stakeholders like investors and government and increase in

expenditure at higher rate in comparison to net profits.

1

2

3

45

6

7

0

5

10

Chart Title

Intensity level Risks KPIs

1 Negative changes in the profits

2 Negative changes in the brand

value of Fannie Mae

3 Negative changes in the capital

generation of Fannie Mae

4 Increasing in employee turnover

You're viewing a preview

Unlock full access by subscribing today!

33

RISK MANAGEMENT

5 Decrease in ROI

6 Increase in legal actions

7 Increase in expenditure at higher

rate in comparison to net profits

4. Report Conclusion:

It can be concluded from the discussion that Fannie Mae in spite of being one of the top

mortgage financing companies and sponsored by the government, suffers from several risks. The

risk culture of the company can be scored 50 out of 100 which means that the company is an

average risk culture as shown. There were several delivery gaps in the findings. First, the actual

data regarding the investment pattern of Fannie and its customer data are not available on its

website. This limited the findings of the research to the data available on the website and the

other secondary sources like Bloomberg.

RISK MANAGEMENT

5 Decrease in ROI

6 Increase in legal actions

7 Increase in expenditure at higher

rate in comparison to net profits

4. Report Conclusion:

It can be concluded from the discussion that Fannie Mae in spite of being one of the top

mortgage financing companies and sponsored by the government, suffers from several risks. The

risk culture of the company can be scored 50 out of 100 which means that the company is an

average risk culture as shown. There were several delivery gaps in the findings. First, the actual

data regarding the investment pattern of Fannie and its customer data are not available on its

website. This limited the findings of the research to the data available on the website and the

other secondary sources like Bloomberg.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

34

RISK MANAGEMENT

References:

Aalbers, M. B. (2016). The financialization of home and the mortgage market crisis. In The

Financialization of Housing(pp. 40-63). Routledge.

Adrian, T., & Jones, B. (2018). Shadow banking and market-based finance. International

Monetary Fund.

Betts, A. (2018). Mortgage funds: Examining the emergence of new mortgage finance methods

in Sweden.

Bloomberg.com. (2019). Retrieved from https://www.bloomberg.com/quote/FNMA:US

Brustbauer, J. (2016). Enterprise risk management in SMEs: Towards a structural

model. International Small Business Journal, 34(1), 70-85.

Cho, M., Furey, L. D., & Mohr, T. (2017). Communicating corporate social responsibility on

social media: Strategies, stakeholders, and public engagement on corporate

Facebook. Business and Professional Communication Quarterly, 80(1), 52-69.

De Silva, M., Howells, J., & Meyer, M. (2018). Innovation intermediaries and collaboration:

Knowledge–based practices and internal value creation. Research Policy, 47(1), 70-87.

El-hadj, M. B., Faye, I., & Geh, Z. F. (2018). The Way Forward: A Stakeholder Analysis.

In Housing Market Dynamics in Africa(pp. 255-272). Palgrave Macmillan, London.

Fanniemae.com. (2019). Retrieved from http://www.fanniemae.com/portal/business-

partners.html

Fhfa.gov. (2019). Retrieved from https://www.fhfa.gov/AboutUs

RISK MANAGEMENT

References:

Aalbers, M. B. (2016). The financialization of home and the mortgage market crisis. In The

Financialization of Housing(pp. 40-63). Routledge.

Adrian, T., & Jones, B. (2018). Shadow banking and market-based finance. International

Monetary Fund.

Betts, A. (2018). Mortgage funds: Examining the emergence of new mortgage finance methods

in Sweden.

Bloomberg.com. (2019). Retrieved from https://www.bloomberg.com/quote/FNMA:US

Brustbauer, J. (2016). Enterprise risk management in SMEs: Towards a structural

model. International Small Business Journal, 34(1), 70-85.

Cho, M., Furey, L. D., & Mohr, T. (2017). Communicating corporate social responsibility on

social media: Strategies, stakeholders, and public engagement on corporate

Facebook. Business and Professional Communication Quarterly, 80(1), 52-69.

De Silva, M., Howells, J., & Meyer, M. (2018). Innovation intermediaries and collaboration:

Knowledge–based practices and internal value creation. Research Policy, 47(1), 70-87.

El-hadj, M. B., Faye, I., & Geh, Z. F. (2018). The Way Forward: A Stakeholder Analysis.

In Housing Market Dynamics in Africa(pp. 255-272). Palgrave Macmillan, London.

Fanniemae.com. (2019). Retrieved from http://www.fanniemae.com/portal/business-

partners.html

Fhfa.gov. (2019). Retrieved from https://www.fhfa.gov/AboutUs

35

RISK MANAGEMENT

Huang, S., Ng, J., Roychowdhury, S., & Sletten, E. (2016). Increased creditor rights, institutional

investors and corporate myopia. Singapore Management University School of

Accountancy Research Paper, (2016-38).

Jarzabkowski, P., Chalkias, K., Cacciatori, E., & Bednarek, R. (2018). Between State and

Market: Protection Gap Entities and Catastrophic Risk.

Khan, H. U., Lalitha, V. M., & Omonaiye, J. F. (2017). Employees' perception as internal

customers about online services: A case study of banking sector in Nigeria. International

Journal of Business Innovation and Research, 13(2), 181-202.

Korschun, D. (2015). Boundary-spanning employees and relationships with external

stakeholders: A social identity approach. Academy of Management Review, 40(4), 611-

629.

Krishnamurthy, A. (2017). Policies for Crises Prevention and Management. International

Journal of Central Banking.

Navarro, C., Moreno, A., & Al-Sumait, F. (2017). Social media expectations between public

relations professionals and their stakeholders: Results of the ComGap study in

Spain. Public Relations Review, 43(4), 700-708.