Ask a question from expert

(Solved) Assignment - Financial Accounting

24 Pages4569 Words479 Views

Added on 2020-11-12

(Solved) Assignment - Financial Accounting

Added on 2020-11-12

BookmarkShareRelated Documents

FINANCIAL ACCOUNTING

TABLE OF CONTENTSINTRODUCTION...........................................................................................................................1BUSINESS REPORT......................................................................................................................11. Financial accounting and its purpose......................................................................................12. Regulations related to financial accounting............................................................................13. Accounting rules and principles..............................................................................................24. Conventions and concepts relating to consistency and material disclosure............................3CLIENT 1........................................................................................................................................3CLIENT 2......................................................................................................................................12CLIENT 3......................................................................................................................................15CLIENT 4......................................................................................................................................17CLIENT 5......................................................................................................................................18CLIENT 6......................................................................................................................................19CONCLUSION..............................................................................................................................20REFERENCES .............................................................................................................................22

INTRODUCTIONFinancial accounting is a part of financial management that assist managers and accountsin terms of deal with financial challenges and issues. Financial accounting is beneficial for boththe government and private organisations to maintain financial discipline and control foreffective management and control (Agasisti and Catalano, 2013). Book-keeping and accountingsystem for individuals and shareholders are defined in this report. Financial accounting and itspurpose is also defined with practical evaluation. Regulations and policies associated withfinancial accounting are considered in this report. Accounting principles and rules that aregoverned the presentation and prepare financial statements are included in this report.Conventions and concepts related to consistency and material disclosure are covered in thisreport. Preparation of financial accounts for sole traders are considered here.BUSINESS REPORT1. Financial accounting and its purposeFinancial accounting is an essential element for successful operation and management ofbusiness. To manage and controlling of money related outcomes everywhere, a scale is used forminimal intense assignment. It ought not to be easy to assess outcomes, regardless of whetherexchanges are posted precisely in their worry organize. Financial analysis and accounting helps in organising the financial information and detailsthat are subjected to financial plans and decision making process. It is also crucial forascertaining the faith and trust of stakeholders of any organisation. There are types of financialstatements that are prepared to present the financial position and performance of business tostakeholders as cash flow statement, Income statement, financial position statement and changein accounting principles.2. Regulations related to financial accountingIn each business association, an accountant is used to take after essential guidelines anddirection that are made by the worried organizations of board to record every last exchange in anamended way. It provides a base to stay far from any sort of mix-ups that are useful for the mostpart and it might also happen while recording in an agreement to look with such sort of issues,1

the majority of an organization is following basic principles and models. Besides, thought issimply to wind up more significant to consider each choice at real predominance. IASB: It is known as a universal body that is made up to control and administration forrecording of important records (Alver, Alver and Talpas, 2013). These are shaped so as tomanage basic guidelines in regard to get exact outcomes in upcoming duration. It givesfundamental models to record the entire information in a legitimate way. IFRS: It is essentially named as "Universal money related revealing standard" that isviable arrangement of bookkeeping standard and that is made by an autonomous body called asIASB (International bookkeeping standard board). It is related with quality administration ofaccounting so every exchange is being recorded in an appropriate way.3. Accounting rules and principlesThere are various types of rules and principles that an organisation has to follow while preparingfinancial statements. Those are explained below briefly:Debit what comes in credit what goes out: This principle applied in the case of realaccount. It is related to tangible things like assets and goods.Debit all expenses and losses credit all incomes and gains: This rule is related tonominal account. When an expense happens, capital decreases with debit balance andwhen an income is received it increases capital with credit balance.Debit the receiver credit the giver: This rule is implemented when the nature of accountis personal that is related to a person.Economic entity assumption: This principle is based on a concept when business andowner have separate entities.Cost principle: This principle bound company to record all the assets, liabilities andinvestments at cost in financial statements (Barth, 2015).Full discloser principle: This principle works on the concept of full and accuratediscloser of the information that all the information which is provided to the investor isaccurate. Going concern principle: This principle takes over that a company will move to existlong adequate to carry out its objectives and allegiances and will not pay off in thepredictable future.2

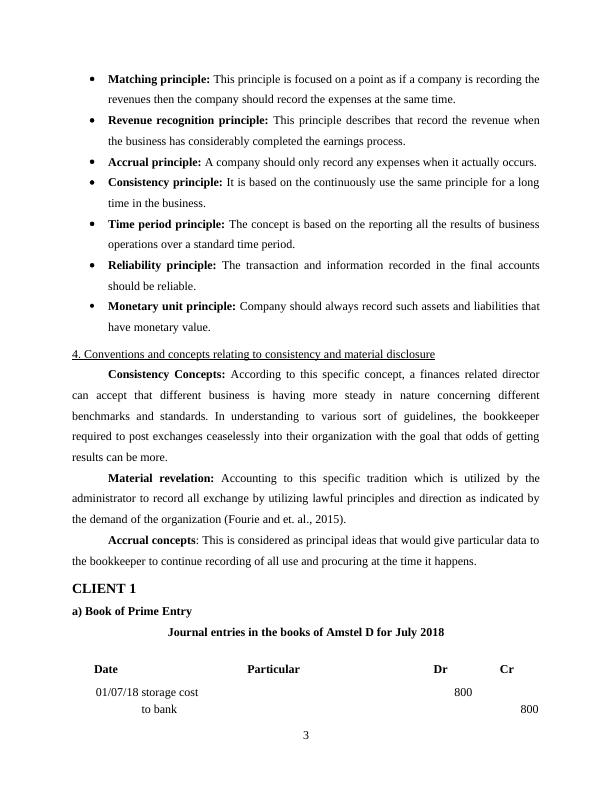

Matching principle: This principle is focused on a point as if a company is recording therevenues then the company should record the expenses at the same time.Revenue recognition principle: This principle describes that record the revenue whenthe business has considerably completed the earnings process.Accrual principle: A company should only record any expenses when it actually occurs.Consistency principle: It is based on the continuously use the same principle for a longtime in the business.Time period principle: The concept is based on the reporting all the results of businessoperations over a standard time period.Reliability principle: The transaction and information recorded in the final accountsshould be reliable.Monetary unit principle: Company should always record such assets and liabilities thathave monetary value.4. Conventions and concepts relating to consistency and material disclosureConsistency Concepts: According to this specific concept, a finances related directorcan accept that different business is having more steady in nature concerning differentbenchmarks and standards. In understanding to various sort of guidelines, the bookkeeperrequired to post exchanges ceaselessly into their organization with the goal that odds of gettingresults can be more. Material revelation: Accounting to this specific tradition which is utilized by theadministrator to record all exchange by utilizing lawful principles and direction as indicated bythe demand of the organization (Fourie and et. al., 2015). Accrual concepts: This is considered as principal ideas that would give particular data tothe bookkeeper to continue recording of all use and procuring at the time it happens.CLIENT 1a) Book of Prime EntryJournal entries in the books of Amstel D for July 2018DateParticularDrCr01/07/18storage cost 800to bank8003

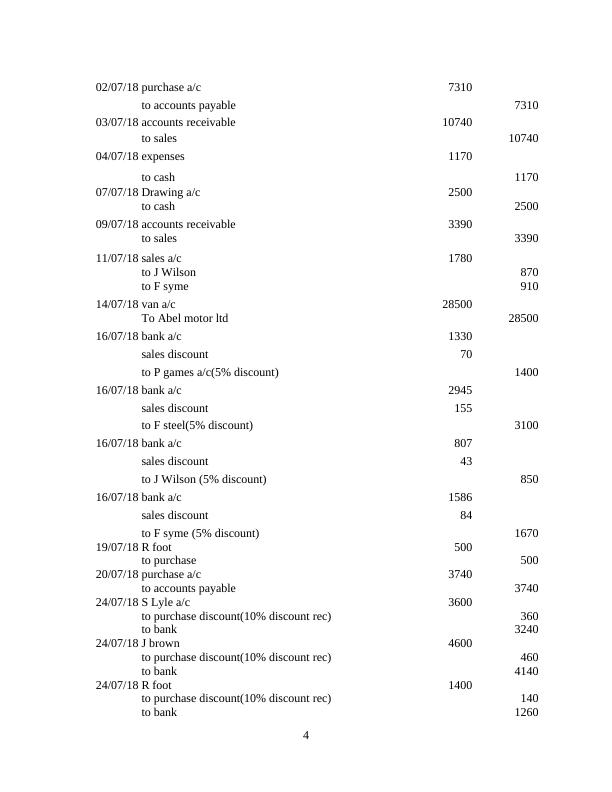

02/07/18purchase a/c7310to accounts payable731003/07/18accounts receivable10740to sales1074004/07/18expenses 1170to cash117007/07/18Drawing a/c2500to cash250009/07/18accounts receivable3390to sales339011/07/18sales a/c 1780to J Wilson870to F syme91014/07/18van a/c 28500To Abel motor ltd 2850016/07/18bank a/c1330sales discount70to P games a/c(5% discount)140016/07/18bank a/c2945sales discount155to F steel(5% discount)310016/07/18bank a/c807sales discount43to J Wilson (5% discount)85016/07/18bank a/c1586sales discount84to F syme (5% discount)167019/07/18R foot500to purchase50020/07/18purchase a/c3740to accounts payable374024/07/18S Lyle a/c 3600to purchase discount(10% discount rec)360to bank324024/07/18J brown4600to purchase discount(10% discount rec)460to bank414024/07/18R foot1400to purchase discount(10% discount rec)140to bank12604

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial accounting table of contents inTRODUCTION 1lg...

|39

|5192

|104

Financial Accounting Principles Assignment - Doclg...

|30

|7212

|286

(PDF) Financial Accounting Principleslg...

|21

|4547

|232

Financial Accounting Principles- Doclg...

|35

|6213

|120

Financial Accounting Principles Assignment (Doc)lg...

|19

|4093

|395

Financial Accounting Principles : Doclg...

|20

|4019

|483