FIN201 Corporate Finance 1: Financial Decision-Making Analysis

VerifiedAdded on 2024/07/03

|12

|1538

|292

Homework Assignment

AI Summary

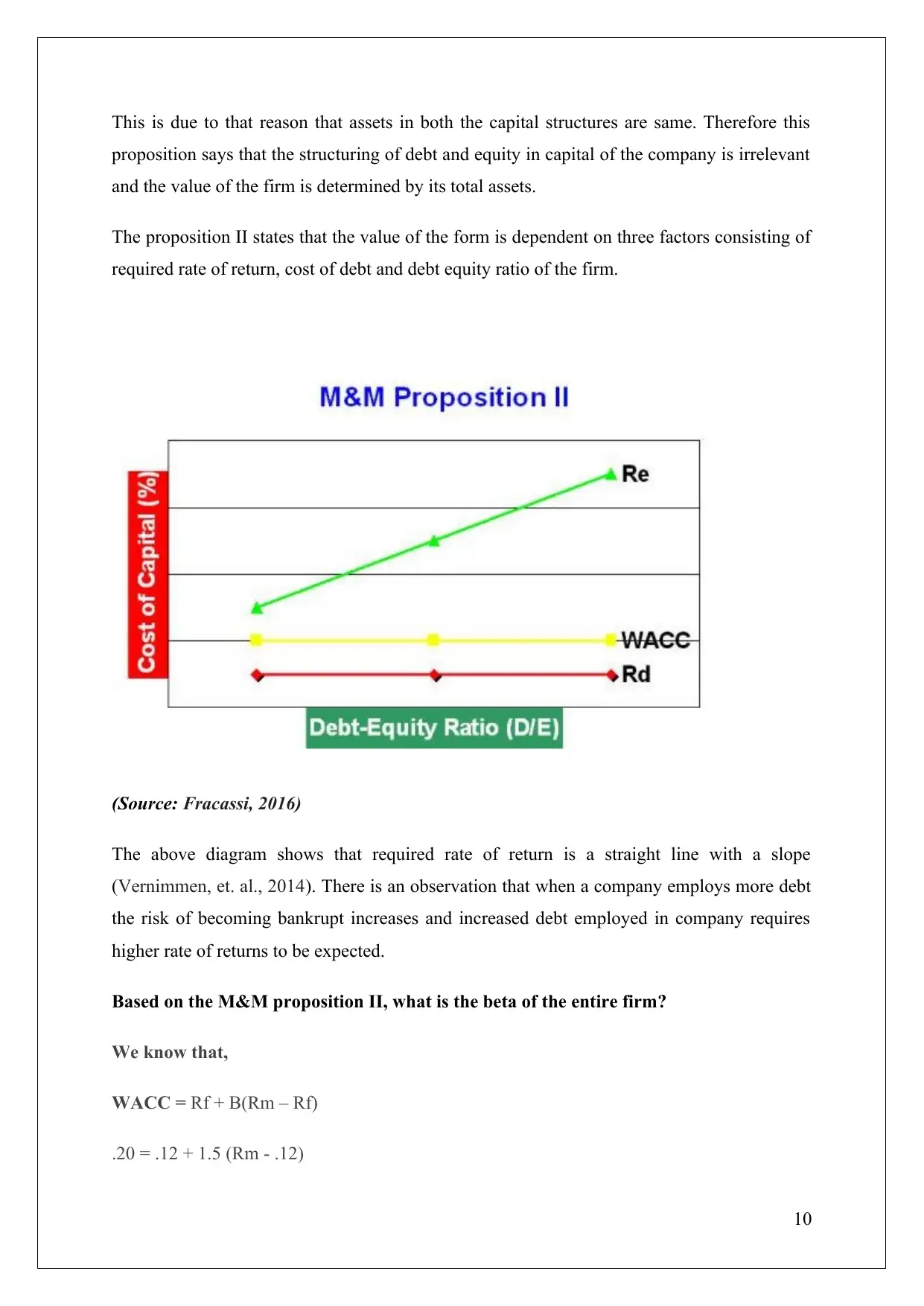

This assignment solution covers key concepts in corporate finance, including investment analysis, bond valuation, and capital budgeting. Question 1 involves calculating future values of deposits and present value of investments, as well as determining yield to maturity and effective annual yield for a bond. Question 2 focuses on project selection using the payback period and NPV rules, highlighting the differences in their conclusions and discussing other evaluation methods like IRR and ARR. Question 3 addresses the weighted average cost of capital (WACC) and cost of equity capital, along with explanations of the Modigliani-Miller (M&M) propositions I, II, and III, including graphical representations and calculations of firm beta. Desklib offers this solution and many more resources to aid students in their studies.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.