Finance Assignment: Financial Valuation, Investment, and Loan Analysis

VerifiedAdded on 2020/03/04

|14

|3299

|87

Homework Assignment

AI Summary

This finance assignment provides detailed solutions to complex financial problems. The assignment covers a range of topics including the two-period certainty model, share valuation, time value of money, deferred perpetuities, loan repayments, and investment choice techniques. It includes calculations for dividends, present value, internal rate of return (IRR), net present value (NPV), bond valuation, and loan amortization schedules. The solutions demonstrate the application of financial formulas and concepts to real-world scenarios, such as investment projects, loan terms, and bond valuation, offering a comprehensive understanding of financial analysis. The assignment includes step-by-step calculations and explanations to help students understand the concepts and problem-solving techniques.

QUESTION `1. [6 + 8 = 14 Marks.]

a) This is a two period certainty model problem.

Assume that William Brown has a sole income from Bobcat Ltd in which he owns

12% of the ordinary share capital.

In its financial year 2016-17 just ended, Bobcat Ltd reported net profits after tax of

$600,000, and announced its net profits after tax expectation for the next financial

year, 2017-18, to be 25% higher than this year’s figure. The company operates with a

dividend payout ratio of 70%, which it plans to continue, and will pay the annual

dividend for 2016-17 in mid-August, 2017, and the dividend for 2017-18 in mid-

August, 2018.

In mid-August, 2018, Jack wishes to spend $100,000, which will include the cost of a

new car.. How much can he consume in mid-August, 2017 if the capital market offers

an interest rate of 9% per year?

Answer:

Dividend payable in Aug. 2017 = Net profits after tax * dividend payout ratio

= $6, 00,000 * 70%

= $4, 20,000

Dividends available to Jack = $4,20,000 * 12%

= $50,400

Net profits after tax in 2018 = $6,00,000 * 1.25

= $7,50,000

Dividend payable in Aug. 2017 = 7,50,000 * 70%

= $5,25,000

Dividends to be available to Jack in 2018 = $5,25,000 * 12%

= $63,000

Present value of dividend = dividend payable in 2018 / (1+rate of interest)^1

= 63000 / 1.09^1

= $57,798.2

Hence total amount available with Jack = $50,400 + $57,798.2

= $1,08,198.16

a) This is a two period certainty model problem.

Assume that William Brown has a sole income from Bobcat Ltd in which he owns

12% of the ordinary share capital.

In its financial year 2016-17 just ended, Bobcat Ltd reported net profits after tax of

$600,000, and announced its net profits after tax expectation for the next financial

year, 2017-18, to be 25% higher than this year’s figure. The company operates with a

dividend payout ratio of 70%, which it plans to continue, and will pay the annual

dividend for 2016-17 in mid-August, 2017, and the dividend for 2017-18 in mid-

August, 2018.

In mid-August, 2018, Jack wishes to spend $100,000, which will include the cost of a

new car.. How much can he consume in mid-August, 2017 if the capital market offers

an interest rate of 9% per year?

Answer:

Dividend payable in Aug. 2017 = Net profits after tax * dividend payout ratio

= $6, 00,000 * 70%

= $4, 20,000

Dividends available to Jack = $4,20,000 * 12%

= $50,400

Net profits after tax in 2018 = $6,00,000 * 1.25

= $7,50,000

Dividend payable in Aug. 2017 = 7,50,000 * 70%

= $5,25,000

Dividends to be available to Jack in 2018 = $5,25,000 * 12%

= $63,000

Present value of dividend = dividend payable in 2018 / (1+rate of interest)^1

= 63000 / 1.09^1

= $57,798.2

Hence total amount available with Jack = $50,400 + $57,798.2

= $1,08,198.16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jack needs to spend $100000 in mid August, hence the amount he can consume today will be

the amount present value of amount available with Jack in 2017 less $100000.

= $1,08,198.16 - $100,000

= $8,198.16

QUESTION 1 continued.

b) This question relates to the valuation of shares.

Big Ideas Ltd has just paid a dividend of $1.20 a share. Investors require a 12% per

annum return on investments such as Big Ideas. What would a share in Big Ideas Ltd

be expected to sell for today (August, 2017) if the dividend is expected to increase by

20% in August, 2018, 15% in August, 2019, 10% in August, 2020 and thereafter by 5

per cent a year forever, from August, 2021 onwards?

Answer:

Year Dividend growth rate Expected dividend

2017 $1.2

2018 20% $1.44

2019 15% $1.65

2020 10% $1.82

2021 5% $1.91

Price of share in year 2020 = expected dividend / (rate of return – growth rate)

= 1.91 / (0.12-0.05)

= $27.32

Price of share in 2017 = D1 / (1+r)^1 + D2 / (1+r)^2 + D3 / (1+r)^3 + P4 / (1+r)^4

= 1.44 / 1.12^1 + 1.65 / 1.12^2 + 1.82 / 1.12^3 + 27.32 / 1.12^3

= $1.28 + $1.31 + $1.29+ $19.44

= $23.32

Question 2

a) This question relates to the time value of money and deferred perpetuities.

the amount present value of amount available with Jack in 2017 less $100000.

= $1,08,198.16 - $100,000

= $8,198.16

QUESTION 1 continued.

b) This question relates to the valuation of shares.

Big Ideas Ltd has just paid a dividend of $1.20 a share. Investors require a 12% per

annum return on investments such as Big Ideas. What would a share in Big Ideas Ltd

be expected to sell for today (August, 2017) if the dividend is expected to increase by

20% in August, 2018, 15% in August, 2019, 10% in August, 2020 and thereafter by 5

per cent a year forever, from August, 2021 onwards?

Answer:

Year Dividend growth rate Expected dividend

2017 $1.2

2018 20% $1.44

2019 15% $1.65

2020 10% $1.82

2021 5% $1.91

Price of share in year 2020 = expected dividend / (rate of return – growth rate)

= 1.91 / (0.12-0.05)

= $27.32

Price of share in 2017 = D1 / (1+r)^1 + D2 / (1+r)^2 + D3 / (1+r)^3 + P4 / (1+r)^4

= 1.44 / 1.12^1 + 1.65 / 1.12^2 + 1.82 / 1.12^3 + 27.32 / 1.12^3

= $1.28 + $1.31 + $1.29+ $19.44

= $23.32

Question 2

a) This question relates to the time value of money and deferred perpetuities.

Colin Greenway attended Bunyip High School in the 1970s. After leaving school,

Colin became a successful entrepreneur and is now very wealthy. He wishes to

establish a perpetual scholarship fund which will provide $10,000 a year, payable to

five high performing students at Bunyip High School each year in Year 12, that is,

$50,000 a year, starting in early 2020. It is now early 2017. The High School

Principal believes that the required funds can be invested at 5 per cent a year in

perpetuity.

i) What is the present value in early 2017 of the whole income stream, and thus

the amount which Colin must contribute to establish the fund?

Answer:

PVof perpetuity in 2020 = C1 / r

= 50000 / 0.05

= $10,00,000

PV of perpetuity in 2017 = PV2020 / (1+r)^3

= 1000000 / 1.05^3

= $ 8,63,837.6

ii) The High School Principal, while most appreciative of Colin’s great

generosity, mentions that fees at Bunyip High are rising on average by 3 per

cent every year because of inflation, and that in several years, $10,000 will not

be enough to keep a student in year 12 for a whole year. Colin decides that he

will increase the amount to establish the fund so as to provide for increases in

the scholarship amount by 3 per cent a year in perpetuity, the first increase

occurring in early 2021. How much extra (above the amount calculated in i)

above, will Colin need to contribute in early 2017 so as to provide for these

inflation increases forever?

[HINT: Consider a formula similar to the dividend growth model.]

Answer:

Colin became a successful entrepreneur and is now very wealthy. He wishes to

establish a perpetual scholarship fund which will provide $10,000 a year, payable to

five high performing students at Bunyip High School each year in Year 12, that is,

$50,000 a year, starting in early 2020. It is now early 2017. The High School

Principal believes that the required funds can be invested at 5 per cent a year in

perpetuity.

i) What is the present value in early 2017 of the whole income stream, and thus

the amount which Colin must contribute to establish the fund?

Answer:

PVof perpetuity in 2020 = C1 / r

= 50000 / 0.05

= $10,00,000

PV of perpetuity in 2017 = PV2020 / (1+r)^3

= 1000000 / 1.05^3

= $ 8,63,837.6

ii) The High School Principal, while most appreciative of Colin’s great

generosity, mentions that fees at Bunyip High are rising on average by 3 per

cent every year because of inflation, and that in several years, $10,000 will not

be enough to keep a student in year 12 for a whole year. Colin decides that he

will increase the amount to establish the fund so as to provide for increases in

the scholarship amount by 3 per cent a year in perpetuity, the first increase

occurring in early 2021. How much extra (above the amount calculated in i)

above, will Colin need to contribute in early 2017 so as to provide for these

inflation increases forever?

[HINT: Consider a formula similar to the dividend growth model.]

Answer:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year Scholarship

amount

PV discounted at 5%

2017

2018 $50,000 $47,619.04

2019 $50,000 $45,351.47

2020 $50,000 $43,191.87

Total PV of cash flows $136,162.4

PV of perpetuity in 2020 = C2 / r-g

Here, the inflation rate is 3% per year starting from 2021. Hence we consider inflation as the

growth rate.

C2 ( cash flow in 2021) = 50000 * 1.03

= $51,500

Hence PV of perpetuity in 2020 = 51500 / (0.05 – 0.03)

= $25,75,000

PV of perpetuity2020 in 2017 = (PV2020 / (1+r)^3 ) + PV of cash flows from 2018 to 2020

= (2575000 / 1.05^3) + $136,162.4

= $2,360,544.21

Extra amount to be contributed by Colin in early 2017 = $2,360,544.21 – 8,63,837.6

= $1,496,707

b) This question relates to loan repayments and loan terms.

Ron and Robin Reid wish to borrow $540,000 to buy a home. The loan from Biggles

Bank requires equal monthly repayments over 20 years, and carries.an interest rate of

7.8% per annum, compounded monthly. The first repayment is due at the end of the

first month.

You are required to calculate:

i) the effective annual interest rate on the above loan.

Answer:

Effective Annual interest rate = [1+ i/n]^n - 1

amount

PV discounted at 5%

2017

2018 $50,000 $47,619.04

2019 $50,000 $45,351.47

2020 $50,000 $43,191.87

Total PV of cash flows $136,162.4

PV of perpetuity in 2020 = C2 / r-g

Here, the inflation rate is 3% per year starting from 2021. Hence we consider inflation as the

growth rate.

C2 ( cash flow in 2021) = 50000 * 1.03

= $51,500

Hence PV of perpetuity in 2020 = 51500 / (0.05 – 0.03)

= $25,75,000

PV of perpetuity2020 in 2017 = (PV2020 / (1+r)^3 ) + PV of cash flows from 2018 to 2020

= (2575000 / 1.05^3) + $136,162.4

= $2,360,544.21

Extra amount to be contributed by Colin in early 2017 = $2,360,544.21 – 8,63,837.6

= $1,496,707

b) This question relates to loan repayments and loan terms.

Ron and Robin Reid wish to borrow $540,000 to buy a home. The loan from Biggles

Bank requires equal monthly repayments over 20 years, and carries.an interest rate of

7.8% per annum, compounded monthly. The first repayment is due at the end of the

first month.

You are required to calculate:

i) the effective annual interest rate on the above loan.

Answer:

Effective Annual interest rate = [1+ i/n]^n - 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

i = 7.8%

n = 12

hence, EAR = [1+ 0.078/12]^12 - 1

= 8.08%

ii) the amount of the monthly repayment (consisting of interest and principal

repayment components) if the same amount is to be repaid every month over

the 20 year period of the loan.

Answer:

PMT = Pi / (1-(1+i)^-n)

P = $540,000

I = 7.8% / 12 = 0.7%

N = 20*12 = 240

PMT = (540000*0.0065) / (1-(1.0065)^-240)

= 3510 / 0.788

= $4,449.7

Hence a monthly repayment of $4,449.7 is to be repaid every month for the 20 year loan

period.

iii) the amount of $X, if - instead of the above - Biggles Bank agrees that Ron and

Robin will repay the loan by paying the bank $3,300 per month for the first 12

months, then $3,750 a month for the next 12 months, and after that $X per

month for the balance of the 20 year term.

Answer:

PV of annuity = C * [(1-(1+i)^-n) / i]

PV of $3300 to be paid for first 12 months = 3300 * [(1-1.0065^-12) / 0.0065]

n = 12

hence, EAR = [1+ 0.078/12]^12 - 1

= 8.08%

ii) the amount of the monthly repayment (consisting of interest and principal

repayment components) if the same amount is to be repaid every month over

the 20 year period of the loan.

Answer:

PMT = Pi / (1-(1+i)^-n)

P = $540,000

I = 7.8% / 12 = 0.7%

N = 20*12 = 240

PMT = (540000*0.0065) / (1-(1.0065)^-240)

= 3510 / 0.788

= $4,449.7

Hence a monthly repayment of $4,449.7 is to be repaid every month for the 20 year loan

period.

iii) the amount of $X, if - instead of the above - Biggles Bank agrees that Ron and

Robin will repay the loan by paying the bank $3,300 per month for the first 12

months, then $3,750 a month for the next 12 months, and after that $X per

month for the balance of the 20 year term.

Answer:

PV of annuity = C * [(1-(1+i)^-n) / i]

PV of $3300 to be paid for first 12 months = 3300 * [(1-1.0065^-12) / 0.0065]

= $37,976.43

PV of $3750 to be paid for next 12 months = 3750 * [(1-1.0065^-12) / 0.0065]

= $43,155.04

PV of deferred annuity = 43155.04 / (1.0065)^12

= $39,926.96

PV of payments made in 2 years = $37,976.43 + $39,926.96

= $77,903.4

Total amount to be paid by end of 20 years = 4,449.7 * 240 = $10,67,928

Hence, balance amount to be paid = $10,67,928 - $77,903.4

= $9,90,025

Let X be the amount to be paid per month for the rest of the period

PV of annuity for 18 years = X * [(1-1.0065^-216) / 0.0065]

= 115.88 X

PV of deferred annuity = 115.88X / (1.0065^24)

990025 = 115.88X / 1.17

X = $9,980.86

Hence, an installment of $9980.8 will be paid after two years for a period of 18 years.

iv) how long (in years and months) it would take to repay the loan if,

alternatively, Ron and Robin decide to repay $2,500 per month, with the first

repayment again being at the end of the first month after taking the loan, and

continuing until the loan was repaid.

Answer:

The question has given the loan installment of $2500 which is not possible because the

monthly interest on the loan itself is $3,510; hence we are assuming a print mistake and

taking the installment as $25,000.

25000 = (540000*0.0065) / (1-(1.0065)^-n)

25000 = 3510 / (1-(1.0065)^-n)

1-(1.0065) ^-n = 0.14

PV of $3750 to be paid for next 12 months = 3750 * [(1-1.0065^-12) / 0.0065]

= $43,155.04

PV of deferred annuity = 43155.04 / (1.0065)^12

= $39,926.96

PV of payments made in 2 years = $37,976.43 + $39,926.96

= $77,903.4

Total amount to be paid by end of 20 years = 4,449.7 * 240 = $10,67,928

Hence, balance amount to be paid = $10,67,928 - $77,903.4

= $9,90,025

Let X be the amount to be paid per month for the rest of the period

PV of annuity for 18 years = X * [(1-1.0065^-216) / 0.0065]

= 115.88 X

PV of deferred annuity = 115.88X / (1.0065^24)

990025 = 115.88X / 1.17

X = $9,980.86

Hence, an installment of $9980.8 will be paid after two years for a period of 18 years.

iv) how long (in years and months) it would take to repay the loan if,

alternatively, Ron and Robin decide to repay $2,500 per month, with the first

repayment again being at the end of the first month after taking the loan, and

continuing until the loan was repaid.

Answer:

The question has given the loan installment of $2500 which is not possible because the

monthly interest on the loan itself is $3,510; hence we are assuming a print mistake and

taking the installment as $25,000.

25000 = (540000*0.0065) / (1-(1.0065)^-n)

25000 = 3510 / (1-(1.0065)^-n)

1-(1.0065) ^-n = 0.14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

n = 24

hence number of years taken to repay the loan = 2 years

v) under option iv) above, the amount of the final repayment. [NOTE: Towards

the end of the loan repayment period, after the final full monthly instalment of

$2,500 is paid, a lesser amount is likely to be outstanding. That amount, plus

interest to the end of the following month, is the final loan repayment

amount.]

Answer:

The full payment has been made in the last month of the second year. Hence, there is no

amount outstanding in the following month.

Question 3

a) This question relates to alternative investment choice techniques

Stanley Livingstone is considering the following cash flows for two mutually

exclusive projects.

Year Cash Flows, Investment X ($) Cash Flows, Investment Y ($)

0 -40,000 -40,000

1 12,000 18,000

2 18,000 18,000

3 27,000 18,000

You are required to answer the following questions:

i) If the cash flows after year 0 occur evenly over each year, what is the payback

period for each project, and on this basis, which project would you prefer?

Answer:

hence number of years taken to repay the loan = 2 years

v) under option iv) above, the amount of the final repayment. [NOTE: Towards

the end of the loan repayment period, after the final full monthly instalment of

$2,500 is paid, a lesser amount is likely to be outstanding. That amount, plus

interest to the end of the following month, is the final loan repayment

amount.]

Answer:

The full payment has been made in the last month of the second year. Hence, there is no

amount outstanding in the following month.

Question 3

a) This question relates to alternative investment choice techniques

Stanley Livingstone is considering the following cash flows for two mutually

exclusive projects.

Year Cash Flows, Investment X ($) Cash Flows, Investment Y ($)

0 -40,000 -40,000

1 12,000 18,000

2 18,000 18,000

3 27,000 18,000

You are required to answer the following questions:

i) If the cash flows after year 0 occur evenly over each year, what is the payback

period for each project, and on this basis, which project would you prefer?

Answer:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

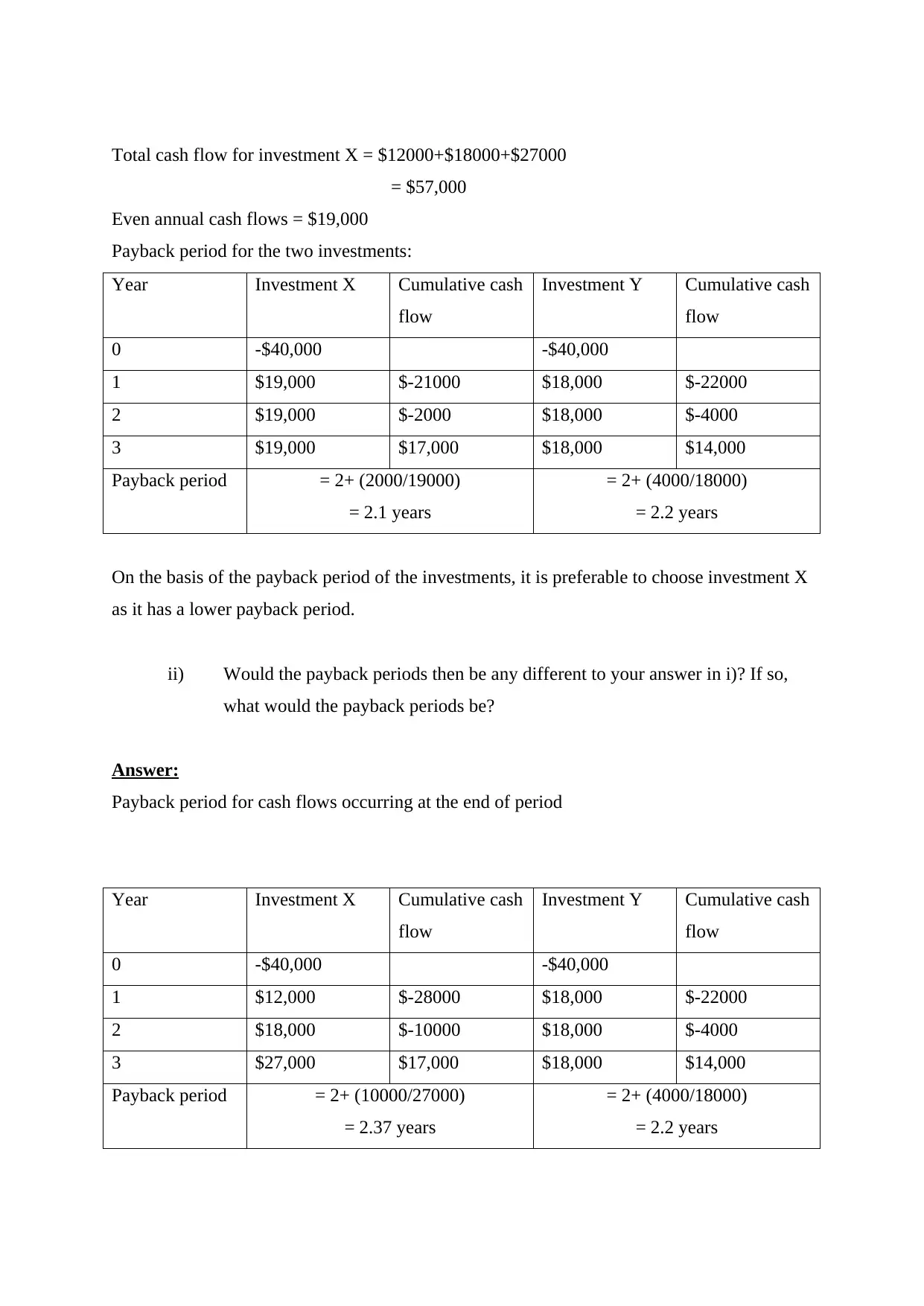

Total cash flow for investment X = $12000+$18000+$27000

= $57,000

Even annual cash flows = $19,000

Payback period for the two investments:

Year Investment X Cumulative cash

flow

Investment Y Cumulative cash

flow

0 -$40,000 -$40,000

1 $19,000 $-21000 $18,000 $-22000

2 $19,000 $-2000 $18,000 $-4000

3 $19,000 $17,000 $18,000 $14,000

Payback period = 2+ (2000/19000)

= 2.1 years

= 2+ (4000/18000)

= 2.2 years

On the basis of the payback period of the investments, it is preferable to choose investment X

as it has a lower payback period.

ii) Would the payback periods then be any different to your answer in i)? If so,

what would the payback periods be?

Answer:

Payback period for cash flows occurring at the end of period

Year Investment X Cumulative cash

flow

Investment Y Cumulative cash

flow

0 -$40,000 -$40,000

1 $12,000 $-28000 $18,000 $-22000

2 $18,000 $-10000 $18,000 $-4000

3 $27,000 $17,000 $18,000 $14,000

Payback period = 2+ (10000/27000)

= 2.37 years

= 2+ (4000/18000)

= 2.2 years

= $57,000

Even annual cash flows = $19,000

Payback period for the two investments:

Year Investment X Cumulative cash

flow

Investment Y Cumulative cash

flow

0 -$40,000 -$40,000

1 $19,000 $-21000 $18,000 $-22000

2 $19,000 $-2000 $18,000 $-4000

3 $19,000 $17,000 $18,000 $14,000

Payback period = 2+ (2000/19000)

= 2.1 years

= 2+ (4000/18000)

= 2.2 years

On the basis of the payback period of the investments, it is preferable to choose investment X

as it has a lower payback period.

ii) Would the payback periods then be any different to your answer in i)? If so,

what would the payback periods be?

Answer:

Payback period for cash flows occurring at the end of period

Year Investment X Cumulative cash

flow

Investment Y Cumulative cash

flow

0 -$40,000 -$40,000

1 $12,000 $-28000 $18,000 $-22000

2 $18,000 $-10000 $18,000 $-4000

3 $27,000 $17,000 $18,000 $14,000

Payback period = 2+ (10000/27000)

= 2.37 years

= 2+ (4000/18000)

= 2.2 years

The payback period for investment X has increased as a result of uneven cash flows, hence

now it is preferable to go with investment Y.

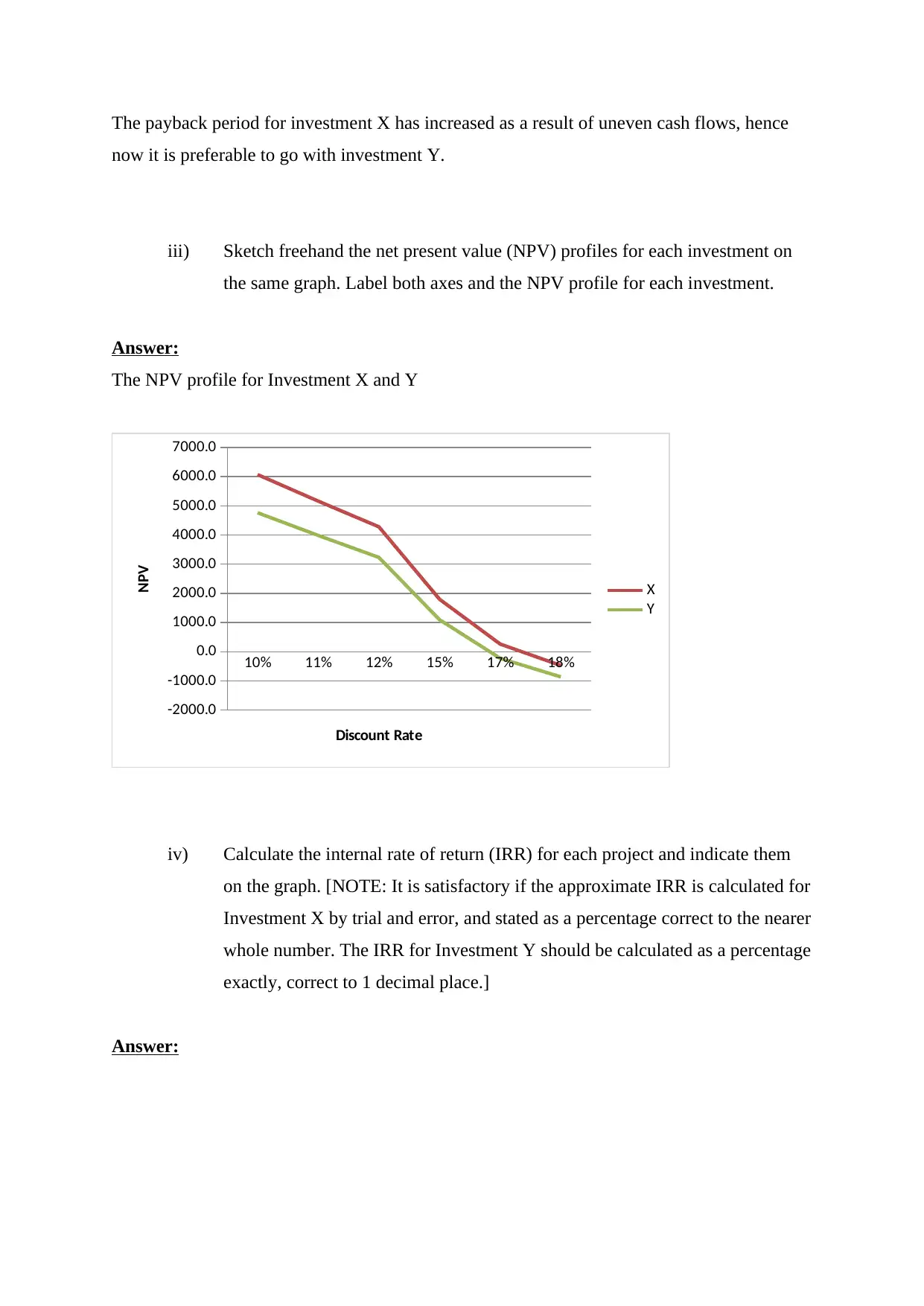

iii) Sketch freehand the net present value (NPV) profiles for each investment on

the same graph. Label both axes and the NPV profile for each investment.

Answer:

The NPV profile for Investment X and Y

10% 11% 12% 15% 17% 18%

-2000.0

-1000.0

0.0

1000.0

2000.0

3000.0

4000.0

5000.0

6000.0

7000.0

X

Y

Discount Rate

NPV

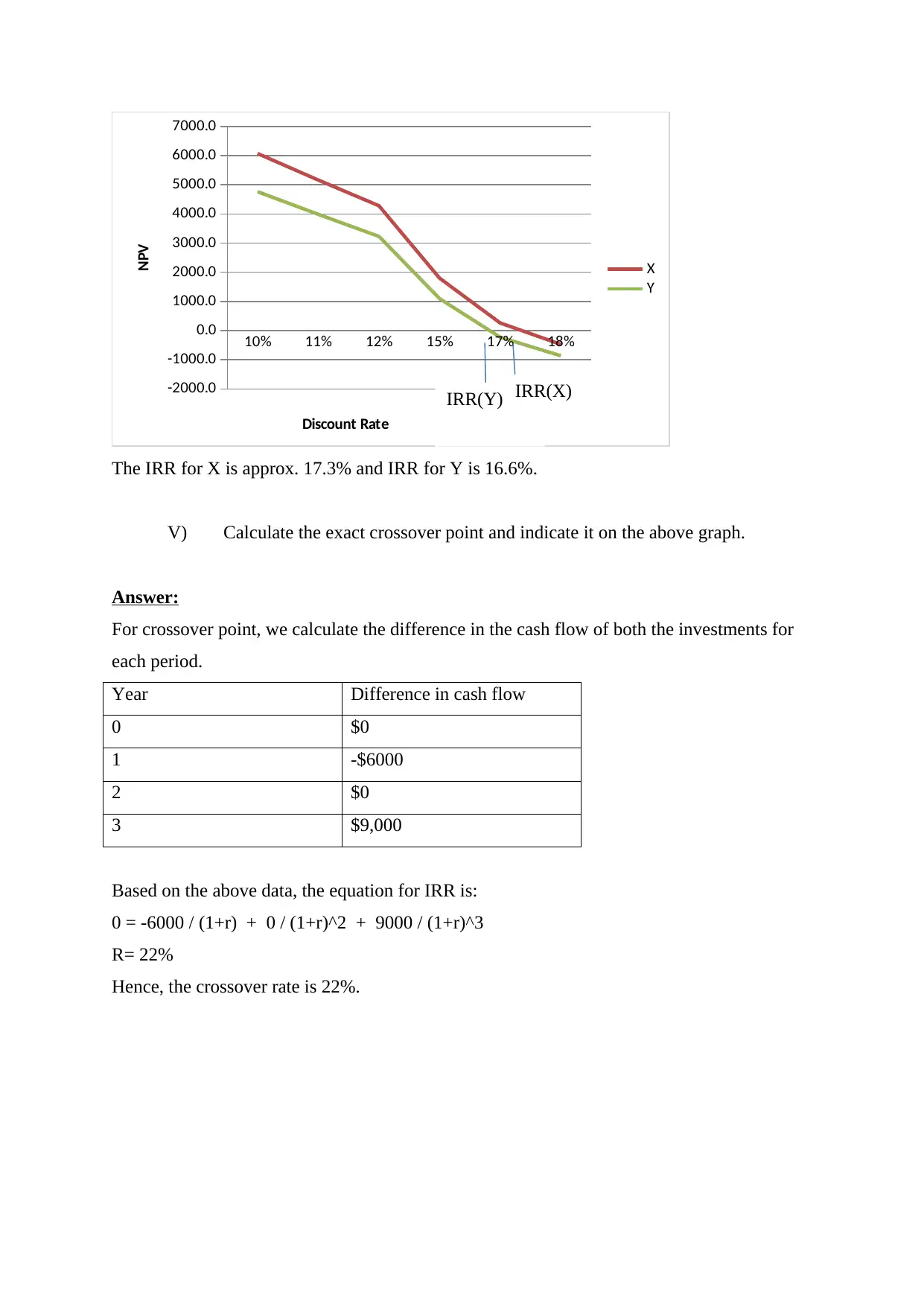

iv) Calculate the internal rate of return (IRR) for each project and indicate them

on the graph. [NOTE: It is satisfactory if the approximate IRR is calculated for

Investment X by trial and error, and stated as a percentage correct to the nearer

whole number. The IRR for Investment Y should be calculated as a percentage

exactly, correct to 1 decimal place.]

Answer:

now it is preferable to go with investment Y.

iii) Sketch freehand the net present value (NPV) profiles for each investment on

the same graph. Label both axes and the NPV profile for each investment.

Answer:

The NPV profile for Investment X and Y

10% 11% 12% 15% 17% 18%

-2000.0

-1000.0

0.0

1000.0

2000.0

3000.0

4000.0

5000.0

6000.0

7000.0

X

Y

Discount Rate

NPV

iv) Calculate the internal rate of return (IRR) for each project and indicate them

on the graph. [NOTE: It is satisfactory if the approximate IRR is calculated for

Investment X by trial and error, and stated as a percentage correct to the nearer

whole number. The IRR for Investment Y should be calculated as a percentage

exactly, correct to 1 decimal place.]

Answer:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10% 11% 12% 15% 17% 18%

-2000.0

-1000.0

0.0

1000.0

2000.0

3000.0

4000.0

5000.0

6000.0

7000.0

X

Y

Discount Rate

NPV

The IRR for X is approx. 17.3% and IRR for Y is 16.6%.

V) Calculate the exact crossover point and indicate it on the above graph.

Answer:

For crossover point, we calculate the difference in the cash flow of both the investments for

each period.

Year Difference in cash flow

0 $0

1 -$6000

2 $0

3 $9,000

Based on the above data, the equation for IRR is:

0 = -6000 / (1+r) + 0 / (1+r)^2 + 9000 / (1+r)^3

R= 22%

Hence, the crossover rate is 22%.

IRR(Y) IRR(X)

-2000.0

-1000.0

0.0

1000.0

2000.0

3000.0

4000.0

5000.0

6000.0

7000.0

X

Y

Discount Rate

NPV

The IRR for X is approx. 17.3% and IRR for Y is 16.6%.

V) Calculate the exact crossover point and indicate it on the above graph.

Answer:

For crossover point, we calculate the difference in the cash flow of both the investments for

each period.

Year Difference in cash flow

0 $0

1 -$6000

2 $0

3 $9,000

Based on the above data, the equation for IRR is:

0 = -6000 / (1+r) + 0 / (1+r)^2 + 9000 / (1+r)^3

R= 22%

Hence, the crossover rate is 22%.

IRR(Y) IRR(X)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10% 11% 12% 15% 17% 18% 22%

-4000.0

-2000.0

0.0

2000.0

4000.0

6000.0

8000.0

X

Y

Discount Rate

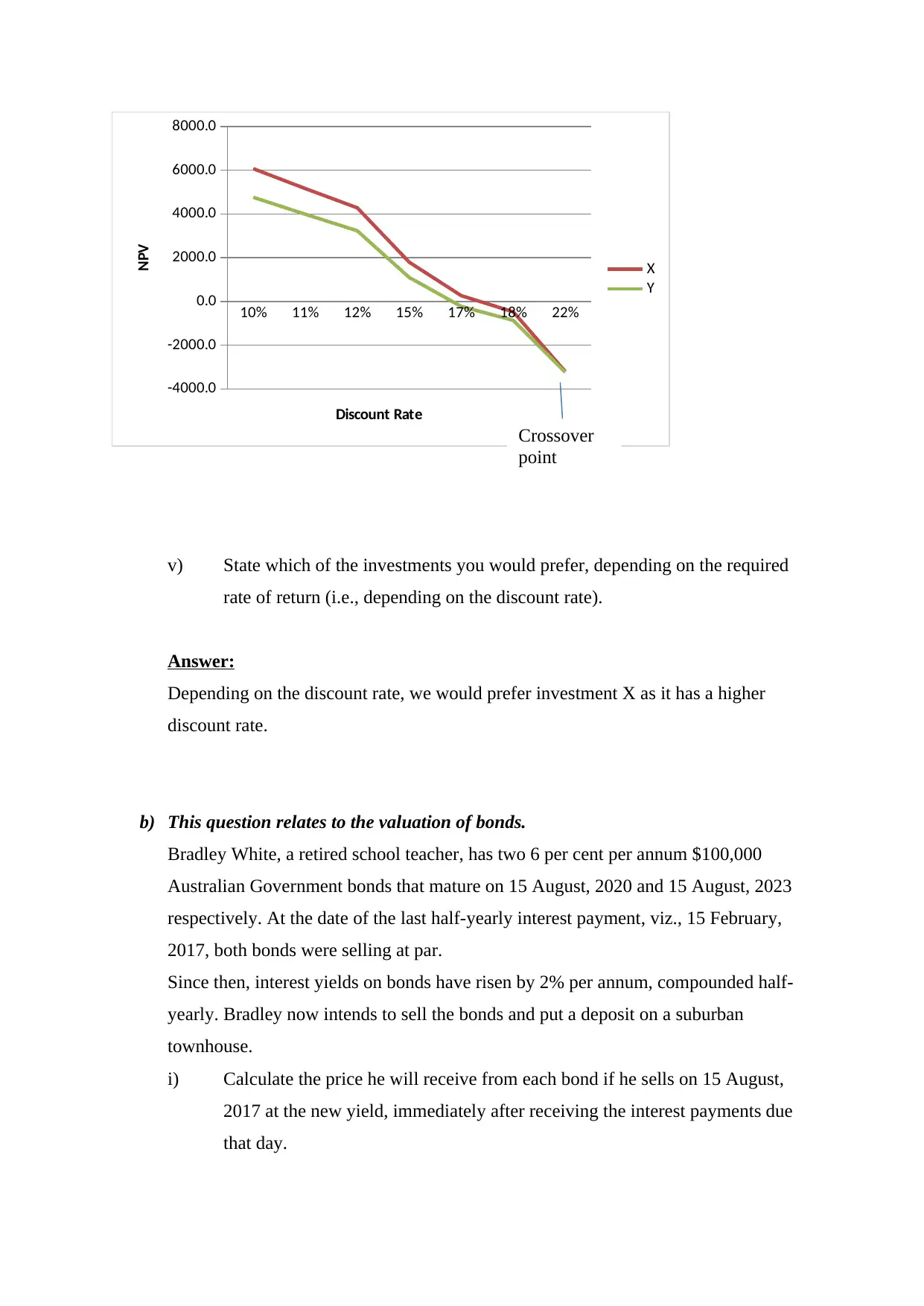

NPV

v) State which of the investments you would prefer, depending on the required

rate of return (i.e., depending on the discount rate).

Answer:

Depending on the discount rate, we would prefer investment X as it has a higher

discount rate.

b) This question relates to the valuation of bonds.

Bradley White, a retired school teacher, has two 6 per cent per annum $100,000

Australian Government bonds that mature on 15 August, 2020 and 15 August, 2023

respectively. At the date of the last half-yearly interest payment, viz., 15 February,

2017, both bonds were selling at par.

Since then, interest yields on bonds have risen by 2% per annum, compounded half-

yearly. Bradley now intends to sell the bonds and put a deposit on a suburban

townhouse.

i) Calculate the price he will receive from each bond if he sells on 15 August,

2017 at the new yield, immediately after receiving the interest payments due

that day.

Crossover

point

-4000.0

-2000.0

0.0

2000.0

4000.0

6000.0

8000.0

X

Y

Discount Rate

NPV

v) State which of the investments you would prefer, depending on the required

rate of return (i.e., depending on the discount rate).

Answer:

Depending on the discount rate, we would prefer investment X as it has a higher

discount rate.

b) This question relates to the valuation of bonds.

Bradley White, a retired school teacher, has two 6 per cent per annum $100,000

Australian Government bonds that mature on 15 August, 2020 and 15 August, 2023

respectively. At the date of the last half-yearly interest payment, viz., 15 February,

2017, both bonds were selling at par.

Since then, interest yields on bonds have risen by 2% per annum, compounded half-

yearly. Bradley now intends to sell the bonds and put a deposit on a suburban

townhouse.

i) Calculate the price he will receive from each bond if he sells on 15 August,

2017 at the new yield, immediately after receiving the interest payments due

that day.

Crossover

point

Answer:

Price of bond = C * F * [(1-(1+r)^-t] / r + F / (1+r)^t

We assume the face value of the bond to be $1000 as it is the standard price of a bond.

Yield on bond expiring in 2020 when selling at par in Feb, 2017:

1000 = 3%*1000 * [(1-(1+r)^-7] / r + 1000 / (1+r)^7

R = 3%

Hence, the semi annual yield on bond is 3%.

Yield on bond expiring in 2023 when selling at par in Feb, 2017:

1000 = 3%*1000 * [(1-(1+r)^-13] / r + 1000 / (1+r)^13

R = 3%

New yield on bond expiring in 2020 = 3% + 3% = 6%

Price of 1st bond = 30 * [(1-(1+0.06)^-7] / 0.06 + 1000 / (1+0.06)^7

= $832.52

New yield on bond expiring in 2023= 3% + 6% = 9%

Price of 2nd bond = 30 * [(1-(1+0.09)^-13] / 0.04 + 1000 / (1+0.09)^13

= $477.16

ii) Explain the relative price movements in the two bonds, as evidenced in your

answer to above.

Answer:

Price of bond = C * F * [(1-(1+r)^-t] / r + F / (1+r)^t

We assume the face value of the bond to be $1000 as it is the standard price of a bond.

Yield on bond expiring in 2020 when selling at par in Feb, 2017:

1000 = 3%*1000 * [(1-(1+r)^-7] / r + 1000 / (1+r)^7

R = 3%

Hence, the semi annual yield on bond is 3%.

Yield on bond expiring in 2023 when selling at par in Feb, 2017:

1000 = 3%*1000 * [(1-(1+r)^-13] / r + 1000 / (1+r)^13

R = 3%

New yield on bond expiring in 2020 = 3% + 3% = 6%

Price of 1st bond = 30 * [(1-(1+0.06)^-7] / 0.06 + 1000 / (1+0.06)^7

= $832.52

New yield on bond expiring in 2023= 3% + 6% = 9%

Price of 2nd bond = 30 * [(1-(1+0.09)^-13] / 0.04 + 1000 / (1+0.09)^13

= $477.16

ii) Explain the relative price movements in the two bonds, as evidenced in your

answer to above.

Answer:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.