Final Accounts: Sole Traders and Partnership Financial Statements

VerifiedAdded on 2020/10/22

|19

|4397

|396

Report

AI Summary

This report comprehensively addresses the preparation of final accounts for sole traders and partnerships, covering key aspects such as closing accounts, producing trial balances, and constructing accounts from incomplete records. It delves into the processes and limitations of preparing final accounts, including profit and loss statements and balance sheets. The report explores methods for calculating opening and closing capital, as well as cash and account balances using incomplete information. It also covers the preparation of sales and purchases ledger control accounts, calculation of account balances using markups and margins, and the key components of partnership agreements and accounts. Furthermore, it addresses the preparation of profit and loss appropriation accounts, the allocation of profit to partners, and the preparation of capital and current accounts. Finally, the report concludes with the calculation of closing balances and the preparation of the statement of financial position, providing a thorough understanding of financial reporting for these business structures.

FINAL ACCOUNTS FOR

SOLE TRADERS AND

PARTNERSHIPS

SOLE TRADERS AND

PARTNERSHIPS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Identify the reasons for closing off accounts and producing a trial balance....................1

1.2 The process, and limitations, of preparing a set of final accounts from a trial balance.. .1

1.3 Describe the methods of constructing accounts from incomplete records.......................2

1.4 Provide reasons for imbalances resulting from incorrect double entries.........................3

1.5 Provide reasons for incomplete records arising from insufficient data and inconsistencies

within the data provided.........................................................................................................3

TASK 2............................................................................................................................................3

2.1 Calculate opening and/or closing capital using incomplete information.........................3

2.2 Calculate opening and/or closing cash/account balance using incomplete information. .4

2.3 Prepare sales and purchases ledger control accounts to calculate sales, purchases and bank

figures.....................................................................................................................................4

2.4 Calculation of account balances using mark ups and margins.........................................5

TASK 3............................................................................................................................................6

3.1 Components of final Account...........................................................................................6

3.2 Profit and loss statement of Sole proprietor.....................................................................6

3.3 Balance sheet of the company..........................................................................................8

TASK 4............................................................................................................................................9

4.1 Key components of partnership agreement......................................................................9

4.2 Describe key components of partnership accounts.......................................................10

TASK 5..........................................................................................................................................11

5.1 Preparation of Profit and Loss Appropriation Account:.................................................11

5.2 Allocation of profit to partners after allowing for interest on capital, interest on drawings

and any salary paid to partner(s)..........................................................................................13

5.3 Preparation of capital and current accounts for each partner:........................................13

TASK 6..........................................................................................................................................14

6.1 Calculation of closing balances on each partner's capital and current accounts............14

6.2 Preparation of statement of financial position................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Identify the reasons for closing off accounts and producing a trial balance....................1

1.2 The process, and limitations, of preparing a set of final accounts from a trial balance.. .1

1.3 Describe the methods of constructing accounts from incomplete records.......................2

1.4 Provide reasons for imbalances resulting from incorrect double entries.........................3

1.5 Provide reasons for incomplete records arising from insufficient data and inconsistencies

within the data provided.........................................................................................................3

TASK 2............................................................................................................................................3

2.1 Calculate opening and/or closing capital using incomplete information.........................3

2.2 Calculate opening and/or closing cash/account balance using incomplete information. .4

2.3 Prepare sales and purchases ledger control accounts to calculate sales, purchases and bank

figures.....................................................................................................................................4

2.4 Calculation of account balances using mark ups and margins.........................................5

TASK 3............................................................................................................................................6

3.1 Components of final Account...........................................................................................6

3.2 Profit and loss statement of Sole proprietor.....................................................................6

3.3 Balance sheet of the company..........................................................................................8

TASK 4............................................................................................................................................9

4.1 Key components of partnership agreement......................................................................9

4.2 Describe key components of partnership accounts.......................................................10

TASK 5..........................................................................................................................................11

5.1 Preparation of Profit and Loss Appropriation Account:.................................................11

5.2 Allocation of profit to partners after allowing for interest on capital, interest on drawings

and any salary paid to partner(s)..........................................................................................13

5.3 Preparation of capital and current accounts for each partner:........................................13

TASK 6..........................................................................................................................................14

6.1 Calculation of closing balances on each partner's capital and current accounts............14

6.2 Preparation of statement of financial position................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Final accounts prepare at the end of financial year and it shows the financial position of

the sole traders and partnership firm (Bull, 2014). These accounts include such as trading, profit

and loss account and balance sheet. It is prepare with the help of necessary records and

transactions. These statements will provide a base for the sole traders as well as for partners to

build strategies and take decision on the basis of available data. Trading accounts provide gross

profit of the company which is related to the operating activities and it is also called primary

accounts. Profit and loss account will include all the expenses and revenues of the company

which is generated by at the time of selling and distributing products. Balance sheet is the last

final accounts or it is also last process of identifying company's actual position. This report

include all the statements of final accounts in respect of sole traders and partnership firm. It is

also involve the legal requirements of partnership firms and it's components.

TASK 1

1.1 Identify the reasons for closing off accounts and producing a trial balance

For sole traders and partnership it is of utmost importance to close off accounts and

producing trial balance. Ledgers in sole proprietorship are closed at the end of the year so as to

check the balance amount that is available in a particular ledger. A trial balance is a list of all the

balances in the nominal ledger accounts. It helps to check that every ledger in the book is closed

and are matched with a counter entry if required. This helps the sole traders to prove the

arithmetical accuracy for the accounts that they have developed. Also this helps to locate if there

is no accounting errors while recording or at the time of book keeping process.

1.2 The process, and limitations, of preparing a set of final accounts from a trial balance.

The process of preparation of final statements to accounts from trial balance is crucial

task that helps the organisation to know the current position of the business that it operates in.

There are various steps that are followed to prepare final accounts from trial balance which

includes the following:

First step includes the reading the list of items that are their in trial balance.

After this for preparing income statement, the accountant has to record all the debit

entries in the trial balance which are of in the nature of expense to the debit side of

income statements and do the same for recording incomes.

1

Final accounts prepare at the end of financial year and it shows the financial position of

the sole traders and partnership firm (Bull, 2014). These accounts include such as trading, profit

and loss account and balance sheet. It is prepare with the help of necessary records and

transactions. These statements will provide a base for the sole traders as well as for partners to

build strategies and take decision on the basis of available data. Trading accounts provide gross

profit of the company which is related to the operating activities and it is also called primary

accounts. Profit and loss account will include all the expenses and revenues of the company

which is generated by at the time of selling and distributing products. Balance sheet is the last

final accounts or it is also last process of identifying company's actual position. This report

include all the statements of final accounts in respect of sole traders and partnership firm. It is

also involve the legal requirements of partnership firms and it's components.

TASK 1

1.1 Identify the reasons for closing off accounts and producing a trial balance

For sole traders and partnership it is of utmost importance to close off accounts and

producing trial balance. Ledgers in sole proprietorship are closed at the end of the year so as to

check the balance amount that is available in a particular ledger. A trial balance is a list of all the

balances in the nominal ledger accounts. It helps to check that every ledger in the book is closed

and are matched with a counter entry if required. This helps the sole traders to prove the

arithmetical accuracy for the accounts that they have developed. Also this helps to locate if there

is no accounting errors while recording or at the time of book keeping process.

1.2 The process, and limitations, of preparing a set of final accounts from a trial balance.

The process of preparation of final statements to accounts from trial balance is crucial

task that helps the organisation to know the current position of the business that it operates in.

There are various steps that are followed to prepare final accounts from trial balance which

includes the following:

First step includes the reading the list of items that are their in trial balance.

After this for preparing income statement, the accountant has to record all the debit

entries in the trial balance which are of in the nature of expense to the debit side of

income statements and do the same for recording incomes.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

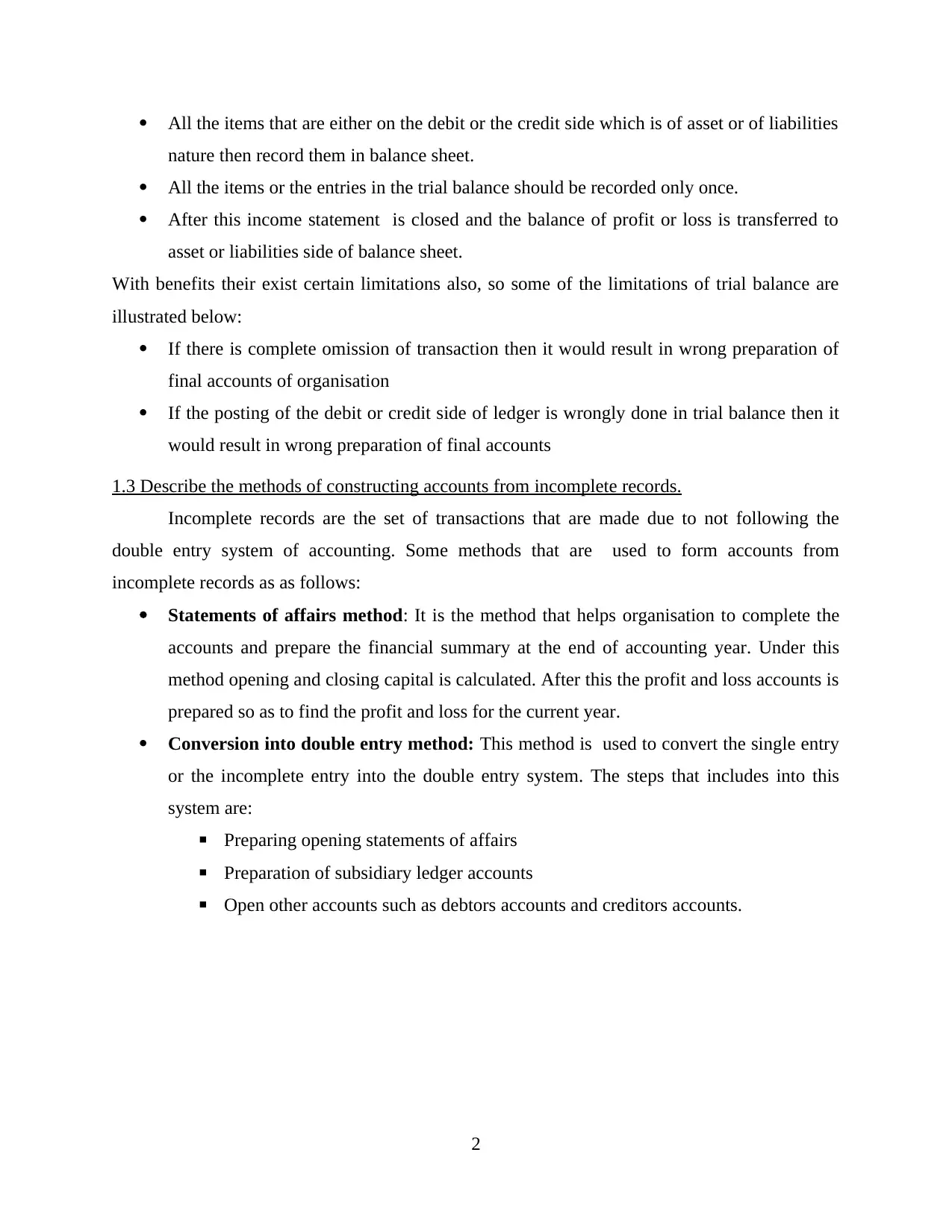

All the items that are either on the debit or the credit side which is of asset or of liabilities

nature then record them in balance sheet.

All the items or the entries in the trial balance should be recorded only once.

After this income statement is closed and the balance of profit or loss is transferred to

asset or liabilities side of balance sheet.

With benefits their exist certain limitations also, so some of the limitations of trial balance are

illustrated below:

If there is complete omission of transaction then it would result in wrong preparation of

final accounts of organisation

If the posting of the debit or credit side of ledger is wrongly done in trial balance then it

would result in wrong preparation of final accounts

1.3 Describe the methods of constructing accounts from incomplete records.

Incomplete records are the set of transactions that are made due to not following the

double entry system of accounting. Some methods that are used to form accounts from

incomplete records as as follows:

Statements of affairs method: It is the method that helps organisation to complete the

accounts and prepare the financial summary at the end of accounting year. Under this

method opening and closing capital is calculated. After this the profit and loss accounts is

prepared so as to find the profit and loss for the current year.

Conversion into double entry method: This method is used to convert the single entry

or the incomplete entry into the double entry system. The steps that includes into this

system are:

▪ Preparing opening statements of affairs

▪ Preparation of subsidiary ledger accounts

▪ Open other accounts such as debtors accounts and creditors accounts.

2

nature then record them in balance sheet.

All the items or the entries in the trial balance should be recorded only once.

After this income statement is closed and the balance of profit or loss is transferred to

asset or liabilities side of balance sheet.

With benefits their exist certain limitations also, so some of the limitations of trial balance are

illustrated below:

If there is complete omission of transaction then it would result in wrong preparation of

final accounts of organisation

If the posting of the debit or credit side of ledger is wrongly done in trial balance then it

would result in wrong preparation of final accounts

1.3 Describe the methods of constructing accounts from incomplete records.

Incomplete records are the set of transactions that are made due to not following the

double entry system of accounting. Some methods that are used to form accounts from

incomplete records as as follows:

Statements of affairs method: It is the method that helps organisation to complete the

accounts and prepare the financial summary at the end of accounting year. Under this

method opening and closing capital is calculated. After this the profit and loss accounts is

prepared so as to find the profit and loss for the current year.

Conversion into double entry method: This method is used to convert the single entry

or the incomplete entry into the double entry system. The steps that includes into this

system are:

▪ Preparing opening statements of affairs

▪ Preparation of subsidiary ledger accounts

▪ Open other accounts such as debtors accounts and creditors accounts.

2

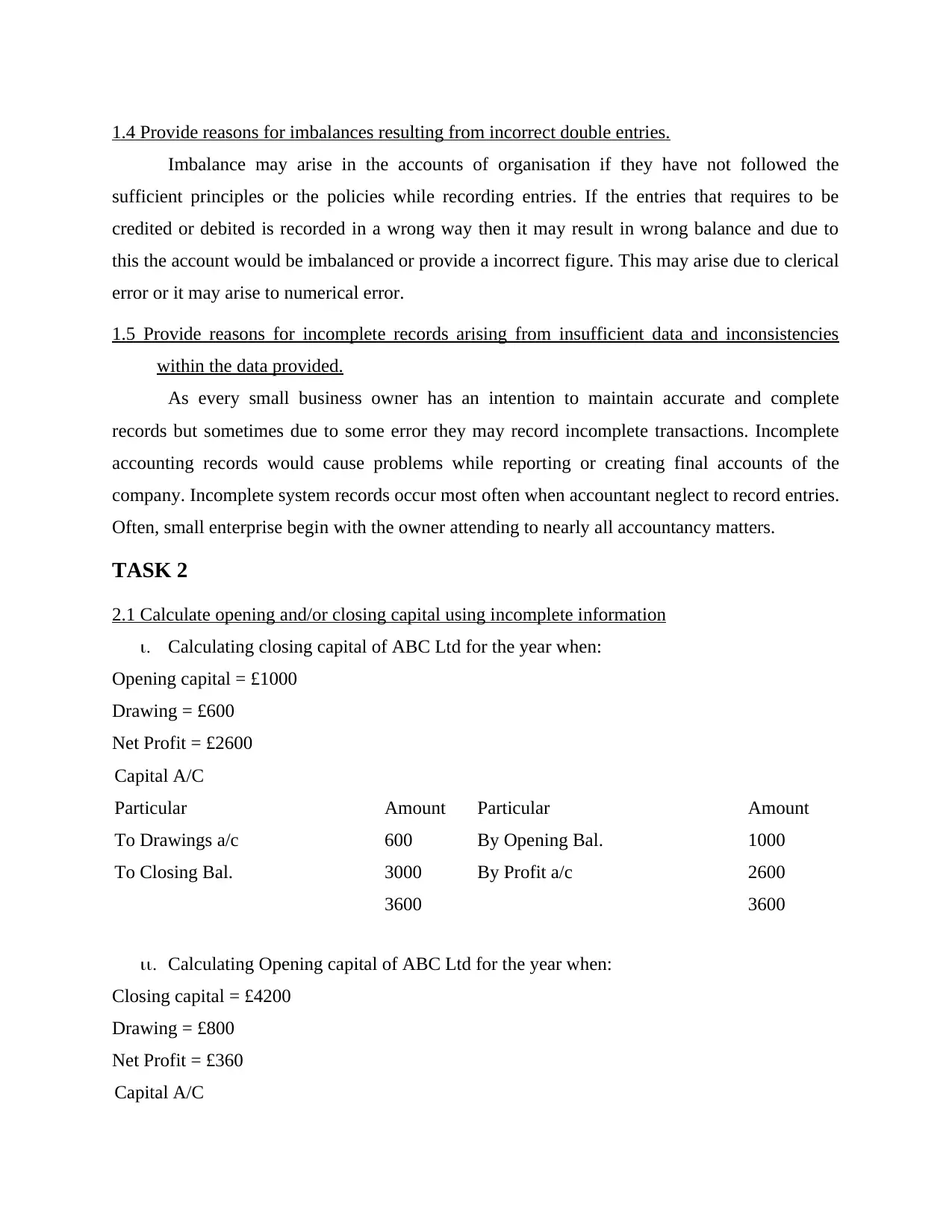

1.4 Provide reasons for imbalances resulting from incorrect double entries.

Imbalance may arise in the accounts of organisation if they have not followed the

sufficient principles or the policies while recording entries. If the entries that requires to be

credited or debited is recorded in a wrong way then it may result in wrong balance and due to

this the account would be imbalanced or provide a incorrect figure. This may arise due to clerical

error or it may arise to numerical error.

1.5 Provide reasons for incomplete records arising from insufficient data and inconsistencies

within the data provided.

As every small business owner has an intention to maintain accurate and complete

records but sometimes due to some error they may record incomplete transactions. Incomplete

accounting records would cause problems while reporting or creating final accounts of the

company. Incomplete system records occur most often when accountant neglect to record entries.

Often, small enterprise begin with the owner attending to nearly all accountancy matters.

TASK 2

2.1 Calculate opening and/or closing capital using incomplete information

i. Calculating closing capital of ABC Ltd for the year when:

Opening capital = £1000

Drawing = £600

Net Profit = £2600

Capital A/C

Particular Amount Particular Amount

To Drawings a/c 600 By Opening Bal. 1000

To Closing Bal. 3000 By Profit a/c 2600

3600 3600

ii. Calculating Opening capital of ABC Ltd for the year when:

Closing capital = £4200

Drawing = £800

Net Profit = £360

Capital A/C

Imbalance may arise in the accounts of organisation if they have not followed the

sufficient principles or the policies while recording entries. If the entries that requires to be

credited or debited is recorded in a wrong way then it may result in wrong balance and due to

this the account would be imbalanced or provide a incorrect figure. This may arise due to clerical

error or it may arise to numerical error.

1.5 Provide reasons for incomplete records arising from insufficient data and inconsistencies

within the data provided.

As every small business owner has an intention to maintain accurate and complete

records but sometimes due to some error they may record incomplete transactions. Incomplete

accounting records would cause problems while reporting or creating final accounts of the

company. Incomplete system records occur most often when accountant neglect to record entries.

Often, small enterprise begin with the owner attending to nearly all accountancy matters.

TASK 2

2.1 Calculate opening and/or closing capital using incomplete information

i. Calculating closing capital of ABC Ltd for the year when:

Opening capital = £1000

Drawing = £600

Net Profit = £2600

Capital A/C

Particular Amount Particular Amount

To Drawings a/c 600 By Opening Bal. 1000

To Closing Bal. 3000 By Profit a/c 2600

3600 3600

ii. Calculating Opening capital of ABC Ltd for the year when:

Closing capital = £4200

Drawing = £800

Net Profit = £360

Capital A/C

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

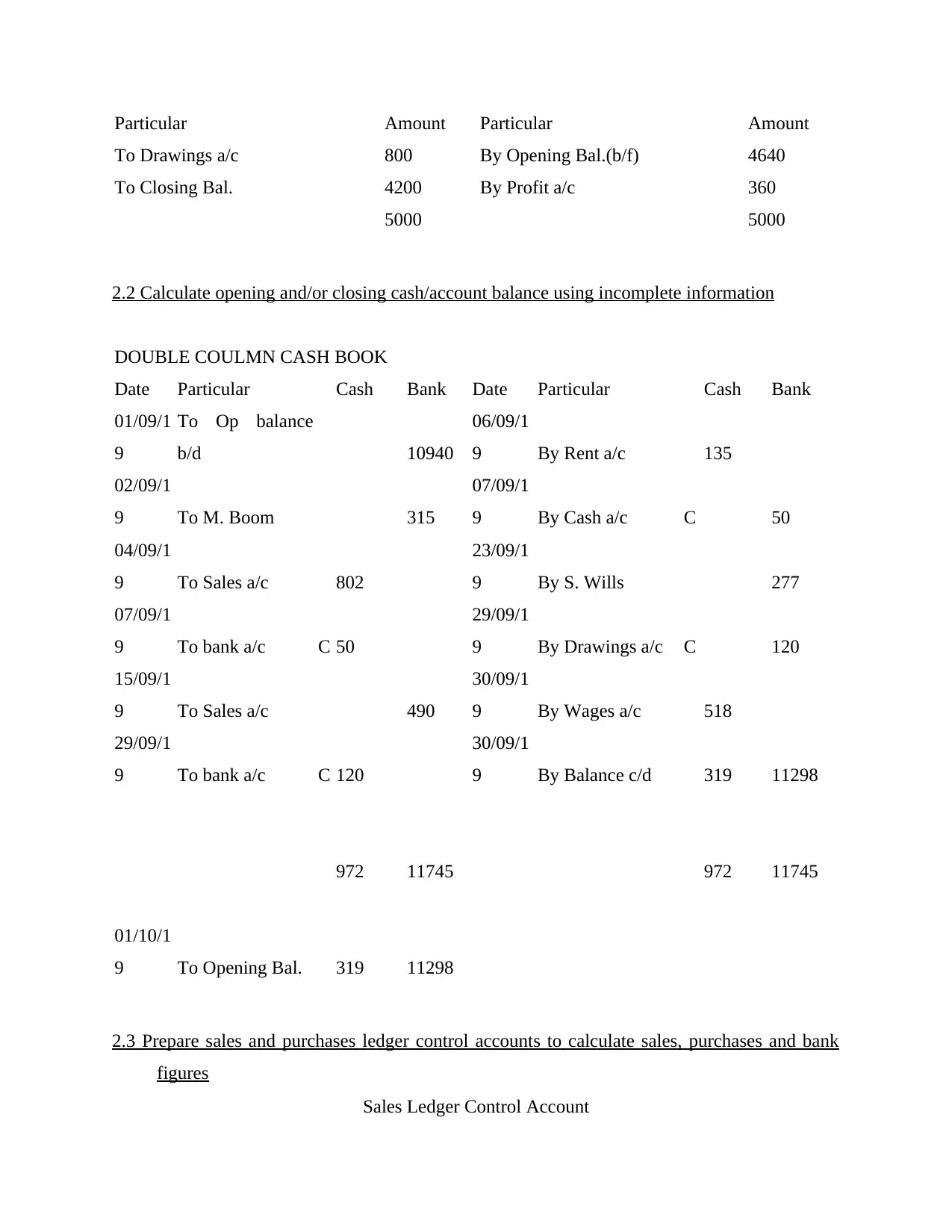

Particular Amount Particular Amount

To Drawings a/c 800 By Opening Bal.(b/f) 4640

To Closing Bal. 4200 By Profit a/c 360

5000 5000

2.2 Calculate opening and/or closing cash/account balance using incomplete information

DOUBLE COULMN CASH BOOK

Date Particular Cash Bank Date Particular Cash Bank

01/09/1

9

To Op balance

b/d 10940

06/09/1

9 By Rent a/c 135

02/09/1

9 To M. Boom 315

07/09/1

9 By Cash a/c C 50

04/09/1

9 To Sales a/c 802

23/09/1

9 By S. Wills 277

07/09/1

9 To bank a/c C 50

29/09/1

9 By Drawings a/c C 120

15/09/1

9 To Sales a/c 490

30/09/1

9 By Wages a/c 518

29/09/1

9 To bank a/c C 120

30/09/1

9 By Balance c/d 319 11298

972 11745 972 11745

01/10/1

9 To Opening Bal. 319 11298

2.3 Prepare sales and purchases ledger control accounts to calculate sales, purchases and bank

figures

Sales Ledger Control Account

To Drawings a/c 800 By Opening Bal.(b/f) 4640

To Closing Bal. 4200 By Profit a/c 360

5000 5000

2.2 Calculate opening and/or closing cash/account balance using incomplete information

DOUBLE COULMN CASH BOOK

Date Particular Cash Bank Date Particular Cash Bank

01/09/1

9

To Op balance

b/d 10940

06/09/1

9 By Rent a/c 135

02/09/1

9 To M. Boom 315

07/09/1

9 By Cash a/c C 50

04/09/1

9 To Sales a/c 802

23/09/1

9 By S. Wills 277

07/09/1

9 To bank a/c C 50

29/09/1

9 By Drawings a/c C 120

15/09/1

9 To Sales a/c 490

30/09/1

9 By Wages a/c 518

29/09/1

9 To bank a/c C 120

30/09/1

9 By Balance c/d 319 11298

972 11745 972 11745

01/10/1

9 To Opening Bal. 319 11298

2.3 Prepare sales and purchases ledger control accounts to calculate sales, purchases and bank

figures

Sales Ledger Control Account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

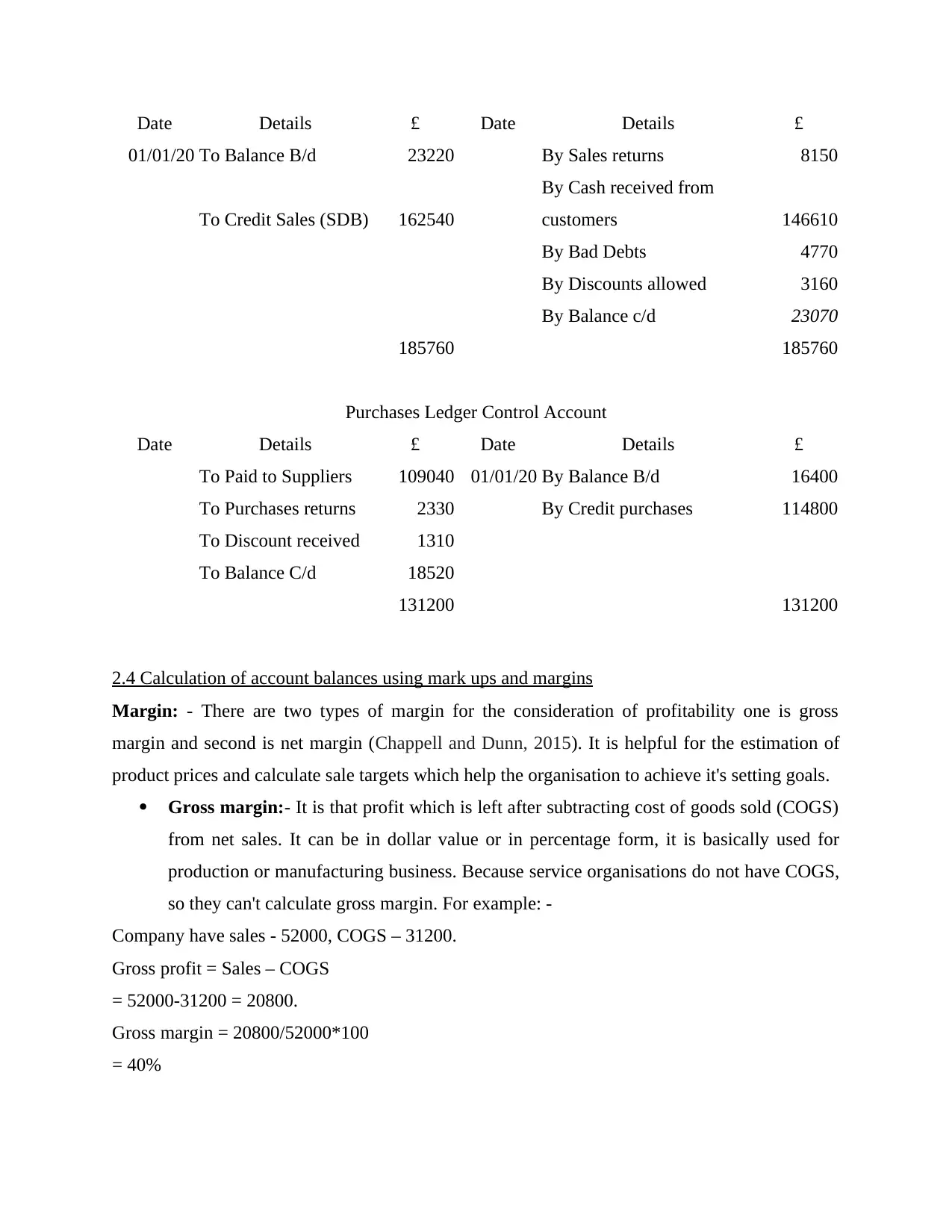

Date Details £ Date Details £

01/01/20 To Balance B/d 23220 By Sales returns 8150

To Credit Sales (SDB) 162540

By Cash received from

customers 146610

By Bad Debts 4770

By Discounts allowed 3160

By Balance c/d 23070

185760 185760

Purchases Ledger Control Account

Date Details £ Date Details £

To Paid to Suppliers 109040 01/01/20 By Balance B/d 16400

To Purchases returns 2330 By Credit purchases 114800

To Discount received 1310

To Balance C/d 18520

131200 131200

2.4 Calculation of account balances using mark ups and margins

Margin: - There are two types of margin for the consideration of profitability one is gross

margin and second is net margin (Chappell and Dunn, 2015). It is helpful for the estimation of

product prices and calculate sale targets which help the organisation to achieve it's setting goals.

Gross margin:- It is that profit which is left after subtracting cost of goods sold (COGS)

from net sales. It can be in dollar value or in percentage form, it is basically used for

production or manufacturing business. Because service organisations do not have COGS,

so they can't calculate gross margin. For example: -

Company have sales - 52000, COGS – 31200.

Gross profit = Sales – COGS

= 52000-31200 = 20800.

Gross margin = 20800/52000*100

= 40%

01/01/20 To Balance B/d 23220 By Sales returns 8150

To Credit Sales (SDB) 162540

By Cash received from

customers 146610

By Bad Debts 4770

By Discounts allowed 3160

By Balance c/d 23070

185760 185760

Purchases Ledger Control Account

Date Details £ Date Details £

To Paid to Suppliers 109040 01/01/20 By Balance B/d 16400

To Purchases returns 2330 By Credit purchases 114800

To Discount received 1310

To Balance C/d 18520

131200 131200

2.4 Calculation of account balances using mark ups and margins

Margin: - There are two types of margin for the consideration of profitability one is gross

margin and second is net margin (Chappell and Dunn, 2015). It is helpful for the estimation of

product prices and calculate sale targets which help the organisation to achieve it's setting goals.

Gross margin:- It is that profit which is left after subtracting cost of goods sold (COGS)

from net sales. It can be in dollar value or in percentage form, it is basically used for

production or manufacturing business. Because service organisations do not have COGS,

so they can't calculate gross margin. For example: -

Company have sales - 52000, COGS – 31200.

Gross profit = Sales – COGS

= 52000-31200 = 20800.

Gross margin = 20800/52000*100

= 40%

Net margin: - It is that profit which is pay before paying any tax, it means tax is

excluded in this profit. Remaining amount after deducting overhead expenses from gross

profit is called net profit. For example: -

Gross profit – 20800, Overhead expenses – 15600.

Net profit = 20800-15600 = 5200

Net margin = 5200/52000*100 = 10%

Markup: - It is that amount which is higher than the cost of product manufacture in the

organisation. Price of products need to cover all the cost of goods sold and overheads expenses.

It is generally used for sales of products not for services.

For example: -

Markup percentage value = Sales - COGS / COGS * 100

= 52000-31200 / 31200 *100

= 66.67%.

TASK 3

3.1 Components of final Account

Trading Account: - It is primary account in the trader's a/c it helps in find out gross

profit or gross loss of an organisation. Which is prepare through trading activity and it

involves buying and selling of raw material. In this account Cost of goods sold is

subtracted from net sales (COGS) at the time of calculating gross profit/loss. It includes

the direct expenses and revenues which is related to the business. It is separated from

other investment accounts on the basis of different activities, purpose and risk which is

involved (Doering, P., Neumann, S. and Paul, S., 2015Goede, G. W., 2015. Hoenig and

Morris, 2014).

Profit and Loss account: - In this statement organisation summarize the cost, expenses

and revenue at a particular time period. In the profit and loss account, gross profit is

added in the credit side. After deducting all expenses they get net profit or net loss of the

company. It can prepare quarterly or monthly which is totally depend upon the

organisation. It is very important to compare P&L statements of different year for

effective analysis. On the basis of analysis management build strategies for the company

and take appropriate decision.

excluded in this profit. Remaining amount after deducting overhead expenses from gross

profit is called net profit. For example: -

Gross profit – 20800, Overhead expenses – 15600.

Net profit = 20800-15600 = 5200

Net margin = 5200/52000*100 = 10%

Markup: - It is that amount which is higher than the cost of product manufacture in the

organisation. Price of products need to cover all the cost of goods sold and overheads expenses.

It is generally used for sales of products not for services.

For example: -

Markup percentage value = Sales - COGS / COGS * 100

= 52000-31200 / 31200 *100

= 66.67%.

TASK 3

3.1 Components of final Account

Trading Account: - It is primary account in the trader's a/c it helps in find out gross

profit or gross loss of an organisation. Which is prepare through trading activity and it

involves buying and selling of raw material. In this account Cost of goods sold is

subtracted from net sales (COGS) at the time of calculating gross profit/loss. It includes

the direct expenses and revenues which is related to the business. It is separated from

other investment accounts on the basis of different activities, purpose and risk which is

involved (Doering, P., Neumann, S. and Paul, S., 2015Goede, G. W., 2015. Hoenig and

Morris, 2014).

Profit and Loss account: - In this statement organisation summarize the cost, expenses

and revenue at a particular time period. In the profit and loss account, gross profit is

added in the credit side. After deducting all expenses they get net profit or net loss of the

company. It can prepare quarterly or monthly which is totally depend upon the

organisation. It is very important to compare P&L statements of different year for

effective analysis. On the basis of analysis management build strategies for the company

and take appropriate decision.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Balance sheet: - It shows the financial position of the firm through it's assets, equity

capita, debt and liabilities. Management analyse this statement on the basis of available

information and take decision according to it. This statement can prepare for individual

such as sole proprietors as well as for organisation and it include partnership firm,

companies and public or private sector both. It shows the clear picture of all items like

how much fund have from debt or from equity. No of shareholders and the market value

of shares. Generally balance sheet prepare on every quarter, six month or yearly basis. It

provide accurate information regarding their transactions which is going to help in the

future. Comparison of balance sheet will show the differences among the items, so

management can analyse that and make strategies according to it.

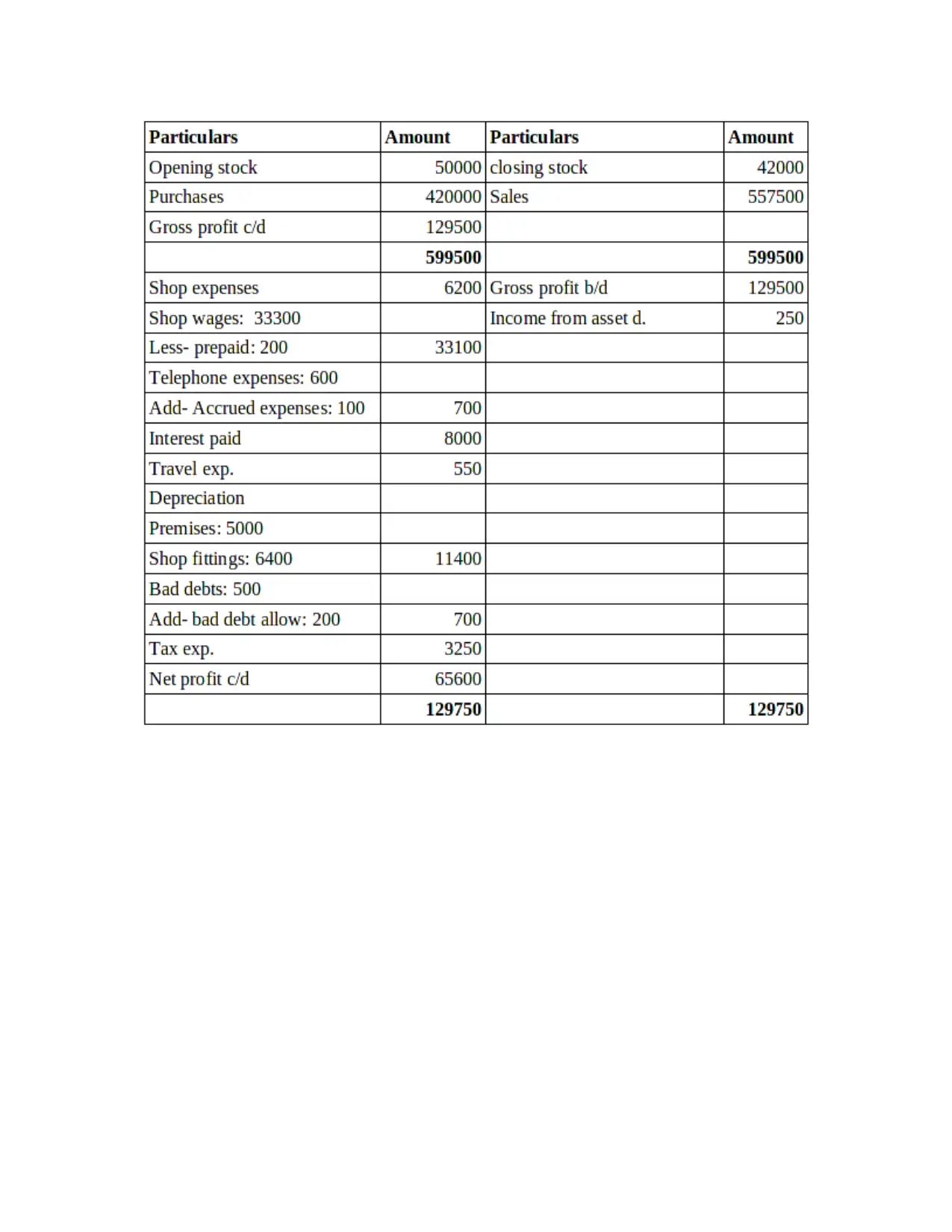

3.2 Profit and loss statement of Sole proprietor

Trading and Profit and loss statement

capita, debt and liabilities. Management analyse this statement on the basis of available

information and take decision according to it. This statement can prepare for individual

such as sole proprietors as well as for organisation and it include partnership firm,

companies and public or private sector both. It shows the clear picture of all items like

how much fund have from debt or from equity. No of shareholders and the market value

of shares. Generally balance sheet prepare on every quarter, six month or yearly basis. It

provide accurate information regarding their transactions which is going to help in the

future. Comparison of balance sheet will show the differences among the items, so

management can analyse that and make strategies according to it.

3.2 Profit and loss statement of Sole proprietor

Trading and Profit and loss statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

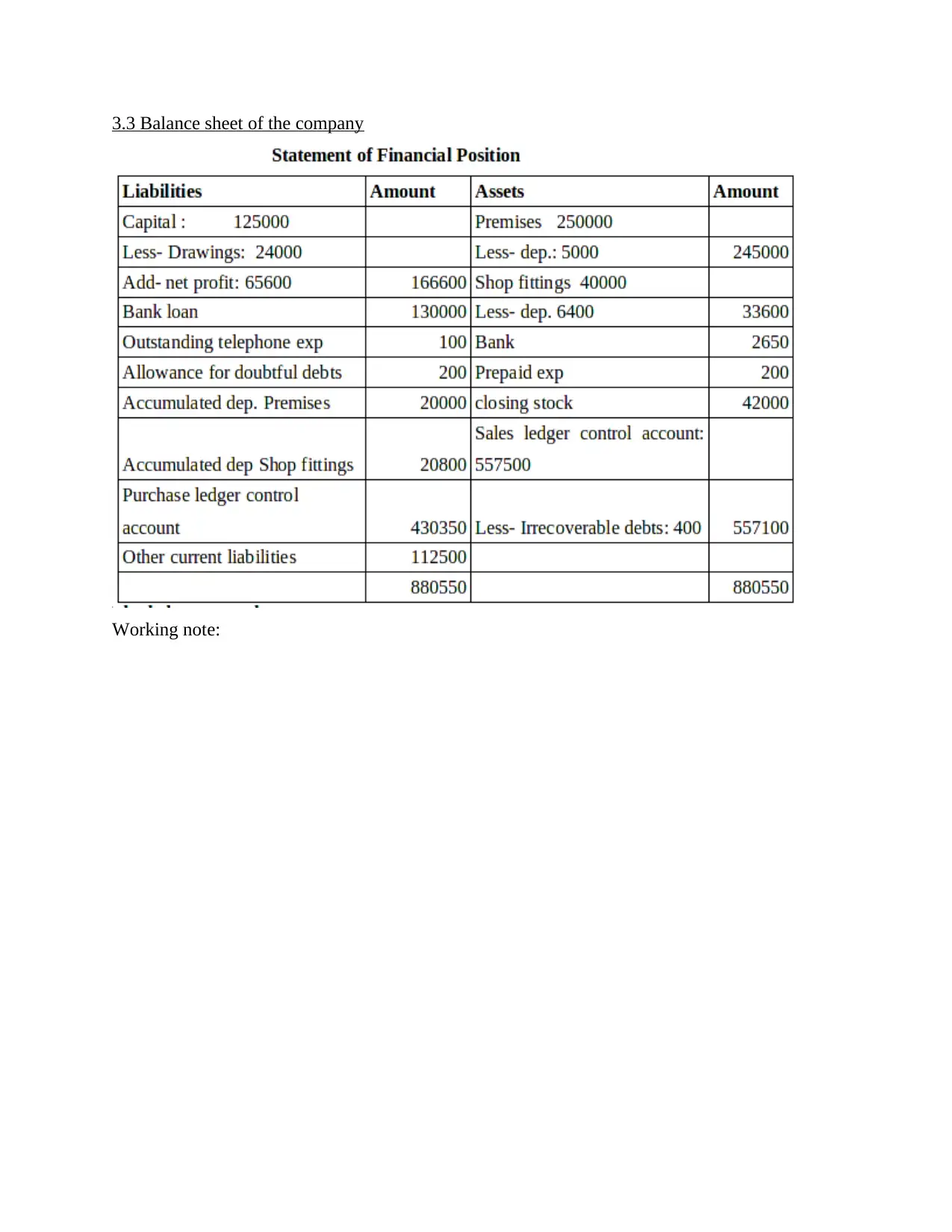

3.3 Balance sheet of the company

Working note:

Working note:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.