City and Islington College - Final Accounts Project - L3 Business

VerifiedAdded on 2022/12/27

|14

|2438

|33

Project

AI Summary

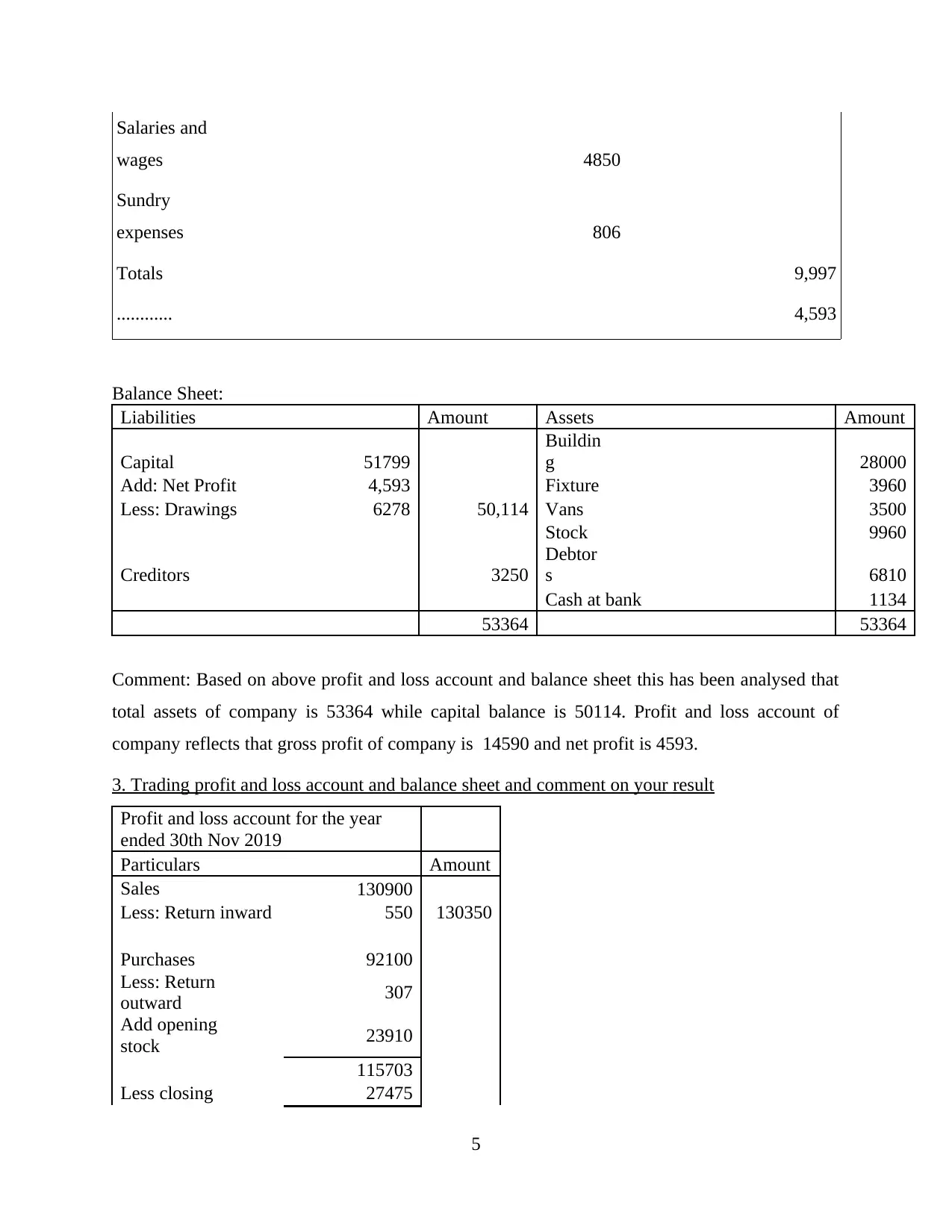

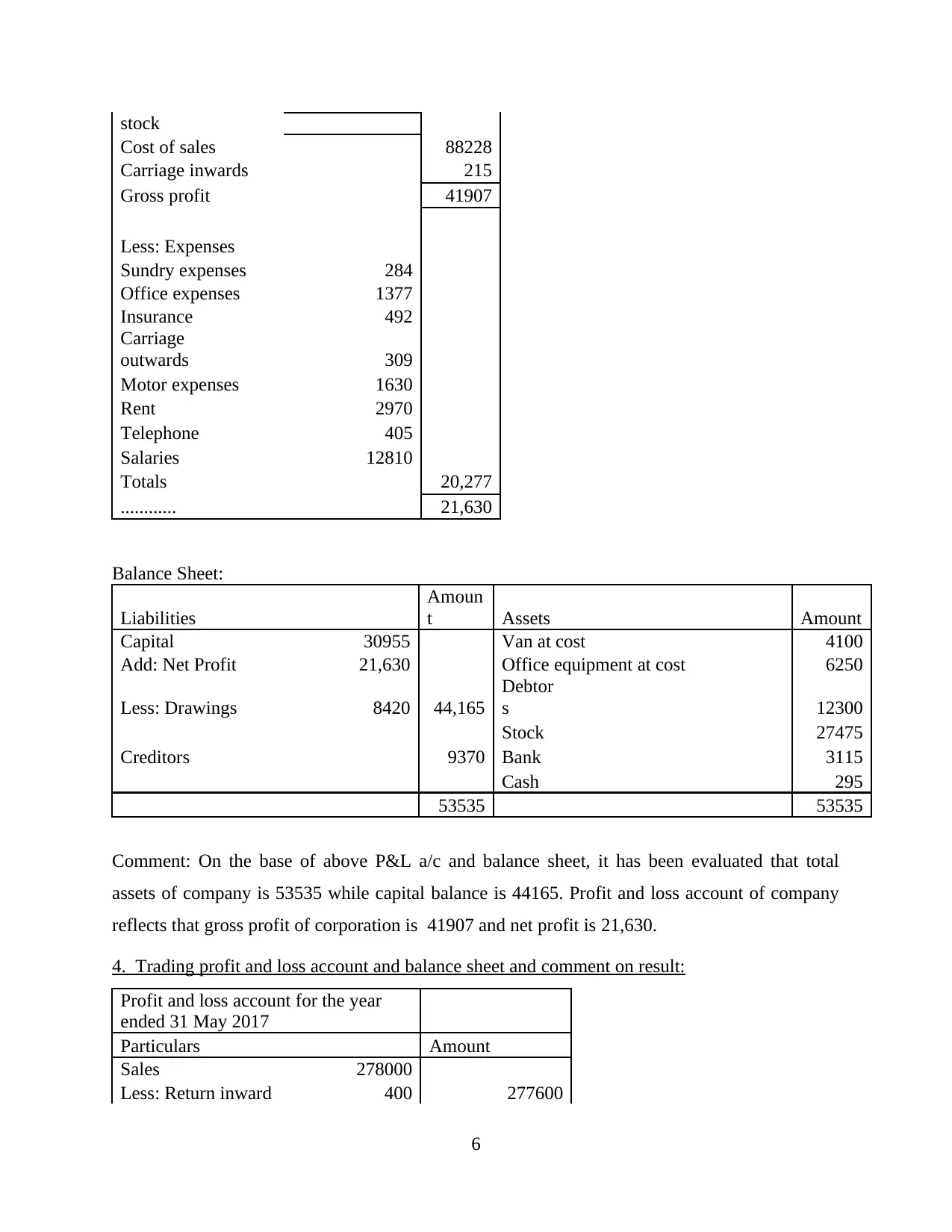

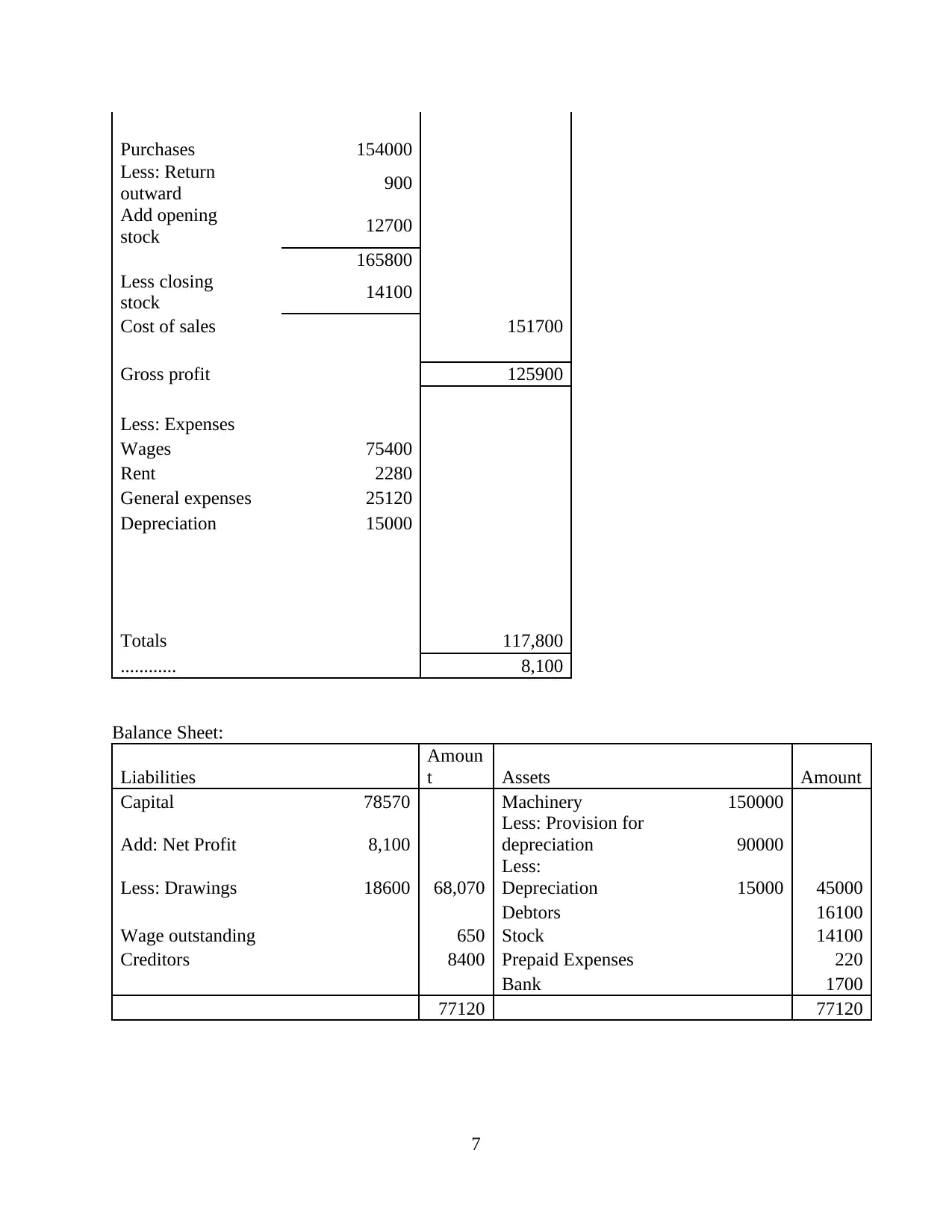

This project presents a comprehensive solution to a final accounts assignment, addressing key aspects of financial accounting. The project includes the completion of fill-in-the-gaps exercises, preparation of balance sheets and profit and loss accounts, and detailed comments on the results. It covers topics such as depreciation of fixed assets, provision for depreciation, accruals, and prepayments, with explanations and examples. The assignment involves calculations of profit or loss on disposal, comparisons of straight-line and reducing balance depreciation methods, and analysis of the effects of accruals and prepayments on net profit. The student provides trading, profit and loss accounts and balance sheets for different periods, followed by detailed commentary on the financial performance and position of the businesses. The project also includes the importance of depreciation and its application to final accounts and why provision for depreciation is needed. References from academic journals and books are also included to support the arguments.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.