Final Assessment- Financial Markets | Solutions

VerifiedAdded on 2022/07/29

|10

|2485

|22

AI Summary

There are only 4 questions for this online exam but it will take only 2 hrs. Later I will send you lecture slides and tutorial questions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINAL ASSESSMENT COVER SHEET

Student Name:

Student Number:

EXAM DETAILS

Course Code: BAFI1005

Course Description: Financial Markets

Exam Date 21/04/2020

Release time: 9:00 am SGP Time

Submission cut off time: 11:30 am SGP time

Exam Duration: 2 hours + 15 min reading time + 15 additional

minutes for download and submission

Total number of pages: 11 pages

INSTRUCTIONS TO CANDIDATES

1

The assessment consists of a series of 4 problems with scenario analysis.

You must complete all problems and each component of the problem. The

assessment is worth a total of 50 marks.

2 This is an OPEN BOOK assessment.

3 You are expected to answer the questions within the scope of this course

covering Topic 1 to 8.

4 Please write your answers in the space provided on this assessment paper

after each question.

5

This exam paper adds to 50 marks and comprises 50% of the total marks

allocated in this course. To obtain a pass in this course, you must achieve at

least 50 % overall in course assessment

1

Student Name:

Student Number:

EXAM DETAILS

Course Code: BAFI1005

Course Description: Financial Markets

Exam Date 21/04/2020

Release time: 9:00 am SGP Time

Submission cut off time: 11:30 am SGP time

Exam Duration: 2 hours + 15 min reading time + 15 additional

minutes for download and submission

Total number of pages: 11 pages

INSTRUCTIONS TO CANDIDATES

1

The assessment consists of a series of 4 problems with scenario analysis.

You must complete all problems and each component of the problem. The

assessment is worth a total of 50 marks.

2 This is an OPEN BOOK assessment.

3 You are expected to answer the questions within the scope of this course

covering Topic 1 to 8.

4 Please write your answers in the space provided on this assessment paper

after each question.

5

This exam paper adds to 50 marks and comprises 50% of the total marks

allocated in this course. To obtain a pass in this course, you must achieve at

least 50 % overall in course assessment

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Submission:

1

This assessment must be submitted electronically via Canvas in .doc

or .docx format only and must constitute your own work. Submission for this

assignment is via Turnitin, therefore it is automatically checked for any form of

plagiarism, resulting in academic misconduct if plagiarism occurs. You are

required to upload the file in .doc or .docx format only; not as .pdf. If the file is

uploaded in any other format that is not recognised via Turnitin and you don’t

receive a similarity score – the assessment will not be marked and a grade of

zero for the assessment will be applied.

2 You can only submit once as your final answer.

3 Name your answer file as: surname_studentID before submission.

4

As this is a final assessment, late submissions will not be accepted. If

circumstances occur that prevent you being able to undertake the

assessment on the due date – you will have to apply for special

consideration: This webpage provides instructions about how to go about

this: https://www.rmit.edu.au/students/student-essentials/assessment-and-

exams/assessment/special-consideration

5

The submission window will close exactly at the cut-off time. Please

submit well before cut-off time to ensure that nothing impedes your ability to

upload the assessment, such as internet/wifi issues. This will not be a

sufficient excuse to grant extensions – you are responsible for ensuring that

you are able to submit the assessment on time.

Answer Requirement:

1 Where mathematical calculations are required you must state the equation

used as well as each step in your calculations.

2

Please write answers in the spaces provided. You can extend the space to fit

your answers, but please label the sub-question number clearly.

The format is detailed below:

Font type: Arial

Font size: 12pt

Spacing: 1.5 line spacing

2

1

This assessment must be submitted electronically via Canvas in .doc

or .docx format only and must constitute your own work. Submission for this

assignment is via Turnitin, therefore it is automatically checked for any form of

plagiarism, resulting in academic misconduct if plagiarism occurs. You are

required to upload the file in .doc or .docx format only; not as .pdf. If the file is

uploaded in any other format that is not recognised via Turnitin and you don’t

receive a similarity score – the assessment will not be marked and a grade of

zero for the assessment will be applied.

2 You can only submit once as your final answer.

3 Name your answer file as: surname_studentID before submission.

4

As this is a final assessment, late submissions will not be accepted. If

circumstances occur that prevent you being able to undertake the

assessment on the due date – you will have to apply for special

consideration: This webpage provides instructions about how to go about

this: https://www.rmit.edu.au/students/student-essentials/assessment-and-

exams/assessment/special-consideration

5

The submission window will close exactly at the cut-off time. Please

submit well before cut-off time to ensure that nothing impedes your ability to

upload the assessment, such as internet/wifi issues. This will not be a

sufficient excuse to grant extensions – you are responsible for ensuring that

you are able to submit the assessment on time.

Answer Requirement:

1 Where mathematical calculations are required you must state the equation

used as well as each step in your calculations.

2

Please write answers in the spaces provided. You can extend the space to fit

your answers, but please label the sub-question number clearly.

The format is detailed below:

Font type: Arial

Font size: 12pt

Spacing: 1.5 line spacing

2

Assessment Declaration

This is an individual piece of assessment. That means it must be your own

work and you can’t copy or have someone else complete any part of the work

for you.

By submitting this assessment, you are declaring that you have read,

understood and agree to the content and expectations of the Assessment

declaration.

3

This is an individual piece of assessment. That means it must be your own

work and you can’t copy or have someone else complete any part of the work

for you.

By submitting this assessment, you are declaring that you have read,

understood and agree to the content and expectations of the Assessment

declaration.

3

Final Assessment Questions

The final assessment comprises four (4) questions. You are required to answer all

four (4) questions. This section is worth a total of 50 marks, with marks for each

question specified at the end of the question.

Question1

On 16th March 2020, the Federal reserve in the US announced that it will lower the

primary credit rate by 150 basis points to 0.25 percent to support the US economy

amid the coronavirus outbreak, effective March 16, 2020.

Jack is a new investor. He read the above news but could not figure out how the

“Federal Reserve could support the economy by cutting interest rates”. You are his

financial advisor, so he asked for your help.

REQUIRED:

a. Please explain in detail the reasoning or theories behind the statement -

“Federal Reserve could support the economy by cutting interest rates”.

b. Please introduce the main instrument used by Federal Reserve to achieve its

targeted interest rate.

c. Please explain how it works in detail.

(5+2+5=12marks)

a) The FED is well deciding on reducing the interest rate level that is by 150 basis

point and the actions have been well taken by the FED in order to revive the

economy that is going into a global recession. Now the set of actions taken by the

government has been particularly taken down for the purpose of reducing the

borrowing cost or finance cost that is there in the economy so that business entities,

corporations and individuals are able to see cheap availability of finance which in

turn helps them meet their business operational as well as investment needs.

4

The final assessment comprises four (4) questions. You are required to answer all

four (4) questions. This section is worth a total of 50 marks, with marks for each

question specified at the end of the question.

Question1

On 16th March 2020, the Federal reserve in the US announced that it will lower the

primary credit rate by 150 basis points to 0.25 percent to support the US economy

amid the coronavirus outbreak, effective March 16, 2020.

Jack is a new investor. He read the above news but could not figure out how the

“Federal Reserve could support the economy by cutting interest rates”. You are his

financial advisor, so he asked for your help.

REQUIRED:

a. Please explain in detail the reasoning or theories behind the statement -

“Federal Reserve could support the economy by cutting interest rates”.

b. Please introduce the main instrument used by Federal Reserve to achieve its

targeted interest rate.

c. Please explain how it works in detail.

(5+2+5=12marks)

a) The FED is well deciding on reducing the interest rate level that is by 150 basis

point and the actions have been well taken by the FED in order to revive the

economy that is going into a global recession. Now the set of actions taken by the

government has been particularly taken down for the purpose of reducing the

borrowing cost or finance cost that is there in the economy so that business entities,

corporations and individuals are able to see cheap availability of finance which in

turn helps them meet their business operational as well as investment needs.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

b) Cash Rate is the Key Instrument that is used by the Federal Reserves to achieve

its targeted interest rate. There are other instruments and operations as well that are

carried like changes in reserves ratio and buying and selling of bonds via Open

Market Purchase to increase liquidity and to push the economy.

c) A reduction in the interest rate helps business entities, organisation and

individuals to lower down the cost of finance, which lowers down the cost of

operations in turn. After, the outbreak of COVID-19 people would be relatively would

not be willing to spend much on business expansion programs and investments due

to global recession which in turn would be reducing the revenue or cash flows that

they have expected. Now what the Federal Reserves have actually done in reduced

the interest rate, now considering the fact that finance cost plays a major and

significant role a reduction in the finance cost would somehow offset the loss in the

expected cash flows and business entities would be induced to invest into projects

and finance due to cheap availability of finance. Now, these actions would not only

boost the economy by increasing business activities, but would see a surge in the

employment levels, transactions level operating and all on an overall basis would be

helping the US Economy revive. However, there are other key business and

economic factors, which too play a significant role while analysing and

conceptualizing these set of idea which must be considered and noted.

Question 2

As a financial advisor, you have been asked a lot of questions recently on yield

curves. So, you decided to hold an online seminar for your clients to explain the

following questions using US yield curve as an example. You downloaded the data

of Daily Treasury Yield Rates of the U.S from the website of U.S. DEPARTMENT OF

THE TREASURY as below. (Mo=month, Yr=Year, Date format is Month/Date/Year)

Table1: Daily treasury yield rates of the US treasury bill and bond

Time to maturities of US Treasury bill and bond

Date 1 Mo 2 Mo 3 Mo 6 Mo 1 Yr 2 Yr 3 Yr 5 Yr 7 Yr 10 Yr 20 Yr 30 Yr

5

its targeted interest rate. There are other instruments and operations as well that are

carried like changes in reserves ratio and buying and selling of bonds via Open

Market Purchase to increase liquidity and to push the economy.

c) A reduction in the interest rate helps business entities, organisation and

individuals to lower down the cost of finance, which lowers down the cost of

operations in turn. After, the outbreak of COVID-19 people would be relatively would

not be willing to spend much on business expansion programs and investments due

to global recession which in turn would be reducing the revenue or cash flows that

they have expected. Now what the Federal Reserves have actually done in reduced

the interest rate, now considering the fact that finance cost plays a major and

significant role a reduction in the finance cost would somehow offset the loss in the

expected cash flows and business entities would be induced to invest into projects

and finance due to cheap availability of finance. Now, these actions would not only

boost the economy by increasing business activities, but would see a surge in the

employment levels, transactions level operating and all on an overall basis would be

helping the US Economy revive. However, there are other key business and

economic factors, which too play a significant role while analysing and

conceptualizing these set of idea which must be considered and noted.

Question 2

As a financial advisor, you have been asked a lot of questions recently on yield

curves. So, you decided to hold an online seminar for your clients to explain the

following questions using US yield curve as an example. You downloaded the data

of Daily Treasury Yield Rates of the U.S from the website of U.S. DEPARTMENT OF

THE TREASURY as below. (Mo=month, Yr=Year, Date format is Month/Date/Year)

Table1: Daily treasury yield rates of the US treasury bill and bond

Time to maturities of US Treasury bill and bond

Date 1 Mo 2 Mo 3 Mo 6 Mo 1 Yr 2 Yr 3 Yr 5 Yr 7 Yr 10 Yr 20 Yr 30 Yr

5

08/15/19 2.08 1.97 1.91 1.86 1.72 1.48 1.44 1.42 1.47 1.52 1.8 1.98

08/16/19 2.05 1.95 1.87 1.85 1.71 1.48 1.44 1.42 1.49 1.55 1.82 2.01

03/16/20 0.25 0.25 0.24 0.29 0.29 0.36 0.43 0.49 0.67 0.73 1.1 1.34

REQUIRED:

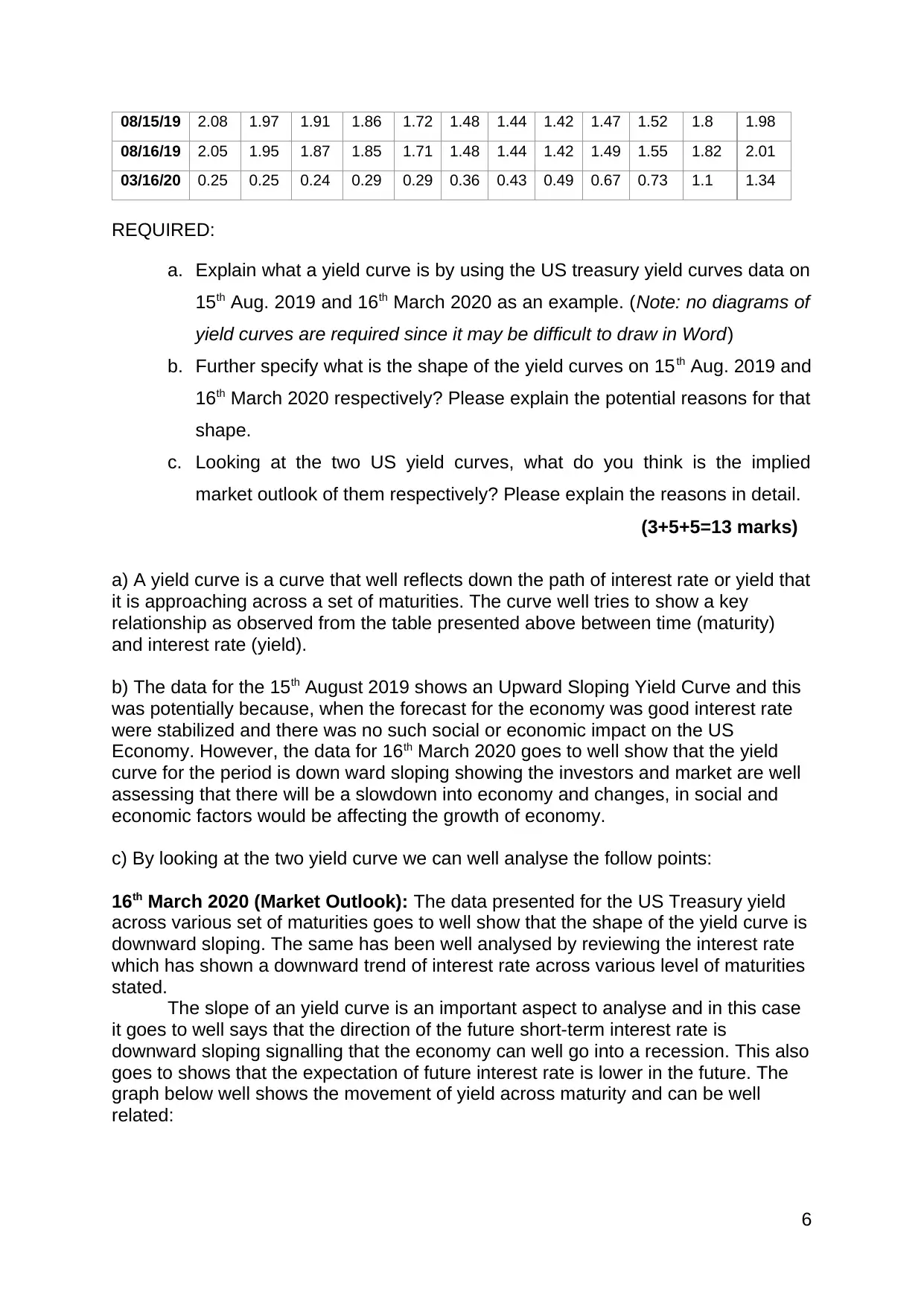

a. Explain what a yield curve is by using the US treasury yield curves data on

15th Aug. 2019 and 16th March 2020 as an example. (Note: no diagrams of

yield curves are required since it may be difficult to draw in Word)

b. Further specify what is the shape of the yield curves on 15th Aug. 2019 and

16th March 2020 respectively? Please explain the potential reasons for that

shape.

c. Looking at the two US yield curves, what do you think is the implied

market outlook of them respectively? Please explain the reasons in detail.

(3+5+5=13 marks)

a) A yield curve is a curve that well reflects down the path of interest rate or yield that

it is approaching across a set of maturities. The curve well tries to show a key

relationship as observed from the table presented above between time (maturity)

and interest rate (yield).

b) The data for the 15th August 2019 shows an Upward Sloping Yield Curve and this

was potentially because, when the forecast for the economy was good interest rate

were stabilized and there was no such social or economic impact on the US

Economy. However, the data for 16th March 2020 goes to well show that the yield

curve for the period is down ward sloping showing the investors and market are well

assessing that there will be a slowdown into economy and changes, in social and

economic factors would be affecting the growth of economy.

c) By looking at the two yield curve we can well analyse the follow points:

16th March 2020 (Market Outlook): The data presented for the US Treasury yield

across various set of maturities goes to well show that the shape of the yield curve is

downward sloping. The same has been well analysed by reviewing the interest rate

which has shown a downward trend of interest rate across various level of maturities

stated.

The slope of an yield curve is an important aspect to analyse and in this case

it goes to well says that the direction of the future short-term interest rate is

downward sloping signalling that the economy can well go into a recession. This also

goes to shows that the expectation of future interest rate is lower in the future. The

graph below well shows the movement of yield across maturity and can be well

related:

6

08/16/19 2.05 1.95 1.87 1.85 1.71 1.48 1.44 1.42 1.49 1.55 1.82 2.01

03/16/20 0.25 0.25 0.24 0.29 0.29 0.36 0.43 0.49 0.67 0.73 1.1 1.34

REQUIRED:

a. Explain what a yield curve is by using the US treasury yield curves data on

15th Aug. 2019 and 16th March 2020 as an example. (Note: no diagrams of

yield curves are required since it may be difficult to draw in Word)

b. Further specify what is the shape of the yield curves on 15th Aug. 2019 and

16th March 2020 respectively? Please explain the potential reasons for that

shape.

c. Looking at the two US yield curves, what do you think is the implied

market outlook of them respectively? Please explain the reasons in detail.

(3+5+5=13 marks)

a) A yield curve is a curve that well reflects down the path of interest rate or yield that

it is approaching across a set of maturities. The curve well tries to show a key

relationship as observed from the table presented above between time (maturity)

and interest rate (yield).

b) The data for the 15th August 2019 shows an Upward Sloping Yield Curve and this

was potentially because, when the forecast for the economy was good interest rate

were stabilized and there was no such social or economic impact on the US

Economy. However, the data for 16th March 2020 goes to well show that the yield

curve for the period is down ward sloping showing the investors and market are well

assessing that there will be a slowdown into economy and changes, in social and

economic factors would be affecting the growth of economy.

c) By looking at the two yield curve we can well analyse the follow points:

16th March 2020 (Market Outlook): The data presented for the US Treasury yield

across various set of maturities goes to well show that the shape of the yield curve is

downward sloping. The same has been well analysed by reviewing the interest rate

which has shown a downward trend of interest rate across various level of maturities

stated.

The slope of an yield curve is an important aspect to analyse and in this case

it goes to well says that the direction of the future short-term interest rate is

downward sloping signalling that the economy can well go into a recession. This also

goes to shows that the expectation of future interest rate is lower in the future. The

graph below well shows the movement of yield across maturity and can be well

related:

6

15th August 2019 (Market Outlook): The data presented for the US Treasury yield

across various set of maturities goes to well show that the shape of the yield curve is

upward sloping. The same has been well analysed by reviewing the interest rate

which has shown a upward trend of interest rate across various level of maturities

stated. This has been particularly due to positive expectation about economy and

social factors on a whole.

Question 3

You are now a fund manager. Your boss asks you to prepare a report regarding

following questions:

a. Please calculate the issuing price of U.S. 10 Year Treasury bond on 16th Aug.

2019 and 16th March 2020 respectively with information given below.

US 10-year Treasury Notes Fact Sheet

Issuing date 16th Aug. 2019 16th March 2020

Bond expiration date 16th Aug. 2029 16th March. 2030

Face value 100 100

Coupon rate (annual) 1.50% 1.50%

Coupon payment semi-annual semi-annual

Tips: the market yield of 10-year treasury notes can be found in the data provided in Question 2

7

across various set of maturities goes to well show that the shape of the yield curve is

upward sloping. The same has been well analysed by reviewing the interest rate

which has shown a upward trend of interest rate across various level of maturities

stated. This has been particularly due to positive expectation about economy and

social factors on a whole.

Question 3

You are now a fund manager. Your boss asks you to prepare a report regarding

following questions:

a. Please calculate the issuing price of U.S. 10 Year Treasury bond on 16th Aug.

2019 and 16th March 2020 respectively with information given below.

US 10-year Treasury Notes Fact Sheet

Issuing date 16th Aug. 2019 16th March 2020

Bond expiration date 16th Aug. 2029 16th March. 2030

Face value 100 100

Coupon rate (annual) 1.50% 1.50%

Coupon payment semi-annual semi-annual

Tips: the market yield of 10-year treasury notes can be found in the data provided in Question 2

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. Compared to the price on 16th Aug. 2019, how has the issuing price of US 10

Year treasury bond changed after the Federal Reserve’s rate cutting on 16th

March 2020? Please explain the potential reason for this.

(6+6=12 marks)

a) The price for each of the bond is calculated as follows:

US 10-year Treasury Notes Fact Sheet

Issuing Date 16th Aug. 2019 16th March 2020

Bond Expiration Date 16th Aug. 2029 16th March. 2030

Face value 100 100

Coupon rate (annual) 1.50% 1.50%

Coupon payment semi-annual semi-annual

Time Period (In Years) 10 10

Market Yield 1.55% 0.73%

Price (Present Value) $ -99.54 $ -107.41

b) The issue price for the 16th August 2019 has well changed from 16th March 2020

due to change in the interest rate that has been observed it can be well said by

looking at the data point given. The calculated price for the bond has been around

$99.54 when the market yield was 1.55% in the year 2019 however the price has

well increased to around $107.41 and this has happened due to fall in the interest

rate level of the bonds. It can be well said that it is primarily because Interest Rate

and Bond prices have an inverse relationship and the same can be well explained in

this case.

Question 4

As a hedge fund manager, you have a bearish view on Tesla Inc. shares (NASDAQ:

TSLA) for the following 2 months given the uncertainties related to the Covid-19.

Assuming Tesla Inc is currently trading at $467.00, the put options with a maturity

of two month and an exercise price of $442 per share, have a premium (cost) of

$1.5 per share. The call option with a maturity of two month and an exercise price of

$487 per share, have a premium (cost) of $3 per share.

a. Calculate the cost if you purchase 1,000,000 of the above put options.

8

Year treasury bond changed after the Federal Reserve’s rate cutting on 16th

March 2020? Please explain the potential reason for this.

(6+6=12 marks)

a) The price for each of the bond is calculated as follows:

US 10-year Treasury Notes Fact Sheet

Issuing Date 16th Aug. 2019 16th March 2020

Bond Expiration Date 16th Aug. 2029 16th March. 2030

Face value 100 100

Coupon rate (annual) 1.50% 1.50%

Coupon payment semi-annual semi-annual

Time Period (In Years) 10 10

Market Yield 1.55% 0.73%

Price (Present Value) $ -99.54 $ -107.41

b) The issue price for the 16th August 2019 has well changed from 16th March 2020

due to change in the interest rate that has been observed it can be well said by

looking at the data point given. The calculated price for the bond has been around

$99.54 when the market yield was 1.55% in the year 2019 however the price has

well increased to around $107.41 and this has happened due to fall in the interest

rate level of the bonds. It can be well said that it is primarily because Interest Rate

and Bond prices have an inverse relationship and the same can be well explained in

this case.

Question 4

As a hedge fund manager, you have a bearish view on Tesla Inc. shares (NASDAQ:

TSLA) for the following 2 months given the uncertainties related to the Covid-19.

Assuming Tesla Inc is currently trading at $467.00, the put options with a maturity

of two month and an exercise price of $442 per share, have a premium (cost) of

$1.5 per share. The call option with a maturity of two month and an exercise price of

$487 per share, have a premium (cost) of $3 per share.

a. Calculate the cost if you purchase 1,000,000 of the above put options.

8

b. Determine the share price for Tesla shares at which you would choose to

“exercise” the above put options.

c. Determine the share price for Tesla shares at which the decision to purchase

the above put options effectively “breaks even” for the fund manager.

d. If you don’t own any shares, but you still want to make profits during this

period. How can you use put and call options to take advantage of the fall in

the share price?

(2+2++3+6=13 marks)

a) Cost of Put Option: 1,000,000*1.5

Cost of Put Option: $1,500,000.

b) The share price at which we would choose the above the put option would be at a

price which is below the strike price that is the when the stock price is below the

strike price of $442.

c) Breakeven Point: $442-$1.5

Breakeven Point: $440.5

d) Selling Call at a rate of $487 and simultaneously buying put option at the level of

$442 will involve a profit of $1.5 for the investor that is $3-$1.5: $1.5.

9

“exercise” the above put options.

c. Determine the share price for Tesla shares at which the decision to purchase

the above put options effectively “breaks even” for the fund manager.

d. If you don’t own any shares, but you still want to make profits during this

period. How can you use put and call options to take advantage of the fall in

the share price?

(2+2++3+6=13 marks)

a) Cost of Put Option: 1,000,000*1.5

Cost of Put Option: $1,500,000.

b) The share price at which we would choose the above the put option would be at a

price which is below the strike price that is the when the stock price is below the

strike price of $442.

c) Breakeven Point: $442-$1.5

Breakeven Point: $440.5

d) Selling Call at a rate of $487 and simultaneously buying put option at the level of

$442 will involve a profit of $1.5 for the investor that is $3-$1.5: $1.5.

9

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.