Capital Structure and Weighted Average Cost of Capital

VerifiedAdded on 2020/09/15

|5

|1690

|211

AI Summary

The assignment requires connecting capital structure to question 5, which involves applying corporate taxes and costs of financial distress models to a café business scenario. The student needs to demonstrate understanding of WACC, capital structure, and their application in a real-world context.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Final Assignment

MICRO-CASES-E25,507Q49

Requirement-A: In order to figure out how much fund left for next year for KB, following should

be considered:

Project X: ($32,555/$26,780) -1 = 21.56% IRR

Project Y: ($30,873/$20,402) -1 = 51.32% IRR

Project Z: ($57,135/$53,048) -1 = 7.70% IRR

Since the average expected rate of return from the market is 20%, Project X and Project Y are the

acceptable projects

KB only owns 47%, and he wants to consume 49% thus loan is required.

49% of $78,450 = $38,440.50

47% of $78,450 = $36,871.50 $1,569 of loan

Therefore: $80,019 – $32,555 – $30,873 – $1,569 = $15022

Requirement-B

$25,507 FV, 3N, 7.77 I/Y, PV = $20,417.96

($8,880/0.077) FV, 5N, 7.7 I/Y, PV = $79,587.29 Present Value of KD’s Investment = $100,004.29

Requirement-C

-$33,459 PV, 6.2/12 = 0.5166 I/Y, 26 x 12 = 312, FV = $167,029.55

MICRO-CASES-KG1,142.20

Requirement-A

$11,000,000/5,000,000 = $2.20 x 0.13 = 0.29

0.29 + 2.20 = 2.49 x 5,000,000 = $12,450,000

Requirement-B

N = 22-4 = 18 x 4 = 72

FV = $4,000

$4,000 x 0.11 = 440/4 = 110 PMT

15/4 = 3.75

PV = $3,008.65

Requirement-C

FV = $1,000

MICRO-CASES-E25,507Q49

Requirement-A: In order to figure out how much fund left for next year for KB, following should

be considered:

Project X: ($32,555/$26,780) -1 = 21.56% IRR

Project Y: ($30,873/$20,402) -1 = 51.32% IRR

Project Z: ($57,135/$53,048) -1 = 7.70% IRR

Since the average expected rate of return from the market is 20%, Project X and Project Y are the

acceptable projects

KB only owns 47%, and he wants to consume 49% thus loan is required.

49% of $78,450 = $38,440.50

47% of $78,450 = $36,871.50 $1,569 of loan

Therefore: $80,019 – $32,555 – $30,873 – $1,569 = $15022

Requirement-B

$25,507 FV, 3N, 7.77 I/Y, PV = $20,417.96

($8,880/0.077) FV, 5N, 7.7 I/Y, PV = $79,587.29 Present Value of KD’s Investment = $100,004.29

Requirement-C

-$33,459 PV, 6.2/12 = 0.5166 I/Y, 26 x 12 = 312, FV = $167,029.55

MICRO-CASES-KG1,142.20

Requirement-A

$11,000,000/5,000,000 = $2.20 x 0.13 = 0.29

0.29 + 2.20 = 2.49 x 5,000,000 = $12,450,000

Requirement-B

N = 22-4 = 18 x 4 = 72

FV = $4,000

$4,000 x 0.11 = 440/4 = 110 PMT

15/4 = 3.75

PV = $3,008.65

Requirement-C

FV = $1,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

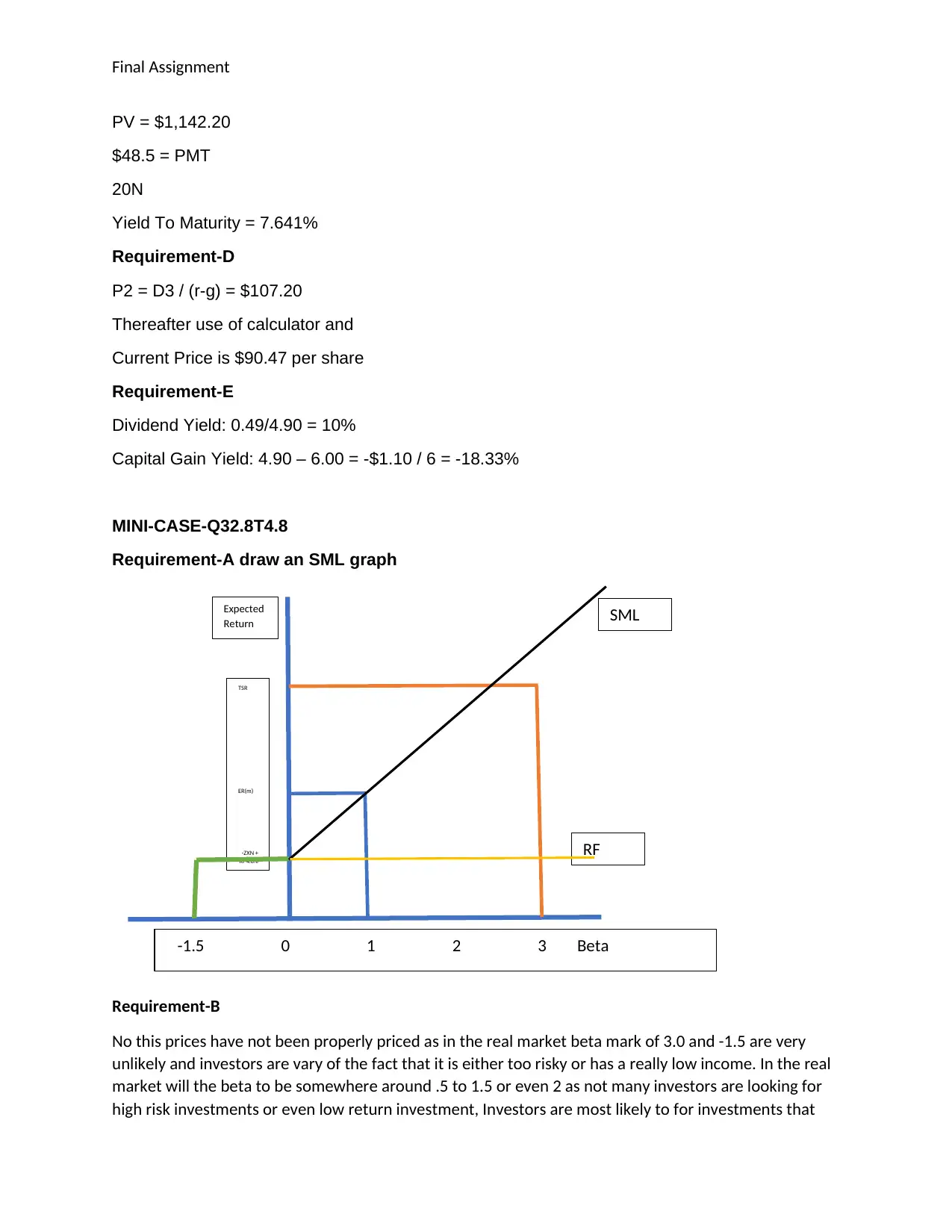

-1.5 0 1 2 3 Beta

SML

TSR

ER(m)

-ZXN +

Rf 4.8%

Expected

Return

RF

Final Assignment

PV = $1,142.20

$48.5 = PMT

20N

Yield To Maturity = 7.641%

Requirement-D

P2 = D3 / (r-g) = $107.20

Thereafter use of calculator and

Current Price is $90.47 per share

Requirement-E

Dividend Yield: 0.49/4.90 = 10%

Capital Gain Yield: 4.90 – 6.00 = -$1.10 / 6 = -18.33%

MINI-CASE-Q32.8T4.8

Requirement-A draw an SML graph

Requirement-B

No this prices have not been properly priced as in the real market beta mark of 3.0 and -1.5 are very

unlikely and investors are vary of the fact that it is either too risky or has a really low income. In the real

market will the beta to be somewhere around .5 to 1.5 or even 2 as not many investors are looking for

high risk investments or even low return investment, Investors are most likely to for investments that

SML

TSR

ER(m)

-ZXN +

Rf 4.8%

Expected

Return

RF

Final Assignment

PV = $1,142.20

$48.5 = PMT

20N

Yield To Maturity = 7.641%

Requirement-D

P2 = D3 / (r-g) = $107.20

Thereafter use of calculator and

Current Price is $90.47 per share

Requirement-E

Dividend Yield: 0.49/4.90 = 10%

Capital Gain Yield: 4.90 – 6.00 = -$1.10 / 6 = -18.33%

MINI-CASE-Q32.8T4.8

Requirement-A draw an SML graph

Requirement-B

No this prices have not been properly priced as in the real market beta mark of 3.0 and -1.5 are very

unlikely and investors are vary of the fact that it is either too risky or has a really low income. In the real

market will the beta to be somewhere around .5 to 1.5 or even 2 as not many investors are looking for

high risk investments or even low return investment, Investors are most likely to for investments that

Final Assignment

come above the SML line but just below the expected return rate of the market (premium market risk)

as it offers better return with a definable risk.

Requirement-C

The more diversified the portfolio the better it is. Using the weighted average of the risks will leave

calculated risk on individuality basis, for example TSR at 66% and ZXN at 34% would have their risk

calculated separately meaning higher risk of securities in the portfolio. The total risk of portfolio

eliminates independency allowing securities to been seen together, thus the risk of the portfolio is

actually less than the weighted average of the risks

Requirement-D

since the beta measures systematic risk of any security as compared to average risky asset in the

market, beta of 3.0 is twice riskier than the market but it also has high rewards whereas beta of -1.5

does not provide you with good insight but the positive is that return will be the same as a government

bond.

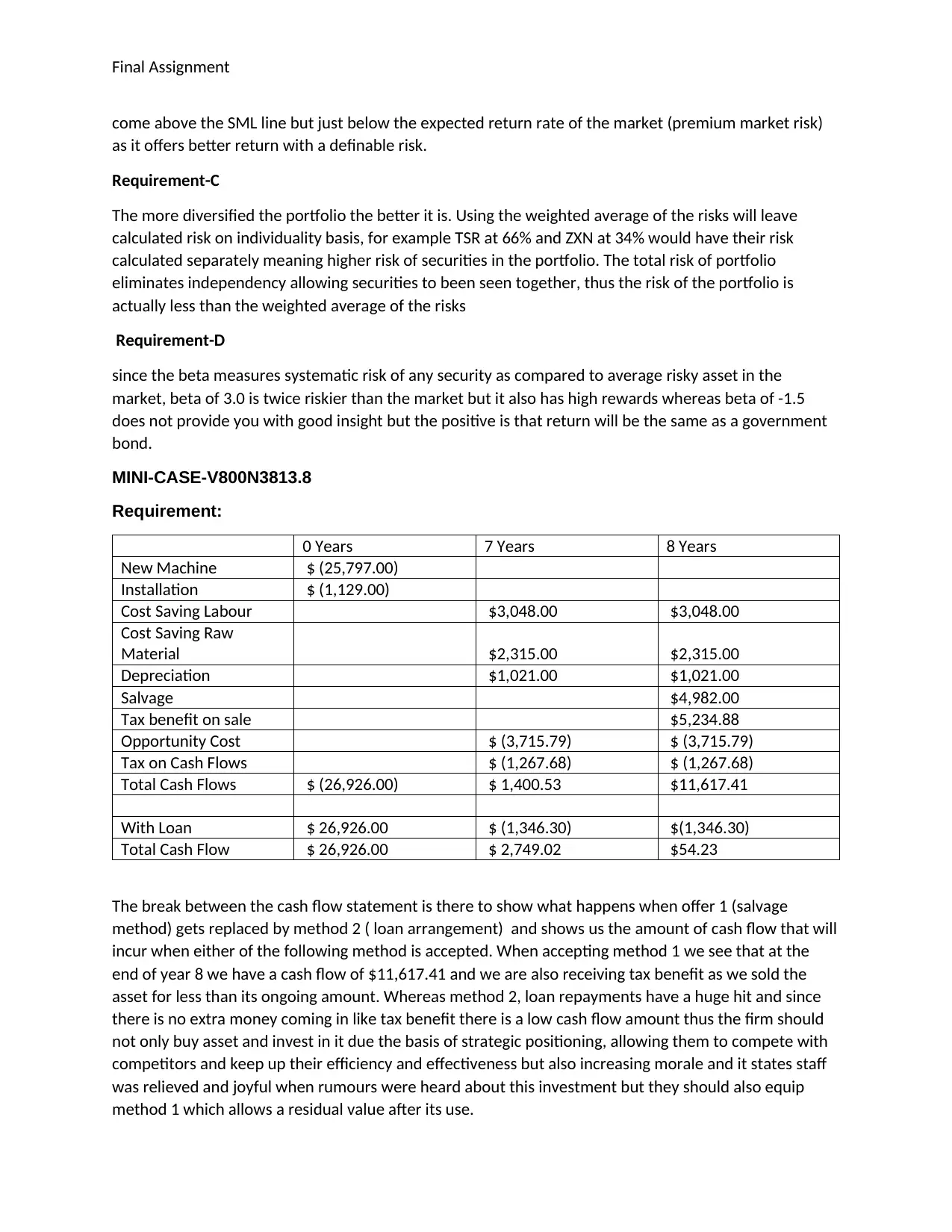

MINI-CASE-V800N3813.8

Requirement:

0 Years 7 Years 8 Years

New Machine $ (25,797.00)

Installation $ (1,129.00)

Cost Saving Labour $3,048.00 $3,048.00

Cost Saving Raw

Material $2,315.00 $2,315.00

Depreciation $1,021.00 $1,021.00

Salvage $4,982.00

Tax benefit on sale $5,234.88

Opportunity Cost $ (3,715.79) $ (3,715.79)

Tax on Cash Flows $ (1,267.68) $ (1,267.68)

Total Cash Flows $ (26,926.00) $ 1,400.53 $11,617.41

With Loan $ 26,926.00 $ (1,346.30) $(1,346.30)

Total Cash Flow $ 26,926.00 $ 2,749.02 $54.23

The break between the cash flow statement is there to show what happens when offer 1 (salvage

method) gets replaced by method 2 ( loan arrangement) and shows us the amount of cash flow that will

incur when either of the following method is accepted. When accepting method 1 we see that at the

end of year 8 we have a cash flow of $11,617.41 and we are also receiving tax benefit as we sold the

asset for less than its ongoing amount. Whereas method 2, loan repayments have a huge hit and since

there is no extra money coming in like tax benefit there is a low cash flow amount thus the firm should

not only buy asset and invest in it due the basis of strategic positioning, allowing them to compete with

competitors and keep up their efficiency and effectiveness but also increasing morale and it states staff

was relieved and joyful when rumours were heard about this investment but they should also equip

method 1 which allows a residual value after its use.

come above the SML line but just below the expected return rate of the market (premium market risk)

as it offers better return with a definable risk.

Requirement-C

The more diversified the portfolio the better it is. Using the weighted average of the risks will leave

calculated risk on individuality basis, for example TSR at 66% and ZXN at 34% would have their risk

calculated separately meaning higher risk of securities in the portfolio. The total risk of portfolio

eliminates independency allowing securities to been seen together, thus the risk of the portfolio is

actually less than the weighted average of the risks

Requirement-D

since the beta measures systematic risk of any security as compared to average risky asset in the

market, beta of 3.0 is twice riskier than the market but it also has high rewards whereas beta of -1.5

does not provide you with good insight but the positive is that return will be the same as a government

bond.

MINI-CASE-V800N3813.8

Requirement:

0 Years 7 Years 8 Years

New Machine $ (25,797.00)

Installation $ (1,129.00)

Cost Saving Labour $3,048.00 $3,048.00

Cost Saving Raw

Material $2,315.00 $2,315.00

Depreciation $1,021.00 $1,021.00

Salvage $4,982.00

Tax benefit on sale $5,234.88

Opportunity Cost $ (3,715.79) $ (3,715.79)

Tax on Cash Flows $ (1,267.68) $ (1,267.68)

Total Cash Flows $ (26,926.00) $ 1,400.53 $11,617.41

With Loan $ 26,926.00 $ (1,346.30) $(1,346.30)

Total Cash Flow $ 26,926.00 $ 2,749.02 $54.23

The break between the cash flow statement is there to show what happens when offer 1 (salvage

method) gets replaced by method 2 ( loan arrangement) and shows us the amount of cash flow that will

incur when either of the following method is accepted. When accepting method 1 we see that at the

end of year 8 we have a cash flow of $11,617.41 and we are also receiving tax benefit as we sold the

asset for less than its ongoing amount. Whereas method 2, loan repayments have a huge hit and since

there is no extra money coming in like tax benefit there is a low cash flow amount thus the firm should

not only buy asset and invest in it due the basis of strategic positioning, allowing them to compete with

competitors and keep up their efficiency and effectiveness but also increasing morale and it states staff

was relieved and joyful when rumours were heard about this investment but they should also equip

method 1 which allows a residual value after its use.

Final Assignment

The impact offers is key as the managers had given hope to invest in this due to unlikable numbers and

profits but suggestions from the oldest staff members is key input as it shows for the fact that most

experienced staff is also asking and looking for this asset to be installed thus creating a safe and healthy

environment amongst managers and staff to freely open and express their feelings.

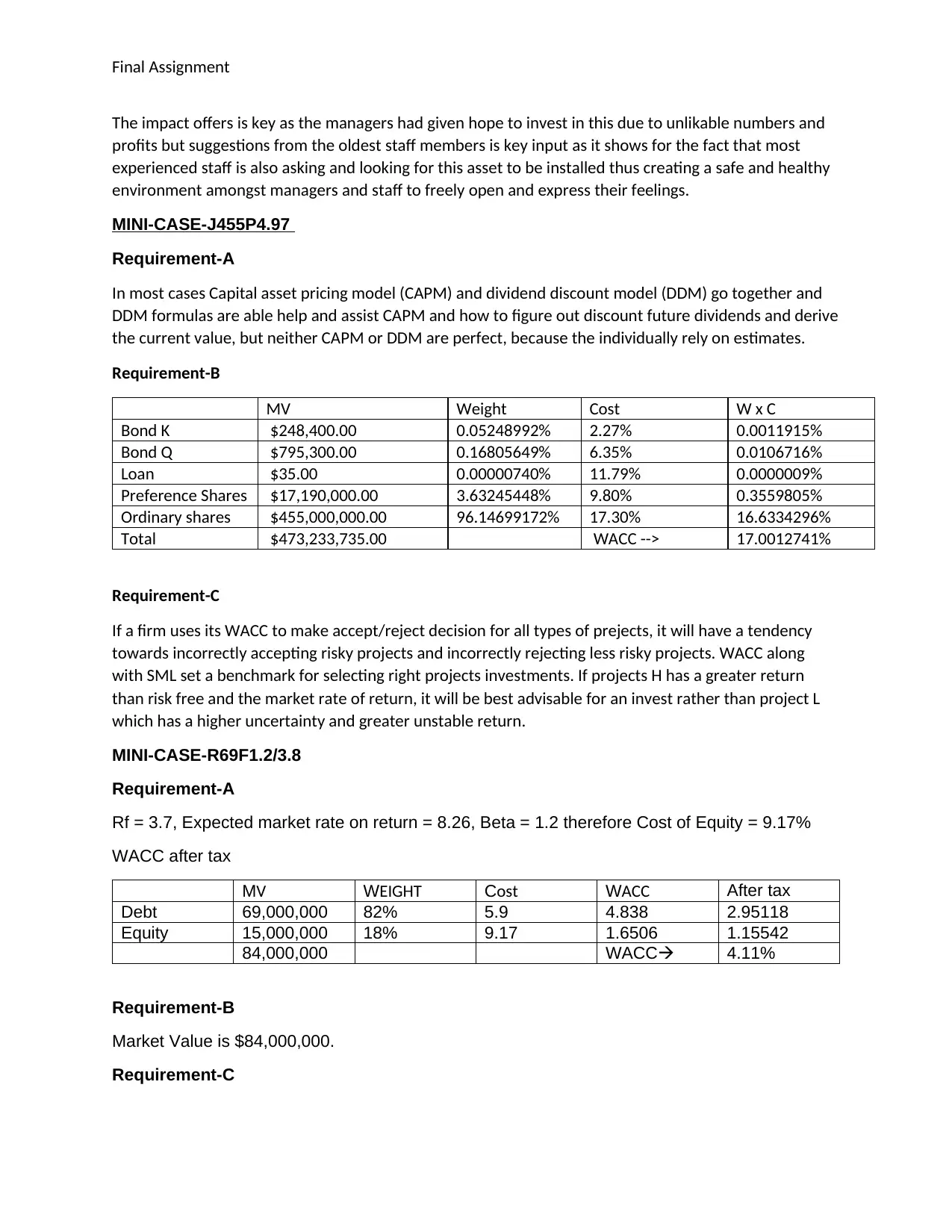

MINI-CASE-J455P4.97

Requirement-A

In most cases Capital asset pricing model (CAPM) and dividend discount model (DDM) go together and

DDM formulas are able help and assist CAPM and how to figure out discount future dividends and derive

the current value, but neither CAPM or DDM are perfect, because the individually rely on estimates.

Requirement-B

MV Weight Cost W x C

Bond K $248,400.00 0.05248992% 2.27% 0.0011915%

Bond Q $795,300.00 0.16805649% 6.35% 0.0106716%

Loan $35.00 0.00000740% 11.79% 0.0000009%

Preference Shares $17,190,000.00 3.63245448% 9.80% 0.3559805%

Ordinary shares $455,000,000.00 96.14699172% 17.30% 16.6334296%

Total $473,233,735.00 WACC --> 17.0012741%

Requirement-C

If a firm uses its WACC to make accept/reject decision for all types of prejects, it will have a tendency

towards incorrectly accepting risky projects and incorrectly rejecting less risky projects. WACC along

with SML set a benchmark for selecting right projects investments. If projects H has a greater return

than risk free and the market rate of return, it will be best advisable for an invest rather than project L

which has a higher uncertainty and greater unstable return.

MINI-CASE-R69F1.2/3.8

Requirement-A

Rf = 3.7, Expected market rate on return = 8.26, Beta = 1.2 therefore Cost of Equity = 9.17%

WACC after tax

MV WEIGHT Cost WACC After tax

Debt 69,000,000 82% 5.9 4.838 2.95118

Equity 15,000,000 18% 9.17 1.6506 1.15542

84,000,000 WACC 4.11%

Requirement-B

Market Value is $84,000,000.

Requirement-C

The impact offers is key as the managers had given hope to invest in this due to unlikable numbers and

profits but suggestions from the oldest staff members is key input as it shows for the fact that most

experienced staff is also asking and looking for this asset to be installed thus creating a safe and healthy

environment amongst managers and staff to freely open and express their feelings.

MINI-CASE-J455P4.97

Requirement-A

In most cases Capital asset pricing model (CAPM) and dividend discount model (DDM) go together and

DDM formulas are able help and assist CAPM and how to figure out discount future dividends and derive

the current value, but neither CAPM or DDM are perfect, because the individually rely on estimates.

Requirement-B

MV Weight Cost W x C

Bond K $248,400.00 0.05248992% 2.27% 0.0011915%

Bond Q $795,300.00 0.16805649% 6.35% 0.0106716%

Loan $35.00 0.00000740% 11.79% 0.0000009%

Preference Shares $17,190,000.00 3.63245448% 9.80% 0.3559805%

Ordinary shares $455,000,000.00 96.14699172% 17.30% 16.6334296%

Total $473,233,735.00 WACC --> 17.0012741%

Requirement-C

If a firm uses its WACC to make accept/reject decision for all types of prejects, it will have a tendency

towards incorrectly accepting risky projects and incorrectly rejecting less risky projects. WACC along

with SML set a benchmark for selecting right projects investments. If projects H has a greater return

than risk free and the market rate of return, it will be best advisable for an invest rather than project L

which has a higher uncertainty and greater unstable return.

MINI-CASE-R69F1.2/3.8

Requirement-A

Rf = 3.7, Expected market rate on return = 8.26, Beta = 1.2 therefore Cost of Equity = 9.17%

WACC after tax

MV WEIGHT Cost WACC After tax

Debt 69,000,000 82% 5.9 4.838 2.95118

Equity 15,000,000 18% 9.17 1.6506 1.15542

84,000,000 WACC 4.11%

Requirement-B

Market Value is $84,000,000.

Requirement-C

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Final Assignment

The dividend discount model is super consistent as it is a method for assessing the present

value of a stock based on its dividend rate. Whereas the discounted cash flow is inconsistent

due to its assessment of every element of a cash flow and then discounting that flow agains the

WACC. Another reason why the DDM is very consistent is because of the fact that the dividend

will remain constant whereas you have to account different periods of time whilst looking at the

discounted cash flow mode

Requirement-D

As the proportion of debt to equity increases, the weighted average cost of capital declines. This

is due to debt being cheaper than equity and also because debt is tax-advantaged. This can

cause misconception because if you a firm takes on more debts then cost of capital does not

matter as it would reach its peak and start to rise again

An all equity firm is something from a utopia but however if it happens it is to be assumed that

WACC does not change and it stays constant as there would be no debt to decrease the cost.

The impact that leveraged firms have on the WACC is of to reduce cost of capital by gaining

ether one debentures, loans or bank overdraft. This will take WACC near to risk free line thus

improving the value of the firm whilst reducing cost.

CODE: MCST

Requirement: connect capital structure to question 5

The models regarding to the corporate taxes and the model providing cots of financial distress

can be applied to the café business. Corporate taxes would be applies if they were to go ahead

with the offer 1 suggested by the staff member of selling the asset as the end of its useful life for

a salvage value thus that way they could have avoided costs of financial distress, choosing the

2nd offer with a near to zero cash flow value the café company could loose its ability to pay short

term debts (liquidity) thus would come under financial distress.

I do not agree that all three of the models are applicable in the real world, due to the fact that

model no. 1 that says no corporate tax applies which could only happen in utopian world and

therefore should be totally obliviated from today’s society where as the other 2 models are

realistic as there are tax’s charged on everything and seeing a company in financial distress due

their high debts is very much common.

The dividend discount model is super consistent as it is a method for assessing the present

value of a stock based on its dividend rate. Whereas the discounted cash flow is inconsistent

due to its assessment of every element of a cash flow and then discounting that flow agains the

WACC. Another reason why the DDM is very consistent is because of the fact that the dividend

will remain constant whereas you have to account different periods of time whilst looking at the

discounted cash flow mode

Requirement-D

As the proportion of debt to equity increases, the weighted average cost of capital declines. This

is due to debt being cheaper than equity and also because debt is tax-advantaged. This can

cause misconception because if you a firm takes on more debts then cost of capital does not

matter as it would reach its peak and start to rise again

An all equity firm is something from a utopia but however if it happens it is to be assumed that

WACC does not change and it stays constant as there would be no debt to decrease the cost.

The impact that leveraged firms have on the WACC is of to reduce cost of capital by gaining

ether one debentures, loans or bank overdraft. This will take WACC near to risk free line thus

improving the value of the firm whilst reducing cost.

CODE: MCST

Requirement: connect capital structure to question 5

The models regarding to the corporate taxes and the model providing cots of financial distress

can be applied to the café business. Corporate taxes would be applies if they were to go ahead

with the offer 1 suggested by the staff member of selling the asset as the end of its useful life for

a salvage value thus that way they could have avoided costs of financial distress, choosing the

2nd offer with a near to zero cash flow value the café company could loose its ability to pay short

term debts (liquidity) thus would come under financial distress.

I do not agree that all three of the models are applicable in the real world, due to the fact that

model no. 1 that says no corporate tax applies which could only happen in utopian world and

therefore should be totally obliviated from today’s society where as the other 2 models are

realistic as there are tax’s charged on everything and seeing a company in financial distress due

their high debts is very much common.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.