Financial Reporting: Framework, Standards, and Performance Analysis

VerifiedAdded on 2020/12/29

|16

|3653

|378

Report

AI Summary

This report provides a comprehensive overview of financial reporting, encompassing its content, purpose, and the significance of financial statements. It delves into the conceptual and regulatory frameworks, highlighting their qualitative characteristics and importance for stakeholders. The report examines the role of financial reporting in achieving organizational objectives and growth, followed by the presentation of financial statements as per IAS 1. It includes a comparative analysis of cash flow, balance sheets, and income statements, along with an interpretation of Marks and Spencer plc's financial performance through ratio analysis. The report also differentiates between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), evaluating the benefits of IFRS adoption and its global compliance levels.

FINANACIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1. Describing the content and purpose of financial reporting.....................................................1

2. Examining the conceptual and regulatory framework their requirement, purpose and

principles with the qualitative characteristics.............................................................................2

3. Identifying the importance of financial reporting for the stakeholder in achieving their

objectives.....................................................................................................................................3

4. Importance of financial reporting for meeting organisational objectives and growth............4

5. Presenting financial statement as per IAS 1............................................................................4

d). Explaining the type of information which is provided by cash flow in comparison with

balance sheet and income statement...........................................................................................6

6. Interpretation of the financial performance of Marks and Spencer plc..................................7

7. Explaining the difference between International Accounting Standard(IAS) and

International Financial Reporting standard.................................................................................9

8. Evaluating the benefits of IFRS............................................................................................10

9. Determining the degree of compliances with IFRS across the world and the factor that

affect the compliances...............................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

1. Describing the content and purpose of financial reporting.....................................................1

2. Examining the conceptual and regulatory framework their requirement, purpose and

principles with the qualitative characteristics.............................................................................2

3. Identifying the importance of financial reporting for the stakeholder in achieving their

objectives.....................................................................................................................................3

4. Importance of financial reporting for meeting organisational objectives and growth............4

5. Presenting financial statement as per IAS 1............................................................................4

d). Explaining the type of information which is provided by cash flow in comparison with

balance sheet and income statement...........................................................................................6

6. Interpretation of the financial performance of Marks and Spencer plc..................................7

7. Explaining the difference between International Accounting Standard(IAS) and

International Financial Reporting standard.................................................................................9

8. Evaluating the benefits of IFRS............................................................................................10

9. Determining the degree of compliances with IFRS across the world and the factor that

affect the compliances...............................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial reporting is the process of presenting and disclosing the monetary performance

and position of the company within a specific time period. It can be refereed as the process

which formatting and disclosing the final accounts or statements to the various stakeholders of

company. The present report will discuss various aspects of financial reporting in organisation.

The context and purpose of preparing will be outlined. It will demonstrate different conceptual

and regulatory framework of reporting with their qualitative characteristics. Importance of

accounting reports to stakeholders and organisation in achieving business objectives will be

discussed. Calculation of Financial statements of Goodwin plc and financial performance of

Marks and Spencer plc will be presented. A comparison on IFRS and IAS will be discussed

along with the benefit of IFRS and degree of compliances in adopting it..

1. Describing the content and purpose of financial reporting.

It can simply be termed as disclosing the monetary information of the company to the

various stakeholders about the company's financial performance and position in a specific period

of time. Financial reporting includes all the financial transaction of the company and

communicates it in the form of financial statements to the internal management and external

users. Financial statements in crucial as it will help in decision making for internal and external

users, for internal management it is beneficial in making strategies to further improve the

financial performance (financial reporting ,2018). For external users it will assist in making

decisions regarding their investment in company.

The content of financial reporting will includes all the feasibility statements which helps

in communicating all the monetary information regarding company’s financial performance. It is

essential for the management of an organisation to get the summarized information about the

performance and monetary position in order to analyse the effectiveness of business operations

in an year.

Financial reporting is an important part of the company as it helps in attracting more

investors and sales holder to invest in company (Council, 2012). The main purpose of financial

reporting are:

1

Financial reporting is the process of presenting and disclosing the monetary performance

and position of the company within a specific time period. It can be refereed as the process

which formatting and disclosing the final accounts or statements to the various stakeholders of

company. The present report will discuss various aspects of financial reporting in organisation.

The context and purpose of preparing will be outlined. It will demonstrate different conceptual

and regulatory framework of reporting with their qualitative characteristics. Importance of

accounting reports to stakeholders and organisation in achieving business objectives will be

discussed. Calculation of Financial statements of Goodwin plc and financial performance of

Marks and Spencer plc will be presented. A comparison on IFRS and IAS will be discussed

along with the benefit of IFRS and degree of compliances in adopting it..

1. Describing the content and purpose of financial reporting.

It can simply be termed as disclosing the monetary information of the company to the

various stakeholders about the company's financial performance and position in a specific period

of time. Financial reporting includes all the financial transaction of the company and

communicates it in the form of financial statements to the internal management and external

users. Financial statements in crucial as it will help in decision making for internal and external

users, for internal management it is beneficial in making strategies to further improve the

financial performance (financial reporting ,2018). For external users it will assist in making

decisions regarding their investment in company.

The content of financial reporting will includes all the feasibility statements which helps

in communicating all the monetary information regarding company’s financial performance. It is

essential for the management of an organisation to get the summarized information about the

performance and monetary position in order to analyse the effectiveness of business operations

in an year.

Financial reporting is an important part of the company as it helps in attracting more

investors and sales holder to invest in company (Council, 2012). The main purpose of financial

reporting are:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To provide accurate and timely information regarding the company's monetary

performance to the management which will assist them in planning, analysing, and

decision making process.

One of the main purpose of the financial reporting is to assist the external users like

stakeholder, investors and creditors to communicate them regarding monetary position of

company which will assist then in making decisions regarding investing their money

(Chen and et.al., 2011).

To provide information the ways in which company is using its resources.

To assist the auditors in getting proper information which helps in their auditing

procedures.

2. Examining the conceptual and regulatory framework their requirement, purpose and principles

with the qualitative characteristics.

In financial reporting, conceptual framework can be dined as the theory of accounting

that has been prepared by the standard board. Conceptual framework helps in dealing with

different financial reporting issues such as the characteristics that helps in making accounting

statement useful. Conceptual framework will help in assist the accountant as to how the

treatment of accounting information has to be reported in the financial statement (Nobe, 2014). It

helps in setting the outlines of the financial statements that assist external users in properly

understand the information. conceptual framework set the guidelines for the company in order to

use the accounting standard such as GAAP principles in treating the financial treatment of

transactions.

Whereas, the regulatory framework of financial reporting helps in setting the rules and

guidelines of preparation the financial statement of under the one set of rules. Regulatory

framework has been developed in order to set one common language of accounting which helps

different organisation and investors to understand the monetary statements in order to compare

and make decisions.

The conceptual and regulatory framework is essential that assist the accountant to prepare

the financial statement that will be reliable, understandable and comparable (Rajgopal and

Venkatachalam, 2011). It is important for the internal as well as to the outside users in their

2

performance to the management which will assist them in planning, analysing, and

decision making process.

One of the main purpose of the financial reporting is to assist the external users like

stakeholder, investors and creditors to communicate them regarding monetary position of

company which will assist then in making decisions regarding investing their money

(Chen and et.al., 2011).

To provide information the ways in which company is using its resources.

To assist the auditors in getting proper information which helps in their auditing

procedures.

2. Examining the conceptual and regulatory framework their requirement, purpose and principles

with the qualitative characteristics.

In financial reporting, conceptual framework can be dined as the theory of accounting

that has been prepared by the standard board. Conceptual framework helps in dealing with

different financial reporting issues such as the characteristics that helps in making accounting

statement useful. Conceptual framework will help in assist the accountant as to how the

treatment of accounting information has to be reported in the financial statement (Nobe, 2014). It

helps in setting the outlines of the financial statements that assist external users in properly

understand the information. conceptual framework set the guidelines for the company in order to

use the accounting standard such as GAAP principles in treating the financial treatment of

transactions.

Whereas, the regulatory framework of financial reporting helps in setting the rules and

guidelines of preparation the financial statement of under the one set of rules. Regulatory

framework has been developed in order to set one common language of accounting which helps

different organisation and investors to understand the monetary statements in order to compare

and make decisions.

The conceptual and regulatory framework is essential that assist the accountant to prepare

the financial statement that will be reliable, understandable and comparable (Rajgopal and

Venkatachalam, 2011). It is important for the internal as well as to the outside users in their

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decision making process. The qualitative characteristics of the regulatory framework are as

follows: Understandable: The financial statement should be understandable for the external users

as well the internal management of the company. Comparable: This characteristics will helps in making financial reporting that can be

compared with other company's financial statements. Relevance: It will assist the stakeholder to get the relevant information regarding the

company's financial performance in a specific accounting period.

Reliable: It is foremost important that the information present in the statement are free

from any error, omission or free from any bias.

3. Identifying the importance of financial reporting for the stakeholder in achieving their

objectives.

There various individuals, groups or organisation that are bothers about the company's

monetary activities and performance. They are known as the stakeholders of the company, which

are an essential part of an organisation which can be affected by the companies financial

performance. The benefits of financial information to stakeholders of organisation are as follows:

Owners: The financial statement of company is beneficial for the owners and top

executive in analysing the performance level of company’s different operations

(Christensen, Hail and Leuz, 2013). These statements would help them in making

decisions, budgets and plans to improve and enhance the financial performance that will

further assist in accomplishing the organisational goals.

Shareholders: they are the important part as they invest their money in organisation and

expect higher return from the company. The financial information will help them in

knowing how their money is being using by company through income and cash flow

statement. Balance sheet will help in knowing the company's current position and their

expected return.

Employees: they are the one who works to increase the productivity of the company. The

monetary information will help them in analysing the profitability and stability of the

3

follows: Understandable: The financial statement should be understandable for the external users

as well the internal management of the company. Comparable: This characteristics will helps in making financial reporting that can be

compared with other company's financial statements. Relevance: It will assist the stakeholder to get the relevant information regarding the

company's financial performance in a specific accounting period.

Reliable: It is foremost important that the information present in the statement are free

from any error, omission or free from any bias.

3. Identifying the importance of financial reporting for the stakeholder in achieving their

objectives.

There various individuals, groups or organisation that are bothers about the company's

monetary activities and performance. They are known as the stakeholders of the company, which

are an essential part of an organisation which can be affected by the companies financial

performance. The benefits of financial information to stakeholders of organisation are as follows:

Owners: The financial statement of company is beneficial for the owners and top

executive in analysing the performance level of company’s different operations

(Christensen, Hail and Leuz, 2013). These statements would help them in making

decisions, budgets and plans to improve and enhance the financial performance that will

further assist in accomplishing the organisational goals.

Shareholders: they are the important part as they invest their money in organisation and

expect higher return from the company. The financial information will help them in

knowing how their money is being using by company through income and cash flow

statement. Balance sheet will help in knowing the company's current position and their

expected return.

Employees: they are the one who works to increase the productivity of the company. The

monetary information will help them in analysing the profitability and stability of the

3

company. It will assist them in identifying their stability in company, and the growth

opportunities in future.

Supplier: they help in supplier the raw material which helps in manufacturing the goods

and services of the company. The financial statement will help them in assuring their

payment by the company on time.

4. Importance of financial reporting for meeting organisational objectives and growth.

Financial reporting is very essential in communicating the financial activity and

performance level to the management of a company. It assist the management in identify and

analyse the statements in order to make decisions, planning and making budgets. Financial

statements is crucial for organisation in order to achieve their organisational goals and

objectives. The importance of financial reporting are:

Financial reporting will assist the management in evaluating and analysing various

business operations and activity in organisation (Costello and WITTENBERG‐

MOERMAN, 2011).

The several statements of monetary performance like cash flow and statement of profit

and loss will help in determining the income and expenses in order to prepare and

formulate different strategies to control the cost in order to increase the revenue of

organisation.

Financial account assist the management in tracking and monetizing the cash outflow and

inflow of the company which will assist in eliminating unnecessary expenses of the

company .

These reports will assist in recording the liability of company which will ensure in

payment of company's expenses (Lusardi and Mitchell, 2014). It will help in increasing

the goodwill of the company and achieving its business objectives.

5. Presenting financial statement as per IAS 1.

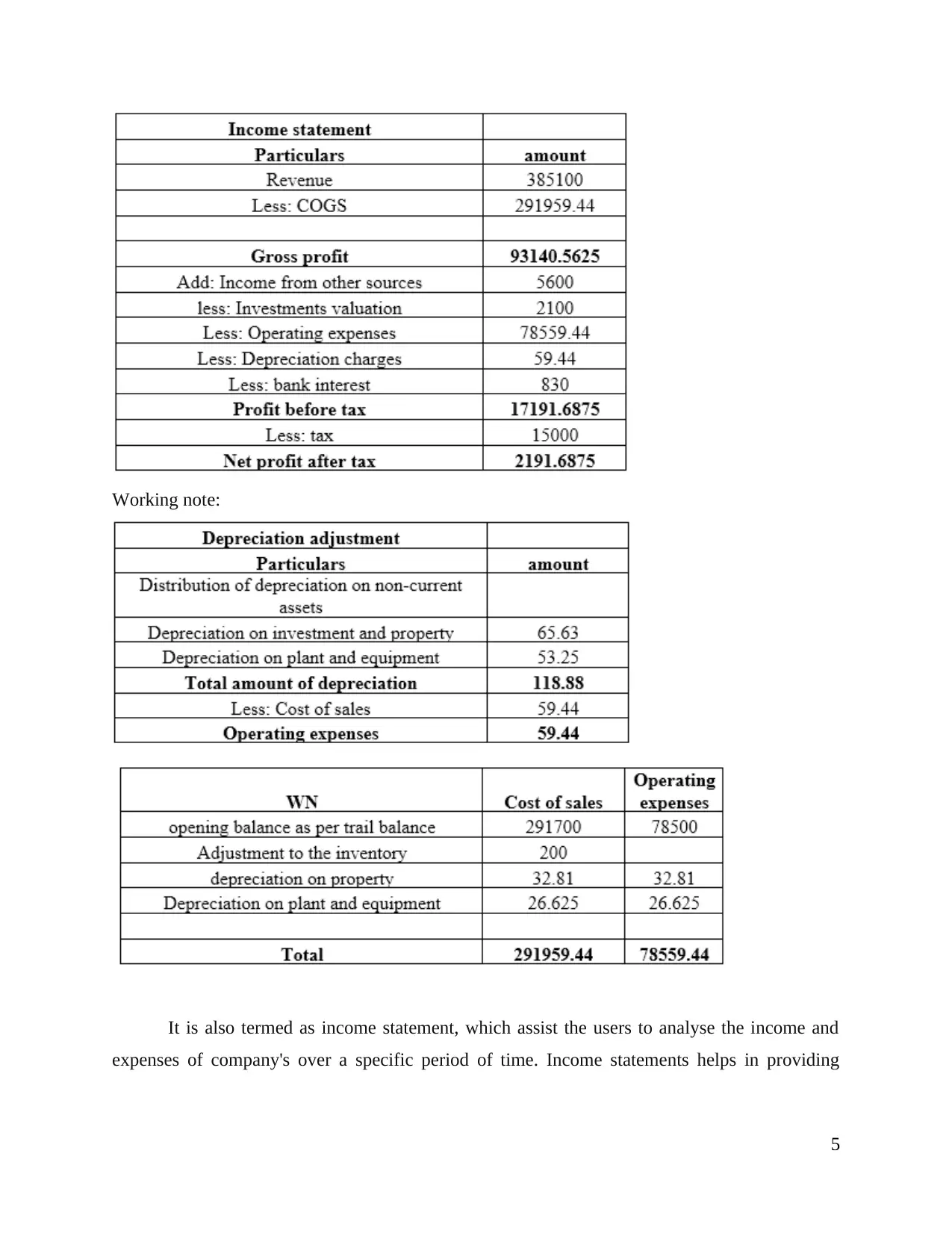

a). Statement of profit and loss:

4

opportunities in future.

Supplier: they help in supplier the raw material which helps in manufacturing the goods

and services of the company. The financial statement will help them in assuring their

payment by the company on time.

4. Importance of financial reporting for meeting organisational objectives and growth.

Financial reporting is very essential in communicating the financial activity and

performance level to the management of a company. It assist the management in identify and

analyse the statements in order to make decisions, planning and making budgets. Financial

statements is crucial for organisation in order to achieve their organisational goals and

objectives. The importance of financial reporting are:

Financial reporting will assist the management in evaluating and analysing various

business operations and activity in organisation (Costello and WITTENBERG‐

MOERMAN, 2011).

The several statements of monetary performance like cash flow and statement of profit

and loss will help in determining the income and expenses in order to prepare and

formulate different strategies to control the cost in order to increase the revenue of

organisation.

Financial account assist the management in tracking and monetizing the cash outflow and

inflow of the company which will assist in eliminating unnecessary expenses of the

company .

These reports will assist in recording the liability of company which will ensure in

payment of company's expenses (Lusardi and Mitchell, 2014). It will help in increasing

the goodwill of the company and achieving its business objectives.

5. Presenting financial statement as per IAS 1.

a). Statement of profit and loss:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working note:

It is also termed as income statement, which assist the users to analyse the income and

expenses of company's over a specific period of time. Income statements helps in providing

5

It is also termed as income statement, which assist the users to analyse the income and

expenses of company's over a specific period of time. Income statements helps in providing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information about company's revenue, expenses, gains and losses with the details of sales over a

specific time period.

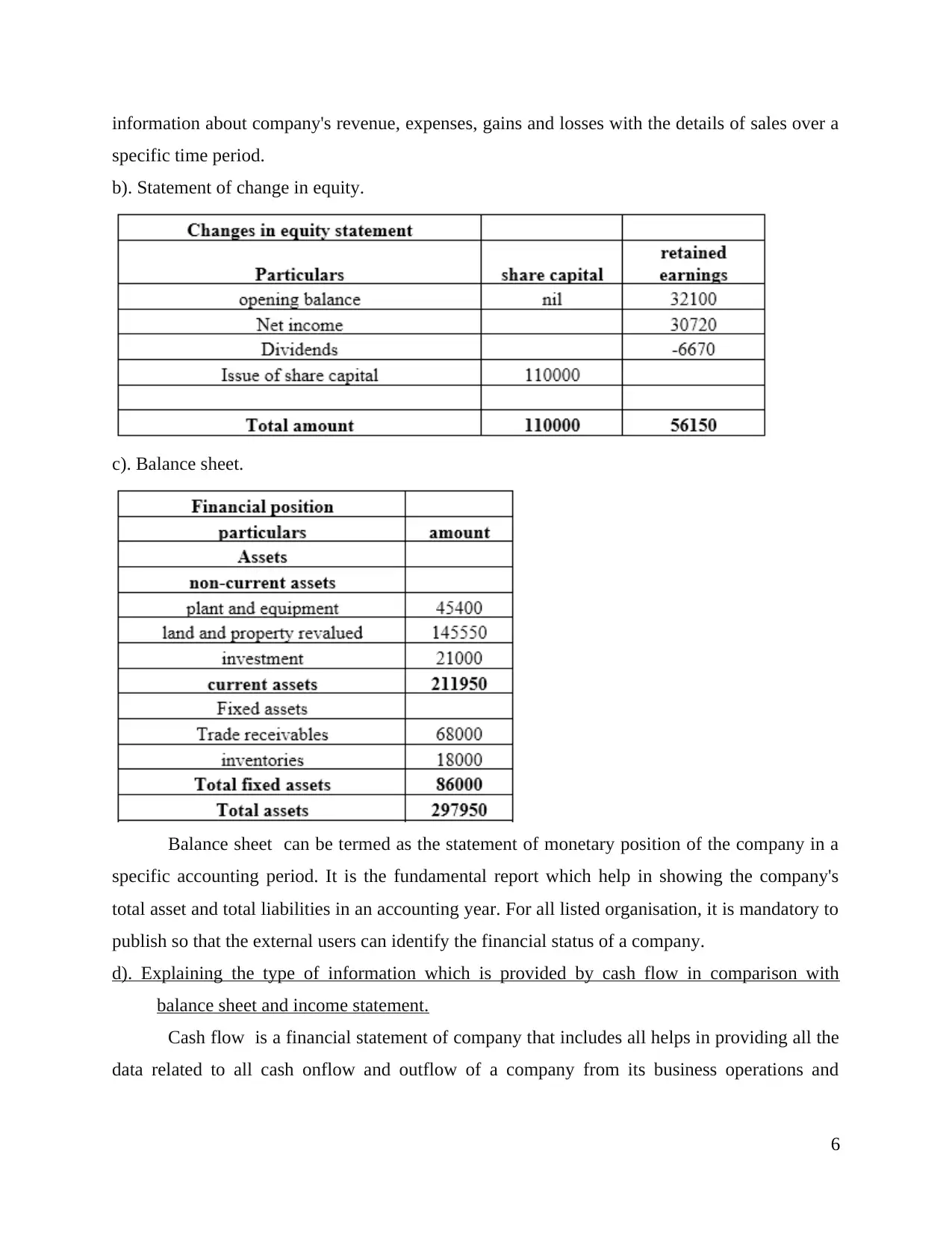

b). Statement of change in equity.

c). Balance sheet.

Balance sheet can be termed as the statement of monetary position of the company in a

specific accounting period. It is the fundamental report which help in showing the company's

total asset and total liabilities in an accounting year. For all listed organisation, it is mandatory to

publish so that the external users can identify the financial status of a company.

d). Explaining the type of information which is provided by cash flow in comparison with

balance sheet and income statement.

Cash flow is a financial statement of company that includes all helps in providing all the

data related to all cash onflow and outflow of a company from its business operations and

6

specific time period.

b). Statement of change in equity.

c). Balance sheet.

Balance sheet can be termed as the statement of monetary position of the company in a

specific accounting period. It is the fundamental report which help in showing the company's

total asset and total liabilities in an accounting year. For all listed organisation, it is mandatory to

publish so that the external users can identify the financial status of a company.

d). Explaining the type of information which is provided by cash flow in comparison with

balance sheet and income statement.

Cash flow is a financial statement of company that includes all helps in providing all the

data related to all cash onflow and outflow of a company from its business operations and

6

investment sources. Whereas, income statements assist in providing information regarding the

income and expenses of the company in a specific accounting period (Palepu, Healy and Peek,

2013). Statement of position or balance sheet is the fundamental reports that help in showing the

company's liability and assets in a period.

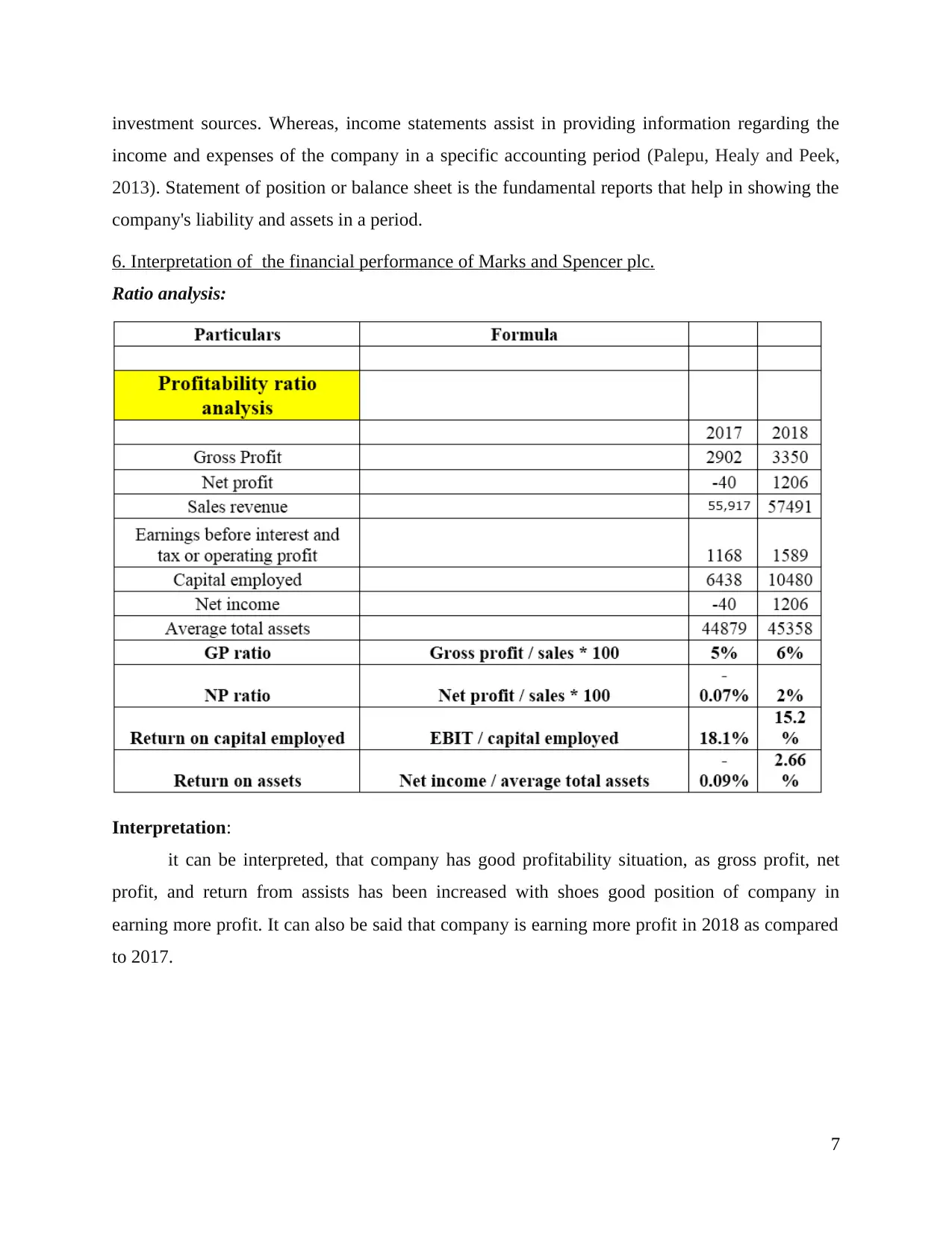

6. Interpretation of the financial performance of Marks and Spencer plc.

Ratio analysis:

Interpretation:

it can be interpreted, that company has good profitability situation, as gross profit, net

profit, and return from assists has been increased with shoes good position of company in

earning more profit. It can also be said that company is earning more profit in 2018 as compared

to 2017.

7

income and expenses of the company in a specific accounting period (Palepu, Healy and Peek,

2013). Statement of position or balance sheet is the fundamental reports that help in showing the

company's liability and assets in a period.

6. Interpretation of the financial performance of Marks and Spencer plc.

Ratio analysis:

Interpretation:

it can be interpreted, that company has good profitability situation, as gross profit, net

profit, and return from assists has been increased with shoes good position of company in

earning more profit. It can also be said that company is earning more profit in 2018 as compared

to 2017.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

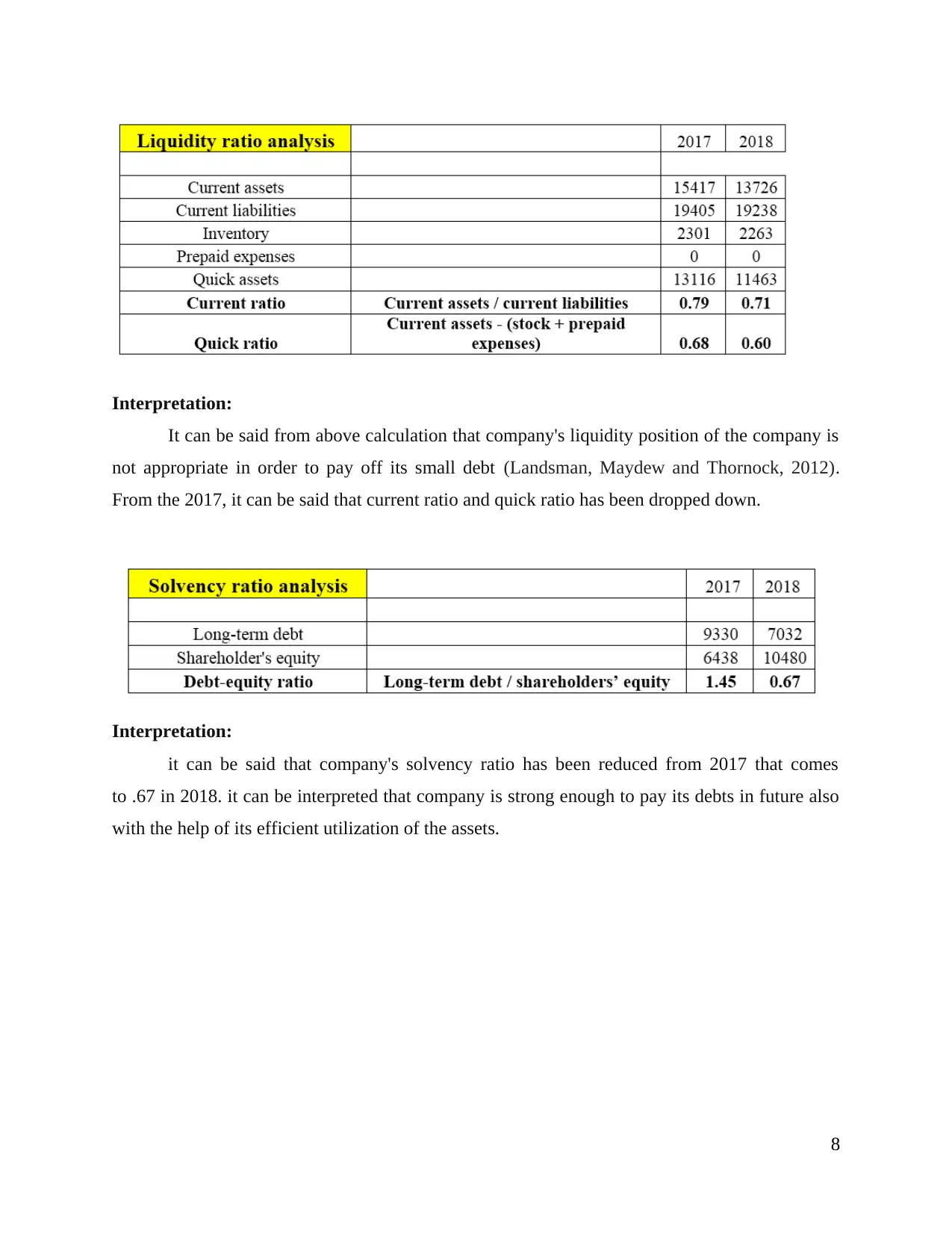

Interpretation:

It can be said from above calculation that company's liquidity position of the company is

not appropriate in order to pay off its small debt (Landsman, Maydew and Thornock, 2012).

From the 2017, it can be said that current ratio and quick ratio has been dropped down.

Interpretation:

it can be said that company's solvency ratio has been reduced from 2017 that comes

to .67 in 2018. it can be interpreted that company is strong enough to pay its debts in future also

with the help of its efficient utilization of the assets.

8

It can be said from above calculation that company's liquidity position of the company is

not appropriate in order to pay off its small debt (Landsman, Maydew and Thornock, 2012).

From the 2017, it can be said that current ratio and quick ratio has been dropped down.

Interpretation:

it can be said that company's solvency ratio has been reduced from 2017 that comes

to .67 in 2018. it can be interpreted that company is strong enough to pay its debts in future also

with the help of its efficient utilization of the assets.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

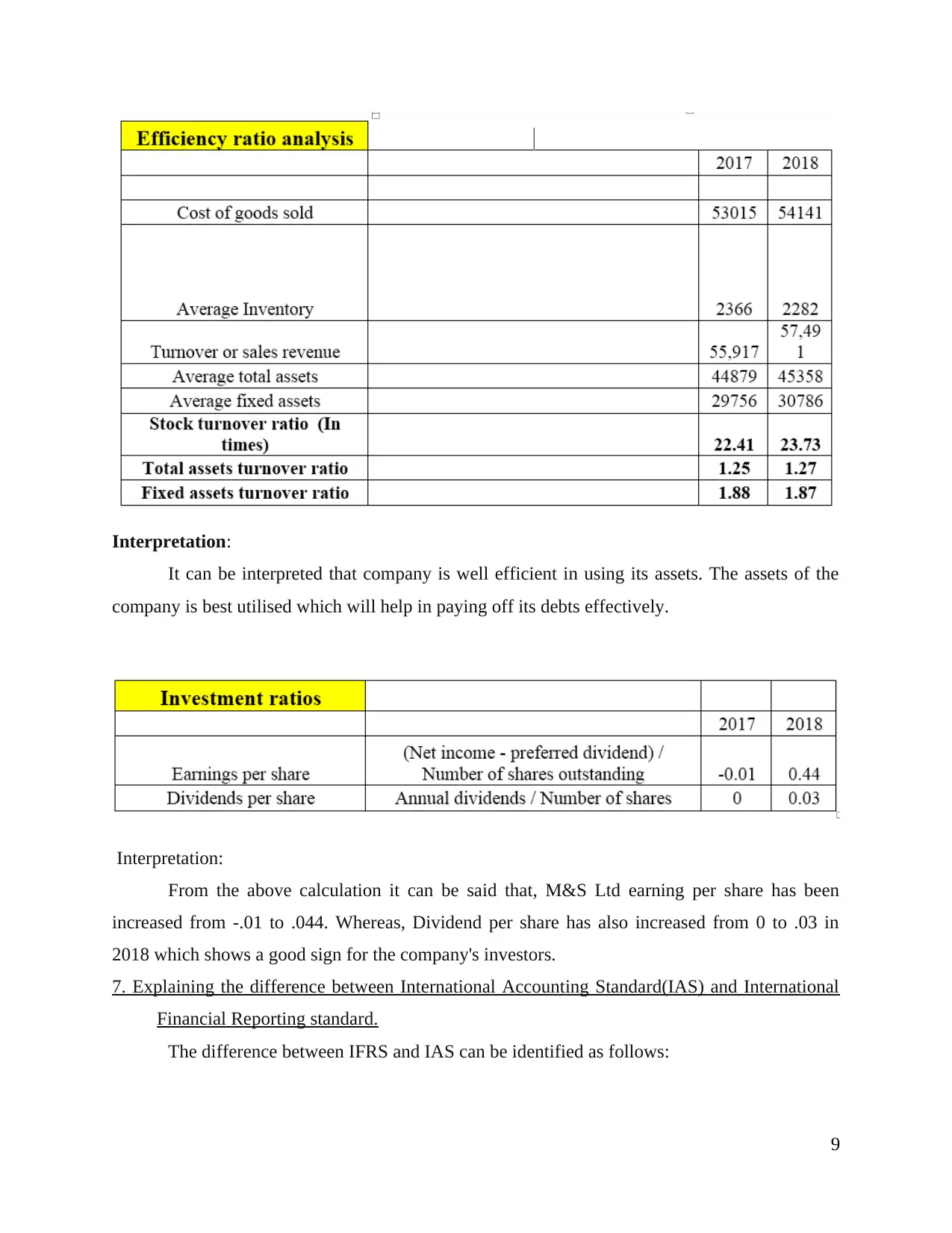

Interpretation:

It can be interpreted that company is well efficient in using its assets. The assets of the

company is best utilised which will help in paying off its debts effectively.

Interpretation:

From the above calculation it can be said that, M&S Ltd earning per share has been

increased from -.01 to .044. Whereas, Dividend per share has also increased from 0 to .03 in

2018 which shows a good sign for the company's investors.

7. Explaining the difference between International Accounting Standard(IAS) and International

Financial Reporting standard.

The difference between IFRS and IAS can be identified as follows:

9

It can be interpreted that company is well efficient in using its assets. The assets of the

company is best utilised which will help in paying off its debts effectively.

Interpretation:

From the above calculation it can be said that, M&S Ltd earning per share has been

increased from -.01 to .044. Whereas, Dividend per share has also increased from 0 to .03 in

2018 which shows a good sign for the company's investors.

7. Explaining the difference between International Accounting Standard(IAS) and International

Financial Reporting standard.

The difference between IFRS and IAS can be identified as follows:

9

International financial reporting standard is a set of accounting standard which has been

developed by international Accounting Standard Board. It helps in providing framework which

assist the company's accountant the disclosure of the monetary information and presenting it in

the final accounts of the organisation. IFRS main goal is to provide a global framework to all the

companies rather than a set of rules which provides guidance in presenting and preparing the

financial statements (DeFond and et.al, 2011). It assist the organisation which have business

activities overseas and connected with different organisations the common set of format will help

in comparing and understand the final accounts of various organisation. IFRS focuses mainly on

the preparation of monetary disclosure of performance which will assist the investors from

worldwide in investing their money. Adopting IFRS provides a world wide standard that assist in

having a common accounting language to all the listed companies. This will help the investors in

easily compare and understand different company' s final accounts.

Whereas, IAS is the older version that has been replaced by IFRS in 2001. it is the first

international accounting standard. The main goal of IAS is to make it easy to compare the

business activities through their final accounts around the world. It helps in setting accounting

guidelines which assist the accountant to increase the transparency in financial statement in order

to increase the international trade and investment. IAS focuses on setting guidelines of

accounting which helps in promoting transparency, accountability and efficiency in financial

market around the world.

8. Evaluating the benefits of IFRS.

For the organisation that are engaged in having business activities in more than one

country, it is very essential for them to have common language of accounting in that countries

also. IFRS helps in setting common framework of preparing and disclosing the financial

information in final accounts of company (Horton, Serafeim and Serafeim, 2013). Having

common accounting language will made it more beneficial for the investors and users of

financial statement to easy compare and understand thee information. Following are the benefits

of IFRS are as follows: Advantage for Investors: As compared to other regulatory framework, IFRS gives more

emphasis on the investors benefit. With the adaptation of IFRS, accountant will prepare

more accurate, timely and comprehensive final accounts that are more understandable for

10

developed by international Accounting Standard Board. It helps in providing framework which

assist the company's accountant the disclosure of the monetary information and presenting it in

the final accounts of the organisation. IFRS main goal is to provide a global framework to all the

companies rather than a set of rules which provides guidance in presenting and preparing the

financial statements (DeFond and et.al, 2011). It assist the organisation which have business

activities overseas and connected with different organisations the common set of format will help

in comparing and understand the final accounts of various organisation. IFRS focuses mainly on

the preparation of monetary disclosure of performance which will assist the investors from

worldwide in investing their money. Adopting IFRS provides a world wide standard that assist in

having a common accounting language to all the listed companies. This will help the investors in

easily compare and understand different company' s final accounts.

Whereas, IAS is the older version that has been replaced by IFRS in 2001. it is the first

international accounting standard. The main goal of IAS is to make it easy to compare the

business activities through their final accounts around the world. It helps in setting accounting

guidelines which assist the accountant to increase the transparency in financial statement in order

to increase the international trade and investment. IAS focuses on setting guidelines of

accounting which helps in promoting transparency, accountability and efficiency in financial

market around the world.

8. Evaluating the benefits of IFRS.

For the organisation that are engaged in having business activities in more than one

country, it is very essential for them to have common language of accounting in that countries

also. IFRS helps in setting common framework of preparing and disclosing the financial

information in final accounts of company (Horton, Serafeim and Serafeim, 2013). Having

common accounting language will made it more beneficial for the investors and users of

financial statement to easy compare and understand thee information. Following are the benefits

of IFRS are as follows: Advantage for Investors: As compared to other regulatory framework, IFRS gives more

emphasis on the investors benefit. With the adaptation of IFRS, accountant will prepare

more accurate, timely and comprehensive final accounts that are more understandable for

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.