Accounting for Managers (ACC00724) - S2 2019: Assignment 2 Analysis

VerifiedAdded on 2022/11/19

|10

|1256

|489

Homework Assignment

AI Summary

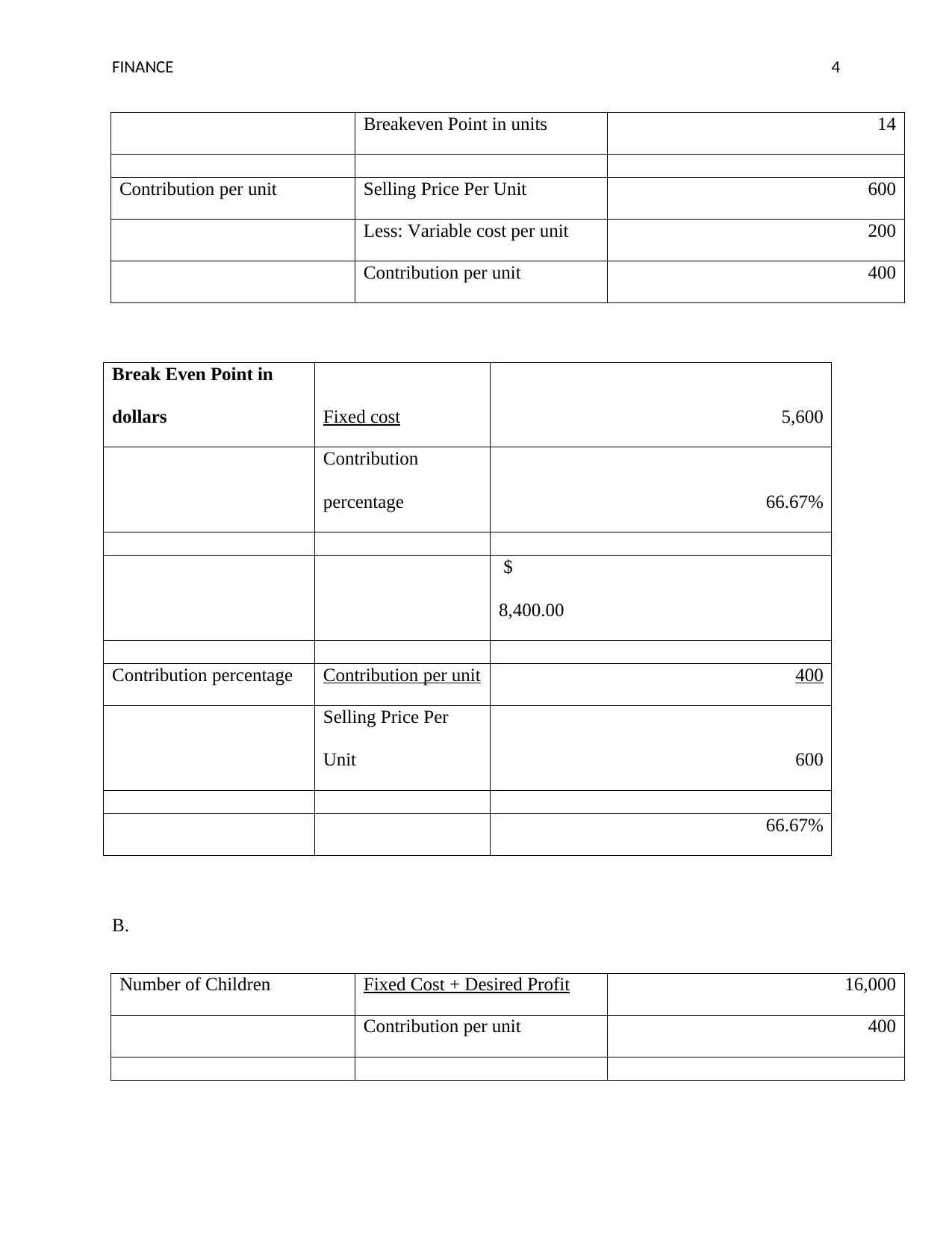

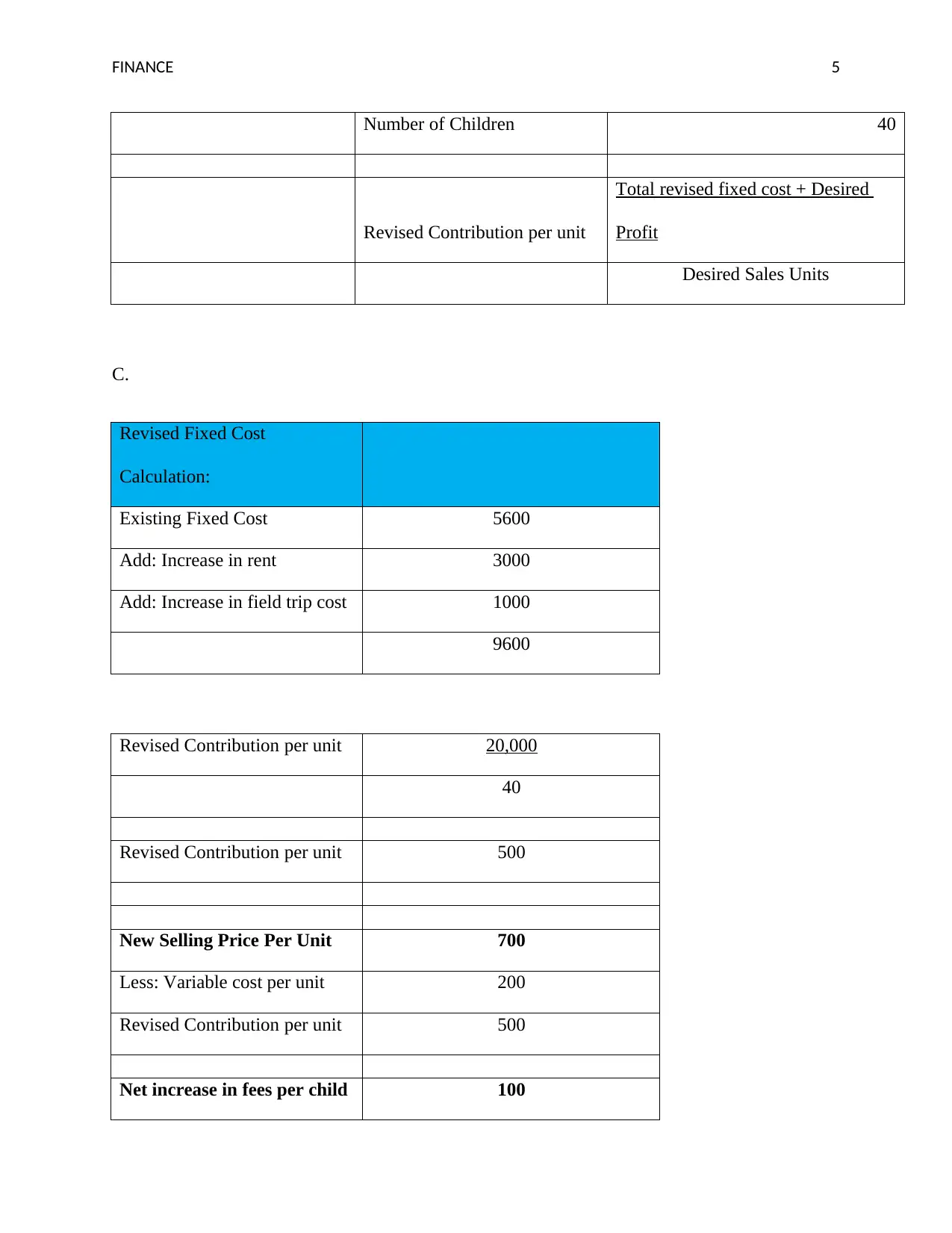

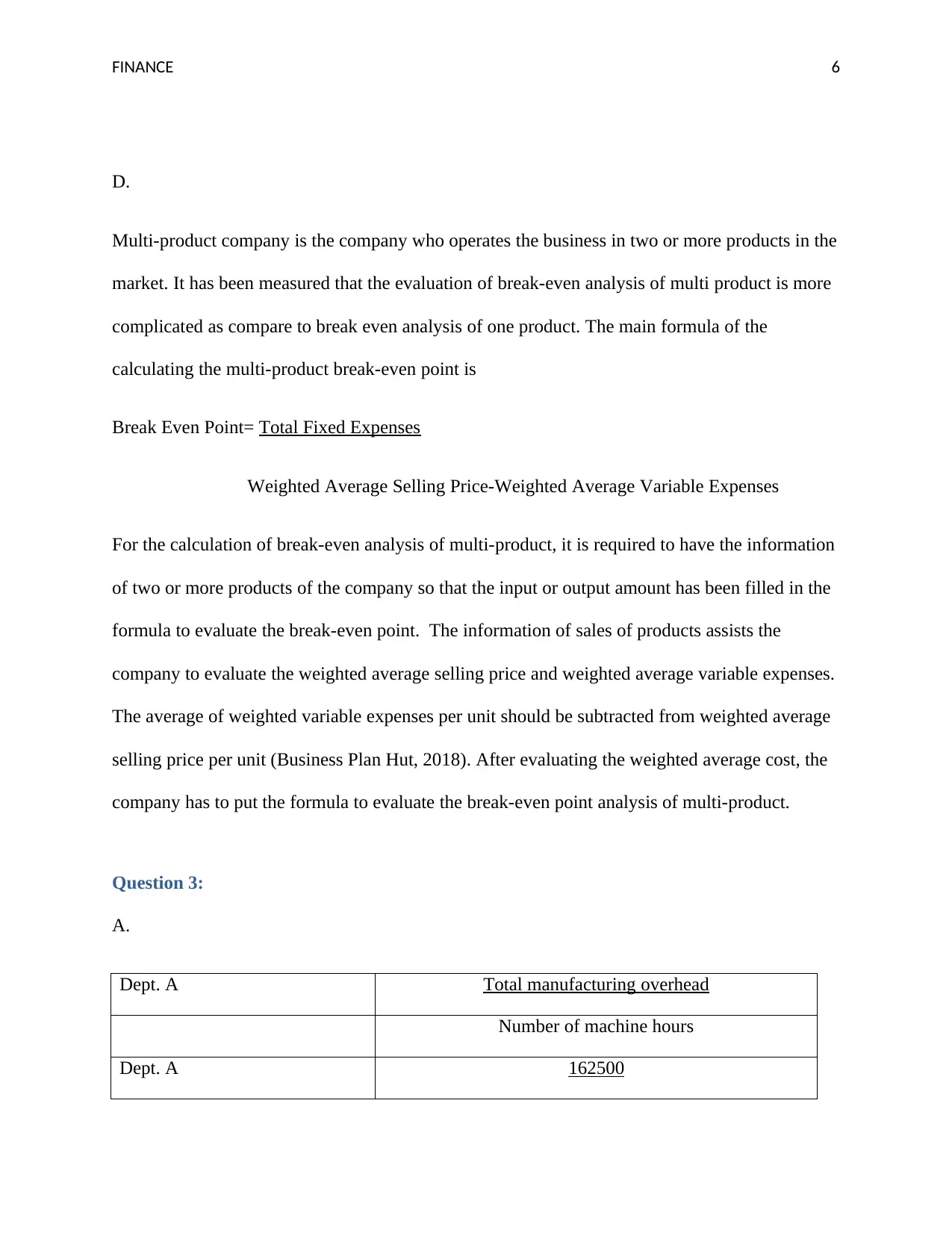

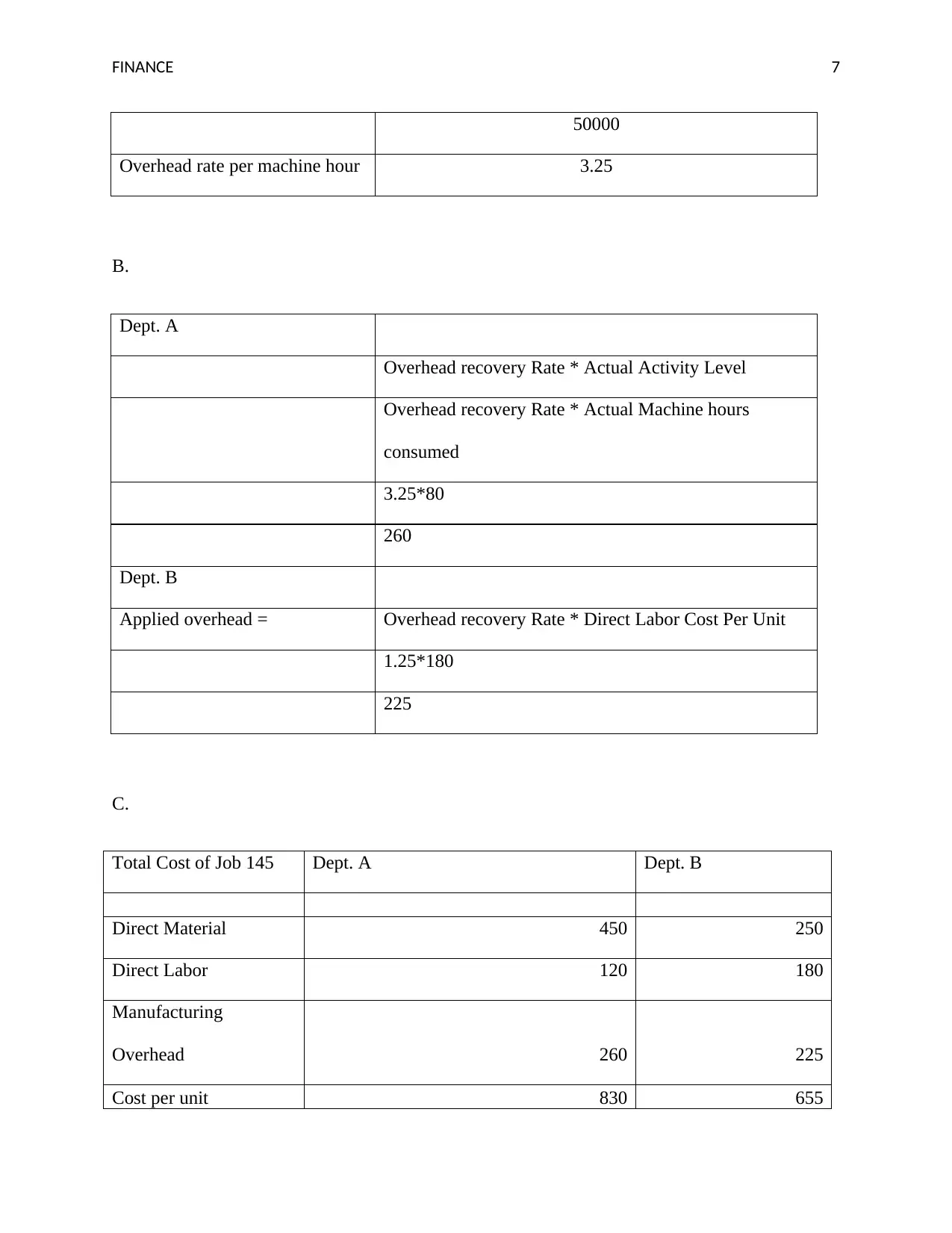

This document presents a comprehensive solution to a finance assignment, addressing key concepts in accounting and financial analysis. The assignment covers the calculation and interpretation of various financial ratios, including profitability, efficiency, and liquidity ratios, to assess a company's financial health. It also delves into break-even analysis, exploring the calculation of break-even points in units and dollars, and the impact of changes in fixed costs, variable costs and selling prices. Additionally, the assignment explores overhead allocation methods, detailing the calculation of predetermined overhead rates and the application of overhead to specific jobs. The solution includes detailed calculations, interpretations of the results, and a discussion of relevant accounting principles, providing a thorough understanding of the topics covered. The assignment also provides a multi-product break-even analysis, and factors to consider when selecting allocation base.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.