Comprehensive Financial Report: Tesco PLC Analysis, Valuation, WACC

VerifiedAdded on 2023/01/12

|12

|2746

|2

Report

AI Summary

This report provides a financial analysis of Tesco PLC, comparing its performance against competitors using ratio analysis. It evaluates Tesco's company valuation using asset-based, dividend discount, and P/E ratio methods, critically assessing each methodology. The report also examines Tesco's capital structure, calculating the cost of debt, cost of equity, and weighted average cost of capital (WACC), while also addressing the challenges in WACC calculation. The analysis reveals insights into Tesco's profitability, liquidity, and financial risk, highlighting areas for improvement and strategic financial management. Desklib provides more solved assignments for students.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

REPORT..........................................................................................................................................1

2.1 Financial Analysis.....................................................................................................................1

a) Financial analysis of the Tesco plc and comparison with that of the competitors.................1

b) Limitations of the ratio analysis..............................................................................................5

2.2 Company Valuation...................................................................................................................5

a) Calculating the value of Tesco plc using various methods.....................................................5

b) Critical evaluation of the valuation methodologies.................................................................6

2.3 Capital Structure........................................................................................................................7

a) Calculations of the cost of bond of convertible bonds............................................................7

b) Calculation of the Cost of Equity............................................................................................7

c) Calculation of the weighted average cost of capital (WACC) of company............................8

d) Evaluation of the difficulties faced by the enterprise in the calculation of WACC................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

REPORT..........................................................................................................................................1

2.1 Financial Analysis.....................................................................................................................1

a) Financial analysis of the Tesco plc and comparison with that of the competitors.................1

b) Limitations of the ratio analysis..............................................................................................5

2.2 Company Valuation...................................................................................................................5

a) Calculating the value of Tesco plc using various methods.....................................................5

b) Critical evaluation of the valuation methodologies.................................................................6

2.3 Capital Structure........................................................................................................................7

a) Calculations of the cost of bond of convertible bonds............................................................7

b) Calculation of the Cost of Equity............................................................................................7

c) Calculation of the weighted average cost of capital (WACC) of company............................8

d) Evaluation of the difficulties faced by the enterprise in the calculation of WACC................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial management refers to planning, organising, controlling and directing financial

activities like procurement & utilisation of the funds of enterprise. This refers to the application

of the management principles over the financial resources of number of companies. Financial

management is essential for the business enterprise to ensure that all the monetary resources are

utilised effectively (Petrova, 2019). Present report is based on the concepts and principles of

financial management. It will cover analysis of the Tesco plc with that of the competitors for

analysing the financial performance of the business. it will also provide about the company

valuation with various techniques and the various methodologies. Study will also be providing

about the capital structure of the entity in different situations.

REPORT

2.1 Financial Analysis

a) Financial analysis of the Tesco plc and comparison with that of the competitors.

Tesco Competitors

Particulars Formula Tesco Morrison plc Sainsbury

Profitability Ratios

Return on

capital

employed

Net operating

profit/Employed

Capital 4.58% 3.97% 1.97%

Employed

Capital

Total assets –

Current liabilities 28367 9916 12124

Net operating

profit 1300 394 239

Return on

Equity

Net Income /

Shareholder's

Equity 8.16% 5.27% 2.59%

Net Income 1210 244 219

Shareholder's

Equity 14834 4631 8456

1

Financial management refers to planning, organising, controlling and directing financial

activities like procurement & utilisation of the funds of enterprise. This refers to the application

of the management principles over the financial resources of number of companies. Financial

management is essential for the business enterprise to ensure that all the monetary resources are

utilised effectively (Petrova, 2019). Present report is based on the concepts and principles of

financial management. It will cover analysis of the Tesco plc with that of the competitors for

analysing the financial performance of the business. it will also provide about the company

valuation with various techniques and the various methodologies. Study will also be providing

about the capital structure of the entity in different situations.

REPORT

2.1 Financial Analysis

a) Financial analysis of the Tesco plc and comparison with that of the competitors.

Tesco Competitors

Particulars Formula Tesco Morrison plc Sainsbury

Profitability Ratios

Return on

capital

employed

Net operating

profit/Employed

Capital 4.58% 3.97% 1.97%

Employed

Capital

Total assets –

Current liabilities 28367 9916 12124

Net operating

profit 1300 394 239

Return on

Equity

Net Income /

Shareholder's

Equity 8.16% 5.27% 2.59%

Net Income 1210 244 219

Shareholder's

Equity 14834 4631 8456

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profit

margin

Total Sales –

COGS/Total Sales 5.83% 3.42% 6.92%

COS 54141 17128 27000

Sales 57490 17735 29007

Operating

profit margin

Operating Income/

Net Sales 2.26% 2.22% 0.82%

Operating

income 1300 394 239

Revenues 57490 17735 29007

Assets

Turnover Sales / Net assets 387.56% 382.96% 343.03%

Sales 57490 17735 29007

Net assets 14834 4631 8456

Liquidity Ratios

Current assets 12668 1382 7589

Current

liabilities 20680 3295 11417

Inventory 2617 713 1929

Quick assets 10051 669 5660

Current ratio

Current assets /

current liabilities 0.61 0.42 0.66

Quick ratio

Current assets -

(stock + prepaid

expenses) 0.49 0.20 0.50

Efficiency Ratios

Inventory 2617 713 1929

Trade

Receivables 1640 347 661

Trade Payables 9354 3085 4444

Days 365 365 365

COS 54141 17128 27000

2

margin

Total Sales –

COGS/Total Sales 5.83% 3.42% 6.92%

COS 54141 17128 27000

Sales 57490 17735 29007

Operating

profit margin

Operating Income/

Net Sales 2.26% 2.22% 0.82%

Operating

income 1300 394 239

Revenues 57490 17735 29007

Assets

Turnover Sales / Net assets 387.56% 382.96% 343.03%

Sales 57490 17735 29007

Net assets 14834 4631 8456

Liquidity Ratios

Current assets 12668 1382 7589

Current

liabilities 20680 3295 11417

Inventory 2617 713 1929

Quick assets 10051 669 5660

Current ratio

Current assets /

current liabilities 0.61 0.42 0.66

Quick ratio

Current assets -

(stock + prepaid

expenses) 0.49 0.20 0.50

Efficiency Ratios

Inventory 2617 713 1929

Trade

Receivables 1640 347 661

Trade Payables 9354 3085 4444

Days 365 365 365

COS 54141 17128 27000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

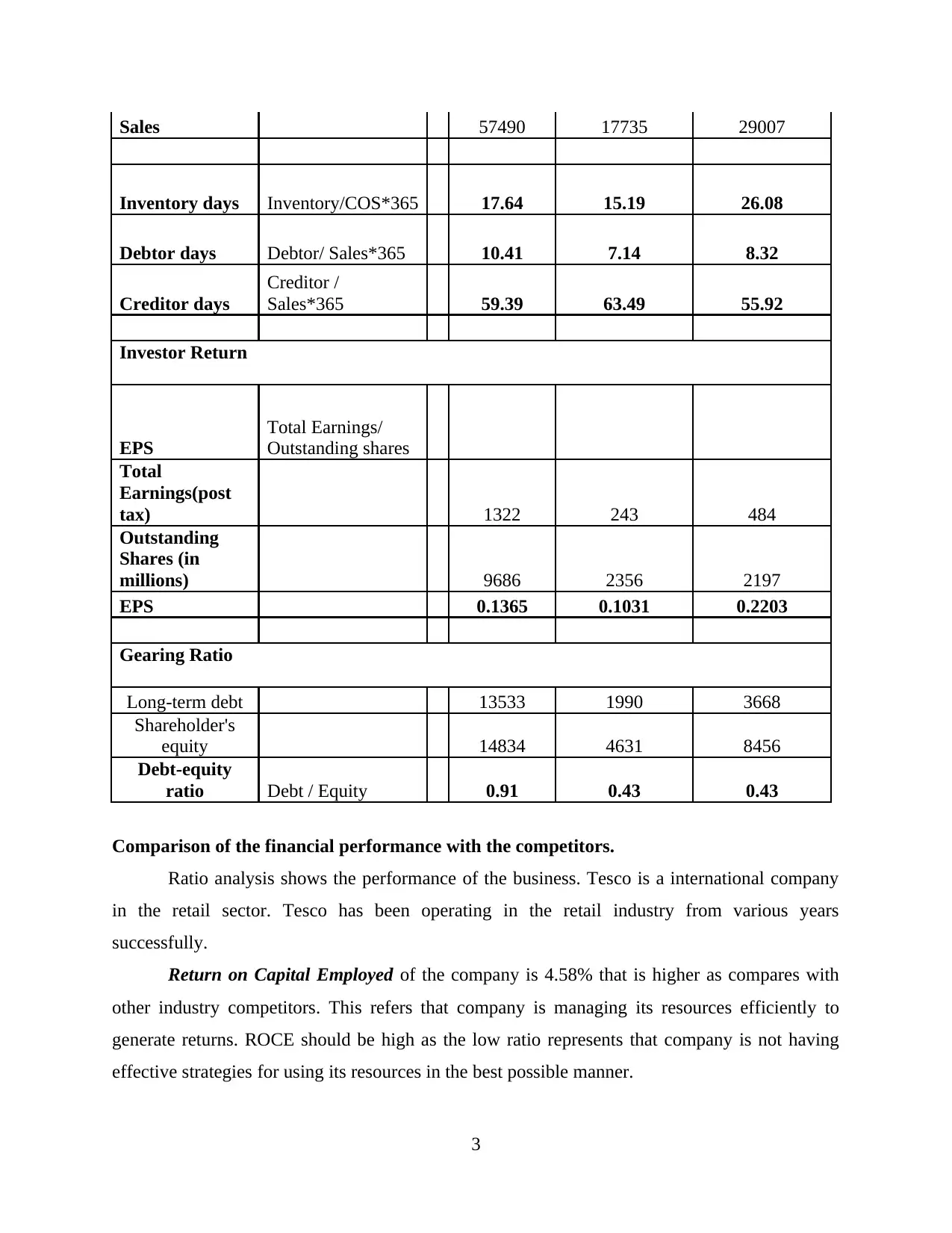

Sales 57490 17735 29007

Inventory days Inventory/COS*365 17.64 15.19 26.08

Debtor days Debtor/ Sales*365 10.41 7.14 8.32

Creditor days

Creditor /

Sales*365 59.39 63.49 55.92

Investor Return

EPS

Total Earnings/

Outstanding shares

Total

Earnings(post

tax) 1322 243 484

Outstanding

Shares (in

millions) 9686 2356 2197

EPS 0.1365 0.1031 0.2203

Gearing Ratio

Long-term debt 13533 1990 3668

Shareholder's

equity 14834 4631 8456

Debt-equity

ratio Debt / Equity 0.91 0.43 0.43

Comparison of the financial performance with the competitors.

Ratio analysis shows the performance of the business. Tesco is a international company

in the retail sector. Tesco has been operating in the retail industry from various years

successfully.

Return on Capital Employed of the company is 4.58% that is higher as compares with

other industry competitors. This refers that company is managing its resources efficiently to

generate returns. ROCE should be high as the low ratio represents that company is not having

effective strategies for using its resources in the best possible manner.

3

Inventory days Inventory/COS*365 17.64 15.19 26.08

Debtor days Debtor/ Sales*365 10.41 7.14 8.32

Creditor days

Creditor /

Sales*365 59.39 63.49 55.92

Investor Return

EPS

Total Earnings/

Outstanding shares

Total

Earnings(post

tax) 1322 243 484

Outstanding

Shares (in

millions) 9686 2356 2197

EPS 0.1365 0.1031 0.2203

Gearing Ratio

Long-term debt 13533 1990 3668

Shareholder's

equity 14834 4631 8456

Debt-equity

ratio Debt / Equity 0.91 0.43 0.43

Comparison of the financial performance with the competitors.

Ratio analysis shows the performance of the business. Tesco is a international company

in the retail sector. Tesco has been operating in the retail industry from various years

successfully.

Return on Capital Employed of the company is 4.58% that is higher as compares with

other industry competitors. This refers that company is managing its resources efficiently to

generate returns. ROCE should be high as the low ratio represents that company is not having

effective strategies for using its resources in the best possible manner.

3

Return on equity represents the return earned by the shareholders over equity

investments. ROE of Tesco is 8.16% where the competitors Morrison & Sainsbury are having

ROE of 5.27% & 2.59% respectively. This could be interpreted that Tesco is generating greater

return as compared with the other companies. Company is required to improve its profits for

increasing the returns.

Gross profit margin of the Tesco is 5.82% and is as per the industry average. Company

should have enough profits left after the cost of sales for carrying out its other operational

activities.

Operating profit margin shows that business is earning sufficient return over its

business. Operating profit of Tesco is 2.26% and of Morrison is 2.22% that is equivalent to the

competitor. Operating profit of the company should be high but due to the slowing economic

growth companies of the retail industry are suffering decline in their profitability.

Current Ratio measures the liquidity position of company. current ratio standard is 2:1

where the ratio of Tesco along with its competitors is very low below 1. This shows that the

companies are not able to meet the obligations from the current assets (Schroeder, Clark and

Cathey, 2019). It could be critical for the company to operate the business smoothly.

Quick ratio of the companies is very low. Liquidity position of the companies shows they

are required to take immediate steps for improving their financial position. Without adequate

liquidity position company may go into liquidations. Retail industry is going through tough and

are therefore required be active and careful about the management decisions.

Efficiency ratios are measured to ensure the management of the company to generate

returns for business. Inventory days of Tesco are 17 days that are adequate as compared with

others. This shows that the inventory is moving fast in the company except in Sainsbury.

Debtors & Creditors days should be management effectively for managing cash cycle of

the business. Debtor days of Tesco is 10days and creditor days 59 days which shows the working

capital cycle of company is higher in comparison with others (Li, 2018).

Debt Equity Ratio is 0.91 of Tesco which is double of other competitors. Financial risk is

high in Tesco as compared with the other competitors. Company are effectively managing its

capital structure keeping it lower.

4

investments. ROE of Tesco is 8.16% where the competitors Morrison & Sainsbury are having

ROE of 5.27% & 2.59% respectively. This could be interpreted that Tesco is generating greater

return as compared with the other companies. Company is required to improve its profits for

increasing the returns.

Gross profit margin of the Tesco is 5.82% and is as per the industry average. Company

should have enough profits left after the cost of sales for carrying out its other operational

activities.

Operating profit margin shows that business is earning sufficient return over its

business. Operating profit of Tesco is 2.26% and of Morrison is 2.22% that is equivalent to the

competitor. Operating profit of the company should be high but due to the slowing economic

growth companies of the retail industry are suffering decline in their profitability.

Current Ratio measures the liquidity position of company. current ratio standard is 2:1

where the ratio of Tesco along with its competitors is very low below 1. This shows that the

companies are not able to meet the obligations from the current assets (Schroeder, Clark and

Cathey, 2019). It could be critical for the company to operate the business smoothly.

Quick ratio of the companies is very low. Liquidity position of the companies shows they

are required to take immediate steps for improving their financial position. Without adequate

liquidity position company may go into liquidations. Retail industry is going through tough and

are therefore required be active and careful about the management decisions.

Efficiency ratios are measured to ensure the management of the company to generate

returns for business. Inventory days of Tesco are 17 days that are adequate as compared with

others. This shows that the inventory is moving fast in the company except in Sainsbury.

Debtors & Creditors days should be management effectively for managing cash cycle of

the business. Debtor days of Tesco is 10days and creditor days 59 days which shows the working

capital cycle of company is higher in comparison with others (Li, 2018).

Debt Equity Ratio is 0.91 of Tesco which is double of other competitors. Financial risk is

high in Tesco as compared with the other competitors. Company are effectively managing its

capital structure keeping it lower.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

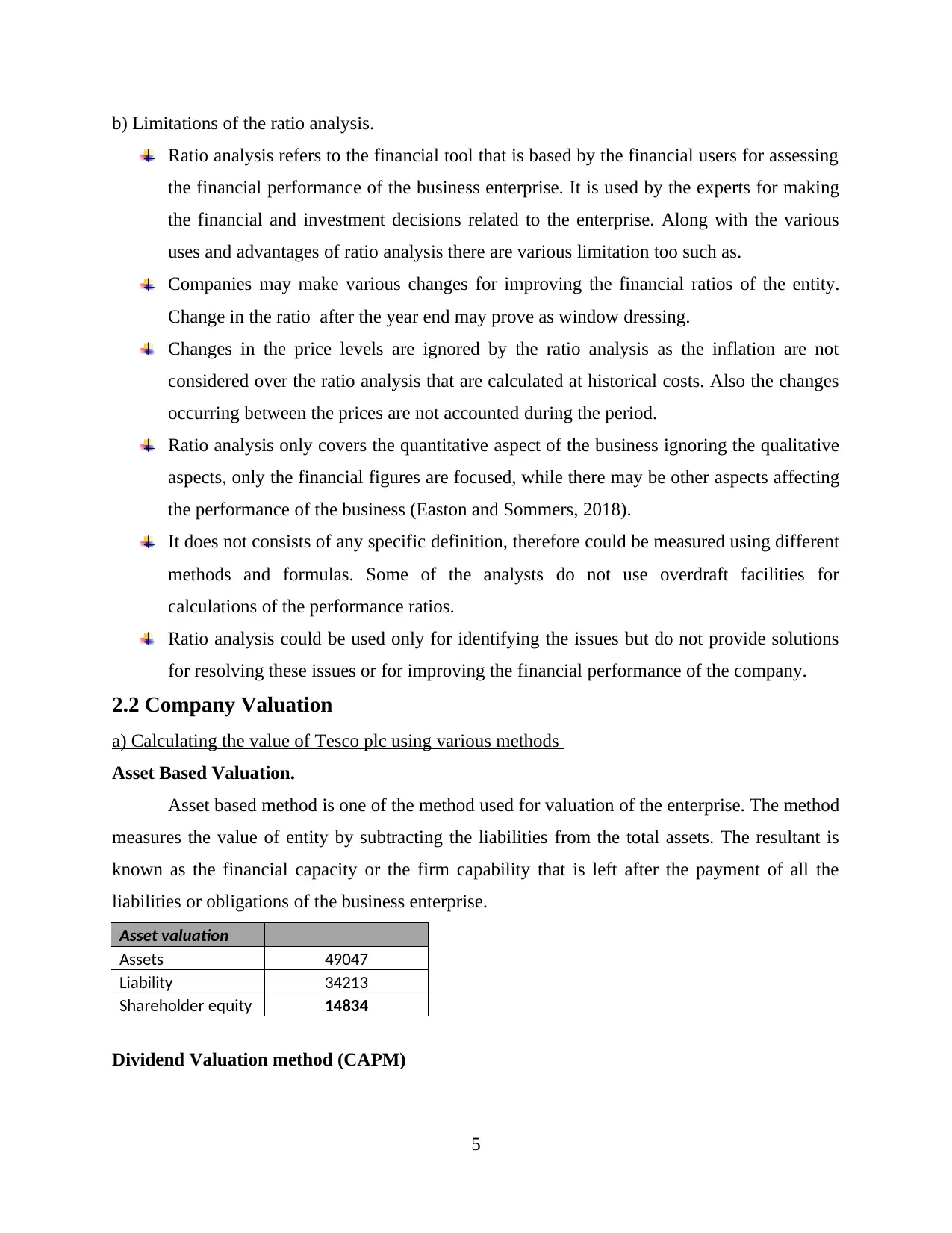

b) Limitations of the ratio analysis.

Ratio analysis refers to the financial tool that is based by the financial users for assessing

the financial performance of the business enterprise. It is used by the experts for making

the financial and investment decisions related to the enterprise. Along with the various

uses and advantages of ratio analysis there are various limitation too such as.

Companies may make various changes for improving the financial ratios of the entity.

Change in the ratio after the year end may prove as window dressing.

Changes in the price levels are ignored by the ratio analysis as the inflation are not

considered over the ratio analysis that are calculated at historical costs. Also the changes

occurring between the prices are not accounted during the period.

Ratio analysis only covers the quantitative aspect of the business ignoring the qualitative

aspects, only the financial figures are focused, while there may be other aspects affecting

the performance of the business (Easton and Sommers, 2018).

It does not consists of any specific definition, therefore could be measured using different

methods and formulas. Some of the analysts do not use overdraft facilities for

calculations of the performance ratios.

Ratio analysis could be used only for identifying the issues but do not provide solutions

for resolving these issues or for improving the financial performance of the company.

2.2 Company Valuation

a) Calculating the value of Tesco plc using various methods

Asset Based Valuation.

Asset based method is one of the method used for valuation of the enterprise. The method

measures the value of entity by subtracting the liabilities from the total assets. The resultant is

known as the financial capacity or the firm capability that is left after the payment of all the

liabilities or obligations of the business enterprise.

Asset valuation

Assets 49047

Liability 34213

Shareholder equity 14834

Dividend Valuation method (CAPM)

5

Ratio analysis refers to the financial tool that is based by the financial users for assessing

the financial performance of the business enterprise. It is used by the experts for making

the financial and investment decisions related to the enterprise. Along with the various

uses and advantages of ratio analysis there are various limitation too such as.

Companies may make various changes for improving the financial ratios of the entity.

Change in the ratio after the year end may prove as window dressing.

Changes in the price levels are ignored by the ratio analysis as the inflation are not

considered over the ratio analysis that are calculated at historical costs. Also the changes

occurring between the prices are not accounted during the period.

Ratio analysis only covers the quantitative aspect of the business ignoring the qualitative

aspects, only the financial figures are focused, while there may be other aspects affecting

the performance of the business (Easton and Sommers, 2018).

It does not consists of any specific definition, therefore could be measured using different

methods and formulas. Some of the analysts do not use overdraft facilities for

calculations of the performance ratios.

Ratio analysis could be used only for identifying the issues but do not provide solutions

for resolving these issues or for improving the financial performance of the company.

2.2 Company Valuation

a) Calculating the value of Tesco plc using various methods

Asset Based Valuation.

Asset based method is one of the method used for valuation of the enterprise. The method

measures the value of entity by subtracting the liabilities from the total assets. The resultant is

known as the financial capacity or the firm capability that is left after the payment of all the

liabilities or obligations of the business enterprise.

Asset valuation

Assets 49047

Liability 34213

Shareholder equity 14834

Dividend Valuation method (CAPM)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

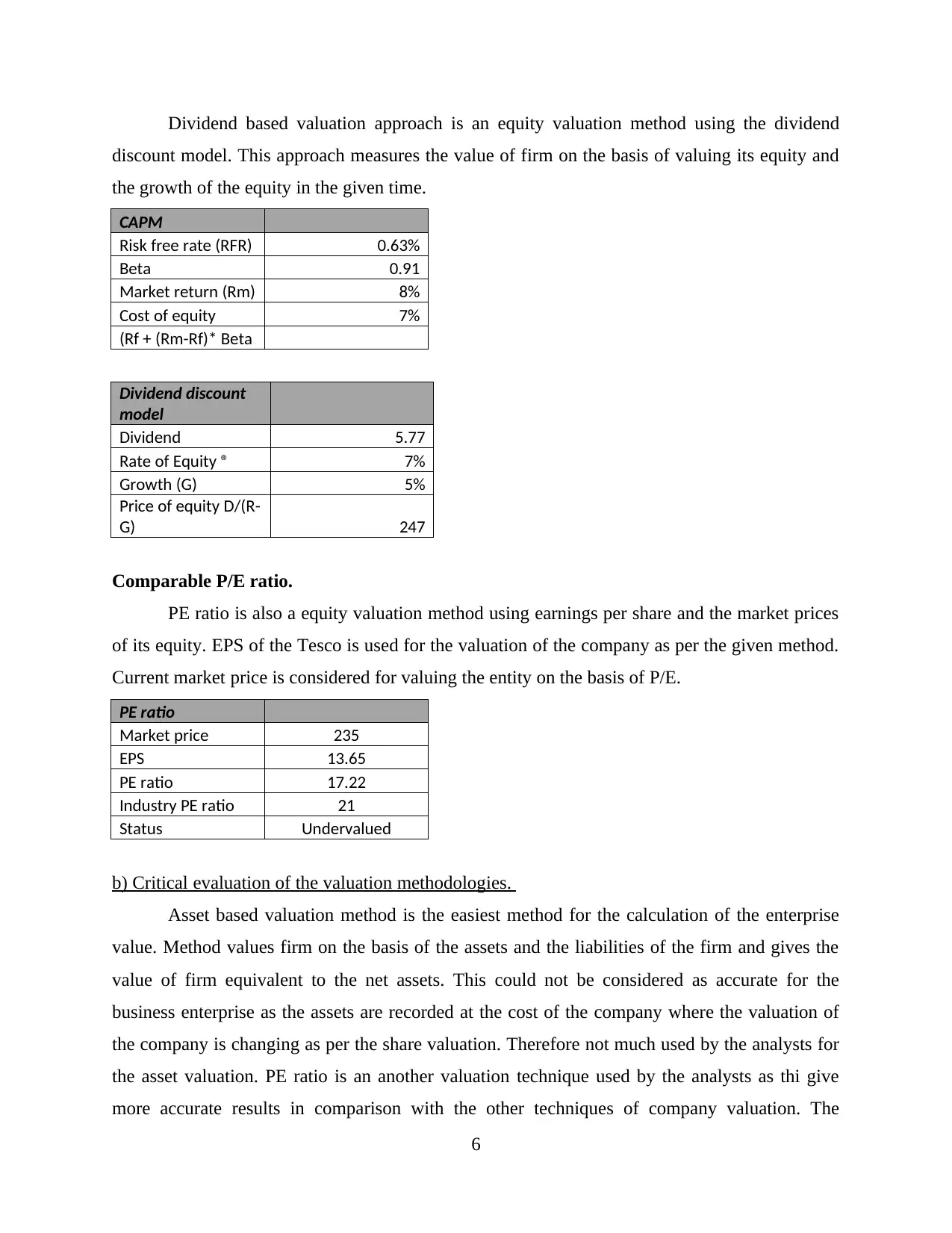

Dividend based valuation approach is an equity valuation method using the dividend

discount model. This approach measures the value of firm on the basis of valuing its equity and

the growth of the equity in the given time.

CAPM

Risk free rate (RFR) 0.63%

Beta 0.91

Market return (Rm) 8%

Cost of equity 7%

(Rf + (Rm-Rf)* Beta

Dividend discount

model

Dividend 5.77

Rate of Equity ® 7%

Growth (G) 5%

Price of equity D/(R-

G) 247

Comparable P/E ratio.

PE ratio is also a equity valuation method using earnings per share and the market prices

of its equity. EPS of the Tesco is used for the valuation of the company as per the given method.

Current market price is considered for valuing the entity on the basis of P/E.

PE ratio

Market price 235

EPS 13.65

PE ratio 17.22

Industry PE ratio 21

Status Undervalued

b) Critical evaluation of the valuation methodologies.

Asset based valuation method is the easiest method for the calculation of the enterprise

value. Method values firm on the basis of the assets and the liabilities of the firm and gives the

value of firm equivalent to the net assets. This could not be considered as accurate for the

business enterprise as the assets are recorded at the cost of the company where the valuation of

the company is changing as per the share valuation. Therefore not much used by the analysts for

the asset valuation. PE ratio is an another valuation technique used by the analysts as thi give

more accurate results in comparison with the other techniques of company valuation. The

6

discount model. This approach measures the value of firm on the basis of valuing its equity and

the growth of the equity in the given time.

CAPM

Risk free rate (RFR) 0.63%

Beta 0.91

Market return (Rm) 8%

Cost of equity 7%

(Rf + (Rm-Rf)* Beta

Dividend discount

model

Dividend 5.77

Rate of Equity ® 7%

Growth (G) 5%

Price of equity D/(R-

G) 247

Comparable P/E ratio.

PE ratio is also a equity valuation method using earnings per share and the market prices

of its equity. EPS of the Tesco is used for the valuation of the company as per the given method.

Current market price is considered for valuing the entity on the basis of P/E.

PE ratio

Market price 235

EPS 13.65

PE ratio 17.22

Industry PE ratio 21

Status Undervalued

b) Critical evaluation of the valuation methodologies.

Asset based valuation method is the easiest method for the calculation of the enterprise

value. Method values firm on the basis of the assets and the liabilities of the firm and gives the

value of firm equivalent to the net assets. This could not be considered as accurate for the

business enterprise as the assets are recorded at the cost of the company where the valuation of

the company is changing as per the share valuation. Therefore not much used by the analysts for

the asset valuation. PE ratio is an another valuation technique used by the analysts as thi give

more accurate results in comparison with the other techniques of company valuation. The

6

method is significant as it is used for assessing whether the shares of the company are under or

over valued. Using the information investors are able to make more accurate and relevant

decisions for the investment of funds (Loughran and McDonald, 2016). When the share prices

of an entity are higher it is assumed to be dearer and cheaper when prices are low. PE ratio is

used for assessing the actual position of the company and not just the valuation on the basis of

assumptions.

There are companies whose share prices are low but are having high PE ratio, this will

give them high returns as compared with the companies with high share prices and lower PE

ratio. It allows investors in making more informed decisions for the business valuation. On the

other there is another technique for the business valuation. This refers to the technique which is

having more of the merit. Many of the analysts uses the method as company is this the perpetual

entity and will be remaining entity. This is base on the concept that the investments will be made

today and the dividend will be received i the coming years on constant basis. This will be used

for valuing g the firm for the enterprise for earning the returns of the enterprise (Maynard,

2017). The method is giving more accurate results as compared with the other techniques. The

method is used for doing more accurate projections of the enterprise valuation. The valuation

methods are used for valuing the firm on the basis with accurate techniques. Valuation of the

business is essential for making the strategies that raises the valuation of the company.

2.3 Capital Structure

a) Calculations of the cost of bond of convertible bonds.

Tax rate 19%

Interest rate 8%

Cost of debt = Kd *(1- Tax rate) 6.48%

b) Calculation of the Cost of Equity

DPS 0.3

MPS 3.2

G 5%

Cost of equity =(DPS/ MPS) + G 14.38%

7

over valued. Using the information investors are able to make more accurate and relevant

decisions for the investment of funds (Loughran and McDonald, 2016). When the share prices

of an entity are higher it is assumed to be dearer and cheaper when prices are low. PE ratio is

used for assessing the actual position of the company and not just the valuation on the basis of

assumptions.

There are companies whose share prices are low but are having high PE ratio, this will

give them high returns as compared with the companies with high share prices and lower PE

ratio. It allows investors in making more informed decisions for the business valuation. On the

other there is another technique for the business valuation. This refers to the technique which is

having more of the merit. Many of the analysts uses the method as company is this the perpetual

entity and will be remaining entity. This is base on the concept that the investments will be made

today and the dividend will be received i the coming years on constant basis. This will be used

for valuing g the firm for the enterprise for earning the returns of the enterprise (Maynard,

2017). The method is giving more accurate results as compared with the other techniques. The

method is used for doing more accurate projections of the enterprise valuation. The valuation

methods are used for valuing the firm on the basis with accurate techniques. Valuation of the

business is essential for making the strategies that raises the valuation of the company.

2.3 Capital Structure

a) Calculations of the cost of bond of convertible bonds.

Tax rate 19%

Interest rate 8%

Cost of debt = Kd *(1- Tax rate) 6.48%

b) Calculation of the Cost of Equity

DPS 0.3

MPS 3.2

G 5%

Cost of equity =(DPS/ MPS) + G 14.38%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

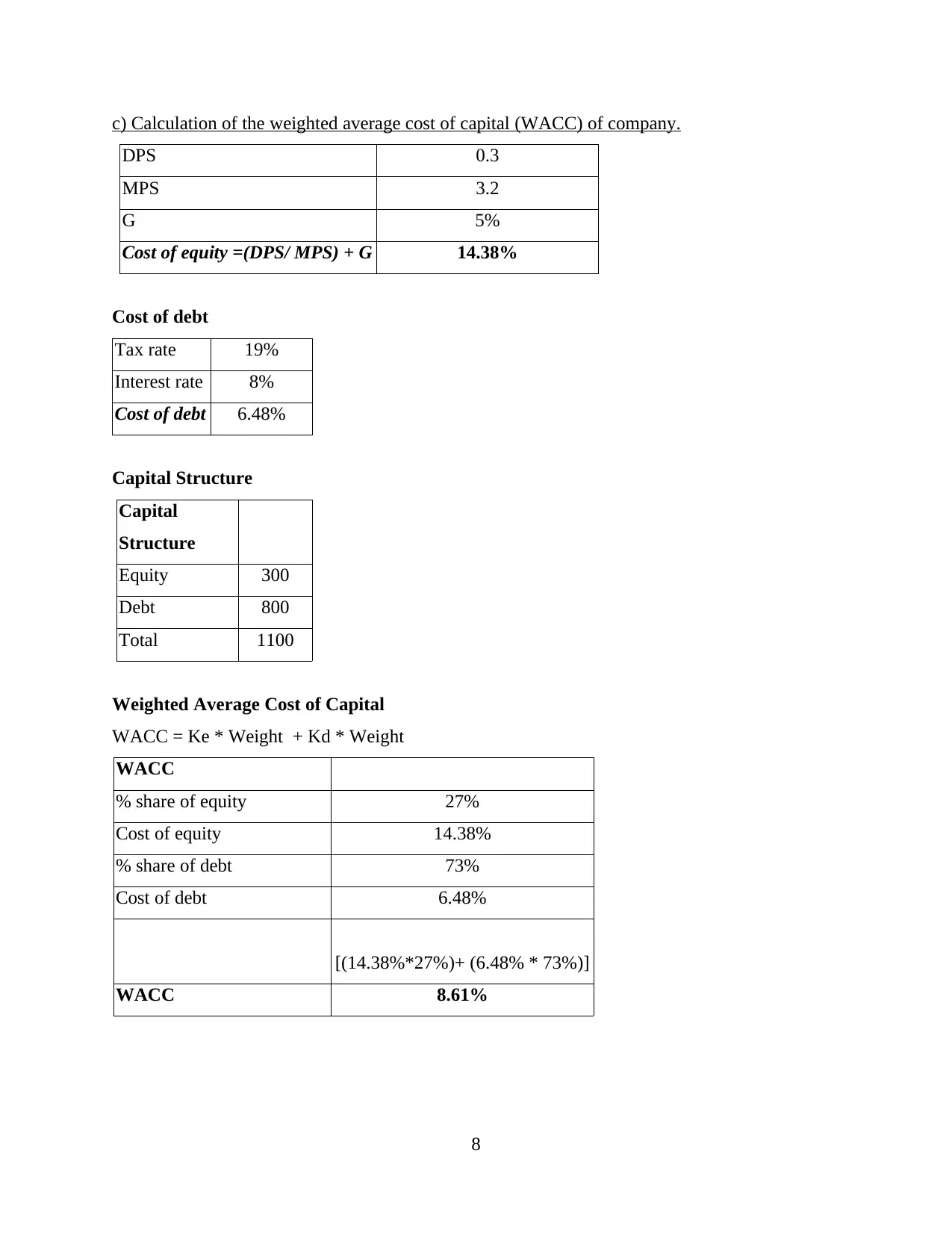

c) Calculation of the weighted average cost of capital (WACC) of company.

DPS 0.3

MPS 3.2

G 5%

Cost of equity =(DPS/ MPS) + G 14.38%

Cost of debt

Tax rate 19%

Interest rate 8%

Cost of debt 6.48%

Capital Structure

Capital

Structure

Equity 300

Debt 800

Total 1100

Weighted Average Cost of Capital

WACC = Ke * Weight + Kd * Weight

WACC

% share of equity 27%

Cost of equity 14.38%

% share of debt 73%

Cost of debt 6.48%

[(14.38%*27%)+ (6.48% * 73%)]

WACC 8.61%

8

DPS 0.3

MPS 3.2

G 5%

Cost of equity =(DPS/ MPS) + G 14.38%

Cost of debt

Tax rate 19%

Interest rate 8%

Cost of debt 6.48%

Capital Structure

Capital

Structure

Equity 300

Debt 800

Total 1100

Weighted Average Cost of Capital

WACC = Ke * Weight + Kd * Weight

WACC

% share of equity 27%

Cost of equity 14.38%

% share of debt 73%

Cost of debt 6.48%

[(14.38%*27%)+ (6.48% * 73%)]

WACC 8.61%

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above measurement it could be interpreted that the WACC of the company is

8.61%. this shows that the cost of capital of the company has been properly managed by the

company. Increasing the cost above this will affect the business.

d) Evaluation of the difficulties faced by the enterprise in the calculation of WACC.

The calculation of WACC is straightforward in theory as compared to theory, because of

the following reason.

There are different methods used while estimating the cost of equity, such that Dividend

discount model and CAPM model. At that time, user aces problem especially related to one of

the variable is an estimate and it is not so easy. WACC model is a forward looking measure and

the entire calculations are based on the expected returns, not in the historical returns. Therefore,

for the equity also, the market value is consider rather than book value.

However, it is critically analyzed that while calculating WACC, there are different term

used such that risk- free bonds that is further used to determine the cost of debts and it is not

always actually matched the terms of the company's debt and as a result, it is consider difficult to

use practically (Siano and Wysocki, 2019). Further, if the company's structure is complex then it

gets more difficult to calculate. WACC because it requires a long calculation and in turn it

consumes lot of time. That is why, using this WACC is consider one of the most simplest

method for theory rather to use practically.

CONCLUSION

From the above study it could be concluded that the financial analysis is very important for

the business enterprise. Ratio analysis is used by the experts for analysing the performance of

business. capital structure of the company should be adequate for keeping the cost of capital of

company to minimum.

9

8.61%. this shows that the cost of capital of the company has been properly managed by the

company. Increasing the cost above this will affect the business.

d) Evaluation of the difficulties faced by the enterprise in the calculation of WACC.

The calculation of WACC is straightforward in theory as compared to theory, because of

the following reason.

There are different methods used while estimating the cost of equity, such that Dividend

discount model and CAPM model. At that time, user aces problem especially related to one of

the variable is an estimate and it is not so easy. WACC model is a forward looking measure and

the entire calculations are based on the expected returns, not in the historical returns. Therefore,

for the equity also, the market value is consider rather than book value.

However, it is critically analyzed that while calculating WACC, there are different term

used such that risk- free bonds that is further used to determine the cost of debts and it is not

always actually matched the terms of the company's debt and as a result, it is consider difficult to

use practically (Siano and Wysocki, 2019). Further, if the company's structure is complex then it

gets more difficult to calculate. WACC because it requires a long calculation and in turn it

consumes lot of time. That is why, using this WACC is consider one of the most simplest

method for theory rather to use practically.

CONCLUSION

From the above study it could be concluded that the financial analysis is very important for

the business enterprise. Ratio analysis is used by the experts for analysing the performance of

business. capital structure of the company should be adequate for keeping the cost of capital of

company to minimum.

9

REFERENCES

Books and Journals

Petrova, P., 2019. Accounting Analysis.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research.54(4). pp.1187-1230.

Easton, M. and Sommers, Z., 2018. Financial Statement Analysis & Valuation, 5e.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Siano, F. and Wysocki, P., 2019. Transfer Learning and Textual Analysis of Accounting

Disclosures: Applying Big Data Methods to Small (er) Data Sets.

Li, W.S., 2018. Competitor Analysis and Accounting Model: Accounting Model. In Strategic

Management Accounting (pp. 125-141). Springer, Singapore.

Online

Tesco Plc. 2019. [Online]. Available through :

<https://www.londonstockexchange.com/exchange/prices/stocks/summary/fundamentals.html?

fourWayKey=GB0008847096GBGBXSET1>.

10

Books and Journals

Petrova, P., 2019. Accounting Analysis.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research.54(4). pp.1187-1230.

Easton, M. and Sommers, Z., 2018. Financial Statement Analysis & Valuation, 5e.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Siano, F. and Wysocki, P., 2019. Transfer Learning and Textual Analysis of Accounting

Disclosures: Applying Big Data Methods to Small (er) Data Sets.

Li, W.S., 2018. Competitor Analysis and Accounting Model: Accounting Model. In Strategic

Management Accounting (pp. 125-141). Springer, Singapore.

Online

Tesco Plc. 2019. [Online]. Available through :

<https://www.londonstockexchange.com/exchange/prices/stocks/summary/fundamentals.html?

fourWayKey=GB0008847096GBGBXSET1>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.