Risk Return Relationship Analysis in JB HiFi

VerifiedAdded on 2021/04/16

|9

|1836

|68

AI Summary

The assignment evaluates the risk return relationship of JB HiFi over a six-month period. The analysis indicates that JB HiFi has a relatively high beta, suggesting that its stock price is highly correlated with market returns. This means that investors can use JB HiFi to reduce risk and improve return generation capacity in their portfolios. However, during economic crises, the risk identification of all stocks may lose friction, leading to losses in value.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Authors Note:

Finance

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE

1

Table of Contents

Task for Case Study 1:...............................................................................................................2

a.1) Historical monthly rates of return for the market index:....................................................2

a.2.i) Historical average rate of return and standard deviation of returns for JB HiFi (JBH):...2

a.2.ii) Historical average rate of return and standard deviation of returns for reference

company:....................................................................................................................................3

a.2.iii) Historical average rate of return and standard deviation of returns for the market

index:..........................................................................................................................................3

b) Calculating portfolio historical average rate of return and standard deviation:....................4

c) Calculating CAPM for JB HiFi (JBH) and reference company:...........................................4

d) Calculating Expected portfolio return and Beta:...................................................................5

e) Discussing the risk and return measure of JB HiFi (JBH):....................................................6

Reference and Bibliography:......................................................................................................8

1

Table of Contents

Task for Case Study 1:...............................................................................................................2

a.1) Historical monthly rates of return for the market index:....................................................2

a.2.i) Historical average rate of return and standard deviation of returns for JB HiFi (JBH):...2

a.2.ii) Historical average rate of return and standard deviation of returns for reference

company:....................................................................................................................................3

a.2.iii) Historical average rate of return and standard deviation of returns for the market

index:..........................................................................................................................................3

b) Calculating portfolio historical average rate of return and standard deviation:....................4

c) Calculating CAPM for JB HiFi (JBH) and reference company:...........................................4

d) Calculating Expected portfolio return and Beta:...................................................................5

e) Discussing the risk and return measure of JB HiFi (JBH):....................................................6

Reference and Bibliography:......................................................................................................8

FINANCE

2

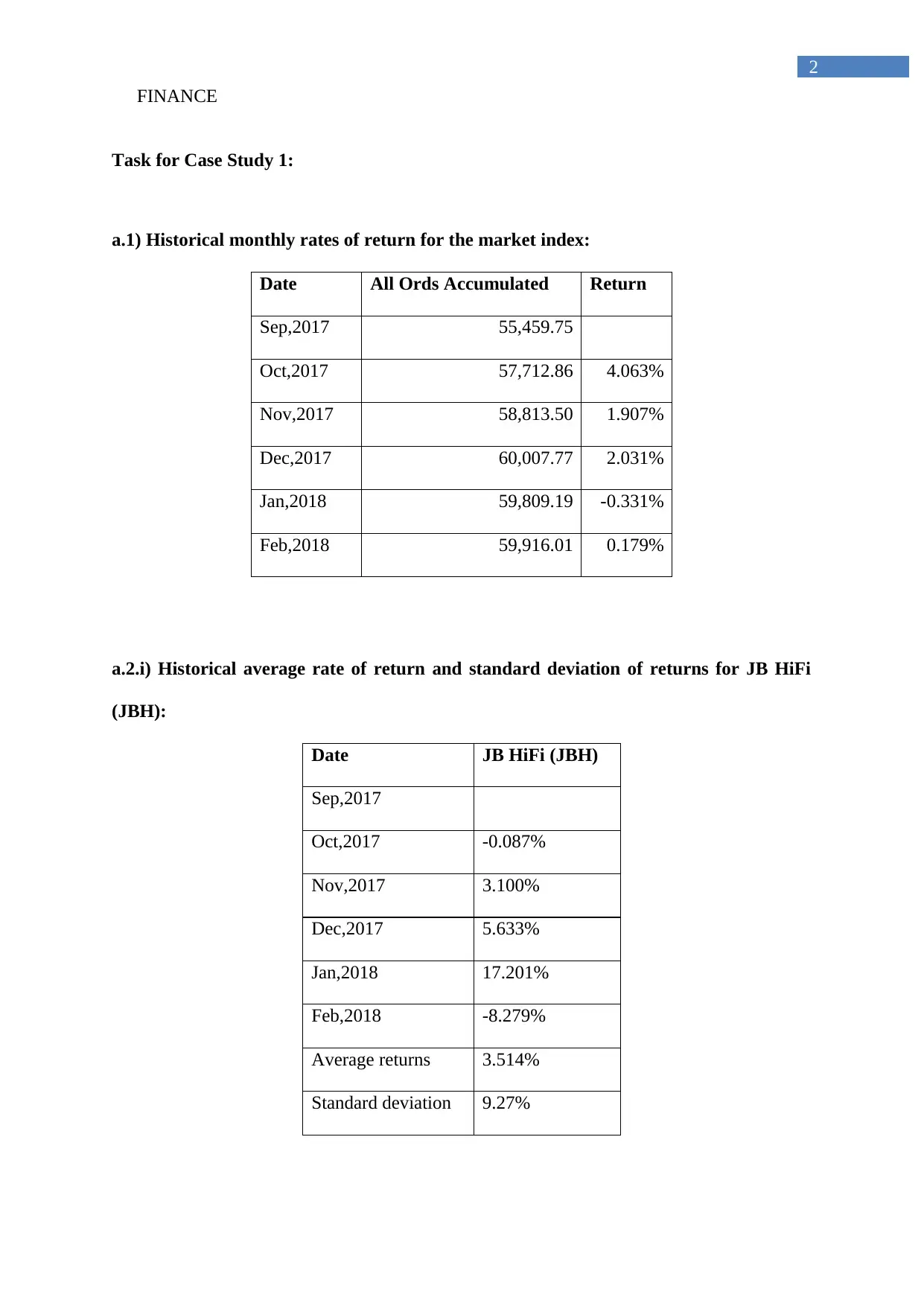

Task for Case Study 1:

a.1) Historical monthly rates of return for the market index:

Date All Ords Accumulated Return

Sep,2017 55,459.75

Oct,2017 57,712.86 4.063%

Nov,2017 58,813.50 1.907%

Dec,2017 60,007.77 2.031%

Jan,2018 59,809.19 -0.331%

Feb,2018 59,916.01 0.179%

a.2.i) Historical average rate of return and standard deviation of returns for JB HiFi

(JBH):

Date JB HiFi (JBH)

Sep,2017

Oct,2017 -0.087%

Nov,2017 3.100%

Dec,2017 5.633%

Jan,2018 17.201%

Feb,2018 -8.279%

Average returns 3.514%

Standard deviation 9.27%

2

Task for Case Study 1:

a.1) Historical monthly rates of return for the market index:

Date All Ords Accumulated Return

Sep,2017 55,459.75

Oct,2017 57,712.86 4.063%

Nov,2017 58,813.50 1.907%

Dec,2017 60,007.77 2.031%

Jan,2018 59,809.19 -0.331%

Feb,2018 59,916.01 0.179%

a.2.i) Historical average rate of return and standard deviation of returns for JB HiFi

(JBH):

Date JB HiFi (JBH)

Sep,2017

Oct,2017 -0.087%

Nov,2017 3.100%

Dec,2017 5.633%

Jan,2018 17.201%

Feb,2018 -8.279%

Average returns 3.514%

Standard deviation 9.27%

FINANCE

3

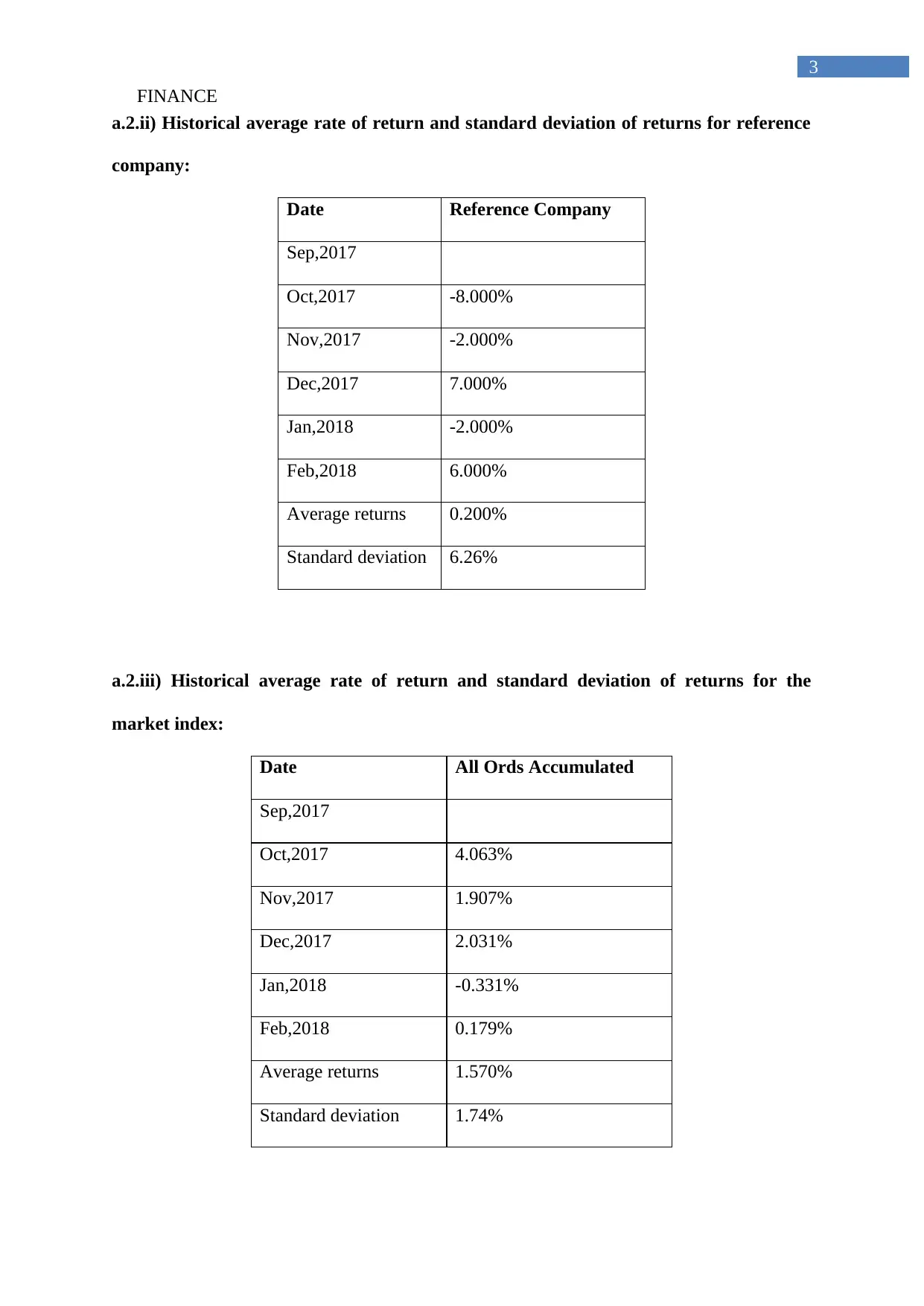

a.2.ii) Historical average rate of return and standard deviation of returns for reference

company:

Date Reference Company

Sep,2017

Oct,2017 -8.000%

Nov,2017 -2.000%

Dec,2017 7.000%

Jan,2018 -2.000%

Feb,2018 6.000%

Average returns 0.200%

Standard deviation 6.26%

a.2.iii) Historical average rate of return and standard deviation of returns for the

market index:

Date All Ords Accumulated

Sep,2017

Oct,2017 4.063%

Nov,2017 1.907%

Dec,2017 2.031%

Jan,2018 -0.331%

Feb,2018 0.179%

Average returns 1.570%

Standard deviation 1.74%

3

a.2.ii) Historical average rate of return and standard deviation of returns for reference

company:

Date Reference Company

Sep,2017

Oct,2017 -8.000%

Nov,2017 -2.000%

Dec,2017 7.000%

Jan,2018 -2.000%

Feb,2018 6.000%

Average returns 0.200%

Standard deviation 6.26%

a.2.iii) Historical average rate of return and standard deviation of returns for the

market index:

Date All Ords Accumulated

Sep,2017

Oct,2017 4.063%

Nov,2017 1.907%

Dec,2017 2.031%

Jan,2018 -0.331%

Feb,2018 0.179%

Average returns 1.570%

Standard deviation 1.74%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE

4

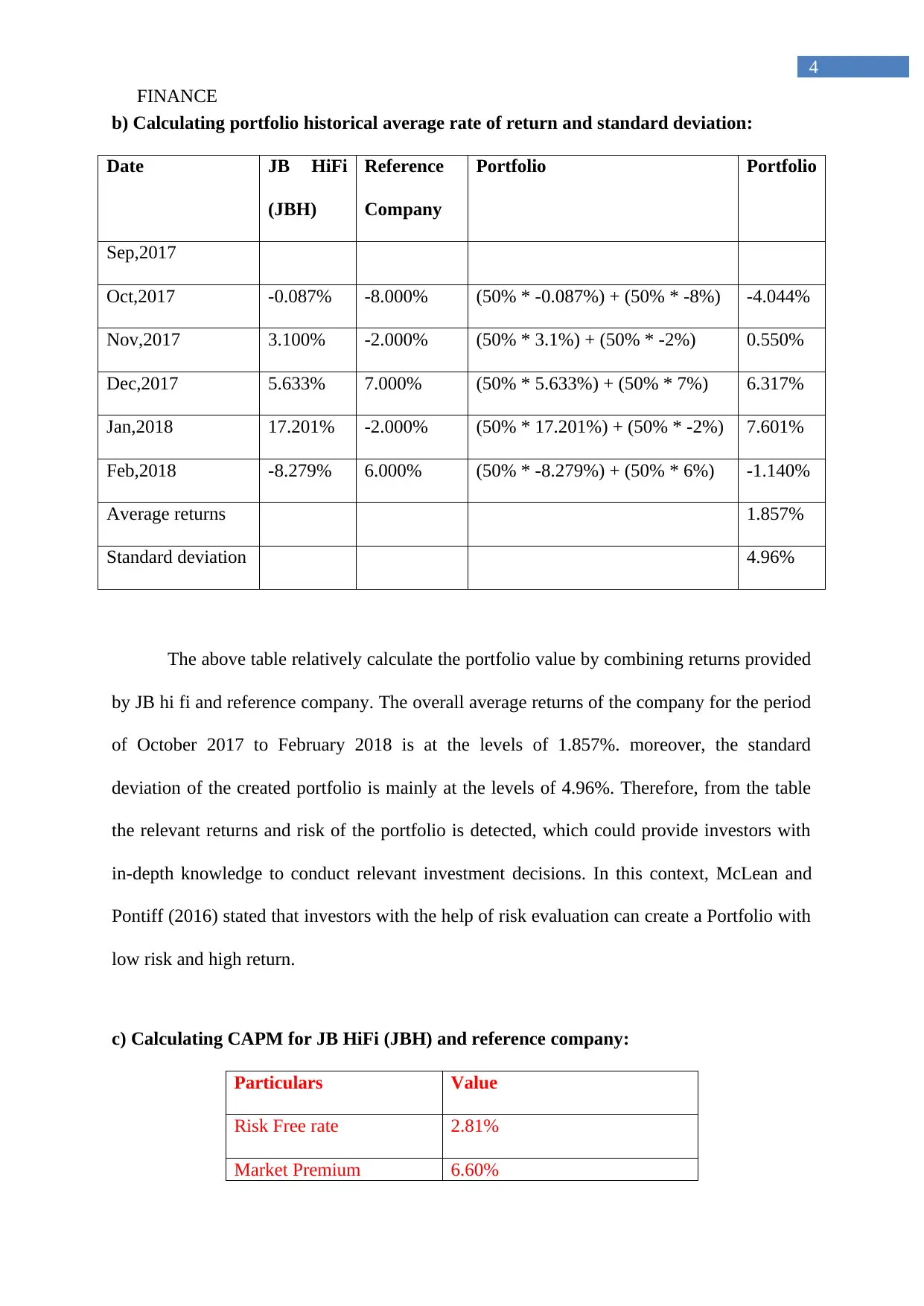

b) Calculating portfolio historical average rate of return and standard deviation:

Date JB HiFi

(JBH)

Reference

Company

Portfolio Portfolio

Sep,2017

Oct,2017 -0.087% -8.000% (50% * -0.087%) + (50% * -8%) -4.044%

Nov,2017 3.100% -2.000% (50% * 3.1%) + (50% * -2%) 0.550%

Dec,2017 5.633% 7.000% (50% * 5.633%) + (50% * 7%) 6.317%

Jan,2018 17.201% -2.000% (50% * 17.201%) + (50% * -2%) 7.601%

Feb,2018 -8.279% 6.000% (50% * -8.279%) + (50% * 6%) -1.140%

Average returns 1.857%

Standard deviation 4.96%

The above table relatively calculate the portfolio value by combining returns provided

by JB hi fi and reference company. The overall average returns of the company for the period

of October 2017 to February 2018 is at the levels of 1.857%. moreover, the standard

deviation of the created portfolio is mainly at the levels of 4.96%. Therefore, from the table

the relevant returns and risk of the portfolio is detected, which could provide investors with

in-depth knowledge to conduct relevant investment decisions. In this context, McLean and

Pontiff (2016) stated that investors with the help of risk evaluation can create a Portfolio with

low risk and high return.

c) Calculating CAPM for JB HiFi (JBH) and reference company:

Particulars Value

Risk Free rate 2.81%

Market Premium 6.60%

4

b) Calculating portfolio historical average rate of return and standard deviation:

Date JB HiFi

(JBH)

Reference

Company

Portfolio Portfolio

Sep,2017

Oct,2017 -0.087% -8.000% (50% * -0.087%) + (50% * -8%) -4.044%

Nov,2017 3.100% -2.000% (50% * 3.1%) + (50% * -2%) 0.550%

Dec,2017 5.633% 7.000% (50% * 5.633%) + (50% * 7%) 6.317%

Jan,2018 17.201% -2.000% (50% * 17.201%) + (50% * -2%) 7.601%

Feb,2018 -8.279% 6.000% (50% * -8.279%) + (50% * 6%) -1.140%

Average returns 1.857%

Standard deviation 4.96%

The above table relatively calculate the portfolio value by combining returns provided

by JB hi fi and reference company. The overall average returns of the company for the period

of October 2017 to February 2018 is at the levels of 1.857%. moreover, the standard

deviation of the created portfolio is mainly at the levels of 4.96%. Therefore, from the table

the relevant returns and risk of the portfolio is detected, which could provide investors with

in-depth knowledge to conduct relevant investment decisions. In this context, McLean and

Pontiff (2016) stated that investors with the help of risk evaluation can create a Portfolio with

low risk and high return.

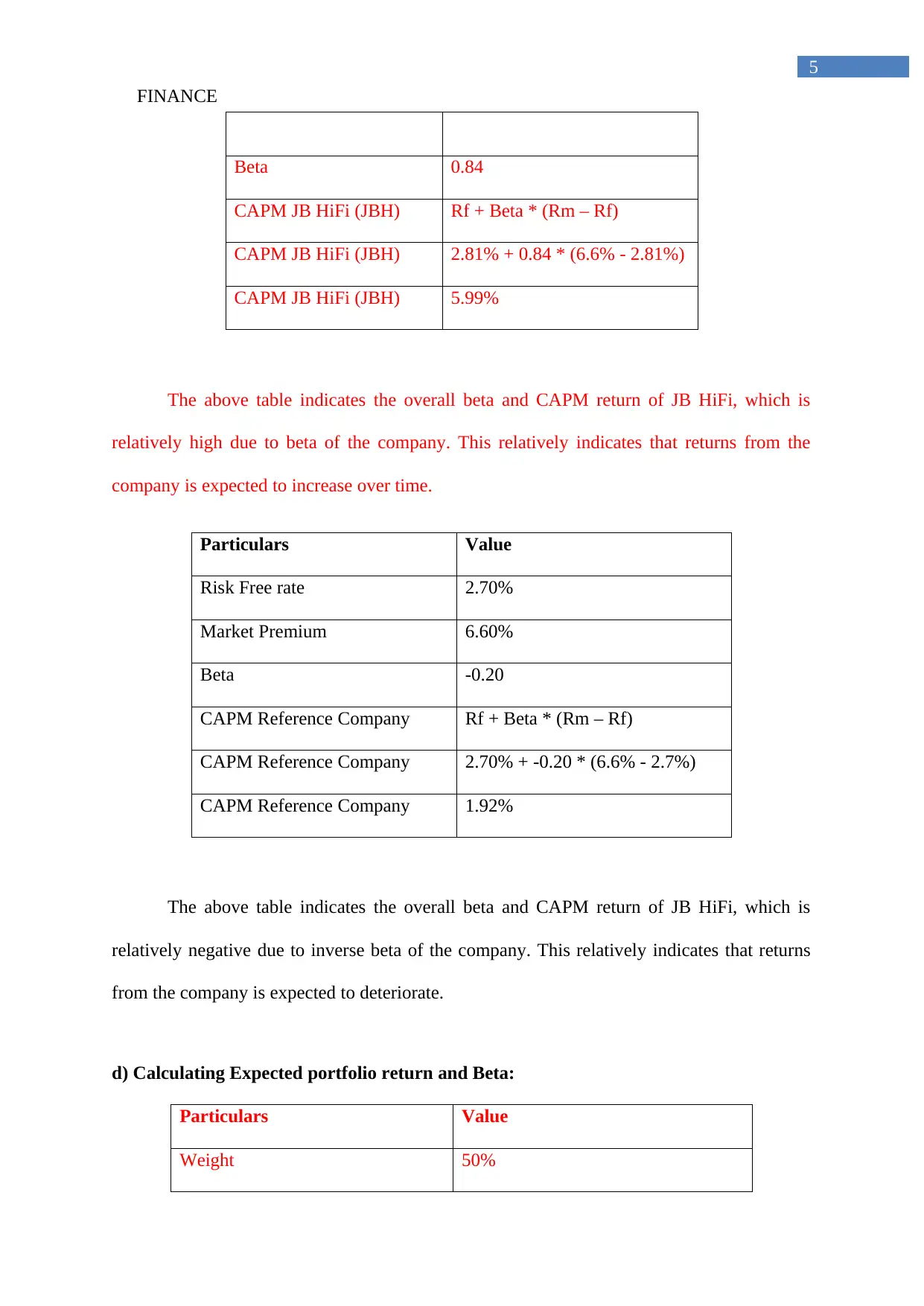

c) Calculating CAPM for JB HiFi (JBH) and reference company:

Particulars Value

Risk Free rate 2.81%

Market Premium 6.60%

FINANCE

5

Beta 0.84

CAPM JB HiFi (JBH) Rf + Beta * (Rm – Rf)

CAPM JB HiFi (JBH) 2.81% + 0.84 * (6.6% - 2.81%)

CAPM JB HiFi (JBH) 5.99%

The above table indicates the overall beta and CAPM return of JB HiFi, which is

relatively high due to beta of the company. This relatively indicates that returns from the

company is expected to increase over time.

Particulars Value

Risk Free rate 2.70%

Market Premium 6.60%

Beta -0.20

CAPM Reference Company Rf + Beta * (Rm – Rf)

CAPM Reference Company 2.70% + -0.20 * (6.6% - 2.7%)

CAPM Reference Company 1.92%

The above table indicates the overall beta and CAPM return of JB HiFi, which is

relatively negative due to inverse beta of the company. This relatively indicates that returns

from the company is expected to deteriorate.

d) Calculating Expected portfolio return and Beta:

Particulars Value

Weight 50%

5

Beta 0.84

CAPM JB HiFi (JBH) Rf + Beta * (Rm – Rf)

CAPM JB HiFi (JBH) 2.81% + 0.84 * (6.6% - 2.81%)

CAPM JB HiFi (JBH) 5.99%

The above table indicates the overall beta and CAPM return of JB HiFi, which is

relatively high due to beta of the company. This relatively indicates that returns from the

company is expected to increase over time.

Particulars Value

Risk Free rate 2.70%

Market Premium 6.60%

Beta -0.20

CAPM Reference Company Rf + Beta * (Rm – Rf)

CAPM Reference Company 2.70% + -0.20 * (6.6% - 2.7%)

CAPM Reference Company 1.92%

The above table indicates the overall beta and CAPM return of JB HiFi, which is

relatively negative due to inverse beta of the company. This relatively indicates that returns

from the company is expected to deteriorate.

d) Calculating Expected portfolio return and Beta:

Particulars Value

Weight 50%

FINANCE

6

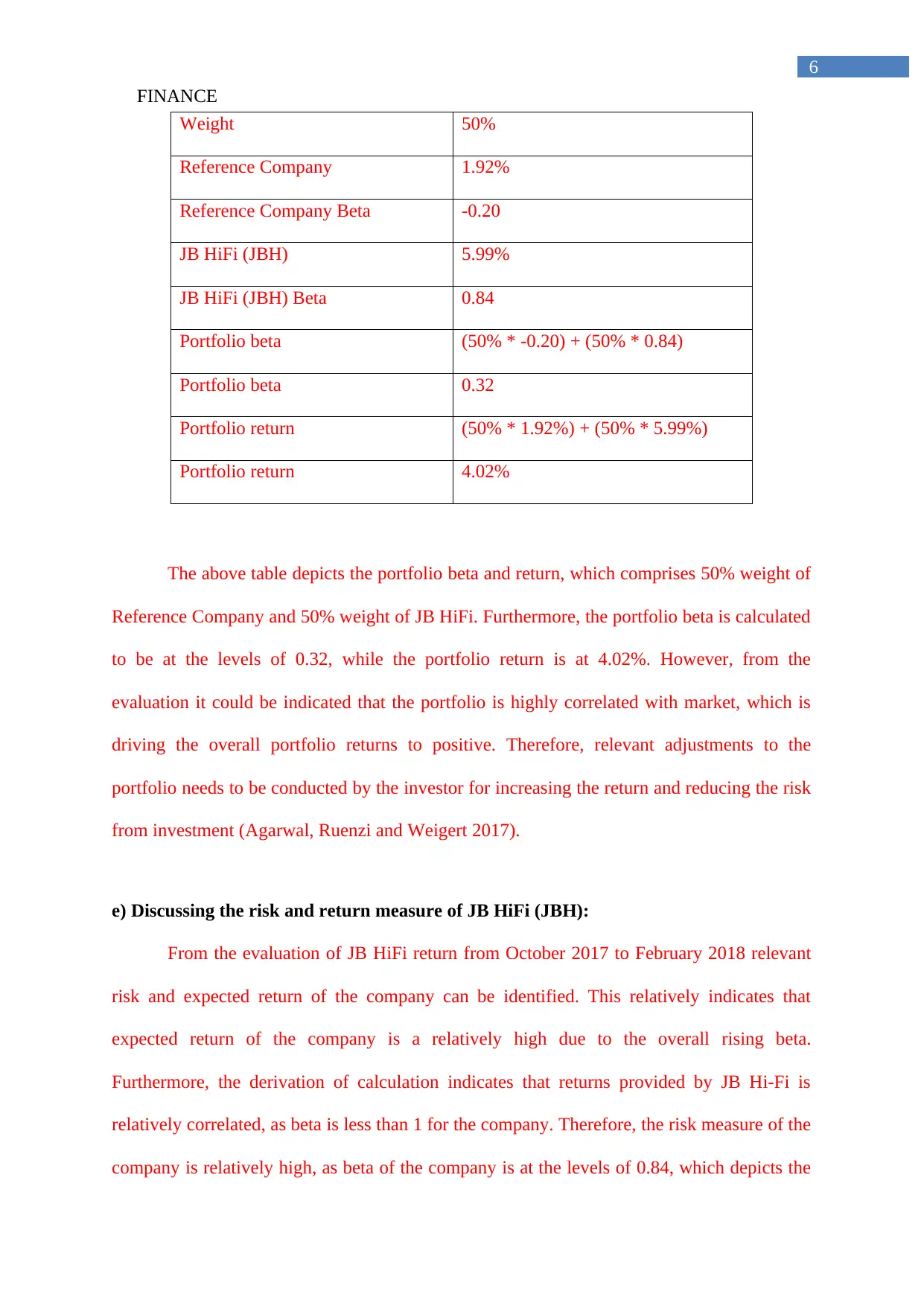

Weight 50%

Reference Company 1.92%

Reference Company Beta -0.20

JB HiFi (JBH) 5.99%

JB HiFi (JBH) Beta 0.84

Portfolio beta (50% * -0.20) + (50% * 0.84)

Portfolio beta 0.32

Portfolio return (50% * 1.92%) + (50% * 5.99%)

Portfolio return 4.02%

The above table depicts the portfolio beta and return, which comprises 50% weight of

Reference Company and 50% weight of JB HiFi. Furthermore, the portfolio beta is calculated

to be at the levels of 0.32, while the portfolio return is at 4.02%. However, from the

evaluation it could be indicated that the portfolio is highly correlated with market, which is

driving the overall portfolio returns to positive. Therefore, relevant adjustments to the

portfolio needs to be conducted by the investor for increasing the return and reducing the risk

from investment (Agarwal, Ruenzi and Weigert 2017).

e) Discussing the risk and return measure of JB HiFi (JBH):

From the evaluation of JB HiFi return from October 2017 to February 2018 relevant

risk and expected return of the company can be identified. This relatively indicates that

expected return of the company is a relatively high due to the overall rising beta.

Furthermore, the derivation of calculation indicates that returns provided by JB Hi-Fi is

relatively correlated, as beta is less than 1 for the company. Therefore, the risk measure of the

company is relatively high, as beta of the company is at the levels of 0.84, which depicts the

6

Weight 50%

Reference Company 1.92%

Reference Company Beta -0.20

JB HiFi (JBH) 5.99%

JB HiFi (JBH) Beta 0.84

Portfolio beta (50% * -0.20) + (50% * 0.84)

Portfolio beta 0.32

Portfolio return (50% * 1.92%) + (50% * 5.99%)

Portfolio return 4.02%

The above table depicts the portfolio beta and return, which comprises 50% weight of

Reference Company and 50% weight of JB HiFi. Furthermore, the portfolio beta is calculated

to be at the levels of 0.32, while the portfolio return is at 4.02%. However, from the

evaluation it could be indicated that the portfolio is highly correlated with market, which is

driving the overall portfolio returns to positive. Therefore, relevant adjustments to the

portfolio needs to be conducted by the investor for increasing the return and reducing the risk

from investment (Agarwal, Ruenzi and Weigert 2017).

e) Discussing the risk and return measure of JB HiFi (JBH):

From the evaluation of JB HiFi return from October 2017 to February 2018 relevant

risk and expected return of the company can be identified. This relatively indicates that

expected return of the company is a relatively high due to the overall rising beta.

Furthermore, the derivation of calculation indicates that returns provided by JB Hi-Fi is

relatively correlated, as beta is less than 1 for the company. Therefore, the risk measure of the

company is relatively high, as beta of the company is at the levels of 0.84, which depicts the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

7

high risk from investment, as it is close to 1. The beta is relatively calculated from the returns

provided by the company and market, which helps in identifying the risk involved in

investment. The overall returns of JB HiFi is detected from the calculation of CAPM, which

evaluates risk free rate, market return, and beta of the company. This evaluation mainly stated

a total return of 5.99%, which is provided by JB HiFi. This positive relationship between JB

HiFi returns and market returns can be used by investors to increase their portfolio returns

against adverse market volatility. In this context, Zhang, Liu and Xu (2014) mentioned that

use of expected return and risk allows investors to formulate portfolios, which are risk averse

and could provide higher returns from investment.

The overall risk attributes of JB HiFi is detected from the valuation of six months,

which is relatively short duration for identifying the actual attribute of the stock. The

increment in months need to be conducted for the calculation of beta and returns. The

calculations indicate that during short period beat of the company is relatively high, which is

indicating a high return, as depicted by CAPM. The high correlation between the market

return and JB HiFi return indicates that any increment in capital market would raise share

price of the company. Furthermore, JB HiFi can be used in portfolio to reduce its risk and

improve return generation capacity of the investors. On the other hand, Bollerslev, Todorov

and Xu (2015) argued that risk identification loses its friction if economic crisis is in motion,

where all the stocks lose their value due to highly volatile capital market.

7

high risk from investment, as it is close to 1. The beta is relatively calculated from the returns

provided by the company and market, which helps in identifying the risk involved in

investment. The overall returns of JB HiFi is detected from the calculation of CAPM, which

evaluates risk free rate, market return, and beta of the company. This evaluation mainly stated

a total return of 5.99%, which is provided by JB HiFi. This positive relationship between JB

HiFi returns and market returns can be used by investors to increase their portfolio returns

against adverse market volatility. In this context, Zhang, Liu and Xu (2014) mentioned that

use of expected return and risk allows investors to formulate portfolios, which are risk averse

and could provide higher returns from investment.

The overall risk attributes of JB HiFi is detected from the valuation of six months,

which is relatively short duration for identifying the actual attribute of the stock. The

increment in months need to be conducted for the calculation of beta and returns. The

calculations indicate that during short period beat of the company is relatively high, which is

indicating a high return, as depicted by CAPM. The high correlation between the market

return and JB HiFi return indicates that any increment in capital market would raise share

price of the company. Furthermore, JB HiFi can be used in portfolio to reduce its risk and

improve return generation capacity of the investors. On the other hand, Bollerslev, Todorov

and Xu (2015) argued that risk identification loses its friction if economic crisis is in motion,

where all the stocks lose their value due to highly volatile capital market.

FINANCE

8

Reference and Bibliography:

Agarwal, V., Ruenzi, S. and Weigert, F., 2017. Tail risk in hedge funds: A unique view from

portfolio holdings. Journal of Financial Economics, 125(3), pp.610-636.

Aliu, F., Pavelková, D. and Dehning, B., 2017. Portfolio risk-return analysis: The case of the

automotive industry in the Czech Republic.

Beshears, J., Choi, J.J., Laibson, D. and Madrian, B.C., 2016. Does Aggregated Returns

Disclosure Increase Portfolio Risk Taking?. The review of financial studies, 30(6), pp.1971-

2005.

Bollerslev, T., Todorov, V. and Xu, L., 2015. Tail risk premia and return

predictability. Journal of Financial Economics, 118(1), pp.113-134.

Bruni, R., Cesarone, F., Scozzari, A. and Tardella, F., 2015. A linear risk-return model for

enhanced indexation in portfolio optimization. OR spectrum, 37(3), pp.735-759.

Hoffmann, A.O. and Post, T., 2015. How return and risk experiences shape investor beliefs

and preferences. Accounting & Finance.

Hung, K., Yang, C.W., Zhao, Y. and Lee, K.H., 2018. Risk Return Relationship in the

Portfolio Selection Models. Theoretical Economics Letters, 8(03), p.358.

McLean, R.D. and Pontiff, J., 2016. Does academic research destroy stock return

predictability?. The Journal of Finance, 71(1), pp.5-32.

Nguyen, T.T., Gordon-Brown, L., Khosravi, A., Creighton, D. and Nahavandi, S., 2015.

Fuzzy portfolio allocation models through a new risk measure and fuzzy sharpe ratio. IEEE

Transactions on Fuzzy Systems, 23(3), pp.656-676.

8

Reference and Bibliography:

Agarwal, V., Ruenzi, S. and Weigert, F., 2017. Tail risk in hedge funds: A unique view from

portfolio holdings. Journal of Financial Economics, 125(3), pp.610-636.

Aliu, F., Pavelková, D. and Dehning, B., 2017. Portfolio risk-return analysis: The case of the

automotive industry in the Czech Republic.

Beshears, J., Choi, J.J., Laibson, D. and Madrian, B.C., 2016. Does Aggregated Returns

Disclosure Increase Portfolio Risk Taking?. The review of financial studies, 30(6), pp.1971-

2005.

Bollerslev, T., Todorov, V. and Xu, L., 2015. Tail risk premia and return

predictability. Journal of Financial Economics, 118(1), pp.113-134.

Bruni, R., Cesarone, F., Scozzari, A. and Tardella, F., 2015. A linear risk-return model for

enhanced indexation in portfolio optimization. OR spectrum, 37(3), pp.735-759.

Hoffmann, A.O. and Post, T., 2015. How return and risk experiences shape investor beliefs

and preferences. Accounting & Finance.

Hung, K., Yang, C.W., Zhao, Y. and Lee, K.H., 2018. Risk Return Relationship in the

Portfolio Selection Models. Theoretical Economics Letters, 8(03), p.358.

McLean, R.D. and Pontiff, J., 2016. Does academic research destroy stock return

predictability?. The Journal of Finance, 71(1), pp.5-32.

Nguyen, T.T., Gordon-Brown, L., Khosravi, A., Creighton, D. and Nahavandi, S., 2015.

Fuzzy portfolio allocation models through a new risk measure and fuzzy sharpe ratio. IEEE

Transactions on Fuzzy Systems, 23(3), pp.656-676.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.