University Finance Report: Crude Oil Futures and Options Analysis

VerifiedAdded on 2021/04/17

|12

|1637

|24

Report

AI Summary

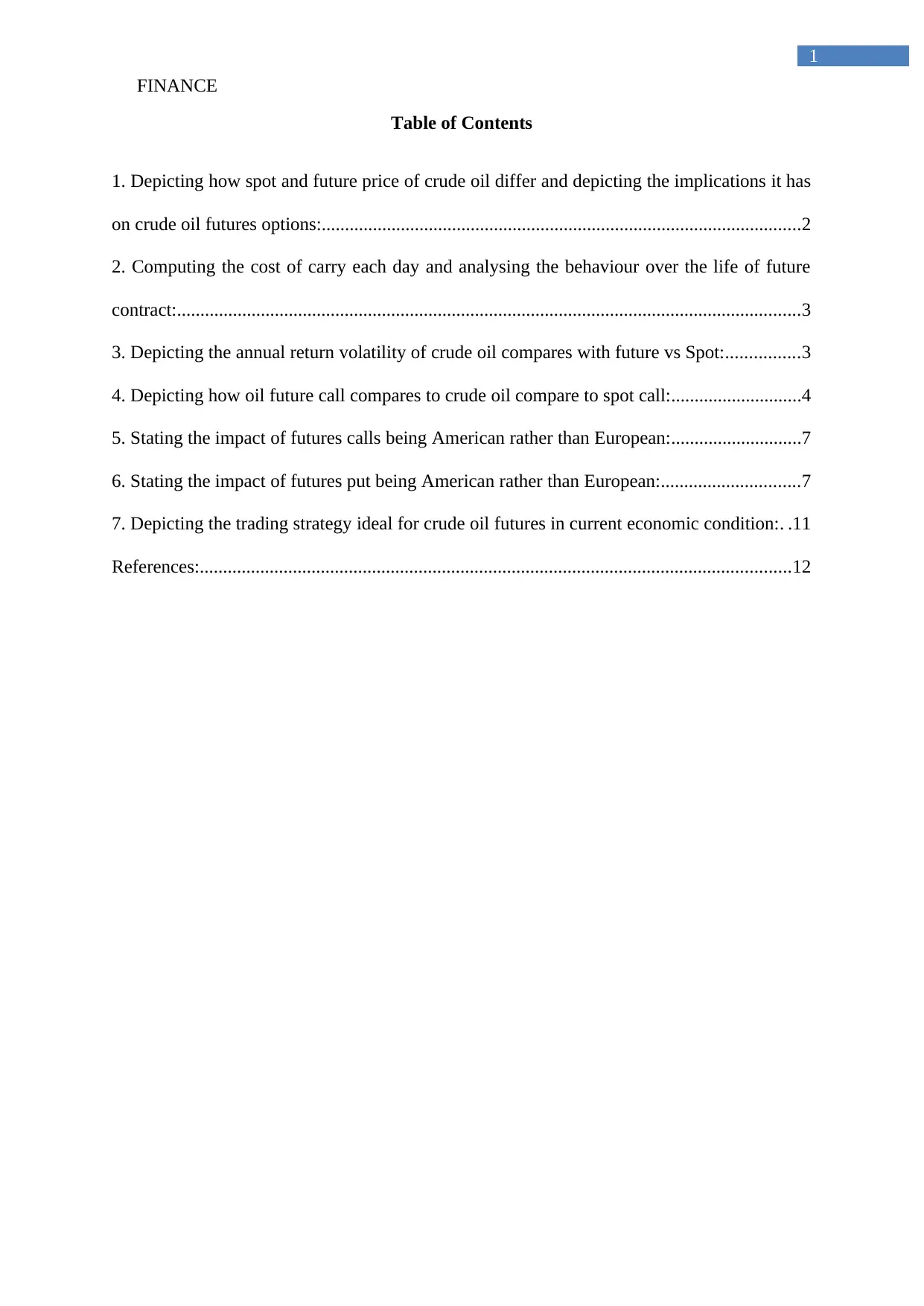

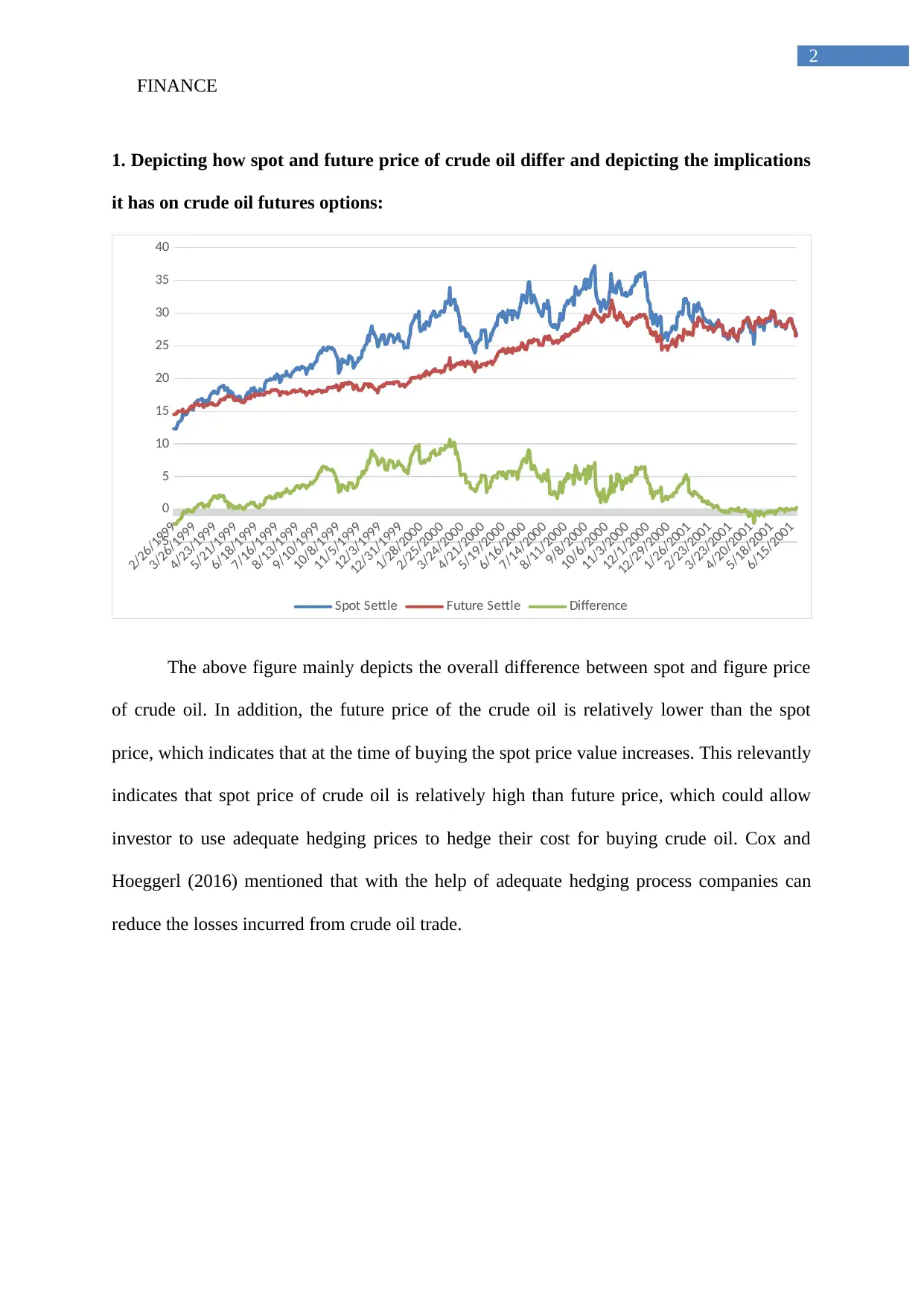

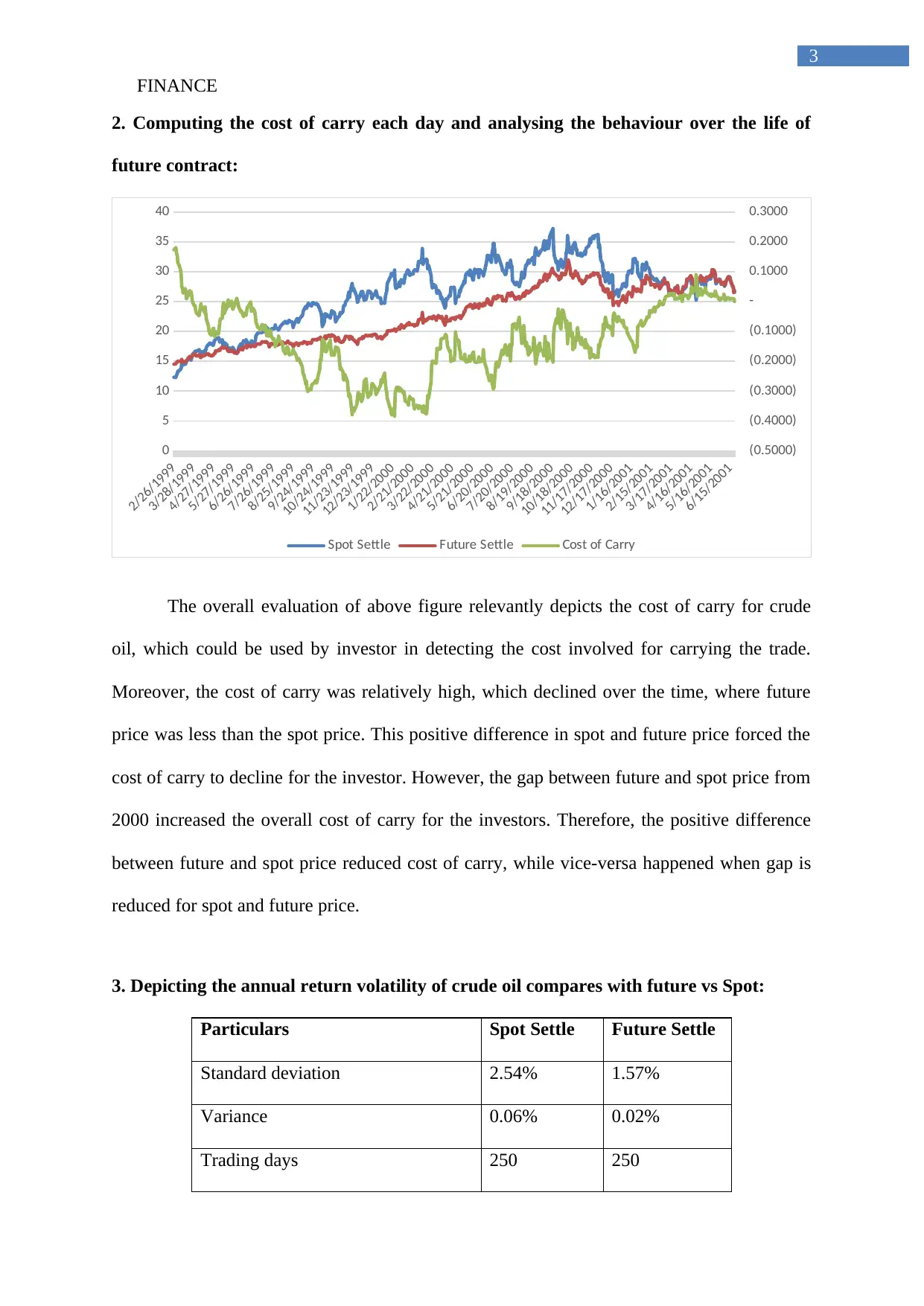

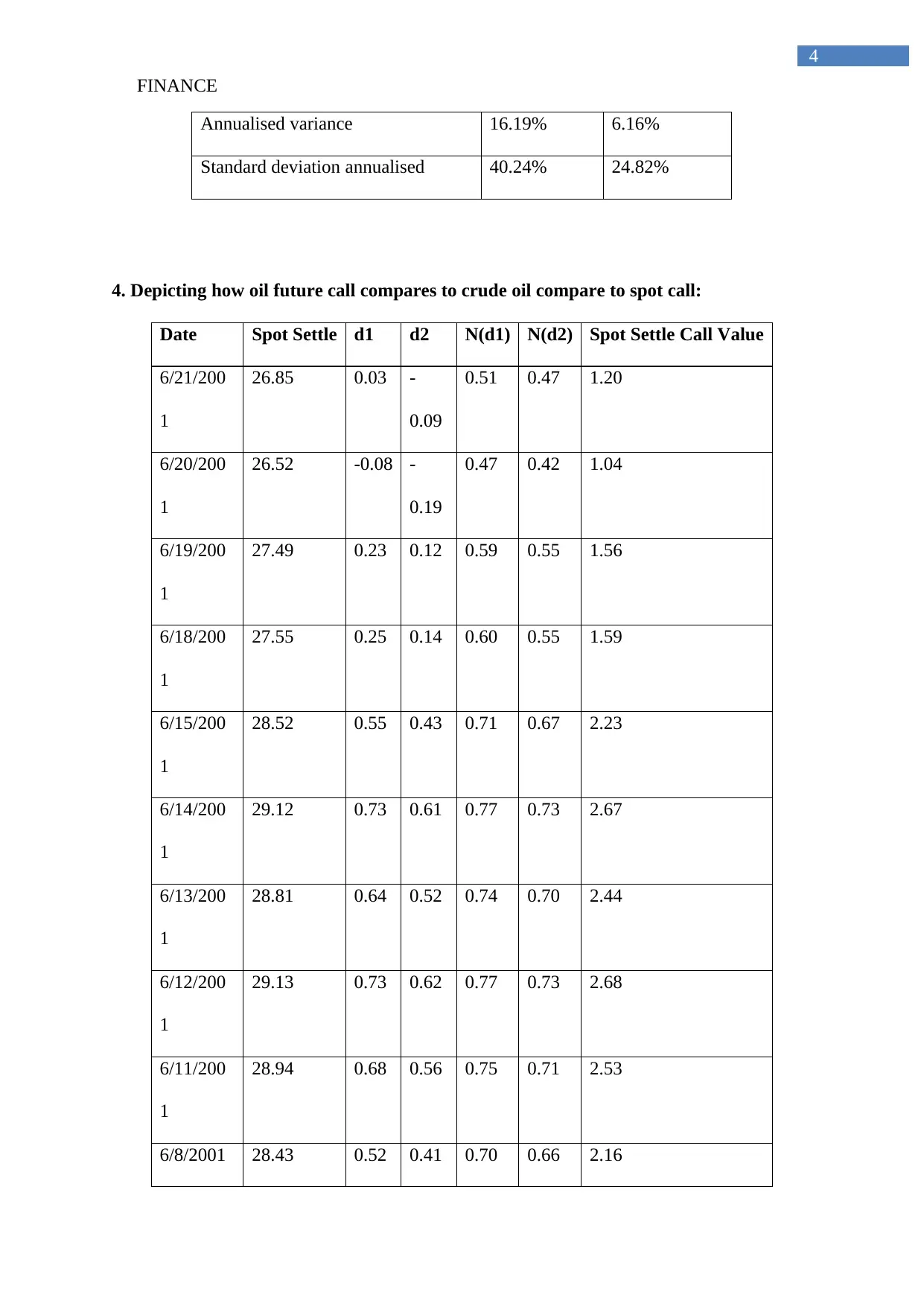

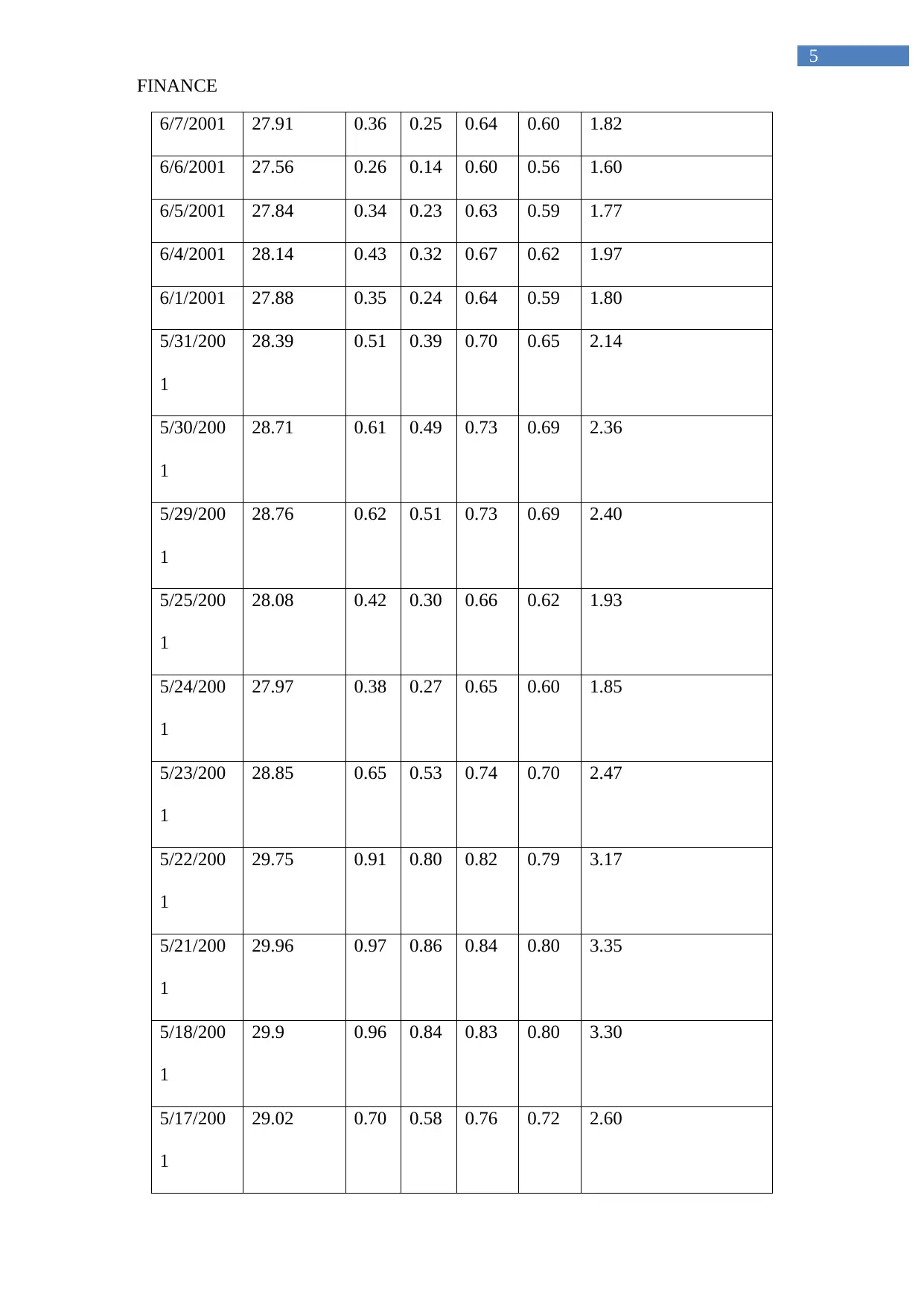

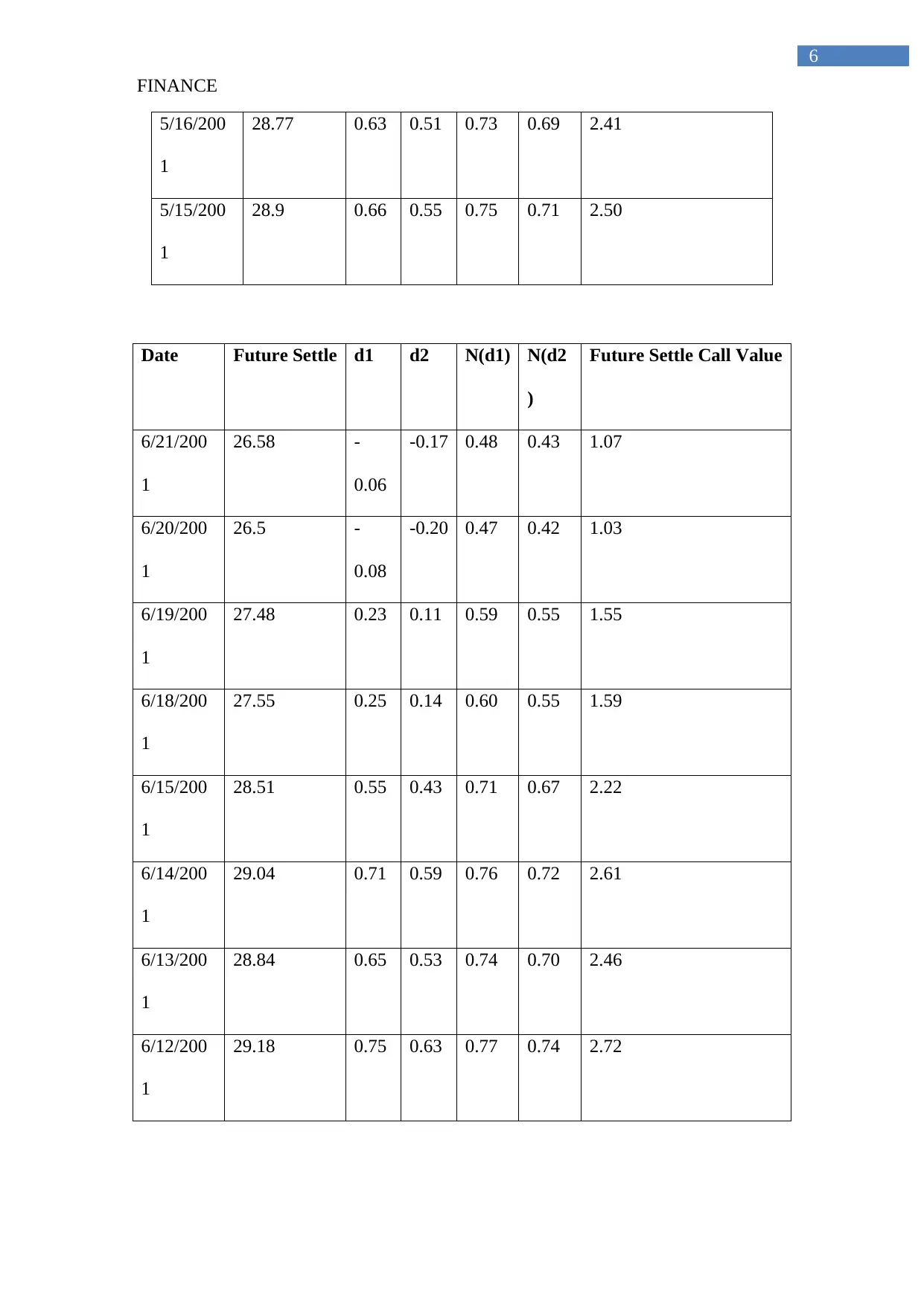

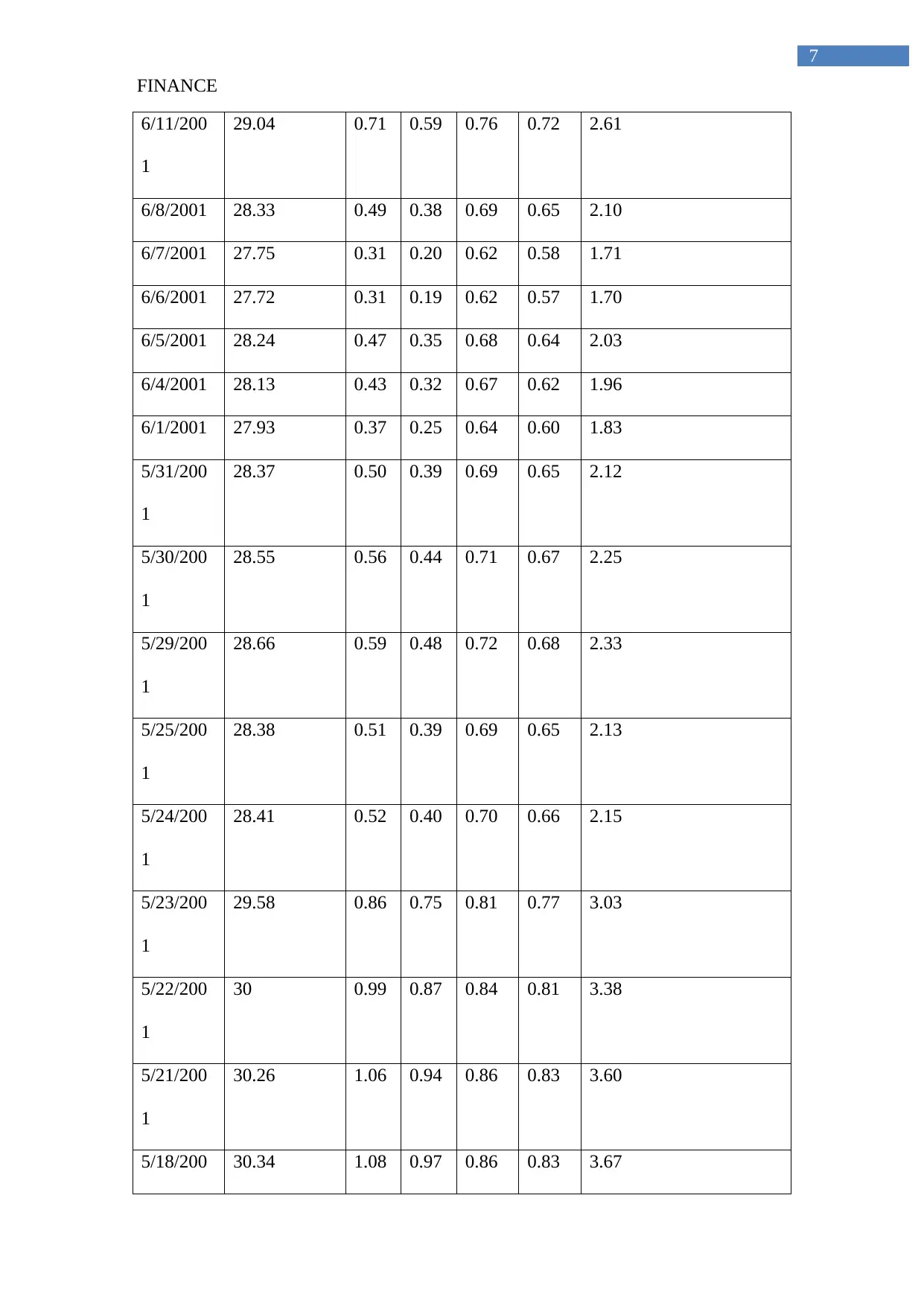

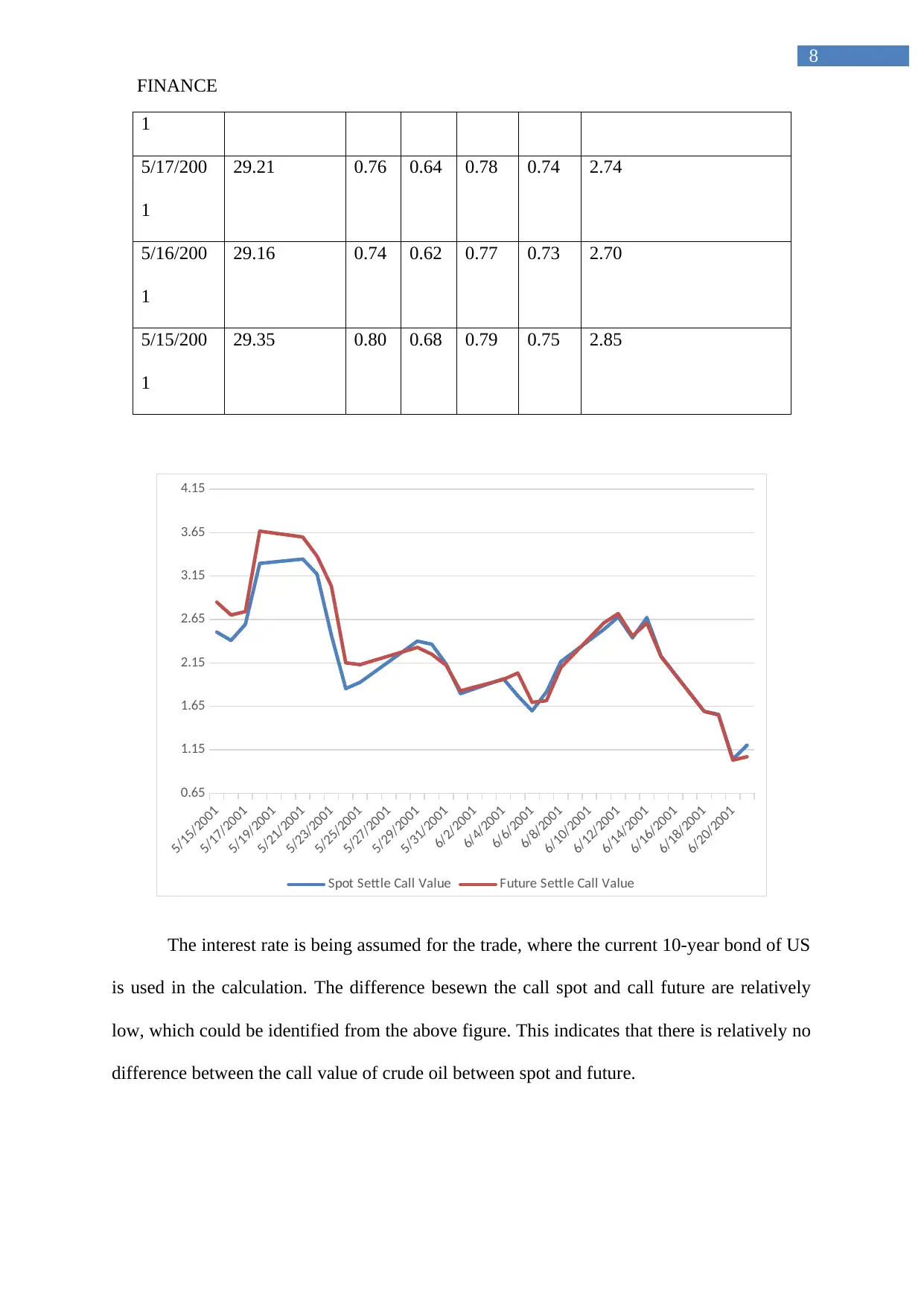

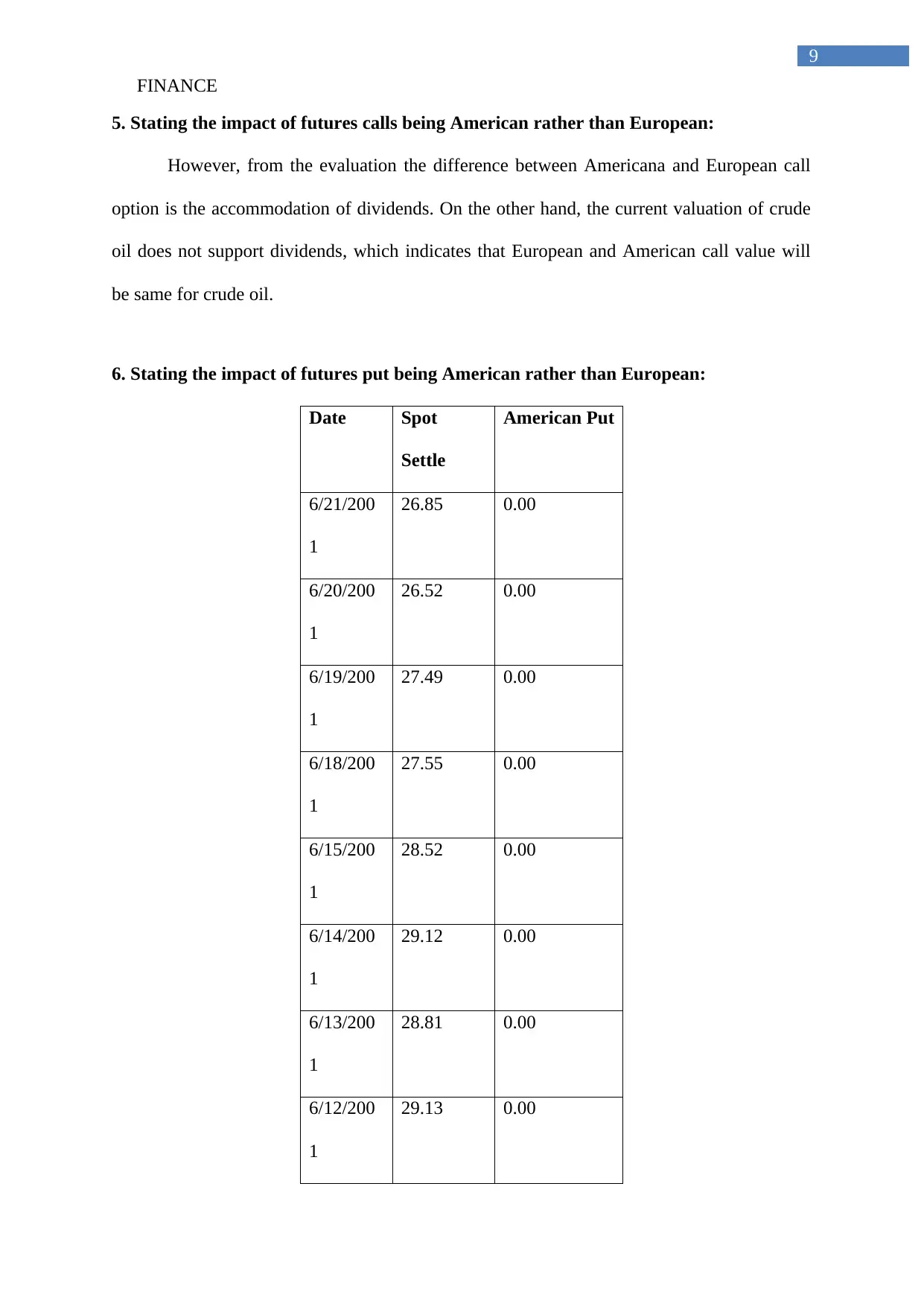

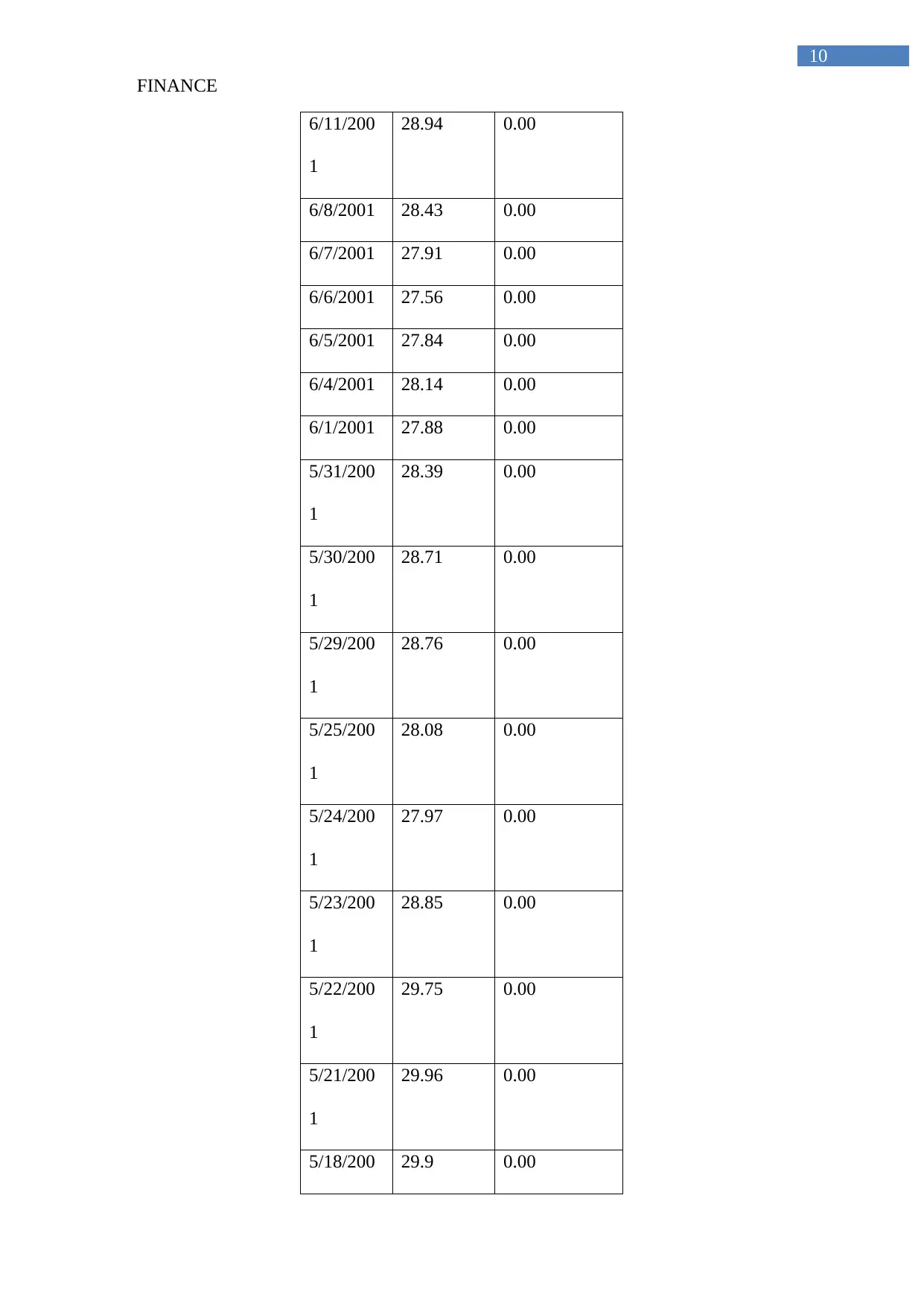

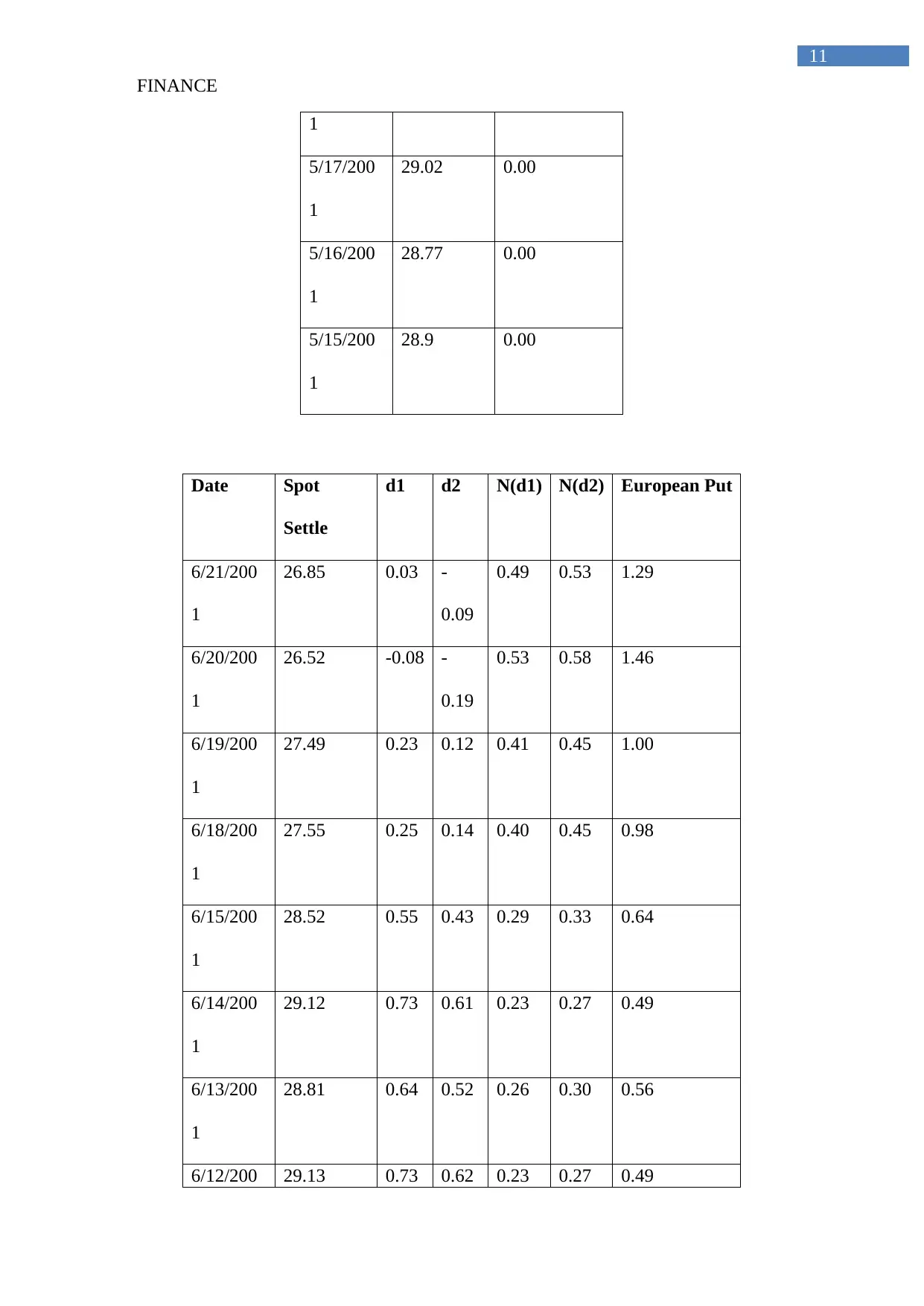

This finance report provides an in-depth analysis of crude oil futures contracts, examining the differences between spot and future prices and their implications for options trading. It computes and analyzes the cost of carry, demonstrating its behavior over the contract's life. The report compares the annual return volatility of crude oil futures versus spot prices and details the valuation of call options. Furthermore, it explores the impact of American versus European options on both call and put values. Finally, the report suggests an ideal trading strategy for crude oil futures in the current economic climate, incorporating hedging techniques to manage risk. The analysis is supported by relevant data and calculations, providing a comprehensive understanding of the crude oil futures market.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.