Comprehensive Financial Accounting Report and Case Studies

VerifiedAdded on 2020/10/05

|25

|7261

|384

Report

AI Summary

This report provides a comprehensive overview of financial accounting, covering its purpose, regulations, and fundamental principles. It defines financial accounting and its role in presenting financial performance and position to stakeholders. The report delves into accounting rules, including debit/credit principles for real, personal, and nominal accounts. It explores key accounting conventions like consistency and material disclosure, and includes detailed case studies with journal entries, ledger accounts, trial balances, and financial statements for multiple clients. The report also addresses topics such as bank reconciliation, control accounts, suspense accounts, and depreciation methods. Overall, the report offers a practical guide to financial accounting concepts and their application.

Finance accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

BUSINESS REPORT......................................................................................................................4

1. Define financial accounting and its purpose ...........................................................................4

2. Regulations relating to financial accounting:..........................................................................5

3. Describe accounting rules and principles................................................................................5

4. Conventions and concepts relating to consistency and material disclosure............................6

CLIENT 1........................................................................................................................................7

(a) Journal Entry in the books of David:......................................................................................7

(b) Ledger Accounts:...................................................................................................................9

(c) Trial Balance as at 31st January, 2018:................................................................................14

CLIENT 2......................................................................................................................................16

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 .............16

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ...................17

CLIENT 3......................................................................................................................................18

(a) Profit and loss account of Bowling Limited:........................................................................18

(b) Balance Sheet of Bowling Limited......................................................................................18

(c) Accounts concepts : Consistency and Prudence:..................................................................19

(d) Purpose of depreciation in formulating accounting statements and methods of

Depreciation:..............................................................................................................................19

CLIENT 4......................................................................................................................................20

(i) Bank reconciliation statement at 1st December 2017:..........................................................20

(ii) Durrell Ltd's updated cash book for December 2017 :........................................................20

(iii) Bank Reconciliation Statement as at 31"t December 2017:...............................................21

CLIENT 5......................................................................................................................................21

(a) Sales Ledger Control and Purchase Ledger Control Account:.............................................21

(b) Control Account:..................................................................................................................22

CLIENT 6......................................................................................................................................22

(a) Suspense Account:................................................................................................................22

(b) Preparation of Trail Balance:...............................................................................................23

INTRODUCTION...........................................................................................................................4

BUSINESS REPORT......................................................................................................................4

1. Define financial accounting and its purpose ...........................................................................4

2. Regulations relating to financial accounting:..........................................................................5

3. Describe accounting rules and principles................................................................................5

4. Conventions and concepts relating to consistency and material disclosure............................6

CLIENT 1........................................................................................................................................7

(a) Journal Entry in the books of David:......................................................................................7

(b) Ledger Accounts:...................................................................................................................9

(c) Trial Balance as at 31st January, 2018:................................................................................14

CLIENT 2......................................................................................................................................16

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 .............16

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ...................17

CLIENT 3......................................................................................................................................18

(a) Profit and loss account of Bowling Limited:........................................................................18

(b) Balance Sheet of Bowling Limited......................................................................................18

(c) Accounts concepts : Consistency and Prudence:..................................................................19

(d) Purpose of depreciation in formulating accounting statements and methods of

Depreciation:..............................................................................................................................19

CLIENT 4......................................................................................................................................20

(i) Bank reconciliation statement at 1st December 2017:..........................................................20

(ii) Durrell Ltd's updated cash book for December 2017 :........................................................20

(iii) Bank Reconciliation Statement as at 31"t December 2017:...............................................21

CLIENT 5......................................................................................................................................21

(a) Sales Ledger Control and Purchase Ledger Control Account:.............................................21

(b) Control Account:..................................................................................................................22

CLIENT 6......................................................................................................................................22

(a) Suspense Account:................................................................................................................22

(b) Preparation of Trail Balance:...............................................................................................23

(c) Journal entries in order to show necessary corrections for eliminating suspense account

balance:......................................................................................................................................23

(d) Difference between a Suspense A/c and Clearing A/c:........................................................24

CONCLUSIONS............................................................................................................................24

REFERENCES .............................................................................................................................25

balance:......................................................................................................................................23

(d) Difference between a Suspense A/c and Clearing A/c:........................................................24

CONCLUSIONS............................................................................................................................24

REFERENCES .............................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial Accounting is an area of accounting that considers cash or other monetary

items as a basis of determination of performance rather than as a determinant of production. In

financial accounting process accounting data or information is classified as cash inflow and out

outflow in terms of revenue and expenditure, assets and liabilities. Financial data and

information are collected and then summarised in order to prepare financial statements, income

statements, cash flows, change in equity for reporting purpose (Edwards, 2013). In financial

accounting main motive of organisation is to present financial data and information in a

systematic manner for user of financial data such as investors, relevant authorities, lenders and

creditors, debtors etc. This report describes purpose of financial accounting, regulations

concerned with financial accounting, rules and principles of accounting, different aspects of

financial reporting including concepts and conventions related to consistency and material

disclosure.

BUSINESS REPORT

1. Define financial accounting and its purpose

Financial accounting: It refers to set of activities related to preparation of financial statements

to present or report financial performance and position to internal or external users of financial

data. Major activities of financial reporting includes recording, classifying, summarising,

posting, analysing and reporting of financial data or information of business organisation

including drafting of financial statements such as balance sheet, profit and loss and cash flow

analysis. Financial accounting not only covers monetary items but also non monetary items

which assists in reporting purpose. Financial accounting starts with collection of financial data

and information and ends with reporting of financial performance and position (Fourie, 2015). In

financial accounting process accounts are prepared in accordance with local and international

accounting assumption and standards.

Purpose of financial accounting: The primary purpose of financial accounting is reporting of

final accounts to external or internal. Financial accounting assists in compliance of rules and

regulations prescribed by relevant authorities. Financial accounting through internal check

ensures accuracy in recording of financial information and data. It assists in identification of

suitable accounting policies, assumptions, conventions and other fundamentals as per business

Financial Accounting is an area of accounting that considers cash or other monetary

items as a basis of determination of performance rather than as a determinant of production. In

financial accounting process accounting data or information is classified as cash inflow and out

outflow in terms of revenue and expenditure, assets and liabilities. Financial data and

information are collected and then summarised in order to prepare financial statements, income

statements, cash flows, change in equity for reporting purpose (Edwards, 2013). In financial

accounting main motive of organisation is to present financial data and information in a

systematic manner for user of financial data such as investors, relevant authorities, lenders and

creditors, debtors etc. This report describes purpose of financial accounting, regulations

concerned with financial accounting, rules and principles of accounting, different aspects of

financial reporting including concepts and conventions related to consistency and material

disclosure.

BUSINESS REPORT

1. Define financial accounting and its purpose

Financial accounting: It refers to set of activities related to preparation of financial statements

to present or report financial performance and position to internal or external users of financial

data. Major activities of financial reporting includes recording, classifying, summarising,

posting, analysing and reporting of financial data or information of business organisation

including drafting of financial statements such as balance sheet, profit and loss and cash flow

analysis. Financial accounting not only covers monetary items but also non monetary items

which assists in reporting purpose. Financial accounting starts with collection of financial data

and information and ends with reporting of financial performance and position (Fourie, 2015). In

financial accounting process accounts are prepared in accordance with local and international

accounting assumption and standards.

Purpose of financial accounting: The primary purpose of financial accounting is reporting of

final accounts to external or internal. Financial accounting assists in compliance of rules and

regulations prescribed by relevant authorities. Financial accounting through internal check

ensures accuracy in recording of financial information and data. It assists in identification of

suitable accounting policies, assumptions, conventions and other fundamentals as per business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

structure of organisation. Financial accounting provides a basis for choosing and implementing a

most appropriate strategy as per business requirement. Actual outcomes regarding financial

performance and position of business organisation under financial accounting process define the

objectives and goals of company.

2. Regulations relating to financial accounting:

Regulations refers steps normally in form of order, taken by relevant authority or

governing body to control and regulate activities of organisations or individuals. To establish

proper control and to maintain uniformity in accounts relevant authorities create regulations.

Regulations relating to financial accounting: Regulations provides guidance for preparation and

presentation of financial accounts such as generally accepted accounting policies and standards.

Some regulations are applicable for business organisations operating its business globally such as

IFRS (International financial reporting framework). For making uniformity in financial

accounting process some regulations are framed regarding accounting assumptions, concepts,

methods, conventions and policies (Hale and Held, 2012). For business organisation regulated

under any specific act, regulations are framed under such relevant act.

3. Describe accounting rules and principles

Data and information are initially recorded using accounting entries. There are some

accounting rules are discussed below which helps the organisation to smooth their financial

accounting process:

Debit what comes in, credit what goes out: This rule is mainly framed for real account.

Real accounts includes all assets of a firm whether tangible or intangible such as plant and

machinery account, furniture and fixture, goodwill, land and buildings account, free hold

premises etc. Real accounts are classified as Tangible real accounts and Intangible real accounts.

Tangible real accounts includes building accounts, plant account, inventory account etc. Whereas

Intangible real accounts includes accounts of items which do not have any physical existence

such as goodwill, patent, copyright etc.

Debit the receiver, credit the giver: This rule is framed for personal accounts. Personal

account refers to a general ledger account concerned with individuals, firms and associations like

creditors account, debtors account, capital account, banks account etc. Under this rule if person

give something to organisation it treated as inflow therefore personal account will be credited

most appropriate strategy as per business requirement. Actual outcomes regarding financial

performance and position of business organisation under financial accounting process define the

objectives and goals of company.

2. Regulations relating to financial accounting:

Regulations refers steps normally in form of order, taken by relevant authority or

governing body to control and regulate activities of organisations or individuals. To establish

proper control and to maintain uniformity in accounts relevant authorities create regulations.

Regulations relating to financial accounting: Regulations provides guidance for preparation and

presentation of financial accounts such as generally accepted accounting policies and standards.

Some regulations are applicable for business organisations operating its business globally such as

IFRS (International financial reporting framework). For making uniformity in financial

accounting process some regulations are framed regarding accounting assumptions, concepts,

methods, conventions and policies (Hale and Held, 2012). For business organisation regulated

under any specific act, regulations are framed under such relevant act.

3. Describe accounting rules and principles

Data and information are initially recorded using accounting entries. There are some

accounting rules are discussed below which helps the organisation to smooth their financial

accounting process:

Debit what comes in, credit what goes out: This rule is mainly framed for real account.

Real accounts includes all assets of a firm whether tangible or intangible such as plant and

machinery account, furniture and fixture, goodwill, land and buildings account, free hold

premises etc. Real accounts are classified as Tangible real accounts and Intangible real accounts.

Tangible real accounts includes building accounts, plant account, inventory account etc. Whereas

Intangible real accounts includes accounts of items which do not have any physical existence

such as goodwill, patent, copyright etc.

Debit the receiver, credit the giver: This rule is framed for personal accounts. Personal

account refers to a general ledger account concerned with individuals, firms and associations like

creditors account, debtors account, capital account, banks account etc. Under this rule if person

give something to organisation it treated as inflow therefore personal account will be credited

and if person receive something from the organisation than amount should be debited on name of

person (Hall, 2012).

Debit all expenses and losses, credit all incomes and gains: This rules is framed for

nominal account. Nominal account refers to General ledger account concerned with all revenues

or income, expenses, losses and gains. In this rule capital is treated as liability for business and

liability shows credit balances. Incomes and gains leads to increase in capital therefore all

incomes and gains are credited whereas all expenses and losses should be debited because

expenses or losses leads to decrease in capital.

Principles: Following are the major principles of accounting that provides a framework for

preparation of final accounts, are as follows:

1. Dual aspect concept: Dual aspect concept truly resembles to double entry system.

According to dual aspect concept each and every transaction in an business organisation

affects both debit and credit side simultaneously. Under Single entry system only one

side of an account is affected which creates complexity in accounting calculation

therefore single entry system is avoided by entities (Jönsson, 2013).

2. Cost principle: This principle emphasises on reporting of assets on their cost. As per

this principle business organisation should record their assets on actual cost.

3. Matching principle: According to this principle, all expenses of business should be

matched with revenues which are occurred or being occurred in particular period.

4. Conventions and concepts relating to consistency and material disclosure

Accounting convention refers to guideline and framework for adoption of accounting

principles. It includes general practices and guidelines which assists in preparation of final

accounts (Mullinova, 2016). Accounting conventions are used in areas where no accounting

standard is prescribed. Conventions are applied by business organisations as per their

requirements to reduce complexity in accounting process.

Convention of consistency: Conventions of consistency emphasises on maintaining

consistency in applied policies and assumptions from period to period. Use of this

convention assists in preparation of comparative accounts and to reduce complexities in

accounting process.

person (Hall, 2012).

Debit all expenses and losses, credit all incomes and gains: This rules is framed for

nominal account. Nominal account refers to General ledger account concerned with all revenues

or income, expenses, losses and gains. In this rule capital is treated as liability for business and

liability shows credit balances. Incomes and gains leads to increase in capital therefore all

incomes and gains are credited whereas all expenses and losses should be debited because

expenses or losses leads to decrease in capital.

Principles: Following are the major principles of accounting that provides a framework for

preparation of final accounts, are as follows:

1. Dual aspect concept: Dual aspect concept truly resembles to double entry system.

According to dual aspect concept each and every transaction in an business organisation

affects both debit and credit side simultaneously. Under Single entry system only one

side of an account is affected which creates complexity in accounting calculation

therefore single entry system is avoided by entities (Jönsson, 2013).

2. Cost principle: This principle emphasises on reporting of assets on their cost. As per

this principle business organisation should record their assets on actual cost.

3. Matching principle: According to this principle, all expenses of business should be

matched with revenues which are occurred or being occurred in particular period.

4. Conventions and concepts relating to consistency and material disclosure

Accounting convention refers to guideline and framework for adoption of accounting

principles. It includes general practices and guidelines which assists in preparation of final

accounts (Mullinova, 2016). Accounting conventions are used in areas where no accounting

standard is prescribed. Conventions are applied by business organisations as per their

requirements to reduce complexity in accounting process.

Convention of consistency: Conventions of consistency emphasises on maintaining

consistency in applied policies and assumptions from period to period. Use of this

convention assists in preparation of comparative accounts and to reduce complexities in

accounting process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Convention of material disclosure: This convention creates uniformity in disclosures of

materiel items in different organisations. Disclosure of material items in final accounts

helps to identify any fraud, error or irregularity in business organisation.

CLIENT 1

(a) Journal Entry in the books of David:

Date Particulars Debit Credit

01/01/18 Premises A/c …...........…........... Dr. 440000

Motor Van A/c…...........…...........Dr. 45250

fixtures A/c…...........…........... Dr. 10100

Inventory A/c …...........…...........Dr. 40900

P Mole A/c …...........…........... Dr. 2200

F Lane A/c…...........…........... Dr. 2100

Bank A/c …........... …........... Dr. 42400

Cash A/c …...........…........... Dr. 10600

To S Hamid A/c 10150

To J. Brown A/c 9600

To Capital A/c (Balancing Figure) 573800

(Being Owner's Capital is calculated )

Therefore, David Study's Capital at 1st January = £

573800

Date Particulars Debit Credit

01/01/18 Storage cost A/c…...........…........... Dr. 800

To bank A/c 800

(Being storage cost is paid)

02/01/18 Purchases A/c…...........…........... Dr. 7680

materiel items in different organisations. Disclosure of material items in final accounts

helps to identify any fraud, error or irregularity in business organisation.

CLIENT 1

(a) Journal Entry in the books of David:

Date Particulars Debit Credit

01/01/18 Premises A/c …...........…........... Dr. 440000

Motor Van A/c…...........…...........Dr. 45250

fixtures A/c…...........…........... Dr. 10100

Inventory A/c …...........…...........Dr. 40900

P Mole A/c …...........…........... Dr. 2200

F Lane A/c…...........…........... Dr. 2100

Bank A/c …........... …........... Dr. 42400

Cash A/c …...........…........... Dr. 10600

To S Hamid A/c 10150

To J. Brown A/c 9600

To Capital A/c (Balancing Figure) 573800

(Being Owner's Capital is calculated )

Therefore, David Study's Capital at 1st January = £

573800

Date Particulars Debit Credit

01/01/18 Storage cost A/c…...........…........... Dr. 800

To bank A/c 800

(Being storage cost is paid)

02/01/18 Purchases A/c…...........…........... Dr. 7680

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

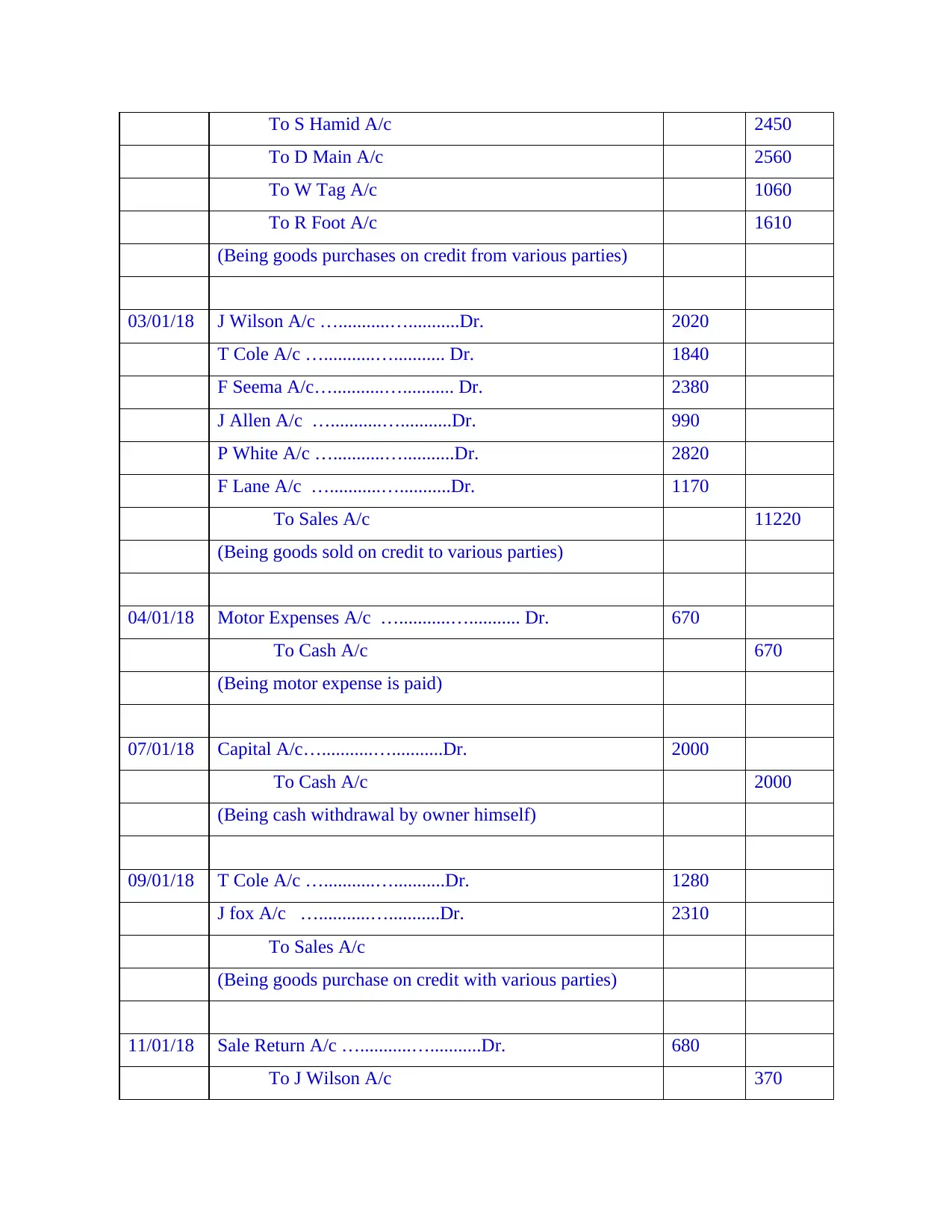

(Being goods purchases on credit from various parties)

03/01/18 J Wilson A/c …...........…...........Dr. 2020

T Cole A/c …...........…........... Dr. 1840

F Seema A/c…...........…........... Dr. 2380

J Allen A/c …...........…...........Dr. 990

P White A/c …...........…...........Dr. 2820

F Lane A/c …...........…...........Dr. 1170

To Sales A/c 11220

(Being goods sold on credit to various parties)

04/01/18 Motor Expenses A/c …...........…........... Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/01/18 Capital A/c…...........…...........Dr. 2000

To Cash A/c 2000

(Being cash withdrawal by owner himself)

09/01/18 T Cole A/c …...........…...........Dr. 1280

J fox A/c …...........…...........Dr. 2310

To Sales A/c

(Being goods purchase on credit with various parties)

11/01/18 Sale Return A/c …...........…...........Dr. 680

To J Wilson A/c 370

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/18 J Wilson A/c …...........…...........Dr. 2020

T Cole A/c …...........…........... Dr. 1840

F Seema A/c…...........…........... Dr. 2380

J Allen A/c …...........…...........Dr. 990

P White A/c …...........…...........Dr. 2820

F Lane A/c …...........…...........Dr. 1170

To Sales A/c 11220

(Being goods sold on credit to various parties)

04/01/18 Motor Expenses A/c …...........…........... Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/01/18 Capital A/c…...........…...........Dr. 2000

To Cash A/c 2000

(Being cash withdrawal by owner himself)

09/01/18 T Cole A/c …...........…...........Dr. 1280

J fox A/c …...........…...........Dr. 2310

To Sales A/c

(Being goods purchase on credit with various parties)

11/01/18 Sale Return A/c …...........…...........Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by the parties

16/01/18 Bank A/c …...........…...........Dr. 7150

Discount Allowed A/c …...........…........... Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

To J Wilson A/c 963

To F Seema A/c 1574

(Being Payment received from parties after allowing

discount @ 5%)

19/01/18 R Foot A/c …...........…........... Dr. 110

To Purchases Return A/c 110

(Being Goods is returned to creditor)

22/01/18 Purchases A/c …...........…...........Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/01/18 S Hamid A/c…...........…........... Dr. 3860

J Brown A/c …...........…...........Dr. 4260

R Foot A/c …...........…........... Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors after receiving

discount @ 10%)

27/01/18 Salaries A/c …...........…........... Dr. 14500

(Being goods is returned back by the parties

16/01/18 Bank A/c …...........…...........Dr. 7150

Discount Allowed A/c …...........…........... Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

To J Wilson A/c 963

To F Seema A/c 1574

(Being Payment received from parties after allowing

discount @ 5%)

19/01/18 R Foot A/c …...........…........... Dr. 110

To Purchases Return A/c 110

(Being Goods is returned to creditor)

22/01/18 Purchases A/c …...........…...........Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/01/18 S Hamid A/c…...........…........... Dr. 3860

J Brown A/c …...........…...........Dr. 4260

R Foot A/c …...........…........... Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors after receiving

discount @ 10%)

27/01/18 Salaries A/c …...........…........... Dr. 14500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

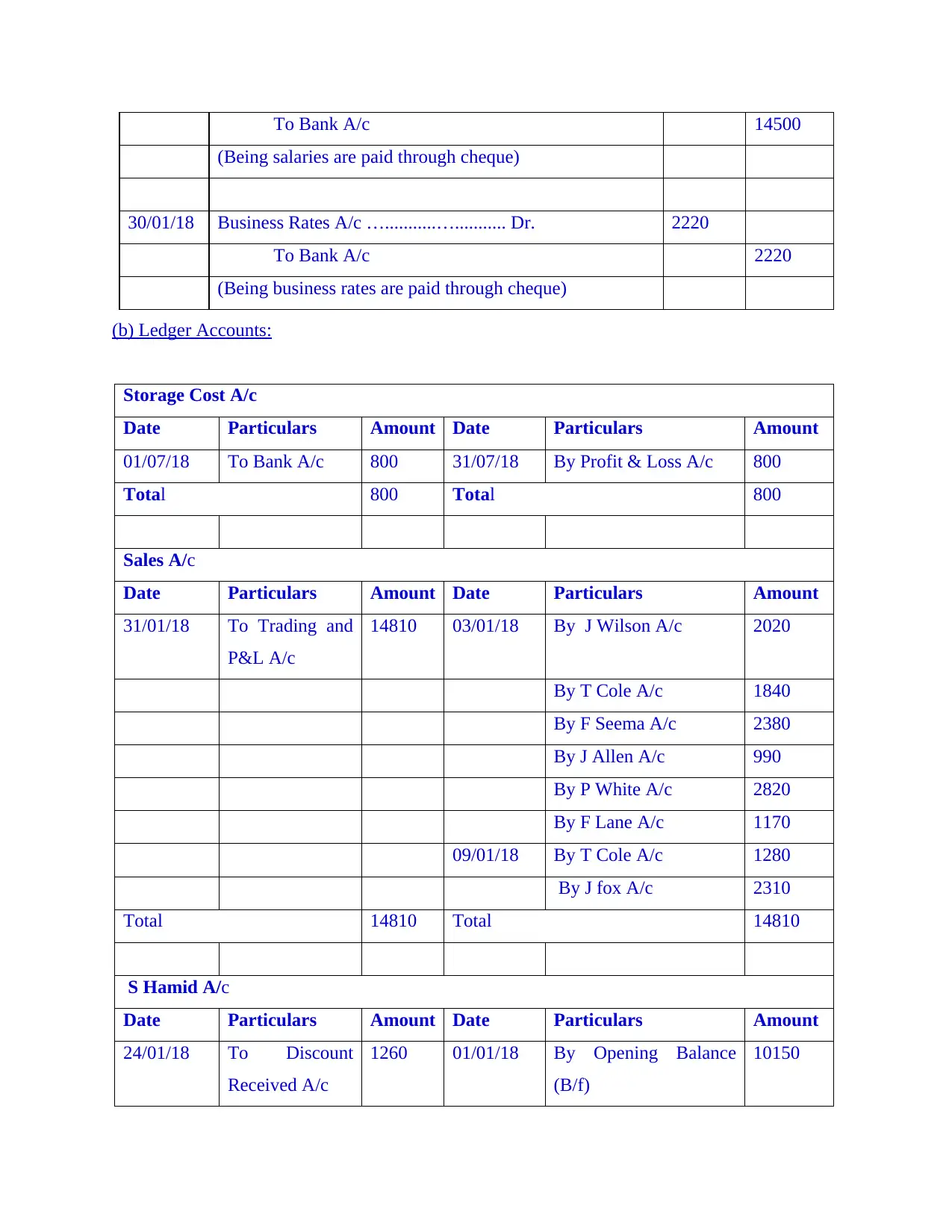

To Bank A/c 14500

(Being salaries are paid through cheque)

30/01/18 Business Rates A/c …...........…........... Dr. 2220

To Bank A/c 2220

(Being business rates are paid through cheque)

(b) Ledger Accounts:

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/18 To Bank A/c 800 31/07/18 By Profit & Loss A/c 800

Total 800 Total 800

Sales A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Trading and

P&L A/c

14810 03/01/18 By J Wilson A/c 2020

By T Cole A/c 1840

By F Seema A/c 2380

By J Allen A/c 990

By P White A/c 2820

By F Lane A/c 1170

09/01/18 By T Cole A/c 1280

By J fox A/c 2310

Total 14810 Total 14810

S Hamid A/c

Date Particulars Amount Date Particulars Amount

24/01/18 To Discount

Received A/c

1260 01/01/18 By Opening Balance

(B/f)

10150

(Being salaries are paid through cheque)

30/01/18 Business Rates A/c …...........…........... Dr. 2220

To Bank A/c 2220

(Being business rates are paid through cheque)

(b) Ledger Accounts:

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/18 To Bank A/c 800 31/07/18 By Profit & Loss A/c 800

Total 800 Total 800

Sales A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Trading and

P&L A/c

14810 03/01/18 By J Wilson A/c 2020

By T Cole A/c 1840

By F Seema A/c 2380

By J Allen A/c 990

By P White A/c 2820

By F Lane A/c 1170

09/01/18 By T Cole A/c 1280

By J fox A/c 2310

Total 14810 Total 14810

S Hamid A/c

Date Particulars Amount Date Particulars Amount

24/01/18 To Discount

Received A/c

1260 01/01/18 By Opening Balance

(B/f)

10150

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To Bank A/c 2600 02/01/18 By purchases A/c 2450

31/01/18 To Closing

Balance C/d

8740

Total 12600 Total 12600

W Tag A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Closing

Balance C/d

1060 02/01/18 By purchases A/c 1060

Total 1060 Total 1060

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2020 11/01/18 By Sales Return A/c 370

16/01/18 By Bank A/c 880

By Discount Allowed

A/c

83

31/01/18 By Closing Balance c/d 687

Total 2020 Total 2020

F Seema A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2380 11/01/18 By Sales Return A/c 310

16/01/18 By Bank A/c 1470

By Discount Allowed

A/c

104

31/01/18 By Closing Balance c/d 496

Total 2380 Total 2380

P White A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Closing

Balance C/d

8740

Total 12600 Total 12600

W Tag A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Closing

Balance C/d

1060 02/01/18 By purchases A/c 1060

Total 1060 Total 1060

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2020 11/01/18 By Sales Return A/c 370

16/01/18 By Bank A/c 880

By Discount Allowed

A/c

83

31/01/18 By Closing Balance c/d 687

Total 2020 Total 2020

F Seema A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2380 11/01/18 By Sales Return A/c 310

16/01/18 By Bank A/c 1470

By Discount Allowed

A/c

104

31/01/18 By Closing Balance c/d 496

Total 2380 Total 2380

P White A/c

Date Particulars Amount Date Particulars Amount

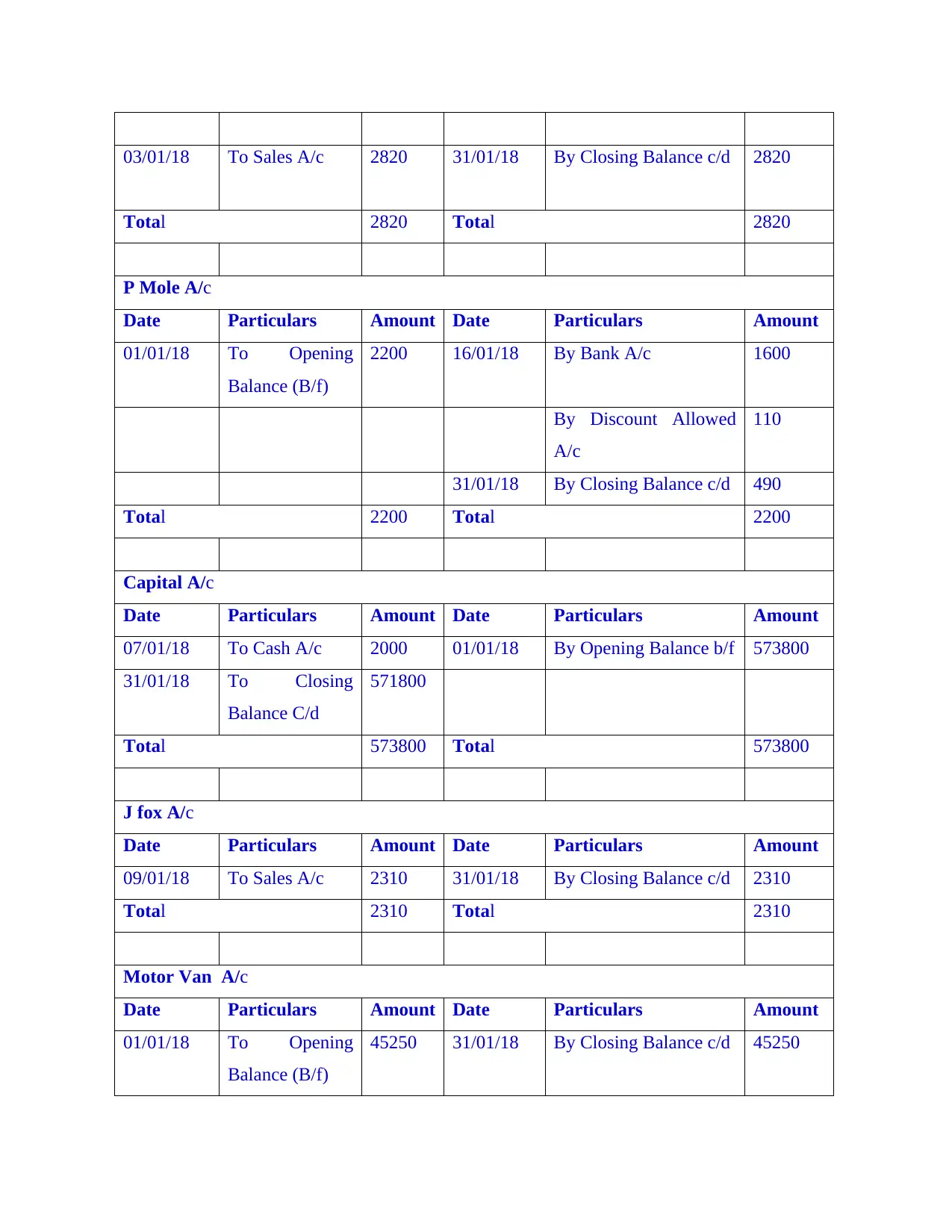

03/01/18 To Sales A/c 2820 31/01/18 By Closing Balance c/d 2820

Total 2820 Total 2820

P Mole A/c

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

2200 16/01/18 By Bank A/c 1600

By Discount Allowed

A/c

110

31/01/18 By Closing Balance c/d 490

Total 2200 Total 2200

Capital A/c

Date Particulars Amount Date Particulars Amount

07/01/18 To Cash A/c 2000 01/01/18 By Opening Balance b/f 573800

31/01/18 To Closing

Balance C/d

571800

Total 573800 Total 573800

J fox A/c

Date Particulars Amount Date Particulars Amount

09/01/18 To Sales A/c 2310 31/01/18 By Closing Balance c/d 2310

Total 2310 Total 2310

Motor Van A/c

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

45250 31/01/18 By Closing Balance c/d 45250

Total 2820 Total 2820

P Mole A/c

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

2200 16/01/18 By Bank A/c 1600

By Discount Allowed

A/c

110

31/01/18 By Closing Balance c/d 490

Total 2200 Total 2200

Capital A/c

Date Particulars Amount Date Particulars Amount

07/01/18 To Cash A/c 2000 01/01/18 By Opening Balance b/f 573800

31/01/18 To Closing

Balance C/d

571800

Total 573800 Total 573800

J fox A/c

Date Particulars Amount Date Particulars Amount

09/01/18 To Sales A/c 2310 31/01/18 By Closing Balance c/d 2310

Total 2310 Total 2310

Motor Van A/c

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

45250 31/01/18 By Closing Balance c/d 45250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.