Finance for Administrative Managers: Costing, Budgeting & Analysis

VerifiedAdded on 2023/06/11

|12

|2485

|153

Report

AI Summary

This report provides a comprehensive overview of finance for administrative managers, covering cost accounting, management accounting, budgeting techniques, and financial statement analysis. It defines cost and management accounting, analyzes cost information for business decisions using scenarios, and discusses the use of budgets in business, including cash, sales, capital, and production budgets. The report also explores budgetary control techniques such as variance analysis and zero-based budgeting, along with their limitations. Furthermore, it examines the financial statements prepared by Tesco Plc, including the income statement, balance sheet, statement of changes in equity, and cash flow statement, followed by a ratio analysis covering profitability, efficiency, gearing, and liquidity ratios, to assess the company's financial health. The document is contributed by a student and available on Desklib, a platform offering study tools for students.

Running head: FINANCE FOR ADMINISTRATIVE MANAGERS

Finance for administrative managers

Name of the student

Name of the university

Student ID

Author note

Finance for administrative managers

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR ADMINISTRATIVE MANAGERS

Table of Contents

Activity 1....................................................................................................................................2

Cost accounting and management accounting.......................................................................2

Cost information required for taking business decisions (Scenario 1)..................................2

Decision making through cost information (Scenario 2).......................................................3

Activity 2....................................................................................................................................4

Using of budget in business...................................................................................................4

Preparation of various budgets...............................................................................................4

Budgets and budgetary control...............................................................................................5

Limitations of budget.............................................................................................................6

Activity 3....................................................................................................................................7

Financial statements prepared by Tesco Plc..........................................................................7

Ratio analysis.........................................................................................................................7

Reference....................................................................................................................................9

Table of Contents

Activity 1....................................................................................................................................2

Cost accounting and management accounting.......................................................................2

Cost information required for taking business decisions (Scenario 1)..................................2

Decision making through cost information (Scenario 2).......................................................3

Activity 2....................................................................................................................................4

Using of budget in business...................................................................................................4

Preparation of various budgets...............................................................................................4

Budgets and budgetary control...............................................................................................5

Limitations of budget.............................................................................................................6

Activity 3....................................................................................................................................7

Financial statements prepared by Tesco Plc..........................................................................7

Ratio analysis.........................................................................................................................7

Reference....................................................................................................................................9

2FINANCE FOR ADMINISTRATIVE MANAGERS

Activity 1

Cost accounting and management accounting

Cost accounting is the technique of recording, collecting, analysing and classifying

the cost related information. On the other hand, the management accounting is the

preparation of non-financial as well as financial information for the purpose of management

use. The main purpose of cost accounting is budgeting and planning, controlling the

organizational operations, making cost related decisions, allocation of resources and

evaluating the performances. On the other hand, the main purpose of management accounting

are analyse the financial information, preparing reports, planning the future needs of the

company and motivating and directing the employees for achieving the business objectives

(Hilton and Platt 2013).

Cost information required for taking business decisions (Scenario 1)

Business decision needs clear knowledge regarding various cost concepts. Different

kinds of costs differ with regard to their nature like fixed or variable and basis of allocation.

Taking into consideration the scenario of example 1, it can be suggested that before taking

final decisions regarding shutting down the furniture division of bespoke office the below

mentioned cost information shall be considered –

Fixed costs that will be required to be spent even after shutting down the division.

The depreciation expenses and maintenance cost of premises and equipment

Payment to the long service staffs (Drury 2013)

Though the cost associated with furniture division of bespoke office is high and the

profits are also falling, before shutting down the management shall consider that the fixed

cost that are to be incurred even after closing down the division will results into negative

Activity 1

Cost accounting and management accounting

Cost accounting is the technique of recording, collecting, analysing and classifying

the cost related information. On the other hand, the management accounting is the

preparation of non-financial as well as financial information for the purpose of management

use. The main purpose of cost accounting is budgeting and planning, controlling the

organizational operations, making cost related decisions, allocation of resources and

evaluating the performances. On the other hand, the main purpose of management accounting

are analyse the financial information, preparing reports, planning the future needs of the

company and motivating and directing the employees for achieving the business objectives

(Hilton and Platt 2013).

Cost information required for taking business decisions (Scenario 1)

Business decision needs clear knowledge regarding various cost concepts. Different

kinds of costs differ with regard to their nature like fixed or variable and basis of allocation.

Taking into consideration the scenario of example 1, it can be suggested that before taking

final decisions regarding shutting down the furniture division of bespoke office the below

mentioned cost information shall be considered –

Fixed costs that will be required to be spent even after shutting down the division.

The depreciation expenses and maintenance cost of premises and equipment

Payment to the long service staffs (Drury 2013)

Though the cost associated with furniture division of bespoke office is high and the

profits are also falling, before shutting down the management shall consider that the fixed

cost that are to be incurred even after closing down the division will results into negative

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR ADMINISTRATIVE MANAGERS

profit. Therefore, rather than closing down the division the management shall try to control

the cost, wherever possible for increasing the profit. For instance, cost of production can be

controlled with new technology of machines (Eldenburg et al. 2016).

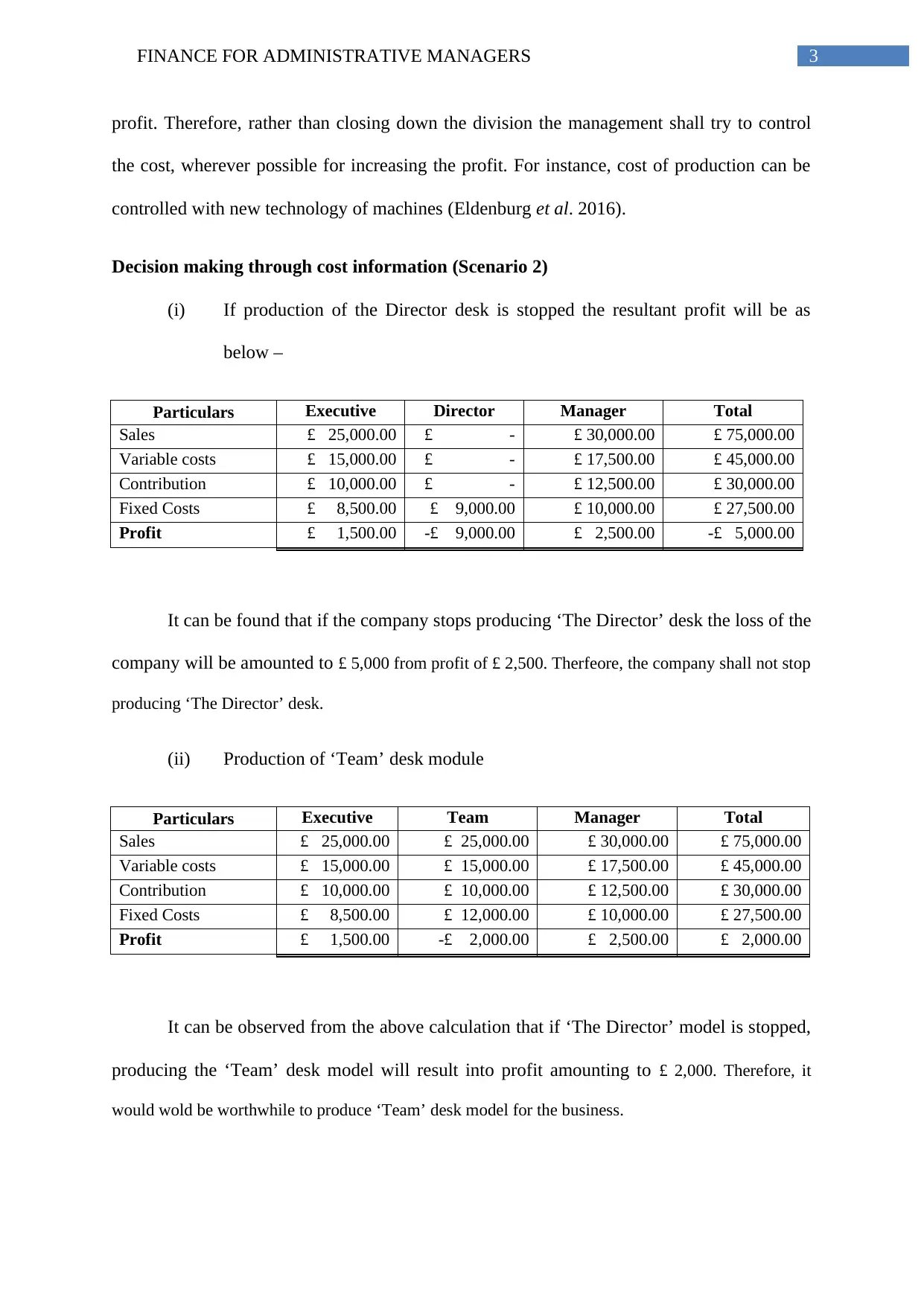

Decision making through cost information (Scenario 2)

(i) If production of the Director desk is stopped the resultant profit will be as

below –

Particulars Executive Director Manager Total

Sales £ 25,000.00 £ - £ 30,000.00 £ 75,000.00

Variable costs £ 15,000.00 £ - £ 17,500.00 £ 45,000.00

Contribution £ 10,000.00 £ - £ 12,500.00 £ 30,000.00

Fixed Costs £ 8,500.00 £ 9,000.00 £ 10,000.00 £ 27,500.00

Profit £ 1,500.00 -£ 9,000.00 £ 2,500.00 -£ 5,000.00

It can be found that if the company stops producing ‘The Director’ desk the loss of the

company will be amounted to £ 5,000 from profit of £ 2,500. Therfeore, the company shall not stop

producing ‘The Director’ desk.

(ii) Production of ‘Team’ desk module

Particulars Executive Team Manager Total

Sales £ 25,000.00 £ 25,000.00 £ 30,000.00 £ 75,000.00

Variable costs £ 15,000.00 £ 15,000.00 £ 17,500.00 £ 45,000.00

Contribution £ 10,000.00 £ 10,000.00 £ 12,500.00 £ 30,000.00

Fixed Costs £ 8,500.00 £ 12,000.00 £ 10,000.00 £ 27,500.00

Profit £ 1,500.00 -£ 2,000.00 £ 2,500.00 £ 2,000.00

It can be observed from the above calculation that if ‘The Director’ model is stopped,

producing the ‘Team’ desk model will result into profit amounting to £ 2,000. Therefore, it

would wold be worthwhile to produce ‘Team’ desk model for the business.

profit. Therefore, rather than closing down the division the management shall try to control

the cost, wherever possible for increasing the profit. For instance, cost of production can be

controlled with new technology of machines (Eldenburg et al. 2016).

Decision making through cost information (Scenario 2)

(i) If production of the Director desk is stopped the resultant profit will be as

below –

Particulars Executive Director Manager Total

Sales £ 25,000.00 £ - £ 30,000.00 £ 75,000.00

Variable costs £ 15,000.00 £ - £ 17,500.00 £ 45,000.00

Contribution £ 10,000.00 £ - £ 12,500.00 £ 30,000.00

Fixed Costs £ 8,500.00 £ 9,000.00 £ 10,000.00 £ 27,500.00

Profit £ 1,500.00 -£ 9,000.00 £ 2,500.00 -£ 5,000.00

It can be found that if the company stops producing ‘The Director’ desk the loss of the

company will be amounted to £ 5,000 from profit of £ 2,500. Therfeore, the company shall not stop

producing ‘The Director’ desk.

(ii) Production of ‘Team’ desk module

Particulars Executive Team Manager Total

Sales £ 25,000.00 £ 25,000.00 £ 30,000.00 £ 75,000.00

Variable costs £ 15,000.00 £ 15,000.00 £ 17,500.00 £ 45,000.00

Contribution £ 10,000.00 £ 10,000.00 £ 12,500.00 £ 30,000.00

Fixed Costs £ 8,500.00 £ 12,000.00 £ 10,000.00 £ 27,500.00

Profit £ 1,500.00 -£ 2,000.00 £ 2,500.00 £ 2,000.00

It can be observed from the above calculation that if ‘The Director’ model is stopped,

producing the ‘Team’ desk model will result into profit amounting to £ 2,000. Therefore, it

would wold be worthwhile to produce ‘Team’ desk model for the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR ADMINISTRATIVE MANAGERS

Activity 2

Using of budget in business

Budget is the projection of expenses and revenues over the specific period of time in

future. It is compiled and re-assessed on periodic basis. On the other hand, budgetary control

is the technique under which the actual spending and incomes are compared with the

projected spending and income. Based on the deviations among the actual and projections the

management make changes in the plans (Kwakye and Owoo 2014). Budgetary control

techniques used for planning and controlling the finances are cash budget, sales budget,

production budget and capital budget. Requirements of efficient budgetary controls are –

Quick reporting – subordinates shall send the performance reports on time. The

managers shall immediately analyse the report and take necessary actions.

Effective organization – the responsibilities and concerns of each managers shall be

organized efficiently

Reward and punishment – the employees who performs as per the budget shall be

rewarded and the underperformed employees shall be punished accordingly.

Support from the top management – top management shall have clear idea regarding

the budgetary control and must implement that for infusing the sense of seriousness

among subordinates (Brigham et al. 2016).

Preparation of various budgets

Details of various budgets used to control and plan finance and relationship among them

are as follows –

Cash budget – it reveals the projected payments and receipts under the budget period

and determines the cash position of the company. It shows the requirements of cash at

Activity 2

Using of budget in business

Budget is the projection of expenses and revenues over the specific period of time in

future. It is compiled and re-assessed on periodic basis. On the other hand, budgetary control

is the technique under which the actual spending and incomes are compared with the

projected spending and income. Based on the deviations among the actual and projections the

management make changes in the plans (Kwakye and Owoo 2014). Budgetary control

techniques used for planning and controlling the finances are cash budget, sales budget,

production budget and capital budget. Requirements of efficient budgetary controls are –

Quick reporting – subordinates shall send the performance reports on time. The

managers shall immediately analyse the report and take necessary actions.

Effective organization – the responsibilities and concerns of each managers shall be

organized efficiently

Reward and punishment – the employees who performs as per the budget shall be

rewarded and the underperformed employees shall be punished accordingly.

Support from the top management – top management shall have clear idea regarding

the budgetary control and must implement that for infusing the sense of seriousness

among subordinates (Brigham et al. 2016).

Preparation of various budgets

Details of various budgets used to control and plan finance and relationship among them

are as follows –

Cash budget – it reveals the projected payments and receipts under the budget period

and determines the cash position of the company. It shows the requirements of cash at

5FINANCE FOR ADMINISTRATIVE MANAGERS

different times under the budget period and assists the management in arranging and

planning the payments required for business operation. Therefore, it assures that the

business operation never suffer the shortage of cash. Apart from this, cash budget

assists in coordinating and controlling the cash payments and cash receipts (Chen,

Weikart and Williams 2014).

Sales budget – the sales budget provides idea regarding the plan and programme of

comprehensive sales for the specific period. It reveals the potential of sales with

regard to values, quantities, products and period. Sales budget plays important role in

preparing other budgets. Various factors taken into consideration while preparing the

sales budget are purchasing power of the customers, competition level, economic

status, past sales records and demand trend for the product.

Capital budget – it gives the projections regarding the capital resources of the

business. It reveals the plans of projected cost for the purposes of replacement,

expansion and investment. Therefore, the capital budget plays important role in

planning the capital expenditure (Hashim and Piatti 2016).

Production budget – the production budget that is also known as the output budget is

prepared on the basis of production budget. It shows the estimated cost for carrying

out plans associated with production. The production budget is segregated further

into material budget, labour budget and overhead budget.

Budgets and budgetary control

Details of various budgetary techniques used to control and plan finance are as follows –

Variance analysis – under the variance analysis the actual payments or receipts are

compared with the budget and the variances are found out. The variance can be

favourable as well as unfavourable. For instance, if the actual usage of raw material is

more than the budget it will have unfavourable variance. On the contrary, if the actual

different times under the budget period and assists the management in arranging and

planning the payments required for business operation. Therefore, it assures that the

business operation never suffer the shortage of cash. Apart from this, cash budget

assists in coordinating and controlling the cash payments and cash receipts (Chen,

Weikart and Williams 2014).

Sales budget – the sales budget provides idea regarding the plan and programme of

comprehensive sales for the specific period. It reveals the potential of sales with

regard to values, quantities, products and period. Sales budget plays important role in

preparing other budgets. Various factors taken into consideration while preparing the

sales budget are purchasing power of the customers, competition level, economic

status, past sales records and demand trend for the product.

Capital budget – it gives the projections regarding the capital resources of the

business. It reveals the plans of projected cost for the purposes of replacement,

expansion and investment. Therefore, the capital budget plays important role in

planning the capital expenditure (Hashim and Piatti 2016).

Production budget – the production budget that is also known as the output budget is

prepared on the basis of production budget. It shows the estimated cost for carrying

out plans associated with production. The production budget is segregated further

into material budget, labour budget and overhead budget.

Budgets and budgetary control

Details of various budgetary techniques used to control and plan finance are as follows –

Variance analysis – under the variance analysis the actual payments or receipts are

compared with the budget and the variances are found out. The variance can be

favourable as well as unfavourable. For instance, if the actual usage of raw material is

more than the budget it will have unfavourable variance. On the contrary, if the actual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR ADMINISTRATIVE MANAGERS

usage of raw material is less than the budget it will have favourable variance (Glantz,

Slinker and Neilands 2016).

Zero based budgeting – it is one of the most popular budgetary control techniques as

the next period’s budget is prepared on zero bases. Therefore, the difference among

the actual and budget will be nil. If any excess is fount that is adjusted. With the help

of this budget every dollar that is spent can be controlled. It is based on the current

year’s income (Callaghan, Hawke and Mignerey 2014).

Limitations of budget

Limitations of budgets are as follows –

It only provides estimates and therefore, the outcomes cannot be measured reliably

It can be used as a technique to hide the inefficiencies of the management. Boosting

the expenses deliberately and ignoring the important items are common practice.

Budget put psychological pressures and therefore restricts the freedom of action.

It leads to inflexibility as the mentioned figures are not the final figures. With the

changes in price there is change in estimation (Schick 2015).

usage of raw material is less than the budget it will have favourable variance (Glantz,

Slinker and Neilands 2016).

Zero based budgeting – it is one of the most popular budgetary control techniques as

the next period’s budget is prepared on zero bases. Therefore, the difference among

the actual and budget will be nil. If any excess is fount that is adjusted. With the help

of this budget every dollar that is spent can be controlled. It is based on the current

year’s income (Callaghan, Hawke and Mignerey 2014).

Limitations of budget

Limitations of budgets are as follows –

It only provides estimates and therefore, the outcomes cannot be measured reliably

It can be used as a technique to hide the inefficiencies of the management. Boosting

the expenses deliberately and ignoring the important items are common practice.

Budget put psychological pressures and therefore restricts the freedom of action.

It leads to inflexibility as the mentioned figures are not the final figures. With the

changes in price there is change in estimation (Schick 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR ADMINISTRATIVE MANAGERS

Activity 3

Financial statements prepared by Tesco Plc

Main financial statements prepared by Tesco Plc and their purposes are as follows –

Income statement – it reports the expenses and revenues of the company. The costs of

sales are deducted from revenue to show the gross profit. Further the operating

expenses, financial expenses and tax expenses are deducted from the gross profit to

show the net profit or loss for the period.

Balance sheet – it shows the assets of the company along with the liabilities and

owners equity of the company. The assets and liabilities are segregated among current

and non-current. As the balance sheet is prepared on particular time period it states

the financial position if the company at particular period of time (Tesco plc 2018).

Statements of changes in equity – this statement presents the shareholder’s equity

along with the payment of dividend. This statement is used to see whether the asset of

the company is majorly financed through equity as against debt.

Cash flow statement – cash flow statement of the company is segregated into

operating activities, investing activities and financing activities. It shows the cash

inflows and cash outflows of the company which is important to plan the payment

structure and allocation of cash resources for major expenses (Tesco plc 2018).

Ratio analysis

Ratio Formula 2017 2016

Profitability ratio

Gross profit ratio Gross profit/sales*100 5.19 5.27

Net profit margin Net profit/sales*100 -0.10 0.24

Efficiency ratio

Account receivable ratio sales/average receivables 38.82 28.93

Activity 3

Financial statements prepared by Tesco Plc

Main financial statements prepared by Tesco Plc and their purposes are as follows –

Income statement – it reports the expenses and revenues of the company. The costs of

sales are deducted from revenue to show the gross profit. Further the operating

expenses, financial expenses and tax expenses are deducted from the gross profit to

show the net profit or loss for the period.

Balance sheet – it shows the assets of the company along with the liabilities and

owners equity of the company. The assets and liabilities are segregated among current

and non-current. As the balance sheet is prepared on particular time period it states

the financial position if the company at particular period of time (Tesco plc 2018).

Statements of changes in equity – this statement presents the shareholder’s equity

along with the payment of dividend. This statement is used to see whether the asset of

the company is majorly financed through equity as against debt.

Cash flow statement – cash flow statement of the company is segregated into

operating activities, investing activities and financing activities. It shows the cash

inflows and cash outflows of the company which is important to plan the payment

structure and allocation of cash resources for major expenses (Tesco plc 2018).

Ratio analysis

Ratio Formula 2017 2016

Profitability ratio

Gross profit ratio Gross profit/sales*100 5.19 5.27

Net profit margin Net profit/sales*100 -0.10 0.24

Efficiency ratio

Account receivable ratio sales/average receivables 38.82 28.93

8FINANCE FOR ADMINISTRATIVE MANAGERS

Inventory turnover ratio COGS/Average inventories 22.41 18.97

Gearing ratio

Debt equity ratio

Total liabilities/shareholders

equity 6.15 4.10

Liquidity ratio

Current ratio Current assets/current liabilities 0.79 0.82

Profitability ratio – it is used to measure the profit earning capability of the company after

meeting its expenses from the revenues. The gross profit margin of the company is reduced

from 5.27% to 5.19% over the years from 2016 to 2017. On the other hand the company was

not able to generate positive income for the year 2017 that led to negative net profit margin

(Tesco plc 2018).

Efficiency ratio – it is used to measure the ability of the company to utilise the assets and

managing the liabilities efficiently. Both the efficiency ratios of the company are better in

2017 as compared to 2016. Therefore, the company has increased its efficiency (Vogel 2014).

Gearing ratio – it states the proportion of the assets raised through borrowing and the

proportion raised through owner’s equity. If 0.40 portion of assets or lower than that is raised

through debt the company is considered as lower leveraged. However, the company is

significantly leveraged as the debt equity ratio has been increased from 4.10 to 6.15 (Tesco

plc 2018).

Liquidity ratio – it reveals the ability of the company to meet the short term obligations with

the short term assets. It can be identified that the liquidity position of the company has been

deteriorated as the current ratio has been reduced from 0.82 to 0.79 (Delen, Kuzey and Uyar

2013).

Inventory turnover ratio COGS/Average inventories 22.41 18.97

Gearing ratio

Debt equity ratio

Total liabilities/shareholders

equity 6.15 4.10

Liquidity ratio

Current ratio Current assets/current liabilities 0.79 0.82

Profitability ratio – it is used to measure the profit earning capability of the company after

meeting its expenses from the revenues. The gross profit margin of the company is reduced

from 5.27% to 5.19% over the years from 2016 to 2017. On the other hand the company was

not able to generate positive income for the year 2017 that led to negative net profit margin

(Tesco plc 2018).

Efficiency ratio – it is used to measure the ability of the company to utilise the assets and

managing the liabilities efficiently. Both the efficiency ratios of the company are better in

2017 as compared to 2016. Therefore, the company has increased its efficiency (Vogel 2014).

Gearing ratio – it states the proportion of the assets raised through borrowing and the

proportion raised through owner’s equity. If 0.40 portion of assets or lower than that is raised

through debt the company is considered as lower leveraged. However, the company is

significantly leveraged as the debt equity ratio has been increased from 4.10 to 6.15 (Tesco

plc 2018).

Liquidity ratio – it reveals the ability of the company to meet the short term obligations with

the short term assets. It can be identified that the liquidity position of the company has been

deteriorated as the current ratio has been reduced from 0.82 to 0.79 (Delen, Kuzey and Uyar

2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE FOR ADMINISTRATIVE MANAGERS

From the ratio analysis it is further analysed that as the company is highly leveraged,

further borrowing can lead the company to unsustainable position. Therefore, in case of fund

requirement it shall raise through equity instead of debt.

From the ratio analysis it is further analysed that as the company is highly leveraged,

further borrowing can lead the company to unsustainable position. Therefore, in case of fund

requirement it shall raise through equity instead of debt.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR ADMINISTRATIVE MANAGERS

Reference

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

Callaghan, S., Hawke, K. and Mignerey, C., 2014. Five myths (and realities) about zero-

based budgeting. McKinsey & Company, p.2.

Chen, G.G., Weikart, L.A. and Williams, D.W., 2014. Budget tools: Financial methods in the

public sector. CQ Press.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Eldenburg, L.G., Wolcott, S.K., Chen, L.H. and Cook, G., 2016. Cost management:

Measuring, monitoring, and motivating performance. Wiley Global Education.

Glantz, S.A., Slinker, B.K. and Neilands, T.B., 2016. Primer of applied regression &

analysis of variance. McGraw-Hill Medical Publishing Division.

Hashim, A. and Piatti, M., 2016. A Diagnostic Framework to Assess the Capacity of a

Government's Financial Management Information System as a Budget Management Tool.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Kwakye, J.K. and Owoo, N., 2014. Righting the Ills of Budget Preparation, Implementation

and Oversight in Ghana.

Reference

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

Callaghan, S., Hawke, K. and Mignerey, C., 2014. Five myths (and realities) about zero-

based budgeting. McKinsey & Company, p.2.

Chen, G.G., Weikart, L.A. and Williams, D.W., 2014. Budget tools: Financial methods in the

public sector. CQ Press.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Eldenburg, L.G., Wolcott, S.K., Chen, L.H. and Cook, G., 2016. Cost management:

Measuring, monitoring, and motivating performance. Wiley Global Education.

Glantz, S.A., Slinker, B.K. and Neilands, T.B., 2016. Primer of applied regression &

analysis of variance. McGraw-Hill Medical Publishing Division.

Hashim, A. and Piatti, M., 2016. A Diagnostic Framework to Assess the Capacity of a

Government's Financial Management Information System as a Budget Management Tool.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Kwakye, J.K. and Owoo, N., 2014. Righting the Ills of Budget Preparation, Implementation

and Oversight in Ghana.

11FINANCE FOR ADMINISTRATIVE MANAGERS

Schick, A., 2015. The road to PPB: The stages of budget reform. In Public Budgeting (pp. 39-

56). Routledge.

Tesco plc. 2018. Tesco PLC. [online] Available at: https://www.tescoplc.com/ [Accessed 21

Jun. 2018].

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Schick, A., 2015. The road to PPB: The stages of budget reform. In Public Budgeting (pp. 39-

56). Routledge.

Tesco plc. 2018. Tesco PLC. [online] Available at: https://www.tescoplc.com/ [Accessed 21

Jun. 2018].

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.