ACC00716 Finance: Evaluating Pinto Limited's Project Viability

VerifiedAdded on 2023/06/12

|10

|1752

|461

Case Study

AI Summary

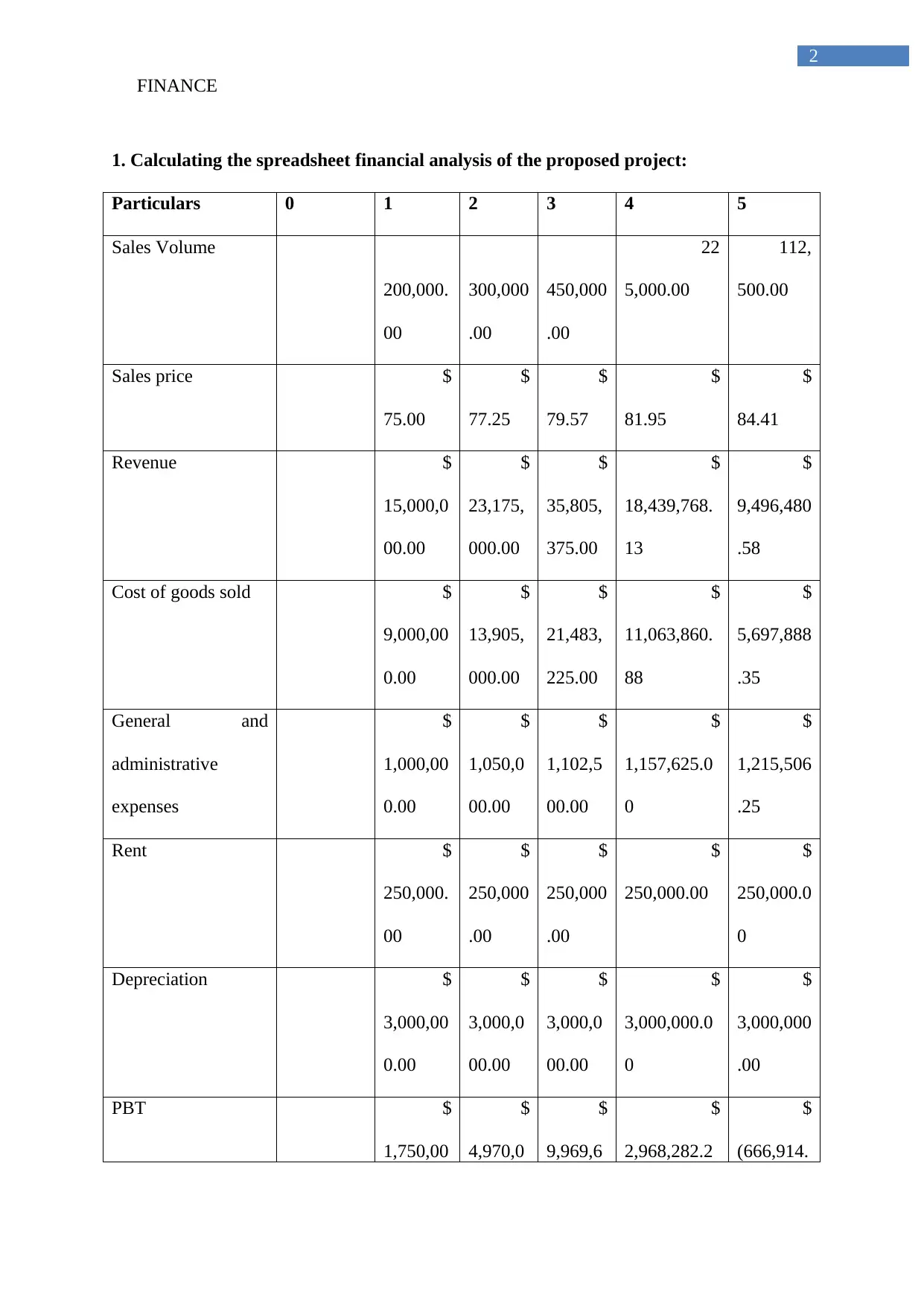

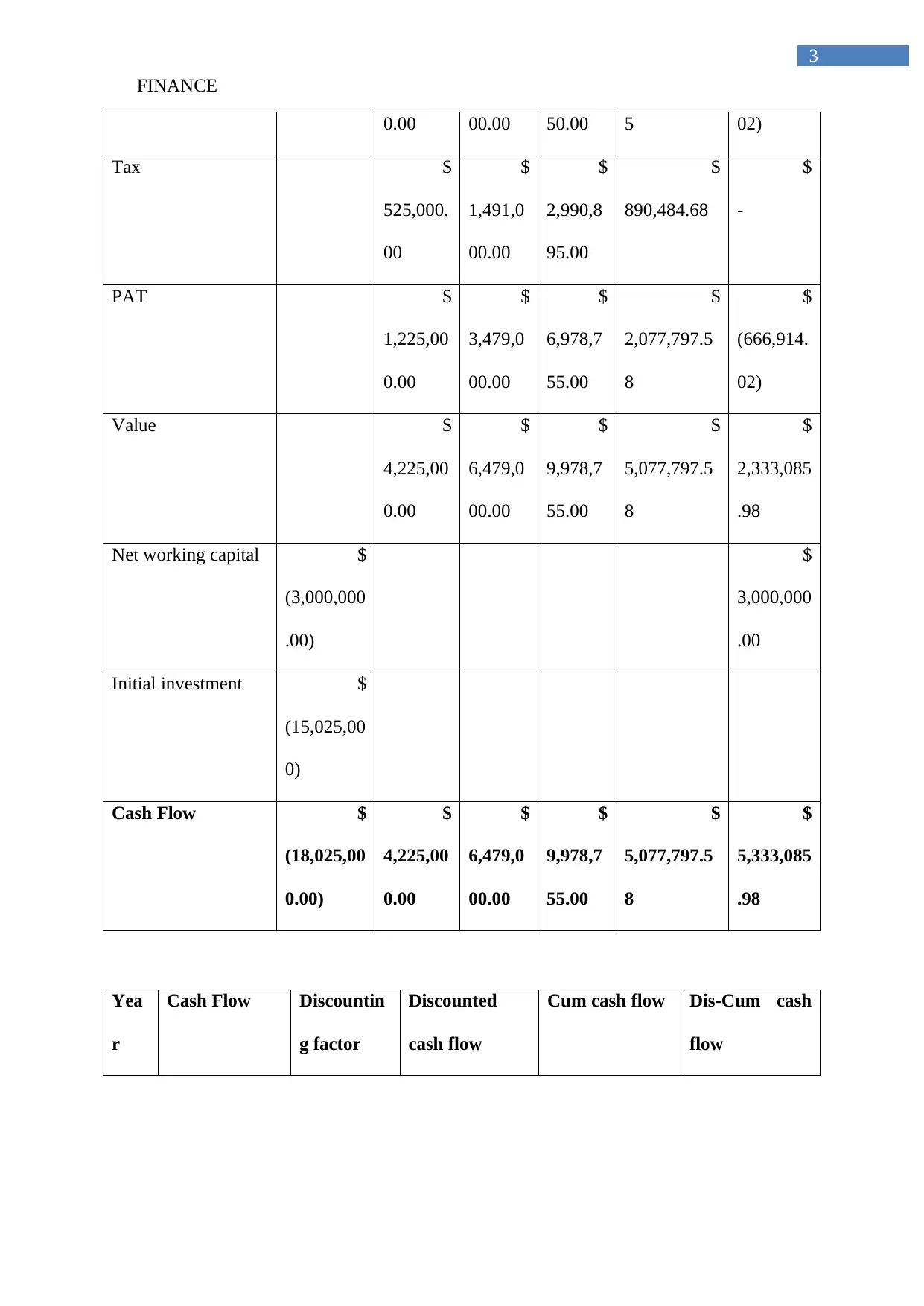

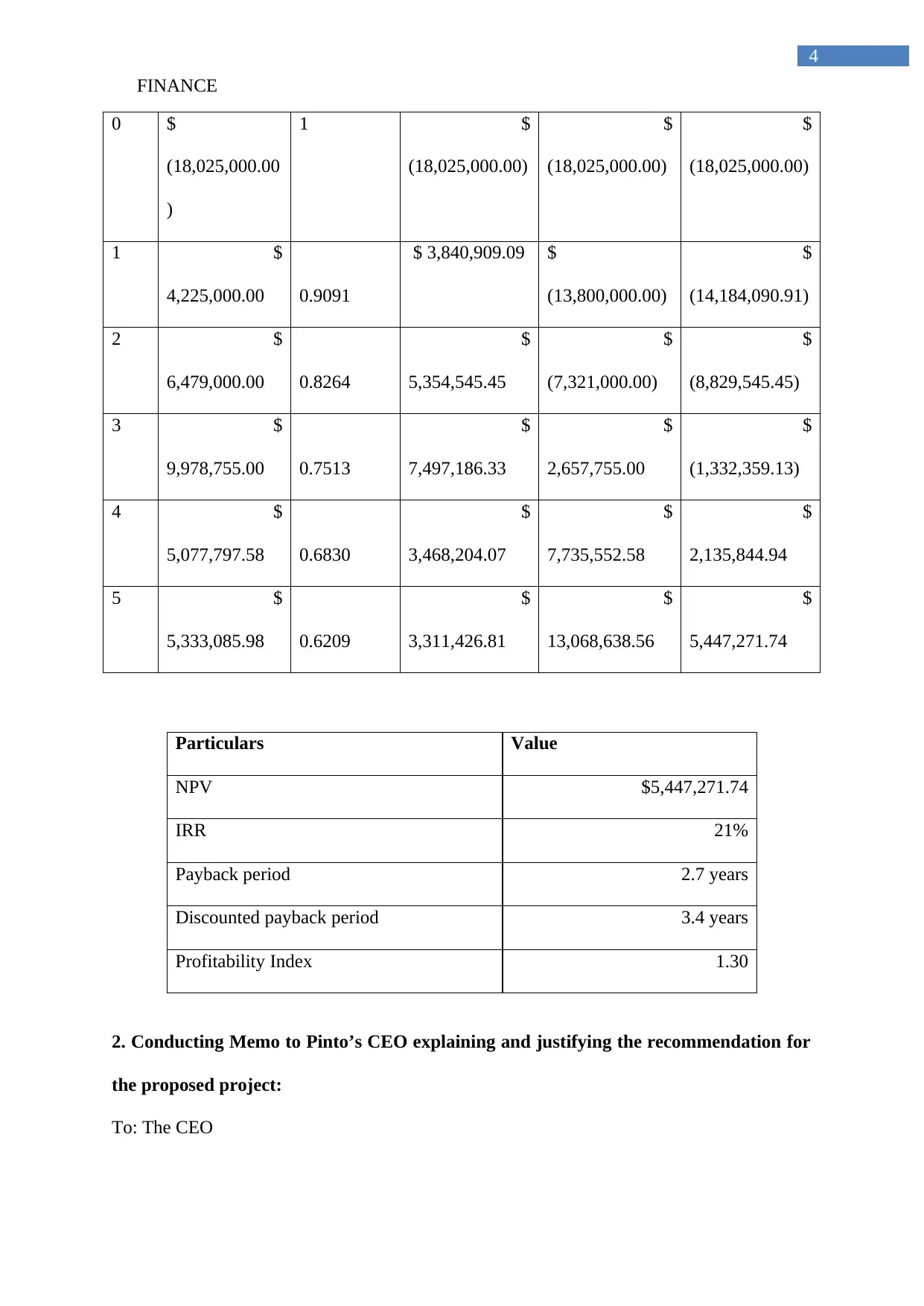

This case study provides a financial analysis of Pinto Limited's proposed project, evaluating its viability using investment appraisal techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), payback period, discounted payback period, and profitability index. The analysis includes calculations of cash flows over a five-year period, considering sales volume, sales price, cost of goods sold, administrative expenses, rent, and depreciation. A memo to the CEO recommends the project based on a positive NPV of $5,447,271.74, an IRR of 21%, a payback period of 2.7 years, and a profitability index of 1.30. Sensitivity analysis, including optimistic and pessimistic scenarios, is also conducted to assess the project's resilience to changes in sales volume and price. The analysis concludes that the project is financially viable and should be pursued to improve the firm's value.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.