Introduction to Finance and Financial Analysis of Liverton Co.

VerifiedAdded on 2023/06/04

|16

|3833

|173

AI Summary

This report includes the financial analysis of Liverton Co.'s business income statements, calculation of ratio and their analysis, and financial statements. It also covers break-even point and sales revenue calculation, margin of safety, and new strategies for the company. Additionally, it includes the calculation of payback period, net present value, and average rate of return.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Introduction to

Finance

Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................3

Question 1........................................................................................................................................3

A) Calculation of the ratios of Liverton Co.'s with their interpretation for the year 2019 and

2018:............................................................................................................................................3

B) Analysis of financial statements.............................................................................................5

Question 2........................................................................................................................................5

A) Opening statements of the financial position at the starting of July.......................................5

B) Prepare a monthly cash flow forecast.....................................................................................7

C) Additional Expenditure...........................................................................................................7

Question 3 .......................................................................................................................................7

A) Break-even point and sales revenue calculation for the year ended 2019 and 2020..............7

B) Margin of safety......................................................................................................................9

C) New strategies that company can formed...............................................................................9

Question 4......................................................................................................................................10

(a) calculation of pay back period, Net present value and average rate of return......................10

B) Methods of Appraisal Technique..........................................................................................13

C) Capital Investment Appraisal Techniques............................................................................13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION ..........................................................................................................................3

Question 1........................................................................................................................................3

A) Calculation of the ratios of Liverton Co.'s with their interpretation for the year 2019 and

2018:............................................................................................................................................3

B) Analysis of financial statements.............................................................................................5

Question 2........................................................................................................................................5

A) Opening statements of the financial position at the starting of July.......................................5

B) Prepare a monthly cash flow forecast.....................................................................................7

C) Additional Expenditure...........................................................................................................7

Question 3 .......................................................................................................................................7

A) Break-even point and sales revenue calculation for the year ended 2019 and 2020..............7

B) Margin of safety......................................................................................................................9

C) New strategies that company can formed...............................................................................9

Question 4......................................................................................................................................10

(a) calculation of pay back period, Net present value and average rate of return......................10

B) Methods of Appraisal Technique..........................................................................................13

C) Capital Investment Appraisal Techniques............................................................................13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Finance refers to an effective management system which involves various activities like

lending, borrowing, investing, forecasting and saving. In the system of finance credit, money is

effectively utilized as the mean for many exchanges. Along with this in modern financial system

financial services, markets and instruments are also involved. Efficient finance system allows

smooth and appropriate process of funds investment, allocation (Belousova and et.al, 2019). The

main aim of this report is to analyse how finance help Liverton Co.'s business in their smooth

functioning of all the business operations and activities which help them in their financial

positions. Report includes the analyses of Liverton Co.'s business income statements.

Furthermore, report includes calculation of ratio and their analysis. Along with this report

includes analysis of Free Air Ltd revenue and Net present value which implies to be high

profitable for the projects of Scrap pit plc.

Question 1

A) Calculation of the ratios of Liverton Co.'s with their interpretation for the year 2019 and

2018:

Gross profit margin: It show the picture about how effectively business management is

generating revenue. If company generate higher revenue means company is more efficient and

manage their profit effectively.

(Sales – Cost of goods sold) *100 / sales

(3495 – 2182) *100 / 3495

37.57%

Interpretation of gross profit margin: In above case gross profit ratio of the company is

37.57% which is identical with the 38% that indicates better as a growing and develop sector and

company will get this only after reducing the cost of goods (Choudhury, 2018).

Assets Usage Ratio: This ratio analyse how effectively management of business use its assets at

its provision to make money and generate profit. It is also classifying into the efficient ratio

which is help business to earn sales incomes from their held assets which has monetary value

with the help of using net revenue with average of total assets.

Total sales / Average total assets

3495 (3812 + 2503) / 2

Finance refers to an effective management system which involves various activities like

lending, borrowing, investing, forecasting and saving. In the system of finance credit, money is

effectively utilized as the mean for many exchanges. Along with this in modern financial system

financial services, markets and instruments are also involved. Efficient finance system allows

smooth and appropriate process of funds investment, allocation (Belousova and et.al, 2019). The

main aim of this report is to analyse how finance help Liverton Co.'s business in their smooth

functioning of all the business operations and activities which help them in their financial

positions. Report includes the analyses of Liverton Co.'s business income statements.

Furthermore, report includes calculation of ratio and their analysis. Along with this report

includes analysis of Free Air Ltd revenue and Net present value which implies to be high

profitable for the projects of Scrap pit plc.

Question 1

A) Calculation of the ratios of Liverton Co.'s with their interpretation for the year 2019 and

2018:

Gross profit margin: It show the picture about how effectively business management is

generating revenue. If company generate higher revenue means company is more efficient and

manage their profit effectively.

(Sales – Cost of goods sold) *100 / sales

(3495 – 2182) *100 / 3495

37.57%

Interpretation of gross profit margin: In above case gross profit ratio of the company is

37.57% which is identical with the 38% that indicates better as a growing and develop sector and

company will get this only after reducing the cost of goods (Choudhury, 2018).

Assets Usage Ratio: This ratio analyse how effectively management of business use its assets at

its provision to make money and generate profit. It is also classifying into the efficient ratio

which is help business to earn sales incomes from their held assets which has monetary value

with the help of using net revenue with average of total assets.

Total sales / Average total assets

3495 (3812 + 2503) / 2

3495 / 3157.5 = 1.10 times

Interpretation of Assets Usage Ratio: The ideal assets usage ratio is 2.5 times or more but as

per above case ideal ratio is 1.10 times which is less as compared to the ideal ratio. This state

that company have to improve their ability of revenue generation and have to effectively use

their assets (Elheddad and et.al, 2021).

Current Ratio: This is also referring as liquidity ratio. This ratio analyses the ability of business

to pay off its all short-term debt obligations with its short term assets. It mainly measures how

business meet their short term obligations in less period of time.

Current assets / Current liability

1687 / 744 = 2.87 times

Interpretation of Current ratio: Ideal current ratio is 2:1 but in above case current ratio is 2.27

which is higher than the ideal ratio. This is the most appropriate and suitable in which business

has more current assets.

Acid Test Ratio: This ratio is also known as quick ratio. This ratio measures the short-term

assets of company to its short-term liability to analyse company has sufficient amount of cash to

pay its short term liabilities.

Acid test ratio = (Current assets – stock) / Current liability

= (1687 – 150) / 744

= 2.06 times

Interpretation of Acid test ratio: The ideal acid test ratio is 1:1 but as per above case acid test

ratio is 2.06 times is which more than ideal ratio and indicates more safe and accurate to meet all

short-term liabilities (Hasan, 2020).

Inventories holding period Ratio: This ratio is shows the number of days’ period for which a

company holds its inventory before sales. It measures how many days it takes for inventory to

shift in company.

Inventory holding period = (Average inventory / cost of goods sold) *365

= (150+102) / 2] / 2182*365

= (126+2183) * 365

= 21.08 days

Interpretation of Inventory holding period: Ideal inventory holding period is between 5 to 10

days in above case inventory holding period is 21.08 days which indicates that money is tied up

Interpretation of Assets Usage Ratio: The ideal assets usage ratio is 2.5 times or more but as

per above case ideal ratio is 1.10 times which is less as compared to the ideal ratio. This state

that company have to improve their ability of revenue generation and have to effectively use

their assets (Elheddad and et.al, 2021).

Current Ratio: This is also referring as liquidity ratio. This ratio analyses the ability of business

to pay off its all short-term debt obligations with its short term assets. It mainly measures how

business meet their short term obligations in less period of time.

Current assets / Current liability

1687 / 744 = 2.87 times

Interpretation of Current ratio: Ideal current ratio is 2:1 but in above case current ratio is 2.27

which is higher than the ideal ratio. This is the most appropriate and suitable in which business

has more current assets.

Acid Test Ratio: This ratio is also known as quick ratio. This ratio measures the short-term

assets of company to its short-term liability to analyse company has sufficient amount of cash to

pay its short term liabilities.

Acid test ratio = (Current assets – stock) / Current liability

= (1687 – 150) / 744

= 2.06 times

Interpretation of Acid test ratio: The ideal acid test ratio is 1:1 but as per above case acid test

ratio is 2.06 times is which more than ideal ratio and indicates more safe and accurate to meet all

short-term liabilities (Hasan, 2020).

Inventories holding period Ratio: This ratio is shows the number of days’ period for which a

company holds its inventory before sales. It measures how many days it takes for inventory to

shift in company.

Inventory holding period = (Average inventory / cost of goods sold) *365

= (150+102) / 2] / 2182*365

= (126+2183) * 365

= 21.08 days

Interpretation of Inventory holding period: Ideal inventory holding period is between 5 to 10

days in above case inventory holding period is 21.08 days which indicates that money is tied up

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

in the form of inventory for longer period of time. High inventory turnover is a better sign as it

shows the business ability to soak sudden spurts in demand (Islam and Ahmad, 2020).

Debt equity ratio: This ratio measures the business total liability with its shareholder equity.

Debt equity ratio which is high shows that company borrowed more funds from the capital

market. On the other side less debt equity ratio shows that all the assets are used at optimum

level and has low borrowed funds.

Debt equity ratio: Total debt / Total equity

= 170 / 2898

= 0.058 times.

Interpretation of Debt equity ratio: In above case debt equity is 0.058 which shows that

company has less borrowed funds and low risk.

B) Analysis of financial statements

Financial statements are a yearly statement which is divided into incomes and expenditures.

Financial statements main purpose is to reviewing and analysing financial statements of

company to make better decision for the better performance of business. It is also help in

showing the lending settlement with an impartial view of monetary well-being of business and

this can be highly beneficial for taking the selection of concerning leading. This statements

involves the profit statements, coins flow and stability sheets. This evaluation is done through the

executives, authorities corporation, workers and various persons who help in accounting

information of commercial firms. On the other hand, evaluation is conduct by outsiders with the

accession to post monetary statements. This will involve creditors, authorities, credit score. It

helps company's in taking proper care and appropriate selection for the improvement of

company's monetary role (Ledhem and Mekidiche, 2021).

Question 2

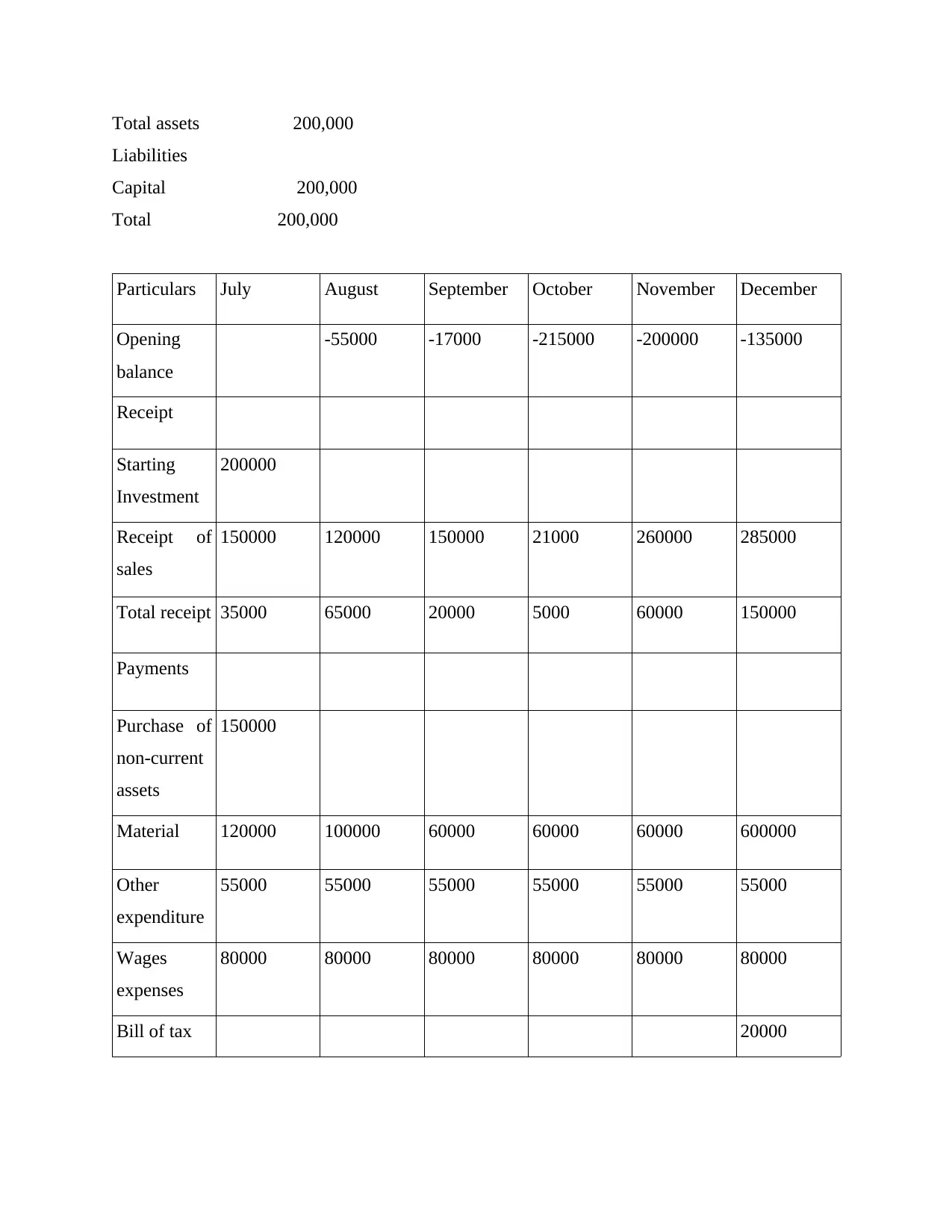

A) Opening statements of the financial position at the starting of July

Assets

Non-current assets

Tangible assets 150000

Current assets

Cash at bank 50000

shows the business ability to soak sudden spurts in demand (Islam and Ahmad, 2020).

Debt equity ratio: This ratio measures the business total liability with its shareholder equity.

Debt equity ratio which is high shows that company borrowed more funds from the capital

market. On the other side less debt equity ratio shows that all the assets are used at optimum

level and has low borrowed funds.

Debt equity ratio: Total debt / Total equity

= 170 / 2898

= 0.058 times.

Interpretation of Debt equity ratio: In above case debt equity is 0.058 which shows that

company has less borrowed funds and low risk.

B) Analysis of financial statements

Financial statements are a yearly statement which is divided into incomes and expenditures.

Financial statements main purpose is to reviewing and analysing financial statements of

company to make better decision for the better performance of business. It is also help in

showing the lending settlement with an impartial view of monetary well-being of business and

this can be highly beneficial for taking the selection of concerning leading. This statements

involves the profit statements, coins flow and stability sheets. This evaluation is done through the

executives, authorities corporation, workers and various persons who help in accounting

information of commercial firms. On the other hand, evaluation is conduct by outsiders with the

accession to post monetary statements. This will involve creditors, authorities, credit score. It

helps company's in taking proper care and appropriate selection for the improvement of

company's monetary role (Ledhem and Mekidiche, 2021).

Question 2

A) Opening statements of the financial position at the starting of July

Assets

Non-current assets

Tangible assets 150000

Current assets

Cash at bank 50000

Total assets 200,000

Liabilities

Capital 200,000

Total 200,000

Particulars July August September October November December

Opening

balance

-55000 -17000 -215000 -200000 -135000

Receipt

Starting

Investment

200000

Receipt of

sales

150000 120000 150000 21000 260000 285000

Total receipt 35000 65000 20000 5000 60000 150000

Payments

Purchase of

non-current

assets

150000

Material 120000 100000 60000 60000 60000 600000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages

expenses

80000 80000 80000 80000 80000 80000

Bill of tax 20000

Liabilities

Capital 200,000

Total 200,000

Particulars July August September October November December

Opening

balance

-55000 -17000 -215000 -200000 -135000

Receipt

Starting

Investment

200000

Receipt of

sales

150000 120000 150000 21000 260000 285000

Total receipt 35000 65000 20000 5000 60000 150000

Payments

Purchase of

non-current

assets

150000

Material 120000 100000 60000 60000 60000 600000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages

expenses

80000 80000 80000 80000 80000 80000

Bill of tax 20000

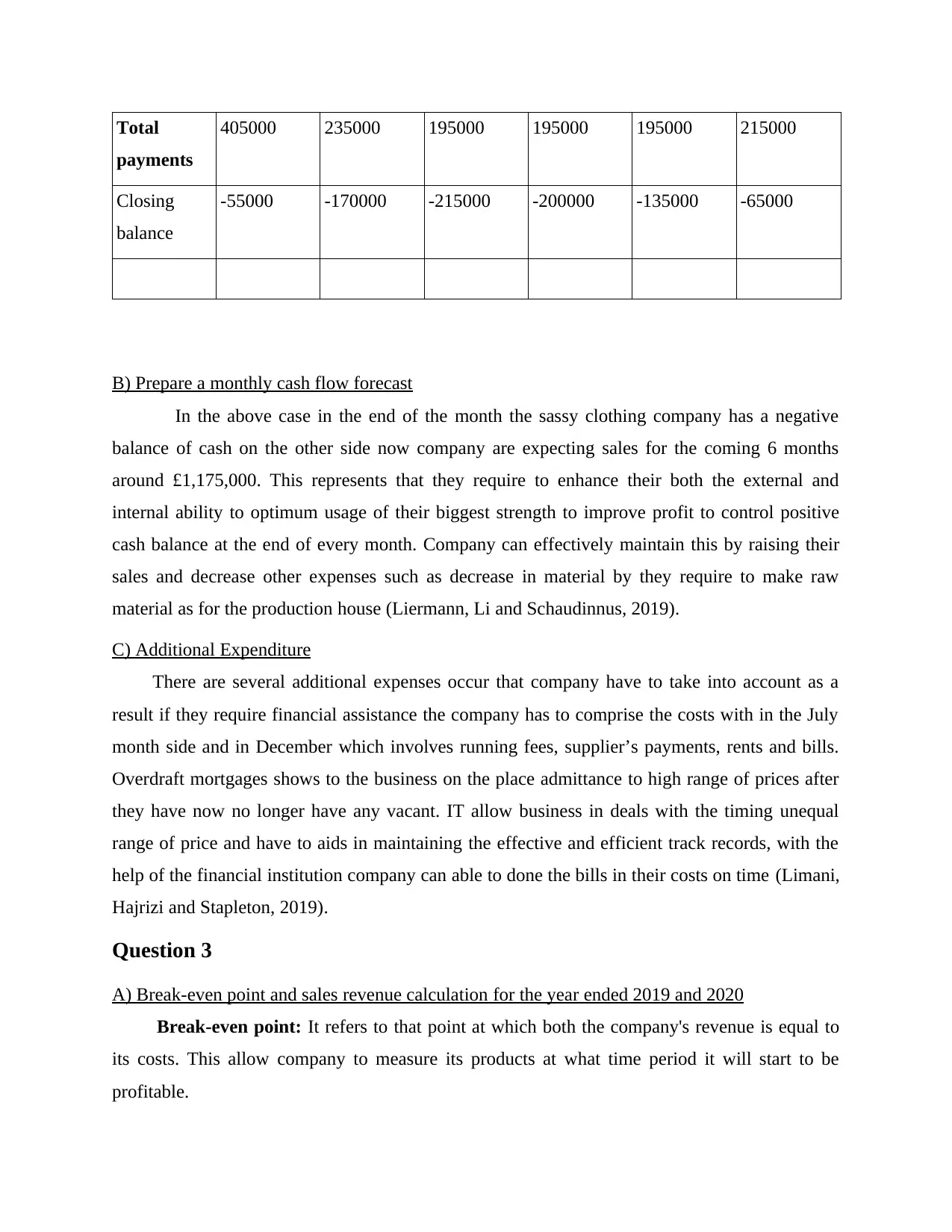

Total

payments

405000 235000 195000 195000 195000 215000

Closing

balance

-55000 -170000 -215000 -200000 -135000 -65000

B) Prepare a monthly cash flow forecast

In the above case in the end of the month the sassy clothing company has a negative

balance of cash on the other side now company are expecting sales for the coming 6 months

around £1,175,000. This represents that they require to enhance their both the external and

internal ability to optimum usage of their biggest strength to improve profit to control positive

cash balance at the end of every month. Company can effectively maintain this by raising their

sales and decrease other expenses such as decrease in material by they require to make raw

material as for the production house (Liermann, Li and Schaudinnus, 2019).

C) Additional Expenditure

There are several additional expenses occur that company have to take into account as a

result if they require financial assistance the company has to comprise the costs with in the July

month side and in December which involves running fees, supplier’s payments, rents and bills.

Overdraft mortgages shows to the business on the place admittance to high range of prices after

they have now no longer have any vacant. IT allow business in deals with the timing unequal

range of price and have to aids in maintaining the effective and efficient track records, with the

help of the financial institution company can able to done the bills in their costs on time (Limani,

Hajrizi and Stapleton, 2019).

Question 3

A) Break-even point and sales revenue calculation for the year ended 2019 and 2020

Break-even point: It refers to that point at which both the company's revenue is equal to

its costs. This allow company to measure its products at what time period it will start to be

profitable.

payments

405000 235000 195000 195000 195000 215000

Closing

balance

-55000 -170000 -215000 -200000 -135000 -65000

B) Prepare a monthly cash flow forecast

In the above case in the end of the month the sassy clothing company has a negative

balance of cash on the other side now company are expecting sales for the coming 6 months

around £1,175,000. This represents that they require to enhance their both the external and

internal ability to optimum usage of their biggest strength to improve profit to control positive

cash balance at the end of every month. Company can effectively maintain this by raising their

sales and decrease other expenses such as decrease in material by they require to make raw

material as for the production house (Liermann, Li and Schaudinnus, 2019).

C) Additional Expenditure

There are several additional expenses occur that company have to take into account as a

result if they require financial assistance the company has to comprise the costs with in the July

month side and in December which involves running fees, supplier’s payments, rents and bills.

Overdraft mortgages shows to the business on the place admittance to high range of prices after

they have now no longer have any vacant. IT allow business in deals with the timing unequal

range of price and have to aids in maintaining the effective and efficient track records, with the

help of the financial institution company can able to done the bills in their costs on time (Limani,

Hajrizi and Stapleton, 2019).

Question 3

A) Break-even point and sales revenue calculation for the year ended 2019 and 2020

Break-even point: It refers to that point at which both the company's revenue is equal to

its costs. This allow company to measure its products at what time period it will start to be

profitable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

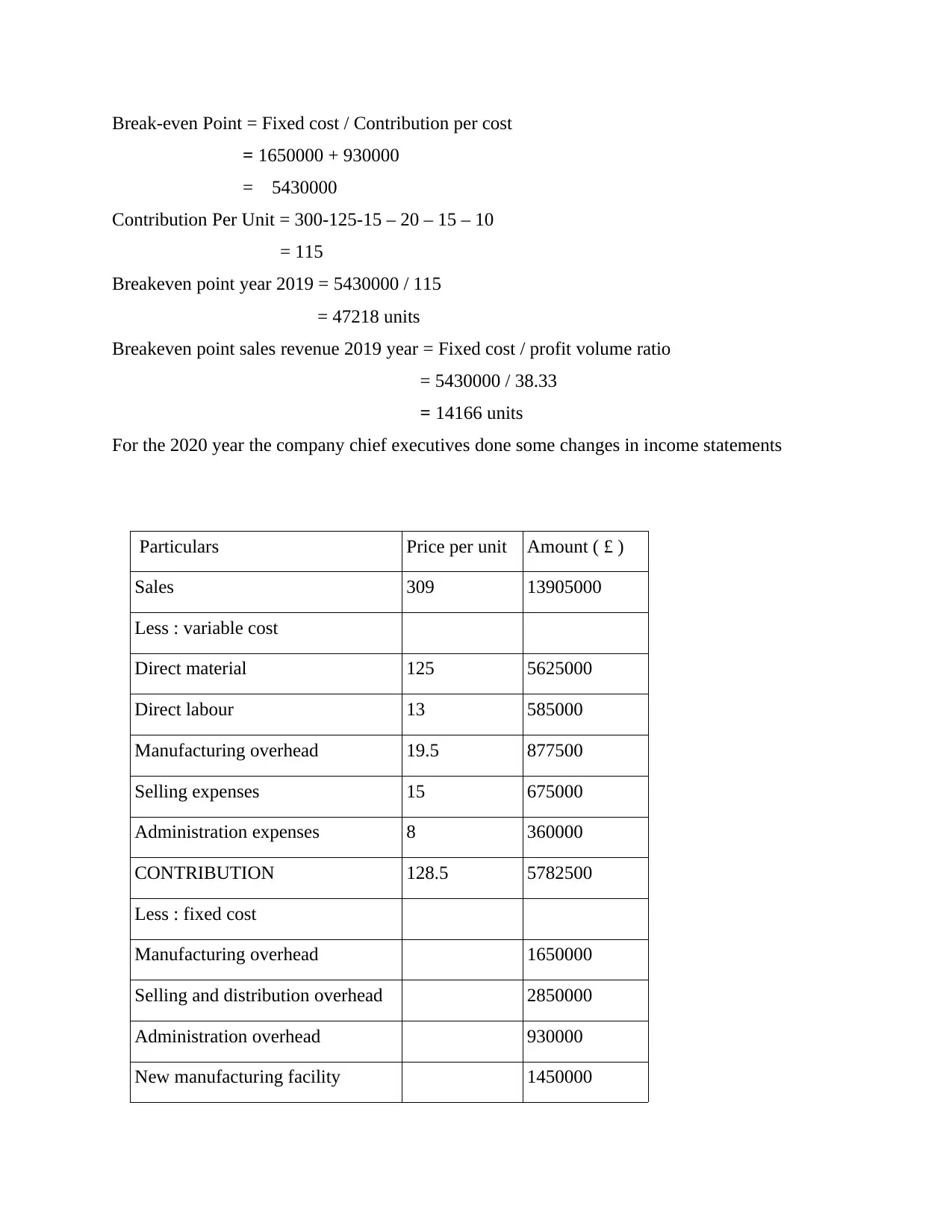

Break-even Point = Fixed cost / Contribution per cost

= 1650000 + 930000

= 5430000

Contribution Per Unit = 300-125-15 – 20 – 15 – 10

= 115

Breakeven point year 2019 = 5430000 / 115

= 47218 units

Breakeven point sales revenue 2019 year = Fixed cost / profit volume ratio

= 5430000 / 38.33

= 14166 units

For the 2020 year the company chief executives done some changes in income statements

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

= 1650000 + 930000

= 5430000

Contribution Per Unit = 300-125-15 – 20 – 15 – 10

= 115

Breakeven point year 2019 = 5430000 / 115

= 47218 units

Breakeven point sales revenue 2019 year = Fixed cost / profit volume ratio

= 5430000 / 38.33

= 14166 units

For the 2020 year the company chief executives done some changes in income statements

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

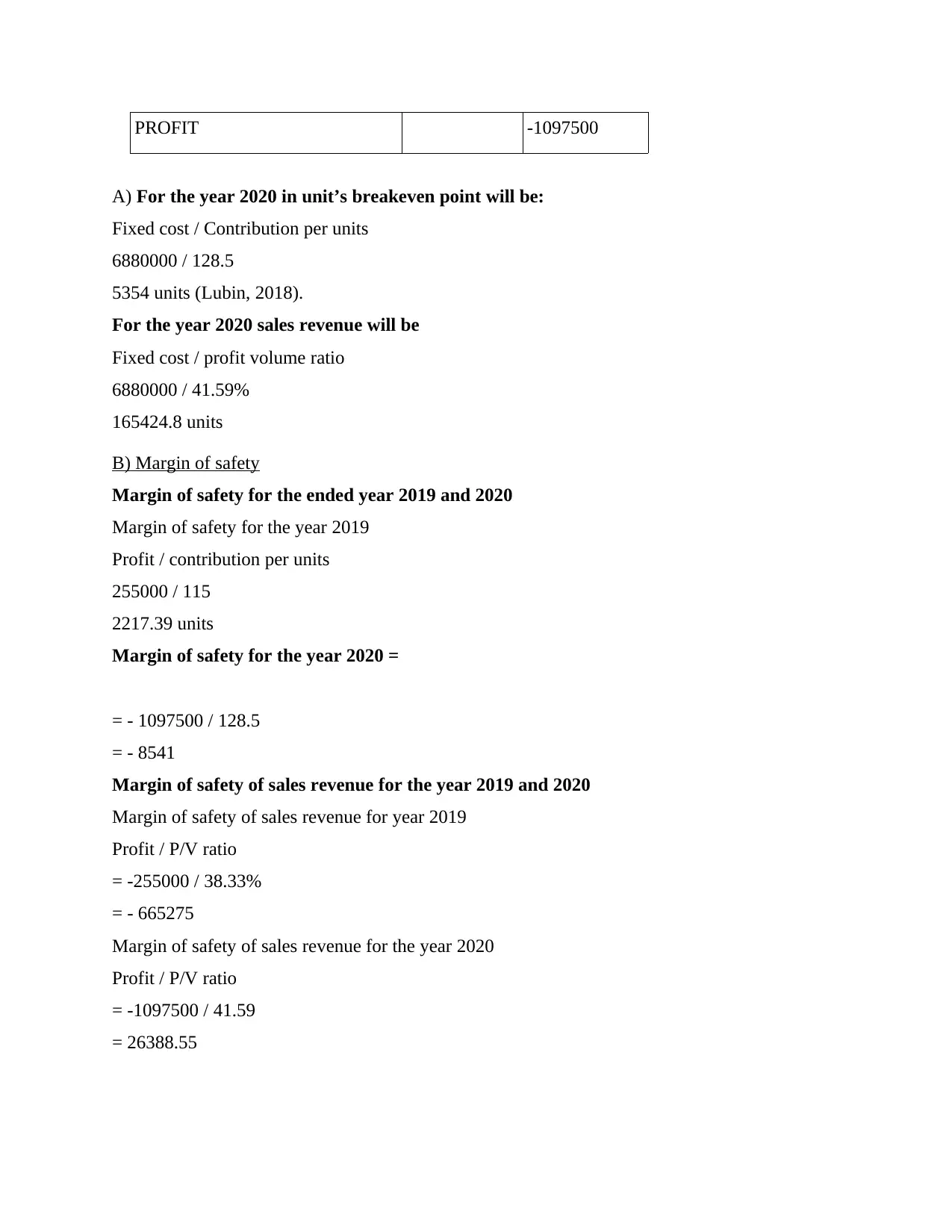

PROFIT -1097500

A) For the year 2020 in unit’s breakeven point will be:

Fixed cost / Contribution per units

6880000 / 128.5

5354 units (Lubin, 2018).

For the year 2020 sales revenue will be

Fixed cost / profit volume ratio

6880000 / 41.59%

165424.8 units

B) Margin of safety

Margin of safety for the ended year 2019 and 2020

Margin of safety for the year 2019

Profit / contribution per units

255000 / 115

2217.39 units

Margin of safety for the year 2020 =

= - 1097500 / 128.5

= - 8541

Margin of safety of sales revenue for the year 2019 and 2020

Margin of safety of sales revenue for year 2019

Profit / P/V ratio

= -255000 / 38.33%

= - 665275

Margin of safety of sales revenue for the year 2020

Profit / P/V ratio

= -1097500 / 41.59

= 26388.55

A) For the year 2020 in unit’s breakeven point will be:

Fixed cost / Contribution per units

6880000 / 128.5

5354 units (Lubin, 2018).

For the year 2020 sales revenue will be

Fixed cost / profit volume ratio

6880000 / 41.59%

165424.8 units

B) Margin of safety

Margin of safety for the ended year 2019 and 2020

Margin of safety for the year 2019

Profit / contribution per units

255000 / 115

2217.39 units

Margin of safety for the year 2020 =

= - 1097500 / 128.5

= - 8541

Margin of safety of sales revenue for the year 2019 and 2020

Margin of safety of sales revenue for year 2019

Profit / P/V ratio

= -255000 / 38.33%

= - 665275

Margin of safety of sales revenue for the year 2020

Profit / P/V ratio

= -1097500 / 41.59

= 26388.55

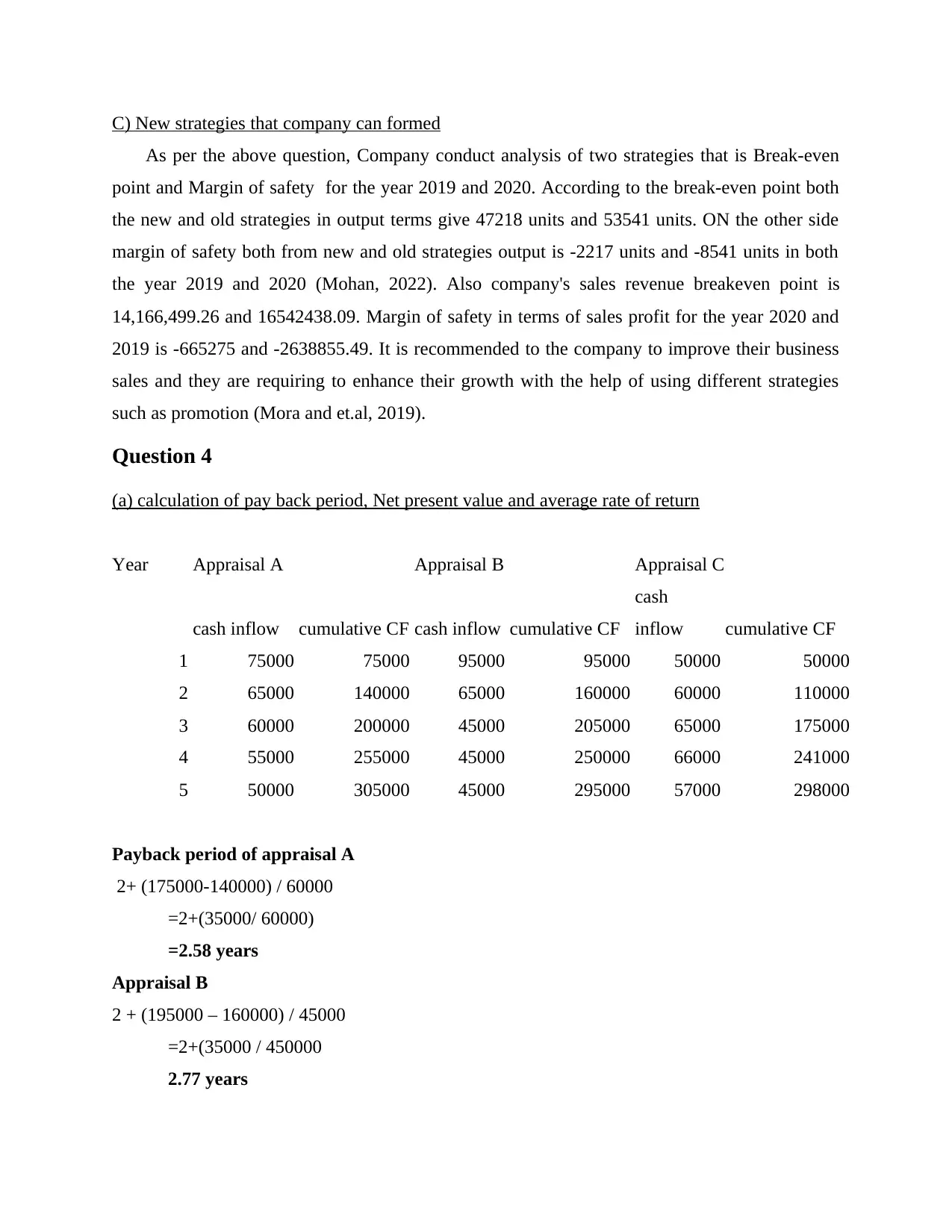

C) New strategies that company can formed

As per the above question, Company conduct analysis of two strategies that is Break-even

point and Margin of safety for the year 2019 and 2020. According to the break-even point both

the new and old strategies in output terms give 47218 units and 53541 units. ON the other side

margin of safety both from new and old strategies output is -2217 units and -8541 units in both

the year 2019 and 2020 (Mohan, 2022). Also company's sales revenue breakeven point is

14,166,499.26 and 16542438.09. Margin of safety in terms of sales profit for the year 2020 and

2019 is -665275 and -2638855.49. It is recommended to the company to improve their business

sales and they are requiring to enhance their growth with the help of using different strategies

such as promotion (Mora and et.al, 2019).

Question 4

(a) calculation of pay back period, Net present value and average rate of return

Year Appraisal A Appraisal B Appraisal C

cash inflow cumulative CF cash inflow cumulative CF

cash

inflow cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Payback period of appraisal A

2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

2 + (195000 – 160000) / 45000

=2+(35000 / 450000

2.77 years

As per the above question, Company conduct analysis of two strategies that is Break-even

point and Margin of safety for the year 2019 and 2020. According to the break-even point both

the new and old strategies in output terms give 47218 units and 53541 units. ON the other side

margin of safety both from new and old strategies output is -2217 units and -8541 units in both

the year 2019 and 2020 (Mohan, 2022). Also company's sales revenue breakeven point is

14,166,499.26 and 16542438.09. Margin of safety in terms of sales profit for the year 2020 and

2019 is -665275 and -2638855.49. It is recommended to the company to improve their business

sales and they are requiring to enhance their growth with the help of using different strategies

such as promotion (Mora and et.al, 2019).

Question 4

(a) calculation of pay back period, Net present value and average rate of return

Year Appraisal A Appraisal B Appraisal C

cash inflow cumulative CF cash inflow cumulative CF

cash

inflow cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Payback period of appraisal A

2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

2 + (195000 – 160000) / 45000

=2+(35000 / 450000

2.77 years

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

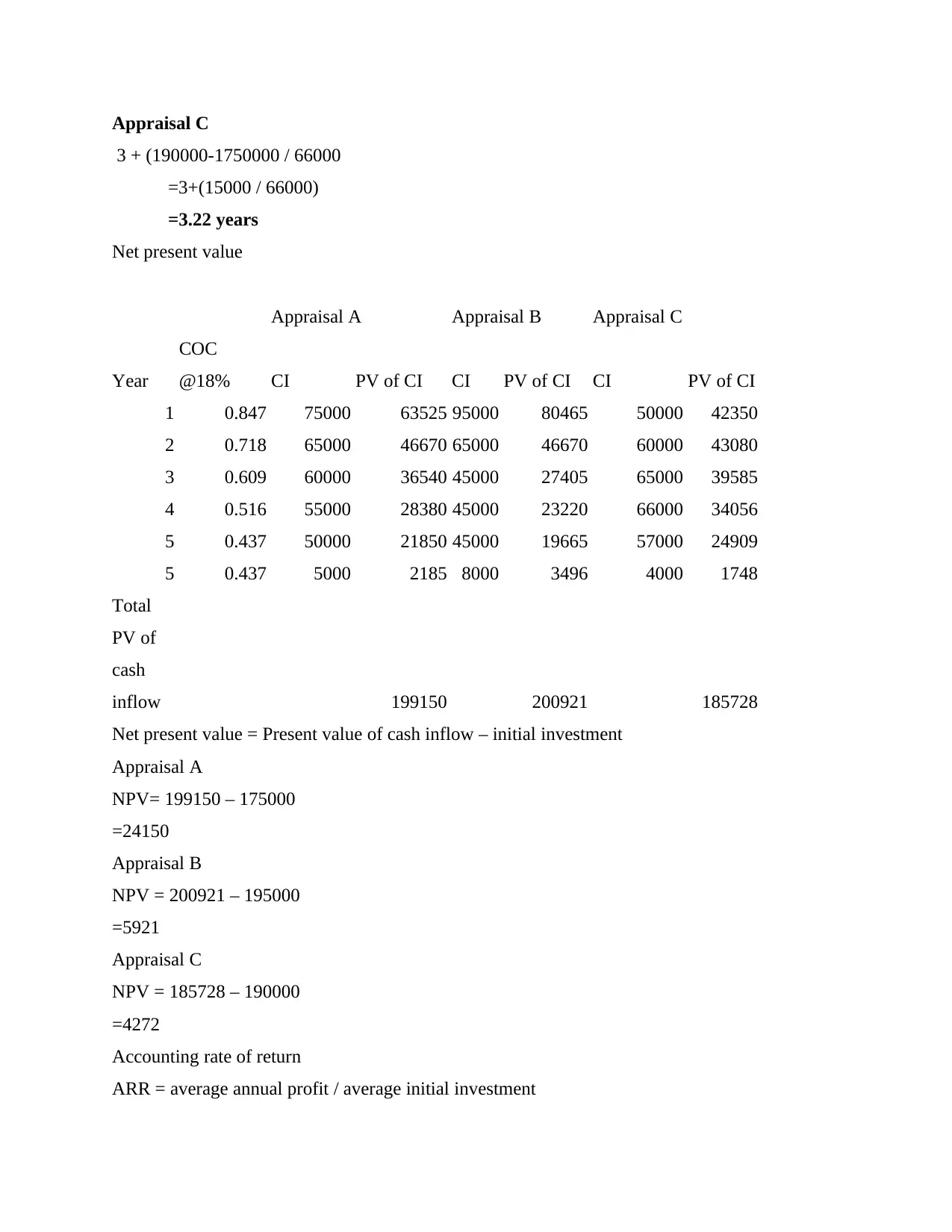

Appraisal C

3 + (190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

Net present value = Present value of cash inflow – initial investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=4272

Accounting rate of return

ARR = average annual profit / average initial investment

3 + (190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

Net present value = Present value of cash inflow – initial investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=4272

Accounting rate of return

ARR = average annual profit / average initial investment

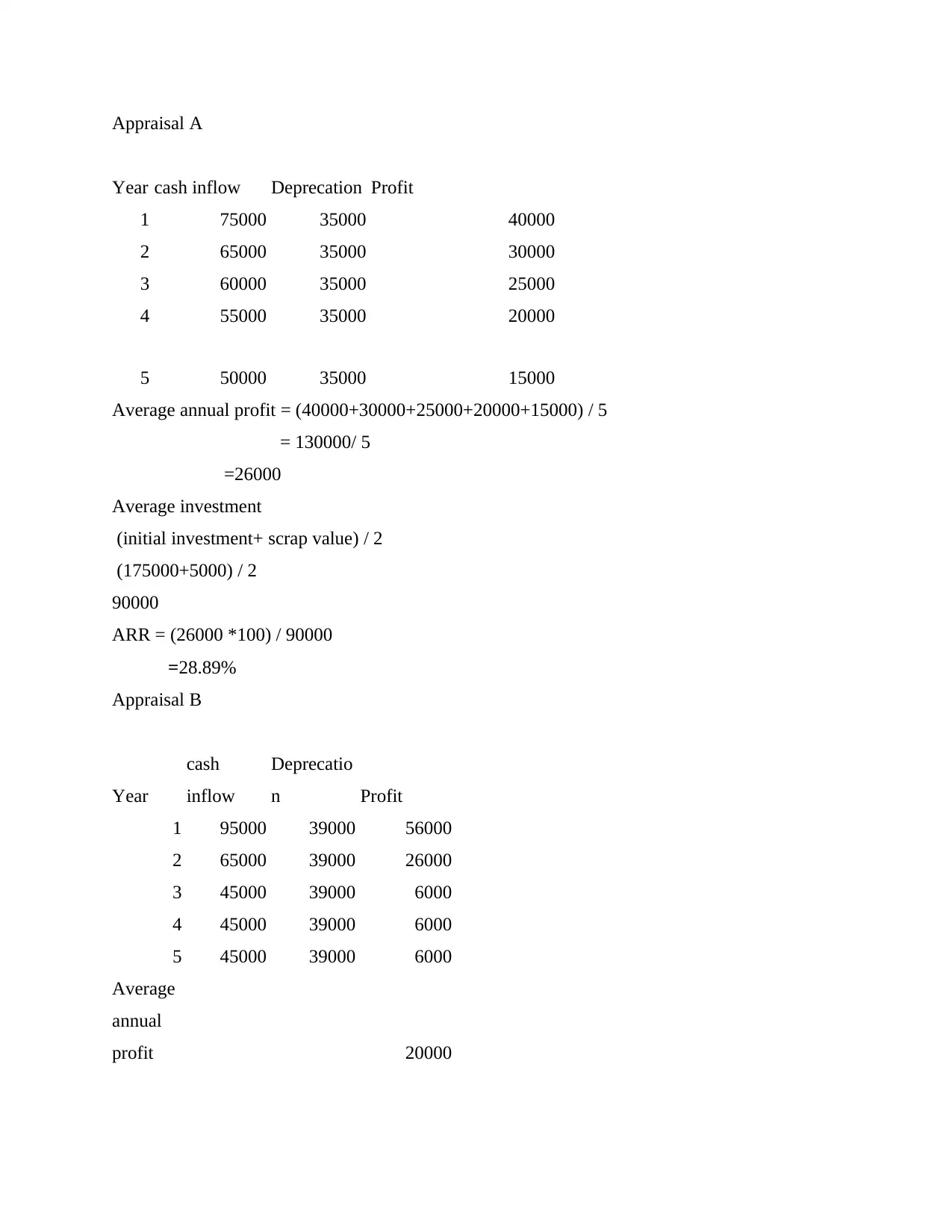

Appraisal A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

=26000

Average investment

(initial investment+ scrap value) / 2

(175000+5000) / 2

90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

Year

cash

inflow

Deprecatio

n Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average

annual

profit 20000

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

=26000

Average investment

(initial investment+ scrap value) / 2

(175000+5000) / 2

90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

Year

cash

inflow

Deprecatio

n Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average

annual

profit 20000

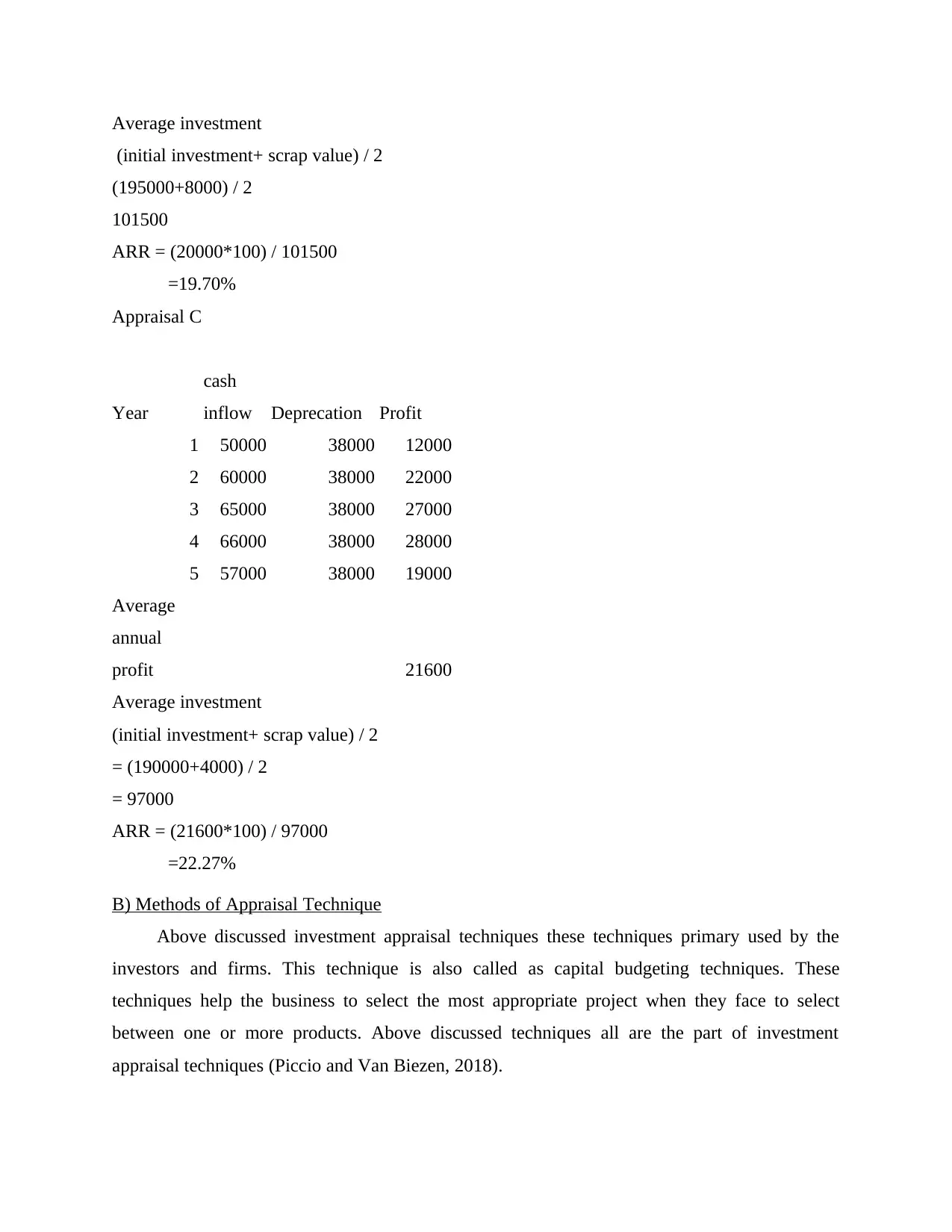

Average investment

(initial investment+ scrap value) / 2

(195000+8000) / 2

101500

ARR = (20000*100) / 101500

=19.70%

Appraisal C

Year

cash

inflow Deprecation Profit

1 50000 38000 12000

2 60000 38000 22000

3 65000 38000 27000

4 66000 38000 28000

5 57000 38000 19000

Average

annual

profit 21600

Average investment

(initial investment+ scrap value) / 2

= (190000+4000) / 2

= 97000

ARR = (21600*100) / 97000

=22.27%

B) Methods of Appraisal Technique

Above discussed investment appraisal techniques these techniques primary used by the

investors and firms. This technique is also called as capital budgeting techniques. These

techniques help the business to select the most appropriate project when they face to select

between one or more products. Above discussed techniques all are the part of investment

appraisal techniques (Piccio and Van Biezen, 2018).

(initial investment+ scrap value) / 2

(195000+8000) / 2

101500

ARR = (20000*100) / 101500

=19.70%

Appraisal C

Year

cash

inflow Deprecation Profit

1 50000 38000 12000

2 60000 38000 22000

3 65000 38000 27000

4 66000 38000 28000

5 57000 38000 19000

Average

annual

profit 21600

Average investment

(initial investment+ scrap value) / 2

= (190000+4000) / 2

= 97000

ARR = (21600*100) / 97000

=22.27%

B) Methods of Appraisal Technique

Above discussed investment appraisal techniques these techniques primary used by the

investors and firms. This technique is also called as capital budgeting techniques. These

techniques help the business to select the most appropriate project when they face to select

between one or more products. Above discussed techniques all are the part of investment

appraisal techniques (Piccio and Van Biezen, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

After analysing above techniques company should select project A for their business operations

in comparison to the other discussed projects. Company can choose project A because it provides

high return on investment as well as it effectively recovers the cost of investment in 2.58 years as

comparison to other project like project B recovers its cost of investment in 2.77 years and

Project C recover its cost of investment in 3.22 years. Appraisal1 net present value is 24150 on

the other side net present appraisal value are 4272 and 5921. Along with this Project A average

rate of return is 28.89%, project B average rate of return is 19.70 and project C average rate of

return is 22.27%

C) Capital Investment Appraisal Techniques

This technique is mainly used by the company management to take effective decision in regards

of project to take decision about the investment and how to finance them to achieve all the goals

of company. There are various ways to describe the capital budgeting decisions. Company

should choose that project which gives high profit and return of shareholders. There are various

capital investment appraisal techniques which are discussed below:

Payback Period: This period indicates the time require to cop up the original cash investment. It

states that total cash expenditure has to be equal to the duration of time require for the

cumulative total net cash flow from the investment. Investor can easily recover their investment

amount with the help of this method. There is various step that follow for calculating payback

period (Shanmuganathan, 2020).

Primary, analyse the project total cash flow

Calculate the estimated cash flow after the tax over the useful life of the project.

Advantages of Payback period

Simple: Payback period technique method is simple and effective as this method help the

company that don't have big amount of investment.

Quick solution: Payback period method is easy and effective to calculate. Owners can

efficiently able to calculate specific project payback period. This support the owner to make

accurate and fast decision, which is essential for the companies with scared resources.

Disadvantages of Payback period

Not considered time value of money: Pay back not considered the time value of money because

it is not give accurate and clear picture as which one project is highly appropriate among two or

more projects (Tsindeliani, 2019).

in comparison to the other discussed projects. Company can choose project A because it provides

high return on investment as well as it effectively recovers the cost of investment in 2.58 years as

comparison to other project like project B recovers its cost of investment in 2.77 years and

Project C recover its cost of investment in 3.22 years. Appraisal1 net present value is 24150 on

the other side net present appraisal value are 4272 and 5921. Along with this Project A average

rate of return is 28.89%, project B average rate of return is 19.70 and project C average rate of

return is 22.27%

C) Capital Investment Appraisal Techniques

This technique is mainly used by the company management to take effective decision in regards

of project to take decision about the investment and how to finance them to achieve all the goals

of company. There are various ways to describe the capital budgeting decisions. Company

should choose that project which gives high profit and return of shareholders. There are various

capital investment appraisal techniques which are discussed below:

Payback Period: This period indicates the time require to cop up the original cash investment. It

states that total cash expenditure has to be equal to the duration of time require for the

cumulative total net cash flow from the investment. Investor can easily recover their investment

amount with the help of this method. There is various step that follow for calculating payback

period (Shanmuganathan, 2020).

Primary, analyse the project total cash flow

Calculate the estimated cash flow after the tax over the useful life of the project.

Advantages of Payback period

Simple: Payback period technique method is simple and effective as this method help the

company that don't have big amount of investment.

Quick solution: Payback period method is easy and effective to calculate. Owners can

efficiently able to calculate specific project payback period. This support the owner to make

accurate and fast decision, which is essential for the companies with scared resources.

Disadvantages of Payback period

Not considered time value of money: Pay back not considered the time value of money because

it is not give accurate and clear picture as which one project is highly appropriate among two or

more projects (Tsindeliani, 2019).

Not considered projects profitability: It refers that payback period not effectively considered

project profitability it is basically considered inflow of cash up to the period till the original cost

of investment does not recovers.

Ignores the cash flow received after the payback period: Until the payback period has over

largest cash flow may not take place for some projects. May be due to these projects have high

investment return and project have short time for payback may be more preferable.

Average rate of return: It indicates to the rate of return percentage which is expected on

investment. In average rate of return, the average revenue of the asset of the company is divided

by the initial investment of the company. This ratio is calculated to know the expected return

during the lifetime of the asset. It is usually used when there are multiple projects. From different

projects, it provides different expected returns from various projects. It helps in calculating the

profitability of the business (Wang and et.al, 2020).

CONCLUSION

In this report the financial position of the Liver ton co. has been calculated. It is being calculated

with the help of the financial statements and the various ratios. These ratios include gross profit,

current ratio, debt equity, etc. Along with these the breakeven point and the margin of safety are

also calculated. The new strategies are formed according to the position being analysed by the

Liver-ton co. 's financial reports. The company has predicted the future returns with the help of

various analysis. Like average rate of return, net present value, payback period, etc.

project profitability it is basically considered inflow of cash up to the period till the original cost

of investment does not recovers.

Ignores the cash flow received after the payback period: Until the payback period has over

largest cash flow may not take place for some projects. May be due to these projects have high

investment return and project have short time for payback may be more preferable.

Average rate of return: It indicates to the rate of return percentage which is expected on

investment. In average rate of return, the average revenue of the asset of the company is divided

by the initial investment of the company. This ratio is calculated to know the expected return

during the lifetime of the asset. It is usually used when there are multiple projects. From different

projects, it provides different expected returns from various projects. It helps in calculating the

profitability of the business (Wang and et.al, 2020).

CONCLUSION

In this report the financial position of the Liver ton co. has been calculated. It is being calculated

with the help of the financial statements and the various ratios. These ratios include gross profit,

current ratio, debt equity, etc. Along with these the breakeven point and the margin of safety are

also calculated. The new strategies are formed according to the position being analysed by the

Liver-ton co. 's financial reports. The company has predicted the future returns with the help of

various analysis. Like average rate of return, net present value, payback period, etc.

REFERENCES

Books and Journals

Belousova and et.al, 2019. The financial literacy assessment among students majoring in the

field of finance. EurAsian Journal of BioSciences, 13(1). China's green finance and

economic growth. Resources Policy, 75. p.102476.

Choudhury, M.A., 2018. The ontological law of Tawhid contra ‘Shari’ah-compliance’in Islamic

portfolio finance. International Journal of Law and Management.

Elheddad and et.al, 2021. The effect of the Fourth Industrial Revolution on the environment: The

relationship between electronic finance and pollution in OECD countries. Technological

Forecasting and Social Change, 163. p.120485.

Hasan, Z., 2020. Risk and Islamic Finance: A Misconception Corrected. In handbook of research

on theory and practice of global Islamic finance (pp. 441-454). IGI Global.

Islam, R. and Ahmad, R., 2020. Applicability of Mudarabah and Musharakah as Islamic micro-

equity finance to underprivileged women in Malaysia. The European Journal of

Development Research, 32(1). pp.176-197.

Ledhem, M.A. and Mekidiche, M., 2021. Islamic finance and economic growth nexus: an

empirical evidence from Southeast Asia using dynamic panel one-step system GMM

analysis. Journal of Islamic Accounting and Business Research.

Liermann, V., Li, S. and Schaudinnus, N., 2019. Deep learning: An introduction. In The Impact

of Digital Transformation and Fintech on the Finance Professional (pp. 305-340). Palgrave

Macmillan, Cham.

Limani, Y., Hajrizi, E. and Stapleton, L., 2019. The Impact of Industry 4.0 on Advanced

Operations Management.

Lubin, D., 2018. Dance of the trillions: Developing countries and global finance. Brookings

Institution Press.

Mohan, P.S., 2022. Implementing nationally determined contributions under the Paris

agreement: an assessment of climate finance in Caribbean small island developing

states. Climate Policy. pp.1-9.

Mora and et.al, 2019. The effects of mean wind speed uncertainty on project finance debt sizing

for offshore wind farms. Applied Energy, 252. p.113419.

Piccio, D.R. and Van Biezen, I., 2018. Political finance and the cartel party thesis. In Handbook

of political party funding. Edward Elgar Publishing.

Shanmuganathan, M., 2020. Behavioural finance in an era of artificial intelligence: Longitudinal

case study of robo-advisors in investment decisions. Journal of Behavioral and

Experimental Finance, 27. p.100297.

Tsindeliani, I.A., 2019. Principles of the public financial law as the means of legal regulation of

public finance. Journal of Legal, Ethical and Regulatory Issues, 22(5). pp.1-12.

Wang and et.al, 2020. The impact of digital finance on financial efficiency. Managerial and

Decision Economics, 41(7). pp.1225-1236.

Books and Journals

Belousova and et.al, 2019. The financial literacy assessment among students majoring in the

field of finance. EurAsian Journal of BioSciences, 13(1). China's green finance and

economic growth. Resources Policy, 75. p.102476.

Choudhury, M.A., 2018. The ontological law of Tawhid contra ‘Shari’ah-compliance’in Islamic

portfolio finance. International Journal of Law and Management.

Elheddad and et.al, 2021. The effect of the Fourth Industrial Revolution on the environment: The

relationship between electronic finance and pollution in OECD countries. Technological

Forecasting and Social Change, 163. p.120485.

Hasan, Z., 2020. Risk and Islamic Finance: A Misconception Corrected. In handbook of research

on theory and practice of global Islamic finance (pp. 441-454). IGI Global.

Islam, R. and Ahmad, R., 2020. Applicability of Mudarabah and Musharakah as Islamic micro-

equity finance to underprivileged women in Malaysia. The European Journal of

Development Research, 32(1). pp.176-197.

Ledhem, M.A. and Mekidiche, M., 2021. Islamic finance and economic growth nexus: an

empirical evidence from Southeast Asia using dynamic panel one-step system GMM

analysis. Journal of Islamic Accounting and Business Research.

Liermann, V., Li, S. and Schaudinnus, N., 2019. Deep learning: An introduction. In The Impact

of Digital Transformation and Fintech on the Finance Professional (pp. 305-340). Palgrave

Macmillan, Cham.

Limani, Y., Hajrizi, E. and Stapleton, L., 2019. The Impact of Industry 4.0 on Advanced

Operations Management.

Lubin, D., 2018. Dance of the trillions: Developing countries and global finance. Brookings

Institution Press.

Mohan, P.S., 2022. Implementing nationally determined contributions under the Paris

agreement: an assessment of climate finance in Caribbean small island developing

states. Climate Policy. pp.1-9.

Mora and et.al, 2019. The effects of mean wind speed uncertainty on project finance debt sizing

for offshore wind farms. Applied Energy, 252. p.113419.

Piccio, D.R. and Van Biezen, I., 2018. Political finance and the cartel party thesis. In Handbook

of political party funding. Edward Elgar Publishing.

Shanmuganathan, M., 2020. Behavioural finance in an era of artificial intelligence: Longitudinal

case study of robo-advisors in investment decisions. Journal of Behavioral and

Experimental Finance, 27. p.100297.

Tsindeliani, I.A., 2019. Principles of the public financial law as the means of legal regulation of

public finance. Journal of Legal, Ethical and Regulatory Issues, 22(5). pp.1-12.

Wang and et.al, 2020. The impact of digital finance on financial efficiency. Managerial and

Decision Economics, 41(7). pp.1225-1236.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.