Finance and Accounting Report: AASB Standards and Applications

VerifiedAdded on 2022/09/26

|12

|1174

|17

Report

AI Summary

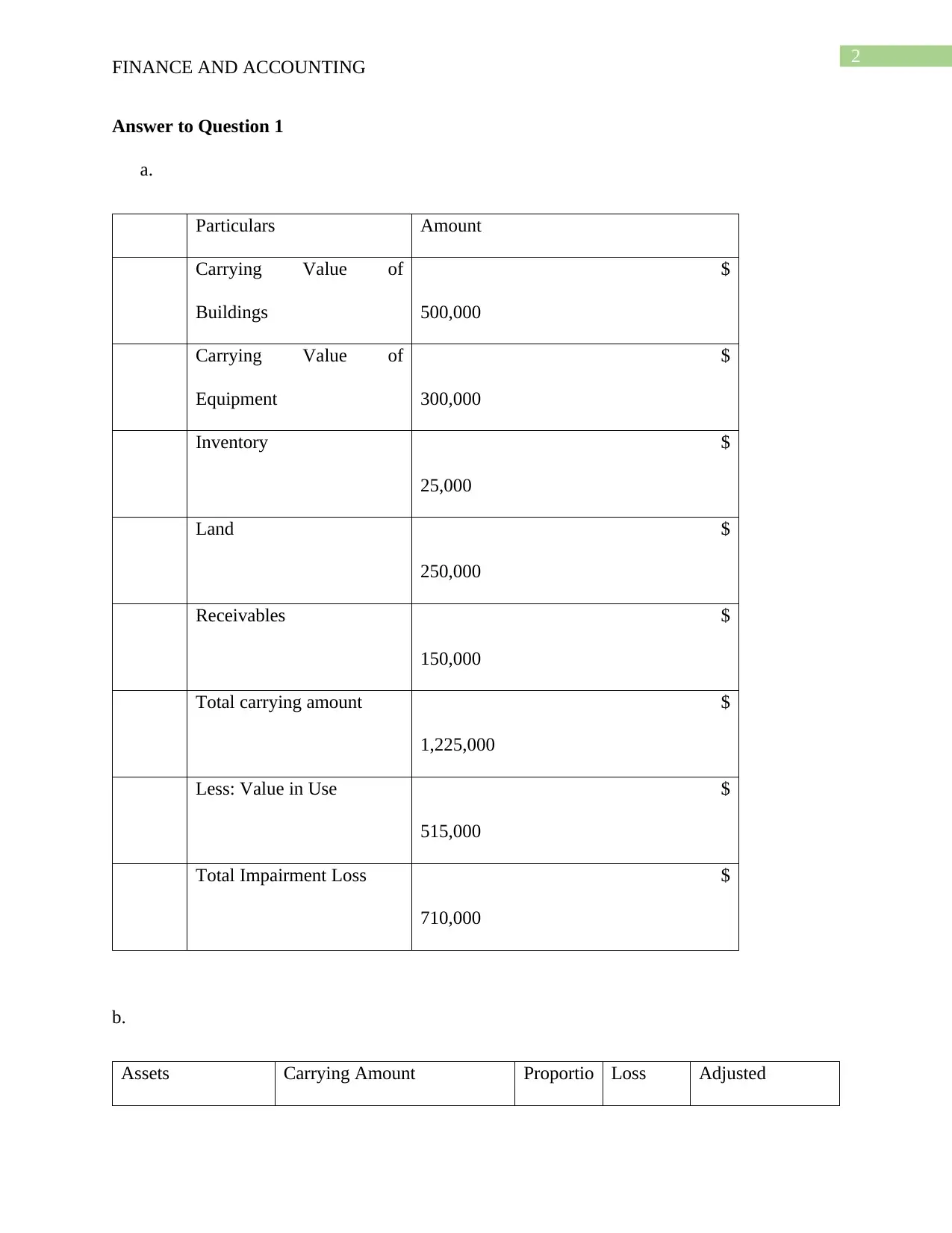

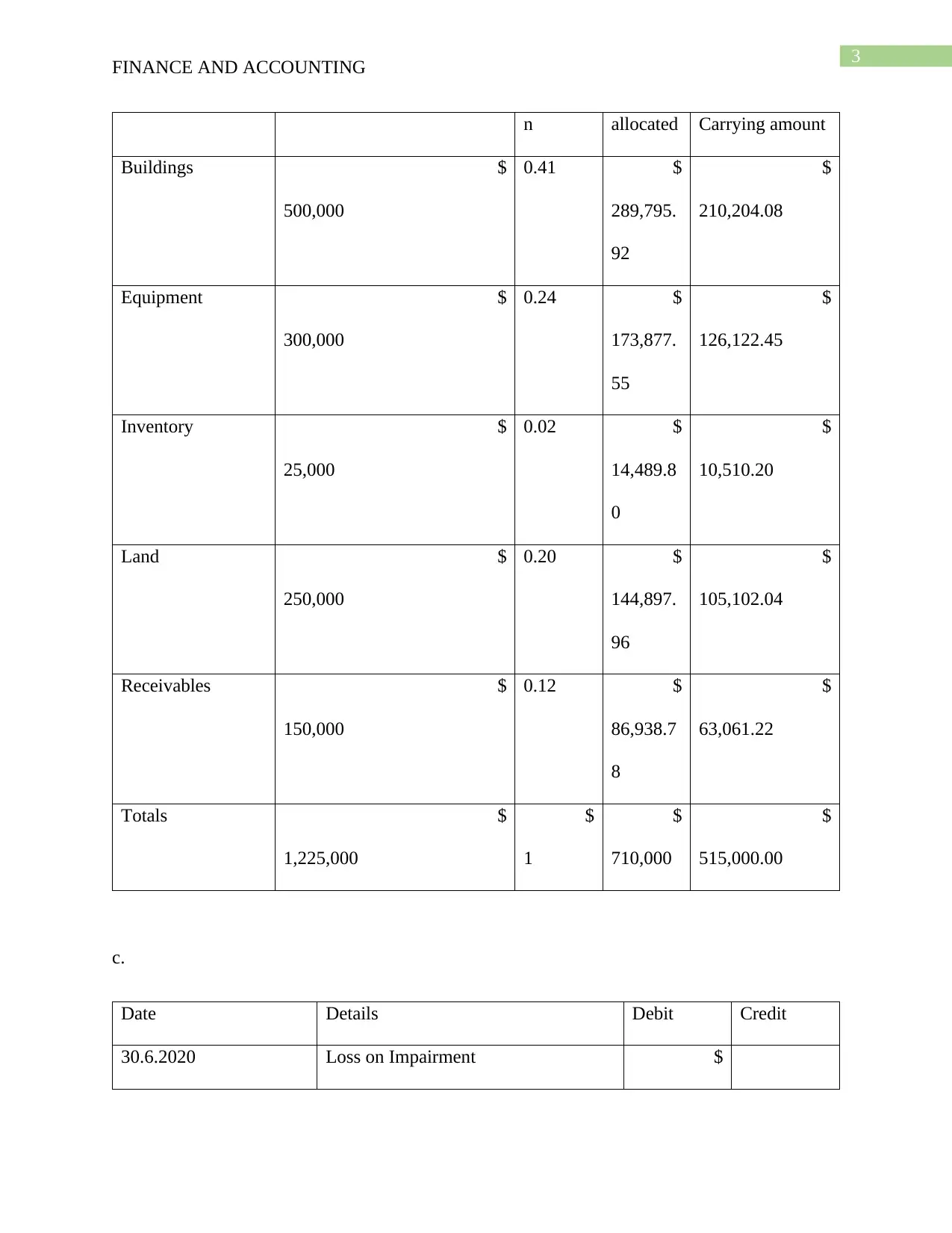

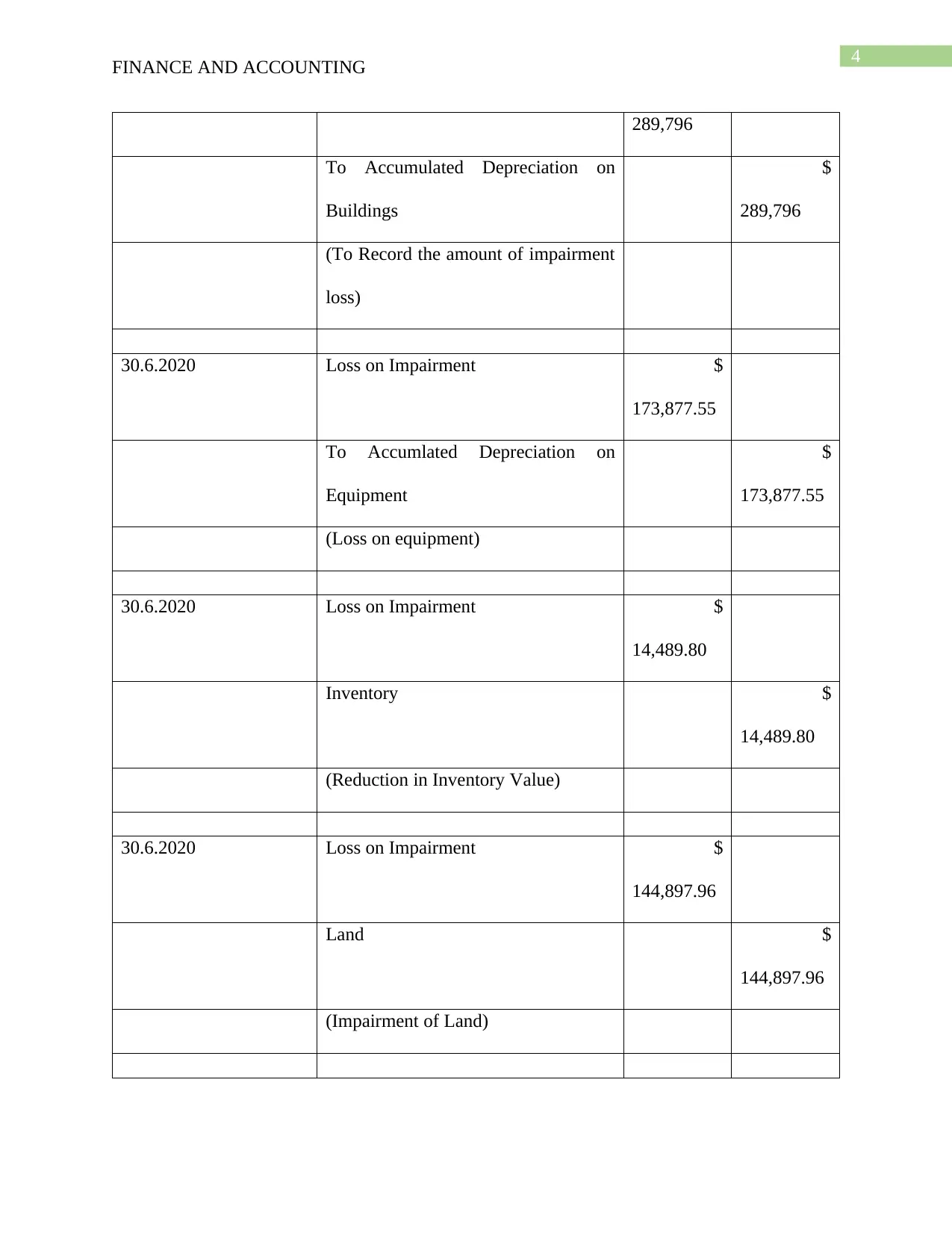

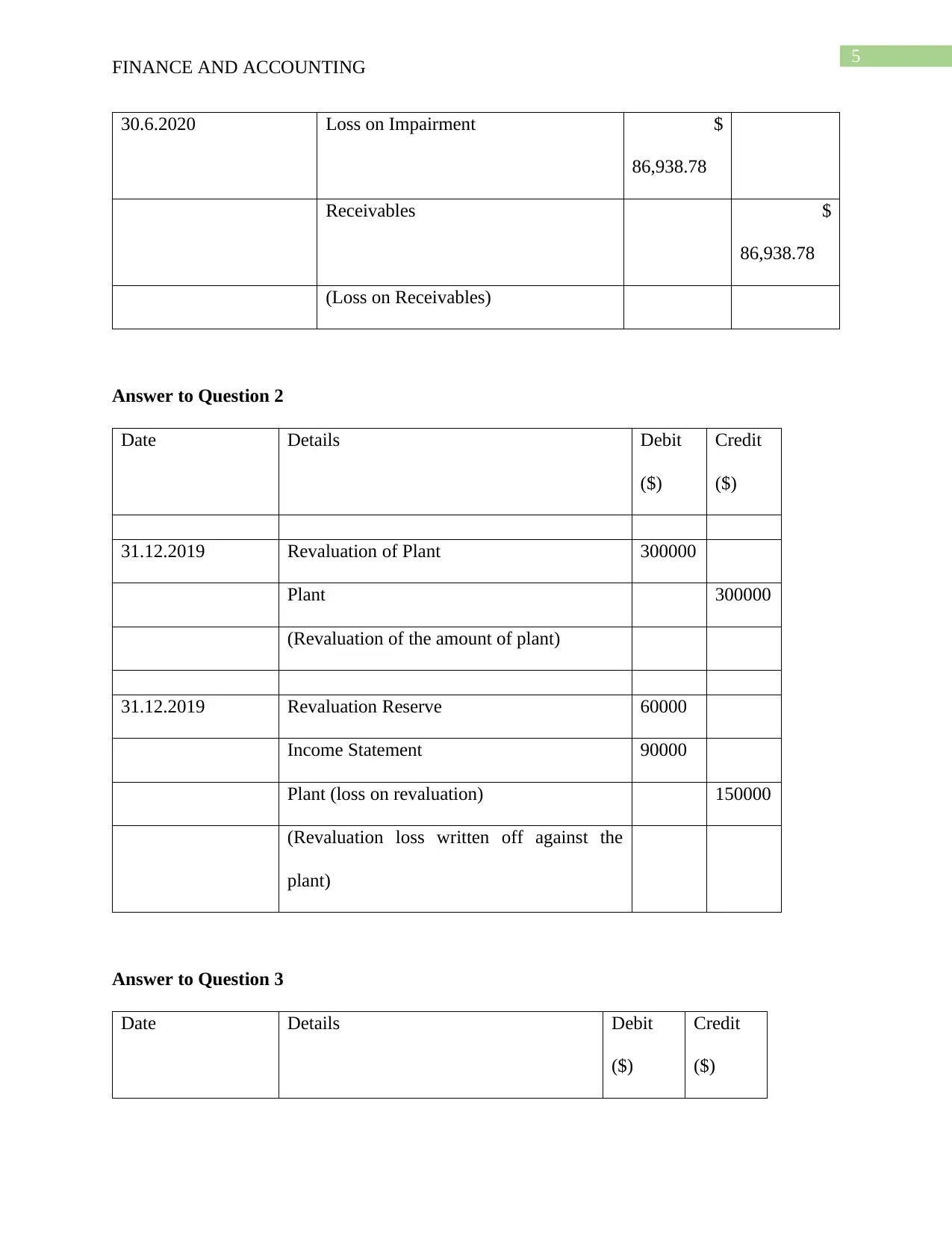

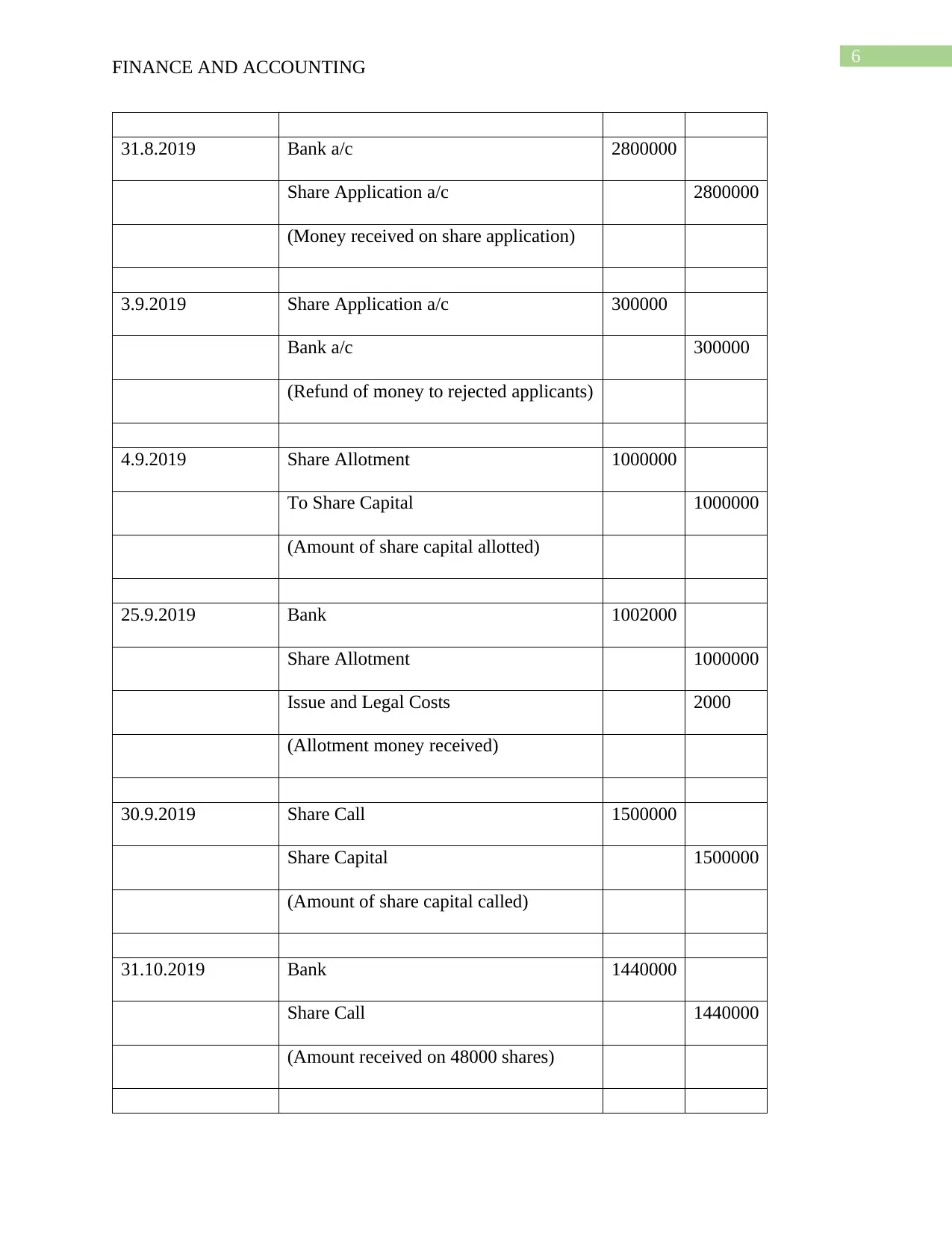

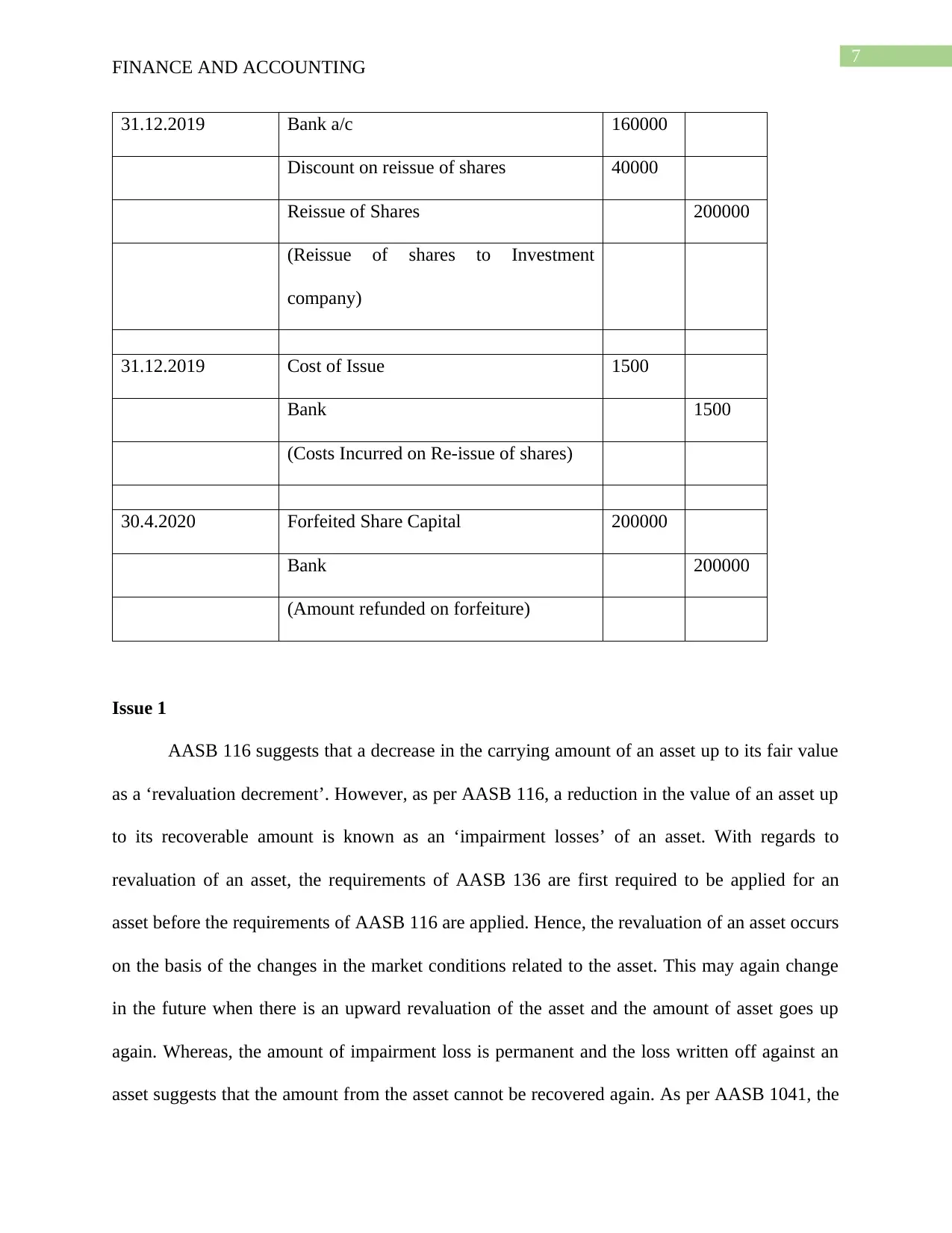

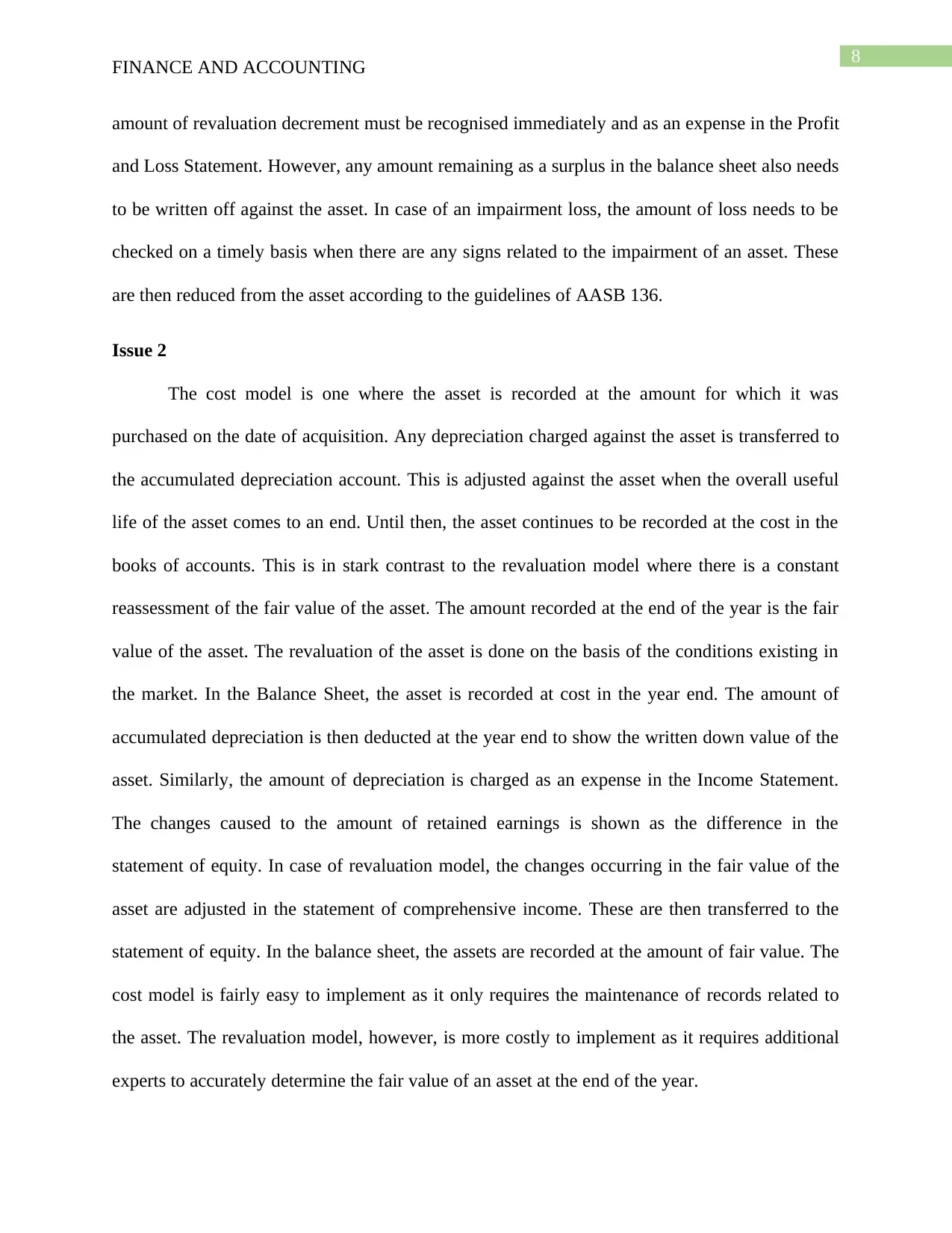

This finance and accounting report provides a detailed analysis of impairment losses, asset revaluation, and share capital transactions. The report begins by calculating and allocating impairment losses across various assets, including buildings, equipment, inventory, land, and receivables. It then addresses the accounting treatment of asset revaluation, demonstrating the journal entries for revaluation of plant assets and the subsequent accounting for revaluation losses. The report also covers share capital transactions, including share applications, allotments, and calls, along with journal entries for each transaction. The report also differentiates between impairment loss and revaluation decrement, and compares cost and revaluation models for asset valuation, offering insights into the advantages of the revaluation model for a growing business. Finally, the report concludes with a bibliography citing relevant sources, including AASB standards.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.