Persimmon Plc: Financial Performance, Investment, and Cost Analysis

VerifiedAdded on 2023/01/11

|13

|2522

|26

Report

AI Summary

This report provides a comprehensive financial analysis of Persimmon Plc, a leading UK house building company. It begins with an introduction to financial accounting and its relevance to the company's operations. The report then delves into the financial performance of Persimmon Plc, utilizing ratio analysis to assess liquidity, profitability, and efficiency. The analysis covers the years 2018 and 2019, comparing key ratios like current ratio, quick ratio, return on capital employed, return on equity, gross profit margin, and net profit margin. The report also examines investment appraisal techniques, comparing Software project A and Hardware project B using NPV, payback period, and IRR, recommending the more profitable option. Finally, the report explores cost analysis of existing and proposed products using marginal and absorption costing methods, providing recommendations on which product to focus on. The report concludes with recommendations and a discussion of the company's financial health and strategic decisions.

FINANCE AND

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

Financial performance of the company using ratio analysis.......................................................1

Appraisal of possible investment and sources of finance............................................................4

Cost analysis of present and proposed products..........................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

Financial performance of the company using ratio analysis.......................................................1

Appraisal of possible investment and sources of finance............................................................4

Cost analysis of present and proposed products..........................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

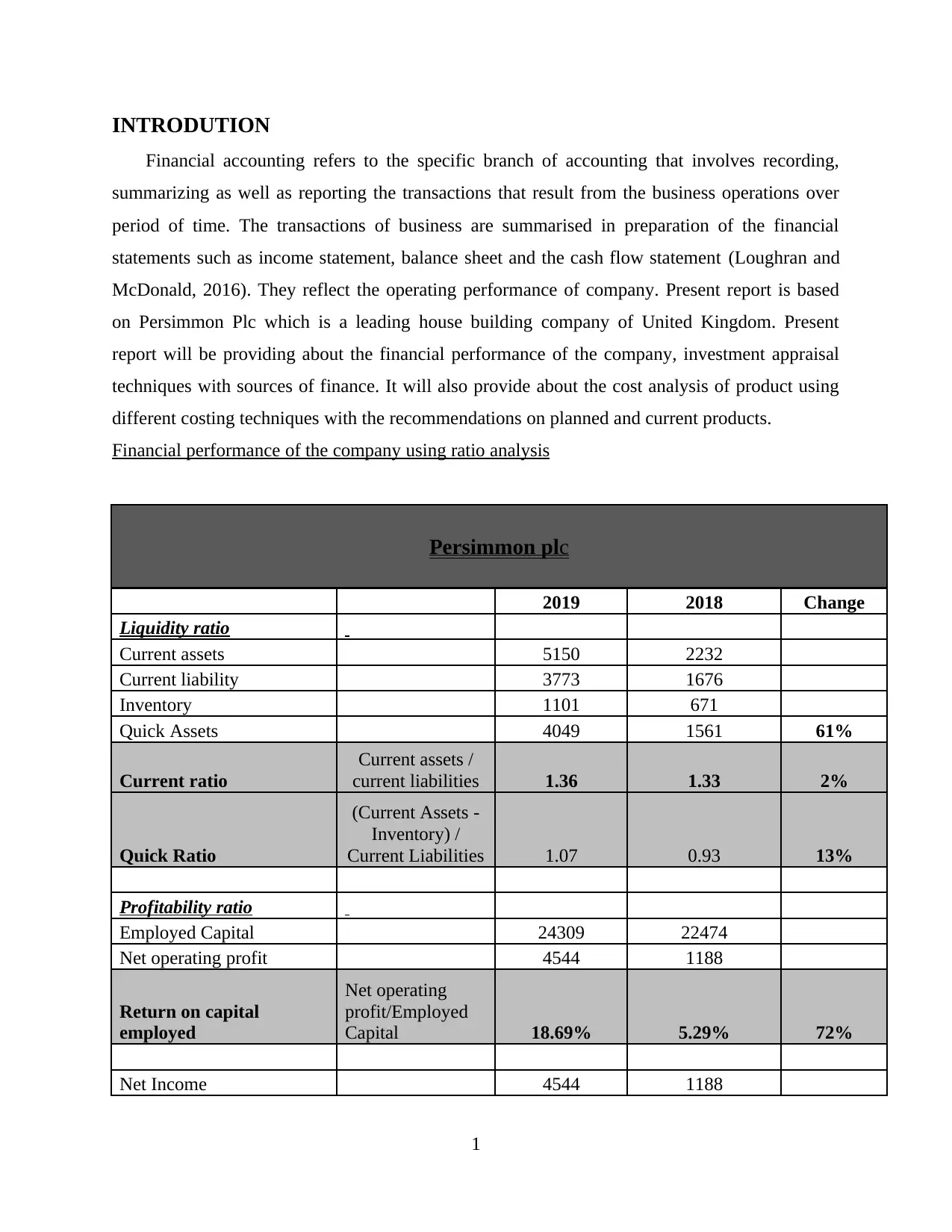

INTRODUTION

Financial accounting refers to the specific branch of accounting that involves recording,

summarizing as well as reporting the transactions that result from the business operations over

period of time. The transactions of business are summarised in preparation of the financial

statements such as income statement, balance sheet and the cash flow statement (Loughran and

McDonald, 2016). They reflect the operating performance of company. Present report is based

on Persimmon Plc which is a leading house building company of United Kingdom. Present

report will be providing about the financial performance of the company, investment appraisal

techniques with sources of finance. It will also provide about the cost analysis of product using

different costing techniques with the recommendations on planned and current products.

Financial performance of the company using ratio analysis

Persimmon plc

2019 2018 Change

Liquidity ratio

Current assets 5150 2232

Current liability 3773 1676

Inventory 1101 671

Quick Assets 4049 1561 61%

Current ratio

Current assets /

current liabilities 1.36 1.33 2%

Quick Ratio

(Current Assets -

Inventory) /

Current Liabilities 1.07 0.93 13%

Profitability ratio

Employed Capital 24309 22474

Net operating profit 4544 1188

Return on capital

employed

Net operating

profit/Employed

Capital 18.69% 5.29% 72%

Net Income 4544 1188

1

Financial accounting refers to the specific branch of accounting that involves recording,

summarizing as well as reporting the transactions that result from the business operations over

period of time. The transactions of business are summarised in preparation of the financial

statements such as income statement, balance sheet and the cash flow statement (Loughran and

McDonald, 2016). They reflect the operating performance of company. Present report is based

on Persimmon Plc which is a leading house building company of United Kingdom. Present

report will be providing about the financial performance of the company, investment appraisal

techniques with sources of finance. It will also provide about the cost analysis of product using

different costing techniques with the recommendations on planned and current products.

Financial performance of the company using ratio analysis

Persimmon plc

2019 2018 Change

Liquidity ratio

Current assets 5150 2232

Current liability 3773 1676

Inventory 1101 671

Quick Assets 4049 1561 61%

Current ratio

Current assets /

current liabilities 1.36 1.33 2%

Quick Ratio

(Current Assets -

Inventory) /

Current Liabilities 1.07 0.93 13%

Profitability ratio

Employed Capital 24309 22474

Net operating profit 4544 1188

Return on capital

employed

Net operating

profit/Employed

Capital 18.69% 5.29% 72%

Net Income 4544 1188

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

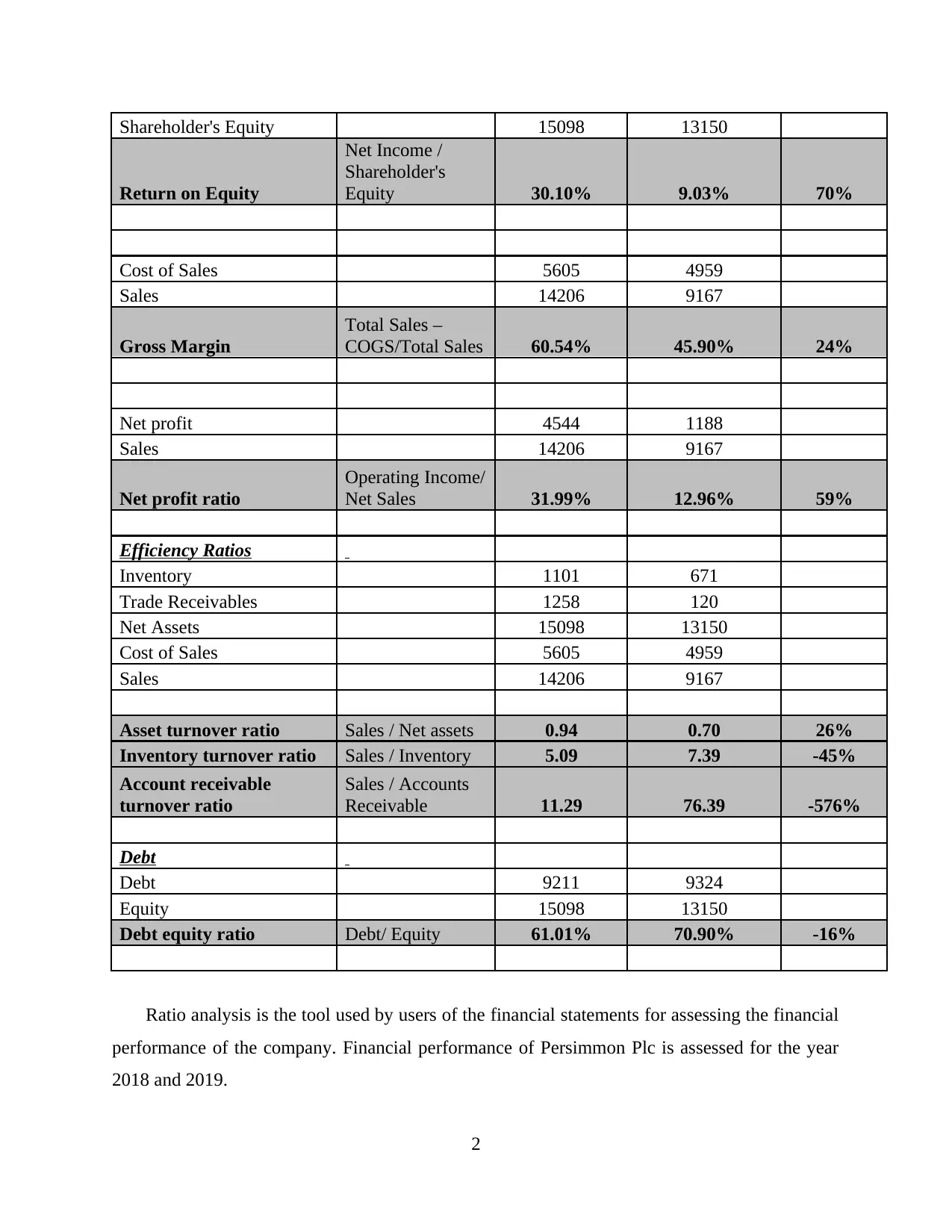

Shareholder's Equity 15098 13150

Return on Equity

Net Income /

Shareholder's

Equity 30.10% 9.03% 70%

Cost of Sales 5605 4959

Sales 14206 9167

Gross Margin

Total Sales –

COGS/Total Sales 60.54% 45.90% 24%

Net profit 4544 1188

Sales 14206 9167

Net profit ratio

Operating Income/

Net Sales 31.99% 12.96% 59%

Efficiency Ratios

Inventory 1101 671

Trade Receivables 1258 120

Net Assets 15098 13150

Cost of Sales 5605 4959

Sales 14206 9167

Asset turnover ratio Sales / Net assets 0.94 0.70 26%

Inventory turnover ratio Sales / Inventory 5.09 7.39 -45%

Account receivable

turnover ratio

Sales / Accounts

Receivable 11.29 76.39 -576%

Debt

Debt 9211 9324

Equity 15098 13150

Debt equity ratio Debt/ Equity 61.01% 70.90% -16%

Ratio analysis is the tool used by users of the financial statements for assessing the financial

performance of the company. Financial performance of Persimmon Plc is assessed for the year

2018 and 2019.

2

Return on Equity

Net Income /

Shareholder's

Equity 30.10% 9.03% 70%

Cost of Sales 5605 4959

Sales 14206 9167

Gross Margin

Total Sales –

COGS/Total Sales 60.54% 45.90% 24%

Net profit 4544 1188

Sales 14206 9167

Net profit ratio

Operating Income/

Net Sales 31.99% 12.96% 59%

Efficiency Ratios

Inventory 1101 671

Trade Receivables 1258 120

Net Assets 15098 13150

Cost of Sales 5605 4959

Sales 14206 9167

Asset turnover ratio Sales / Net assets 0.94 0.70 26%

Inventory turnover ratio Sales / Inventory 5.09 7.39 -45%

Account receivable

turnover ratio

Sales / Accounts

Receivable 11.29 76.39 -576%

Debt

Debt 9211 9324

Equity 15098 13150

Debt equity ratio Debt/ Equity 61.01% 70.90% -16%

Ratio analysis is the tool used by users of the financial statements for assessing the financial

performance of the company. Financial performance of Persimmon Plc is assessed for the year

2018 and 2019.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current ratio is used for assessing the liquidity position of company. It identifies where the

company is able to meet the short term obligations with the current assets. Current ratio of

company is 1.36 with upward movement of 2% from last year. Industry average is 2:1. Current

ratio is below industry average and company is required to make the liquidity position of

company strong (Conley, Gonçalves and Hansen, 2018). Liquidity position could be

strengthened by using long term debts in place of short term loans to meet working capital

requirements.

Quick ratio measures liquidity without including inventory in the current assets. This

identifies the actual liquidity position as inventory is not considered current asset by most of the

experts. Quick ratio of company is 1.07 with increase of 13% from last year. it provides that

company is taking measures to improve liquidity position of company.

Return on capital employed is the ratio that measures efficiency of the management in

effectively utilising resources of the organisation. ROCE of company is 18.69% with significant

rise from 5.29% in last year. it reflects that the strategies adopted by company last year have

given good results It has helped the company to reach required level of return over the capital

employed of the firm. It could further increase the return on capital employed by writing off the

assets that are not used by company. Higher returns reflect that management is making effective

use of the resources for generating adequate returns.

Return on Equity states the return generated by the firm over its equity investments. ROE

of company was 9.03% last year that has increased to 30% in 2019. Return shows that the

company has earned significant returns this year (Wood, 2016). Also the company has issued

new shares in the market. a firm with higher returns have number of opportunities available to it.

Investors are concerned mainly with the return that they will be getting over their investments.

Return shows that there would be increase in wealth of shareholders along with increase in

market cap. Company should generate adequate returns over the investments

Gross profit margin refers to the amount of profit earned from carrying out the business

activities during the financial year. Company is having gross profit margin of 60.54% with

increase of 24%.Revenues of the firm has increased significantly from the last year where it has

maintained strict control over the cost of sales. Gross margin of firm should be hgh as it reflects

the amount left with the company to carry out further operations and earn sufficient net profits.

3

company is able to meet the short term obligations with the current assets. Current ratio of

company is 1.36 with upward movement of 2% from last year. Industry average is 2:1. Current

ratio is below industry average and company is required to make the liquidity position of

company strong (Conley, Gonçalves and Hansen, 2018). Liquidity position could be

strengthened by using long term debts in place of short term loans to meet working capital

requirements.

Quick ratio measures liquidity without including inventory in the current assets. This

identifies the actual liquidity position as inventory is not considered current asset by most of the

experts. Quick ratio of company is 1.07 with increase of 13% from last year. it provides that

company is taking measures to improve liquidity position of company.

Return on capital employed is the ratio that measures efficiency of the management in

effectively utilising resources of the organisation. ROCE of company is 18.69% with significant

rise from 5.29% in last year. it reflects that the strategies adopted by company last year have

given good results It has helped the company to reach required level of return over the capital

employed of the firm. It could further increase the return on capital employed by writing off the

assets that are not used by company. Higher returns reflect that management is making effective

use of the resources for generating adequate returns.

Return on Equity states the return generated by the firm over its equity investments. ROE

of company was 9.03% last year that has increased to 30% in 2019. Return shows that the

company has earned significant returns this year (Wood, 2016). Also the company has issued

new shares in the market. a firm with higher returns have number of opportunities available to it.

Investors are concerned mainly with the return that they will be getting over their investments.

Return shows that there would be increase in wealth of shareholders along with increase in

market cap. Company should generate adequate returns over the investments

Gross profit margin refers to the amount of profit earned from carrying out the business

activities during the financial year. Company is having gross profit margin of 60.54% with

increase of 24%.Revenues of the firm has increased significantly from the last year where it has

maintained strict control over the cost of sales. Gross margin of firm should be hgh as it reflects

the amount left with the company to carry out further operations and earn sufficient net profits.

3

Rise in the gross profits is seen due to success of the strategies adopted by the organisation for

improving the performance of business.

Net Profit margin is one of the most important profitability ration used by experts and

financial analysts. It represents the performance of company in carrying out the business during

the given time frame. Every business strives for earning maximum profits at minimal costs.

Company is highly profitable as it has earned 32% net profit this year with high jump from 13%

last year.

Asset turnover reflects the efficiency of managing sales over the assets of firm. asset

turnover is 0.94 which was 0.70 in 2018. Company is required to increase the asst turnover ratio

as it is very low.

Inventory turnover ratio has shown a decline from last year. The inventory turnover

should be high as it shows the frequency of inventory movement in an enterprise (Han and et.al.,

2018). Company is required to improve the inventory turnover by adopting effective marketing

strategies.

Receivables turnover shows the collection period. Turnover has return to adequate level

from the last year. This shows that company is making fast collection of the receivables. This

helps in managing the cash cycle.

Debt equity ratio of company is 61% which is used to assess financial risk in the enterprise.

Debt equity ratio of the entity is adequate. Company is having an appropriate mix of debt and

equity. It helps in managing the capital structure of the enterprise. It could be assessed that

company uses equity capital for raising funds more than the debt financing.

Appraisal of possible investment and sources of finance

Persimmon plc is proposing to invest in Software project A or Hardware project B.

Company is planning to choose the best project from the two options. Software project A

requires investment of £100000 and Hardware project requires investment of £120000.

Estimated cash flows from the project are:

Year Project A – Software Project Project B – Laundrette Project

0 (£100,000) (£120,000)

1 £28,000 £31,000

2 £32,000 £38,000

4

improving the performance of business.

Net Profit margin is one of the most important profitability ration used by experts and

financial analysts. It represents the performance of company in carrying out the business during

the given time frame. Every business strives for earning maximum profits at minimal costs.

Company is highly profitable as it has earned 32% net profit this year with high jump from 13%

last year.

Asset turnover reflects the efficiency of managing sales over the assets of firm. asset

turnover is 0.94 which was 0.70 in 2018. Company is required to increase the asst turnover ratio

as it is very low.

Inventory turnover ratio has shown a decline from last year. The inventory turnover

should be high as it shows the frequency of inventory movement in an enterprise (Han and et.al.,

2018). Company is required to improve the inventory turnover by adopting effective marketing

strategies.

Receivables turnover shows the collection period. Turnover has return to adequate level

from the last year. This shows that company is making fast collection of the receivables. This

helps in managing the cash cycle.

Debt equity ratio of company is 61% which is used to assess financial risk in the enterprise.

Debt equity ratio of the entity is adequate. Company is having an appropriate mix of debt and

equity. It helps in managing the capital structure of the enterprise. It could be assessed that

company uses equity capital for raising funds more than the debt financing.

Appraisal of possible investment and sources of finance

Persimmon plc is proposing to invest in Software project A or Hardware project B.

Company is planning to choose the best project from the two options. Software project A

requires investment of £100000 and Hardware project requires investment of £120000.

Estimated cash flows from the project are:

Year Project A – Software Project Project B – Laundrette Project

0 (£100,000) (£120,000)

1 £28,000 £31,000

2 £32,000 £38,000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

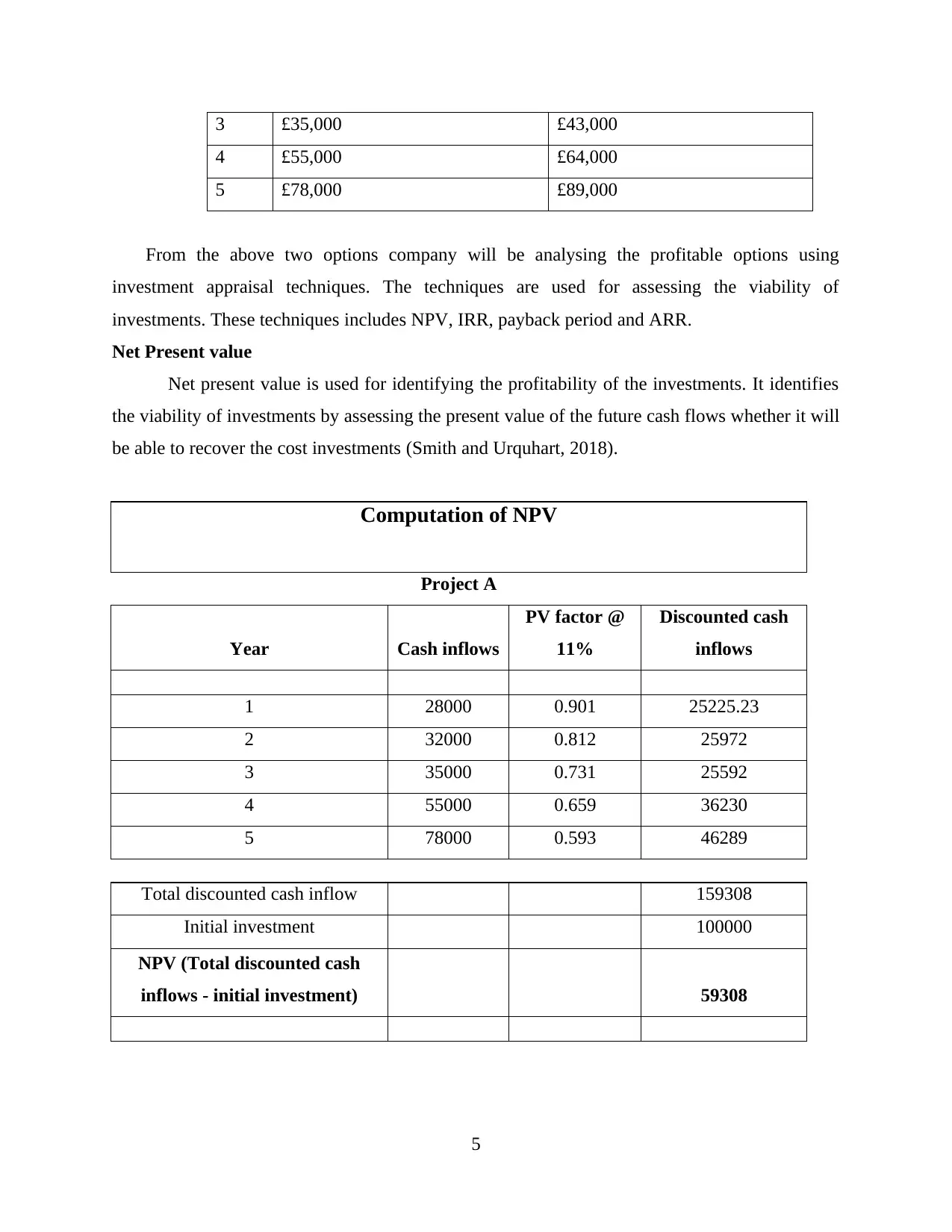

3 £35,000 £43,000

4 £55,000 £64,000

5 £78,000 £89,000

From the above two options company will be analysing the profitable options using

investment appraisal techniques. The techniques are used for assessing the viability of

investments. These techniques includes NPV, IRR, payback period and ARR.

Net Present value

Net present value is used for identifying the profitability of the investments. It identifies

the viability of investments by assessing the present value of the future cash flows whether it will

be able to recover the cost investments (Smith and Urquhart, 2018).

Computation of NPV

Project A

Year Cash inflows

PV factor @

11%

Discounted cash

inflows

1 28000 0.901 25225.23

2 32000 0.812 25972

3 35000 0.731 25592

4 55000 0.659 36230

5 78000 0.593 46289

Total discounted cash inflow 159308

Initial investment 100000

NPV (Total discounted cash

inflows - initial investment) 59308

5

4 £55,000 £64,000

5 £78,000 £89,000

From the above two options company will be analysing the profitable options using

investment appraisal techniques. The techniques are used for assessing the viability of

investments. These techniques includes NPV, IRR, payback period and ARR.

Net Present value

Net present value is used for identifying the profitability of the investments. It identifies

the viability of investments by assessing the present value of the future cash flows whether it will

be able to recover the cost investments (Smith and Urquhart, 2018).

Computation of NPV

Project A

Year Cash inflows

PV factor @

11%

Discounted cash

inflows

1 28000 0.901 25225.23

2 32000 0.812 25972

3 35000 0.731 25592

4 55000 0.659 36230

5 78000 0.593 46289

Total discounted cash inflow 159308

Initial investment 100000

NPV (Total discounted cash

inflows - initial investment) 59308

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Computation of NPV

Project B

Year Cash inflows

PV

factor @

11%

Discounted

cash inflows

1 31000 0.901 27927.93

2 38000 0.812 30842

3 43000 0.731 31441

4 64000 0.659 42159

5 89000 0.593 52817

Total discounted cash inflow 185187

Initial investment 120000

NPV (Total discounted cash

inflows - initial investment) 65187

Payback Period

Payback period measures the length of time in which company will be recovering its cost

of investment.

Computation of Payback period

Project A Project B

Year

Cash

inflows

Cumulative cash

inflows

Cash

inflows

Cumulative cash

inflows

1 28000 28000 31000 31000

2 32000 60000 38000 69000

6

Project B

Year Cash inflows

PV

factor @

11%

Discounted

cash inflows

1 31000 0.901 27927.93

2 38000 0.812 30842

3 43000 0.731 31441

4 64000 0.659 42159

5 89000 0.593 52817

Total discounted cash inflow 185187

Initial investment 120000

NPV (Total discounted cash

inflows - initial investment) 65187

Payback Period

Payback period measures the length of time in which company will be recovering its cost

of investment.

Computation of Payback period

Project A Project B

Year

Cash

inflows

Cumulative cash

inflows

Cash

inflows

Cumulative cash

inflows

1 28000 28000 31000 31000

2 32000 60000 38000 69000

6

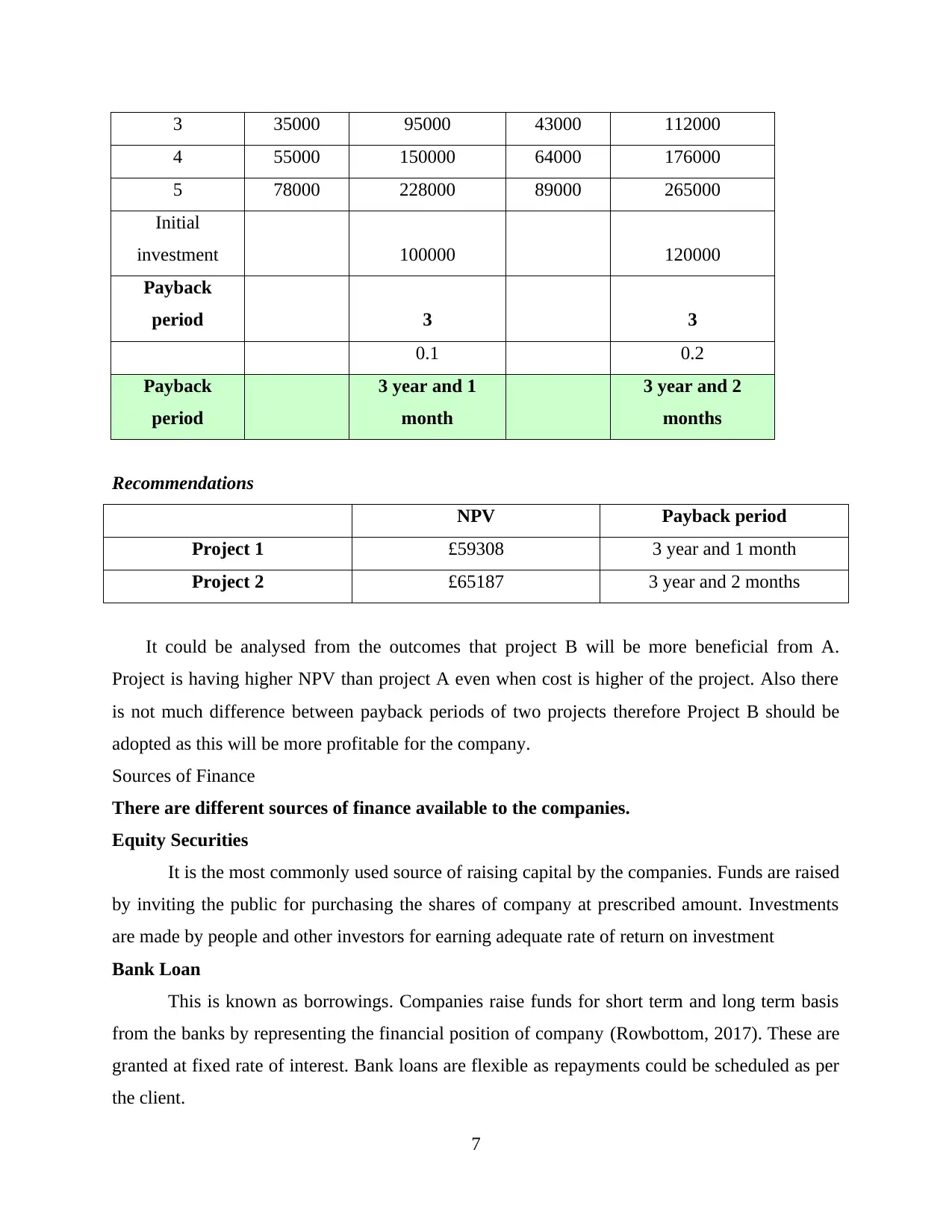

3 35000 95000 43000 112000

4 55000 150000 64000 176000

5 78000 228000 89000 265000

Initial

investment 100000 120000

Payback

period 3 3

0.1 0.2

Payback

period

3 year and 1

month

3 year and 2

months

Recommendations

NPV Payback period

Project 1 £59308 3 year and 1 month

Project 2 £65187 3 year and 2 months

It could be analysed from the outcomes that project B will be more beneficial from A.

Project is having higher NPV than project A even when cost is higher of the project. Also there

is not much difference between payback periods of two projects therefore Project B should be

adopted as this will be more profitable for the company.

Sources of Finance

There are different sources of finance available to the companies.

Equity Securities

It is the most commonly used source of raising capital by the companies. Funds are raised

by inviting the public for purchasing the shares of company at prescribed amount. Investments

are made by people and other investors for earning adequate rate of return on investment

Bank Loan

This is known as borrowings. Companies raise funds for short term and long term basis

from the banks by representing the financial position of company (Rowbottom, 2017). These are

granted at fixed rate of interest. Bank loans are flexible as repayments could be scheduled as per

the client.

7

4 55000 150000 64000 176000

5 78000 228000 89000 265000

Initial

investment 100000 120000

Payback

period 3 3

0.1 0.2

Payback

period

3 year and 1

month

3 year and 2

months

Recommendations

NPV Payback period

Project 1 £59308 3 year and 1 month

Project 2 £65187 3 year and 2 months

It could be analysed from the outcomes that project B will be more beneficial from A.

Project is having higher NPV than project A even when cost is higher of the project. Also there

is not much difference between payback periods of two projects therefore Project B should be

adopted as this will be more profitable for the company.

Sources of Finance

There are different sources of finance available to the companies.

Equity Securities

It is the most commonly used source of raising capital by the companies. Funds are raised

by inviting the public for purchasing the shares of company at prescribed amount. Investments

are made by people and other investors for earning adequate rate of return on investment

Bank Loan

This is known as borrowings. Companies raise funds for short term and long term basis

from the banks by representing the financial position of company (Rowbottom, 2017). These are

granted at fixed rate of interest. Bank loans are flexible as repayments could be scheduled as per

the client.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

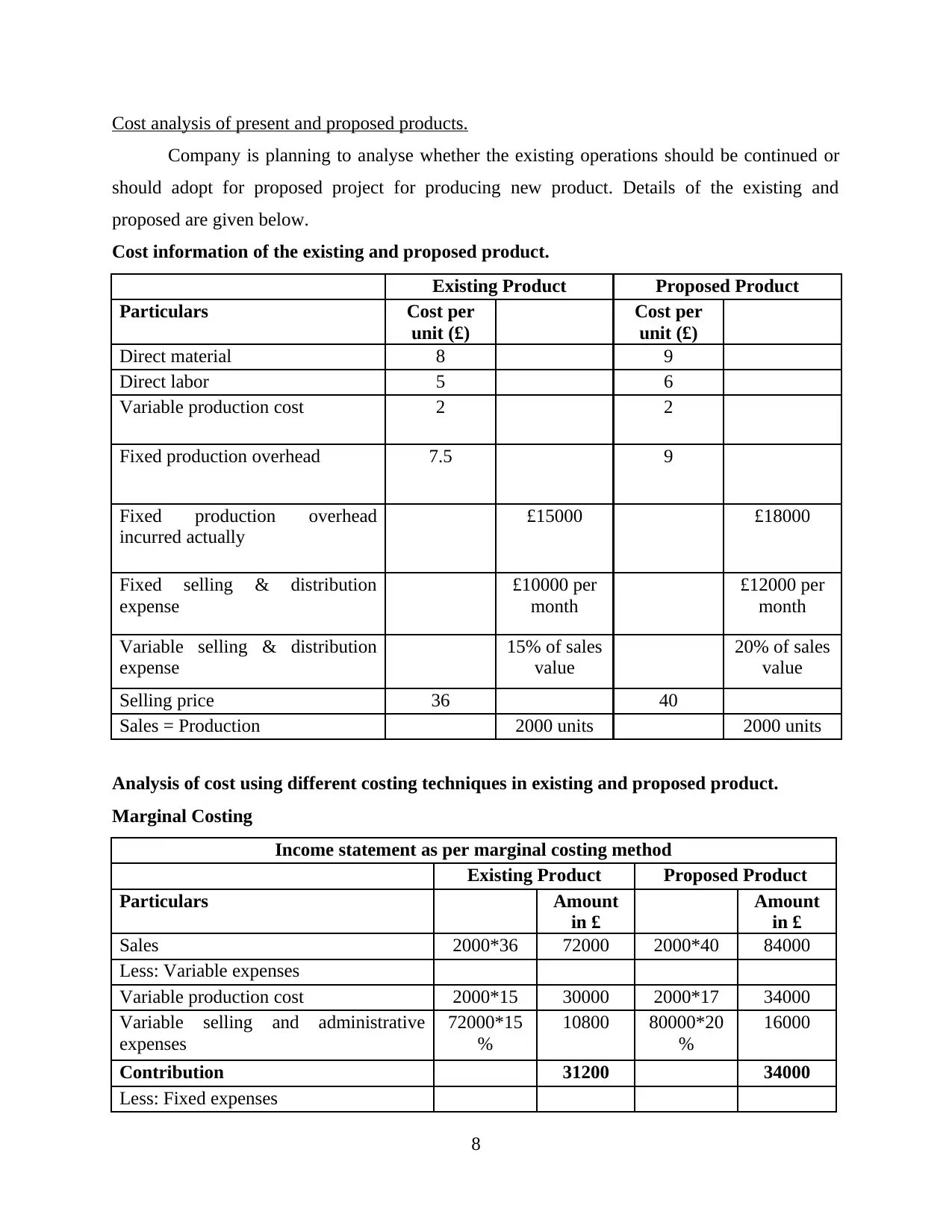

Cost analysis of present and proposed products.

Company is planning to analyse whether the existing operations should be continued or

should adopt for proposed project for producing new product. Details of the existing and

proposed are given below.

Cost information of the existing and proposed product.

Existing Product Proposed Product

Particulars Cost per

unit (£)

Cost per

unit (£)

Direct material 8 9

Direct labor 5 6

Variable production cost 2 2

Fixed production overhead 7.5 9

Fixed production overhead

incurred actually

£15000 £18000

Fixed selling & distribution

expense

£10000 per

month

£12000 per

month

Variable selling & distribution

expense

15% of sales

value

20% of sales

value

Selling price 36 40

Sales = Production 2000 units 2000 units

Analysis of cost using different costing techniques in existing and proposed product.

Marginal Costing

Income statement as per marginal costing method

Existing Product Proposed Product

Particulars Amount

in £

Amount

in £

Sales 2000*36 72000 2000*40 84000

Less: Variable expenses

Variable production cost 2000*15 30000 2000*17 34000

Variable selling and administrative

expenses

72000*15

%

10800 80000*20

%

16000

Contribution 31200 34000

Less: Fixed expenses

8

Company is planning to analyse whether the existing operations should be continued or

should adopt for proposed project for producing new product. Details of the existing and

proposed are given below.

Cost information of the existing and proposed product.

Existing Product Proposed Product

Particulars Cost per

unit (£)

Cost per

unit (£)

Direct material 8 9

Direct labor 5 6

Variable production cost 2 2

Fixed production overhead 7.5 9

Fixed production overhead

incurred actually

£15000 £18000

Fixed selling & distribution

expense

£10000 per

month

£12000 per

month

Variable selling & distribution

expense

15% of sales

value

20% of sales

value

Selling price 36 40

Sales = Production 2000 units 2000 units

Analysis of cost using different costing techniques in existing and proposed product.

Marginal Costing

Income statement as per marginal costing method

Existing Product Proposed Product

Particulars Amount

in £

Amount

in £

Sales 2000*36 72000 2000*40 84000

Less: Variable expenses

Variable production cost 2000*15 30000 2000*17 34000

Variable selling and administrative

expenses

72000*15

%

10800 80000*20

%

16000

Contribution 31200 34000

Less: Fixed expenses

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed production overhead 15000 18000

Fixed selling and distribution expenses 10000 12000

Net operating income 6200 4000

Cost card

Unit product cost Existing

Product

Proposed

Product

Particulars Amount in £ Amount in £

Direct material 8 9

Direct labor 5 6

Variable production cost 2 2

Total variable production

cost

15 17

Absorption Costing

Income statement as per absorption costing

Existing Product Proposed Product

Particulars Amount

in £

Amount

in £

Sales 2000*36 72000 2000*40 84000

less:

Cost of goods sold (2000*22.5

)

45000 (2000*26) 52000

Gross margin 27000 32000

less: Variable selling & distribution

expense

72000*15

%

10800 80000*20

%

16000

Fixed selling & distribution expense 10000 12000

Net operating income 6200 4000

Cost card

Unit product cost Existing

Product

Proposed

Product

Particulars Amount in £ Amount in £

Direct material 8 9

Direct labor 5 6

9

Fixed selling and distribution expenses 10000 12000

Net operating income 6200 4000

Cost card

Unit product cost Existing

Product

Proposed

Product

Particulars Amount in £ Amount in £

Direct material 8 9

Direct labor 5 6

Variable production cost 2 2

Total variable production

cost

15 17

Absorption Costing

Income statement as per absorption costing

Existing Product Proposed Product

Particulars Amount

in £

Amount

in £

Sales 2000*36 72000 2000*40 84000

less:

Cost of goods sold (2000*22.5

)

45000 (2000*26) 52000

Gross margin 27000 32000

less: Variable selling & distribution

expense

72000*15

%

10800 80000*20

%

16000

Fixed selling & distribution expense 10000 12000

Net operating income 6200 4000

Cost card

Unit product cost Existing

Product

Proposed

Product

Particulars Amount in £ Amount in £

Direct material 8 9

Direct labor 5 6

9

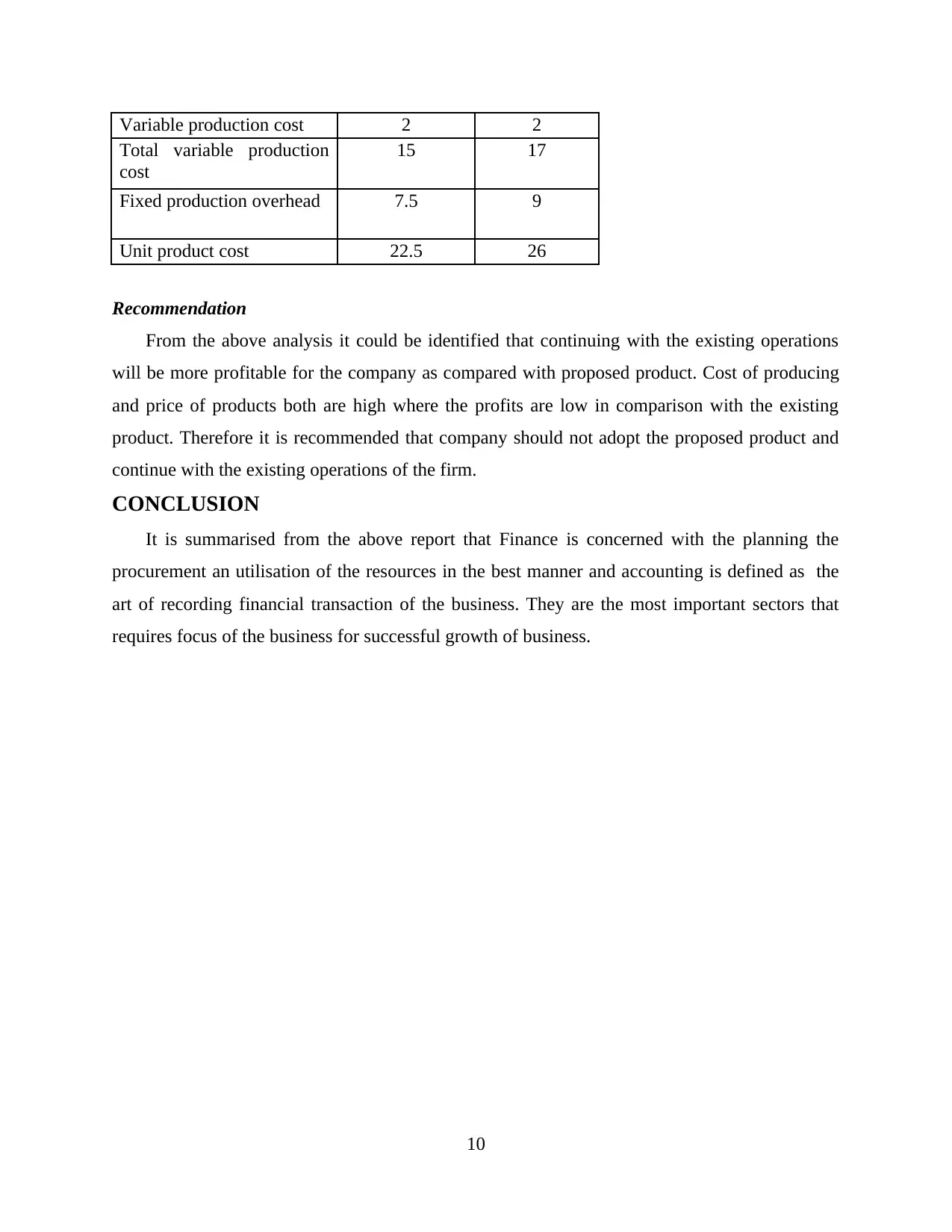

Variable production cost 2 2

Total variable production

cost

15 17

Fixed production overhead 7.5 9

Unit product cost 22.5 26

Recommendation

From the above analysis it could be identified that continuing with the existing operations

will be more profitable for the company as compared with proposed product. Cost of producing

and price of products both are high where the profits are low in comparison with the existing

product. Therefore it is recommended that company should not adopt the proposed product and

continue with the existing operations of the firm.

CONCLUSION

It is summarised from the above report that Finance is concerned with the planning the

procurement an utilisation of the resources in the best manner and accounting is defined as the

art of recording financial transaction of the business. They are the most important sectors that

requires focus of the business for successful growth of business.

10

Total variable production

cost

15 17

Fixed production overhead 7.5 9

Unit product cost 22.5 26

Recommendation

From the above analysis it could be identified that continuing with the existing operations

will be more profitable for the company as compared with proposed product. Cost of producing

and price of products both are high where the profits are low in comparison with the existing

product. Therefore it is recommended that company should not adopt the proposed product and

continue with the existing operations of the firm.

CONCLUSION

It is summarised from the above report that Finance is concerned with the planning the

procurement an utilisation of the resources in the best manner and accounting is defined as the

art of recording financial transaction of the business. They are the most important sectors that

requires focus of the business for successful growth of business.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.