Analysis of Finance and Funding within the Travel and Tourism Sector

VerifiedAdded on 2023/04/11

|13

|3677

|134

Report

AI Summary

This report provides a comprehensive analysis of finance and funding within the travel and tourism sector, focusing on Merlin Entertainment Plc. It begins with an introduction to the importance of finance and funding in the industry, followed by an examination of cost and volume analysis, including fixed and variable costs, direct and indirect costs, and the contribution margin. The report then explores various pricing methods used in the sector, such as cost-plus pricing, competition-based pricing, and value-added pricing, along with the factors that influence profitability, including political and economic environments. It also discusses different types of management accounting information and its role in decision-making, and briefly analyzes the financial performance of The Restaurant Group. Finally, the report concludes with a discussion on the sources and distribution of funding for capital projects within the travel and tourism industry.

FINANCE AND FUNDING IN

THE TRAVEL AND TOURISM

SECTOR

THE TRAVEL AND TOURISM

SECTOR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Importance of cost and volume analysis in financial management of travel and tourism

businesses...............................................................................................................................1

1.2 Pricing methods used in travel and tourism sector...........................................................2

1.3 Factors influencing profit for travel and tourism businesses............................................5

TASK 2............................................................................................................................................6

2.1 Different types of management accounting information..................................................6

2.2 Use of management accounting information as a decision-making tool..........................6

TASK 3............................................................................................................................................6

3.1 Financial performance of The Restaurant Group.............................................................6

Interpretation....................................................................................................................................7

TASK 4............................................................................................................................................9

4.1 Sources and distribution of funding for development of capital projects........................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Importance of cost and volume analysis in financial management of travel and tourism

businesses...............................................................................................................................1

1.2 Pricing methods used in travel and tourism sector...........................................................2

1.3 Factors influencing profit for travel and tourism businesses............................................5

TASK 2............................................................................................................................................6

2.1 Different types of management accounting information..................................................6

2.2 Use of management accounting information as a decision-making tool..........................6

TASK 3............................................................................................................................................6

3.1 Financial performance of The Restaurant Group.............................................................6

Interpretation....................................................................................................................................7

TASK 4............................................................................................................................................9

4.1 Sources and distribution of funding for development of capital projects........................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Finance plays a significant role in business to survive in the market. Funding is a process

of collecting money as well as allotting in the business. The present report describes about the

finance and funding in a travel and tourism industry which is the fast growing industry

worldwide. In present case, Merlin Entertainment Plc is used to describe about the finance and

funding. The report throws light on cost, volume and profit elements which play an important

role in managing financial accounts of the firm. It describes about management accounting

information as well as sources of finance. It gives overview of financial performance of The

Restaurant Group Plc.

TASK 1

1.1 Importance of cost and volume analysis in financial management of travel and tourism

businesses

Cost and volume is a term which is used by the financial managers to derive cost of

product and services. The analysis has various components such as fixed and variable cost, direct

and indirect cost etc. In this, the cost must be included in the product, price for selling the

product must be constant in a financial year and all units which are produced within an

accounting year must be sold in the market (Evans, Stonehouse, and Campbell, 2012). The

analysis is very important to Merlin Entertainment firm to manage financial situation. Various

importance of the cost volume analysis is given as below: Fixed cost: Fixed cost is a cost which does not change and vary according to the

production units. If the services and products of the firm will change then the cost will

remain constant in the travel and tourism enterprise. The cost plays important role to

derive a break even point of the firm and it is helpful to determine cost and price of the

product and service. It is a basic expense of the production process which cannot be

avoided by the organisation (Eagles, 2014). It will help the Merlin entertainment to know

about the total cost as well as to derive prices of services offered by the travel and

tourism company. Examples of fixed cost are rent of building, amortization, taxation

amount, depreciation on assets etc. Variable cost: It is a cost of product which varies according to the production volume. If

in the business, production level increases or decreases then variable cost gets fluctuate.

1

Finance plays a significant role in business to survive in the market. Funding is a process

of collecting money as well as allotting in the business. The present report describes about the

finance and funding in a travel and tourism industry which is the fast growing industry

worldwide. In present case, Merlin Entertainment Plc is used to describe about the finance and

funding. The report throws light on cost, volume and profit elements which play an important

role in managing financial accounts of the firm. It describes about management accounting

information as well as sources of finance. It gives overview of financial performance of The

Restaurant Group Plc.

TASK 1

1.1 Importance of cost and volume analysis in financial management of travel and tourism

businesses

Cost and volume is a term which is used by the financial managers to derive cost of

product and services. The analysis has various components such as fixed and variable cost, direct

and indirect cost etc. In this, the cost must be included in the product, price for selling the

product must be constant in a financial year and all units which are produced within an

accounting year must be sold in the market (Evans, Stonehouse, and Campbell, 2012). The

analysis is very important to Merlin Entertainment firm to manage financial situation. Various

importance of the cost volume analysis is given as below: Fixed cost: Fixed cost is a cost which does not change and vary according to the

production units. If the services and products of the firm will change then the cost will

remain constant in the travel and tourism enterprise. The cost plays important role to

derive a break even point of the firm and it is helpful to determine cost and price of the

product and service. It is a basic expense of the production process which cannot be

avoided by the organisation (Eagles, 2014). It will help the Merlin entertainment to know

about the total cost as well as to derive prices of services offered by the travel and

tourism company. Examples of fixed cost are rent of building, amortization, taxation

amount, depreciation on assets etc. Variable cost: It is a cost of product which varies according to the production volume. If

in the business, production level increases or decreases then variable cost gets fluctuate.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable cost varies in same direction of the production level for example; if production

level increases then variable cost will also increase. On the other hand, if output level

decreases then respective cost will decrease. It is very helpful to determine cost as well as

price of products and services. Example of variable cost are raw material cost, fuel cost,

labour cost, commission which charges on the basis of production level. Labour cost

fluctuates when cost charges as per the production units of the organisation. Direct cost: Another component of cost volume profit analysis is direct cost which is

incurred to produce products and services (Mancini, 2012). The cost is directly associated

with the production process as well as business entity. It is clearly associated in specific

activity of production process. In the business, very few direct costs are attached with the

total cost and with the specific activity of production. Direct costs of business are such as

direct material, direct labour, manufacturing supplies etc. The cost volume analysis is

important to determine direct cost of the products and services of the mentioned firm. Indirect cost: A cost which is not directly associated with production process is known as

indirect cost. The cost which is not directly accountable in total cost is the fixed cost or

variable cost. Indirect cost include various overhead cost which are associated with the

enterprise rather than total cost of goods and services. Indirect costs are such as

administration costs, labour overhead cost, security costs, personnel costs etc. These costs

are accounted in other costs instead of production cost of total cost. Administration costs

are such as utilities, rent of facilities as well as property and building, depreciation on

assets or equipments etc (Morrison, 2013).

Contribution margin: Contribution margin can be counted as a portion of profit. It is a

margin which remains after deducting all the variable expenses from total revenue or

sales of the organisation. The mentioned analysis is helpful for Merlin Entertainment to

derive contribution margin. Sum of money which remains is used by the firm to cover the

overall fixed cost and after that whatever remains is considered as a profit of the

organisation.

1.2 Pricing methods used in travel and tourism sector

Price is an important factor of an organisation and motto of the firm is to earn maximum

profit. . There are various pricing strategies which are helpful to the management at the time of

2

level increases then variable cost will also increase. On the other hand, if output level

decreases then respective cost will decrease. It is very helpful to determine cost as well as

price of products and services. Example of variable cost are raw material cost, fuel cost,

labour cost, commission which charges on the basis of production level. Labour cost

fluctuates when cost charges as per the production units of the organisation. Direct cost: Another component of cost volume profit analysis is direct cost which is

incurred to produce products and services (Mancini, 2012). The cost is directly associated

with the production process as well as business entity. It is clearly associated in specific

activity of production process. In the business, very few direct costs are attached with the

total cost and with the specific activity of production. Direct costs of business are such as

direct material, direct labour, manufacturing supplies etc. The cost volume analysis is

important to determine direct cost of the products and services of the mentioned firm. Indirect cost: A cost which is not directly associated with production process is known as

indirect cost. The cost which is not directly accountable in total cost is the fixed cost or

variable cost. Indirect cost include various overhead cost which are associated with the

enterprise rather than total cost of goods and services. Indirect costs are such as

administration costs, labour overhead cost, security costs, personnel costs etc. These costs

are accounted in other costs instead of production cost of total cost. Administration costs

are such as utilities, rent of facilities as well as property and building, depreciation on

assets or equipments etc (Morrison, 2013).

Contribution margin: Contribution margin can be counted as a portion of profit. It is a

margin which remains after deducting all the variable expenses from total revenue or

sales of the organisation. The mentioned analysis is helpful for Merlin Entertainment to

derive contribution margin. Sum of money which remains is used by the firm to cover the

overall fixed cost and after that whatever remains is considered as a profit of the

organisation.

1.2 Pricing methods used in travel and tourism sector

Price is an important factor of an organisation and motto of the firm is to earn maximum

profit. . There are various pricing strategies which are helpful to the management at the time of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

taking pricing decision. Merlin entertainment Plc also uses a pricing strategy to determine price

of its goods and services (Hamilton, 2014). Various pricing strategies are given as below: Cost plus pricing method: One of the most used pricing strategies is cost plus pricing

method where the price is determined on the basis of profit margin. This method is easy

and management can easily derive price of product without any obstacles. As per the

method, percentage of margin is added in total cost of production and the outcome is

considered as a price of services. Hence, total cost of product plus percentage of profit

will be price in the business. For example, suppose total cost is 100 and company want to

charge 20% of the profit, then price will be 100+20% = 120. Competition based pricing method: It is another method to set out the price of services in

business enterprise. According to the method, management charge price after comparing

pricing policy of its rivalry firms. In this, price is determined lower than competitor’s

who are serving same services to the consumers (Akyol, and KILINÇ, 2014). The method

is also used by the firm but sometimes it is unfavourable for the business conditions. For

example, price of travel service is 2000 in a business and its rivalry firm charges 1950 for

the same service. At this situation, the management of previous business will charge 1900

of the service. Hence, the prices are derived like this way according to the pricing

strategy. Marginal cost pricing method: Another method of pricing strategy is marginal cost

pricing method where only variable cost is considered to derive price of products. As per

this method, if production volume gets change then price of product also fluctuate in the

same direction of volume of production. The price will fluctuate because mentioned

method depends on the variable cost. Skimmed pricing method: As per skimmed pricing strategy, management charges higher

price at the initial stage of business (Page, 2014). When the company able to get higher

market share and increase number of customers in comparison to initial then prices will

charge lower. This strategy is highly effective and mostly used by the business entities.

Value added pricing method: According to the pricing method prices are determined as

per the quality of product and brand image of the company. When company have high

market share and good brand image then price of its product and service will be high in

3

of its goods and services (Hamilton, 2014). Various pricing strategies are given as below: Cost plus pricing method: One of the most used pricing strategies is cost plus pricing

method where the price is determined on the basis of profit margin. This method is easy

and management can easily derive price of product without any obstacles. As per the

method, percentage of margin is added in total cost of production and the outcome is

considered as a price of services. Hence, total cost of product plus percentage of profit

will be price in the business. For example, suppose total cost is 100 and company want to

charge 20% of the profit, then price will be 100+20% = 120. Competition based pricing method: It is another method to set out the price of services in

business enterprise. According to the method, management charge price after comparing

pricing policy of its rivalry firms. In this, price is determined lower than competitor’s

who are serving same services to the consumers (Akyol, and KILINÇ, 2014). The method

is also used by the firm but sometimes it is unfavourable for the business conditions. For

example, price of travel service is 2000 in a business and its rivalry firm charges 1950 for

the same service. At this situation, the management of previous business will charge 1900

of the service. Hence, the prices are derived like this way according to the pricing

strategy. Marginal cost pricing method: Another method of pricing strategy is marginal cost

pricing method where only variable cost is considered to derive price of products. As per

this method, if production volume gets change then price of product also fluctuate in the

same direction of volume of production. The price will fluctuate because mentioned

method depends on the variable cost. Skimmed pricing method: As per skimmed pricing strategy, management charges higher

price at the initial stage of business (Page, 2014). When the company able to get higher

market share and increase number of customers in comparison to initial then prices will

charge lower. This strategy is highly effective and mostly used by the business entities.

Value added pricing method: According to the pricing method prices are determined as

per the quality of product and brand image of the company. When company have high

market share and good brand image then price of its product and service will be high in

3

the market. Under this method company not consider price of any rivalry firms and

another components. Here only taste and preferences and goodwill of the company is to

be consider for derive price. The method widely used by organizations which have better

brand and high market share in industry.

In the present case Merlin Entertainment Plc is a UK based organisation and operating in

the travel and tourism sector. The firm provides its services to the consumers worldwide and

have a brand image in the mentioned fast growing industry (Readman, 2012). Hence, the

company using value added pricing strategy to determine price of its services. The company uses

the method because it offers good quality of services and have a brand image in eyes of

consumers. The company has various brands in the world such as FallsCreek, SEA-LIFE, Thorpe

Park etc. This brands are also using value added pricing method due to having brand image in the

world. Return on investment method: Another method is return on investment for derive cost of

product and services offered by the travel and tourism company. As per the method the

firm set prices on the basis of return which is made by management from investment. In

order to this when return of investment which is made by firm will high then prices goes

down. Higher the return on investment is better for the business organisations. The

method is very helpful to the managers to take decisions related to price fixing. High

return will lead to increase profit of the firm and when profit is high then company charge

less price of product by which more number of consumers attracts towards it.

Absorption cost pricing method: The method considers two variable of cost at the time

of taking decision of price fixing. The variables are such as fixed cost and variable cost

which help to management in order to take pricing decisions (Jayawardena, and et.al.,

2013). As per the method company analyse fixed and variable cost and derive total cost

of the production. Hence, the firm set out price of the product as per the total cost which

incurred in production process. Mostly firms are using the method for determine price to

sale products in market. Mentioned pricing method is very easy and total cost of

production is also covered.

4

another components. Here only taste and preferences and goodwill of the company is to

be consider for derive price. The method widely used by organizations which have better

brand and high market share in industry.

In the present case Merlin Entertainment Plc is a UK based organisation and operating in

the travel and tourism sector. The firm provides its services to the consumers worldwide and

have a brand image in the mentioned fast growing industry (Readman, 2012). Hence, the

company using value added pricing strategy to determine price of its services. The company uses

the method because it offers good quality of services and have a brand image in eyes of

consumers. The company has various brands in the world such as FallsCreek, SEA-LIFE, Thorpe

Park etc. This brands are also using value added pricing method due to having brand image in the

world. Return on investment method: Another method is return on investment for derive cost of

product and services offered by the travel and tourism company. As per the method the

firm set prices on the basis of return which is made by management from investment. In

order to this when return of investment which is made by firm will high then prices goes

down. Higher the return on investment is better for the business organisations. The

method is very helpful to the managers to take decisions related to price fixing. High

return will lead to increase profit of the firm and when profit is high then company charge

less price of product by which more number of consumers attracts towards it.

Absorption cost pricing method: The method considers two variable of cost at the time

of taking decision of price fixing. The variables are such as fixed cost and variable cost

which help to management in order to take pricing decisions (Jayawardena, and et.al.,

2013). As per the method company analyse fixed and variable cost and derive total cost

of the production. Hence, the firm set out price of the product as per the total cost which

incurred in production process. Mostly firms are using the method for determine price to

sale products in market. Mentioned pricing method is very easy and total cost of

production is also covered.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.3 Factors influencing profit for travel and tourism businesses

Profit is very sensitive element of the company and all the organisations are operated in

industry to earn the element. Profit is a sum of money which remains after deducting all the

direct and indirect expenditures of products and services from total sales and revenue. When

remaining amount is in positive value then considers as a profit while when amount remains is in

negative term then considers as a loss of the firm (Guiver, and Stanford, 2014). All companies

want to maximize profit from the production. Profit is an element which affects by various

factors in positive as well as negative manner in Merlin Entertainment Plc. Various factors by

which profit affected are given as below: Political environment: It is a major factor which impact on profit of travel and tourism

sector. Political factors are such as rule and regulations, policies of government for

services offered in international market, various taxation and tariff policies etc. When

taxes for travel and tourism industry will increase then it leads to increase cost of goods.

By increasing costs profit will be affected in negative terms. As per the rules and

regulations if rules are not in favour of the firm then hamper profitability of the company. Economic environment: Another factor is economic environment where recession and

inflation is majorly impact to the every organisation. Inflation is lead to increase price of

the products and services offered by the Merlin organisation. When prices are increase

then firm is not able to earn more profit in comparison to previous situation. Another

economic factors such as exchange rates and interest rates are also impacted to the profit

level in positive and negative manner (von der Weppen, and Cochrane, 2012). Sometimes

factors are fluctuated in favour of company and sometimes not. Social environment: Social factors are directly impact to sales of the products and

services. Various social factors are such as religion of people, marital status, economic

status, tastes and preferences of consumers, lifestyle of customers, education etc. As per

the factors when lifestyle of consumers change then they used to go for another products

and services which are suitable to them. In order to this when tastes and preferences are

change then consumers are not want same products and to fulfil that firm have to offer

another goods services which lead to increase cost. It will impact to profit of travel and

tourism business adversely.

5

Profit is very sensitive element of the company and all the organisations are operated in

industry to earn the element. Profit is a sum of money which remains after deducting all the

direct and indirect expenditures of products and services from total sales and revenue. When

remaining amount is in positive value then considers as a profit while when amount remains is in

negative term then considers as a loss of the firm (Guiver, and Stanford, 2014). All companies

want to maximize profit from the production. Profit is an element which affects by various

factors in positive as well as negative manner in Merlin Entertainment Plc. Various factors by

which profit affected are given as below: Political environment: It is a major factor which impact on profit of travel and tourism

sector. Political factors are such as rule and regulations, policies of government for

services offered in international market, various taxation and tariff policies etc. When

taxes for travel and tourism industry will increase then it leads to increase cost of goods.

By increasing costs profit will be affected in negative terms. As per the rules and

regulations if rules are not in favour of the firm then hamper profitability of the company. Economic environment: Another factor is economic environment where recession and

inflation is majorly impact to the every organisation. Inflation is lead to increase price of

the products and services offered by the Merlin organisation. When prices are increase

then firm is not able to earn more profit in comparison to previous situation. Another

economic factors such as exchange rates and interest rates are also impacted to the profit

level in positive and negative manner (von der Weppen, and Cochrane, 2012). Sometimes

factors are fluctuated in favour of company and sometimes not. Social environment: Social factors are directly impact to sales of the products and

services. Various social factors are such as religion of people, marital status, economic

status, tastes and preferences of consumers, lifestyle of customers, education etc. As per

the factors when lifestyle of consumers change then they used to go for another products

and services which are suitable to them. In order to this when tastes and preferences are

change then consumers are not want same products and to fulfil that firm have to offer

another goods services which lead to increase cost. It will impact to profit of travel and

tourism business adversely.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Seasonal variations: According to this method tourists prefer holidays and for cold

destinations they prefer summer season. In order to this business of travel and tourism

companies are not high in winter seasons and in off seasons. Hence, in the off season

fixed cost remain constant and variable are change but company have to bear fixed cost

which lead to decrease overall profit (Ji, Li, and King, 2016). To reduce this impact

company should charge higher price in season and lower price in off season by which

profit will equal in all seasons. Bed debts: As per the mentioned factor it majorly impact to the profit level of every

business entities. Debt is known as a long term loan of business which lead to affect

profit in negative terms. Bed debt is never recovered by businesses, in order to this when

company provide services on credit and consumer is not give amount to the firm. Here

the amount will be counted as a bed debt and it will affect to the profit of travel and

tourism organisation.

Planning: Planning is a process to run the business effectively and increase its financial

performance. When the company is not able to prepare and formulate proper plan then

cost will hamper by it (Rogerson, 2014). When cost hamper then ultimately profit get

fluctuate and impact to the overall financial performance of the mentioned business

organisation. The company need to make proper plan for every function of business

which will help to increase profit level.

TASK 2

2.1 Different types of management accounting information

2.2 Use of management accounting information as a decision-making tool

Enclosed in power point presentation

TASK 3

3.1 Financial performance of The Restaurant Group

Financial Ratios Formulas 2015 2014

Liquidity Ratios

Current Ratio Current Asset (CA) / Current

Liabilities (CL)

0.28 0.24

6

destinations they prefer summer season. In order to this business of travel and tourism

companies are not high in winter seasons and in off seasons. Hence, in the off season

fixed cost remain constant and variable are change but company have to bear fixed cost

which lead to decrease overall profit (Ji, Li, and King, 2016). To reduce this impact

company should charge higher price in season and lower price in off season by which

profit will equal in all seasons. Bed debts: As per the mentioned factor it majorly impact to the profit level of every

business entities. Debt is known as a long term loan of business which lead to affect

profit in negative terms. Bed debt is never recovered by businesses, in order to this when

company provide services on credit and consumer is not give amount to the firm. Here

the amount will be counted as a bed debt and it will affect to the profit of travel and

tourism organisation.

Planning: Planning is a process to run the business effectively and increase its financial

performance. When the company is not able to prepare and formulate proper plan then

cost will hamper by it (Rogerson, 2014). When cost hamper then ultimately profit get

fluctuate and impact to the overall financial performance of the mentioned business

organisation. The company need to make proper plan for every function of business

which will help to increase profit level.

TASK 2

2.1 Different types of management accounting information

2.2 Use of management accounting information as a decision-making tool

Enclosed in power point presentation

TASK 3

3.1 Financial performance of The Restaurant Group

Financial Ratios Formulas 2015 2014

Liquidity Ratios

Current Ratio Current Asset (CA) / Current

Liabilities (CL)

0.28 0.24

6

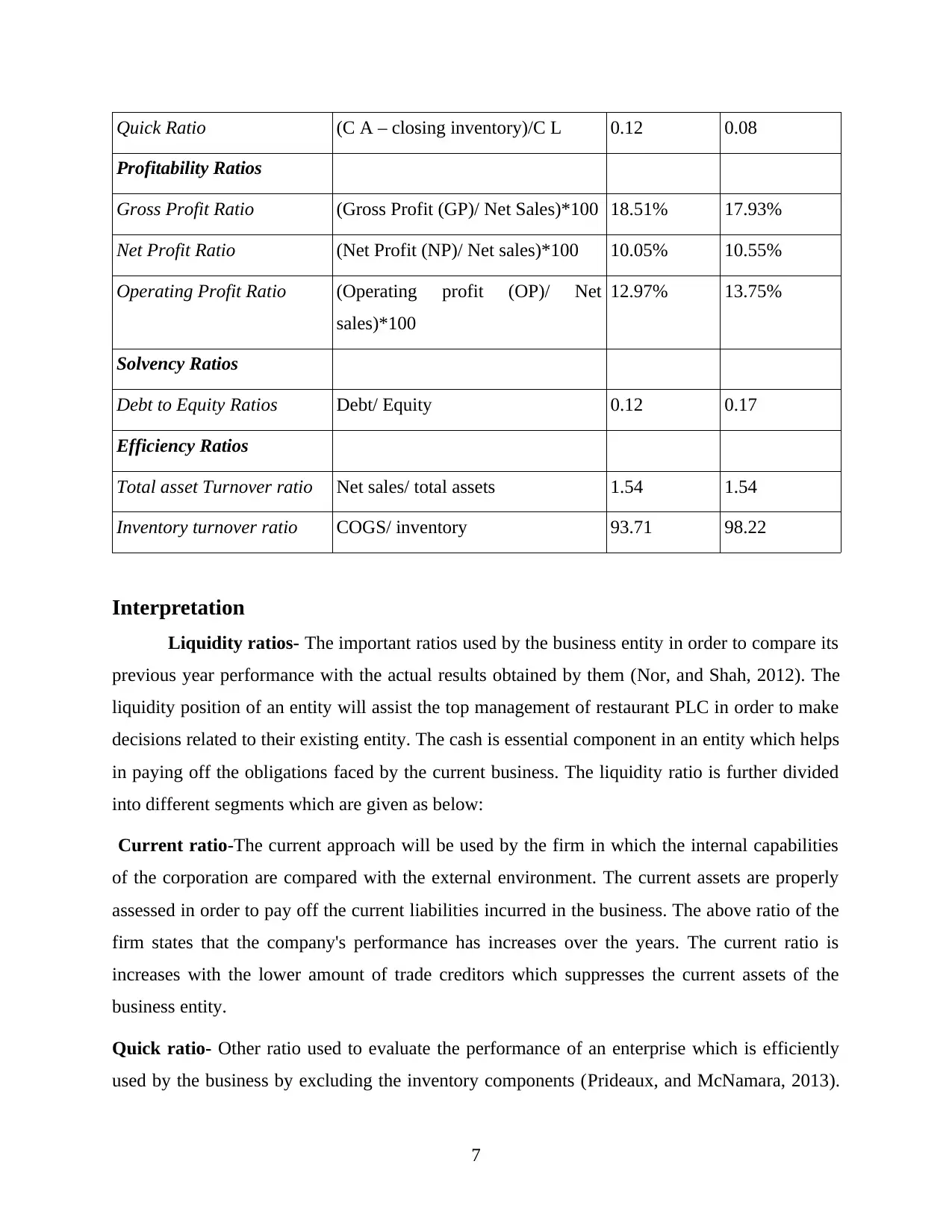

Quick Ratio (C A – closing inventory)/C L 0.12 0.08

Profitability Ratios

Gross Profit Ratio (Gross Profit (GP)/ Net Sales)*100 18.51% 17.93%

Net Profit Ratio (Net Profit (NP)/ Net sales)*100 10.05% 10.55%

Operating Profit Ratio (Operating profit (OP)/ Net

sales)*100

12.97% 13.75%

Solvency Ratios

Debt to Equity Ratios Debt/ Equity 0.12 0.17

Efficiency Ratios

Total asset Turnover ratio Net sales/ total assets 1.54 1.54

Inventory turnover ratio COGS/ inventory 93.71 98.22

Interpretation

Liquidity ratios- The important ratios used by the business entity in order to compare its

previous year performance with the actual results obtained by them (Nor, and Shah, 2012). The

liquidity position of an entity will assist the top management of restaurant PLC in order to make

decisions related to their existing entity. The cash is essential component in an entity which helps

in paying off the obligations faced by the current business. The liquidity ratio is further divided

into different segments which are given as below:

Current ratio-The current approach will be used by the firm in which the internal capabilities

of the corporation are compared with the external environment. The current assets are properly

assessed in order to pay off the current liabilities incurred in the business. The above ratio of the

firm states that the company's performance has increases over the years. The current ratio is

increases with the lower amount of trade creditors which suppresses the current assets of the

business entity.

Quick ratio- Other ratio used to evaluate the performance of an enterprise which is efficiently

used by the business by excluding the inventory components (Prideaux, and McNamara, 2013).

7

Profitability Ratios

Gross Profit Ratio (Gross Profit (GP)/ Net Sales)*100 18.51% 17.93%

Net Profit Ratio (Net Profit (NP)/ Net sales)*100 10.05% 10.55%

Operating Profit Ratio (Operating profit (OP)/ Net

sales)*100

12.97% 13.75%

Solvency Ratios

Debt to Equity Ratios Debt/ Equity 0.12 0.17

Efficiency Ratios

Total asset Turnover ratio Net sales/ total assets 1.54 1.54

Inventory turnover ratio COGS/ inventory 93.71 98.22

Interpretation

Liquidity ratios- The important ratios used by the business entity in order to compare its

previous year performance with the actual results obtained by them (Nor, and Shah, 2012). The

liquidity position of an entity will assist the top management of restaurant PLC in order to make

decisions related to their existing entity. The cash is essential component in an entity which helps

in paying off the obligations faced by the current business. The liquidity ratio is further divided

into different segments which are given as below:

Current ratio-The current approach will be used by the firm in which the internal capabilities

of the corporation are compared with the external environment. The current assets are properly

assessed in order to pay off the current liabilities incurred in the business. The above ratio of the

firm states that the company's performance has increases over the years. The current ratio is

increases with the lower amount of trade creditors which suppresses the current assets of the

business entity.

Quick ratio- Other ratio used to evaluate the performance of an enterprise which is efficiently

used by the business by excluding the inventory components (Prideaux, and McNamara, 2013).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The inventory us excluded as it will not easily convert into cash. The increasing ratio shows the

ability of an entity by raising its existing ability from one period to another.

Profitability- The existing variables of the income statements are assessed properly in

order to comment upon the profitability generated by the business over the years. The

profitability ratios are divided into various divisions which is mention below:

Gross profit- The raw profit produces by an entity by conducting all the business operations. It

is also regarded as the initial profit which is outcome generated by an entity by deducting the

cost of sales from the sales achieved by the business concern. This is increasing over the year

due to the less cost of sales incurred by the firm.

Operating profit- The profit generated by an entity after meeting various operating expenses

like general administration, selling and distribution expenses (Deluna Jr, and Jeon, 2014). The

Restaurant PLC are required to control their operating expenses as it reduces its operating profit.

Net profit- The complete profit generated by an enterprise which can be taken as the final profit

used to assess the final business efficiency. The burden of taxation has reduces the net profit

generated by an enterprise.

Solvency ratios-The ability of an enterprise need to be ensure properly in order to meet

the current obligations of the external market. The ability of the business are judged by counting

their internal abilities in relation to the external debt component.

Debt to equity ratio- The equity are assessed properly in order to beat and reduced the current

debt obligation imposed on this entity. The equity element need to be higher in order to eradicate

the higher imposition of the debt element as it carriers future interest to be paid to all the

investors. This ratio is decreasing which shows the inability of an enterprise in meeting their

external obligations.

Efficiency ratio- The ratio is related to the internal capabilities of the business enterprise

which need to be strong enough in order to meet their current market obligations (Pastras, and

Bramwell, 2013). The internal components are judged by applying various test in assessing the

true value of all the components to ensure the success of the business.

Total asset turnover- This ratio is used to assess the contribution of all the assets of an entity in

generating the sales and the revenue. The assets are important in generating higher sales which in

8

ability of an entity by raising its existing ability from one period to another.

Profitability- The existing variables of the income statements are assessed properly in

order to comment upon the profitability generated by the business over the years. The

profitability ratios are divided into various divisions which is mention below:

Gross profit- The raw profit produces by an entity by conducting all the business operations. It

is also regarded as the initial profit which is outcome generated by an entity by deducting the

cost of sales from the sales achieved by the business concern. This is increasing over the year

due to the less cost of sales incurred by the firm.

Operating profit- The profit generated by an entity after meeting various operating expenses

like general administration, selling and distribution expenses (Deluna Jr, and Jeon, 2014). The

Restaurant PLC are required to control their operating expenses as it reduces its operating profit.

Net profit- The complete profit generated by an enterprise which can be taken as the final profit

used to assess the final business efficiency. The burden of taxation has reduces the net profit

generated by an enterprise.

Solvency ratios-The ability of an enterprise need to be ensure properly in order to meet

the current obligations of the external market. The ability of the business are judged by counting

their internal abilities in relation to the external debt component.

Debt to equity ratio- The equity are assessed properly in order to beat and reduced the current

debt obligation imposed on this entity. The equity element need to be higher in order to eradicate

the higher imposition of the debt element as it carriers future interest to be paid to all the

investors. This ratio is decreasing which shows the inability of an enterprise in meeting their

external obligations.

Efficiency ratio- The ratio is related to the internal capabilities of the business enterprise

which need to be strong enough in order to meet their current market obligations (Pastras, and

Bramwell, 2013). The internal components are judged by applying various test in assessing the

true value of all the components to ensure the success of the business.

Total asset turnover- This ratio is used to assess the contribution of all the assets of an entity in

generating the sales and the revenue. The assets are important in generating higher sales which in

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

turn enhances the level of business enterprise. The stable position of an entity will indicate no

contribution applied by an entity.

Inventory turnover ratio: The ratio indicate that Restaurant Plc is how much efficient to

generate from its inventory. In the present scenario, in the accounting year 2014 inventory

turnover ratio is 98.22 and in the year 2015 it is decreases up to 93.71. It means company not

able to use its inventory in neat year.

TASK 4

4.1 Sources and distribution of funding for development of capital projects

Enclosed in Poster

CONCLUSION

It can be concluded from above project that Merlin Entertainment Plc is a travel and

tourism company which providing its services worldwide. It can be articulated that cost and

volume analysis is very important for every organisation to derive various costs and profit of the

product and services. Cost and volume is assists with various component of costs and useful for

the management. In order to this various pricing strategies which help to management of travel

and tourism company to derive prices of its goods and services. It can be concluded that

company use value added pricing method. Various management accounting information tools are

there which helps in business decision-making. It can be summarized that sources of finance are

useful for managers to develop projects.

9

contribution applied by an entity.

Inventory turnover ratio: The ratio indicate that Restaurant Plc is how much efficient to

generate from its inventory. In the present scenario, in the accounting year 2014 inventory

turnover ratio is 98.22 and in the year 2015 it is decreases up to 93.71. It means company not

able to use its inventory in neat year.

TASK 4

4.1 Sources and distribution of funding for development of capital projects

Enclosed in Poster

CONCLUSION

It can be concluded from above project that Merlin Entertainment Plc is a travel and

tourism company which providing its services worldwide. It can be articulated that cost and

volume analysis is very important for every organisation to derive various costs and profit of the

product and services. Cost and volume is assists with various component of costs and useful for

the management. In order to this various pricing strategies which help to management of travel

and tourism company to derive prices of its goods and services. It can be concluded that

company use value added pricing method. Various management accounting information tools are

there which helps in business decision-making. It can be summarized that sources of finance are

useful for managers to develop projects.

9

REFERENCES

Books and Journals

Akyol, M. and KILINÇ, Ö., 2014. Internet and Halal Tourism Marketing. Electronic Turkish

Studies. 9(8).

Deluna Jr, R. and Jeon, N., 2014. Determinants of International Tourism Demand for the

Philippines: An Augmented Gravity Model Approach.

Eagles, P.F., 2014. Fiscal implications of moving to tourism finance for parks: Ontario provincial

parks. Managing Leisure. 19(1). pp.1-17.

Evans, N., Stonehouse, G. and Campbell, D., 2012. Strategic management for travel and

tourism. Taylor & Francis.

Frerichs, A., and et.al., 2013. Usage of Pre-Made Text-Modules and Peer-Groups for Mitigating

Information Asymmetry in Social Lending: Evidence on Funding Success from German

Platform Smava. International Journal of E-Business Research (IJEBR). 9(3). pp.1-26.

Guiver, J. and Stanford, D., 2014. Why destination visitor travel planning falls between the

cracks. Journal of Destination Marketing & Management. 3(3). pp.140-151.

Hamilton, K., 2014. Wildlife conservation and environmental economics. Environment and

Development Economics. 19(03). pp.299-302.

Jayawardena, C., and et.al., 2013. Trends and sustainability in the Canadian tourism and

hospitality industry. Worldwide Hospitality and Tourism Themes. 5(2). pp.132-150.

Ji, M., Li, M. and King, B., 2016. Incremental Effects of the Shanghai Free-trade Zone—An

Internet Informed Assessment of Hong Kong’s Tourism Competitiveness. Journal of China

Tourism Research. pp.1-18.

Mancini, M., 2012. Access: Introduction to travel and tourism. Nelson Education.

Morrison, A.M., 2013. Marketing and managing tourism destinations. Routledge.

Nor, S. A. M. and Shah, D. R., 2012. Review and identification of tourism potentials of Isfahan

using SWOT model. Life Science Journal. 9(3).

Page, S.J., 2014. Tourism management. Routledge.

10

Books and Journals

Akyol, M. and KILINÇ, Ö., 2014. Internet and Halal Tourism Marketing. Electronic Turkish

Studies. 9(8).

Deluna Jr, R. and Jeon, N., 2014. Determinants of International Tourism Demand for the

Philippines: An Augmented Gravity Model Approach.

Eagles, P.F., 2014. Fiscal implications of moving to tourism finance for parks: Ontario provincial

parks. Managing Leisure. 19(1). pp.1-17.

Evans, N., Stonehouse, G. and Campbell, D., 2012. Strategic management for travel and

tourism. Taylor & Francis.

Frerichs, A., and et.al., 2013. Usage of Pre-Made Text-Modules and Peer-Groups for Mitigating

Information Asymmetry in Social Lending: Evidence on Funding Success from German

Platform Smava. International Journal of E-Business Research (IJEBR). 9(3). pp.1-26.

Guiver, J. and Stanford, D., 2014. Why destination visitor travel planning falls between the

cracks. Journal of Destination Marketing & Management. 3(3). pp.140-151.

Hamilton, K., 2014. Wildlife conservation and environmental economics. Environment and

Development Economics. 19(03). pp.299-302.

Jayawardena, C., and et.al., 2013. Trends and sustainability in the Canadian tourism and

hospitality industry. Worldwide Hospitality and Tourism Themes. 5(2). pp.132-150.

Ji, M., Li, M. and King, B., 2016. Incremental Effects of the Shanghai Free-trade Zone—An

Internet Informed Assessment of Hong Kong’s Tourism Competitiveness. Journal of China

Tourism Research. pp.1-18.

Mancini, M., 2012. Access: Introduction to travel and tourism. Nelson Education.

Morrison, A.M., 2013. Marketing and managing tourism destinations. Routledge.

Nor, S. A. M. and Shah, D. R., 2012. Review and identification of tourism potentials of Isfahan

using SWOT model. Life Science Journal. 9(3).

Page, S.J., 2014. Tourism management. Routledge.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.