Finance & Funding: Analysis of Travel and Tourism Businesses

VerifiedAdded on 2024/05/31

|16

|5172

|423

Report

AI Summary

This report provides a financial analysis of the travel and tourism sector, focusing on funding sources, cost management, and profitability. It examines the importance of cost and volume in financial management, evaluates pricing methods, and identifies factors influencing profit in the travel and tourism business. The report also discusses various types of management accounting information and their use in decision-making. Through an analysis of companies like Dalata Hotel Group Plc. and Carnival Corporation and Plc., the study highlights the application of accounting tools such as payback period and rate of accounting return. It further explores the sources and distribution of funding for capital projects in the tourism industry, offering insights for organizations to optimize financial performance and investment strategies. The report concludes by emphasizing the importance of effective financial management for sustainable growth in the travel and tourism sector.

FINANCE AND FUNDING IN THE TRAVEL AND TOURISM

SECTOR

1

SECTOR

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The study has been made on the basis of financial performance in the hospitality as well as the

business of tours and travels. The study has helped to derive the financial performance of Dalata

Hotel Group Plc. and the Carnival Corporation and Plc. In the conducted study, there has been

found the proper accounting tool for an organisation, which will help the management team of

the respective organisation to evaluate the profitability. This study has evaluated the process to

gain the maximum return on the total investment on the capital projects, which have been made

by the investors as well as the owners of the organisation. The appropriate decision-making tool

for the management of the concerned organisations has been determined from the conducted

study. There have been found the sources of the finding that can be distributed to the various

projects of the organisation. By implementing the technique of payback period accounting tool,

the relative organisation can easily derive higher profitability from the investment made on the

capital project. With the help of rate of accounting of earned return technique, difference

between the estimated return amount and the actual return amount on the total investment can be

derived. The small scale organisation can select short-term loans instead of long-term loans, to

avoid the negative impacts of investing in the capital projects. This is because short-term loan

there may be less of risks in the investment.

2

The study has been made on the basis of financial performance in the hospitality as well as the

business of tours and travels. The study has helped to derive the financial performance of Dalata

Hotel Group Plc. and the Carnival Corporation and Plc. In the conducted study, there has been

found the proper accounting tool for an organisation, which will help the management team of

the respective organisation to evaluate the profitability. This study has evaluated the process to

gain the maximum return on the total investment on the capital projects, which have been made

by the investors as well as the owners of the organisation. The appropriate decision-making tool

for the management of the concerned organisations has been determined from the conducted

study. There have been found the sources of the finding that can be distributed to the various

projects of the organisation. By implementing the technique of payback period accounting tool,

the relative organisation can easily derive higher profitability from the investment made on the

capital project. With the help of rate of accounting of earned return technique, difference

between the estimated return amount and the actual return amount on the total investment can be

derived. The small scale organisation can select short-term loans instead of long-term loans, to

avoid the negative impacts of investing in the capital projects. This is because short-term loan

there may be less of risks in the investment.

2

Table of contents

Introduction......................................................................................................................................4

Aim..................................................................................................................................................4

Task 1 (LO1, AC1.1, 1.2, 1.3, M1, M2, M3, D1, D2, D3)..............................................................4

1.1 Importance of cost and volume in context to financial management of tourism and travel......4

1.2 Evaluation of pricing methods in context to travel and tourism..............................................5

1.3 Factors which influence profit in relation to travel and tourism business...............................7

Task2 (LO2, AC2.1, 2.2, M1, M2, M3, D1, D2, D3)......................................................................8

2.1 Various types of management accounting information.............................................................8

2.2 Assessment of the use of management accounting as a decision-making tool........................10

Task3 (LO3, AC3.1, M1, M2, M3, D1, D2, D3)...........................................................................12

3.1 Financial accounts of travel and tourism.................................................................................12

Task 4 (LO4, AC4.1, M1, M2, M3, D1, D2, D3)..........................................................................13

4.1 Sources and distribution of funding.........................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

3

Introduction......................................................................................................................................4

Aim..................................................................................................................................................4

Task 1 (LO1, AC1.1, 1.2, 1.3, M1, M2, M3, D1, D2, D3)..............................................................4

1.1 Importance of cost and volume in context to financial management of tourism and travel......4

1.2 Evaluation of pricing methods in context to travel and tourism..............................................5

1.3 Factors which influence profit in relation to travel and tourism business...............................7

Task2 (LO2, AC2.1, 2.2, M1, M2, M3, D1, D2, D3)......................................................................8

2.1 Various types of management accounting information.............................................................8

2.2 Assessment of the use of management accounting as a decision-making tool........................10

Task3 (LO3, AC3.1, M1, M2, M3, D1, D2, D3)...........................................................................12

3.1 Financial accounts of travel and tourism.................................................................................12

Task 4 (LO4, AC4.1, M1, M2, M3, D1, D2, D3)..........................................................................13

4.1 Sources and distribution of funding.........................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This study revolves around the understanding of the gains, cost, and volume, management

accounting techniques in relation to the travel and tourism industry. This report deals with the

importance of volume and cost in accordance to the financial management of travel and tourism.

It sheds light on the evaluation and analysis the pricing methods for travel and tourism. The

factors which influence profit in the travel and tourism sector are catered in details. The types of

management accounting information are driven in this study. The uses of decision making

pertaining to the management are evaluated in this report. The interpretation of the travel and

tourism is grounded on the basis of financial stature. The analysis is pertained in this study in

context to the distribution of funding and sources in context to the development of the capital

projects in association with tourism. Cost is determined in the form of direct cost, fixed cost,

variable cost, indirect cost, and allocation and apportionment. The financial performance is

measured in accordance to the test ratio, current ratio, capital gearing return on assets and others.

Aim

The aim of this report is to determine the costs, profits, volume, sources and distribution of

funding and management accounting information in context to the travel and tourism industry.

Task 1 (LO1, AC1.1, 1.2, 1.3, M1, M2, M3, D1, D2, D3)

1.1 Importance of cost and volume in context to financial management of

tourism and travel

Evaluation and understanding of the cost and volume is in relation to the breakeven point. For

the determining this, there are various assumptions which are accorded in context to finding the

volumes and cost. As commented by Becker (2016, p. 22), the assumptions can be generated by

the units sold or the variable and fixed costs. Variable cost is basically the cost that varies in

context to the services provided or the production volume. Fixed cost is identified as the cost

4

This study revolves around the understanding of the gains, cost, and volume, management

accounting techniques in relation to the travel and tourism industry. This report deals with the

importance of volume and cost in accordance to the financial management of travel and tourism.

It sheds light on the evaluation and analysis the pricing methods for travel and tourism. The

factors which influence profit in the travel and tourism sector are catered in details. The types of

management accounting information are driven in this study. The uses of decision making

pertaining to the management are evaluated in this report. The interpretation of the travel and

tourism is grounded on the basis of financial stature. The analysis is pertained in this study in

context to the distribution of funding and sources in context to the development of the capital

projects in association with tourism. Cost is determined in the form of direct cost, fixed cost,

variable cost, indirect cost, and allocation and apportionment. The financial performance is

measured in accordance to the test ratio, current ratio, capital gearing return on assets and others.

Aim

The aim of this report is to determine the costs, profits, volume, sources and distribution of

funding and management accounting information in context to the travel and tourism industry.

Task 1 (LO1, AC1.1, 1.2, 1.3, M1, M2, M3, D1, D2, D3)

1.1 Importance of cost and volume in context to financial management of

tourism and travel

Evaluation and understanding of the cost and volume is in relation to the breakeven point. For

the determining this, there are various assumptions which are accorded in context to finding the

volumes and cost. As commented by Becker (2016, p. 22), the assumptions can be generated by

the units sold or the variable and fixed costs. Variable cost is basically the cost that varies in

context to the services provided or the production volume. Fixed cost is identified as the cost

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which does not change and is unavoidable in any business. The fixed cost can be determined by

insurance, property taxes and the depreciation. The breakeven point is analysed with the help of

this tool. In this context the variable and fixed sales remain constant. In accordance to the

tourism and travel the CVP plays an innate role to analyse the financial matter of the

organization. The fixed costs are entailed on a regular basis and are also often termed as period

costs. The needs of the future are evaluated and analyzed in an efficient and effective regard in

the Carnival Corporation and plc Company (carnivalcorp.com, 2018). The effective decisions are

enabled through this CVP analysis so the company always remain in profit. It also provides with

information that helps the company to analyze the situation. For example, the profit and loss can

be determined using this tool. The variable fixed cost is regarded for an effective and efficient

performance. Apart from the fixed variable, the volume, cost and sales are incorporated to

enhance the efficiency of the organization and the business. Obtaining the data is mostly easy as

the result can be derived by putting the formula. It is a simple tool as extra efforts are not needed

to derive the results. The allocation of the fixed costs is generated on the basis of the absorption

in context to the accounting of costs. The overhead costs and fixed manufacturing cost are

generally assigned and are recorded. After the selling of the units the charge is generated on the

basis of the cost of sold goods. However, the effective result in the travel and tourism can be

generated by the CVP analysis.

1.2 Evaluation of pricing methods in context to travel and tourism

Earning profit is very vital for any organisation. The profit of the business is very important to

maintain efficient and effective management system. The pricing aspect is very crucial as it

determine the price of the goods and the services. There are several methods which help to

analyse the pricing methods in context to the travel and tourism. This includes cost oriented

pricing method, target pricing, market oriented pricing method, transfer pricing and going rate

pricing.

Cost oriented pricing method

Margins are enabled that enables to derive the profit in context to the business. Profits can be

determined easily in context to pricing.

5

insurance, property taxes and the depreciation. The breakeven point is analysed with the help of

this tool. In this context the variable and fixed sales remain constant. In accordance to the

tourism and travel the CVP plays an innate role to analyse the financial matter of the

organization. The fixed costs are entailed on a regular basis and are also often termed as period

costs. The needs of the future are evaluated and analyzed in an efficient and effective regard in

the Carnival Corporation and plc Company (carnivalcorp.com, 2018). The effective decisions are

enabled through this CVP analysis so the company always remain in profit. It also provides with

information that helps the company to analyze the situation. For example, the profit and loss can

be determined using this tool. The variable fixed cost is regarded for an effective and efficient

performance. Apart from the fixed variable, the volume, cost and sales are incorporated to

enhance the efficiency of the organization and the business. Obtaining the data is mostly easy as

the result can be derived by putting the formula. It is a simple tool as extra efforts are not needed

to derive the results. The allocation of the fixed costs is generated on the basis of the absorption

in context to the accounting of costs. The overhead costs and fixed manufacturing cost are

generally assigned and are recorded. After the selling of the units the charge is generated on the

basis of the cost of sold goods. However, the effective result in the travel and tourism can be

generated by the CVP analysis.

1.2 Evaluation of pricing methods in context to travel and tourism

Earning profit is very vital for any organisation. The profit of the business is very important to

maintain efficient and effective management system. The pricing aspect is very crucial as it

determine the price of the goods and the services. There are several methods which help to

analyse the pricing methods in context to the travel and tourism. This includes cost oriented

pricing method, target pricing, market oriented pricing method, transfer pricing and going rate

pricing.

Cost oriented pricing method

Margins are enabled that enables to derive the profit in context to the business. Profits can be

determined easily in context to pricing.

5

Target pricing

It is initiated by identification of the price to which the service can be generated as profitable in

the, market. The target can be computed by the subtraction of the profit in context to the market

price.

Market oriented pricing method

The price is generated by the prevailing competition. This method is determined by the

competition in the market arena. The Carnival Corporation and plc Company is planning a tour

to Australia to which the charges will be £ 40,000 for travel and hotel expenses. The meal

charges will be around £ 160 variable cost per tourist. As commented by Walker and Walker

(2016, p. 2), the Cost oriented pricing is generated in the business arena because it serves as an

efficient margin in context to the business that can result in profit and effectiveness of the

business.

Transfer pricing

As commented by Standing et al. (2014, p. 83), it generally refers to the price initiated for the

transfer of goods from one place to another. For example, transfer of goods from one economic

unit to the other.

Going rate pricing

It is a method in which price is initiated on the basis of the current market price. However, there

are several components which are to be kept in mind in context to pricing strategies. As

commented by Mahrous and Hassan (2017, p. 1049), these include rack rates, seasonal pricing

and last minute pricing. Tourism is a complex market industry and pricing is a major component

of this industry. There are certain common pricing types which includes per person pricing,

6

It is initiated by identification of the price to which the service can be generated as profitable in

the, market. The target can be computed by the subtraction of the profit in context to the market

price.

Market oriented pricing method

The price is generated by the prevailing competition. This method is determined by the

competition in the market arena. The Carnival Corporation and plc Company is planning a tour

to Australia to which the charges will be £ 40,000 for travel and hotel expenses. The meal

charges will be around £ 160 variable cost per tourist. As commented by Walker and Walker

(2016, p. 2), the Cost oriented pricing is generated in the business arena because it serves as an

efficient margin in context to the business that can result in profit and effectiveness of the

business.

Transfer pricing

As commented by Standing et al. (2014, p. 83), it generally refers to the price initiated for the

transfer of goods from one place to another. For example, transfer of goods from one economic

unit to the other.

Going rate pricing

It is a method in which price is initiated on the basis of the current market price. However, there

are several components which are to be kept in mind in context to pricing strategies. As

commented by Mahrous and Hassan (2017, p. 1049), these include rack rates, seasonal pricing

and last minute pricing. Tourism is a complex market industry and pricing is a major component

of this industry. There are certain common pricing types which includes per person pricing,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

single and double occupancy and per unit pricing.

Figure1: Pricing Methods

(Source: Learner)

1.3 Factors which influence profit in relation to travel and tourism business

The factors which generate profit for the Carnival Corporation and Plc are-

Efficient management strategies are effective to influence profit to the tourism and travel

business. As commented by Sharpley and McGrath (2017, p. 65), the manner of planning the

tours are responsible for the generation of profit. If the planning is done on a effective manner

than the profit rate will be high. There are several strategies which can be generated to gain

profit. For example, advertising is a very vital component in the travel and tourism industry.

Promoting the company can enhance the growth of the potential customers. As commented by

Tigre Moura et al. (2015, p. 528), market is all about competition and several promotional

campaigns are entailed by the companies to maintain their profit growth. Tours and travelling

business can be advertised in the social platform by using various social media channels.

Understanding the customers and making an effort to provide their want can also result in the

positive growth for the travel and tourism business. As commented by Varasteh et al. (2015, p.

131), travel and tourism is most dependent on their consumers and providing the facilities that

the consumers are looking for can procure the profit rates in context to the Company. Offering an

7

Figure1: Pricing Methods

(Source: Learner)

1.3 Factors which influence profit in relation to travel and tourism business

The factors which generate profit for the Carnival Corporation and Plc are-

Efficient management strategies are effective to influence profit to the tourism and travel

business. As commented by Sharpley and McGrath (2017, p. 65), the manner of planning the

tours are responsible for the generation of profit. If the planning is done on a effective manner

than the profit rate will be high. There are several strategies which can be generated to gain

profit. For example, advertising is a very vital component in the travel and tourism industry.

Promoting the company can enhance the growth of the potential customers. As commented by

Tigre Moura et al. (2015, p. 528), market is all about competition and several promotional

campaigns are entailed by the companies to maintain their profit growth. Tours and travelling

business can be advertised in the social platform by using various social media channels.

Understanding the customers and making an effort to provide their want can also result in the

positive growth for the travel and tourism business. As commented by Varasteh et al. (2015, p.

131), travel and tourism is most dependent on their consumers and providing the facilities that

the consumers are looking for can procure the profit rates in context to the Company. Offering an

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

exceptional experience with best accommodation in renowned hotels, providing good meal are

required to grab consumers.

In this context, the Carnival Corporation and plc is a supreme travel company where the amount

charged for accommodation is £ 70,000 including various fares (flight, bus, and car). There were

a total of 70 tourists. The meal charges were £ 160 per head (variable cost). There are a total of

70 tourists so the variable cost is £ 160*70 that is equal to £ 11200. The total cost is generally the

addition of the variable and fixed cost which is £ 73,000 after certain discounts. The business

organization is charging £ 900 per individual so the amount charged is £72000. Thus this states

that the organization is generating a loss of £ 1500. The estimated profit decided by the

organization was £ 10000 so it is required by the organization to charge £ 927.77 per head.

Accommodation

Fares

£ 70000

Total cost £160 per person

Total tourists 70 people

Variable cost 160*70= £ 11200

Table 1: variable cost

(Source: Learner)

As commented by Law et al. (2015, p. 431), calculating the variable cost is very simple and

effective to determine the profit. It is simply done by multiplying the total number of tourists

with the total cost.

Task2 (LO2, AC2.1, 2.2, M1, M2, M3, D1, D2, D3)

2.1 Various types of management accounting information

The management accounting in the travel and tourism business is helpful as it helps to manage

and collect data from time to time. It also looks after the working system in internal and external

terms. As commented by Dickinson et al. (2014, p. 84), the accounting is done on the time to

time basis as if any conflict rises, than it can resolved immediately. Defaults generally reduce the

effectiveness and efficiency of the business and managing the flaws of the organization will help

8

required to grab consumers.

In this context, the Carnival Corporation and plc is a supreme travel company where the amount

charged for accommodation is £ 70,000 including various fares (flight, bus, and car). There were

a total of 70 tourists. The meal charges were £ 160 per head (variable cost). There are a total of

70 tourists so the variable cost is £ 160*70 that is equal to £ 11200. The total cost is generally the

addition of the variable and fixed cost which is £ 73,000 after certain discounts. The business

organization is charging £ 900 per individual so the amount charged is £72000. Thus this states

that the organization is generating a loss of £ 1500. The estimated profit decided by the

organization was £ 10000 so it is required by the organization to charge £ 927.77 per head.

Accommodation

Fares

£ 70000

Total cost £160 per person

Total tourists 70 people

Variable cost 160*70= £ 11200

Table 1: variable cost

(Source: Learner)

As commented by Law et al. (2015, p. 431), calculating the variable cost is very simple and

effective to determine the profit. It is simply done by multiplying the total number of tourists

with the total cost.

Task2 (LO2, AC2.1, 2.2, M1, M2, M3, D1, D2, D3)

2.1 Various types of management accounting information

The management accounting in the travel and tourism business is helpful as it helps to manage

and collect data from time to time. It also looks after the working system in internal and external

terms. As commented by Dickinson et al. (2014, p. 84), the accounting is done on the time to

time basis as if any conflict rises, than it can resolved immediately. Defaults generally reduce the

effectiveness and efficiency of the business and managing the flaws of the organization will help

8

to cater good services to the consumers. The various types of management accounting

information are-

Cost allocation report

In this context the allocation is generalized on the basis of resources pertaining ion the business.

They are needed to be present in the early stages so that no complex situation can pertain in the

future. This method is useful as it is helpful to keep an ongoing track or record of the outcomes

related to the business. As commented by Ormond and Sulianti (2017, p. 95), monitoring over

the functions of the business are procured to be helpful in the long run.

In this regard, the Dalata Hotel has planned to earn an estimate of £ 10,000 from their hotel

business. The Dalata hotel has also estimated to earn £ 200000 from their hotels in the Ireland

and UK. The evaluation of the accounting needs to be good to gain profits to an organization. A

bad accounting system will not be able to generate profits in the long run.

Budget report

The budget report is basically a documentation in which the expenses of the future are entailed in

details. The management accounting helps to take in all the future expenses and this is

considered as the best possible way of documenting the reports of the future. The budget report

of a company has several sections depending upon the various financial needs and data in

context to the business. As commented by Mowforth and Munt (2015, p. 2), this includes the

sales information, general income, flexible and fixed expenses. Sometimes the budget reports

(extensive) also includes a letter in context to the financial changes and predictions of the

business. A budget report can be big or small depending on the size of the Company. In this

context, the Dalata Hotel Group plc is having around 38 hotels of three and four stars. So the

budget report of the company will be a big report with graphs and charts. The budget reports

containing future predictions are entailed with the charts and graphs to procure the growth plans

of the organization.

Job cost report

This report is basically the starting point of the data pertaining in the other reports. This lists all

the costs in context to the previous period. The main focus lies on the business arena from where

extra profit can be generated. In this regard, no efforts, time and money are invested on the non

profitable components. The respects through which profits can be evaluated and analysed are

generated in this report in context to the profit generation projects. However, a good estimation

9

information are-

Cost allocation report

In this context the allocation is generalized on the basis of resources pertaining ion the business.

They are needed to be present in the early stages so that no complex situation can pertain in the

future. This method is useful as it is helpful to keep an ongoing track or record of the outcomes

related to the business. As commented by Ormond and Sulianti (2017, p. 95), monitoring over

the functions of the business are procured to be helpful in the long run.

In this regard, the Dalata Hotel has planned to earn an estimate of £ 10,000 from their hotel

business. The Dalata hotel has also estimated to earn £ 200000 from their hotels in the Ireland

and UK. The evaluation of the accounting needs to be good to gain profits to an organization. A

bad accounting system will not be able to generate profits in the long run.

Budget report

The budget report is basically a documentation in which the expenses of the future are entailed in

details. The management accounting helps to take in all the future expenses and this is

considered as the best possible way of documenting the reports of the future. The budget report

of a company has several sections depending upon the various financial needs and data in

context to the business. As commented by Mowforth and Munt (2015, p. 2), this includes the

sales information, general income, flexible and fixed expenses. Sometimes the budget reports

(extensive) also includes a letter in context to the financial changes and predictions of the

business. A budget report can be big or small depending on the size of the Company. In this

context, the Dalata Hotel Group plc is having around 38 hotels of three and four stars. So the

budget report of the company will be a big report with graphs and charts. The budget reports

containing future predictions are entailed with the charts and graphs to procure the growth plans

of the organization.

Job cost report

This report is basically the starting point of the data pertaining in the other reports. This lists all

the costs in context to the previous period. The main focus lies on the business arena from where

extra profit can be generated. In this regard, no efforts, time and money are invested on the non

profitable components. The respects through which profits can be evaluated and analysed are

generated in this report in context to the profit generation projects. However, a good estimation

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is required in order to attain job costing report. As commented by Forno and Garibaldi (2015, p.

202), arrangement of the estimates in cost categories are used to get the actual cost information.

Figure 2: Management Accounting

(Source: Learner)

2.2 Assessment of the use of management accounting as a decision-making

tool

An organisation always has been found with the tendency of investing the maximum funds into

the capital projects. In accordance with the statements of Seetanah and Sannassee (2015, 211), it

has been known that the capital projects of a business are able to obtain comparatively maximum

profit. It has also been found that the larger projects of a business to generate a huge amount of

return on the respective investment of the organisation. From the comments provided by

Giaoutzi (2017, p. 78), it can be seen that there are different techniques, which have been using

in the analysis of the estimated profit that can be obtained from the respective business project.

These techniques also help to predict the returnable amount of the total investment made by the

organisation. These techniques have been listed as follows:

Rate of accounting of earned return

The rate of accounting of the earned return on the total investment of the business on the

respective capital project reflects the differentiation among the amounts. In accordance with the

10

BudgetreportJobcostreport

202), arrangement of the estimates in cost categories are used to get the actual cost information.

Figure 2: Management Accounting

(Source: Learner)

2.2 Assessment of the use of management accounting as a decision-making

tool

An organisation always has been found with the tendency of investing the maximum funds into

the capital projects. In accordance with the statements of Seetanah and Sannassee (2015, 211), it

has been known that the capital projects of a business are able to obtain comparatively maximum

profit. It has also been found that the larger projects of a business to generate a huge amount of

return on the respective investment of the organisation. From the comments provided by

Giaoutzi (2017, p. 78), it can be seen that there are different techniques, which have been using

in the analysis of the estimated profit that can be obtained from the respective business project.

These techniques also help to predict the returnable amount of the total investment made by the

organisation. These techniques have been listed as follows:

Rate of accounting of earned return

The rate of accounting of the earned return on the total investment of the business on the

respective capital project reflects the differentiation among the amounts. In accordance with the

10

BudgetreportJobcostreport

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

words provided by Chen et al. (2016, p. 155), it can be said that the respective technique has

taken into consideration the amount of total investment, and the obtained return amount, which

has been derived from the capital project of the business. With the help of this technique,

difference between the estimated return amount and the actual return amount on the total

investment can be derived. As per the statements of Goodwin (2015, p. 37), it can be said that

this technique is comparatively easy and simple for using the management as an accounting tool.

Cash flow of discounted amount

In the cash flow of the discounted amount, it has been seen that the rate of the discounted amount

has been made on the total return that can be derived from the capital project. As per the

statements were given by Luh Sin et al. (2015, p. 125), it can be said that the cash flow refers to

the rate of the discount that can be derived from the amount of return, in the future outcome of

the project that has possessed the maximum investment.

Risk in investment and analysis of the sensitivity

There can be found various risks related to the investment of the organisation that has been made

on the capital project for gaining higher profit from the total investment. As per the statements

provided by Alegre and Pou (2016, p. 615), it can be said that all the risks, which have been

found to be associated with complete investment made by the organisation would have the

requirement of analysing properly. This will help the management team of the organisation to

take measures against the relative risks. The adopted measures will help the management to

reduce or to prevent the negative impacts of the respective risks. This will literally help the

organisation to suffer from the financial depression.

Payback period

It has been found that the payback period has been chosen as the most efficient as well as

effective tool of accounting, which has be4en used by the management of the respective

organisation on a larger scale. From the words of Padurean et al. (2015, p. 180), it can be said

that this accounting tool is mostly being used in the small-scale business. By implementing the

respective accounting tool, the relative organisation can easily derive higher profitability from

the investment made on the capital project.

11

taken into consideration the amount of total investment, and the obtained return amount, which

has been derived from the capital project of the business. With the help of this technique,

difference between the estimated return amount and the actual return amount on the total

investment can be derived. As per the statements of Goodwin (2015, p. 37), it can be said that

this technique is comparatively easy and simple for using the management as an accounting tool.

Cash flow of discounted amount

In the cash flow of the discounted amount, it has been seen that the rate of the discounted amount

has been made on the total return that can be derived from the capital project. As per the

statements were given by Luh Sin et al. (2015, p. 125), it can be said that the cash flow refers to

the rate of the discount that can be derived from the amount of return, in the future outcome of

the project that has possessed the maximum investment.

Risk in investment and analysis of the sensitivity

There can be found various risks related to the investment of the organisation that has been made

on the capital project for gaining higher profit from the total investment. As per the statements

provided by Alegre and Pou (2016, p. 615), it can be said that all the risks, which have been

found to be associated with complete investment made by the organisation would have the

requirement of analysing properly. This will help the management team of the organisation to

take measures against the relative risks. The adopted measures will help the management to

reduce or to prevent the negative impacts of the respective risks. This will literally help the

organisation to suffer from the financial depression.

Payback period

It has been found that the payback period has been chosen as the most efficient as well as

effective tool of accounting, which has be4en used by the management of the respective

organisation on a larger scale. From the words of Padurean et al. (2015, p. 180), it can be said

that this accounting tool is mostly being used in the small-scale business. By implementing the

respective accounting tool, the relative organisation can easily derive higher profitability from

the investment made on the capital project.

11

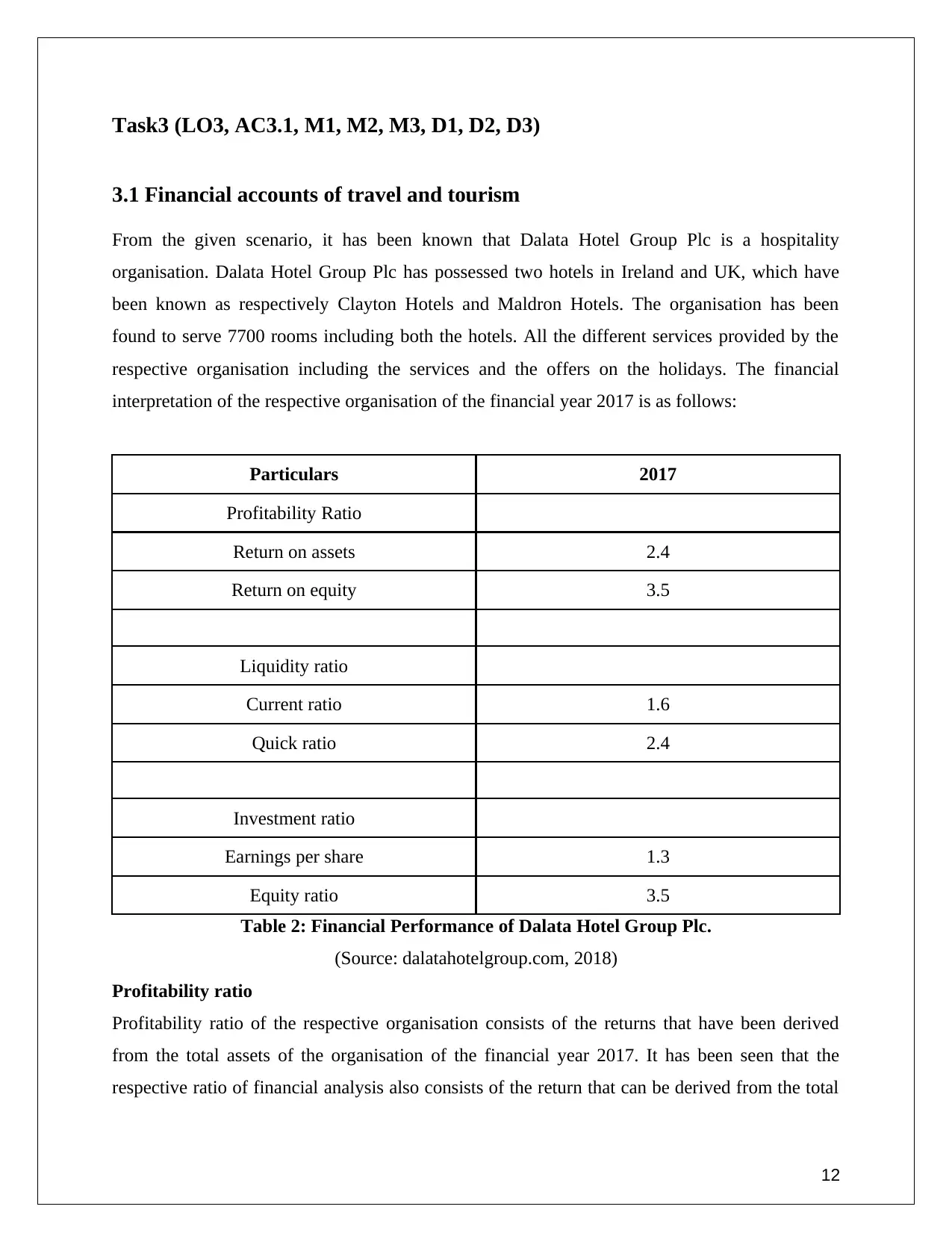

Task3 (LO3, AC3.1, M1, M2, M3, D1, D2, D3)

3.1 Financial accounts of travel and tourism

From the given scenario, it has been known that Dalata Hotel Group Plc is a hospitality

organisation. Dalata Hotel Group Plc has possessed two hotels in Ireland and UK, which have

been known as respectively Clayton Hotels and Maldron Hotels. The organisation has been

found to serve 7700 rooms including both the hotels. All the different services provided by the

respective organisation including the services and the offers on the holidays. The financial

interpretation of the respective organisation of the financial year 2017 is as follows:

Particulars 2017

Profitability Ratio

Return on assets 2.4

Return on equity 3.5

Liquidity ratio

Current ratio 1.6

Quick ratio 2.4

Investment ratio

Earnings per share 1.3

Equity ratio 3.5

Table 2: Financial Performance of Dalata Hotel Group Plc.

(Source: dalatahotelgroup.com, 2018)

Profitability ratio

Profitability ratio of the respective organisation consists of the returns that have been derived

from the total assets of the organisation of the financial year 2017. It has been seen that the

respective ratio of financial analysis also consists of the return that can be derived from the total

12

3.1 Financial accounts of travel and tourism

From the given scenario, it has been known that Dalata Hotel Group Plc is a hospitality

organisation. Dalata Hotel Group Plc has possessed two hotels in Ireland and UK, which have

been known as respectively Clayton Hotels and Maldron Hotels. The organisation has been

found to serve 7700 rooms including both the hotels. All the different services provided by the

respective organisation including the services and the offers on the holidays. The financial

interpretation of the respective organisation of the financial year 2017 is as follows:

Particulars 2017

Profitability Ratio

Return on assets 2.4

Return on equity 3.5

Liquidity ratio

Current ratio 1.6

Quick ratio 2.4

Investment ratio

Earnings per share 1.3

Equity ratio 3.5

Table 2: Financial Performance of Dalata Hotel Group Plc.

(Source: dalatahotelgroup.com, 2018)

Profitability ratio

Profitability ratio of the respective organisation consists of the returns that have been derived

from the total assets of the organisation of the financial year 2017. It has been seen that the

respective ratio of financial analysis also consists of the return that can be derived from the total

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.