Case Study 1: Philip and Jennifer Brown

VerifiedAdded on 2022/12/15

|68

|18816

|493

AI Summary

This case study focuses on the financial situation of Philip and Jennifer Brown, a young couple looking to buy their first home. It covers their background, property details, financial and employment information, and loan requirements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Written Project

Certificate IV in Finance and Mortgage Broking

(CIVMB_AS_v5A3)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Written Project overall result (assessor to complete)

First submission Not yet demonstrated

Resubmission (if applicable) Not applicable

CIVMB_AS_v5A3

Certificate IV in Finance and Mortgage Broking

(CIVMB_AS_v5A3)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Written Project overall result (assessor to complete)

First submission Not yet demonstrated

Resubmission (if applicable) Not applicable

CIVMB_AS_v5A3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Result summary (assessor to complete)

Section 1: Case study 1 — Philip and Jennifer Brown First submission Resubmission (if required)

Task 1 — Key terms, gathering and documenting client information Not yet demonstrated Not applicable

Task 2 — Assessing the clients’ situation Not yet demonstrated Not applicable

Task 3 — Borrowing options Not yet demonstrated Not applicable

Task 4 — Reasonable enquiries Not yet demonstrated Not applicable

Task 5 — First Home Owners Grant and home buyer assistance schemes Not yet demonstrated Not applicable

Task 6 — Professional network and loan settlement process Not yet demonstrated Not applicable

Task 7 — Interest rates Not yet demonstrated Not applicable

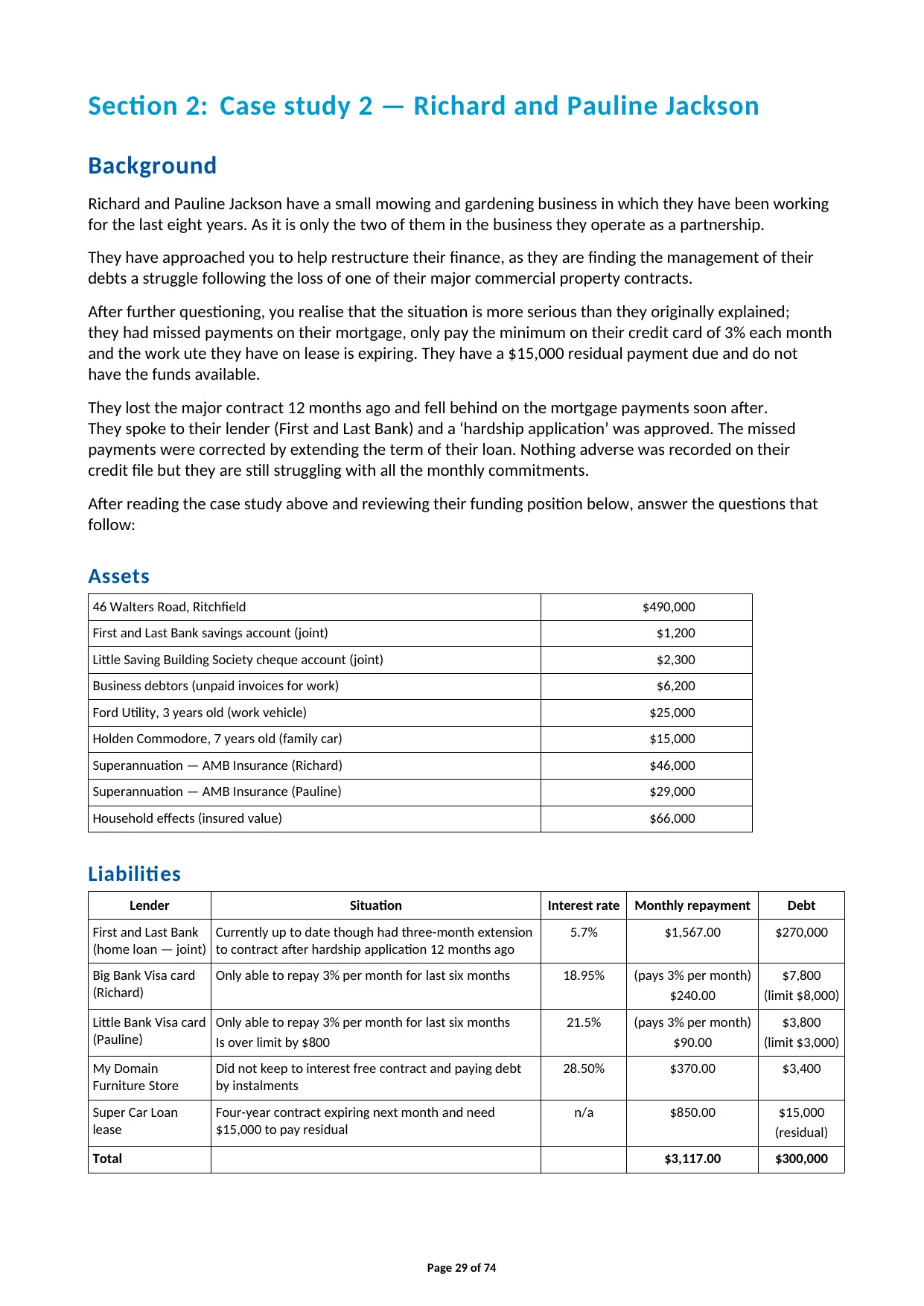

Section 2: Case study 2 — Richard and Pauline Jackson

Task 8 — Establishing level of financial knowledge Not yet demonstrated Not applicable

Task 9 — Responsible lending obligations Not yet demonstrated Not applicable

Task 10 — Self-employed special considerations Not yet demonstrated Not applicable

Task 11 — Advising on strategies Not yet demonstrated Not applicable

Task 12 — Impact of credit history Not yet demonstrated Not applicable

Task 13 — Dispute resolution Not yet demonstrated Not applicable

Task 14 — Effective access to files Not yet demonstrated Not applicable

Section 3: Case study 3 — Mary Jane Smith

Task 15 — Prepare and check a loan application Not yet demonstrated Not applicable

Section 4: Working in financial services

Task 16 — Financial services legislation and industry codes of practice Not yet demonstrated Not applicable

Task 17 — Design a document Not yet demonstrated Not applicable

Task 18 — Applying principles of professional practice to work in the financial

services industry Not yet demonstrated Not applicable

Task 19 — Develop and maintain in-depth knowledge of products and

services used by an organisation Not yet demonstrated Not applicable

Please note: To pass this written Project , you will need to be assessed as DEMONSTRATED in either your

first submission or your resubmission in all tasks above.

Task feedback

Please refer to the assessor’s detailed feedback found at the end of each task so that you know what to do

for any tasks you need to resubmit.

Page 2 of 74

Section 1: Case study 1 — Philip and Jennifer Brown First submission Resubmission (if required)

Task 1 — Key terms, gathering and documenting client information Not yet demonstrated Not applicable

Task 2 — Assessing the clients’ situation Not yet demonstrated Not applicable

Task 3 — Borrowing options Not yet demonstrated Not applicable

Task 4 — Reasonable enquiries Not yet demonstrated Not applicable

Task 5 — First Home Owners Grant and home buyer assistance schemes Not yet demonstrated Not applicable

Task 6 — Professional network and loan settlement process Not yet demonstrated Not applicable

Task 7 — Interest rates Not yet demonstrated Not applicable

Section 2: Case study 2 — Richard and Pauline Jackson

Task 8 — Establishing level of financial knowledge Not yet demonstrated Not applicable

Task 9 — Responsible lending obligations Not yet demonstrated Not applicable

Task 10 — Self-employed special considerations Not yet demonstrated Not applicable

Task 11 — Advising on strategies Not yet demonstrated Not applicable

Task 12 — Impact of credit history Not yet demonstrated Not applicable

Task 13 — Dispute resolution Not yet demonstrated Not applicable

Task 14 — Effective access to files Not yet demonstrated Not applicable

Section 3: Case study 3 — Mary Jane Smith

Task 15 — Prepare and check a loan application Not yet demonstrated Not applicable

Section 4: Working in financial services

Task 16 — Financial services legislation and industry codes of practice Not yet demonstrated Not applicable

Task 17 — Design a document Not yet demonstrated Not applicable

Task 18 — Applying principles of professional practice to work in the financial

services industry Not yet demonstrated Not applicable

Task 19 — Develop and maintain in-depth knowledge of products and

services used by an organisation Not yet demonstrated Not applicable

Please note: To pass this written Project , you will need to be assessed as DEMONSTRATED in either your

first submission or your resubmission in all tasks above.

Task feedback

Please refer to the assessor’s detailed feedback found at the end of each task so that you know what to do

for any tasks you need to resubmit.

Page 2 of 74

Before you begin

Read everything in this document before you start your written Project for Certificate IV in Finance and

Mortgage Broking (CIVMB_AS_v5A3).

About this document

This document is the written Project — half of the overall Written and Oral Project .

This document includes the following parts:

• Instructions for completing and submitting this Project

• Section 1: Case study 1 — Philip and Jennifer Brown

A case study with a series of short-answer questions:

– Task 1 — Key terms, gathering and documenting client information

– Task 2 — Assessing the clients’ situation

– Task 3 — Borrowing options

– Task 4 — Reasonable enquiries

– Task 5 — First Home Owners Grant and home buyer assistance schemes

– Task 6 —Professional network and loan settlement process

– Task 7 — Interest rates

• Section 2: Case study 2 — Richard and Pauline Jackson

A case study and a series of short-answer questions:

– Task 8 — Establishing level of financial knowledge

– Task 9 — Responsible lending obligations

– Task 10 — Self-employed special considerations

– Task 11 — Advising on strategies

– Task 12 — Impact of credit history

– Task 13 — Dispute resolution

– Task 14 — Effective access to files

• Section 3: Case study 3 — Mary Jane Smith

A case study and a series of short-answer questions:

– Task 15 — Prepare and check a loan application

• Section 4: Working in financial services

– Task 16 — Financial services legislation and industry codes of practice

– Task 17 — Design a document

– Task 18 — Applying principles of professional practice to work in the financial services industry

– Task 19 — Develop and maintain in depth knowledge of products and services used by an

organisation

• Appendix 1: Key terms

• Appendix 2: Client information collection tool/Fact finder

• Appendix 3: Loan application.

Page 3 of 74

Read everything in this document before you start your written Project for Certificate IV in Finance and

Mortgage Broking (CIVMB_AS_v5A3).

About this document

This document is the written Project — half of the overall Written and Oral Project .

This document includes the following parts:

• Instructions for completing and submitting this Project

• Section 1: Case study 1 — Philip and Jennifer Brown

A case study with a series of short-answer questions:

– Task 1 — Key terms, gathering and documenting client information

– Task 2 — Assessing the clients’ situation

– Task 3 — Borrowing options

– Task 4 — Reasonable enquiries

– Task 5 — First Home Owners Grant and home buyer assistance schemes

– Task 6 —Professional network and loan settlement process

– Task 7 — Interest rates

• Section 2: Case study 2 — Richard and Pauline Jackson

A case study and a series of short-answer questions:

– Task 8 — Establishing level of financial knowledge

– Task 9 — Responsible lending obligations

– Task 10 — Self-employed special considerations

– Task 11 — Advising on strategies

– Task 12 — Impact of credit history

– Task 13 — Dispute resolution

– Task 14 — Effective access to files

• Section 3: Case study 3 — Mary Jane Smith

A case study and a series of short-answer questions:

– Task 15 — Prepare and check a loan application

• Section 4: Working in financial services

– Task 16 — Financial services legislation and industry codes of practice

– Task 17 — Design a document

– Task 18 — Applying principles of professional practice to work in the financial services industry

– Task 19 — Develop and maintain in depth knowledge of products and services used by an

organisation

• Appendix 1: Key terms

• Appendix 2: Client information collection tool/Fact finder

• Appendix 3: Loan application.

Page 3 of 74

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the written Project within your enrolment period. Your study plan is in the KapLearn Certificate IV in

Finance and Mortgage Broking (CIVMBv5) subject room.

Instructions for completing and submitting the

written Project

Completing the written Project

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these Project s.

• Name your file as follows: Studentnumber_SubjectCode_Project _versionnumber_Submissionnumber

(e.g. 12345678_CIVMB_AS_v5A3_Submission1).

• Include your student ID on the first page of the Project .

Before you submit your work, please do a spell check and proofread your work to ensure that everything

is clear and unambiguous.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the ‘Client information collection tool’ in Appendix 2, assumptions are permitted,

although they must not be in conflict with the information provided in the Case study.

Throughout the Project you will also be required to research additional information from other

organisations in the finance industry to find the right products or services to meet your client’s

requirements or to calculate any service fees that may be applicable.

Page 4 of 74

We recommend that you use the study plan for this subject to help you manage your time to complete

the written Project within your enrolment period. Your study plan is in the KapLearn Certificate IV in

Finance and Mortgage Broking (CIVMBv5) subject room.

Instructions for completing and submitting the

written Project

Completing the written Project

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these Project s.

• Name your file as follows: Studentnumber_SubjectCode_Project _versionnumber_Submissionnumber

(e.g. 12345678_CIVMB_AS_v5A3_Submission1).

• Include your student ID on the first page of the Project .

Before you submit your work, please do a spell check and proofread your work to ensure that everything

is clear and unambiguous.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the ‘Client information collection tool’ in Appendix 2, assumptions are permitted,

although they must not be in conflict with the information provided in the Case study.

Throughout the Project you will also be required to research additional information from other

organisations in the finance industry to find the right products or services to meet your client’s

requirements or to calculate any service fees that may be applicable.

Page 4 of 74

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Submitting the written Project

Only Microsoft Office compatible written Project s submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed Project as a PDF.

The written Project must be completed before submitting it. Incomplete written Project s will be returned

to you unmarked. The written Project must be submitted together with the oral Project . If you do not

submit both completed Project s at the one time it will be returned to you unmarked.

The maximum file size is 20MB for the written and oral Project . Once you submit your written Project for

marking you will be unable to make any further changes to it.

Once you submit your written Project for marking you will be unable to make any further changes to it.

You are able to submit both Project s earlier than the deadline if you are confident you have completed all

parts and have prepared a quality submission.

Please refer to the Project submission/resubmission videos in the Assessment section of under your

‘Project Enrolment’ for details on how to submit/resubmit your written Project .

Your Written Project and Oral Project must be submitted together on or before your due date. Please

check for the due date.

The written Project marking process

You have 26 weeks from the date of your enrolment in this subject to submit your completed Project .

If you reach the end of your initial enrolment period and have been deemed ‘Not yet demonstrated’ in one

or more assessment items, then an additional four (4) weeks will be granted, provided you attempted all

assessment tasks during the initial enrolment period.

Your assessor will mark your written and oral Project and return it to you in the Certificate IV in

Finance and Mortgage Broking (CIVMBv5) subject room in under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written Project . Failure to do so will mean that your Project will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed written and oral Project .

How your written Project is graded

Project tasks are used to determine your ‘competence’ in demonstrating the required knowledge and/or

skills for each subject. As a result, you will be graded as either Demonstrated or Not yet demonstrated.

Page 5 of 74

Only Microsoft Office compatible written Project s submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed Project as a PDF.

The written Project must be completed before submitting it. Incomplete written Project s will be returned

to you unmarked. The written Project must be submitted together with the oral Project . If you do not

submit both completed Project s at the one time it will be returned to you unmarked.

The maximum file size is 20MB for the written and oral Project . Once you submit your written Project for

marking you will be unable to make any further changes to it.

Once you submit your written Project for marking you will be unable to make any further changes to it.

You are able to submit both Project s earlier than the deadline if you are confident you have completed all

parts and have prepared a quality submission.

Please refer to the Project submission/resubmission videos in the Assessment section of under your

‘Project Enrolment’ for details on how to submit/resubmit your written Project .

Your Written Project and Oral Project must be submitted together on or before your due date. Please

check for the due date.

The written Project marking process

You have 26 weeks from the date of your enrolment in this subject to submit your completed Project .

If you reach the end of your initial enrolment period and have been deemed ‘Not yet demonstrated’ in one

or more assessment items, then an additional four (4) weeks will be granted, provided you attempted all

assessment tasks during the initial enrolment period.

Your assessor will mark your written and oral Project and return it to you in the Certificate IV in

Finance and Mortgage Broking (CIVMBv5) subject room in under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written Project . Failure to do so will mean that your Project will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed written and oral Project .

How your written Project is graded

Project tasks are used to determine your ‘competence’ in demonstrating the required knowledge and/or

skills for each subject. As a result, you will be graded as either Demonstrated or Not yet demonstrated.

Page 5 of 74

Your assessor will follow the below process when marking your Project :

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed to be demonstrated in all assessment items in order to be awarded the units

of competency in this subject, including:

• all of the exam questions

• the written and oral Project .

‘Not yet demonstrated’ and resubmissions

Should sections of your Project be marked as ‘not yet demonstrated’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your resubmission responses. You only need to respond to

those sections where the assessor has determined you are ‘not yet demonstrated’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your Project , so your second assessor can see the instructions that were originally

provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written Project is your opportunity to demonstrate your competency against these units:

FNSCRD301 Process applications for credit

FNSFMB401 Prepare a loan application on behalf of finance or mortgage broking clients

FNSFMB402 Identify client needs for broking services

FNSFMB403 Present broking options to client

FNSFMK505 Comply with financial services legislation and industry codes of practice

FNSINC401 Apply principles of professional practice to work in the financial services industry

FNSINC402 Develop and maintain in-depth knowledge of products and services used by an organisation or sector

BSBITU306 Design and produce business documents

BSBCUS301 Deliver and monitor services to customers

BSBCUS402 Address customer needs

FNSSAM403 Prospect for new clients

FNSFMB501 Settle applications and loan arrangements in the finance and mortgage broking industry

Note that the written and oral Project is one of two assessments required to meet the requirements of the

units of competency.

We are here to help

If you have any questions about this written Project you can post your query at the ‘Ask your Tutor’ forum

in your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 6 of 74

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed to be demonstrated in all assessment items in order to be awarded the units

of competency in this subject, including:

• all of the exam questions

• the written and oral Project .

‘Not yet demonstrated’ and resubmissions

Should sections of your Project be marked as ‘not yet demonstrated’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your resubmission responses. You only need to respond to

those sections where the assessor has determined you are ‘not yet demonstrated’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your Project , so your second assessor can see the instructions that were originally

provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written Project is your opportunity to demonstrate your competency against these units:

FNSCRD301 Process applications for credit

FNSFMB401 Prepare a loan application on behalf of finance or mortgage broking clients

FNSFMB402 Identify client needs for broking services

FNSFMB403 Present broking options to client

FNSFMK505 Comply with financial services legislation and industry codes of practice

FNSINC401 Apply principles of professional practice to work in the financial services industry

FNSINC402 Develop and maintain in-depth knowledge of products and services used by an organisation or sector

BSBITU306 Design and produce business documents

BSBCUS301 Deliver and monitor services to customers

BSBCUS402 Address customer needs

FNSSAM403 Prospect for new clients

FNSFMB501 Settle applications and loan arrangements in the finance and mortgage broking industry

Note that the written and oral Project is one of two assessments required to meet the requirements of the

units of competency.

We are here to help

If you have any questions about this written Project you can post your query at the ‘Ask your Tutor’ forum

in your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 6 of 74

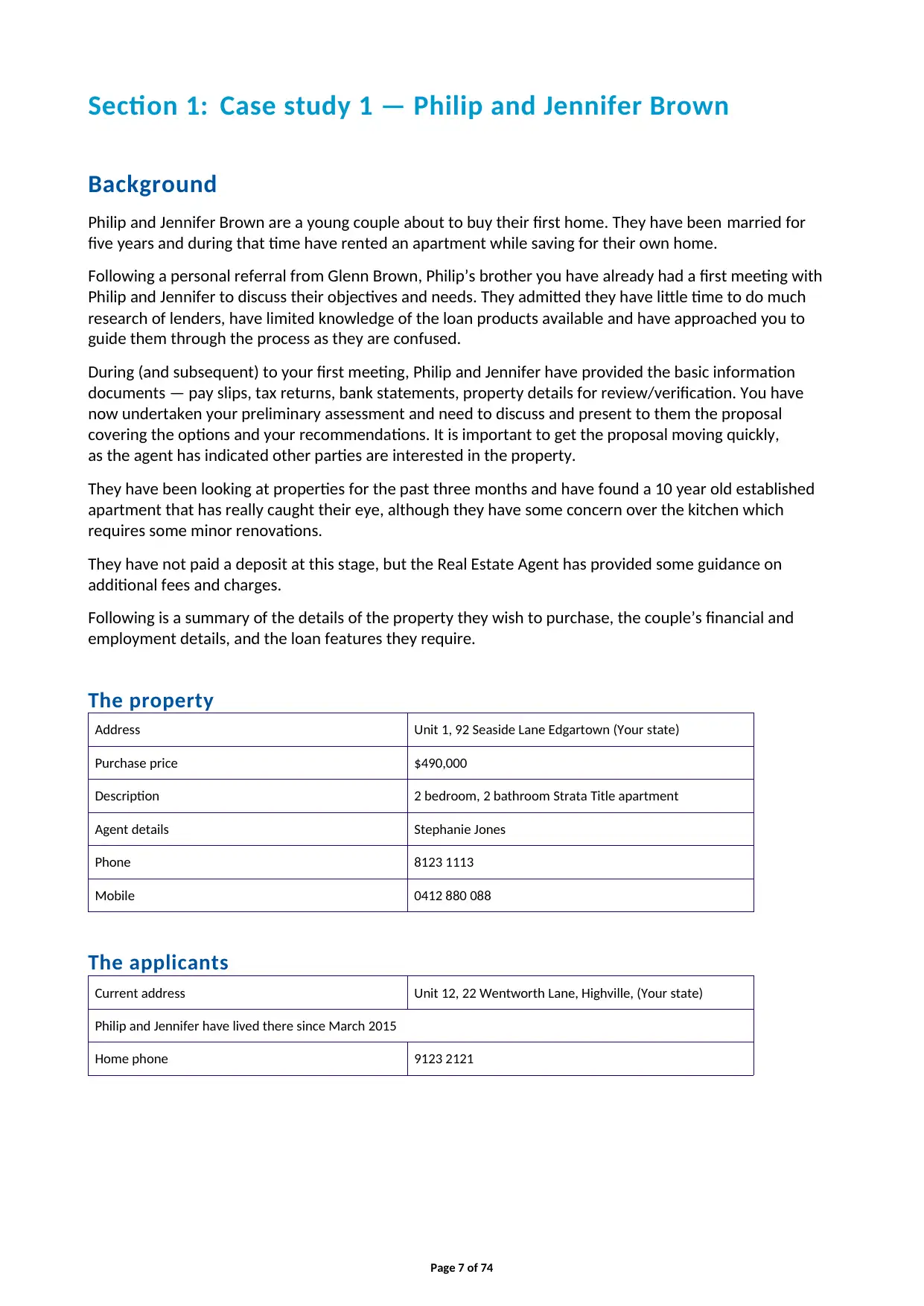

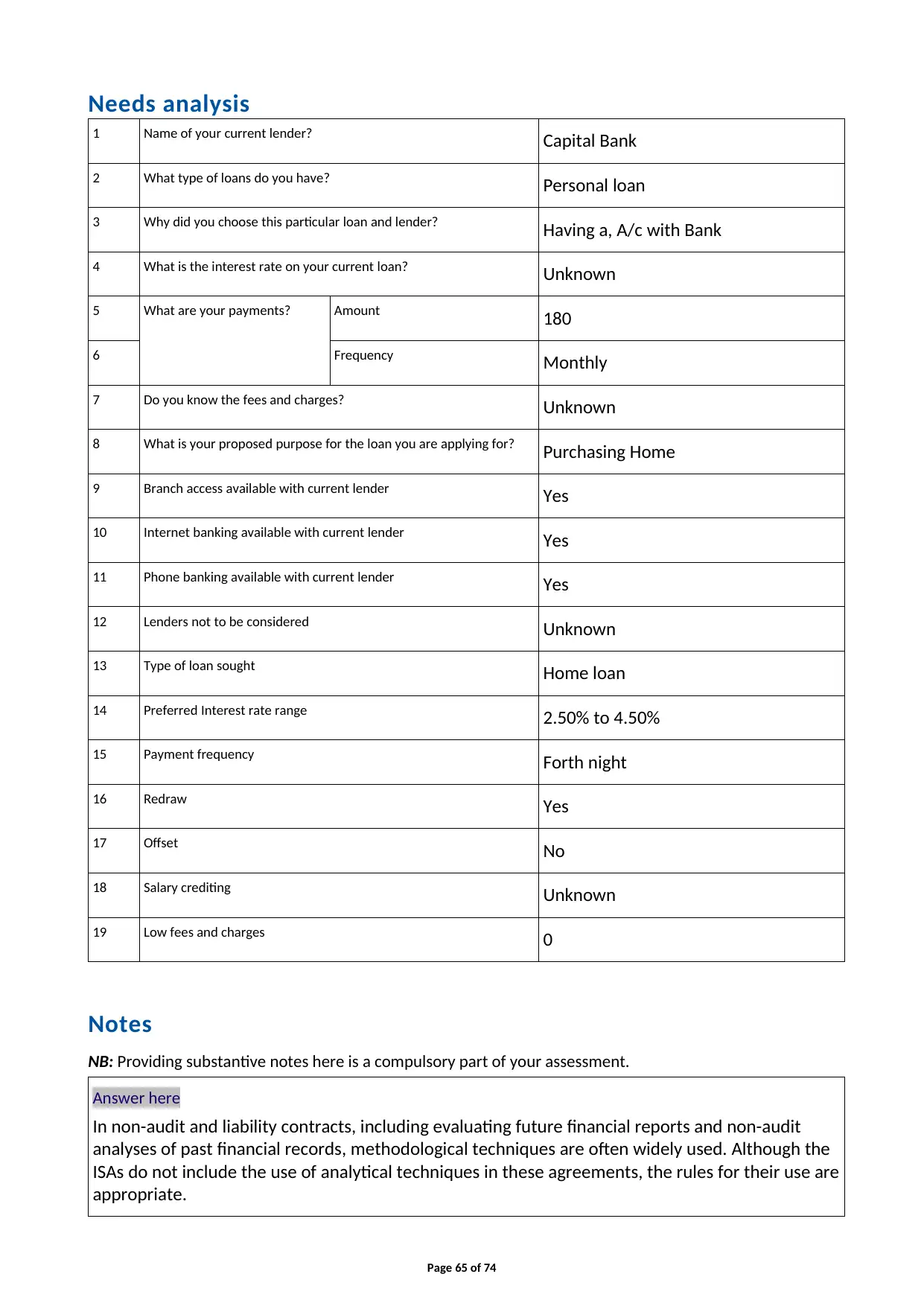

Section 1: Case study 1 — Philip and Jennifer Brown

Background

Philip and Jennifer Brown are a young couple about to buy their first home. They have been married for

five years and during that time have rented an apartment while saving for their own home.

Following a personal referral from Glenn Brown, Philip’s brother you have already had a first meeting with

Philip and Jennifer to discuss their objectives and needs. They admitted they have little time to do much

research of lenders, have limited knowledge of the loan products available and have approached you to

guide them through the process as they are confused.

During (and subsequent) to your first meeting, Philip and Jennifer have provided the basic information

documents — pay slips, tax returns, bank statements, property details for review/verification. You have

now undertaken your preliminary assessment and need to discuss and present to them the proposal

covering the options and your recommendations. It is important to get the proposal moving quickly,

as the agent has indicated other parties are interested in the property.

They have been looking at properties for the past three months and have found a 10 year old established

apartment that has really caught their eye, although they have some concern over the kitchen which

requires some minor renovations.

They have not paid a deposit at this stage, but the Real Estate Agent has provided some guidance on

additional fees and charges.

Following is a summary of the details of the property they wish to purchase, the couple’s financial and

employment details, and the loan features they require.

The property

Address Unit 1, 92 Seaside Lane Edgartown (Your state)

Purchase price $490,000

Description 2 bedroom, 2 bathroom Strata Title apartment

Agent details Stephanie Jones

Phone 8123 1113

Mobile 0412 880 088

The applicants

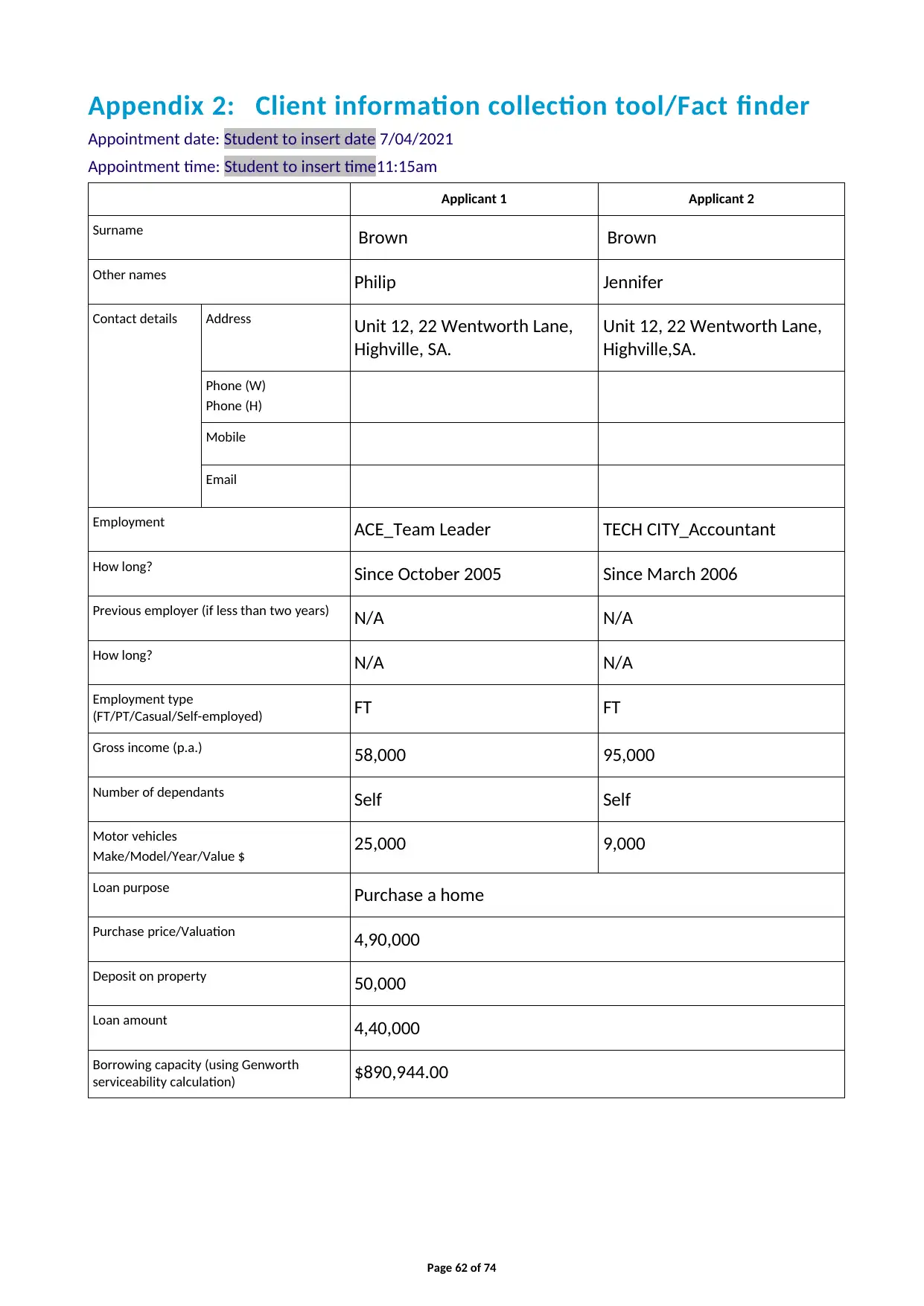

Current address Unit 12, 22 Wentworth Lane, Highville, (Your state)

Philip and Jennifer have lived there since March 2015

Home phone 9123 2121

Page 7 of 74

Background

Philip and Jennifer Brown are a young couple about to buy their first home. They have been married for

five years and during that time have rented an apartment while saving for their own home.

Following a personal referral from Glenn Brown, Philip’s brother you have already had a first meeting with

Philip and Jennifer to discuss their objectives and needs. They admitted they have little time to do much

research of lenders, have limited knowledge of the loan products available and have approached you to

guide them through the process as they are confused.

During (and subsequent) to your first meeting, Philip and Jennifer have provided the basic information

documents — pay slips, tax returns, bank statements, property details for review/verification. You have

now undertaken your preliminary assessment and need to discuss and present to them the proposal

covering the options and your recommendations. It is important to get the proposal moving quickly,

as the agent has indicated other parties are interested in the property.

They have been looking at properties for the past three months and have found a 10 year old established

apartment that has really caught their eye, although they have some concern over the kitchen which

requires some minor renovations.

They have not paid a deposit at this stage, but the Real Estate Agent has provided some guidance on

additional fees and charges.

Following is a summary of the details of the property they wish to purchase, the couple’s financial and

employment details, and the loan features they require.

The property

Address Unit 1, 92 Seaside Lane Edgartown (Your state)

Purchase price $490,000

Description 2 bedroom, 2 bathroom Strata Title apartment

Agent details Stephanie Jones

Phone 8123 1113

Mobile 0412 880 088

The applicants

Current address Unit 12, 22 Wentworth Lane, Highville, (Your state)

Philip and Jennifer have lived there since March 2015

Home phone 9123 2121

Page 7 of 74

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

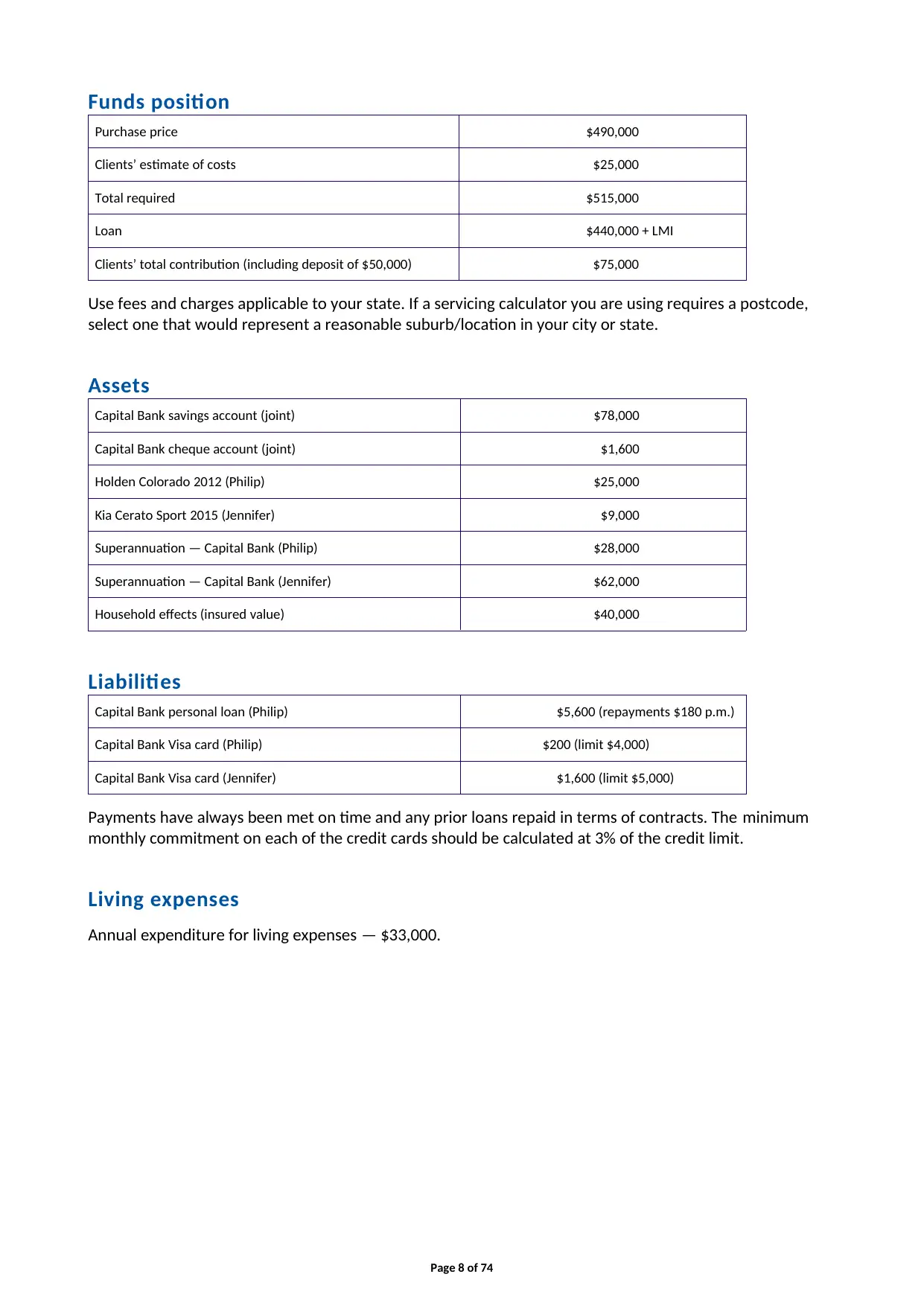

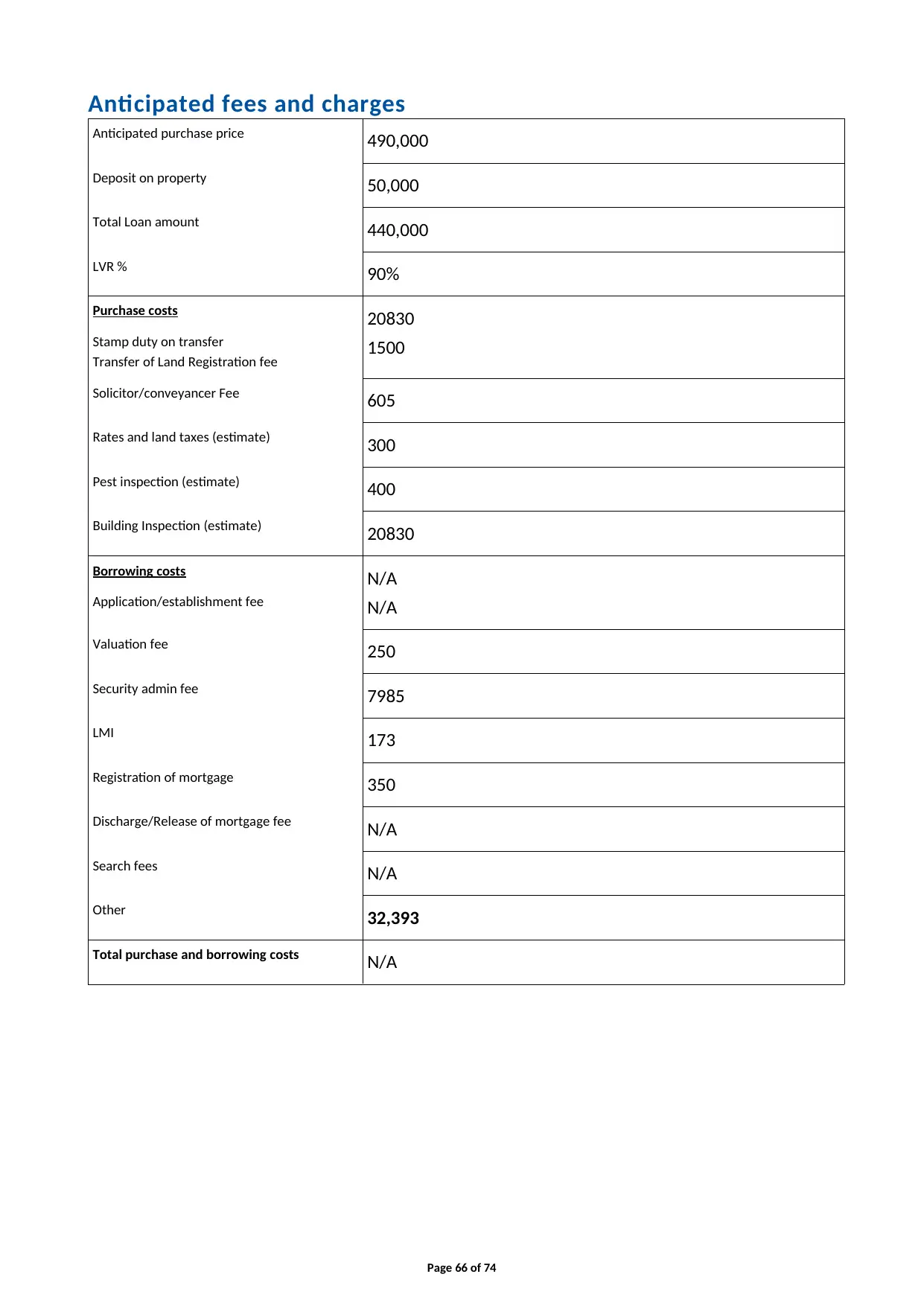

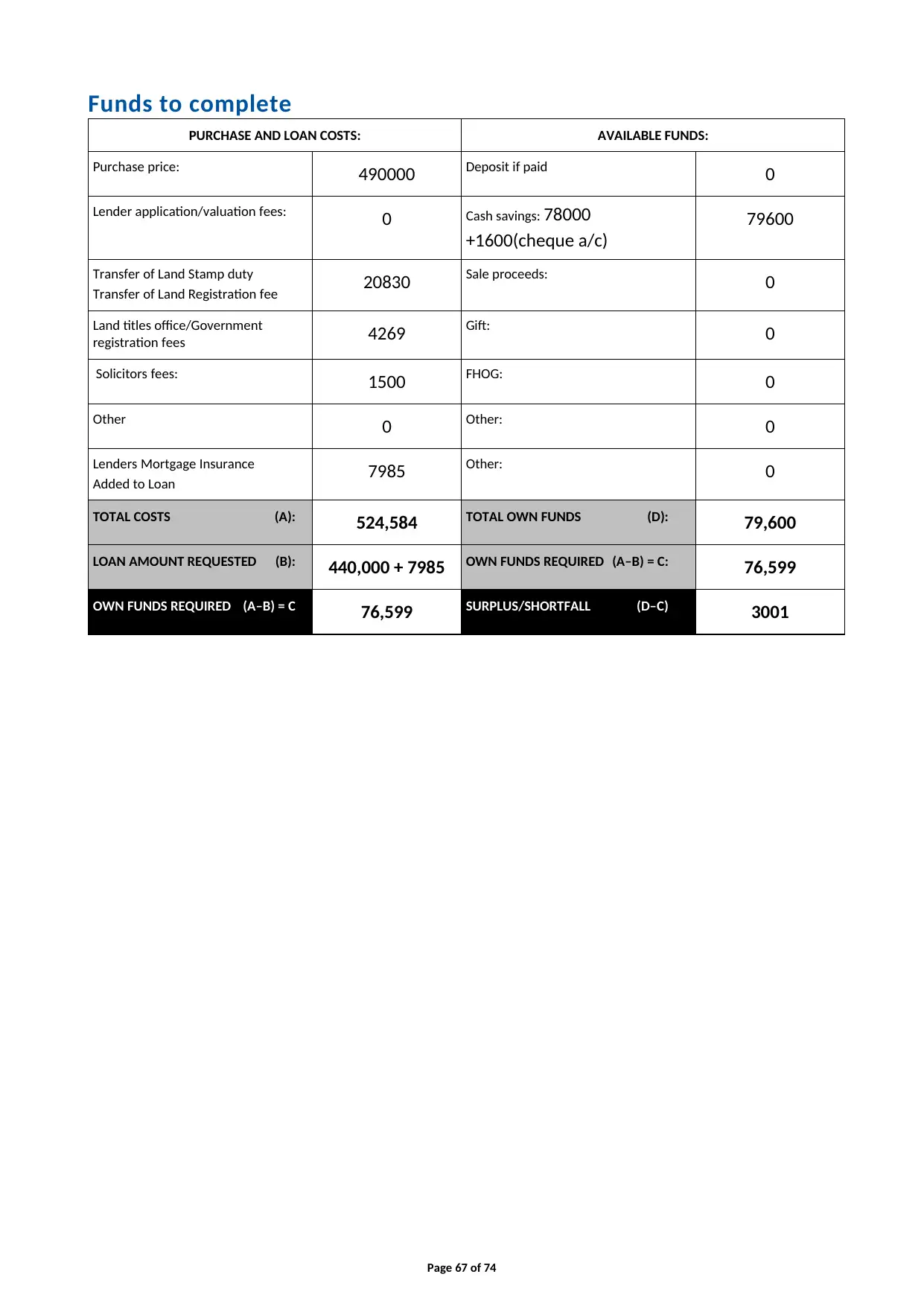

Funds position

Purchase price $490,000

Clients’ estimate of costs $25,000

Total required $515,000

Loan $440,000 + LMI

Clients’ total contribution (including deposit of $50,000) $75,000

Use fees and charges applicable to your state. If a servicing calculator you are using requires a postcode,

select one that would represent a reasonable suburb/location in your city or state.

Assets

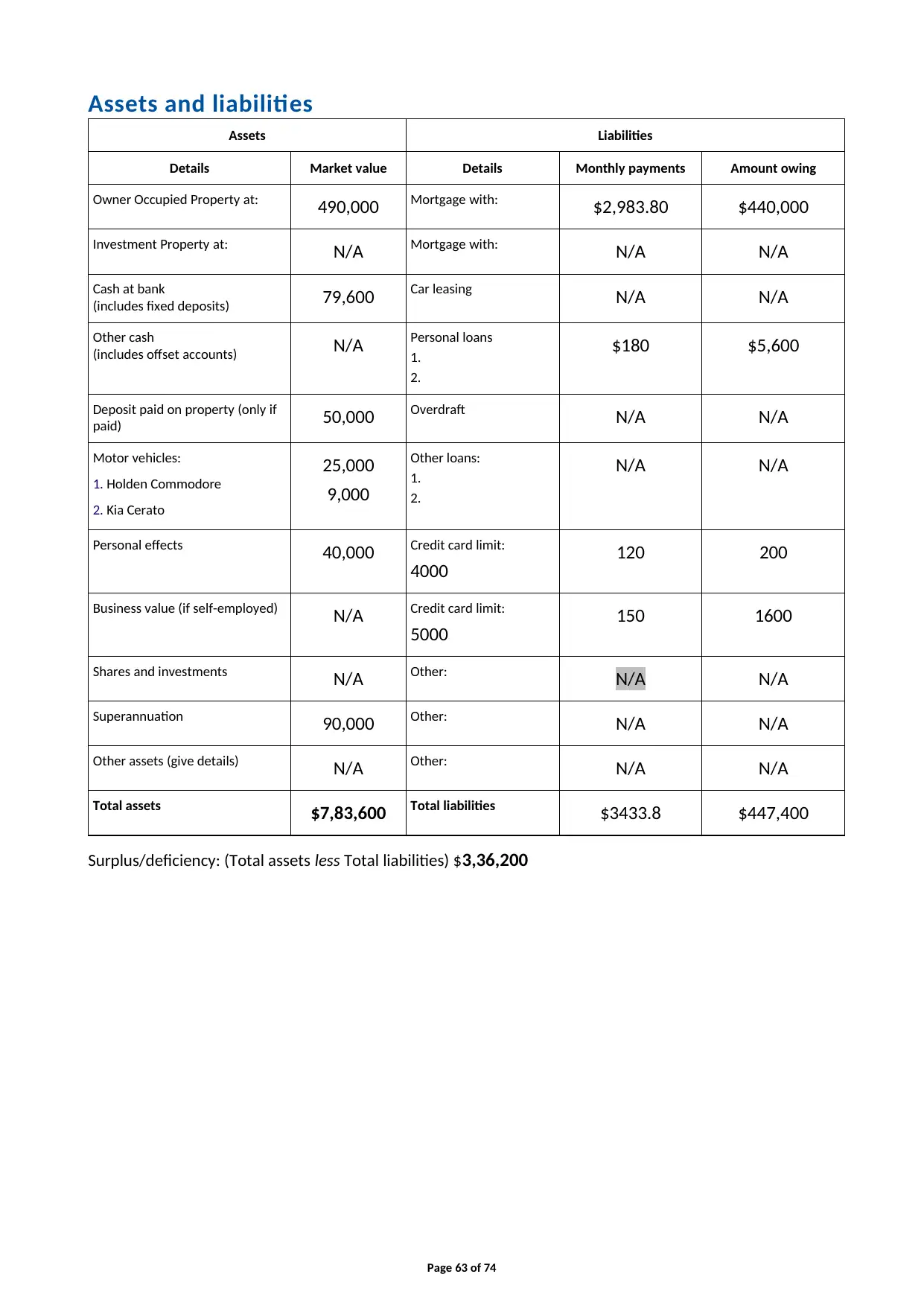

Capital Bank savings account (joint) $78,000

Capital Bank cheque account (joint) $1,600

Holden Colorado 2012 (Philip) $25,000

Kia Cerato Sport 2015 (Jennifer) $9,000

Superannuation — Capital Bank (Philip) $28,000

Superannuation — Capital Bank (Jennifer) $62,000

Household effects (insured value) $40,000

Liabilities

Capital Bank personal loan (Philip) $5,600 (repayments $180 p.m.)

Capital Bank Visa card (Philip) $200 (limit $4,000)

Capital Bank Visa card (Jennifer) $1,600 (limit $5,000)

Payments have always been met on time and any prior loans repaid in terms of contracts. The minimum

monthly commitment on each of the credit cards should be calculated at 3% of the credit limit.

Living expenses

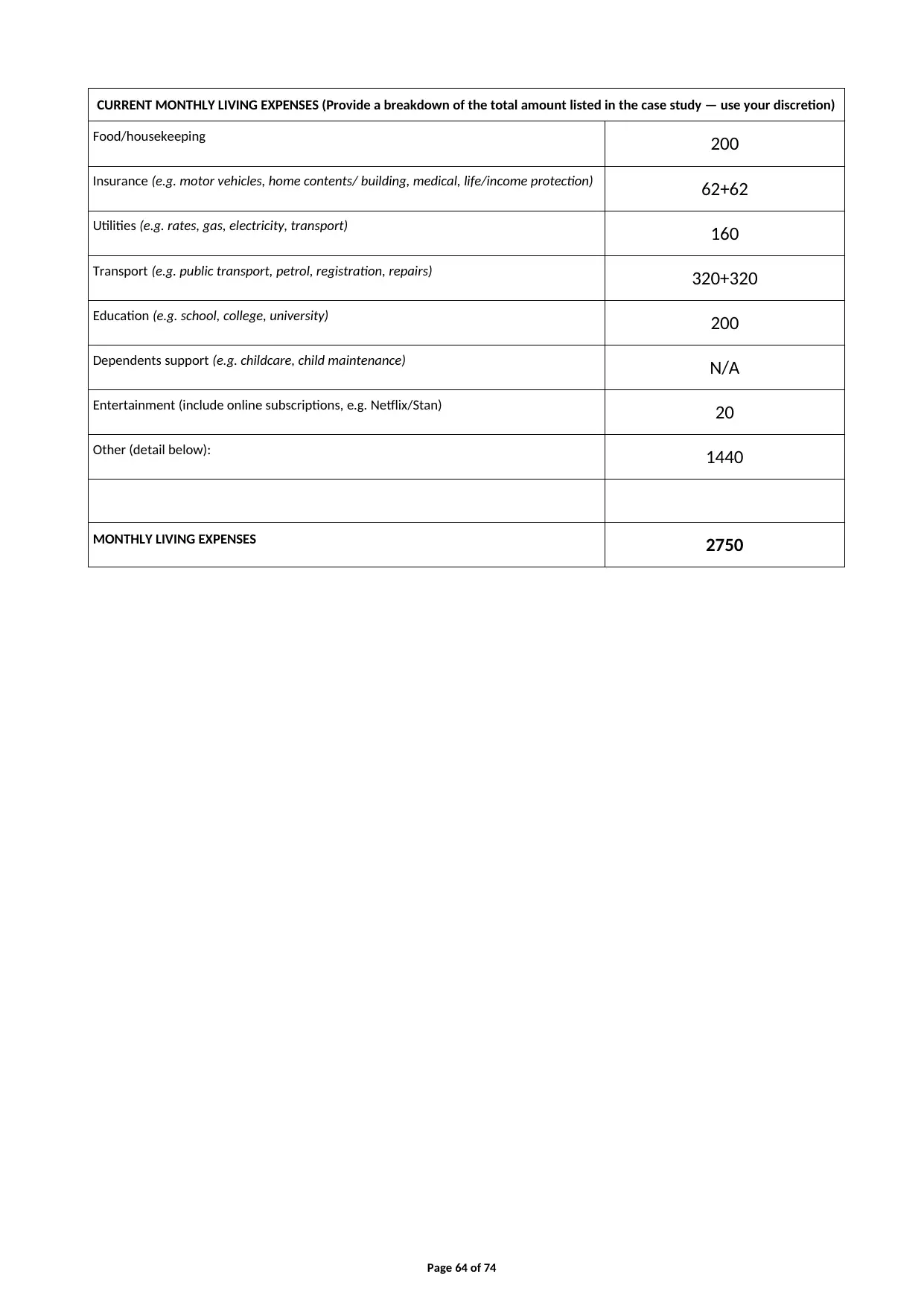

Annual expenditure for living expenses — $33,000.

Page 8 of 74

Purchase price $490,000

Clients’ estimate of costs $25,000

Total required $515,000

Loan $440,000 + LMI

Clients’ total contribution (including deposit of $50,000) $75,000

Use fees and charges applicable to your state. If a servicing calculator you are using requires a postcode,

select one that would represent a reasonable suburb/location in your city or state.

Assets

Capital Bank savings account (joint) $78,000

Capital Bank cheque account (joint) $1,600

Holden Colorado 2012 (Philip) $25,000

Kia Cerato Sport 2015 (Jennifer) $9,000

Superannuation — Capital Bank (Philip) $28,000

Superannuation — Capital Bank (Jennifer) $62,000

Household effects (insured value) $40,000

Liabilities

Capital Bank personal loan (Philip) $5,600 (repayments $180 p.m.)

Capital Bank Visa card (Philip) $200 (limit $4,000)

Capital Bank Visa card (Jennifer) $1,600 (limit $5,000)

Payments have always been met on time and any prior loans repaid in terms of contracts. The minimum

monthly commitment on each of the credit cards should be calculated at 3% of the credit limit.

Living expenses

Annual expenditure for living expenses — $33,000.

Page 8 of 74

Employment and income

Philip (date of birth 21/2/87)

Position Team Leader (full time)

Employer ACE Limited 101 City Rd, Westside (Your state)

Income (gross) $58,000 p.a. monthly gross income: $4,833

Employer contact Dwayne Johnson, HR Manager

Length of service Since October 2005

Driver’s licence 8855KL

Jennifer (date of birth 8/10/88)

Position Accountant (full time)

Employer Tech city 804 High Street, City East (Your state)

Income (gross) $95,000 p.a. monthly gross income: $7,917

Employer contact Bruce Wayne, HR Manager

Length of service Since March 2006

Driver’s licence 17016C

Solicitor’s details

Jones and Co

22 High Street, City East (Your state)

Phone

Email

The solicitor has quoted a fee of $1,500 for the conveyance.

Page 9 of 74

Philip (date of birth 21/2/87)

Position Team Leader (full time)

Employer ACE Limited 101 City Rd, Westside (Your state)

Income (gross) $58,000 p.a. monthly gross income: $4,833

Employer contact Dwayne Johnson, HR Manager

Length of service Since October 2005

Driver’s licence 8855KL

Jennifer (date of birth 8/10/88)

Position Accountant (full time)

Employer Tech city 804 High Street, City East (Your state)

Income (gross) $95,000 p.a. monthly gross income: $7,917

Employer contact Bruce Wayne, HR Manager

Length of service Since March 2006

Driver’s licence 17016C

Solicitor’s details

Jones and Co

22 High Street, City East (Your state)

Phone

The solicitor has quoted a fee of $1,500 for the conveyance.

Page 9 of 74

The loan requirements

• 30 year term

• premium option home loan features

• variable interest rate (for this case use 4.5% p.a.)

• LMI to be capitalised

• proposed settlement date — six weeks from exchange of contracts

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• funds access via card.

Note:

1. The loan application fee is waived under a Special Offer.

2. For this Project , your chosen lender uses Genworth for Lenders Mortgage Insurance – you must use the

Genworth LMI Calculator in this Project : <https://www.genworth.com.au/lenders/lmi-tools/lmi-

premium-estimator/>. For Project purposes, please use the Upfront LMI premium generated by the

calculator.

Other information

• They have advised that the Real Estate Agents have indicated they need to make a formal offer within

the next 10 days, however they are reluctant to do so until they obtain an approval.

• Jennifer has asked if there are any professional package benefits available because she is an accountant.

However, Jennifer has confirmed that she has not renewed her industry association membership.

• Jennifer previously owned and lived in an apartment with her two older sisters when they attended

university, however they sold this property 12 months ago — minimal profit was made from the sale.

• Plans to start a family are five years away.

• They do have plans to take a major overseas trip prior to starting a family.

• Philip is hoping for a promotion within the next 12 months upon possible retirement of a long-term

employee where he works.

They have also expressed a concern about the possibility of interest rates increasing.

Page 10 of 74

• 30 year term

• premium option home loan features

• variable interest rate (for this case use 4.5% p.a.)

• LMI to be capitalised

• proposed settlement date — six weeks from exchange of contracts

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• funds access via card.

Note:

1. The loan application fee is waived under a Special Offer.

2. For this Project , your chosen lender uses Genworth for Lenders Mortgage Insurance – you must use the

Genworth LMI Calculator in this Project : <https://www.genworth.com.au/lenders/lmi-tools/lmi-

premium-estimator/>. For Project purposes, please use the Upfront LMI premium generated by the

calculator.

Other information

• They have advised that the Real Estate Agents have indicated they need to make a formal offer within

the next 10 days, however they are reluctant to do so until they obtain an approval.

• Jennifer has asked if there are any professional package benefits available because she is an accountant.

However, Jennifer has confirmed that she has not renewed her industry association membership.

• Jennifer previously owned and lived in an apartment with her two older sisters when they attended

university, however they sold this property 12 months ago — minimal profit was made from the sale.

• Plans to start a family are five years away.

• They do have plans to take a major overseas trip prior to starting a family.

• Philip is hoping for a promotion within the next 12 months upon possible retirement of a long-term

employee where he works.

They have also expressed a concern about the possibility of interest rates increasing.

Page 10 of 74

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Project tasks (student to complete)

Task 1 — Key terms, gathering and documenting client information

1. Complete the ‘Key terms’ (located at the end of the written Project in Appendix 1).

2. Using the information provided in Case study 1, complete the ‘Client information collection tool’

(located at the end of the written Project in Appendix 2).

3. You will need to complete the Genworth LMI Calculator and Genworth Serviceability Calculator to

assess the security, debt service and borrowing capacity for Jennifer and Philip Brown. To do this, follow

these steps:

(a) Use the details in Case study 1.

(b) Read the Genworth Calculator Supplementary Material Guide available in the KapLearn

CIVMBv5 subject room.

(c) Process the loan application using the Genworth Serviceability Calculator accessible here:

<https://www.genworth.com.au/lenders/lmi-tools/serviceability-calculator>.

(d) Once you have processed it, download a copy of the PDF and save it to your desktop.

Note: You will need to upload a copy of this pdf with your written and oral Project submission. This will

assist your assessor with providing feedback on your written and oral Project submission.

Note: Any assumptions you make should be listed and should not be in conflict with the case study

information already provided.

Assessor feedback for Task 1 — Key terms, gathering and documenting client information

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 11 of 74

Task 1 — Key terms, gathering and documenting client information

1. Complete the ‘Key terms’ (located at the end of the written Project in Appendix 1).

2. Using the information provided in Case study 1, complete the ‘Client information collection tool’

(located at the end of the written Project in Appendix 2).

3. You will need to complete the Genworth LMI Calculator and Genworth Serviceability Calculator to

assess the security, debt service and borrowing capacity for Jennifer and Philip Brown. To do this, follow

these steps:

(a) Use the details in Case study 1.

(b) Read the Genworth Calculator Supplementary Material Guide available in the KapLearn

CIVMBv5 subject room.

(c) Process the loan application using the Genworth Serviceability Calculator accessible here:

<https://www.genworth.com.au/lenders/lmi-tools/serviceability-calculator>.

(d) Once you have processed it, download a copy of the PDF and save it to your desktop.

Note: You will need to upload a copy of this pdf with your written and oral Project submission. This will

assist your assessor with providing feedback on your written and oral Project submission.

Note: Any assumptions you make should be listed and should not be in conflict with the case study

information already provided.

Assessor feedback for Task 1 — Key terms, gathering and documenting client information

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 11 of 74

Task 2 — Assessing the clients’ situation

1. Based on the information provided in the case study and any other online tools used, you now need

to assess the clients’ loan application paying particular attention that you have met legislative

requirements, followed industry codes of practice and met lender credit policy.

Answer questions (a)–(j) for Task 2: Question 1 below.

Provide data to support your comments and conclusions. (450 words)

Note: The assessment of the clients’ needs is a critical prelude to you completing Part 4 of the

Oral Project requirement for this course.

(a) Does the application appear to meet legislative requirements? (e.g. NCCP)

Student response to Task 2: Question 1(a)

Answer here

As per the NCCP Act, credit provider to ensure a credit facility is suitable for the borrower. There

are two key elements that can affect the assessment of loan suitability which appear to have been

satisfied by initial assessment. There also doesn’t appear to be any conflict.

(b) According to the Genworth calculator, what is the maximum borrowing capacity of client?

Student response to Task 2: Question 1(b)

Answer here

Utilising the online calculator from Genworth, the loan value of 440,000 is only about 40% of their

serviceability at the actual rate and half at the stressed rate of 7%. (Please see the attach

Genworth calculation).

(c) Does the client have the capacity to meet deposit and total cash contribution for the loan required?

Student response to Task 2: Question 1(c)

Answer here

Yes

(d) What are the required repayments based on the loan required?

Student response to Task 2: Question 1(d)

Answer here

In terms repayment of loans the payments are recalculated each year and are based on the information

that is given. There are certain methods that need to be done in order to repayments of loans and it

sometime depends on the kind of loan it is and its requitements. Certain plans has been there for the

repayment of loans such as Extended repayment, graduate repayment, income repayment and Income

based repayments.

(e) What will the security be and is it an appropriate type of security?

Page 12 of 74

1. Based on the information provided in the case study and any other online tools used, you now need

to assess the clients’ loan application paying particular attention that you have met legislative

requirements, followed industry codes of practice and met lender credit policy.

Answer questions (a)–(j) for Task 2: Question 1 below.

Provide data to support your comments and conclusions. (450 words)

Note: The assessment of the clients’ needs is a critical prelude to you completing Part 4 of the

Oral Project requirement for this course.

(a) Does the application appear to meet legislative requirements? (e.g. NCCP)

Student response to Task 2: Question 1(a)

Answer here

As per the NCCP Act, credit provider to ensure a credit facility is suitable for the borrower. There

are two key elements that can affect the assessment of loan suitability which appear to have been

satisfied by initial assessment. There also doesn’t appear to be any conflict.

(b) According to the Genworth calculator, what is the maximum borrowing capacity of client?

Student response to Task 2: Question 1(b)

Answer here

Utilising the online calculator from Genworth, the loan value of 440,000 is only about 40% of their

serviceability at the actual rate and half at the stressed rate of 7%. (Please see the attach

Genworth calculation).

(c) Does the client have the capacity to meet deposit and total cash contribution for the loan required?

Student response to Task 2: Question 1(c)

Answer here

Yes

(d) What are the required repayments based on the loan required?

Student response to Task 2: Question 1(d)

Answer here

In terms repayment of loans the payments are recalculated each year and are based on the information

that is given. There are certain methods that need to be done in order to repayments of loans and it

sometime depends on the kind of loan it is and its requitements. Certain plans has been there for the

repayment of loans such as Extended repayment, graduate repayment, income repayment and Income

based repayments.

(e) What will the security be and is it an appropriate type of security?

Page 12 of 74

Student response to Task 2: Question 1(e)

Answer here

To give security or collateral to the banks many options are available but most appropriate type of security

will be Real estate. Benefits are it repay over longer tenure that will be beneficial, enjoying lower rate of

interest and getting tax benefits on interest payments.

(f) (i) Will Jennifer and Philip be required to pay Lenders Mortgage Insurance (LMI) and why?

(ii) If so, what would the premium be?

(iii) Name at least two (2) options borrowers have to pay the LMI fee.

Student response to Task 2: Question 1(f)

(i) Answer here Jeniffer and Philip were unable to pay Lender Mortage Insurance as they were not having

enough amount to get the sufficient loan.

(ii) Answer here

(iii) Answer here Borrower have two option either capitalise the cost into the loan and bringing the total

loan amount.

(g) What loan amount would you recommend, and why?

Student response to Task 2: Question 1(g)

Answer here

The loan amount recommend is $400000

(h) What is the likelihood that the clients will be able to meet all of their financial obligations?

Student response to Task 2: Question 1(h)

Answer here

They can save the income and kind to look into another option to increase their income sources to satisfy

the financial obligation.

(i) Do Jennifer and Philip qualify for concessions on any of the fees and charges? Why or why not?

Student response to Task 2: Question 1(i)

Answer here

No, any concession charges of any charges as they were not qualified for the loan requirement.

(j) What other issues may impact, now or in the future, on the clients’ ability to meet their obligations,

including any possible risks?

Student response to Task 2: Question 1(j)

Answer here

There are many issues that might impact the future possibility like unable to pay loan amount, increasing in

their expense and cost during their time, might face any major loss n future that will be difficult for them.

Page 13 of 74

Answer here

To give security or collateral to the banks many options are available but most appropriate type of security

will be Real estate. Benefits are it repay over longer tenure that will be beneficial, enjoying lower rate of

interest and getting tax benefits on interest payments.

(f) (i) Will Jennifer and Philip be required to pay Lenders Mortgage Insurance (LMI) and why?

(ii) If so, what would the premium be?

(iii) Name at least two (2) options borrowers have to pay the LMI fee.

Student response to Task 2: Question 1(f)

(i) Answer here Jeniffer and Philip were unable to pay Lender Mortage Insurance as they were not having

enough amount to get the sufficient loan.

(ii) Answer here

(iii) Answer here Borrower have two option either capitalise the cost into the loan and bringing the total

loan amount.

(g) What loan amount would you recommend, and why?

Student response to Task 2: Question 1(g)

Answer here

The loan amount recommend is $400000

(h) What is the likelihood that the clients will be able to meet all of their financial obligations?

Student response to Task 2: Question 1(h)

Answer here

They can save the income and kind to look into another option to increase their income sources to satisfy

the financial obligation.

(i) Do Jennifer and Philip qualify for concessions on any of the fees and charges? Why or why not?

Student response to Task 2: Question 1(i)

Answer here

No, any concession charges of any charges as they were not qualified for the loan requirement.

(j) What other issues may impact, now or in the future, on the clients’ ability to meet their obligations,

including any possible risks?

Student response to Task 2: Question 1(j)

Answer here

There are many issues that might impact the future possibility like unable to pay loan amount, increasing in

their expense and cost during their time, might face any major loss n future that will be difficult for them.

Page 13 of 74

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Most lenders stress test loan repayments by adding an additional 2–3% on to the loan repayments to

make sure a borrower can afford the repayments. If interest rates moved 3% higher, what would Philip

and Jennifer’s loan repayments be and do you think they would be able to cope with the extra

repayments? (50 words)

Student response to Task 2: Question 2

Answer here

The Genworth calculator use to calculate their initial serviceability stressed the loan amount from

the current rate of 4.5% to 7%. This brought the payments from $2,272.42 to $2,983.80 and

reduce their maximum loan amount from $1,169,853 to $890,944. In the current economic

climate with the headwinds over the global pandemic, it is estimated that RBA will not raising

rates for a year. This allows the borrowers to be confident in a floating rate loan at the current

levels to remain constant.

3. Identify appropriate product options you can present to the clients that may remove this interest rate

risk? (50 words)

Student response to Task 2: Question 3

Answer here

In order to remove their interest rate risk, the borrower can structure their mortgage inti some

fixed rate components. Most lender in Australia provide fixed rate loans typically between 1-5

years unlike the united states that regularly provide fixed rates of 15, 20 and 30 years. The

borrower can also have the option to trench their loan into several parts at the various fixed terms

or leave a portion in a floating rate product.

Assessor feedback for Task 2 — Assessing the clients’ situation

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 14 of 74

make sure a borrower can afford the repayments. If interest rates moved 3% higher, what would Philip

and Jennifer’s loan repayments be and do you think they would be able to cope with the extra

repayments? (50 words)

Student response to Task 2: Question 2

Answer here

The Genworth calculator use to calculate their initial serviceability stressed the loan amount from

the current rate of 4.5% to 7%. This brought the payments from $2,272.42 to $2,983.80 and

reduce their maximum loan amount from $1,169,853 to $890,944. In the current economic

climate with the headwinds over the global pandemic, it is estimated that RBA will not raising

rates for a year. This allows the borrowers to be confident in a floating rate loan at the current

levels to remain constant.

3. Identify appropriate product options you can present to the clients that may remove this interest rate

risk? (50 words)

Student response to Task 2: Question 3

Answer here

In order to remove their interest rate risk, the borrower can structure their mortgage inti some

fixed rate components. Most lender in Australia provide fixed rate loans typically between 1-5

years unlike the united states that regularly provide fixed rates of 15, 20 and 30 years. The

borrower can also have the option to trench their loan into several parts at the various fixed terms

or leave a portion in a floating rate product.

Assessor feedback for Task 2 — Assessing the clients’ situation

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 14 of 74

Task 3 — Borrowing options

Although Philip and Jennifer are looking to borrow at approximately 90% LVR, what other options could you

present that would avoid the cost of LMI? Provide a minimum of two (2) options. (50 words)

Student response to Task 3

Answer here

They do not have many options available as loans greater than an 80% LVR in Australia require LMI

with few exceptions. This first is a professional license (CA or CPA, Solicitors, Doctors) that may

allow them to be waived at certain lending institutions. Another option to waived LMI is to have a

guarantor. If this is a lower cost option or available, then this would be an available option to

explore for the Philip and Jennifer.

Assessor feedback for Task 3 — Borrowing options

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 15 of 74

Although Philip and Jennifer are looking to borrow at approximately 90% LVR, what other options could you

present that would avoid the cost of LMI? Provide a minimum of two (2) options. (50 words)

Student response to Task 3

Answer here

They do not have many options available as loans greater than an 80% LVR in Australia require LMI

with few exceptions. This first is a professional license (CA or CPA, Solicitors, Doctors) that may

allow them to be waived at certain lending institutions. Another option to waived LMI is to have a

guarantor. If this is a lower cost option or available, then this would be an available option to

explore for the Philip and Jennifer.

Assessor feedback for Task 3 — Borrowing options

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 15 of 74

Task 4 — Reasonable enquiries

In the course of gathering information about the couple, you are required under the National Consumer

Credit Protection Act 2009 to make all ‘reasonable’ enquiries to determine a borrower’s objectives,

requirements and financial situation.

Identify at least six (6) ‘reasonable’ enquiries that you would make with the clients in the case study and

explain why these enquiries are important in terms of NCCP compliance. (150 words)

Student response to Task 4

Answer here

AS the NCCP Act 2009 is designed to protect consumer and ensure ethical and professional

standards in the finance industry. Six inquiries that should be made are as follows; credit in this

case study, is provided to purchase a residential property. Another, when it is a primary residence

or investment property. The third would be the consumer’s financial situation followed by their

requirements for the types of mortgage loans. The fifth may be the effect on rising interest rate

and family expenses as stressed by the Genworth serviceability calculator. Lastly, assessing

whether the credit contracts meets the consumer’s requirements and objectives.

These are all important terms as the sixth point raised addresses suitability. Ensuring from these

inquiries that the credit product is appropriate for the reason the clients are looking for a loan.

Ensuring the clients are in a suitable financial position with saving and stability of income. The

spirit of the act is too not creating a hardship if the clients get overextended.

Assessor feedback for Task 4 — Reasonable enquiries

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 16 of 74

In the course of gathering information about the couple, you are required under the National Consumer

Credit Protection Act 2009 to make all ‘reasonable’ enquiries to determine a borrower’s objectives,

requirements and financial situation.

Identify at least six (6) ‘reasonable’ enquiries that you would make with the clients in the case study and

explain why these enquiries are important in terms of NCCP compliance. (150 words)

Student response to Task 4

Answer here

AS the NCCP Act 2009 is designed to protect consumer and ensure ethical and professional

standards in the finance industry. Six inquiries that should be made are as follows; credit in this

case study, is provided to purchase a residential property. Another, when it is a primary residence

or investment property. The third would be the consumer’s financial situation followed by their

requirements for the types of mortgage loans. The fifth may be the effect on rising interest rate

and family expenses as stressed by the Genworth serviceability calculator. Lastly, assessing

whether the credit contracts meets the consumer’s requirements and objectives.

These are all important terms as the sixth point raised addresses suitability. Ensuring from these

inquiries that the credit product is appropriate for the reason the clients are looking for a loan.

Ensuring the clients are in a suitable financial position with saving and stability of income. The

spirit of the act is too not creating a hardship if the clients get overextended.

Assessor feedback for Task 4 — Reasonable enquiries

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 16 of 74

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task 5 — First Home Owners Grant and home buyer assistance

schemes

(a) Describe the First Home Owner’s Grant or home buyer assistance scheme benefits and stamp duty

concessions that are available in your State or Territory.

Note: Please identify which State or Territory you are from in your answer. (100 words)

Student response to Task 5(a)

Answer here

The First Home Owner Grant (FHOG) is paid by the State Government to eligible first home

owners. The payment is made only after an application has been submitted to and approved by

RevenueSA or a financial institution authorised by RevenueSA to process applications.

(b) Who would be eligible and what would be their benefit?

Student response to Task 5(b)

Answer here

FHOG applies to the purchase or construction of a new residential property, including a house,

flat, unit, townhouse or apartment that meets local planning standards anywhere in South

Australia. FHOG ceased for established homes from 1 July 2014.

The market value of the property does not exceed $575 000, a $15 000 FHOG is potentially

available, provided that all other eligibility criteria are satisfied.

(c) Are Philip and Jennifer eligible for any assistance? Explain why.

Page 17 of 74

schemes

(a) Describe the First Home Owner’s Grant or home buyer assistance scheme benefits and stamp duty

concessions that are available in your State or Territory.

Note: Please identify which State or Territory you are from in your answer. (100 words)

Student response to Task 5(a)

Answer here

The First Home Owner Grant (FHOG) is paid by the State Government to eligible first home

owners. The payment is made only after an application has been submitted to and approved by

RevenueSA or a financial institution authorised by RevenueSA to process applications.

(b) Who would be eligible and what would be their benefit?

Student response to Task 5(b)

Answer here

FHOG applies to the purchase or construction of a new residential property, including a house,

flat, unit, townhouse or apartment that meets local planning standards anywhere in South

Australia. FHOG ceased for established homes from 1 July 2014.

The market value of the property does not exceed $575 000, a $15 000 FHOG is potentially

available, provided that all other eligibility criteria are satisfied.

(c) Are Philip and Jennifer eligible for any assistance? Explain why.

Page 17 of 74

Student response to Task 5(c)

Answer here

Registered persons are individuals who may never have previously bought a house. They will be

candidates for the grant in the case of Philip and Jennifer Brown, as she shared a home with her 2

elder siblings in the discussion. Philip Brown would be able to earn the award, but he would not be

available in the event of a shared submission with Jennifer. Regarding stamp duty grants in South

Australia if an accommodation bought by way of a valid contract is over $500 000 worth of market

value, the buyer shall be entitled to a $21 330 stamp duty award. Since Philip and Jennifer's flat is

priced at $490,000, this would not be accessible. Then Philip and Jennifer are able to pay $500,000

for the apartments where they are entitled.

Assessor feedback for Task 5 — First Home Owners Grant and home buyer assistance schemes

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 18 of 74

Answer here

Registered persons are individuals who may never have previously bought a house. They will be

candidates for the grant in the case of Philip and Jennifer Brown, as she shared a home with her 2

elder siblings in the discussion. Philip Brown would be able to earn the award, but he would not be

available in the event of a shared submission with Jennifer. Regarding stamp duty grants in South

Australia if an accommodation bought by way of a valid contract is over $500 000 worth of market

value, the buyer shall be entitled to a $21 330 stamp duty award. Since Philip and Jennifer's flat is

priced at $490,000, this would not be accessible. Then Philip and Jennifer are able to pay $500,000

for the apartments where they are entitled.

Assessor feedback for Task 5 — First Home Owners Grant and home buyer assistance schemes

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 18 of 74

Task 6 — Professional network and loan settlement process

1. Name three (3) parties, who are not directly involved in the processing of a loan and what their role is.

Explain how you would communicate with them in an efficient and effective manner so that they

understand pre-settlement conditions and their involvement required. (75 words)

Student response to Task 6: Question 1

Answer here

Real estate- I can consult directly with a real-estate firm and will remind the applicant of the pre-

approved, officially approved application and the deadline for payment. The property

development agent is an essential element to keep in the process. Creditor – The loan risk is very

low until the trustee has supplied the creditor with all the details required. I will remind the

creditor at any point of the development of the loan. Transporter- It is important that a direct line

of contact is established with the transporter creditors, so all the funds must be deposited with

the forwarding agent.

2. Explain how you would develop and maintain relevant networks with professionals such as those you

detailed above or other professionals to ensure you are up to date with the products or services they

provide. (50 words)

Student response to Task 6: Question 2

Answer here

Every week conferences: I'll have the chance to chat to experts on a weekly basis and get updates

about new goods and programs that might improve.

Teleconferences: Communicating to dealers would give me a clear guide if there are goods that I

could not have been sure about before.

Briefings: The current developments on manufactured goods will be provided to you during

seminars

Page 19 of 74

1. Name three (3) parties, who are not directly involved in the processing of a loan and what their role is.

Explain how you would communicate with them in an efficient and effective manner so that they

understand pre-settlement conditions and their involvement required. (75 words)

Student response to Task 6: Question 1

Answer here

Real estate- I can consult directly with a real-estate firm and will remind the applicant of the pre-

approved, officially approved application and the deadline for payment. The property

development agent is an essential element to keep in the process. Creditor – The loan risk is very

low until the trustee has supplied the creditor with all the details required. I will remind the

creditor at any point of the development of the loan. Transporter- It is important that a direct line

of contact is established with the transporter creditors, so all the funds must be deposited with

the forwarding agent.

2. Explain how you would develop and maintain relevant networks with professionals such as those you

detailed above or other professionals to ensure you are up to date with the products or services they

provide. (50 words)

Student response to Task 6: Question 2

Answer here

Every week conferences: I'll have the chance to chat to experts on a weekly basis and get updates

about new goods and programs that might improve.

Teleconferences: Communicating to dealers would give me a clear guide if there are goods that I

could not have been sure about before.

Briefings: The current developments on manufactured goods will be provided to you during

seminars

Page 19 of 74

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. You want to ensure that Philip and Jennifer have all the key insurance protections in place in case

something unfortunate was to happen to one of them.

(a) What process would you follow during your discussion with the clients to ensure you have a good

assessment of their needs? (50 words)

Student response to Task 6: Question 3(a)

Answer here

I might like to clarify the value of quality assurance when coping with such a significant financial

partnership, which could save costs if anything happens well after agreement.

● Home insurance provides coverage against injury or destruction of houses, particularly

apartments, units and townhouses.

● Insurance of content protects loss or injury to residential goods or services which is estate

leased or bought by the insured individual. The one scheme also blends buildings (home)

and material insurance.

● Personal responsibility applies to the obligation of the insured to compensate another

person for disability, sickness or death and negligence or harm to goods that another

person owns. Civil liability protection typically requires insurance plans on premises and

belongings.

● Mortgage insurance is a kind of life insurance intended to preserve one very particular yet

essential thing, which is your estate. The mortgage coverage policy may also refer to as a

new mortgage policy, if the borrower is not willing to afford the debt.

(b) Explain who you should refer Philip and Jennifer to obtain advice on these types of products?

(10 words)

Student response to Task 6: Question 3(b)

Answer here

They can prefer ant professional guide or experienced person who is in this field. to tell them about

consequences of the products. This will help them to take the right decision regarding this as they were

advice by professional person.

Page 20 of 74

something unfortunate was to happen to one of them.

(a) What process would you follow during your discussion with the clients to ensure you have a good

assessment of their needs? (50 words)

Student response to Task 6: Question 3(a)

Answer here

I might like to clarify the value of quality assurance when coping with such a significant financial

partnership, which could save costs if anything happens well after agreement.

● Home insurance provides coverage against injury or destruction of houses, particularly

apartments, units and townhouses.

● Insurance of content protects loss or injury to residential goods or services which is estate

leased or bought by the insured individual. The one scheme also blends buildings (home)

and material insurance.

● Personal responsibility applies to the obligation of the insured to compensate another

person for disability, sickness or death and negligence or harm to goods that another

person owns. Civil liability protection typically requires insurance plans on premises and

belongings.

● Mortgage insurance is a kind of life insurance intended to preserve one very particular yet

essential thing, which is your estate. The mortgage coverage policy may also refer to as a

new mortgage policy, if the borrower is not willing to afford the debt.

(b) Explain who you should refer Philip and Jennifer to obtain advice on these types of products?

(10 words)

Student response to Task 6: Question 3(b)

Answer here

They can prefer ant professional guide or experienced person who is in this field. to tell them about

consequences of the products. This will help them to take the right decision regarding this as they were

advice by professional person.

Page 20 of 74

4. Briefly explain why it is important for the broker to remain informed of developments in the lending

process despite not being actively involved at every stage. (150 words)

Student response to Task 6: Question 4

Answer here

In the case, the broker is the intermediary man in the details exchanged with the customer,

dealer, transport provider and the solicitor on all facets of the loan process. For the involved

authorities to do what they're doing in some phases of the loan application process; everyone

should be told at the point of a loan.

Page 21 of 74

process despite not being actively involved at every stage. (150 words)

Student response to Task 6: Question 4

Answer here

In the case, the broker is the intermediary man in the details exchanged with the customer,

dealer, transport provider and the solicitor on all facets of the loan process. For the involved

authorities to do what they're doing in some phases of the loan application process; everyone

should be told at the point of a loan.

Page 21 of 74

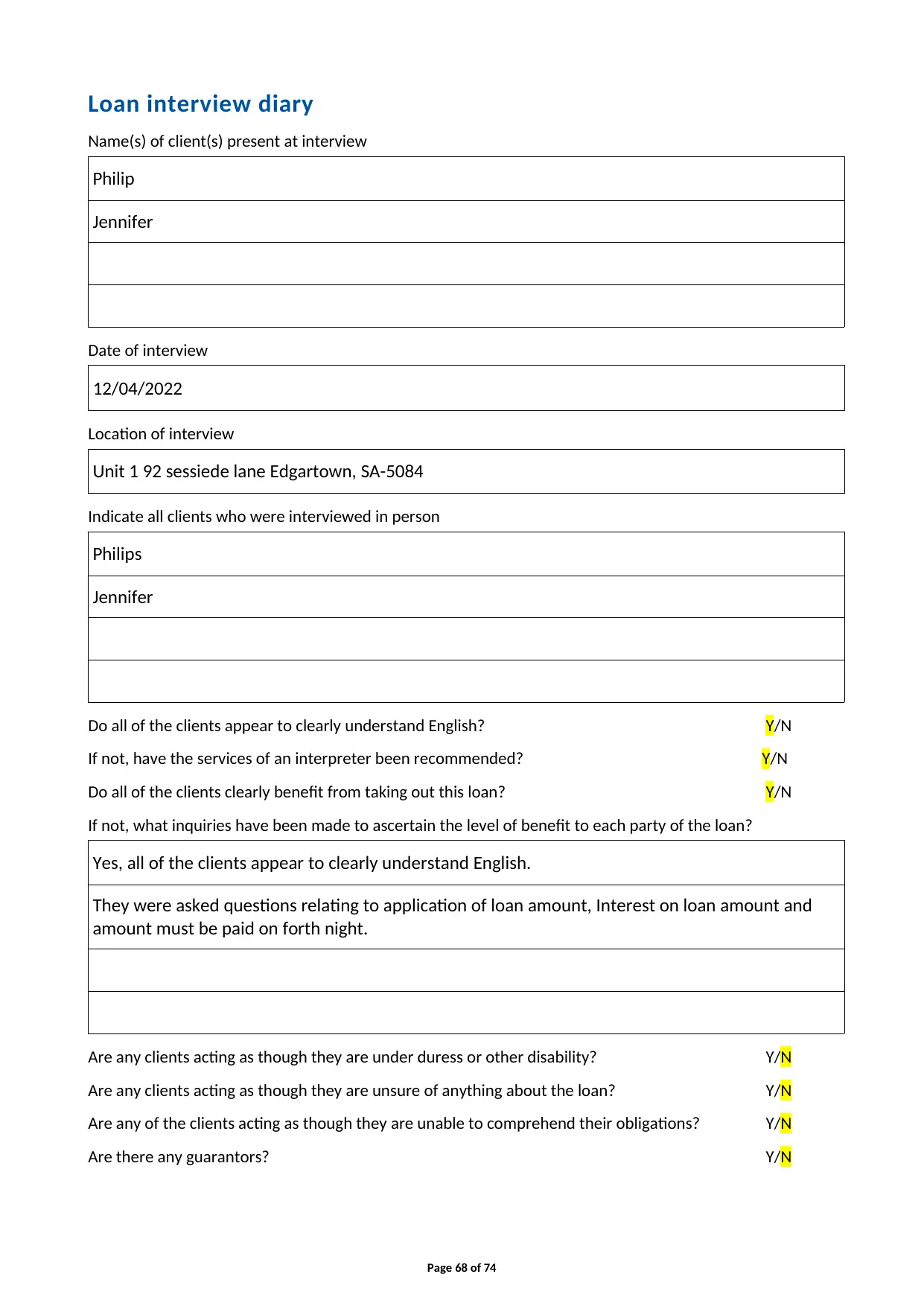

5. The application form and related documents have now been signed and forwarded to the Lender for

approval. Philip and Jennifer have agreed that you will keep their Solicitor informed of progress if/when

the loan is approved.

Refer to the ‘Example of an Organisation’s Policies and Procedures’ within the toolbox document and

explain what the service standards and timelines are for the following steps: (50 words)

(a) Advising the client’s solicitor/conveyancer that the loan is approved.

Student response to Task 6: Question 5(a)

Answer here

● Workers must learn to respond efficiently and appropriately to telephone calls.

● Staff to accept feedback from their clients and respond within two (2) working days. If the

customer is not provided with a complete answer, please remind the customer and

monitor the status of your question or concern. It is necessary to keep the consumer up to

date with how the question or issue progresses.

● Professionals must ensure the execution of client-related activities in the time limits set.

Please keep the person and/or the provider updated if you are unable to maintain

schedules.

● Personnel to inform consumers within 24 hours of receiving mortgage approvals.

● Workers are enabled before they depart to ensure that communications and/or voicemail

messages from the office are sent.

● Personnel shall understand and respond in two (2) business days to any consumer

grievances.

● Make sure the solicitor / transporter information is stored on the register for each user.

● Strongly recommend the loan consent solicitor / transmitter (if customer acceptance)

within 24 hours.

(b) Advise the client’s solicitor/conveyancer that the loan documents have been executed by the

client and returned to the lender.

Page 22 of 74

approval. Philip and Jennifer have agreed that you will keep their Solicitor informed of progress if/when

the loan is approved.

Refer to the ‘Example of an Organisation’s Policies and Procedures’ within the toolbox document and

explain what the service standards and timelines are for the following steps: (50 words)

(a) Advising the client’s solicitor/conveyancer that the loan is approved.

Student response to Task 6: Question 5(a)

Answer here

● Workers must learn to respond efficiently and appropriately to telephone calls.

● Staff to accept feedback from their clients and respond within two (2) working days. If the

customer is not provided with a complete answer, please remind the customer and

monitor the status of your question or concern. It is necessary to keep the consumer up to

date with how the question or issue progresses.

● Professionals must ensure the execution of client-related activities in the time limits set.

Please keep the person and/or the provider updated if you are unable to maintain

schedules.

● Personnel to inform consumers within 24 hours of receiving mortgage approvals.

● Workers are enabled before they depart to ensure that communications and/or voicemail

messages from the office are sent.

● Personnel shall understand and respond in two (2) business days to any consumer

grievances.

● Make sure the solicitor / transporter information is stored on the register for each user.

● Strongly recommend the loan consent solicitor / transmitter (if customer acceptance)

within 24 hours.

(b) Advise the client’s solicitor/conveyancer that the loan documents have been executed by the

client and returned to the lender.

Page 22 of 74

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Student response to Task 6: Question 5(b)

Answer here

This document and all loan other requirement related to these has properly executed by the clint and it

clearly scrutinize all process in better manner. It is important to get the approval from the clients.

(c) Advise the client and the client’s solicitor/conveyancer that the settlement date has been

confirmed.

Student response to Task 6: Question 5(c)

Client: This loan document has been executed and date is confirmed of loan settlement.

Answer here

Solicitor/Conveyancer:

Answer here

It is important to settle down the date of loan settlement to move ahead from this procedure and they

have fulfilled all requirements

6. Clients have now called to execute loan offer and mortgage documents and are nervous that their

Solicitor is very busy and difficult to contact. They want to know who will be responsible for what tasks

from this point in the lead up to settlement and immediately following settlement.

Explain to Philip and Jennifer who is responsible for completion of what tasks once the loan documents

have been returned to the lender and in the lead up to settlement and once settlement occurs. Focus on

the lending organisation and the client’s solicitor/conveyancer roles in this part of the lending process.

(150 words)

Page 23 of 74

Answer here

This document and all loan other requirement related to these has properly executed by the clint and it

clearly scrutinize all process in better manner. It is important to get the approval from the clients.

(c) Advise the client and the client’s solicitor/conveyancer that the settlement date has been

confirmed.

Student response to Task 6: Question 5(c)

Client: This loan document has been executed and date is confirmed of loan settlement.

Answer here

Solicitor/Conveyancer:

Answer here

It is important to settle down the date of loan settlement to move ahead from this procedure and they

have fulfilled all requirements

6. Clients have now called to execute loan offer and mortgage documents and are nervous that their

Solicitor is very busy and difficult to contact. They want to know who will be responsible for what tasks

from this point in the lead up to settlement and immediately following settlement.

Explain to Philip and Jennifer who is responsible for completion of what tasks once the loan documents