BUSI 4079 Finance Assignment 1: Arbitrage, Options, and FX Analysis

VerifiedAdded on 2023/04/21

|8

|1165

|277

Homework Assignment

AI Summary

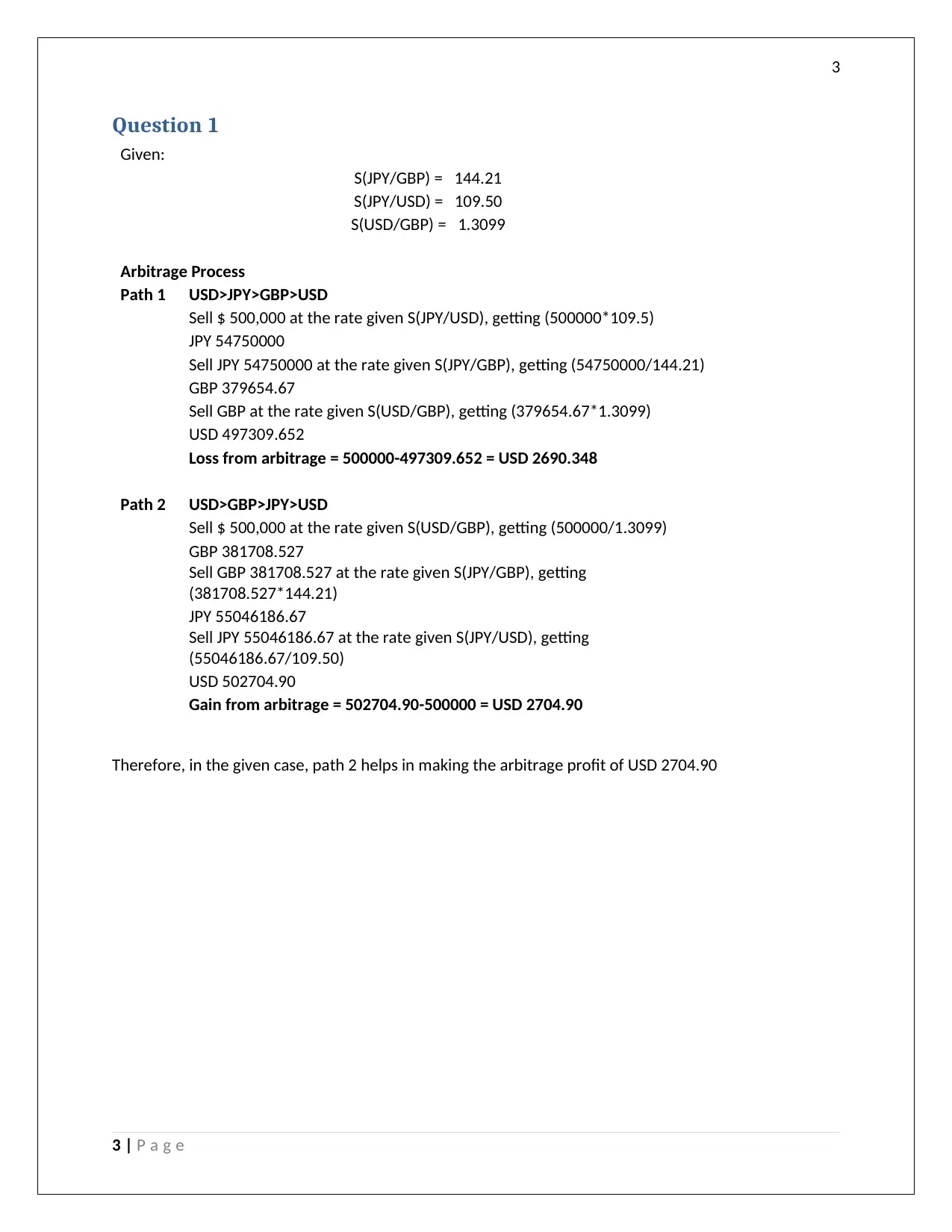

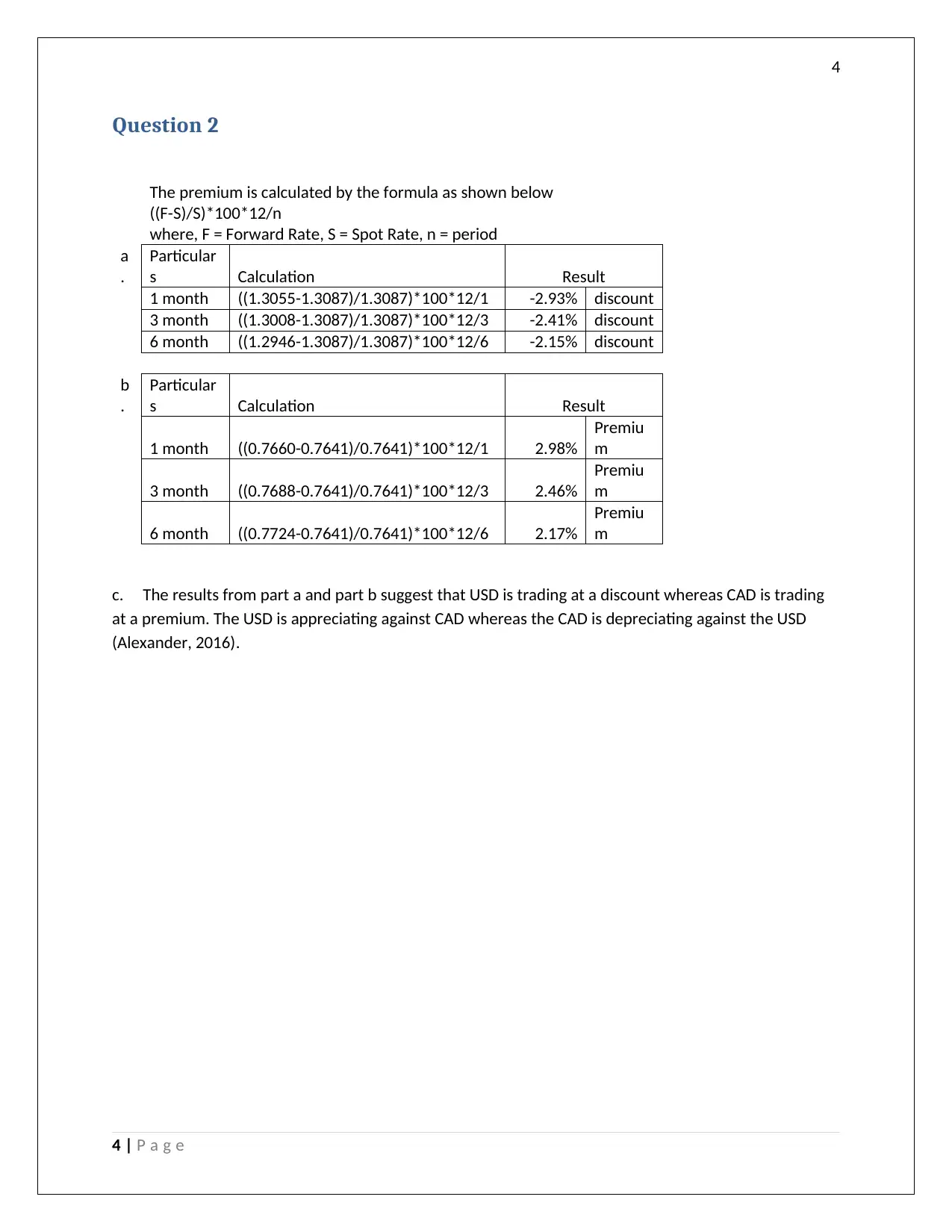

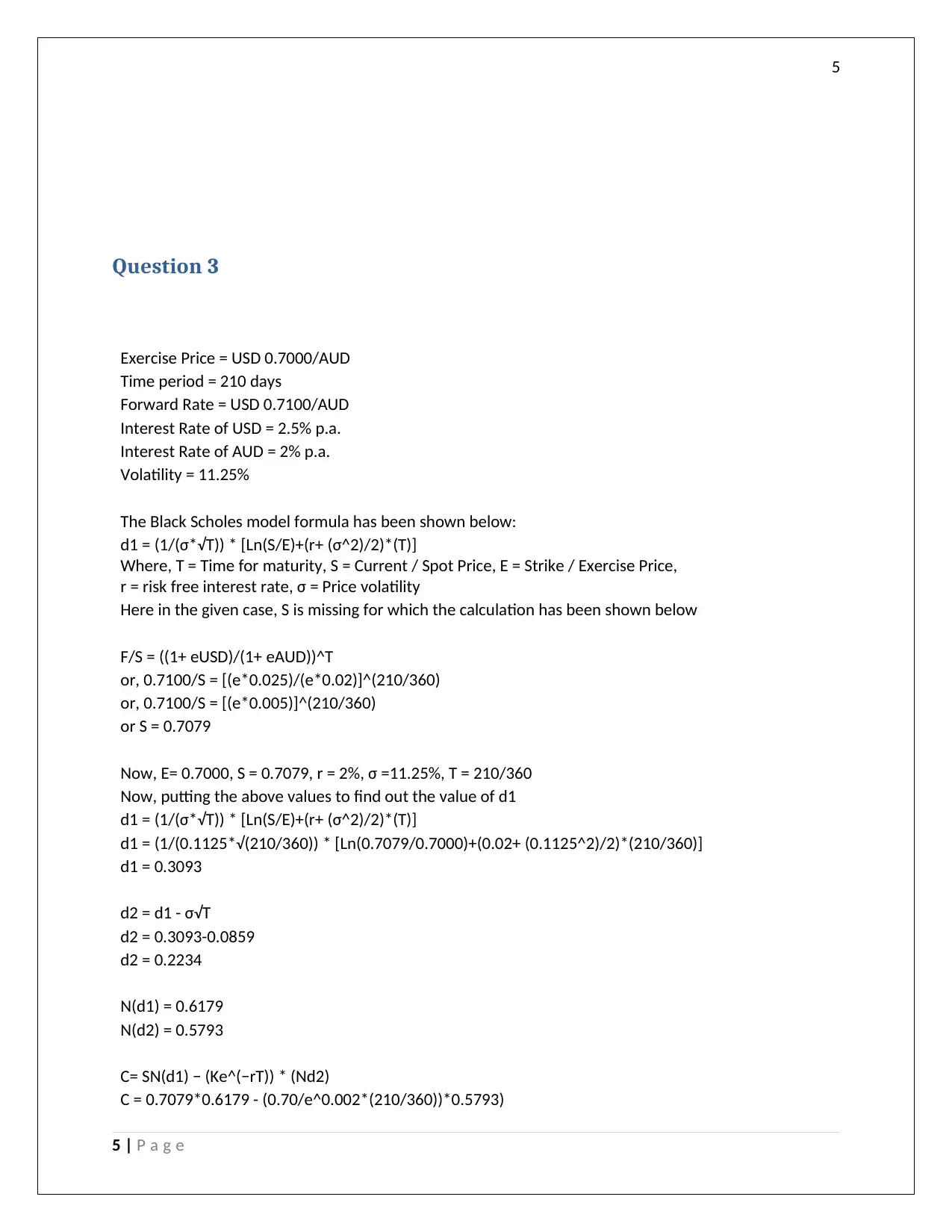

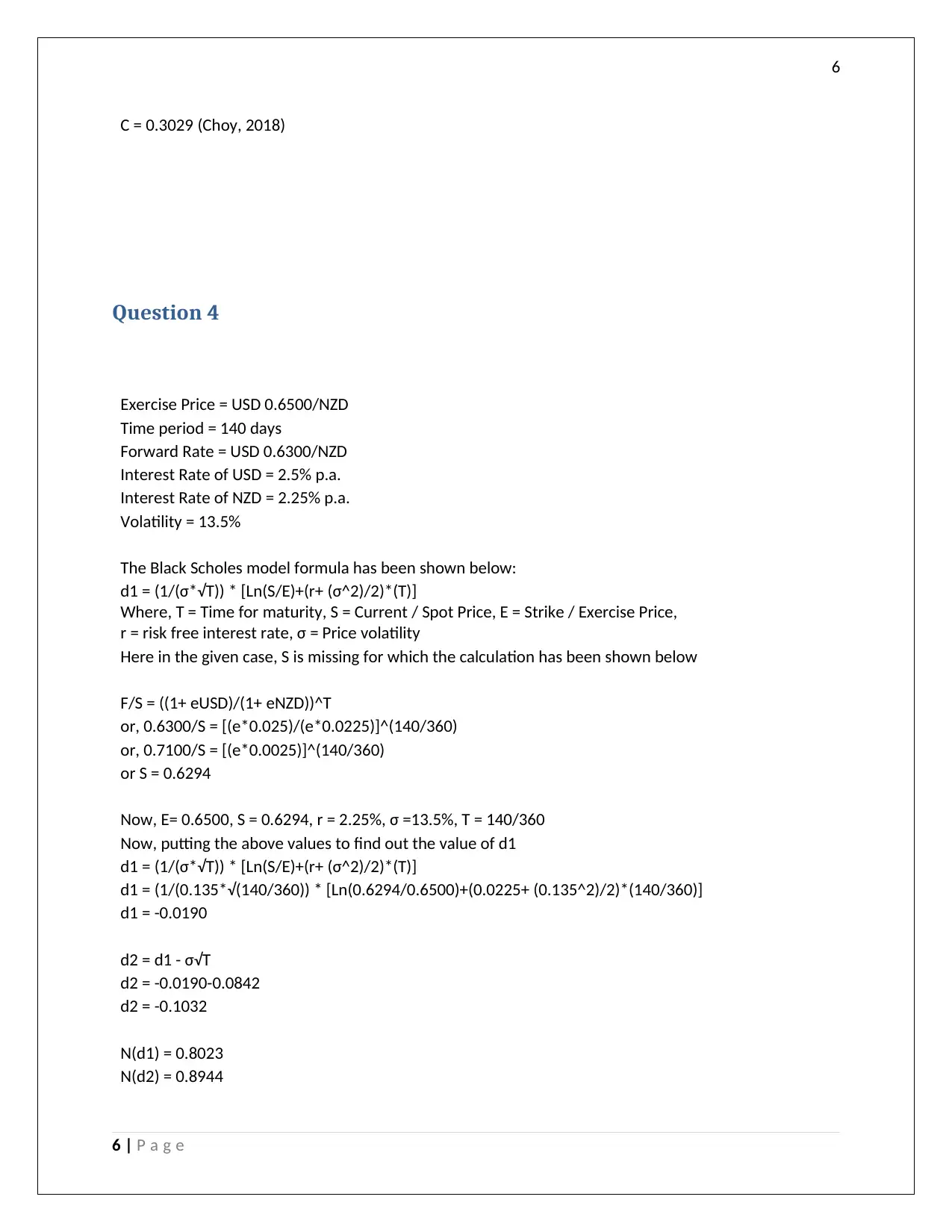

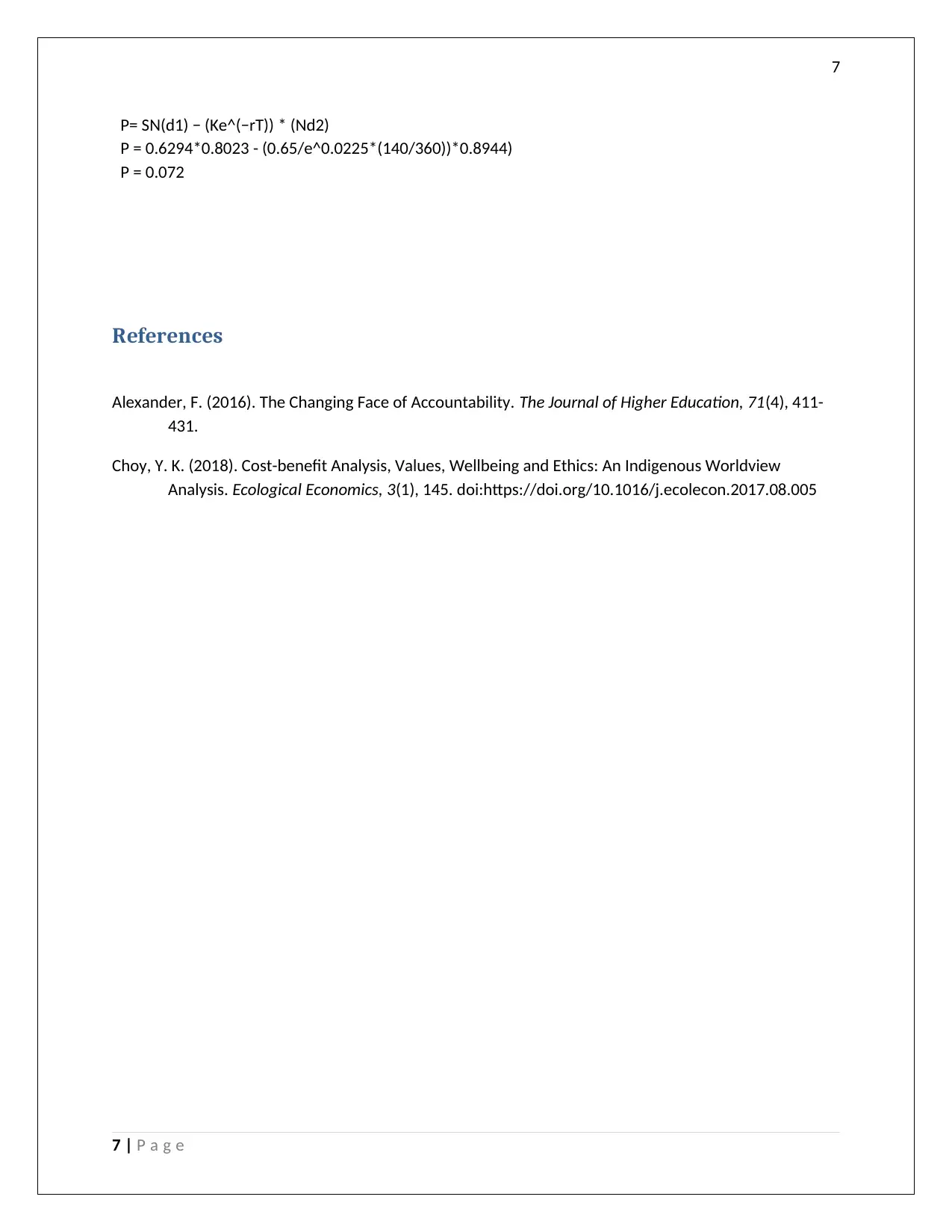

This finance assignment, completed by a student and available on Desklib, explores several key concepts in international finance. The assignment begins with a currency arbitrage problem, calculating potential profits from exploiting exchange rate discrepancies across different currency pairs (USD, JPY, and GBP). It then delves into forward exchange rates, calculating premiums and discounts for USD and CAD. The assignment utilizes the Black-Scholes model to price currency options, calculating option values for AUD and NZD options, incorporating factors like spot rates, forward rates, interest rates, volatility, and time to maturity. The assignment demonstrates the application of financial formulas and concepts in real-world scenarios, providing a comprehensive overview of foreign exchange and options trading.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.