ACC00716 Finance Case Study: Time Value, Bonds, Risk & Return Analysis

VerifiedAdded on 2023/06/12

|9

|1676

|192

Case Study

AI Summary

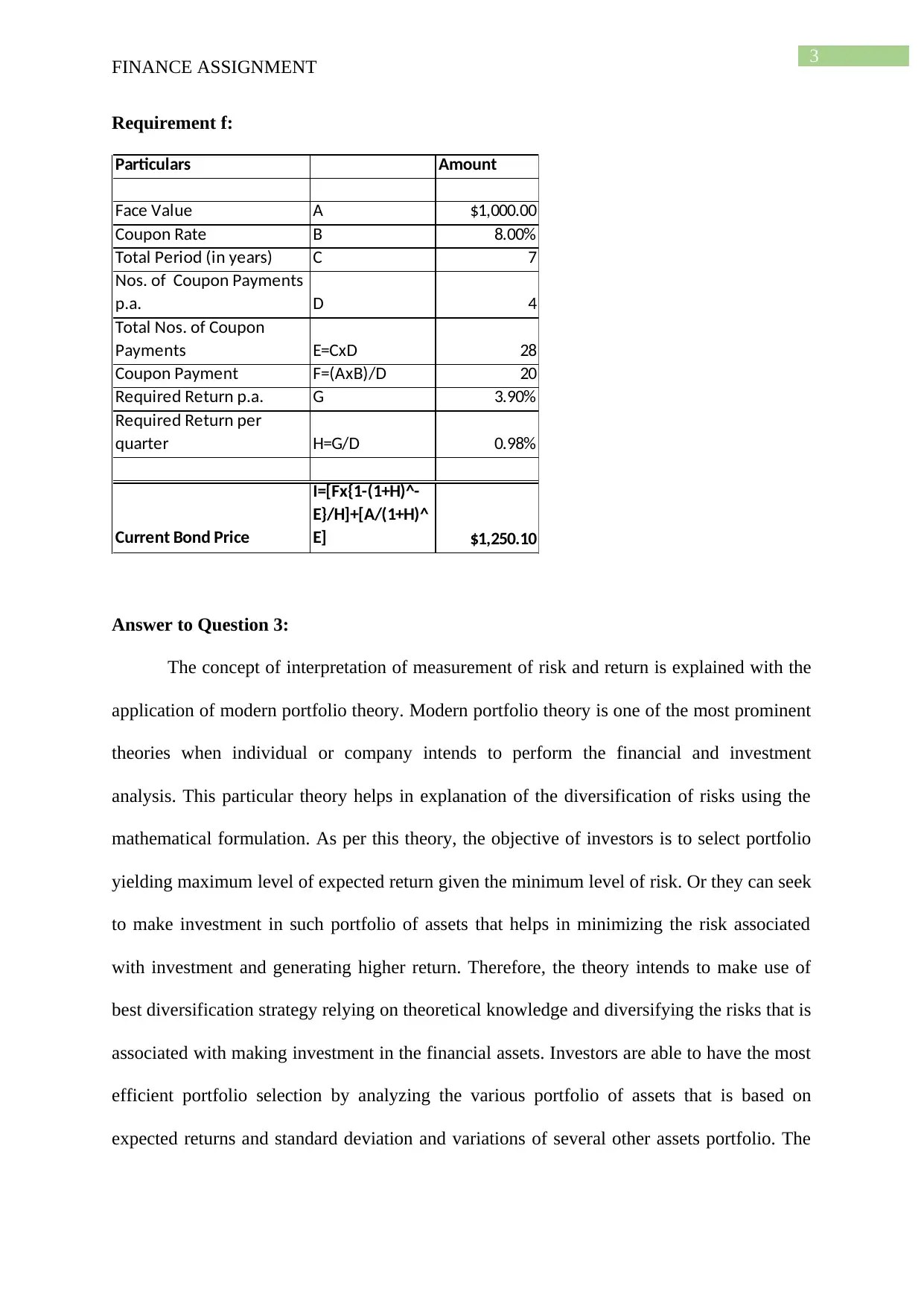

This finance case study provides solutions to questions on time value of money and bond valuation, alongside a risk and return analysis using modern portfolio theory. It explains concepts like diversification, risk-free rates, and beta values, demonstrating how to construct an efficient portfolio by balancing risk and return. The analysis includes calculations for expected portfolio return and beta, highlighting the benefits of diversification. Desklib offers a wide range of similar solved assignments and resources for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.