BAP53 Corporate Finance: Capital Budgeting & Bega Cheese Analysis

VerifiedAdded on 2023/06/10

|5

|739

|385

Case Study

AI Summary

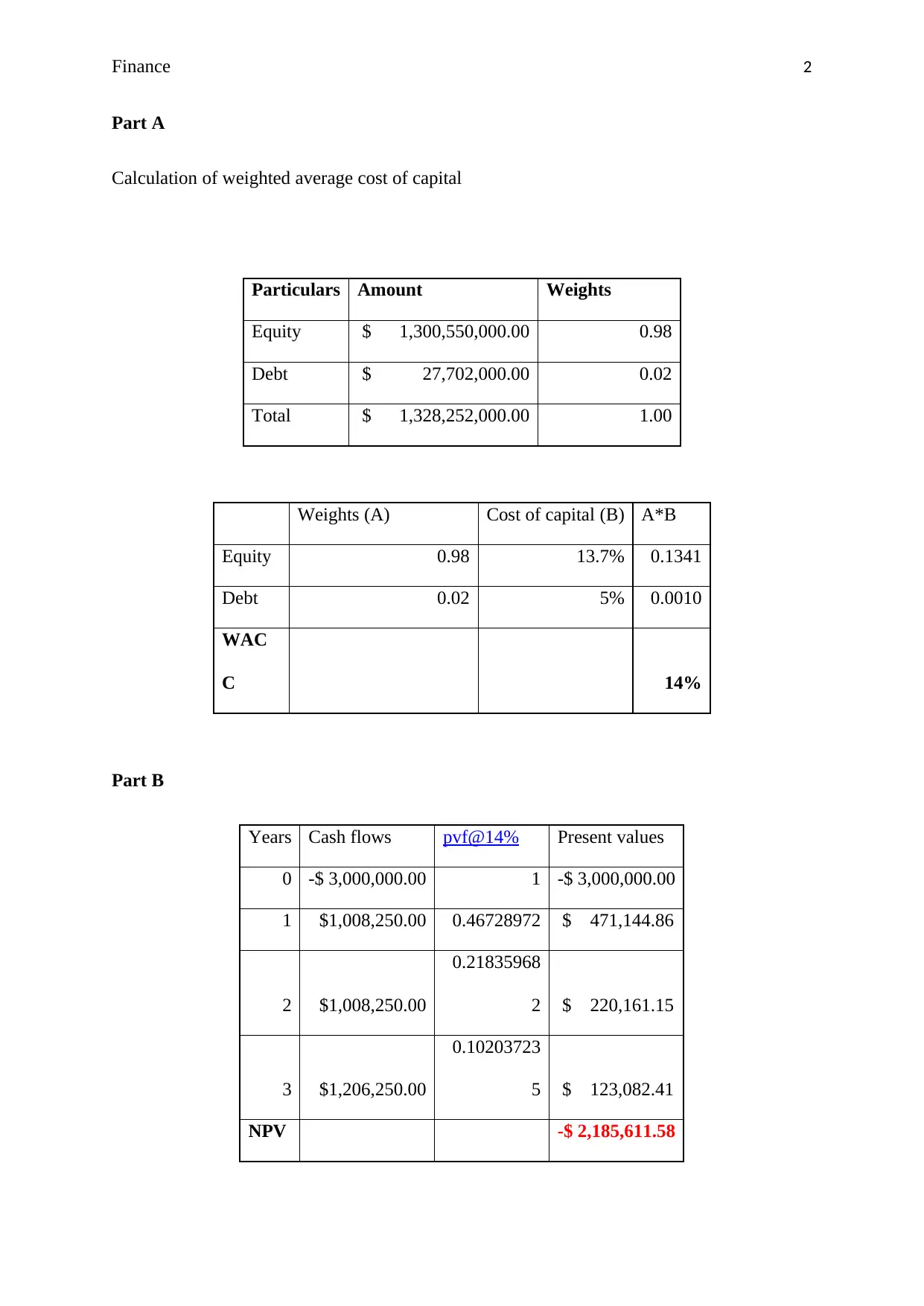

This case study assesses whether Bega Cheese should invest in a new yogurt range using Net Present Value (NPV) analysis. The solution calculates the Weighted Average Cost of Capital (WACC) and evaluates the project's NPV under normal, best-case, and worst-case scenarios. The analysis reveals a negative NPV in all scenarios, leading to the recommendation that Bega Cheese should not proceed with the investment. The study highlights the importance of NPV as a capital budgeting technique for evaluating project profitability and making informed investment decisions. Desklib offers more solved assignments and resources for students.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.