University Finance Case Study: Bega Cheese Portfolio Analysis and CAPM

VerifiedAdded on 2020/07/23

|9

|1917

|374

Case Study

AI Summary

This finance case study analyzes the Bega Cheese portfolio, a leading Australian dairy company. The study assesses historical monthly rates of return for the market index and computes average return and standard deviation. It calculates the portfolio's historical average rate of return and standard deviation, considering equal weights for Bega Cheese and a reference company. The expected rate of return is determined using the CAPM model, and the portfolio's beta is calculated. The analysis reveals a positive expected return for Bega Cheese and a negative return for the reference company. The study concludes that the CAPM model effectively measures stock return using risk-free return, market return, and beta, and that the portfolio demonstrates lower risk compared to the market as a whole. The findings highlight the importance of portfolio management in financial analysis for making informed investment decisions.

Finance Case Study 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

a....................................................................................................................................................3

1. Assessing historical monthly rates of return for the market index..........................................3

2. Computation of historical average return and standard deviation...........................................4

b. Calculating portfolio’s historical average rate of return and standard deviation.....................4

3. Assessing expected rate of return by taking into account CAPM model................................5

4. Expected return of portfolio and beta......................................................................................6

5...................................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

a....................................................................................................................................................3

1. Assessing historical monthly rates of return for the market index..........................................3

2. Computation of historical average return and standard deviation...........................................4

b. Calculating portfolio’s historical average rate of return and standard deviation.....................4

3. Assessing expected rate of return by taking into account CAPM model................................5

4. Expected return of portfolio and beta......................................................................................6

5...................................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

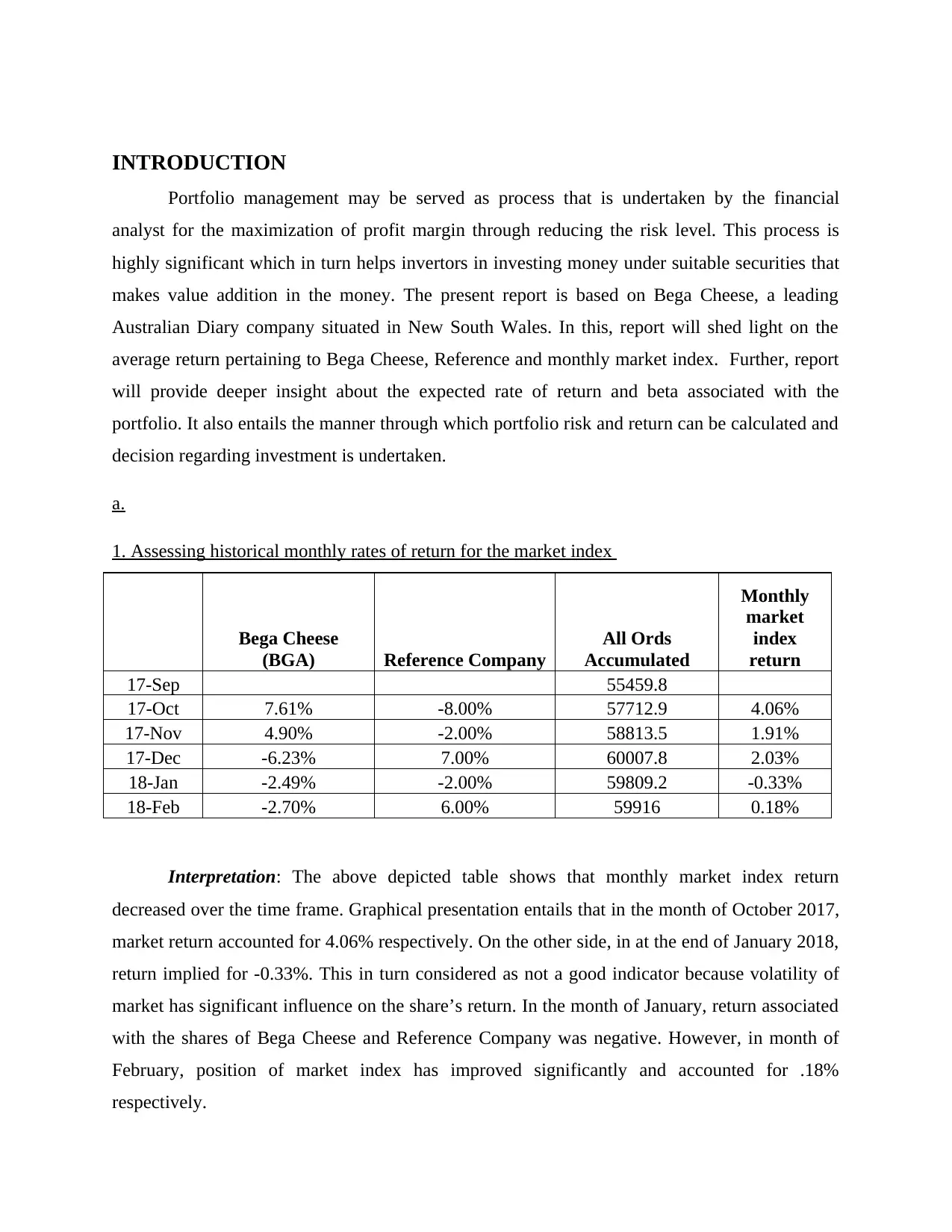

INTRODUCTION

Portfolio management may be served as process that is undertaken by the financial

analyst for the maximization of profit margin through reducing the risk level. This process is

highly significant which in turn helps invertors in investing money under suitable securities that

makes value addition in the money. The present report is based on Bega Cheese, a leading

Australian Diary company situated in New South Wales. In this, report will shed light on the

average return pertaining to Bega Cheese, Reference and monthly market index. Further, report

will provide deeper insight about the expected rate of return and beta associated with the

portfolio. It also entails the manner through which portfolio risk and return can be calculated and

decision regarding investment is undertaken.

a.

1. Assessing historical monthly rates of return for the market index

Bega Cheese

(BGA) Reference Company

All Ords

Accumulated

Monthly

market

index

return

17-Sep 55459.8

17-Oct 7.61% -8.00% 57712.9 4.06%

17-Nov 4.90% -2.00% 58813.5 1.91%

17-Dec -6.23% 7.00% 60007.8 2.03%

18-Jan -2.49% -2.00% 59809.2 -0.33%

18-Feb -2.70% 6.00% 59916 0.18%

Interpretation: The above depicted table shows that monthly market index return

decreased over the time frame. Graphical presentation entails that in the month of October 2017,

market return accounted for 4.06% respectively. On the other side, in at the end of January 2018,

return implied for -0.33%. This in turn considered as not a good indicator because volatility of

market has significant influence on the share’s return. In the month of January, return associated

with the shares of Bega Cheese and Reference Company was negative. However, in month of

February, position of market index has improved significantly and accounted for .18%

respectively.

Portfolio management may be served as process that is undertaken by the financial

analyst for the maximization of profit margin through reducing the risk level. This process is

highly significant which in turn helps invertors in investing money under suitable securities that

makes value addition in the money. The present report is based on Bega Cheese, a leading

Australian Diary company situated in New South Wales. In this, report will shed light on the

average return pertaining to Bega Cheese, Reference and monthly market index. Further, report

will provide deeper insight about the expected rate of return and beta associated with the

portfolio. It also entails the manner through which portfolio risk and return can be calculated and

decision regarding investment is undertaken.

a.

1. Assessing historical monthly rates of return for the market index

Bega Cheese

(BGA) Reference Company

All Ords

Accumulated

Monthly

market

index

return

17-Sep 55459.8

17-Oct 7.61% -8.00% 57712.9 4.06%

17-Nov 4.90% -2.00% 58813.5 1.91%

17-Dec -6.23% 7.00% 60007.8 2.03%

18-Jan -2.49% -2.00% 59809.2 -0.33%

18-Feb -2.70% 6.00% 59916 0.18%

Interpretation: The above depicted table shows that monthly market index return

decreased over the time frame. Graphical presentation entails that in the month of October 2017,

market return accounted for 4.06% respectively. On the other side, in at the end of January 2018,

return implied for -0.33%. This in turn considered as not a good indicator because volatility of

market has significant influence on the share’s return. In the month of January, return associated

with the shares of Bega Cheese and Reference Company was negative. However, in month of

February, position of market index has improved significantly and accounted for .18%

respectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Computation of historical average return and standard deviation

Bega Cheese

(BGA)

Reference

Company

Monthly

market index

return

17-Sep

17-Oct 7.61% -8.00% 4.06%

17-Nov 4.90% -2.00% 1.91%

17-Dec -6.23% 7.00% 2.03%

18-Jan -2.49% -2.00% -0.33%

18-Feb -2.70% 6.00% 0.18%

Average 0.22% 0.20% 1.57%

Standard deviation 0.06 0.06 0.02

Interpretation: From assessment, it has identified that mean return associated with the

shares of Bega Cheese accounted for 0.22%. On the other side, average market index return, in

relation to the period of 5 months implied for 1.57% respectively. In contrast to this, during the

concerned period, mean income enjoyed by the shareholders implies for 0.20%. Referring

overall evaluation, it can be presented that in line with the market index return, average return

offered by Bega Cheese to the investors was good. Further, outcome of standard deviation shows

that in comparison to the market index, return associated with the shares of Bega Cheese and

Reference Company is highly volatile as it accounts for 0.06.

b. Calculating portfolio’s historical average rate of return and standard deviation

Given that: weights are equal such as 50% for Bega cheese and remaining related to Reference

company

Bega Cheese (BGA) Reference Company

weight 0.5 0.5

average return 0.22% 0.20%

Returns 0.11% 0.10%

Historical return on the

portfolio 0.11% + 0.10% = 0.21%

Bega Cheese

(BGA)

Reference

Company

Monthly

market index

return

17-Sep

17-Oct 7.61% -8.00% 4.06%

17-Nov 4.90% -2.00% 1.91%

17-Dec -6.23% 7.00% 2.03%

18-Jan -2.49% -2.00% -0.33%

18-Feb -2.70% 6.00% 0.18%

Average 0.22% 0.20% 1.57%

Standard deviation 0.06 0.06 0.02

Interpretation: From assessment, it has identified that mean return associated with the

shares of Bega Cheese accounted for 0.22%. On the other side, average market index return, in

relation to the period of 5 months implied for 1.57% respectively. In contrast to this, during the

concerned period, mean income enjoyed by the shareholders implies for 0.20%. Referring

overall evaluation, it can be presented that in line with the market index return, average return

offered by Bega Cheese to the investors was good. Further, outcome of standard deviation shows

that in comparison to the market index, return associated with the shares of Bega Cheese and

Reference Company is highly volatile as it accounts for 0.06.

b. Calculating portfolio’s historical average rate of return and standard deviation

Given that: weights are equal such as 50% for Bega cheese and remaining related to Reference

company

Bega Cheese (BGA) Reference Company

weight 0.5 0.5

average return 0.22% 0.20%

Returns 0.11% 0.10%

Historical return on the

portfolio 0.11% + 0.10% = 0.21%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

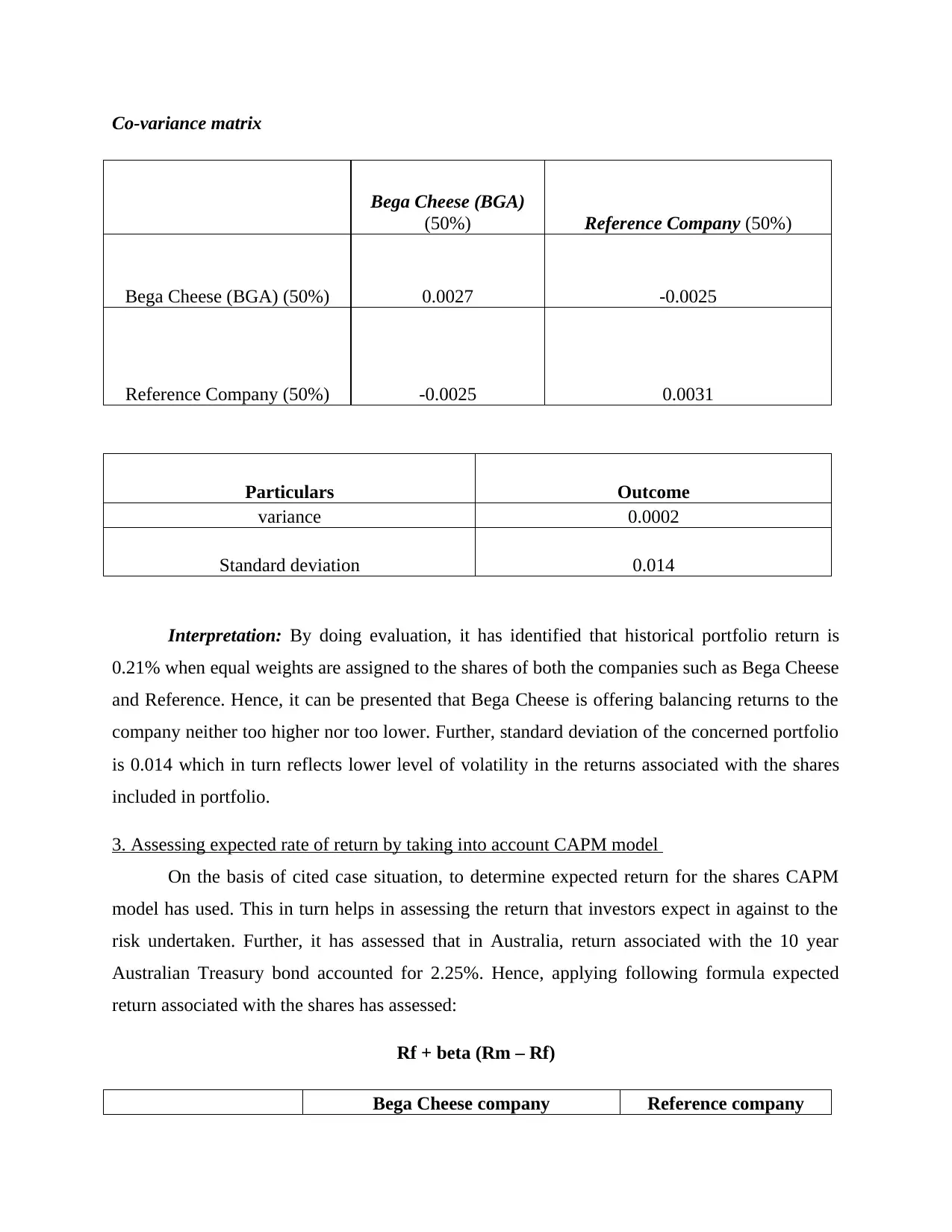

Co-variance matrix

Bega Cheese (BGA)

(50%) Reference Company (50%)

Bega Cheese (BGA) (50%) 0.0027 -0.0025

Reference Company (50%) -0.0025 0.0031

Particulars Outcome

variance 0.0002

Standard deviation 0.014

Interpretation: By doing evaluation, it has identified that historical portfolio return is

0.21% when equal weights are assigned to the shares of both the companies such as Bega Cheese

and Reference. Hence, it can be presented that Bega Cheese is offering balancing returns to the

company neither too higher nor too lower. Further, standard deviation of the concerned portfolio

is 0.014 which in turn reflects lower level of volatility in the returns associated with the shares

included in portfolio.

3. Assessing expected rate of return by taking into account CAPM model

On the basis of cited case situation, to determine expected return for the shares CAPM

model has used. This in turn helps in assessing the return that investors expect in against to the

risk undertaken. Further, it has assessed that in Australia, return associated with the 10 year

Australian Treasury bond accounted for 2.25%. Hence, applying following formula expected

return associated with the shares has assessed:

Rf + beta (Rm – Rf)

Bega Cheese company Reference company

Bega Cheese (BGA)

(50%) Reference Company (50%)

Bega Cheese (BGA) (50%) 0.0027 -0.0025

Reference Company (50%) -0.0025 0.0031

Particulars Outcome

variance 0.0002

Standard deviation 0.014

Interpretation: By doing evaluation, it has identified that historical portfolio return is

0.21% when equal weights are assigned to the shares of both the companies such as Bega Cheese

and Reference. Hence, it can be presented that Bega Cheese is offering balancing returns to the

company neither too higher nor too lower. Further, standard deviation of the concerned portfolio

is 0.014 which in turn reflects lower level of volatility in the returns associated with the shares

included in portfolio.

3. Assessing expected rate of return by taking into account CAPM model

On the basis of cited case situation, to determine expected return for the shares CAPM

model has used. This in turn helps in assessing the return that investors expect in against to the

risk undertaken. Further, it has assessed that in Australia, return associated with the 10 year

Australian Treasury bond accounted for 2.25%. Hence, applying following formula expected

return associated with the shares has assessed:

Rf + beta (Rm – Rf)

Bega Cheese company Reference company

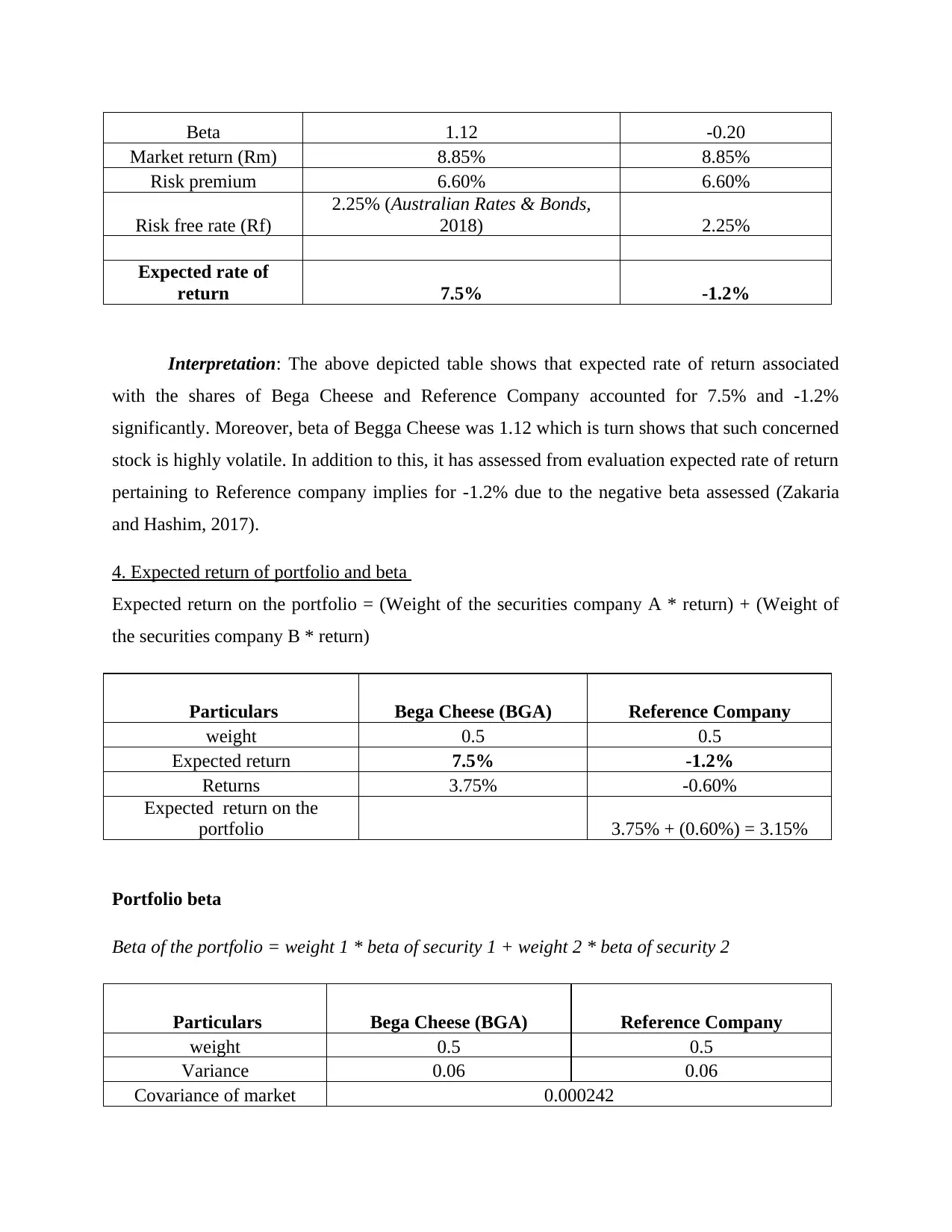

Beta 1.12 -0.20

Market return (Rm) 8.85% 8.85%

Risk premium 6.60% 6.60%

Risk free rate (Rf)

2.25% (Australian Rates & Bonds,

2018) 2.25%

Expected rate of

return 7.5% -1.2%

Interpretation: The above depicted table shows that expected rate of return associated

with the shares of Bega Cheese and Reference Company accounted for 7.5% and -1.2%

significantly. Moreover, beta of Begga Cheese was 1.12 which is turn shows that such concerned

stock is highly volatile. In addition to this, it has assessed from evaluation expected rate of return

pertaining to Reference company implies for -1.2% due to the negative beta assessed (Zakaria

and Hashim, 2017).

4. Expected return of portfolio and beta

Expected return on the portfolio = (Weight of the securities company A * return) + (Weight of

the securities company B * return)

Particulars Bega Cheese (BGA) Reference Company

weight 0.5 0.5

Expected return 7.5% -1.2%

Returns 3.75% -0.60%

Expected return on the

portfolio 3.75% + (0.60%) = 3.15%

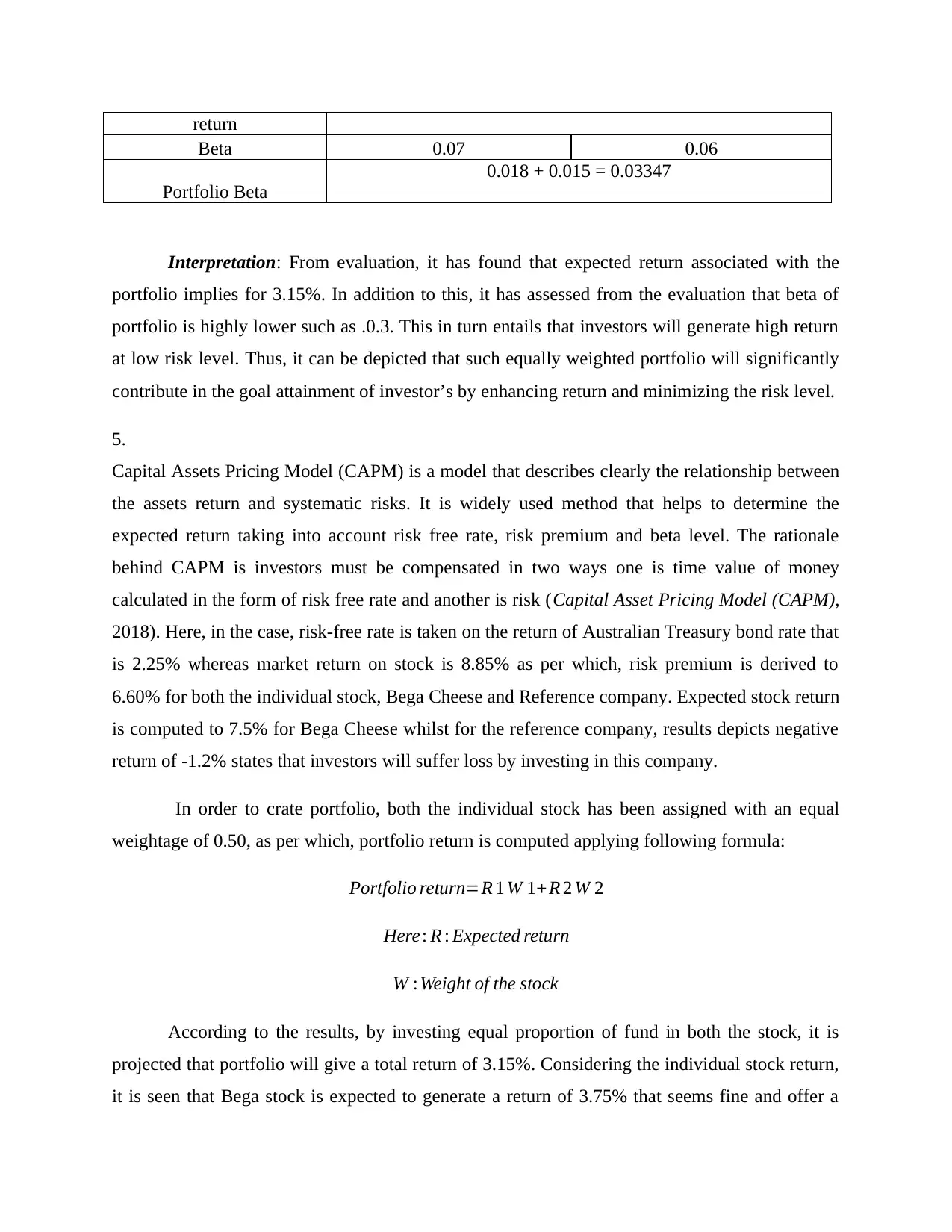

Portfolio beta

Beta of the portfolio = weight 1 * beta of security 1 + weight 2 * beta of security 2

Particulars Bega Cheese (BGA) Reference Company

weight 0.5 0.5

Variance 0.06 0.06

Covariance of market 0.000242

Market return (Rm) 8.85% 8.85%

Risk premium 6.60% 6.60%

Risk free rate (Rf)

2.25% (Australian Rates & Bonds,

2018) 2.25%

Expected rate of

return 7.5% -1.2%

Interpretation: The above depicted table shows that expected rate of return associated

with the shares of Bega Cheese and Reference Company accounted for 7.5% and -1.2%

significantly. Moreover, beta of Begga Cheese was 1.12 which is turn shows that such concerned

stock is highly volatile. In addition to this, it has assessed from evaluation expected rate of return

pertaining to Reference company implies for -1.2% due to the negative beta assessed (Zakaria

and Hashim, 2017).

4. Expected return of portfolio and beta

Expected return on the portfolio = (Weight of the securities company A * return) + (Weight of

the securities company B * return)

Particulars Bega Cheese (BGA) Reference Company

weight 0.5 0.5

Expected return 7.5% -1.2%

Returns 3.75% -0.60%

Expected return on the

portfolio 3.75% + (0.60%) = 3.15%

Portfolio beta

Beta of the portfolio = weight 1 * beta of security 1 + weight 2 * beta of security 2

Particulars Bega Cheese (BGA) Reference Company

weight 0.5 0.5

Variance 0.06 0.06

Covariance of market 0.000242

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

return

Beta 0.07 0.06

Portfolio Beta

0.018 + 0.015 = 0.03347

Interpretation: From evaluation, it has found that expected return associated with the

portfolio implies for 3.15%. In addition to this, it has assessed from the evaluation that beta of

portfolio is highly lower such as .0.3. This in turn entails that investors will generate high return

at low risk level. Thus, it can be depicted that such equally weighted portfolio will significantly

contribute in the goal attainment of investor’s by enhancing return and minimizing the risk level.

5.

Capital Assets Pricing Model (CAPM) is a model that describes clearly the relationship between

the assets return and systematic risks. It is widely used method that helps to determine the

expected return taking into account risk free rate, risk premium and beta level. The rationale

behind CAPM is investors must be compensated in two ways one is time value of money

calculated in the form of risk free rate and another is risk (Capital Asset Pricing Model (CAPM),

2018). Here, in the case, risk-free rate is taken on the return of Australian Treasury bond rate that

is 2.25% whereas market return on stock is 8.85% as per which, risk premium is derived to

6.60% for both the individual stock, Bega Cheese and Reference company. Expected stock return

is computed to 7.5% for Bega Cheese whilst for the reference company, results depicts negative

return of -1.2% states that investors will suffer loss by investing in this company.

In order to crate portfolio, both the individual stock has been assigned with an equal

weightage of 0.50, as per which, portfolio return is computed applying following formula:

Portfolio return=R 1 W 1+ R 2 W 2

Here : R : Expected return

W :Weight of the stock

According to the results, by investing equal proportion of fund in both the stock, it is

projected that portfolio will give a total return of 3.15%. Considering the individual stock return,

it is seen that Bega stock is expected to generate a return of 3.75% that seems fine and offer a

Beta 0.07 0.06

Portfolio Beta

0.018 + 0.015 = 0.03347

Interpretation: From evaluation, it has found that expected return associated with the

portfolio implies for 3.15%. In addition to this, it has assessed from the evaluation that beta of

portfolio is highly lower such as .0.3. This in turn entails that investors will generate high return

at low risk level. Thus, it can be depicted that such equally weighted portfolio will significantly

contribute in the goal attainment of investor’s by enhancing return and minimizing the risk level.

5.

Capital Assets Pricing Model (CAPM) is a model that describes clearly the relationship between

the assets return and systematic risks. It is widely used method that helps to determine the

expected return taking into account risk free rate, risk premium and beta level. The rationale

behind CAPM is investors must be compensated in two ways one is time value of money

calculated in the form of risk free rate and another is risk (Capital Asset Pricing Model (CAPM),

2018). Here, in the case, risk-free rate is taken on the return of Australian Treasury bond rate that

is 2.25% whereas market return on stock is 8.85% as per which, risk premium is derived to

6.60% for both the individual stock, Bega Cheese and Reference company. Expected stock return

is computed to 7.5% for Bega Cheese whilst for the reference company, results depicts negative

return of -1.2% states that investors will suffer loss by investing in this company.

In order to crate portfolio, both the individual stock has been assigned with an equal

weightage of 0.50, as per which, portfolio return is computed applying following formula:

Portfolio return=R 1 W 1+ R 2 W 2

Here : R : Expected return

W :Weight of the stock

According to the results, by investing equal proportion of fund in both the stock, it is

projected that portfolio will give a total return of 3.15%. Considering the individual stock return,

it is seen that Bega stock is expected to generate a return of 3.75% that seems fine and offer a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

good return to the investor however; in contrast, Reference Company’s stock shows negative

results of -0.60% evident loss by putting money in this company’s stock (Fernholz, 2016).

Portfolio is subjected with the market risk and in order to measure the risk, portfolio beta is

calculated that helps to measure the volatility taking market as a whole. Portfolio beta is

measured by using the following formula:

Beta of the portfolio = weight 1 * beta of security 1 + weight 2 * beta of security 2

Beta coefficient of 1 show that stock and the market suffers same risk however value

below 1 indicates lower risk than overall market. Here, in the case, the value of beta coefficient

of the portfolio is derived 0.03 that evident portfolio is less risk and shows lower average risk

and return in comparison to the overall market.

CONCLUSION

The findings of the study concluded that CAPM is the best model to measure the return

of a stock using various components such as risk-free return, market return and beta value. The

output through the model reflects greater return in Bega Cheese Company compared to

Reference Company. By investing equal proportion of 50% in both the company’s stock, it is

anticipated that project is expected to generate a return of 3.15% at beta coefficient of 0.75

evident lower risk compared to the market as a whole. The research investigation brought the

fact into consideration portfolio management is a great tool in which analyst apply various

financial tools and models so as to analyze the risk and return measures for the investment

decisions.

results of -0.60% evident loss by putting money in this company’s stock (Fernholz, 2016).

Portfolio is subjected with the market risk and in order to measure the risk, portfolio beta is

calculated that helps to measure the volatility taking market as a whole. Portfolio beta is

measured by using the following formula:

Beta of the portfolio = weight 1 * beta of security 1 + weight 2 * beta of security 2

Beta coefficient of 1 show that stock and the market suffers same risk however value

below 1 indicates lower risk than overall market. Here, in the case, the value of beta coefficient

of the portfolio is derived 0.03 that evident portfolio is less risk and shows lower average risk

and return in comparison to the overall market.

CONCLUSION

The findings of the study concluded that CAPM is the best model to measure the return

of a stock using various components such as risk-free return, market return and beta value. The

output through the model reflects greater return in Bega Cheese Company compared to

Reference Company. By investing equal proportion of 50% in both the company’s stock, it is

anticipated that project is expected to generate a return of 3.15% at beta coefficient of 0.75

evident lower risk compared to the market as a whole. The research investigation brought the

fact into consideration portfolio management is a great tool in which analyst apply various

financial tools and models so as to analyze the risk and return measures for the investment

decisions.

REFERENCES

Books and Journals

Fernholz, R., 2016. A new decomposition of portfolio return. arXiv preprint arXiv:1606.05877.

Zakaria, N. and Hashim, F., 2017. Emerging Markets: Evaluating Graham’s Stock Selection

Criteria on Portfolio Return in Saudi Arabia Stock Market. International Journal of

Economics and Financial Issues. 7(2). pp.453-459.

Online

Australian Rates & Bonds. 2018. [Online]. Available through:

<https://www.bloomberg.com/markets/rates-bonds/government-bonds/australia>.

Capital Asset Pricing Model (CAPM). 2018. [Online]. Available through:

<http://www.investinganswers.com/financial-dictionary/stock-valuation/capital-asset-

pricing-model-capm-1125>.

Books and Journals

Fernholz, R., 2016. A new decomposition of portfolio return. arXiv preprint arXiv:1606.05877.

Zakaria, N. and Hashim, F., 2017. Emerging Markets: Evaluating Graham’s Stock Selection

Criteria on Portfolio Return in Saudi Arabia Stock Market. International Journal of

Economics and Financial Issues. 7(2). pp.453-459.

Online

Australian Rates & Bonds. 2018. [Online]. Available through:

<https://www.bloomberg.com/markets/rates-bonds/government-bonds/australia>.

Capital Asset Pricing Model (CAPM). 2018. [Online]. Available through:

<http://www.investinganswers.com/financial-dictionary/stock-valuation/capital-asset-

pricing-model-capm-1125>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.