A Comparative Analysis of Ramsay Health Care Limited and Quadrant Private Equity

VerifiedAdded on 2022/10/17

|14

|2828

|393

Assignment

AI Summary

Contents Introduction 3 Items in Equity Section 3 Equity Section – Movements 4 Liabilities section 5 Liabilities section – Movements 6 Comparison of the sources of funds 8 Part B 9 References 13 Introduction Ramsay Health Care Limited is a private healthcare service provider found and established in Australia. The share price fell significantly in 2018 when a public inquiry was announced by the government in the aged care center (Estia Health, 2018).

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Corporate and Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Finance

Abstract

The assignment is based upon the different sources that a company uses to raise funds. In

this report, two companies are selected for evaluation that is Ramsay Health Care Limited

and Quadrant Private Equity both operates in the field of health. The comparative analysis is

done considering a time frame of three years. With the help of this report, the fund movement

of the companies will be known with ease. Further, the second part of the part is devoted to

the classification of different entities for reporting purpose.

2

Abstract

The assignment is based upon the different sources that a company uses to raise funds. In

this report, two companies are selected for evaluation that is Ramsay Health Care Limited

and Quadrant Private Equity both operates in the field of health. The comparative analysis is

done considering a time frame of three years. With the help of this report, the fund movement

of the companies will be known with ease. Further, the second part of the part is devoted to

the classification of different entities for reporting purpose.

2

Finance

Contents

Introduction...........................................................................................................................................................3

Items in Equity Section...........................................................................................................................................3

Equity Section – Movements..................................................................................................................................4

Liabilities section....................................................................................................................................................5

Liabilities section – Movements.............................................................................................................................6

Comparison of the sources of funds.......................................................................................................................8

Part B......................................................................................................................................................................9

References............................................................................................................................................................13

3

Contents

Introduction...........................................................................................................................................................3

Items in Equity Section...........................................................................................................................................3

Equity Section – Movements..................................................................................................................................4

Liabilities section....................................................................................................................................................5

Liabilities section – Movements.............................................................................................................................6

Comparison of the sources of funds.......................................................................................................................8

Part B......................................................................................................................................................................9

References............................................................................................................................................................13

3

Finance

Introduction

Ramsay Health Care Limited is a private healthcare service provider found and established in

Australia. With specialization in surgery, psychiatric care and rehabilitation, it has been able to

successfully spread its operation to the UK, USA, France, Malaysia, and Indonesia. It has

more than 100 facility operation centers in Australia making it the largest service provider.

The global operations are over 500 locations committed to delivering high-quality healthcare

services to the patients (Ramsay Health Care, 2018). It is a well-respected name in the

industry and has an excellent track record in patient care, staff engagement and hospital

management.

Quadrant Private Equity floated an aged care operation in 2014 in Australia under the name

Estia Health. Today it is listed on the ASX and valued in millions. It operates through its 69

locations in New South Wales, South Australia, Victoria, and Queensland. The share price fell

significantly in 2018 when a public inquiry was announced by the government in the aged

care center (Estia Health, 2018).

Items in Equity Section

The equity section comprises of issued capital, treasury shares, and convertible adjustable-

rate equity securities (CARES), other reserves and retained earnings. Issued share capital

refers to the ordinary shares that are entitled to one vote per share, either in person or in

proxy at the general meetings of the shareholders (Ramsay Health Care, 2018). They are

entitled to receive dividends as and when declared and also enjoy the rights of participation in

the surplus assets of the company in the event of winding up in proportion to the number and

amounts paid up on the shares. Treasury shares are held by the Employee share plans and

these are deducted from the equity. CARES are the non-cumulative, redeemable, convertible

preference shares issued by Ramsay with a face value of $100 per CARES. The dividend

rate is calculated based on the market rate and the margin. CARES do not have any maturity

date but it can be converted into shares upon the happening of the regulatory event which is

declared by Ramsay. CARES holders do not enjoy voting rights in general meetings.

Estia Health’s Equity section comprises of Issued Capital, Share-based payments reserve

and retained earnings which in this case are accumulated losses (Estia Health, 2018).

4

Introduction

Ramsay Health Care Limited is a private healthcare service provider found and established in

Australia. With specialization in surgery, psychiatric care and rehabilitation, it has been able to

successfully spread its operation to the UK, USA, France, Malaysia, and Indonesia. It has

more than 100 facility operation centers in Australia making it the largest service provider.

The global operations are over 500 locations committed to delivering high-quality healthcare

services to the patients (Ramsay Health Care, 2018). It is a well-respected name in the

industry and has an excellent track record in patient care, staff engagement and hospital

management.

Quadrant Private Equity floated an aged care operation in 2014 in Australia under the name

Estia Health. Today it is listed on the ASX and valued in millions. It operates through its 69

locations in New South Wales, South Australia, Victoria, and Queensland. The share price fell

significantly in 2018 when a public inquiry was announced by the government in the aged

care center (Estia Health, 2018).

Items in Equity Section

The equity section comprises of issued capital, treasury shares, and convertible adjustable-

rate equity securities (CARES), other reserves and retained earnings. Issued share capital

refers to the ordinary shares that are entitled to one vote per share, either in person or in

proxy at the general meetings of the shareholders (Ramsay Health Care, 2018). They are

entitled to receive dividends as and when declared and also enjoy the rights of participation in

the surplus assets of the company in the event of winding up in proportion to the number and

amounts paid up on the shares. Treasury shares are held by the Employee share plans and

these are deducted from the equity. CARES are the non-cumulative, redeemable, convertible

preference shares issued by Ramsay with a face value of $100 per CARES. The dividend

rate is calculated based on the market rate and the margin. CARES do not have any maturity

date but it can be converted into shares upon the happening of the regulatory event which is

declared by Ramsay. CARES holders do not enjoy voting rights in general meetings.

Estia Health’s Equity section comprises of Issued Capital, Share-based payments reserve

and retained earnings which in this case are accumulated losses (Estia Health, 2018).

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Finance

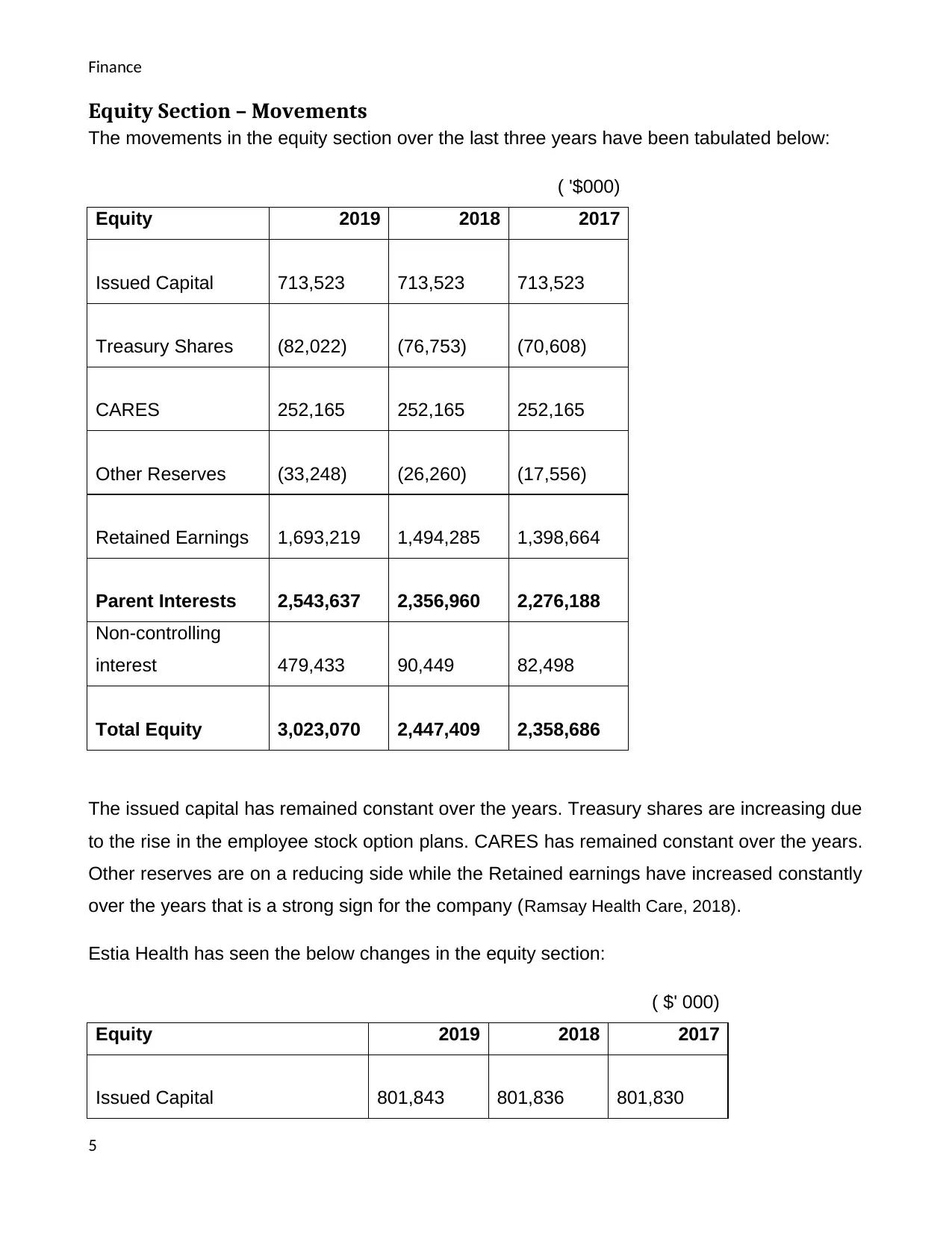

Equity Section – Movements

The movements in the equity section over the last three years have been tabulated below:

( '$000)

Equity 2019 2018 2017

Issued Capital 713,523 713,523 713,523

Treasury Shares (82,022) (76,753) (70,608)

CARES 252,165 252,165 252,165

Other Reserves (33,248) (26,260) (17,556)

Retained Earnings 1,693,219 1,494,285 1,398,664

Parent Interests 2,543,637 2,356,960 2,276,188

Non-controlling

interest 479,433 90,449 82,498

Total Equity 3,023,070 2,447,409 2,358,686

The issued capital has remained constant over the years. Treasury shares are increasing due

to the rise in the employee stock option plans. CARES has remained constant over the years.

Other reserves are on a reducing side while the Retained earnings have increased constantly

over the years that is a strong sign for the company (Ramsay Health Care, 2018).

Estia Health has seen the below changes in the equity section:

( $' 000)

Equity 2019 2018 2017

Issued Capital 801,843 801,836 801,830

5

Equity Section – Movements

The movements in the equity section over the last three years have been tabulated below:

( '$000)

Equity 2019 2018 2017

Issued Capital 713,523 713,523 713,523

Treasury Shares (82,022) (76,753) (70,608)

CARES 252,165 252,165 252,165

Other Reserves (33,248) (26,260) (17,556)

Retained Earnings 1,693,219 1,494,285 1,398,664

Parent Interests 2,543,637 2,356,960 2,276,188

Non-controlling

interest 479,433 90,449 82,498

Total Equity 3,023,070 2,447,409 2,358,686

The issued capital has remained constant over the years. Treasury shares are increasing due

to the rise in the employee stock option plans. CARES has remained constant over the years.

Other reserves are on a reducing side while the Retained earnings have increased constantly

over the years that is a strong sign for the company (Ramsay Health Care, 2018).

Estia Health has seen the below changes in the equity section:

( $' 000)

Equity 2019 2018 2017

Issued Capital 801,843 801,836 801,830

5

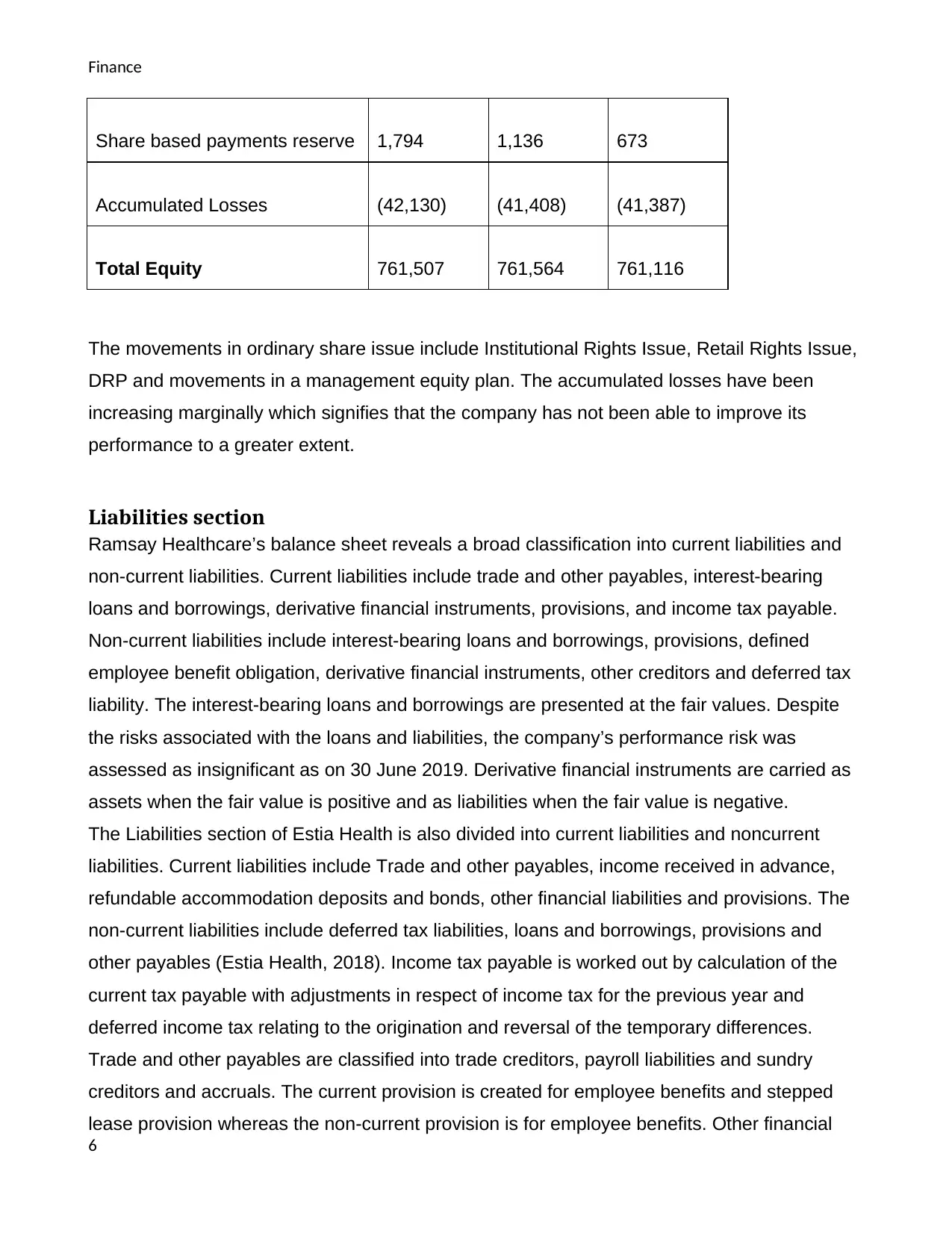

Finance

Share based payments reserve 1,794 1,136 673

Accumulated Losses (42,130) (41,408) (41,387)

Total Equity 761,507 761,564 761,116

The movements in ordinary share issue include Institutional Rights Issue, Retail Rights Issue,

DRP and movements in a management equity plan. The accumulated losses have been

increasing marginally which signifies that the company has not been able to improve its

performance to a greater extent.

Liabilities section

Ramsay Healthcare’s balance sheet reveals a broad classification into current liabilities and

non-current liabilities. Current liabilities include trade and other payables, interest-bearing

loans and borrowings, derivative financial instruments, provisions, and income tax payable.

Non-current liabilities include interest-bearing loans and borrowings, provisions, defined

employee benefit obligation, derivative financial instruments, other creditors and deferred tax

liability. The interest-bearing loans and borrowings are presented at the fair values. Despite

the risks associated with the loans and liabilities, the company’s performance risk was

assessed as insignificant as on 30 June 2019. Derivative financial instruments are carried as

assets when the fair value is positive and as liabilities when the fair value is negative.

The Liabilities section of Estia Health is also divided into current liabilities and noncurrent

liabilities. Current liabilities include Trade and other payables, income received in advance,

refundable accommodation deposits and bonds, other financial liabilities and provisions. The

non-current liabilities include deferred tax liabilities, loans and borrowings, provisions and

other payables (Estia Health, 2018). Income tax payable is worked out by calculation of the

current tax payable with adjustments in respect of income tax for the previous year and

deferred income tax relating to the origination and reversal of the temporary differences.

Trade and other payables are classified into trade creditors, payroll liabilities and sundry

creditors and accruals. The current provision is created for employee benefits and stepped

lease provision whereas the non-current provision is for employee benefits. Other financial

6

Share based payments reserve 1,794 1,136 673

Accumulated Losses (42,130) (41,408) (41,387)

Total Equity 761,507 761,564 761,116

The movements in ordinary share issue include Institutional Rights Issue, Retail Rights Issue,

DRP and movements in a management equity plan. The accumulated losses have been

increasing marginally which signifies that the company has not been able to improve its

performance to a greater extent.

Liabilities section

Ramsay Healthcare’s balance sheet reveals a broad classification into current liabilities and

non-current liabilities. Current liabilities include trade and other payables, interest-bearing

loans and borrowings, derivative financial instruments, provisions, and income tax payable.

Non-current liabilities include interest-bearing loans and borrowings, provisions, defined

employee benefit obligation, derivative financial instruments, other creditors and deferred tax

liability. The interest-bearing loans and borrowings are presented at the fair values. Despite

the risks associated with the loans and liabilities, the company’s performance risk was

assessed as insignificant as on 30 June 2019. Derivative financial instruments are carried as

assets when the fair value is positive and as liabilities when the fair value is negative.

The Liabilities section of Estia Health is also divided into current liabilities and noncurrent

liabilities. Current liabilities include Trade and other payables, income received in advance,

refundable accommodation deposits and bonds, other financial liabilities and provisions. The

non-current liabilities include deferred tax liabilities, loans and borrowings, provisions and

other payables (Estia Health, 2018). Income tax payable is worked out by calculation of the

current tax payable with adjustments in respect of income tax for the previous year and

deferred income tax relating to the origination and reversal of the temporary differences.

Trade and other payables are classified into trade creditors, payroll liabilities and sundry

creditors and accruals. The current provision is created for employee benefits and stepped

lease provision whereas the non-current provision is for employee benefits. Other financial

6

Finance

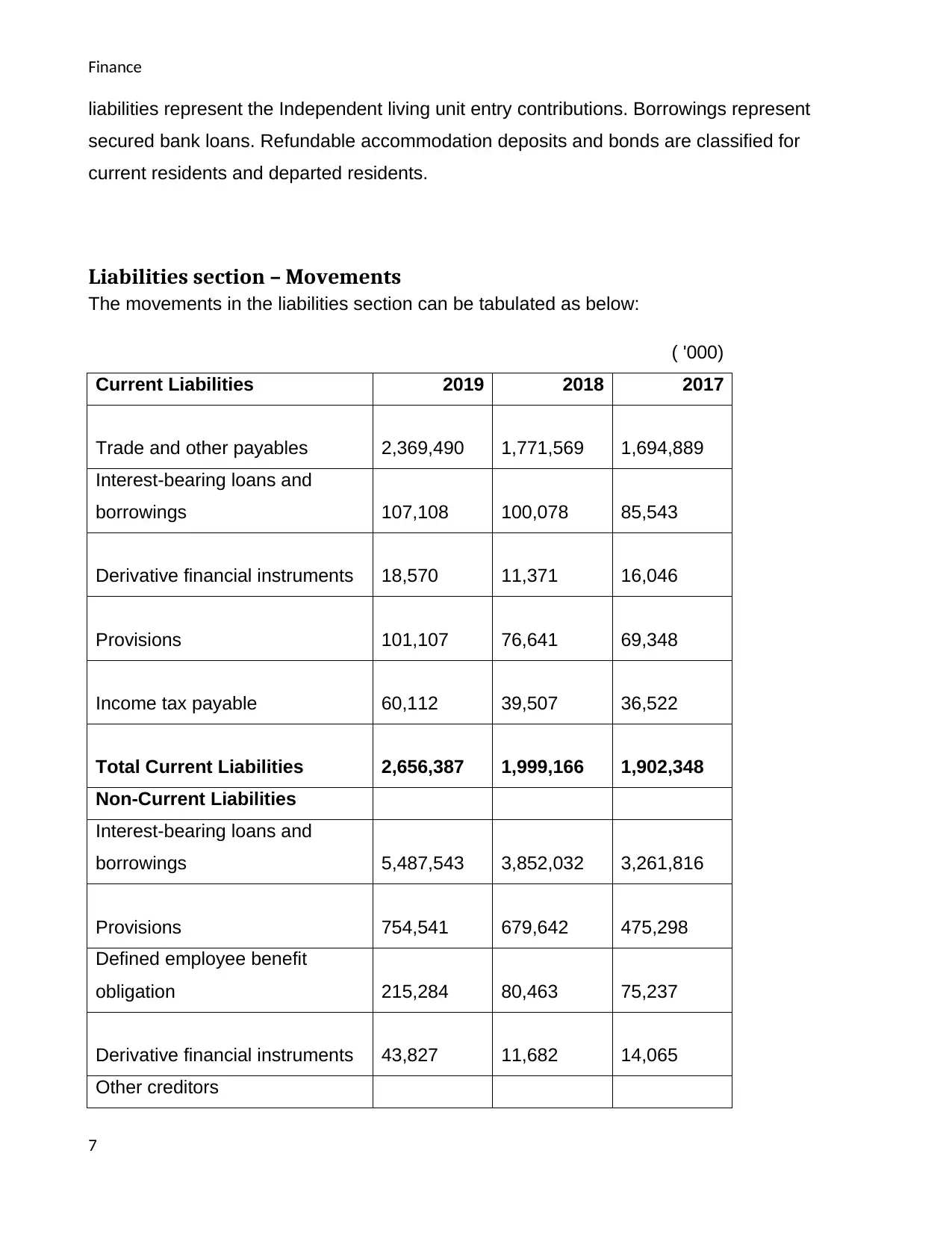

liabilities represent the Independent living unit entry contributions. Borrowings represent

secured bank loans. Refundable accommodation deposits and bonds are classified for

current residents and departed residents.

Liabilities section – Movements

The movements in the liabilities section can be tabulated as below:

( '000)

Current Liabilities 2019 2018 2017

Trade and other payables 2,369,490 1,771,569 1,694,889

Interest-bearing loans and

borrowings 107,108 100,078 85,543

Derivative financial instruments 18,570 11,371 16,046

Provisions 101,107 76,641 69,348

Income tax payable 60,112 39,507 36,522

Total Current Liabilities 2,656,387 1,999,166 1,902,348

Non-Current Liabilities

Interest-bearing loans and

borrowings 5,487,543 3,852,032 3,261,816

Provisions 754,541 679,642 475,298

Defined employee benefit

obligation 215,284 80,463 75,237

Derivative financial instruments 43,827 11,682 14,065

Other creditors

7

liabilities represent the Independent living unit entry contributions. Borrowings represent

secured bank loans. Refundable accommodation deposits and bonds are classified for

current residents and departed residents.

Liabilities section – Movements

The movements in the liabilities section can be tabulated as below:

( '000)

Current Liabilities 2019 2018 2017

Trade and other payables 2,369,490 1,771,569 1,694,889

Interest-bearing loans and

borrowings 107,108 100,078 85,543

Derivative financial instruments 18,570 11,371 16,046

Provisions 101,107 76,641 69,348

Income tax payable 60,112 39,507 36,522

Total Current Liabilities 2,656,387 1,999,166 1,902,348

Non-Current Liabilities

Interest-bearing loans and

borrowings 5,487,543 3,852,032 3,261,816

Provisions 754,541 679,642 475,298

Defined employee benefit

obligation 215,284 80,463 75,237

Derivative financial instruments 43,827 11,682 14,065

Other creditors

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

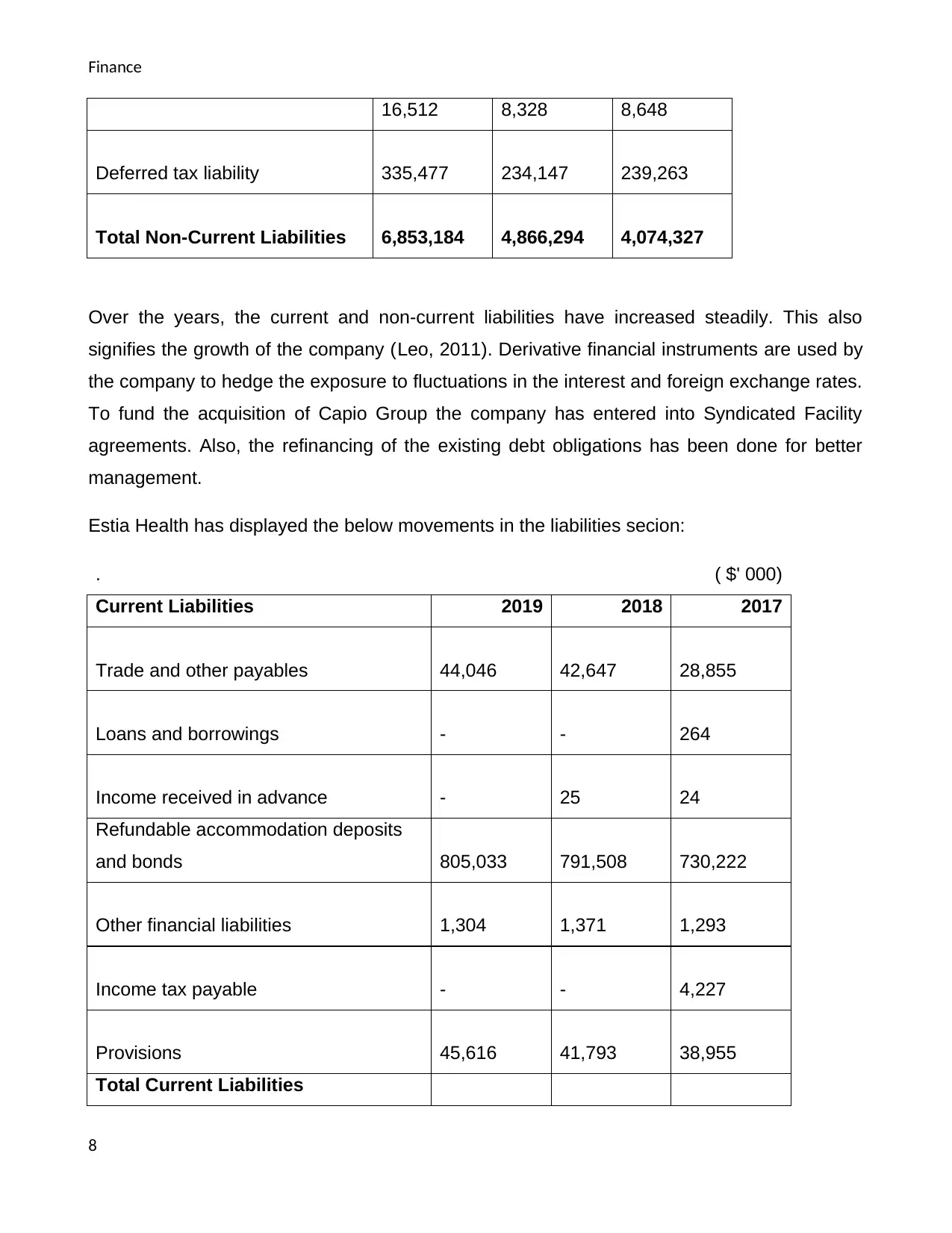

16,512 8,328 8,648

Deferred tax liability 335,477 234,147 239,263

Total Non-Current Liabilities 6,853,184 4,866,294 4,074,327

Over the years, the current and non-current liabilities have increased steadily. This also

signifies the growth of the company (Leo, 2011). Derivative financial instruments are used by

the company to hedge the exposure to fluctuations in the interest and foreign exchange rates.

To fund the acquisition of Capio Group the company has entered into Syndicated Facility

agreements. Also, the refinancing of the existing debt obligations has been done for better

management.

Estia Health has displayed the below movements in the liabilities secion:

. ( $' 000)

Current Liabilities 2019 2018 2017

Trade and other payables 44,046 42,647 28,855

Loans and borrowings - - 264

Income received in advance - 25 24

Refundable accommodation deposits

and bonds 805,033 791,508 730,222

Other financial liabilities 1,304 1,371 1,293

Income tax payable - - 4,227

Provisions 45,616 41,793 38,955

Total Current Liabilities

8

16,512 8,328 8,648

Deferred tax liability 335,477 234,147 239,263

Total Non-Current Liabilities 6,853,184 4,866,294 4,074,327

Over the years, the current and non-current liabilities have increased steadily. This also

signifies the growth of the company (Leo, 2011). Derivative financial instruments are used by

the company to hedge the exposure to fluctuations in the interest and foreign exchange rates.

To fund the acquisition of Capio Group the company has entered into Syndicated Facility

agreements. Also, the refinancing of the existing debt obligations has been done for better

management.

Estia Health has displayed the below movements in the liabilities secion:

. ( $' 000)

Current Liabilities 2019 2018 2017

Trade and other payables 44,046 42,647 28,855

Loans and borrowings - - 264

Income received in advance - 25 24

Refundable accommodation deposits

and bonds 805,033 791,508 730,222

Other financial liabilities 1,304 1,371 1,293

Income tax payable - - 4,227

Provisions 45,616 41,793 38,955

Total Current Liabilities

8

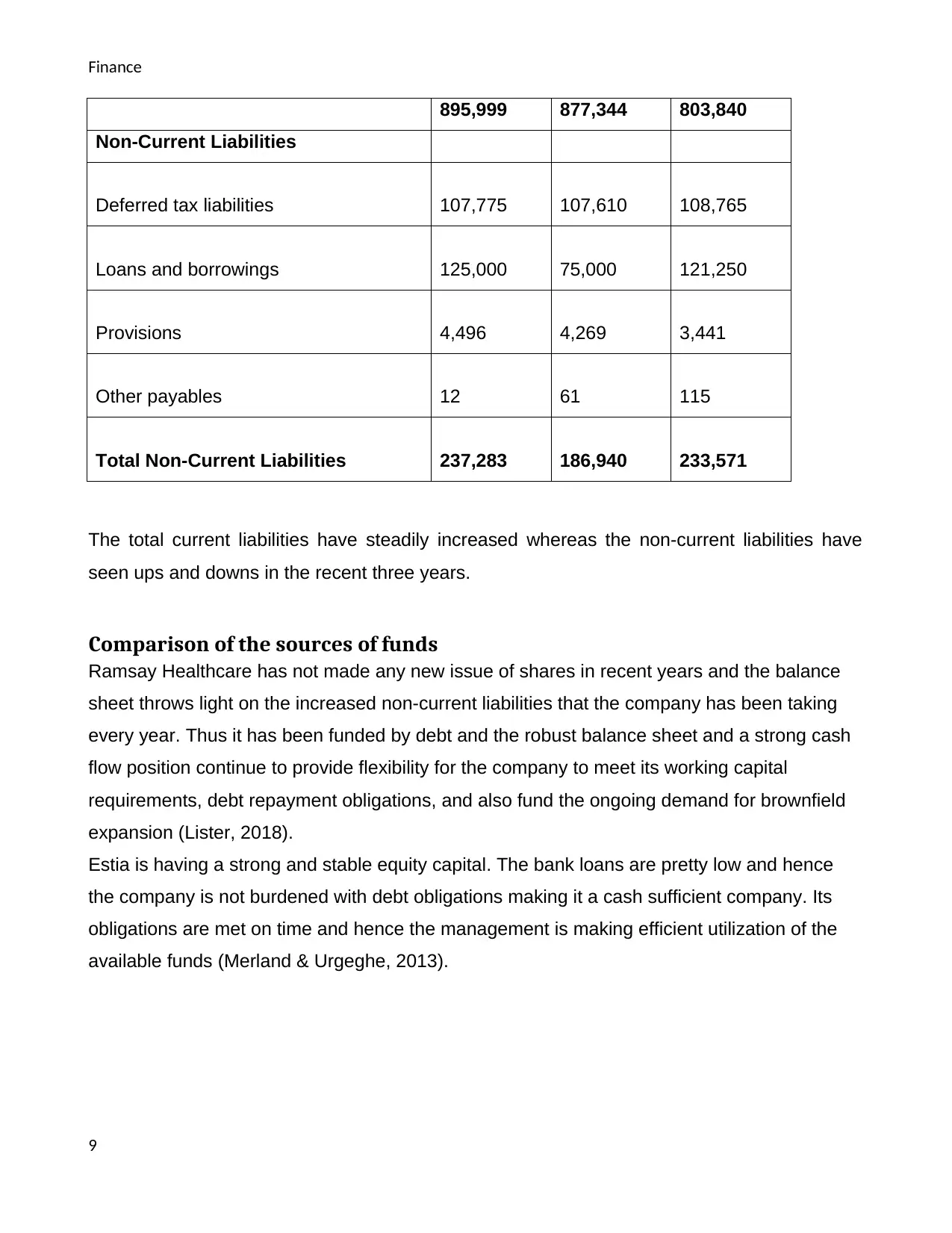

Finance

895,999 877,344 803,840

Non-Current Liabilities

Deferred tax liabilities 107,775 107,610 108,765

Loans and borrowings 125,000 75,000 121,250

Provisions 4,496 4,269 3,441

Other payables 12 61 115

Total Non-Current Liabilities 237,283 186,940 233,571

The total current liabilities have steadily increased whereas the non-current liabilities have

seen ups and downs in the recent three years.

Comparison of the sources of funds

Ramsay Healthcare has not made any new issue of shares in recent years and the balance

sheet throws light on the increased non-current liabilities that the company has been taking

every year. Thus it has been funded by debt and the robust balance sheet and a strong cash

flow position continue to provide flexibility for the company to meet its working capital

requirements, debt repayment obligations, and also fund the ongoing demand for brownfield

expansion (Lister, 2018).

Estia is having a strong and stable equity capital. The bank loans are pretty low and hence

the company is not burdened with debt obligations making it a cash sufficient company. Its

obligations are met on time and hence the management is making efficient utilization of the

available funds (Merland & Urgeghe, 2013).

9

895,999 877,344 803,840

Non-Current Liabilities

Deferred tax liabilities 107,775 107,610 108,765

Loans and borrowings 125,000 75,000 121,250

Provisions 4,496 4,269 3,441

Other payables 12 61 115

Total Non-Current Liabilities 237,283 186,940 233,571

The total current liabilities have steadily increased whereas the non-current liabilities have

seen ups and downs in the recent three years.

Comparison of the sources of funds

Ramsay Healthcare has not made any new issue of shares in recent years and the balance

sheet throws light on the increased non-current liabilities that the company has been taking

every year. Thus it has been funded by debt and the robust balance sheet and a strong cash

flow position continue to provide flexibility for the company to meet its working capital

requirements, debt repayment obligations, and also fund the ongoing demand for brownfield

expansion (Lister, 2018).

Estia is having a strong and stable equity capital. The bank loans are pretty low and hence

the company is not burdened with debt obligations making it a cash sufficient company. Its

obligations are met on time and hence the management is making efficient utilization of the

available funds (Merland & Urgeghe, 2013).

9

Finance

Part B

Proprietary companies

A proprietary company is a private entity that does not offer its shares to the general public.

There are two types of proprietary companies- one which is limited by shares and the other

which is unlimited. The basic requirement of a proprietary company is to have one registered

office. A minimum requirement for the existence of a company is one shareholder which can

be extended up to 50 and such shareholder should not be working as an employee. It is

mandatory to a. Minimum one director but appointing a company secretary is optional for

such companies (PWC, 2019). The shareholders of a limited proprietary company are liable to

the extent of the face value of shares which are owned by them. It is totally opposite in the

case of a proprietary company which is unlimited by share capital. In such a case the

shareholder's liability is unlimited.

Small proprietary

A company has to meet two criteria at least to be considered as a small proprietary- Firstly,

the net value of the asset that is owned by proprietary should not exceed 12.5 million dollars

at the end of a financial year. Secondly, the number of employees appointed in a proprietary

company must not exceed 50 at the end of the financial year. Also, the gross operating profit

earned during the year must not exceed an amount of $25 million (ASIC, 2019).

Large proprietary

A company is considered to be a large proprietary when it satisfies the following criteria.

Firstly, the gross value of the assets which are owned by the proprietary or any other

company that it controls must have a minimum value of $ 25 million at the end of the financial

year. (PWC, 2019) The minimum number of employees that a company should have at the

end of your must be equal to 100. The total consolidated profits for a given financial year

should be at least $50 million.

Reporting entity

10

Part B

Proprietary companies

A proprietary company is a private entity that does not offer its shares to the general public.

There are two types of proprietary companies- one which is limited by shares and the other

which is unlimited. The basic requirement of a proprietary company is to have one registered

office. A minimum requirement for the existence of a company is one shareholder which can

be extended up to 50 and such shareholder should not be working as an employee. It is

mandatory to a. Minimum one director but appointing a company secretary is optional for

such companies (PWC, 2019). The shareholders of a limited proprietary company are liable to

the extent of the face value of shares which are owned by them. It is totally opposite in the

case of a proprietary company which is unlimited by share capital. In such a case the

shareholder's liability is unlimited.

Small proprietary

A company has to meet two criteria at least to be considered as a small proprietary- Firstly,

the net value of the asset that is owned by proprietary should not exceed 12.5 million dollars

at the end of a financial year. Secondly, the number of employees appointed in a proprietary

company must not exceed 50 at the end of the financial year. Also, the gross operating profit

earned during the year must not exceed an amount of $25 million (ASIC, 2019).

Large proprietary

A company is considered to be a large proprietary when it satisfies the following criteria.

Firstly, the gross value of the assets which are owned by the proprietary or any other

company that it controls must have a minimum value of $ 25 million at the end of the financial

year. (PWC, 2019) The minimum number of employees that a company should have at the

end of your must be equal to 100. The total consolidated profits for a given financial year

should be at least $50 million.

Reporting entity

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Finance

All companies that comply with general purpose financial reporting for evaluating a company's

financial position and its performance is known as a reporting entity. These financial

statements that are prepared by a company are used by several stakeholders of the company

which includes shareholders, creditors, debenture holders, potential investors, lenders, etc.

The financial statements that are prepared by the company should be reliable because many

important decisions are taken based on them. A non-reporting entity is the one where users of

these financial statements are not dependent on the general purpose financial report. Such

entities prepare a special purpose financial report (ASIC, 2019).

Implications and compliance of large proprietary

A proprietary limited company is required to comply with the corporation's activities in 2001. It

is very important for these companies to carry out an audit procedure periodically. It is

compulsory for such companies to have at least one director who is an ordinary resident of

Australia. The director should delegate his responsibilities and duties lawfully to others. The

financial statements, as well as the director's report, must be prepared at the end of the

financial year. There are various factors like size and type of a company on which the

disclosure requirement depends. The disclosure requirements are stricter in case of a public

company because they raise funds from the public on the basis of their financial statements.

If a large proprietary company is not exempted then it must submit its financial statements

and directors’ report to the Australian Securities and Investment Commission. A small

proprietary company is not required to submit these statements. The shareholders and the

directors are considered to be the owner of a large proprietary company. The role is

completely different from each other (ASIC, 2013). It is not important for an equity holder to

participate in the workings of an organization and at the same time, it is not important for a

director to have an equity holding in the company. Equity shareholders get dividends out of

the profits as a return whereas the directors of the company receive salary for the services

that they have rendered. The small proprietary companies are just required to record the

financial transactions and lodge this statement to the ATO. It is a basic requirement that such

companies should have proprietary Limited at the end of its name. All the legal documents

should contain the official name of the company which is registered with the ASIC (Mrsland &

Urgeghe, 2013). Also, if there is any nonprofit organization that is revenue exceeds AUS$

11

All companies that comply with general purpose financial reporting for evaluating a company's

financial position and its performance is known as a reporting entity. These financial

statements that are prepared by a company are used by several stakeholders of the company

which includes shareholders, creditors, debenture holders, potential investors, lenders, etc.

The financial statements that are prepared by the company should be reliable because many

important decisions are taken based on them. A non-reporting entity is the one where users of

these financial statements are not dependent on the general purpose financial report. Such

entities prepare a special purpose financial report (ASIC, 2019).

Implications and compliance of large proprietary

A proprietary limited company is required to comply with the corporation's activities in 2001. It

is very important for these companies to carry out an audit procedure periodically. It is

compulsory for such companies to have at least one director who is an ordinary resident of

Australia. The director should delegate his responsibilities and duties lawfully to others. The

financial statements, as well as the director's report, must be prepared at the end of the

financial year. There are various factors like size and type of a company on which the

disclosure requirement depends. The disclosure requirements are stricter in case of a public

company because they raise funds from the public on the basis of their financial statements.

If a large proprietary company is not exempted then it must submit its financial statements

and directors’ report to the Australian Securities and Investment Commission. A small

proprietary company is not required to submit these statements. The shareholders and the

directors are considered to be the owner of a large proprietary company. The role is

completely different from each other (ASIC, 2013). It is not important for an equity holder to

participate in the workings of an organization and at the same time, it is not important for a

director to have an equity holding in the company. Equity shareholders get dividends out of

the profits as a return whereas the directors of the company receive salary for the services

that they have rendered. The small proprietary companies are just required to record the

financial transactions and lodge this statement to the ATO. It is a basic requirement that such

companies should have proprietary Limited at the end of its name. All the legal documents

should contain the official name of the company which is registered with the ASIC (Mrsland &

Urgeghe, 2013). Also, if there is any nonprofit organization that is revenue exceeds AUS$

11

Finance

150000 then, it must register for goods and services tax. The company should make sure that

all the legal and statutory requirements are met timely. According to chapter 6D of the

corporation's act 2001, the PLC's are disallowed to disclose any crucial information to its

investors. A public limited company has to face a greater regulatory burden when compared

to the PLC. This shows that PLC has greater freedom relating to trade and also it faces less

competition in the industry.

12

150000 then, it must register for goods and services tax. The company should make sure that

all the legal and statutory requirements are met timely. According to chapter 6D of the

corporation's act 2001, the PLC's are disallowed to disclose any crucial information to its

investors. A public limited company has to face a greater regulatory burden when compared

to the PLC. This shows that PLC has greater freedom relating to trade and also it faces less

competition in the industry.

12

Finance

Conclusion

Ramsay Healthcare has displayed overall growth in all its areas of operations and hence the

future of the company looks bright with strong liquidity position and market stability. Estia

Health is a company with a strong foundation and a clear strategy for future growth with

specific measures to deliver the same. However, both the companies are operating with a

strong fundamentals and it is a clear indication that both the companies will project strong

results and ensure quality return to the shareholders. The second part of the report indicates

that large proprietary is a good option as it helps the business activities however the business

needs to have a system of a strong compliance.

13

Conclusion

Ramsay Healthcare has displayed overall growth in all its areas of operations and hence the

future of the company looks bright with strong liquidity position and market stability. Estia

Health is a company with a strong foundation and a clear strategy for future growth with

specific measures to deliver the same. However, both the companies are operating with a

strong fundamentals and it is a clear indication that both the companies will project strong

results and ensure quality return to the shareholders. The second part of the report indicates

that large proprietary is a good option as it helps the business activities however the business

needs to have a system of a strong compliance.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

References

ASIC 2019, Using 'Limited', 'No Liability' or 'Proprietary' in a name, viewed 24 September

2019, https://asic.gov.au/about-asic/contact-us/how-to-complain/using-limited-no-liability-or-

proprietary-in-a-name/

Estia health 2018, Estia health 2018 annual report & accounts, viewed 24 September 2019,

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_EHE_2018.pdf

Laux, B 2014, Discussion of The role of revenue recognition in performance reporting.

Accounting and Business Research, vol. 44, no. 4, pp. 380-382, doi:

10.1080/00014788.2014.897867

Leo, K. J 2011, Company Accounting (9th ed), Boston:McGraw Hill

Lister, J 2018, Advantages and Disadvantages of Financial Risks Within Companies, viewed

24 September 2019 <https://smallbusiness.chron.com/advantages-disadvantages-financial-

risks-within-companies-16048.html>

Melville, A 2013, International Financial Reporting – A Practical Guide, Pearson, Education

Limited, UK

Mersland, R., & Urgeghe, L 2013, International Debt Financing and Performance of

Microfinance Institutions, Strategic Change, vol. 22, pp. 36-47

Mersland, R., & Urgeghe, L 2013, International Debt Financing and Performance of

Microfinance Institutions, Strategic Change 22, 36-47

PWC 2019, Doing Business in Australia, viewed 24 September 2019,

https://www.pwc.com.au/legal/assets/legaltalk/doing-business-australia-2016.pdf

Ramsay 2018, Ramsay 2018 annual report & accounts, viewed 24 September 2019,

https://www.ramsayhealth.com/Investors/Annual-and-Financial-Reports/Annual-Report-2018

14

References

ASIC 2019, Using 'Limited', 'No Liability' or 'Proprietary' in a name, viewed 24 September

2019, https://asic.gov.au/about-asic/contact-us/how-to-complain/using-limited-no-liability-or-

proprietary-in-a-name/

Estia health 2018, Estia health 2018 annual report & accounts, viewed 24 September 2019,

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_EHE_2018.pdf

Laux, B 2014, Discussion of The role of revenue recognition in performance reporting.

Accounting and Business Research, vol. 44, no. 4, pp. 380-382, doi:

10.1080/00014788.2014.897867

Leo, K. J 2011, Company Accounting (9th ed), Boston:McGraw Hill

Lister, J 2018, Advantages and Disadvantages of Financial Risks Within Companies, viewed

24 September 2019 <https://smallbusiness.chron.com/advantages-disadvantages-financial-

risks-within-companies-16048.html>

Melville, A 2013, International Financial Reporting – A Practical Guide, Pearson, Education

Limited, UK

Mersland, R., & Urgeghe, L 2013, International Debt Financing and Performance of

Microfinance Institutions, Strategic Change, vol. 22, pp. 36-47

Mersland, R., & Urgeghe, L 2013, International Debt Financing and Performance of

Microfinance Institutions, Strategic Change 22, 36-47

PWC 2019, Doing Business in Australia, viewed 24 September 2019,

https://www.pwc.com.au/legal/assets/legaltalk/doing-business-australia-2016.pdf

Ramsay 2018, Ramsay 2018 annual report & accounts, viewed 24 September 2019,

https://www.ramsayhealth.com/Investors/Annual-and-Financial-Reports/Annual-Report-2018

14

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.