Financial Analysis of Phone Company Project: Investment Appraisal

VerifiedAdded on 2020/06/05

|11

|2341

|424

Report

AI Summary

This report provides a financial analysis of a phone company project, focusing on investment appraisal techniques to evaluate two potential proposals. The analysis includes the computation of the Weighted Average Cost of Capital (WACC), preparation of cash flows, and the application of Net Present Value (NPV) and Internal Rate of Return (IRR) to determine project viability. The report highlights that Project B is more viable due to a higher NPV and IRR. Sensitivity analysis is conducted to assess the impact of changes in sales units, revenue, and raw material costs. The report also discusses the advantages and disadvantages of operating leases, recommending their adoption for Project B. Ultimately, the report concludes that capital budgeting methods are crucial for making sound investment decisions and that sensitivity analysis is vital for risk assessment.

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial planning and evaluation is highly significant which in turn provides high level

of assistance to the manager in making selection of best option out of several alternatives.

Moreover, at the time of availability of several options manager faces difficulty in making

selection of the best project that aid in the growth and success of firm. In this regard, financial

tools and techniques such as investment appraisal provide high level of assistance in evaluating

the viability of proposals. Capital budgeting tools clearly state the return and time period within

which firm will recover its initial investment. For this project report, scenario of Phone company

has been considered which is involved in the activities of manufacturing covers. It can be

summarized from the report that business unit should go with the proposal A which in turn offers

higher return to the company. Moreover, in the case of project B, NPV and IRR accounts for

significantly. It can be seen in the report that WACC is 17% which in turn considered as

discounting factor. Along with this, it can be stated that by developing strategic and competent

framework on the basis of sensitivity analysis business unit can gain competitive edge over

others. FG

Financial planning and evaluation is highly significant which in turn provides high level

of assistance to the manager in making selection of best option out of several alternatives.

Moreover, at the time of availability of several options manager faces difficulty in making

selection of the best project that aid in the growth and success of firm. In this regard, financial

tools and techniques such as investment appraisal provide high level of assistance in evaluating

the viability of proposals. Capital budgeting tools clearly state the return and time period within

which firm will recover its initial investment. For this project report, scenario of Phone company

has been considered which is involved in the activities of manufacturing covers. It can be

summarized from the report that business unit should go with the proposal A which in turn offers

higher return to the company. Moreover, in the case of project B, NPV and IRR accounts for

significantly. It can be seen in the report that WACC is 17% which in turn considered as

discounting factor. Along with this, it can be stated that by developing strategic and competent

framework on the basis of sensitivity analysis business unit can gain competitive edge over

others. FG

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

a. Computation of WACC to determine required rate of return..................................................1

(b) Preparation of cash flows and inclusion or exclusion of items..............................................1

© Viability of alternative.............................................................................................................3

(d) Uneual lives of the project and its impact on recommendation.............................................4

e.Sensitivity analysis....................................................................................................................4

f. Sensitivity analysis of sale unit, revenue and raw material cost..............................................5

(g) Advantage and disadvantage of lease....................................................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

Table 1Calcualtion of NPV.............................................................................................................3

Table 2Calculation of IRR...............................................................................................................3

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

a. Computation of WACC to determine required rate of return..................................................1

(b) Preparation of cash flows and inclusion or exclusion of items..............................................1

© Viability of alternative.............................................................................................................3

(d) Uneual lives of the project and its impact on recommendation.............................................4

e.Sensitivity analysis....................................................................................................................4

f. Sensitivity analysis of sale unit, revenue and raw material cost..............................................5

(g) Advantage and disadvantage of lease....................................................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

Table 1Calcualtion of NPV.............................................................................................................3

Table 2Calculation of IRR...............................................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

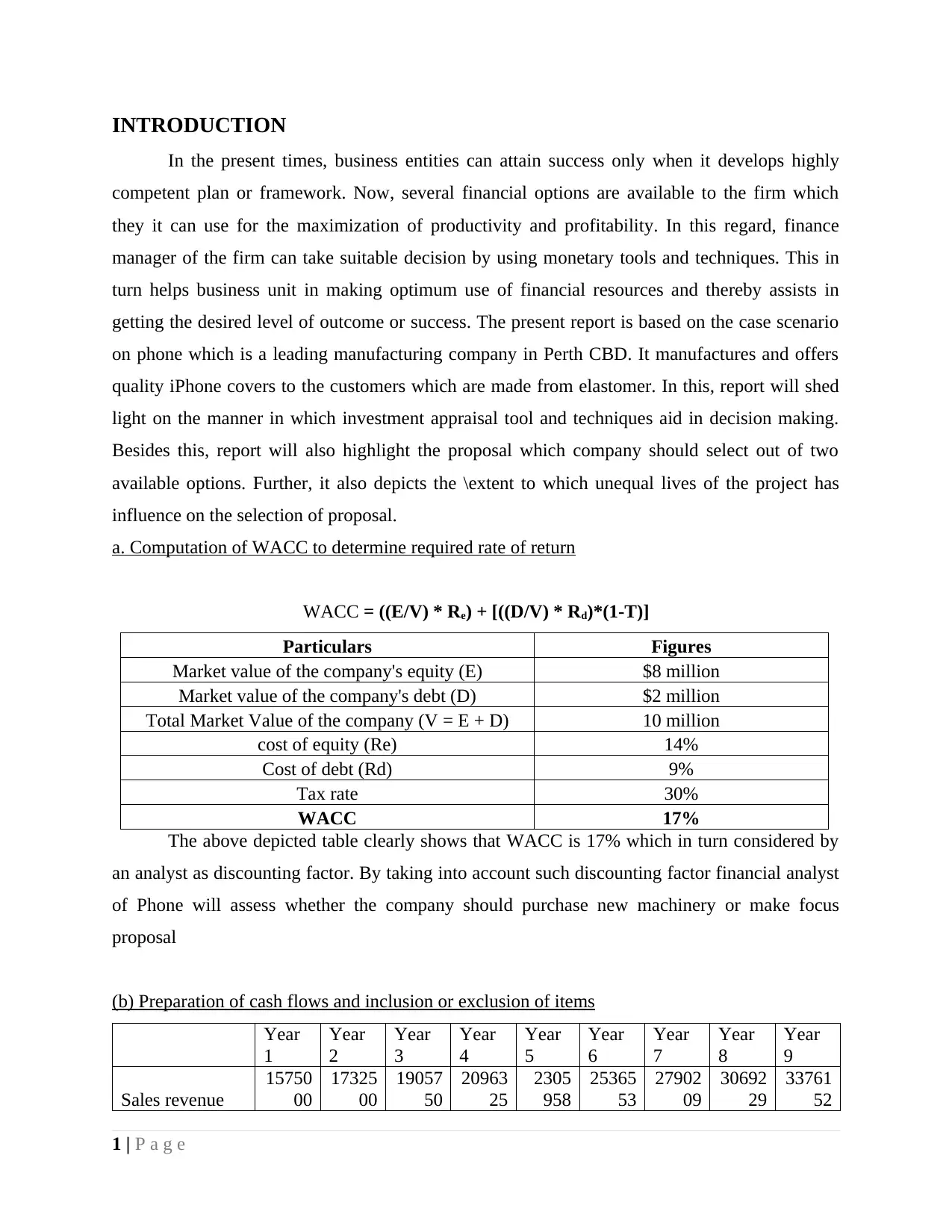

INTRODUCTION

In the present times, business entities can attain success only when it develops highly

competent plan or framework. Now, several financial options are available to the firm which

they it can use for the maximization of productivity and profitability. In this regard, finance

manager of the firm can take suitable decision by using monetary tools and techniques. This in

turn helps business unit in making optimum use of financial resources and thereby assists in

getting the desired level of outcome or success. The present report is based on the case scenario

on phone which is a leading manufacturing company in Perth CBD. It manufactures and offers

quality iPhone covers to the customers which are made from elastomer. In this, report will shed

light on the manner in which investment appraisal tool and techniques aid in decision making.

Besides this, report will also highlight the proposal which company should select out of two

available options. Further, it also depicts the \extent to which unequal lives of the project has

influence on the selection of proposal.

a. Computation of WACC to determine required rate of return

WACC = ((E/V) * Re) + [((D/V) * Rd)*(1-T)]

Particulars Figures

Market value of the company's equity (E) $8 million

Market value of the company's debt (D) $2 million

Total Market Value of the company (V = E + D) 10 million

cost of equity (Re) 14%

Cost of debt (Rd) 9%

Tax rate 30%

WACC 17%

The above depicted table clearly shows that WACC is 17% which in turn considered by

an analyst as discounting factor. By taking into account such discounting factor financial analyst

of Phone will assess whether the company should purchase new machinery or make focus

proposal

(b) Preparation of cash flows and inclusion or exclusion of items

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Sales revenue

15750

00

17325

00

19057

50

20963

25

2305

958

25365

53

27902

09

30692

29

33761

52

1 | P a g e

In the present times, business entities can attain success only when it develops highly

competent plan or framework. Now, several financial options are available to the firm which

they it can use for the maximization of productivity and profitability. In this regard, finance

manager of the firm can take suitable decision by using monetary tools and techniques. This in

turn helps business unit in making optimum use of financial resources and thereby assists in

getting the desired level of outcome or success. The present report is based on the case scenario

on phone which is a leading manufacturing company in Perth CBD. It manufactures and offers

quality iPhone covers to the customers which are made from elastomer. In this, report will shed

light on the manner in which investment appraisal tool and techniques aid in decision making.

Besides this, report will also highlight the proposal which company should select out of two

available options. Further, it also depicts the \extent to which unequal lives of the project has

influence on the selection of proposal.

a. Computation of WACC to determine required rate of return

WACC = ((E/V) * Re) + [((D/V) * Rd)*(1-T)]

Particulars Figures

Market value of the company's equity (E) $8 million

Market value of the company's debt (D) $2 million

Total Market Value of the company (V = E + D) 10 million

cost of equity (Re) 14%

Cost of debt (Rd) 9%

Tax rate 30%

WACC 17%

The above depicted table clearly shows that WACC is 17% which in turn considered by

an analyst as discounting factor. By taking into account such discounting factor financial analyst

of Phone will assess whether the company should purchase new machinery or make focus

proposal

(b) Preparation of cash flows and inclusion or exclusion of items

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Sales revenue

15750

00

17325

00

19057

50

20963

25

2305

958

25365

53

27902

09

30692

29

33761

52

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

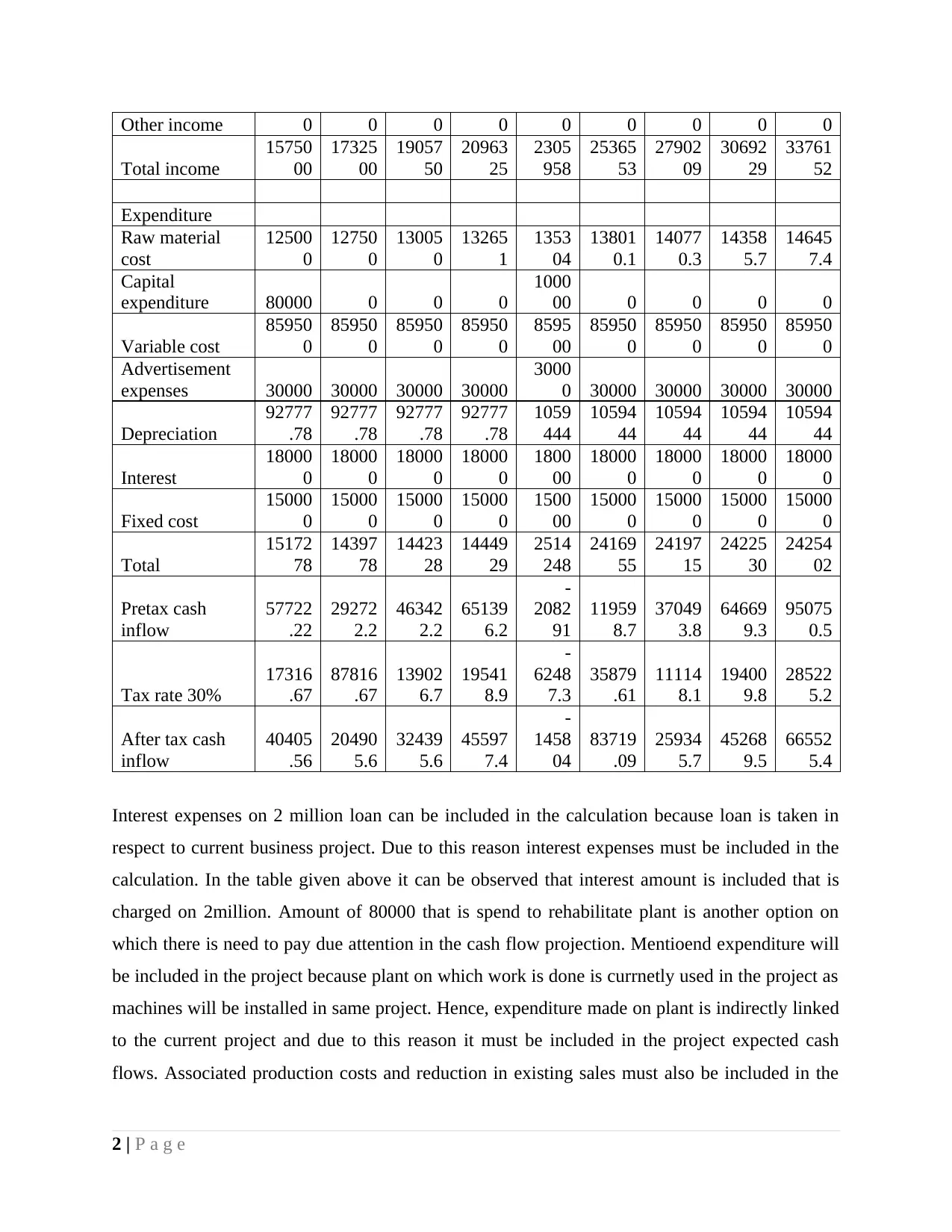

Other income 0 0 0 0 0 0 0 0 0

Total income

15750

00

17325

00

19057

50

20963

25

2305

958

25365

53

27902

09

30692

29

33761

52

Expenditure

Raw material

cost

12500

0

12750

0

13005

0

13265

1

1353

04

13801

0.1

14077

0.3

14358

5.7

14645

7.4

Capital

expenditure 80000 0 0 0

1000

00 0 0 0 0

Variable cost

85950

0

85950

0

85950

0

85950

0

8595

00

85950

0

85950

0

85950

0

85950

0

Advertisement

expenses 30000 30000 30000 30000

3000

0 30000 30000 30000 30000

Depreciation

92777

.78

92777

.78

92777

.78

92777

.78

1059

444

10594

44

10594

44

10594

44

10594

44

Interest

18000

0

18000

0

18000

0

18000

0

1800

00

18000

0

18000

0

18000

0

18000

0

Fixed cost

15000

0

15000

0

15000

0

15000

0

1500

00

15000

0

15000

0

15000

0

15000

0

Total

15172

78

14397

78

14423

28

14449

29

2514

248

24169

55

24197

15

24225

30

24254

02

Pretax cash

inflow

57722

.22

29272

2.2

46342

2.2

65139

6.2

-

2082

91

11959

8.7

37049

3.8

64669

9.3

95075

0.5

Tax rate 30%

17316

.67

87816

.67

13902

6.7

19541

8.9

-

6248

7.3

35879

.61

11114

8.1

19400

9.8

28522

5.2

After tax cash

inflow

40405

.56

20490

5.6

32439

5.6

45597

7.4

-

1458

04

83719

.09

25934

5.7

45268

9.5

66552

5.4

Interest expenses on 2 million loan can be included in the calculation because loan is taken in

respect to current business project. Due to this reason interest expenses must be included in the

calculation. In the table given above it can be observed that interest amount is included that is

charged on 2million. Amount of 80000 that is spend to rehabilitate plant is another option on

which there is need to pay due attention in the cash flow projection. Mentioend expenditure will

be included in the project because plant on which work is done is currnetly used in the project as

machines will be installed in same project. Hence, expenditure made on plant is indirectly linked

to the current project and due to this reason it must be included in the project expected cash

flows. Associated production costs and reduction in existing sales must also be included in the

2 | P a g e

Total income

15750

00

17325

00

19057

50

20963

25

2305

958

25365

53

27902

09

30692

29

33761

52

Expenditure

Raw material

cost

12500

0

12750

0

13005

0

13265

1

1353

04

13801

0.1

14077

0.3

14358

5.7

14645

7.4

Capital

expenditure 80000 0 0 0

1000

00 0 0 0 0

Variable cost

85950

0

85950

0

85950

0

85950

0

8595

00

85950

0

85950

0

85950

0

85950

0

Advertisement

expenses 30000 30000 30000 30000

3000

0 30000 30000 30000 30000

Depreciation

92777

.78

92777

.78

92777

.78

92777

.78

1059

444

10594

44

10594

44

10594

44

10594

44

Interest

18000

0

18000

0

18000

0

18000

0

1800

00

18000

0

18000

0

18000

0

18000

0

Fixed cost

15000

0

15000

0

15000

0

15000

0

1500

00

15000

0

15000

0

15000

0

15000

0

Total

15172

78

14397

78

14423

28

14449

29

2514

248

24169

55

24197

15

24225

30

24254

02

Pretax cash

inflow

57722

.22

29272

2.2

46342

2.2

65139

6.2

-

2082

91

11959

8.7

37049

3.8

64669

9.3

95075

0.5

Tax rate 30%

17316

.67

87816

.67

13902

6.7

19541

8.9

-

6248

7.3

35879

.61

11114

8.1

19400

9.8

28522

5.2

After tax cash

inflow

40405

.56

20490

5.6

32439

5.6

45597

7.4

-

1458

04

83719

.09

25934

5.7

45268

9.5

66552

5.4

Interest expenses on 2 million loan can be included in the calculation because loan is taken in

respect to current business project. Due to this reason interest expenses must be included in the

calculation. In the table given above it can be observed that interest amount is included that is

charged on 2million. Amount of 80000 that is spend to rehabilitate plant is another option on

which there is need to pay due attention in the cash flow projection. Mentioend expenditure will

be included in the project because plant on which work is done is currnetly used in the project as

machines will be installed in same project. Hence, expenditure made on plant is indirectly linked

to the current project and due to this reason it must be included in the project expected cash

flows. Associated production costs and reduction in existing sales must also be included in the

2 | P a g e

project. This is because production will be done by using machine and due to this reason in this

way production cost is associated with the current project cash inflows.

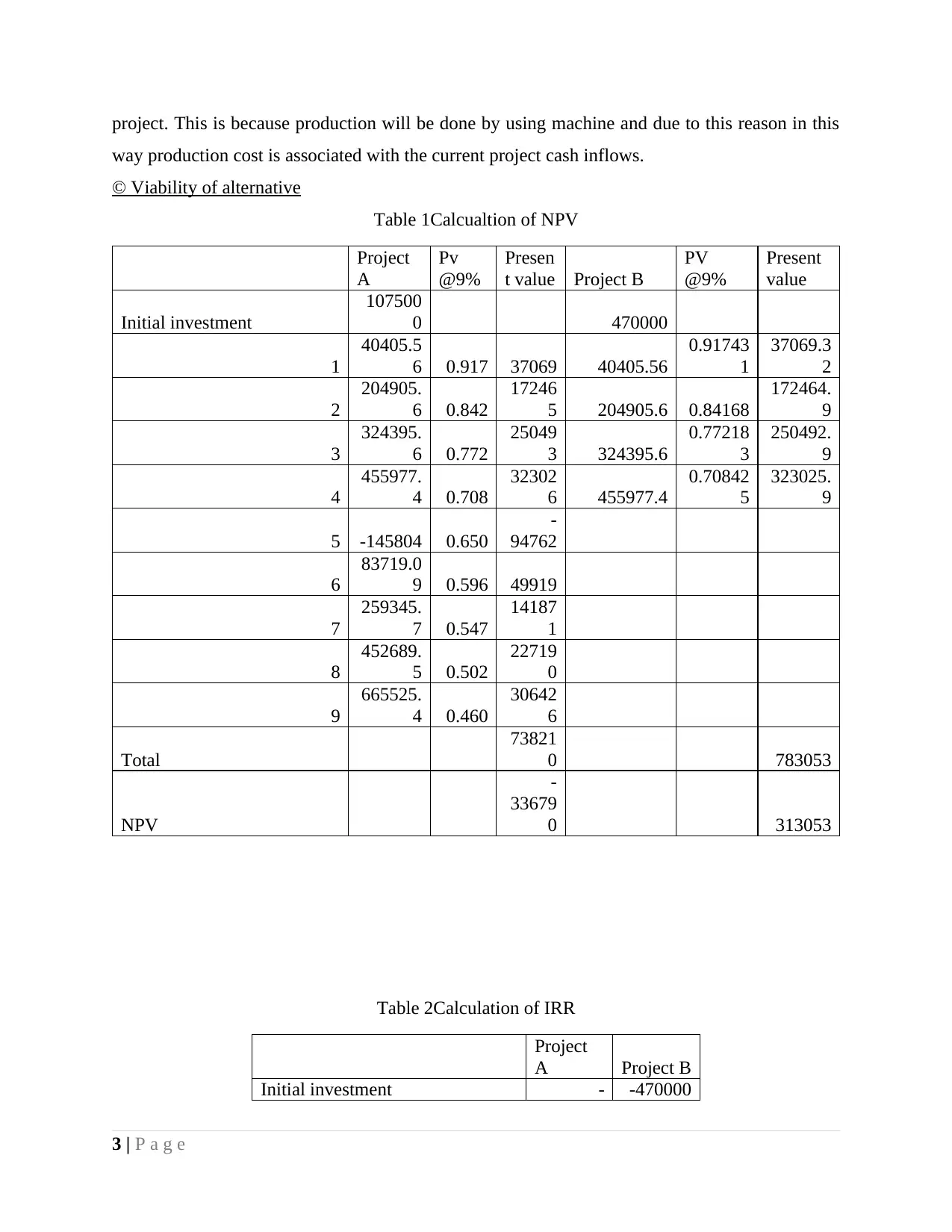

© Viability of alternative

Table 1Calcualtion of NPV

Project

A

Pv

@9%

Presen

t value Project B

PV

@9%

Present

value

Initial investment

107500

0 470000

1

40405.5

6 0.917 37069 40405.56

0.91743

1

37069.3

2

2

204905.

6 0.842

17246

5 204905.6 0.84168

172464.

9

3

324395.

6 0.772

25049

3 324395.6

0.77218

3

250492.

9

4

455977.

4 0.708

32302

6 455977.4

0.70842

5

323025.

9

5 -145804 0.650

-

94762

6

83719.0

9 0.596 49919

7

259345.

7 0.547

14187

1

8

452689.

5 0.502

22719

0

9

665525.

4 0.460

30642

6

Total

73821

0 783053

NPV

-

33679

0 313053

Table 2Calculation of IRR

Project

A Project B

Initial investment - -470000

3 | P a g e

way production cost is associated with the current project cash inflows.

© Viability of alternative

Table 1Calcualtion of NPV

Project

A

Pv

@9%

Presen

t value Project B

PV

@9%

Present

value

Initial investment

107500

0 470000

1

40405.5

6 0.917 37069 40405.56

0.91743

1

37069.3

2

2

204905.

6 0.842

17246

5 204905.6 0.84168

172464.

9

3

324395.

6 0.772

25049

3 324395.6

0.77218

3

250492.

9

4

455977.

4 0.708

32302

6 455977.4

0.70842

5

323025.

9

5 -145804 0.650

-

94762

6

83719.0

9 0.596 49919

7

259345.

7 0.547

14187

1

8

452689.

5 0.502

22719

0

9

665525.

4 0.460

30642

6

Total

73821

0 783053

NPV

-

33679

0 313053

Table 2Calculation of IRR

Project

A Project B

Initial investment - -470000

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

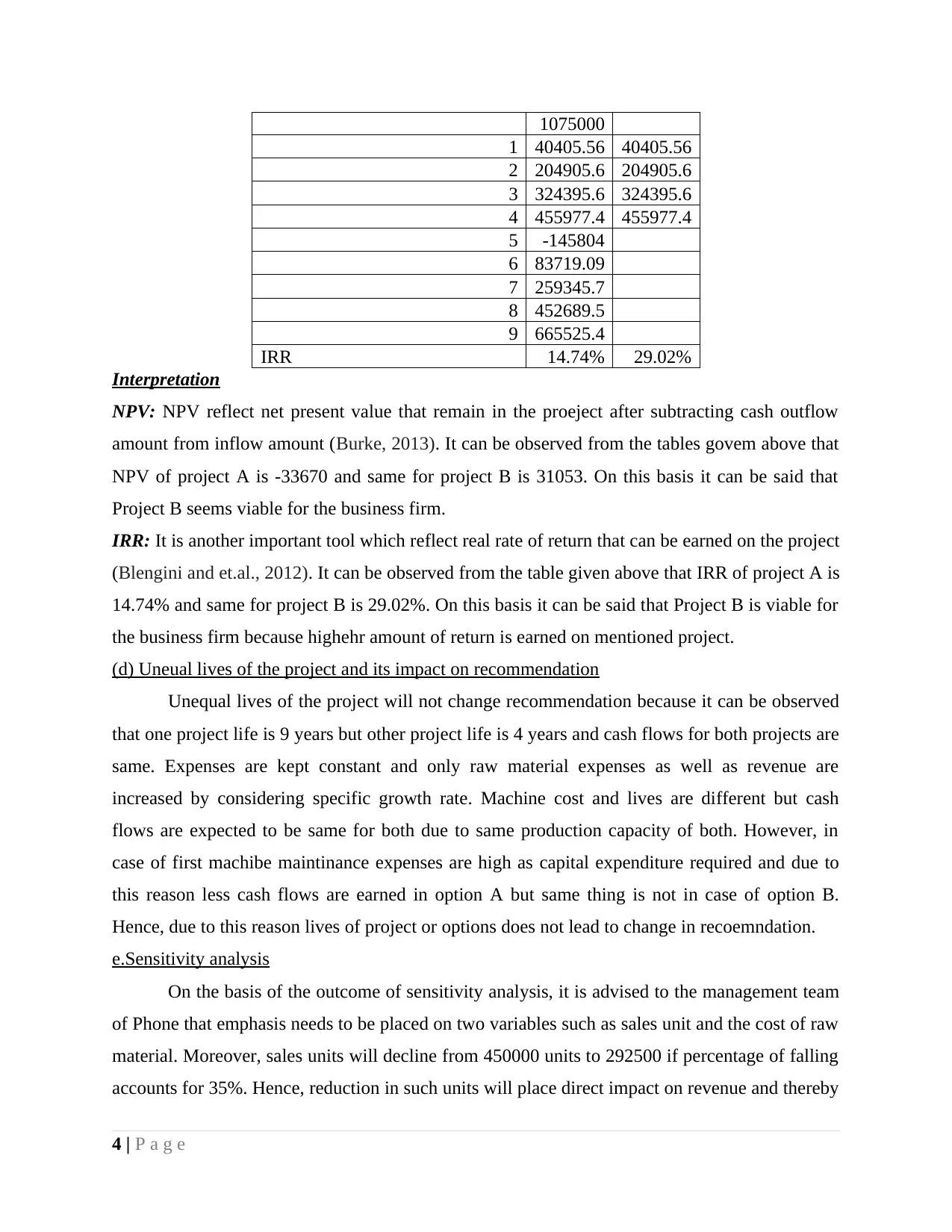

1075000

1 40405.56 40405.56

2 204905.6 204905.6

3 324395.6 324395.6

4 455977.4 455977.4

5 -145804

6 83719.09

7 259345.7

8 452689.5

9 665525.4

IRR 14.74% 29.02%

Interpretation

NPV: NPV reflect net present value that remain in the proeject after subtracting cash outflow

amount from inflow amount (Burke, 2013). It can be observed from the tables govem above that

NPV of project A is -33670 and same for project B is 31053. On this basis it can be said that

Project B seems viable for the business firm.

IRR: It is another important tool which reflect real rate of return that can be earned on the project

(Blengini and et.al., 2012). It can be observed from the table given above that IRR of project A is

14.74% and same for project B is 29.02%. On this basis it can be said that Project B is viable for

the business firm because highehr amount of return is earned on mentioned project.

(d) Uneual lives of the project and its impact on recommendation

Unequal lives of the project will not change recommendation because it can be observed

that one project life is 9 years but other project life is 4 years and cash flows for both projects are

same. Expenses are kept constant and only raw material expenses as well as revenue are

increased by considering specific growth rate. Machine cost and lives are different but cash

flows are expected to be same for both due to same production capacity of both. However, in

case of first machibe maintinance expenses are high as capital expenditure required and due to

this reason less cash flows are earned in option A but same thing is not in case of option B.

Hence, due to this reason lives of project or options does not lead to change in recoemndation.

e.Sensitivity analysis

On the basis of the outcome of sensitivity analysis, it is advised to the management team

of Phone that emphasis needs to be placed on two variables such as sales unit and the cost of raw

material. Moreover, sales units will decline from 450000 units to 292500 if percentage of falling

accounts for 35%. Hence, reduction in such units will place direct impact on revenue and thereby

4 | P a g e

1 40405.56 40405.56

2 204905.6 204905.6

3 324395.6 324395.6

4 455977.4 455977.4

5 -145804

6 83719.09

7 259345.7

8 452689.5

9 665525.4

IRR 14.74% 29.02%

Interpretation

NPV: NPV reflect net present value that remain in the proeject after subtracting cash outflow

amount from inflow amount (Burke, 2013). It can be observed from the tables govem above that

NPV of project A is -33670 and same for project B is 31053. On this basis it can be said that

Project B seems viable for the business firm.

IRR: It is another important tool which reflect real rate of return that can be earned on the project

(Blengini and et.al., 2012). It can be observed from the table given above that IRR of project A is

14.74% and same for project B is 29.02%. On this basis it can be said that Project B is viable for

the business firm because highehr amount of return is earned on mentioned project.

(d) Uneual lives of the project and its impact on recommendation

Unequal lives of the project will not change recommendation because it can be observed

that one project life is 9 years but other project life is 4 years and cash flows for both projects are

same. Expenses are kept constant and only raw material expenses as well as revenue are

increased by considering specific growth rate. Machine cost and lives are different but cash

flows are expected to be same for both due to same production capacity of both. However, in

case of first machibe maintinance expenses are high as capital expenditure required and due to

this reason less cash flows are earned in option A but same thing is not in case of option B.

Hence, due to this reason lives of project or options does not lead to change in recoemndation.

e.Sensitivity analysis

On the basis of the outcome of sensitivity analysis, it is advised to the management team

of Phone that emphasis needs to be placed on two variables such as sales unit and the cost of raw

material. Moreover, sales units will decline from 450000 units to 292500 if percentage of falling

accounts for 35%. Hence, reduction in such units will place direct impact on revenue and thereby

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit margin of firm. Along with this, business unit is required to exert control on material cost

by assessing the best supplier. Besides this, by undertaking the technique of budgetary control

business entity of mobile manufacturing company can control the level of expenses and thereby

would become able to generate high profit (Tsai and et.al., 2011).

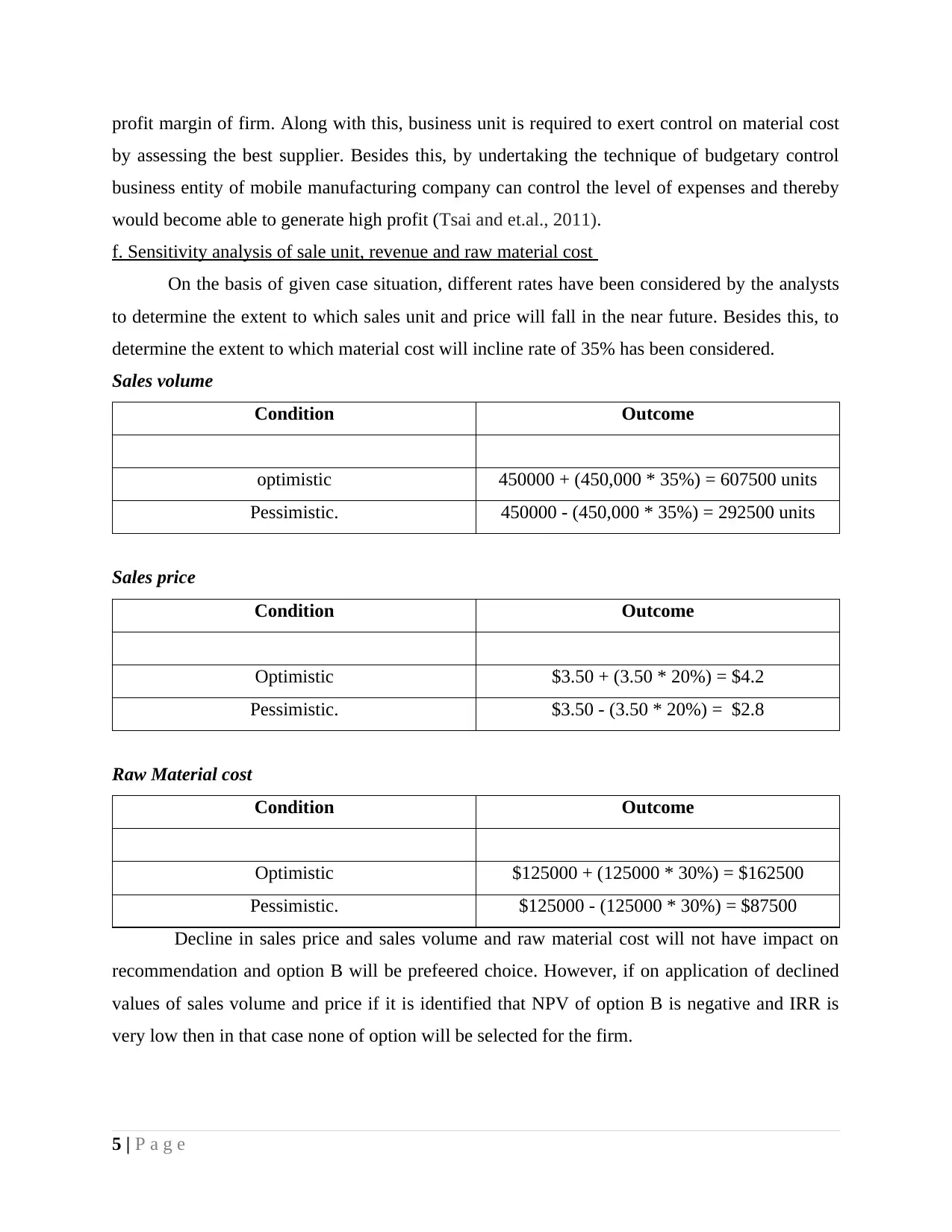

f. Sensitivity analysis of sale unit, revenue and raw material cost

On the basis of given case situation, different rates have been considered by the analysts

to determine the extent to which sales unit and price will fall in the near future. Besides this, to

determine the extent to which material cost will incline rate of 35% has been considered.

Sales volume

Condition Outcome

optimistic 450000 + (450,000 * 35%) = 607500 units

Pessimistic. 450000 - (450,000 * 35%) = 292500 units

Sales price

Condition Outcome

Optimistic $3.50 + (3.50 * 20%) = $4.2

Pessimistic. $3.50 - (3.50 * 20%) = $2.8

Raw Material cost

Condition Outcome

Optimistic $125000 + (125000 * 30%) = $162500

Pessimistic. $125000 - (125000 * 30%) = $87500

Decline in sales price and sales volume and raw material cost will not have impact on

recommendation and option B will be prefeered choice. However, if on application of declined

values of sales volume and price if it is identified that NPV of option B is negative and IRR is

very low then in that case none of option will be selected for the firm.

5 | P a g e

by assessing the best supplier. Besides this, by undertaking the technique of budgetary control

business entity of mobile manufacturing company can control the level of expenses and thereby

would become able to generate high profit (Tsai and et.al., 2011).

f. Sensitivity analysis of sale unit, revenue and raw material cost

On the basis of given case situation, different rates have been considered by the analysts

to determine the extent to which sales unit and price will fall in the near future. Besides this, to

determine the extent to which material cost will incline rate of 35% has been considered.

Sales volume

Condition Outcome

optimistic 450000 + (450,000 * 35%) = 607500 units

Pessimistic. 450000 - (450,000 * 35%) = 292500 units

Sales price

Condition Outcome

Optimistic $3.50 + (3.50 * 20%) = $4.2

Pessimistic. $3.50 - (3.50 * 20%) = $2.8

Raw Material cost

Condition Outcome

Optimistic $125000 + (125000 * 30%) = $162500

Pessimistic. $125000 - (125000 * 30%) = $87500

Decline in sales price and sales volume and raw material cost will not have impact on

recommendation and option B will be prefeered choice. However, if on application of declined

values of sales volume and price if it is identified that NPV of option B is negative and IRR is

very low then in that case none of option will be selected for the firm.

5 | P a g e

(g) Advantage and disadvantage of lease

From assessment, it has been identified that in the case of option B, phone manufacturing

company should lay emphasis on adopting the system of operating lease. On the basis of such

aspect or lease arrangement, firm would become able to use an asset by making payment of rent.

However, such lease does not convey the right of ownership pertaining to asset. Such lease

arrangement has following advantages and drawbacks which business unit needs to keep in mind

while taking decision in relation to the same:

Advantages of operating lease

Operating lease arrangement is highly effectual which in turn provides high level of

assistance in reducing the level of business risk to a great extent. Hence, by undertaking

such lease for short-term Phone company would become able to get monetary benefits.

Moreover, in the case of operating lease, responsibility pertaining to maintenance will be

carried out by lessor.

Further, in operating lease, business entity will not carry the risk in relation to decline in

the value of assets due to damages

(The pros and cons of an operating lease, 2017).

Disadvantages of operating lease

In this, business entity is accountable in relation to making use of assets as per the terms

and conditions mentioned in the contract.

Under operating lease, lessee would not become able to take benefits in relation to the

increase in value of assets etc.

Hence, such lease arrangement will not place high level of emphasis on WACC because

operating lease arrangement is considered as off-balance sheet transaction. However, rent on

assets will reduce the level of expenses and thereby enhances cash flow significantly.

CONCLUSION

On the basis of above discussion it is concluded that there is significent importance of

capital budgeting methods because by using same best option can be selected by the firm.

However, there are number of factors that need to be consider while estimating cash flows of

project. Sensitivity analysis must also be conducted while making any decision because by using

6 | P a g e

From assessment, it has been identified that in the case of option B, phone manufacturing

company should lay emphasis on adopting the system of operating lease. On the basis of such

aspect or lease arrangement, firm would become able to use an asset by making payment of rent.

However, such lease does not convey the right of ownership pertaining to asset. Such lease

arrangement has following advantages and drawbacks which business unit needs to keep in mind

while taking decision in relation to the same:

Advantages of operating lease

Operating lease arrangement is highly effectual which in turn provides high level of

assistance in reducing the level of business risk to a great extent. Hence, by undertaking

such lease for short-term Phone company would become able to get monetary benefits.

Moreover, in the case of operating lease, responsibility pertaining to maintenance will be

carried out by lessor.

Further, in operating lease, business entity will not carry the risk in relation to decline in

the value of assets due to damages

(The pros and cons of an operating lease, 2017).

Disadvantages of operating lease

In this, business entity is accountable in relation to making use of assets as per the terms

and conditions mentioned in the contract.

Under operating lease, lessee would not become able to take benefits in relation to the

increase in value of assets etc.

Hence, such lease arrangement will not place high level of emphasis on WACC because

operating lease arrangement is considered as off-balance sheet transaction. However, rent on

assets will reduce the level of expenses and thereby enhances cash flow significantly.

CONCLUSION

On the basis of above discussion it is concluded that there is significent importance of

capital budgeting methods because by using same best option can be selected by the firm.

However, there are number of factors that need to be consider while estimating cash flows of

project. Sensitivity analysis must also be conducted while making any decision because by using

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

same it can be identified that in case if any unfortunate event takes place then whether project

will be viable or firm will need to stop work on project in middle.

7 | P a g e

will be viable or firm will need to stop work on project in middle.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Burke, R., 2013. Project management: planning and control techniques. New Jersey. USA.

Blengini, G.A. and et.al., 2012. Life Cycle Assessment guidelines for the sustainable production

and recycling of aggregates: the Sustainable Aggregates Resource Management project

(SARMa). Journal of Cleaner Production. 27. pp.177-181.

Tsai, W.H. and et.al., 2011. Incorporating life cycle assessments into building project decision-

making: an energy consumption and CO 2 emission perspective. Energy. 36(5). pp.3022-

3029.

Online

The pros and cons of an operating lease. 2017. [Online]. Available through: <

http://fspbusiness.co.za/articles/accounting/revealed-the-pros-and-cons-of-a-finance-lease-

and-an-operating-lease-2753.html>. [Accessed on 3rd November 2017].

8 | P a g e

Books and Journals

Burke, R., 2013. Project management: planning and control techniques. New Jersey. USA.

Blengini, G.A. and et.al., 2012. Life Cycle Assessment guidelines for the sustainable production

and recycling of aggregates: the Sustainable Aggregates Resource Management project

(SARMa). Journal of Cleaner Production. 27. pp.177-181.

Tsai, W.H. and et.al., 2011. Incorporating life cycle assessments into building project decision-

making: an energy consumption and CO 2 emission perspective. Energy. 36(5). pp.3022-

3029.

Online

The pros and cons of an operating lease. 2017. [Online]. Available through: <

http://fspbusiness.co.za/articles/accounting/revealed-the-pros-and-cons-of-a-finance-lease-

and-an-operating-lease-2753.html>. [Accessed on 3rd November 2017].

8 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.