University Finance Case Study: Discounted Cash Flow Valuation

VerifiedAdded on 2022/11/18

|11

|1205

|343

Case Study

AI Summary

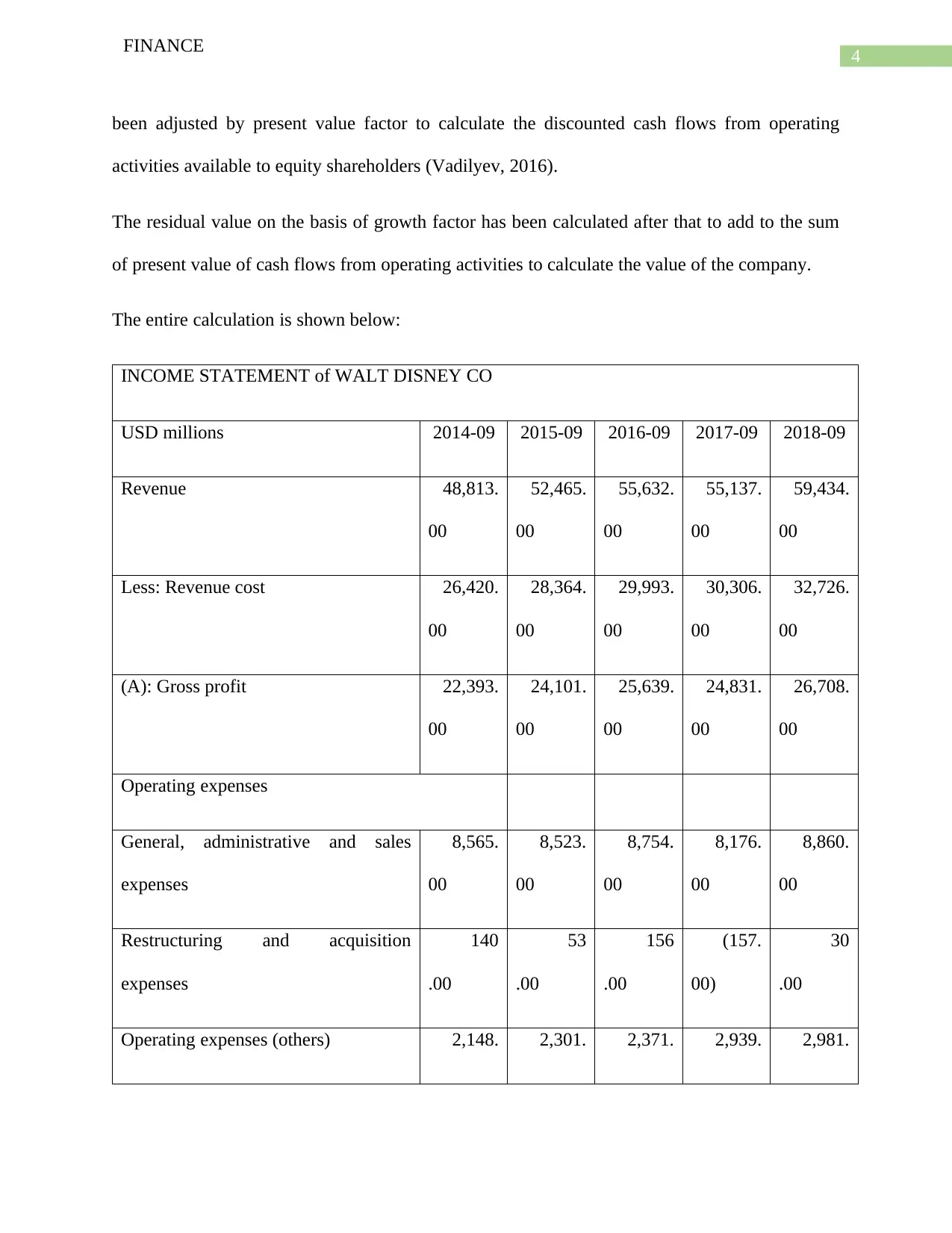

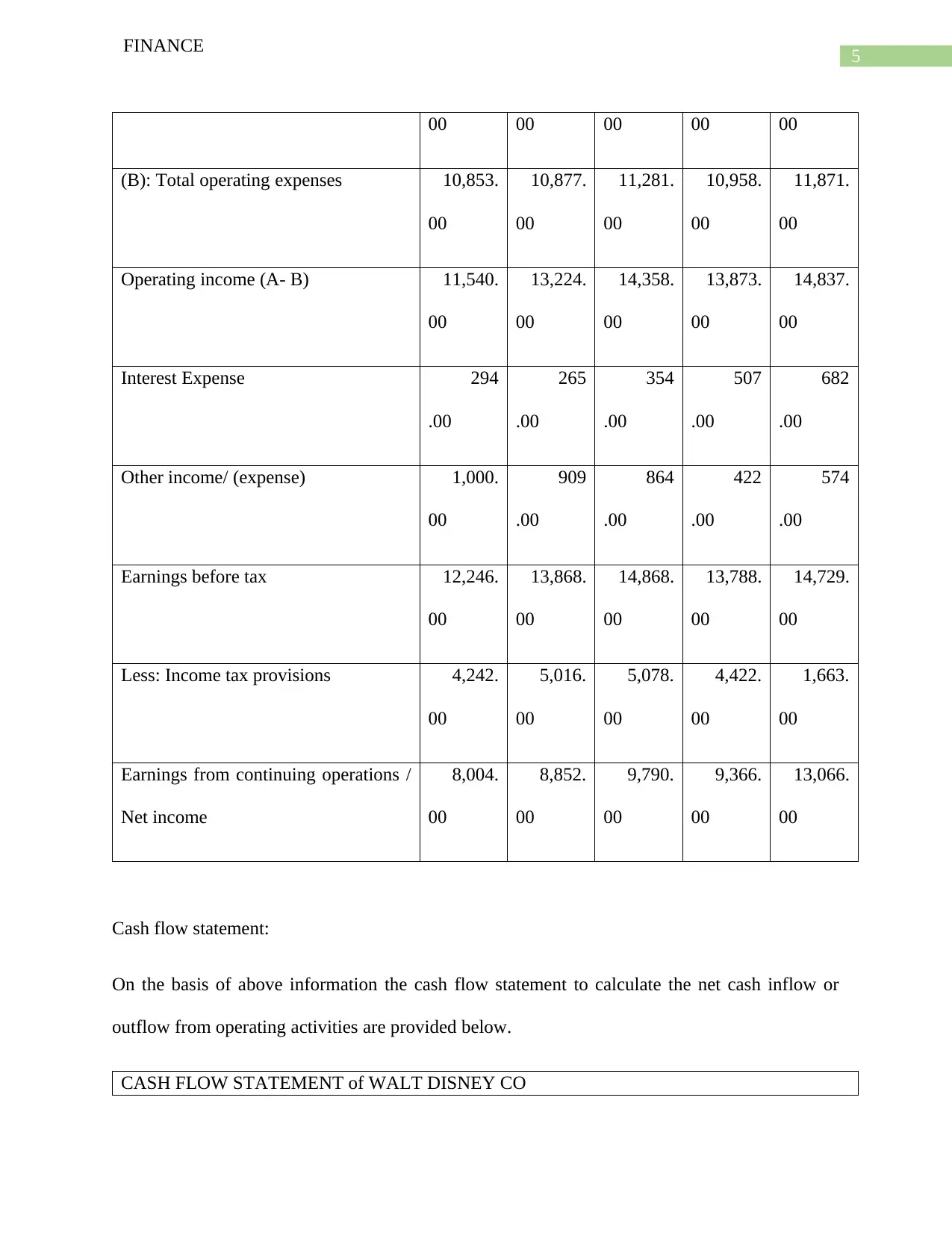

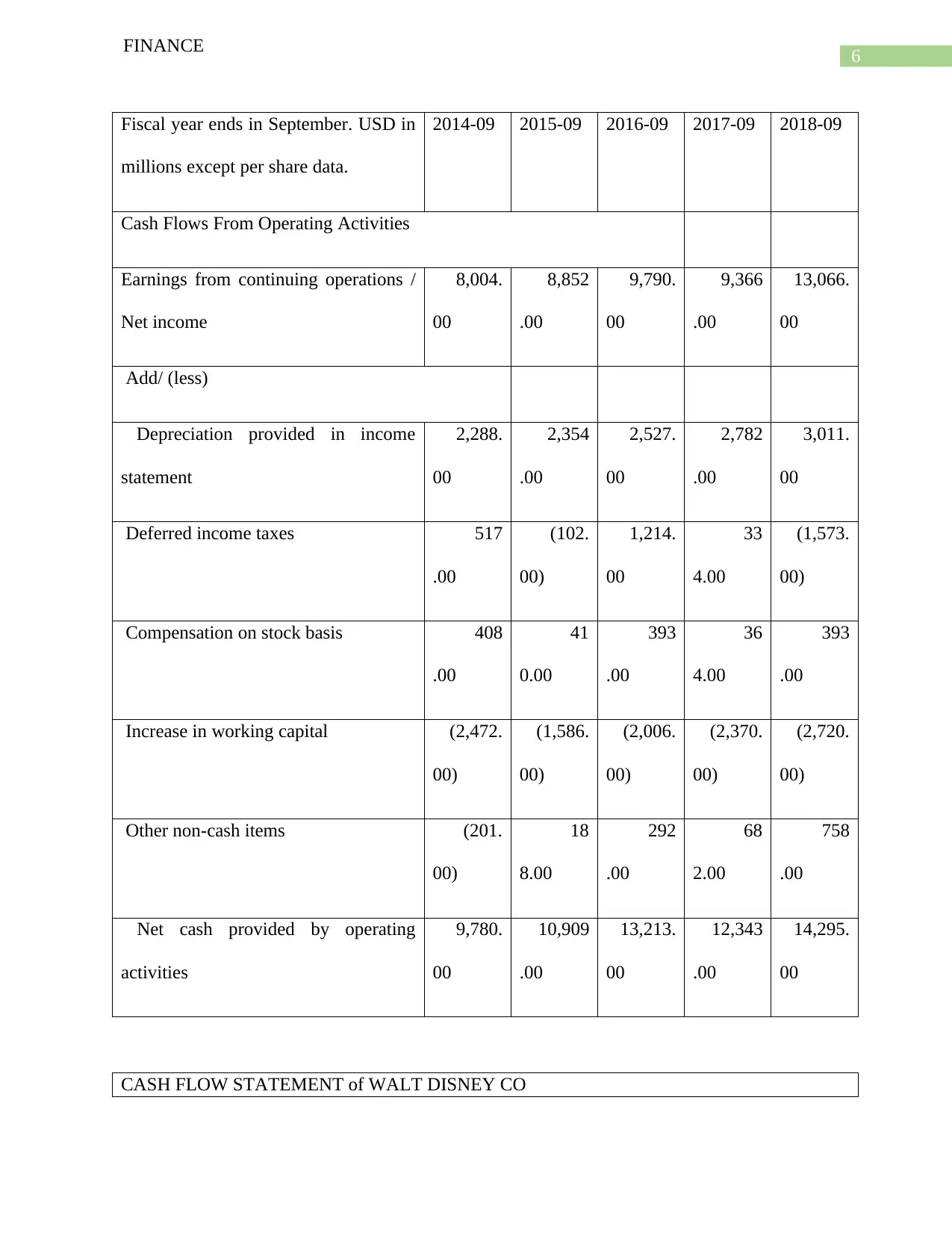

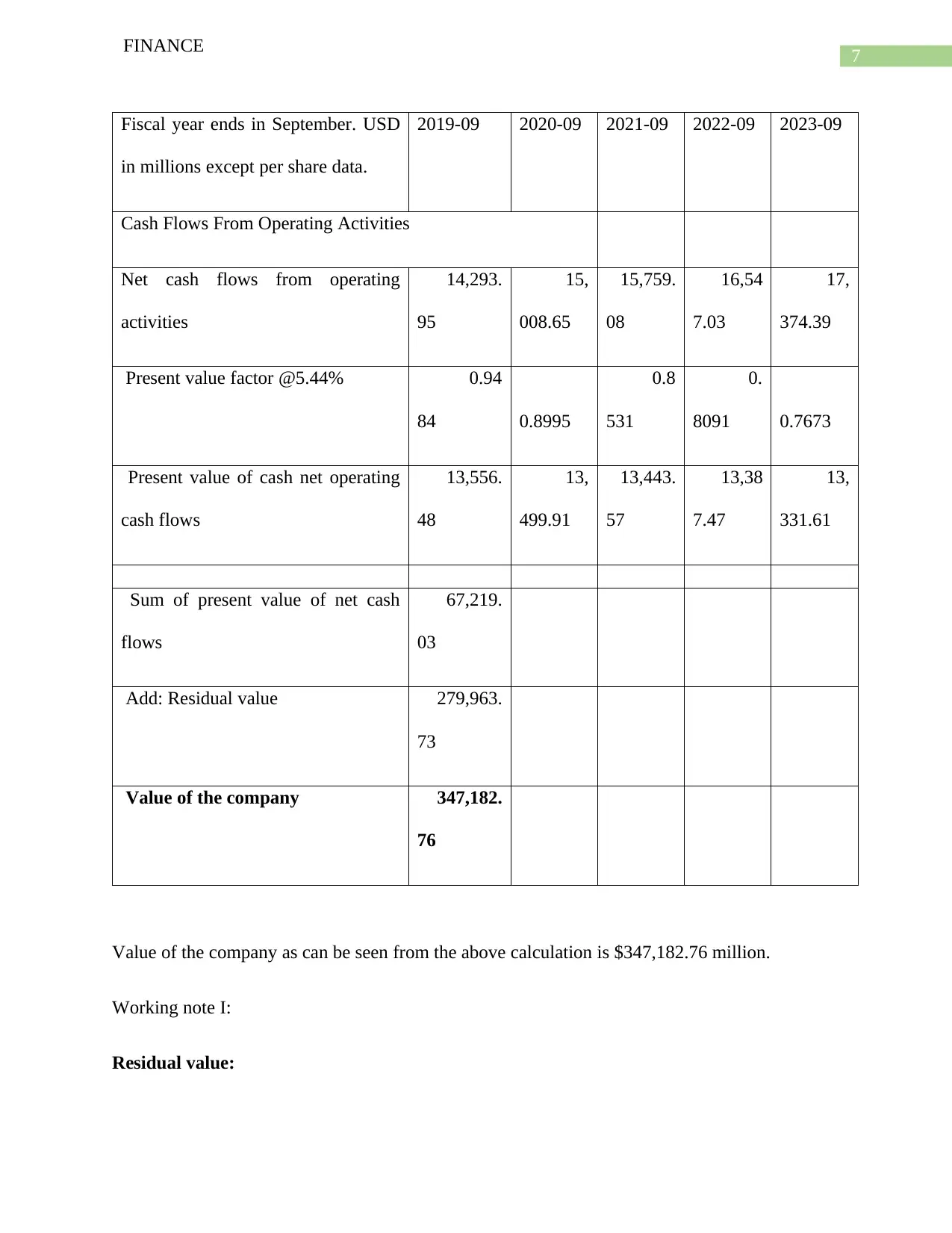

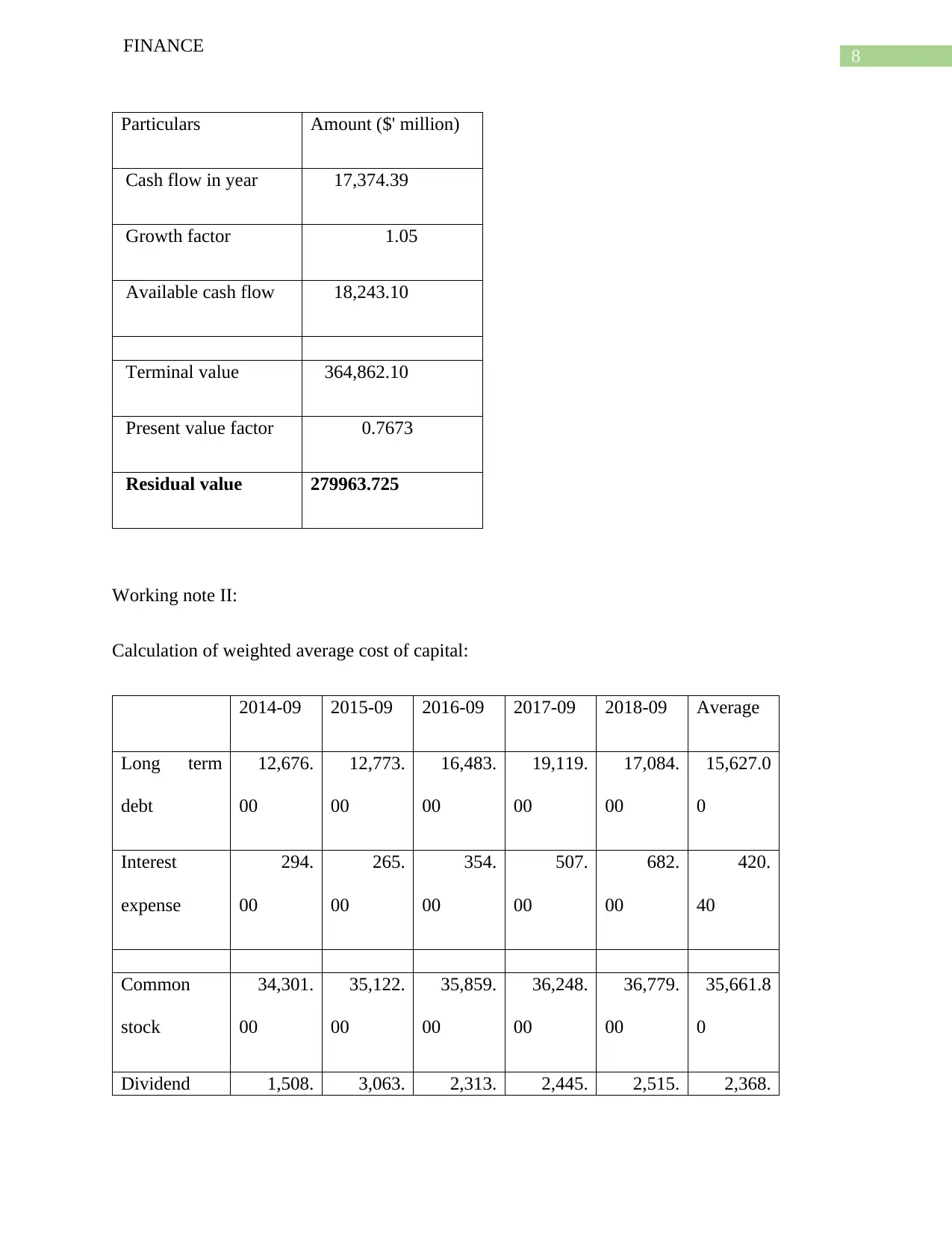

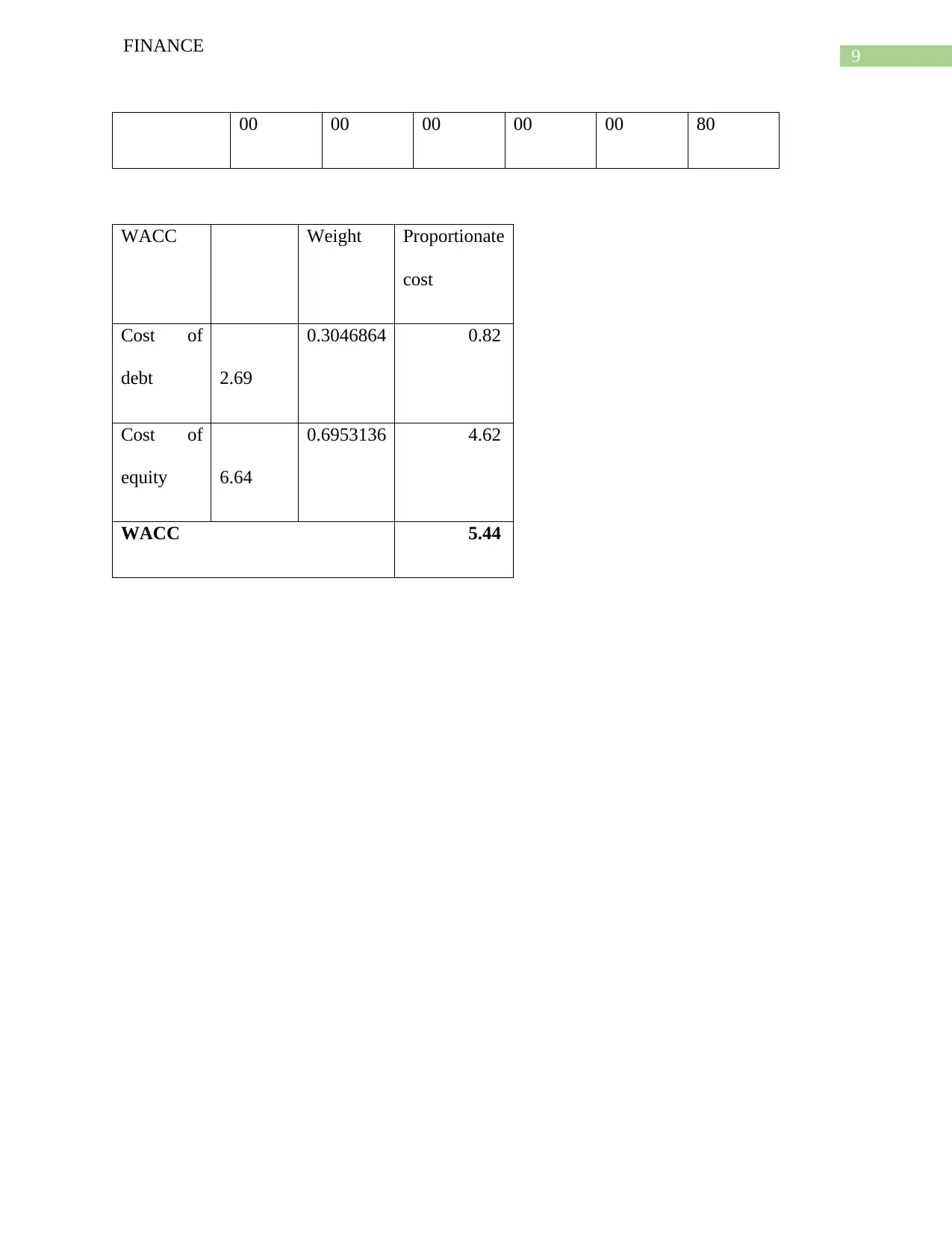

This finance case study analyzes the valuation of a company using the discounted cash flow (DCF) approach. The analysis begins with an income statement and cash flow statement for Walt Disney over a five-year period, providing the basis for projecting future cash flows. The student used net cash flow from operating activities. The projected cash flows are then adjusted by a 5% growth rate. The case study provides detailed calculations of the present value of cash flows, the weighted average cost of capital (WACC), and the residual value to arrive at a final company valuation of $347,182.76 million. The analysis also includes working notes for residual value and WACC calculations, along with relevant references to support the methodology and assumptions used. The study addresses the components of the income approach as required in the assignment brief.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.