Finance 3 Accounting and Finance Part 1 Telstra Corporation Limited

31 Pages8412 Words67 Views

Added on 2021-06-17

About This Document

The company deals in developing telecommunication networks and offering product and services which includes fixed line and mobile telephony, data services, internet and other network services. 17.4 million mobile services; 6.8 million fixed voice services and 3.5 million retail fixed broadband services to its customers worldwide (Telstra.

Finance 3 Accounting and Finance Part 1 Telstra Corporation Limited

Added on 2021-06-17

ShareRelated Documents

RUNNING HEAD: FINANCE

Management accounting and Finance

Management accounting and Finance

Finance

2

Part 1

Telstra Corporation Limited is an Australia based telecommunications and technology

company having its headquarters situated at Melbourne. The company deals in developing

telecommunication networks and offering product and services which includes fixed line and

mobile telephony, data services, internet and other network services. Telstra provides approx.

17.4 million mobile services; 6.8 million fixed voice services and 3.5 million retail fixed

broadband services to its customers worldwide (Telstra. 2018).

Company has a vision and mission of connecting more and more people with offering more

opportunities to them. In order to accomplish this, Telstra focuses on using simple and easy

technology and solutions that are easily accessible to its users. It also focuses on becoming

the largest national mobile network of Australia (Reuters. 2018).

As of 2017, the company has earned a net profit of $3874 million. Telstra Corporation is

listed on Australian Stock Exchange (ASX) with a ticker symbol of ASX: TLS. The company

is now focused on expanding its operations in the international markets and looking forward

for its successful growth in future (Bloomberg. 2018).

Financial analysis is the process of measuring the performance of a company in terms of its

profitability, capital structure, efficiency and liquidity. The analysis includes a critical

examination of the financial statements prepared by an enterprise at the end of every fiscal

year. On the basis of the evaluation, decisions related to that company are been taken by

investors and other key people. The information presented in the statements is used for the

analysis and the same is been compared with the industry average or over the years (Lee, Lee

and Lee, 2009)

However, there are various tools used for conducting a financial analysis. Among the various

available techniques, the most commonly used is the ratio analysis. This technique involves

2

Part 1

Telstra Corporation Limited is an Australia based telecommunications and technology

company having its headquarters situated at Melbourne. The company deals in developing

telecommunication networks and offering product and services which includes fixed line and

mobile telephony, data services, internet and other network services. Telstra provides approx.

17.4 million mobile services; 6.8 million fixed voice services and 3.5 million retail fixed

broadband services to its customers worldwide (Telstra. 2018).

Company has a vision and mission of connecting more and more people with offering more

opportunities to them. In order to accomplish this, Telstra focuses on using simple and easy

technology and solutions that are easily accessible to its users. It also focuses on becoming

the largest national mobile network of Australia (Reuters. 2018).

As of 2017, the company has earned a net profit of $3874 million. Telstra Corporation is

listed on Australian Stock Exchange (ASX) with a ticker symbol of ASX: TLS. The company

is now focused on expanding its operations in the international markets and looking forward

for its successful growth in future (Bloomberg. 2018).

Financial analysis is the process of measuring the performance of a company in terms of its

profitability, capital structure, efficiency and liquidity. The analysis includes a critical

examination of the financial statements prepared by an enterprise at the end of every fiscal

year. On the basis of the evaluation, decisions related to that company are been taken by

investors and other key people. The information presented in the statements is used for the

analysis and the same is been compared with the industry average or over the years (Lee, Lee

and Lee, 2009)

However, there are various tools used for conducting a financial analysis. Among the various

available techniques, the most commonly used is the ratio analysis. This technique involves

Finance

3

the calculation of different categorized ratios which determine and measure the financial

performance of a company from every aspect. Most of the investors rely on the key ratios

which provide a snapshot of the company’s financial position. On the basis of this ratio they

take their decisions regarding making investment in the particular company. The ratios are

also very useful for the shareholders of the company as by correctly interpreting them, they

can understand what is the company doing with their investment plus how it is using it and

how much return is been available to them (Vogel, 2014).

Following are the ratios calculated for Telstra Corporation Limited to evaluate its

performance over the years 2016 and 2017.

1. Operating profit margin ratio

Operating profit or Earnings before Interest and Tax is that portion of revenue which is left

after paying all the cost of goods sold and the operating expenses. The amount is expressed as

a percentage of total sales and is used for measuring the profitability of the company (Tracy,

2012). The OPR of Telstra is represented below.

Operating Profit Margin 2016 2017

Operating Profit (A) 6,310 6,238

Revenue (B) 27,050 28,205

OPR(A/B) 23% 22%

(Telstra. 2016).

3

the calculation of different categorized ratios which determine and measure the financial

performance of a company from every aspect. Most of the investors rely on the key ratios

which provide a snapshot of the company’s financial position. On the basis of this ratio they

take their decisions regarding making investment in the particular company. The ratios are

also very useful for the shareholders of the company as by correctly interpreting them, they

can understand what is the company doing with their investment plus how it is using it and

how much return is been available to them (Vogel, 2014).

Following are the ratios calculated for Telstra Corporation Limited to evaluate its

performance over the years 2016 and 2017.

1. Operating profit margin ratio

Operating profit or Earnings before Interest and Tax is that portion of revenue which is left

after paying all the cost of goods sold and the operating expenses. The amount is expressed as

a percentage of total sales and is used for measuring the profitability of the company (Tracy,

2012). The OPR of Telstra is represented below.

Operating Profit Margin 2016 2017

Operating Profit (A) 6,310 6,238

Revenue (B) 27,050 28,205

OPR(A/B) 23% 22%

(Telstra. 2016).

Finance

4

2016 2017

0.2

0.22

0.24

Operating profit ratio

Operating Profit Margin

Years

%

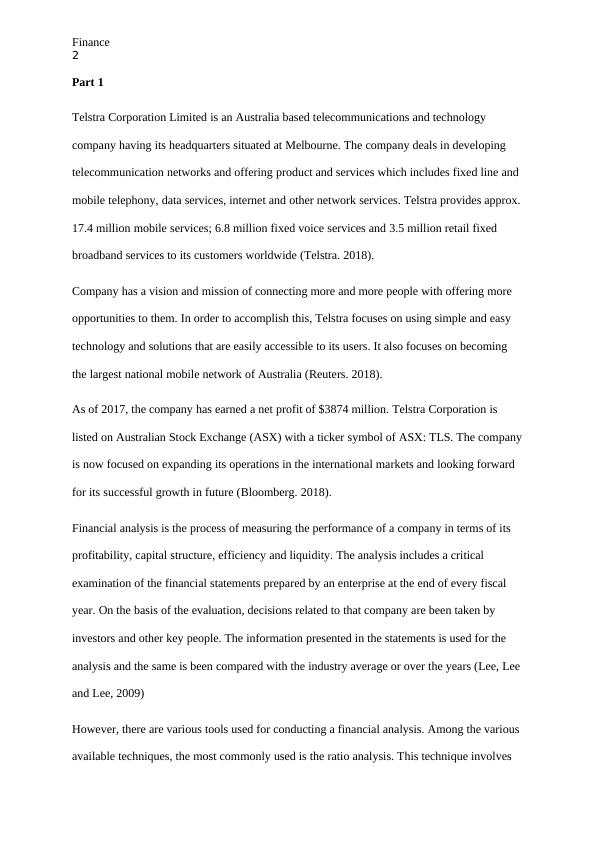

The above graph shows the graphical representation of Telstra’s operating profit margin for

the past two year that are 2016 and 2017. It can be observed from the graph that the company

has a ratio of 23% in 2016 and the same reduces to 22% in 2017. This is because of the

overall reduction in the EBIT of Telstra from $6310 million to $6238 million. However, the

change is minor and has not impacted the profitability of Telstra to a great extent. Also, the

organization’s net profit has risen in the year 2017.

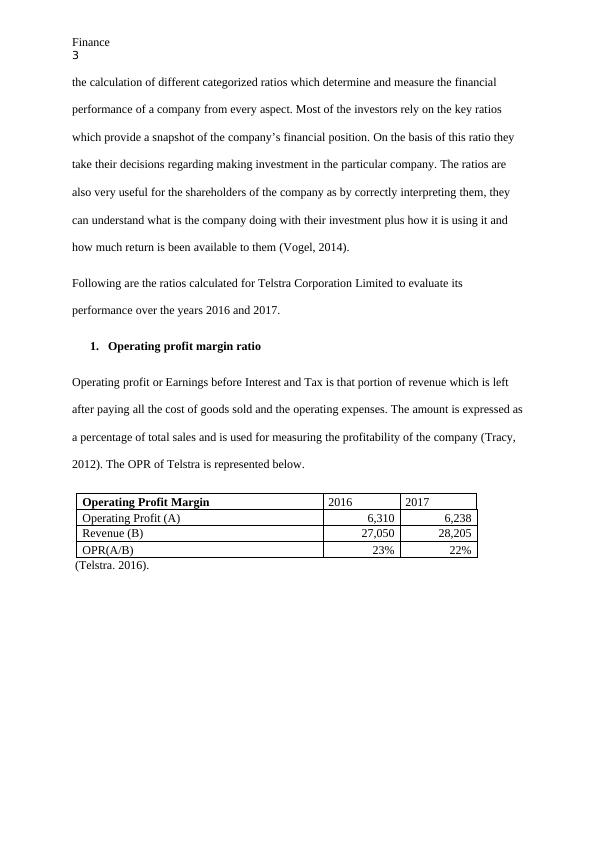

2. Price to equity ratio

It is also known as price earnings ratio. It indicates the willingness of an investor to pay per

dollar of earnings. Therefore, it is also known as price multiple and is calculated by dividing

the market value per share with earnings per share. Generally a high P/E ratio indicates that

the company is doing well, earning profits and has a quality of management (Warren and

Jones, 2018).

Price Earnings ratio 2016 2017

Market price per share (A) 5.6 4.3

Earnings per share (B) 47.4 32.5

P/E ratio (A/B) 0.12 0.13

4

2016 2017

0.2

0.22

0.24

Operating profit ratio

Operating Profit Margin

Years

%

The above graph shows the graphical representation of Telstra’s operating profit margin for

the past two year that are 2016 and 2017. It can be observed from the graph that the company

has a ratio of 23% in 2016 and the same reduces to 22% in 2017. This is because of the

overall reduction in the EBIT of Telstra from $6310 million to $6238 million. However, the

change is minor and has not impacted the profitability of Telstra to a great extent. Also, the

organization’s net profit has risen in the year 2017.

2. Price to equity ratio

It is also known as price earnings ratio. It indicates the willingness of an investor to pay per

dollar of earnings. Therefore, it is also known as price multiple and is calculated by dividing

the market value per share with earnings per share. Generally a high P/E ratio indicates that

the company is doing well, earning profits and has a quality of management (Warren and

Jones, 2018).

Price Earnings ratio 2016 2017

Market price per share (A) 5.6 4.3

Earnings per share (B) 47.4 32.5

P/E ratio (A/B) 0.12 0.13

Finance

5

(Telstra. 2017).

2016 2017

0.10

0.12

0.14

P/E ratio

Price Earnings ratio

Years

Values

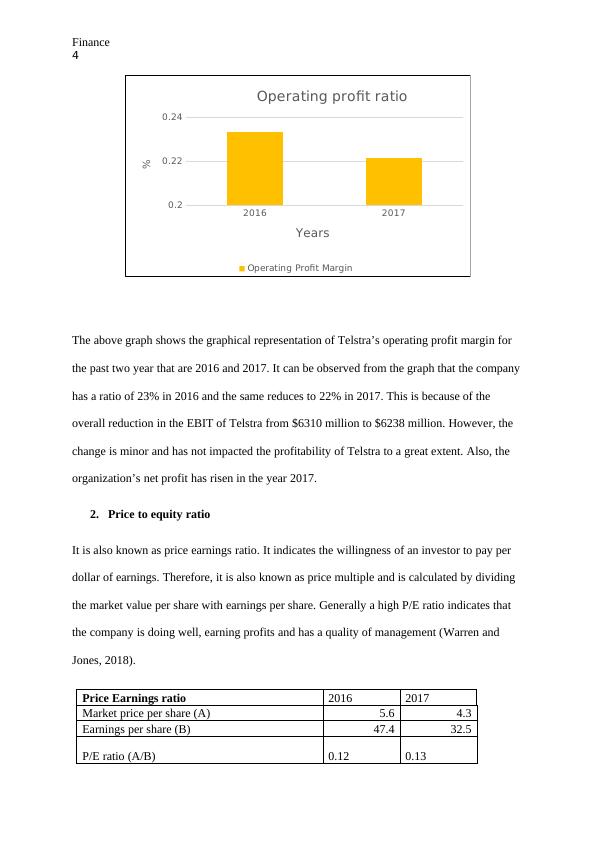

The above graph shows the price earnings ratio of Telstra Corporation for years 2016 and

2017. In 2016, company had a ratio of 0.12 which rises to 0.13 in 2017. This shows an

increase in the P/E ratio due to the high profits and minor change in the share price of the

company. The EPS and MPS of Telstra both have reduced in 2017 but the reduction in the

market price is lower than the fall in company’s EPS which boosted up its ratio. However the

rise indicates that the investors are expecting growth in future and the company is performing

well.

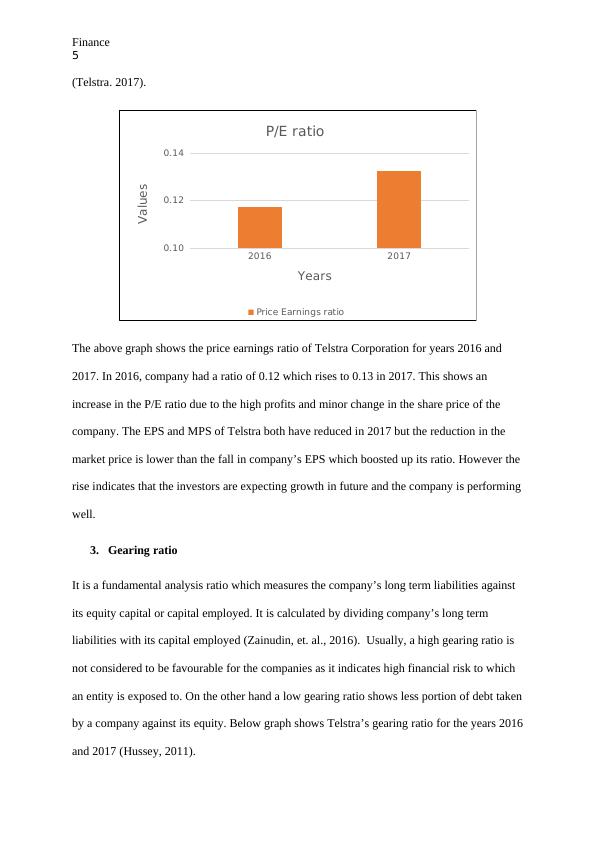

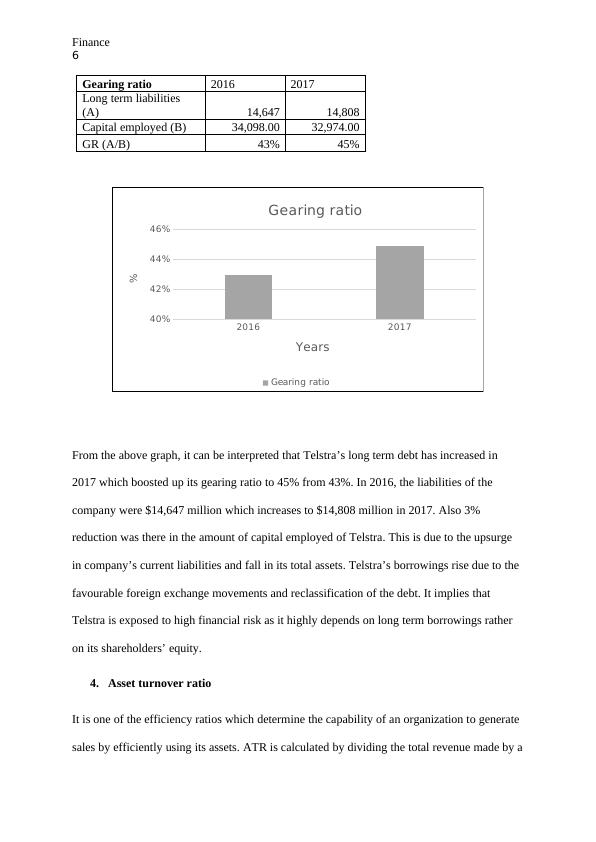

3. Gearing ratio

It is a fundamental analysis ratio which measures the company’s long term liabilities against

its equity capital or capital employed. It is calculated by dividing company’s long term

liabilities with its capital employed (Zainudin, et. al., 2016). Usually, a high gearing ratio is

not considered to be favourable for the companies as it indicates high financial risk to which

an entity is exposed to. On the other hand a low gearing ratio shows less portion of debt taken

by a company against its equity. Below graph shows Telstra’s gearing ratio for the years 2016

and 2017 (Hussey, 2011).

5

(Telstra. 2017).

2016 2017

0.10

0.12

0.14

P/E ratio

Price Earnings ratio

Years

Values

The above graph shows the price earnings ratio of Telstra Corporation for years 2016 and

2017. In 2016, company had a ratio of 0.12 which rises to 0.13 in 2017. This shows an

increase in the P/E ratio due to the high profits and minor change in the share price of the

company. The EPS and MPS of Telstra both have reduced in 2017 but the reduction in the

market price is lower than the fall in company’s EPS which boosted up its ratio. However the

rise indicates that the investors are expecting growth in future and the company is performing

well.

3. Gearing ratio

It is a fundamental analysis ratio which measures the company’s long term liabilities against

its equity capital or capital employed. It is calculated by dividing company’s long term

liabilities with its capital employed (Zainudin, et. al., 2016). Usually, a high gearing ratio is

not considered to be favourable for the companies as it indicates high financial risk to which

an entity is exposed to. On the other hand a low gearing ratio shows less portion of debt taken

by a company against its equity. Below graph shows Telstra’s gearing ratio for the years 2016

and 2017 (Hussey, 2011).

Finance

6

Gearing ratio 2016 2017

Long term liabilities

(A) 14,647 14,808

Capital employed (B) 34,098.00 32,974.00

GR (A/B) 43% 45%

2016 2017

40%

42%

44%

46%

Gearing ratio

Gearing ratio

Years

%

From the above graph, it can be interpreted that Telstra’s long term debt has increased in

2017 which boosted up its gearing ratio to 45% from 43%. In 2016, the liabilities of the

company were $14,647 million which increases to $14,808 million in 2017. Also 3%

reduction was there in the amount of capital employed of Telstra. This is due to the upsurge

in company’s current liabilities and fall in its total assets. Telstra’s borrowings rise due to the

favourable foreign exchange movements and reclassification of the debt. It implies that

Telstra is exposed to high financial risk as it highly depends on long term borrowings rather

on its shareholders’ equity.

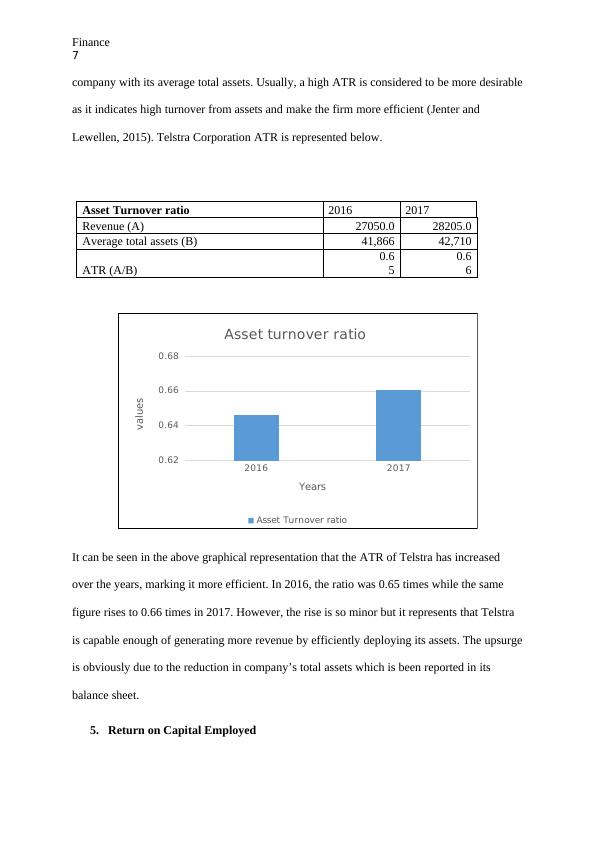

4. Asset turnover ratio

It is one of the efficiency ratios which determine the capability of an organization to generate

sales by efficiently using its assets. ATR is calculated by dividing the total revenue made by a

6

Gearing ratio 2016 2017

Long term liabilities

(A) 14,647 14,808

Capital employed (B) 34,098.00 32,974.00

GR (A/B) 43% 45%

2016 2017

40%

42%

44%

46%

Gearing ratio

Gearing ratio

Years

%

From the above graph, it can be interpreted that Telstra’s long term debt has increased in

2017 which boosted up its gearing ratio to 45% from 43%. In 2016, the liabilities of the

company were $14,647 million which increases to $14,808 million in 2017. Also 3%

reduction was there in the amount of capital employed of Telstra. This is due to the upsurge

in company’s current liabilities and fall in its total assets. Telstra’s borrowings rise due to the

favourable foreign exchange movements and reclassification of the debt. It implies that

Telstra is exposed to high financial risk as it highly depends on long term borrowings rather

on its shareholders’ equity.

4. Asset turnover ratio

It is one of the efficiency ratios which determine the capability of an organization to generate

sales by efficiently using its assets. ATR is calculated by dividing the total revenue made by a

Finance

7

company with its average total assets. Usually, a high ATR is considered to be more desirable

as it indicates high turnover from assets and make the firm more efficient (Jenter and

Lewellen, 2015). Telstra Corporation ATR is represented below.

Asset Turnover ratio 2016 2017

Revenue (A) 27050.0 28205.0

Average total assets (B) 41,866 42,710

ATR (A/B)

0.6

5

0.6

6

2016 2017

0.62

0.64

0.66

0.68

Asset turnover ratio

Asset Turnover ratio

Years

values

It can be seen in the above graphical representation that the ATR of Telstra has increased

over the years, marking it more efficient. In 2016, the ratio was 0.65 times while the same

figure rises to 0.66 times in 2017. However, the rise is so minor but it represents that Telstra

is capable enough of generating more revenue by efficiently deploying its assets. The upsurge

is obviously due to the reduction in company’s total assets which is been reported in its

balance sheet.

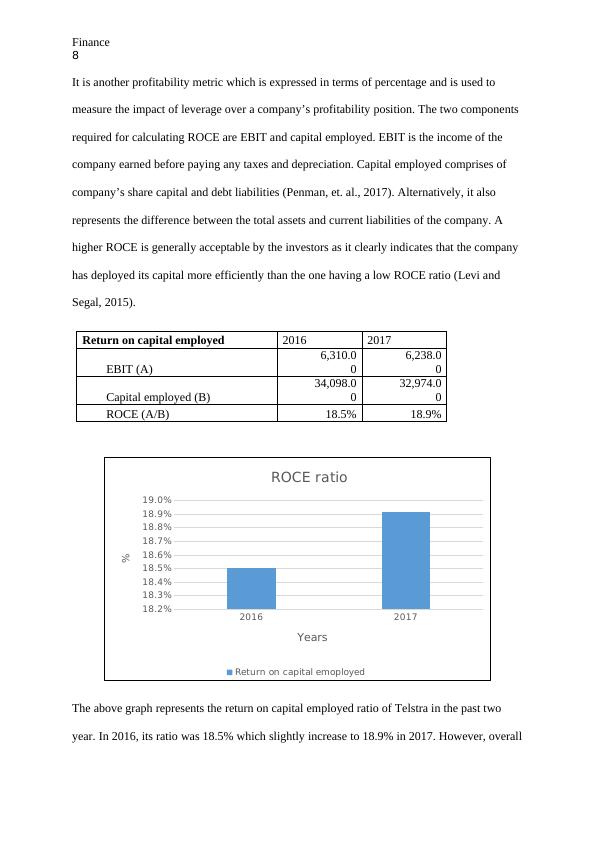

5. Return on Capital Employed

7

company with its average total assets. Usually, a high ATR is considered to be more desirable

as it indicates high turnover from assets and make the firm more efficient (Jenter and

Lewellen, 2015). Telstra Corporation ATR is represented below.

Asset Turnover ratio 2016 2017

Revenue (A) 27050.0 28205.0

Average total assets (B) 41,866 42,710

ATR (A/B)

0.6

5

0.6

6

2016 2017

0.62

0.64

0.66

0.68

Asset turnover ratio

Asset Turnover ratio

Years

values

It can be seen in the above graphical representation that the ATR of Telstra has increased

over the years, marking it more efficient. In 2016, the ratio was 0.65 times while the same

figure rises to 0.66 times in 2017. However, the rise is so minor but it represents that Telstra

is capable enough of generating more revenue by efficiently deploying its assets. The upsurge

is obviously due to the reduction in company’s total assets which is been reported in its

balance sheet.

5. Return on Capital Employed

Finance

8

It is another profitability metric which is expressed in terms of percentage and is used to

measure the impact of leverage over a company’s profitability position. The two components

required for calculating ROCE are EBIT and capital employed. EBIT is the income of the

company earned before paying any taxes and depreciation. Capital employed comprises of

company’s share capital and debt liabilities (Penman, et. al., 2017). Alternatively, it also

represents the difference between the total assets and current liabilities of the company. A

higher ROCE is generally acceptable by the investors as it clearly indicates that the company

has deployed its capital more efficiently than the one having a low ROCE ratio (Levi and

Segal, 2015).

Return on capital employed 2016 2017

EBIT (A)

6,310.0

0

6,238.0

0

Capital employed (B)

34,098.0

0

32,974.0

0

ROCE (A/B) 18.5% 18.9%

2016 2017

18.2%

18.3%

18.4%

18.5%

18.6%

18.7%

18.8%

18.9%

19.0%

ROCE ratio

Return on capital emoployed

Years

%

The above graph represents the return on capital employed ratio of Telstra in the past two

year. In 2016, its ratio was 18.5% which slightly increase to 18.9% in 2017. However, overall

8

It is another profitability metric which is expressed in terms of percentage and is used to

measure the impact of leverage over a company’s profitability position. The two components

required for calculating ROCE are EBIT and capital employed. EBIT is the income of the

company earned before paying any taxes and depreciation. Capital employed comprises of

company’s share capital and debt liabilities (Penman, et. al., 2017). Alternatively, it also

represents the difference between the total assets and current liabilities of the company. A

higher ROCE is generally acceptable by the investors as it clearly indicates that the company

has deployed its capital more efficiently than the one having a low ROCE ratio (Levi and

Segal, 2015).

Return on capital employed 2016 2017

EBIT (A)

6,310.0

0

6,238.0

0

Capital employed (B)

34,098.0

0

32,974.0

0

ROCE (A/B) 18.5% 18.9%

2016 2017

18.2%

18.3%

18.4%

18.5%

18.6%

18.7%

18.8%

18.9%

19.0%

ROCE ratio

Return on capital emoployed

Years

%

The above graph represents the return on capital employed ratio of Telstra in the past two

year. In 2016, its ratio was 18.5% which slightly increase to 18.9% in 2017. However, overall

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Telstra Financial Analysis Assignmentlg...

|16

|3025

|29

LB5212 Financial Analysis Company Report - Telstra Corporation Ltdlg...

|23

|3643

|333

Evaluation of Telstra Annual Reportlg...

|5

|1516

|95

Financial Analysis of Telstra Corporation and Comparison with Queste Communications Limitedlg...

|27

|4185

|91

Financial Analysis of Telstra Corporation and JB HI-FI Limitedlg...

|18

|4110

|282

ASX CGC Principleslg...

|14

|2773

|232