Assignment 2: Financial Plan for Allen Family - [University Name]

VerifiedAdded on 2023/04/25

|15

|3431

|349

Project

AI Summary

This project presents a comprehensive financial plan for the Allen family, addressing various aspects of their financial situation. The plan begins by gathering and organizing both qualitative (goals, risk tolerance) and quantitative (income, expenses, assets, liabilities) information. It includes a detailed cash flow statement and balance sheet, followed by ratio analysis to assess liquidity, debt, and investment performance. The plan then delves into tax planning strategies, recommending income splitting and maximizing RRSP contributions. Debt and cash management are addressed, including mortgage and car loan considerations. Risk management and insurance needs are evaluated, focusing on general insurance and disability coverage. Finally, the plan provides recommendations on investment management, including portfolio diversification. The assignment aims to provide a holistic financial strategy for the Allen family to achieve their financial goals.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Author’s Note

Finance

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

Table of Contents

Financial Plan..................................................................................................................................2

Step 1: Gather and Organize Relevant Qualitative and Quantitative Information..........................2

Step 2: Ratio Analysis.....................................................................................................................5

Step 3: Align Financial Resources and Goals................................................................................12

Step 4: Make an Overall Recommendation...................................................................................13

Table of Contents

Financial Plan..................................................................................................................................2

Step 1: Gather and Organize Relevant Qualitative and Quantitative Information..........................2

Step 2: Ratio Analysis.....................................................................................................................5

Step 3: Align Financial Resources and Goals................................................................................12

Step 4: Make an Overall Recommendation...................................................................................13

2FINANCE

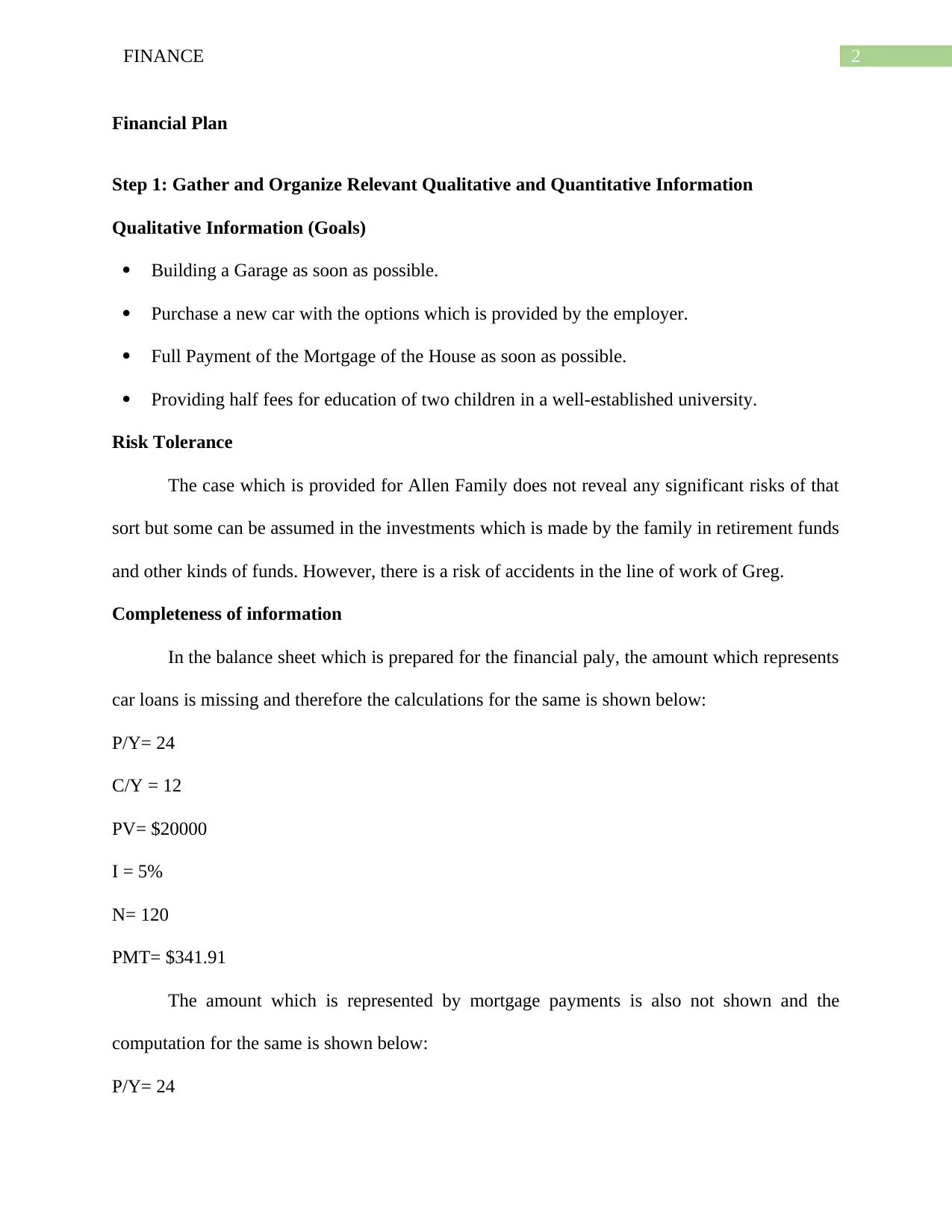

Financial Plan

Step 1: Gather and Organize Relevant Qualitative and Quantitative Information

Qualitative Information (Goals)

Building a Garage as soon as possible.

Purchase a new car with the options which is provided by the employer.

Full Payment of the Mortgage of the House as soon as possible.

Providing half fees for education of two children in a well-established university.

Risk Tolerance

The case which is provided for Allen Family does not reveal any significant risks of that

sort but some can be assumed in the investments which is made by the family in retirement funds

and other kinds of funds. However, there is a risk of accidents in the line of work of Greg.

Completeness of information

In the balance sheet which is prepared for the financial paly, the amount which represents

car loans is missing and therefore the calculations for the same is shown below:

P/Y= 24

C/Y = 12

PV= $20000

I = 5%

N= 120

PMT= $341.91

The amount which is represented by mortgage payments is also not shown and the

computation for the same is shown below:

P/Y= 24

Financial Plan

Step 1: Gather and Organize Relevant Qualitative and Quantitative Information

Qualitative Information (Goals)

Building a Garage as soon as possible.

Purchase a new car with the options which is provided by the employer.

Full Payment of the Mortgage of the House as soon as possible.

Providing half fees for education of two children in a well-established university.

Risk Tolerance

The case which is provided for Allen Family does not reveal any significant risks of that

sort but some can be assumed in the investments which is made by the family in retirement funds

and other kinds of funds. However, there is a risk of accidents in the line of work of Greg.

Completeness of information

In the balance sheet which is prepared for the financial paly, the amount which represents

car loans is missing and therefore the calculations for the same is shown below:

P/Y= 24

C/Y = 12

PV= $20000

I = 5%

N= 120

PMT= $341.91

The amount which is represented by mortgage payments is also not shown and the

computation for the same is shown below:

P/Y= 24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

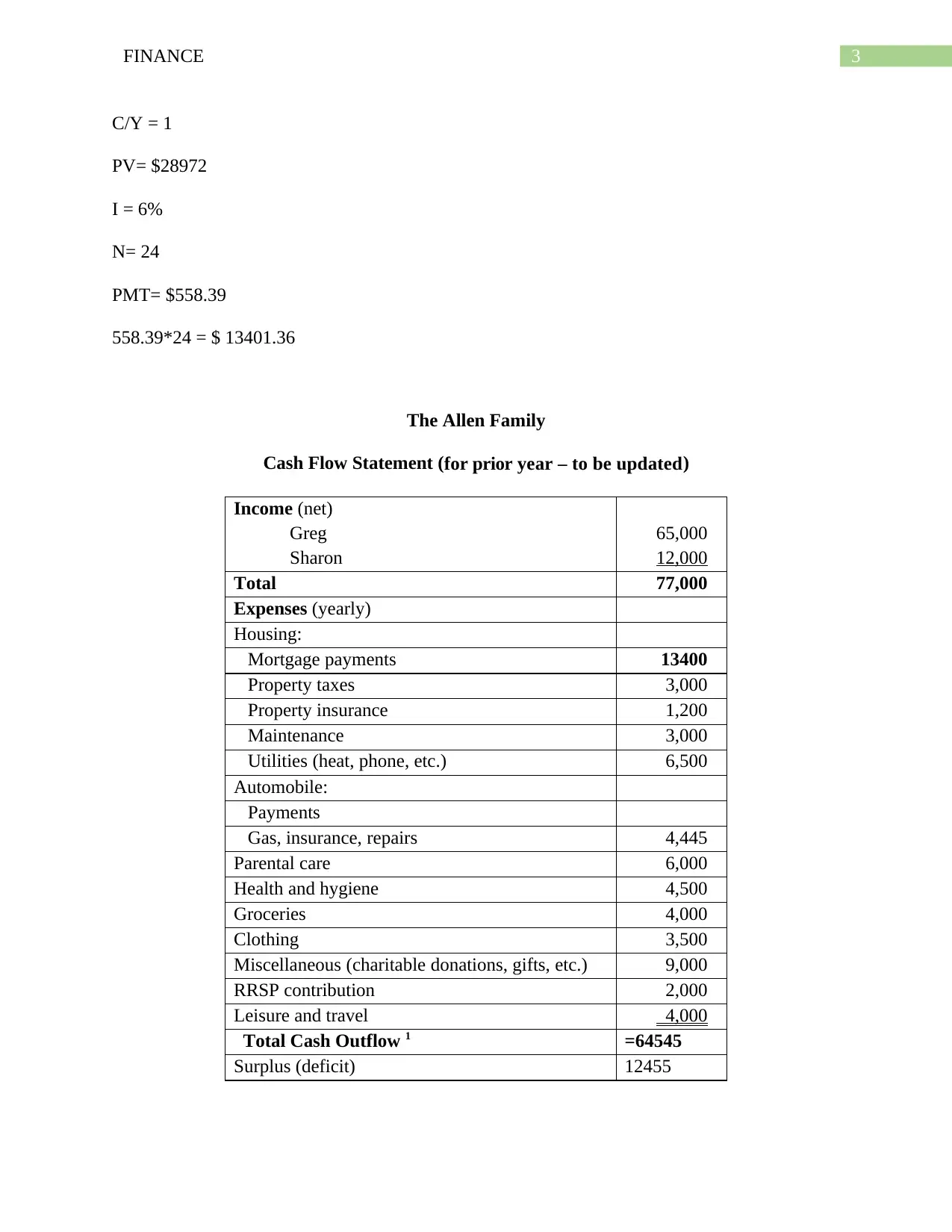

C/Y = 1

PV= $28972

I = 6%

N= 24

PMT= $558.39

558.39*24 = $ 13401.36

The Allen Family

Cash Flow Statement (for prior year – to be updated)

Income (net)

Greg

Sharon

65,000

12,000

Total 77,000

Expenses (yearly)

Housing:

Mortgage payments 13400

Property taxes 3,000

Property insurance 1,200

Maintenance 3,000

Utilities (heat, phone, etc.) 6,500

Automobile:

Payments

Gas, insurance, repairs 4,445

Parental care 6,000

Health and hygiene 4,500

Groceries 4,000

Clothing 3,500

Miscellaneous (charitable donations, gifts, etc.) 9,000

RRSP contribution 2,000

Leisure and travel 4,000

Total Cash Outflow 1 =64545

Surplus (deficit) 12455

C/Y = 1

PV= $28972

I = 6%

N= 24

PMT= $558.39

558.39*24 = $ 13401.36

The Allen Family

Cash Flow Statement (for prior year – to be updated)

Income (net)

Greg

Sharon

65,000

12,000

Total 77,000

Expenses (yearly)

Housing:

Mortgage payments 13400

Property taxes 3,000

Property insurance 1,200

Maintenance 3,000

Utilities (heat, phone, etc.) 6,500

Automobile:

Payments

Gas, insurance, repairs 4,445

Parental care 6,000

Health and hygiene 4,500

Groceries 4,000

Clothing 3,500

Miscellaneous (charitable donations, gifts, etc.) 9,000

RRSP contribution 2,000

Leisure and travel 4,000

Total Cash Outflow 1 =64545

Surplus (deficit) 12455

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE

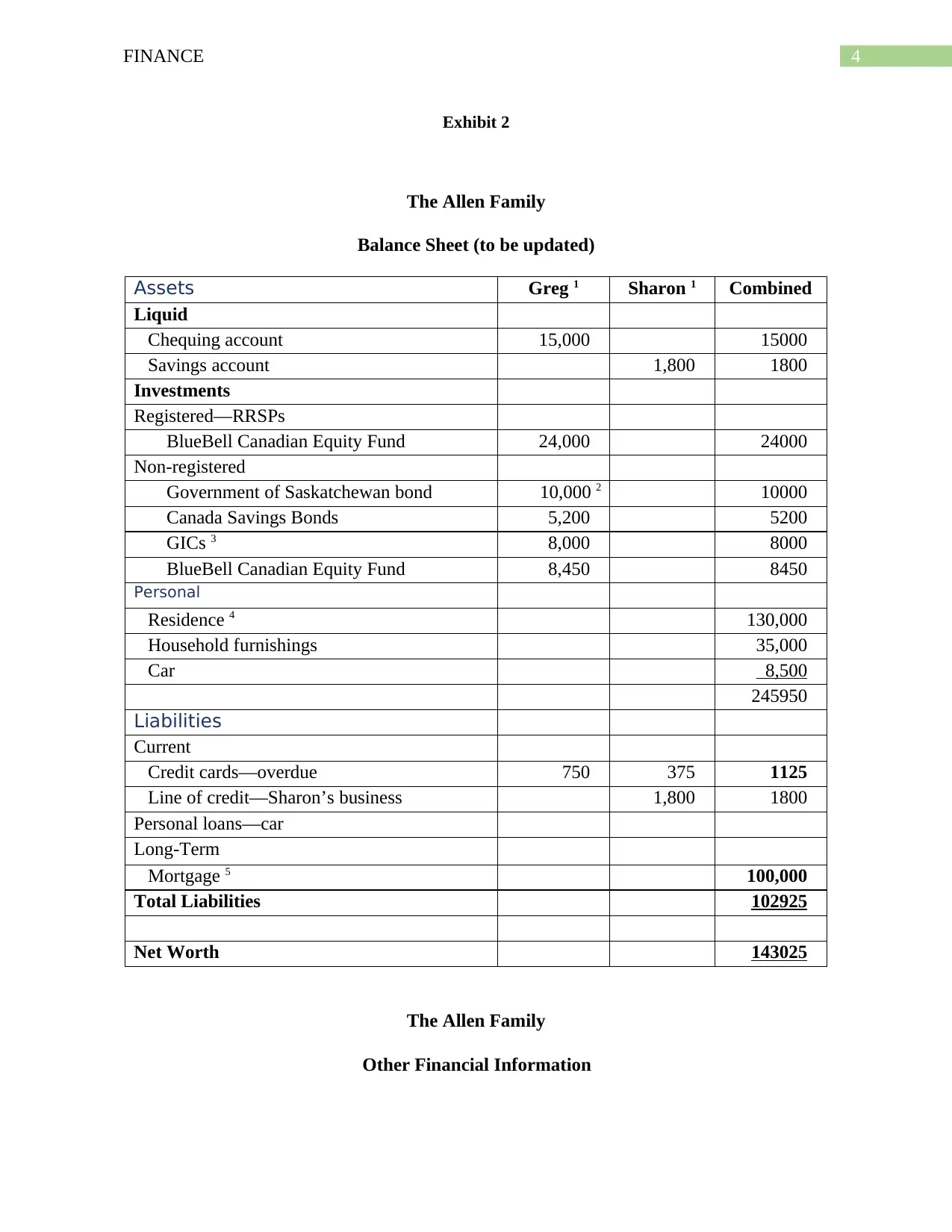

Exhibit 2

The Allen Family

Balance Sheet (to be updated)

Assets Greg 1 Sharon 1 Combined

Liquid

Chequing account 15,000 15000

Savings account 1,800 1800

Investments

Registered—RRSPs

BlueBell Canadian Equity Fund 24,000 24000

Non-registered

Government of Saskatchewan bond 10,000 2 10000

Canada Savings Bonds 5,200 5200

GICs 3 8,000 8000

BlueBell Canadian Equity Fund 8,450 8450

Personal

Residence 4 130,000

Household furnishings 35,000

Car 8,500

245950

Liabilities

Current

Credit cards—overdue 750 375 1125

Line of credit—Sharon’s business 1,800 1800

Personal loans—car

Long-Term

Mortgage 5 100,000

Total Liabilities 102925

Net Worth 143025

The Allen Family

Other Financial Information

Exhibit 2

The Allen Family

Balance Sheet (to be updated)

Assets Greg 1 Sharon 1 Combined

Liquid

Chequing account 15,000 15000

Savings account 1,800 1800

Investments

Registered—RRSPs

BlueBell Canadian Equity Fund 24,000 24000

Non-registered

Government of Saskatchewan bond 10,000 2 10000

Canada Savings Bonds 5,200 5200

GICs 3 8,000 8000

BlueBell Canadian Equity Fund 8,450 8450

Personal

Residence 4 130,000

Household furnishings 35,000

Car 8,500

245950

Liabilities

Current

Credit cards—overdue 750 375 1125

Line of credit—Sharon’s business 1,800 1800

Personal loans—car

Long-Term

Mortgage 5 100,000

Total Liabilities 102925

Net Worth 143025

The Allen Family

Other Financial Information

5FINANCE

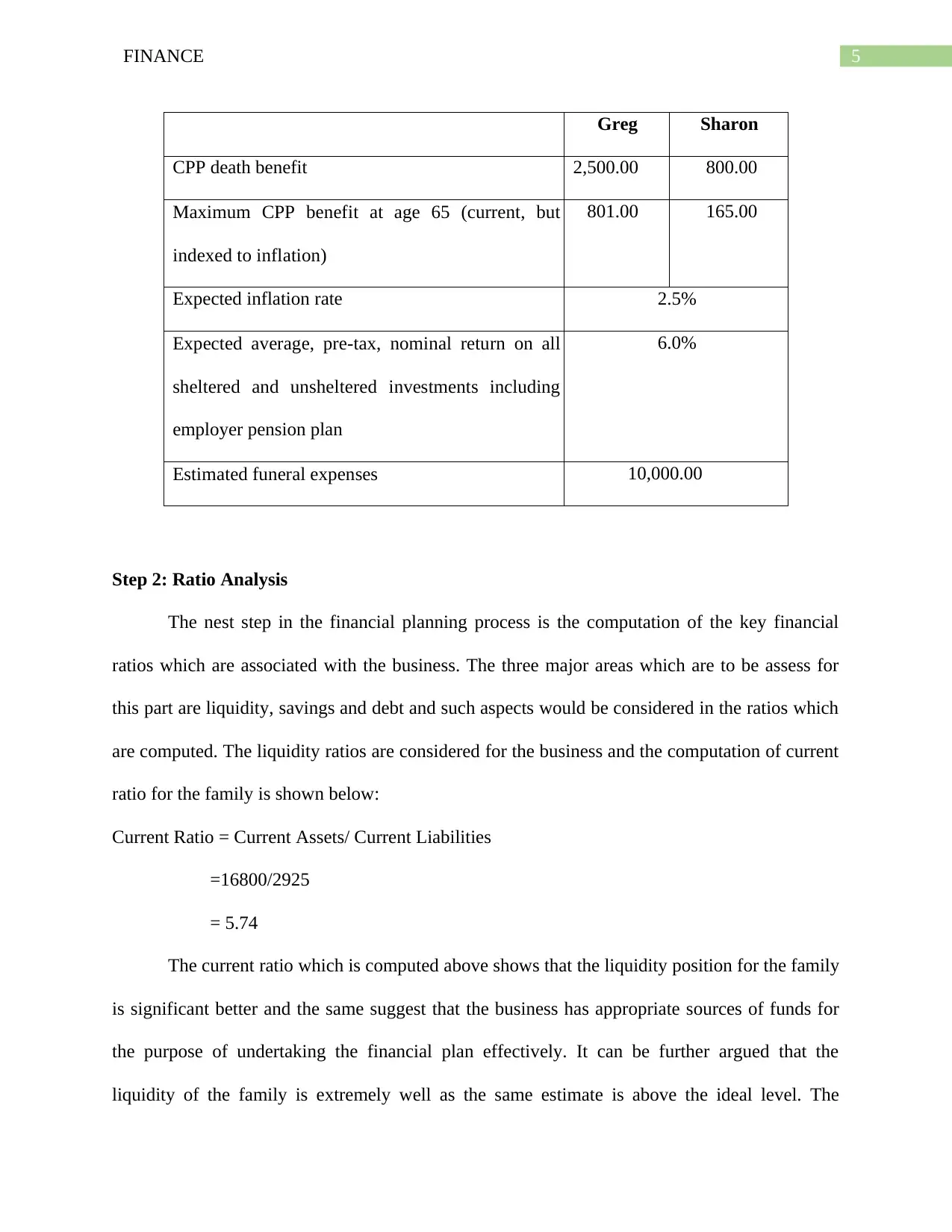

Greg Sharon

CPP death benefit 2,500.00 800.00

Maximum CPP benefit at age 65 (current, but

indexed to inflation)

801.00 165.00

Expected inflation rate 2.5%

Expected average, pre-tax, nominal return on all

sheltered and unsheltered investments including

employer pension plan

6.0%

Estimated funeral expenses 10,000.00

Step 2: Ratio Analysis

The nest step in the financial planning process is the computation of the key financial

ratios which are associated with the business. The three major areas which are to be assess for

this part are liquidity, savings and debt and such aspects would be considered in the ratios which

are computed. The liquidity ratios are considered for the business and the computation of current

ratio for the family is shown below:

Current Ratio = Current Assets/ Current Liabilities

=16800/2925

= 5.74

The current ratio which is computed above shows that the liquidity position for the family

is significant better and the same suggest that the business has appropriate sources of funds for

the purpose of undertaking the financial plan effectively. It can be further argued that the

liquidity of the family is extremely well as the same estimate is above the ideal level. The

Greg Sharon

CPP death benefit 2,500.00 800.00

Maximum CPP benefit at age 65 (current, but

indexed to inflation)

801.00 165.00

Expected inflation rate 2.5%

Expected average, pre-tax, nominal return on all

sheltered and unsheltered investments including

employer pension plan

6.0%

Estimated funeral expenses 10,000.00

Step 2: Ratio Analysis

The nest step in the financial planning process is the computation of the key financial

ratios which are associated with the business. The three major areas which are to be assess for

this part are liquidity, savings and debt and such aspects would be considered in the ratios which

are computed. The liquidity ratios are considered for the business and the computation of current

ratio for the family is shown below:

Current Ratio = Current Assets/ Current Liabilities

=16800/2925

= 5.74

The current ratio which is computed above shows that the liquidity position for the family

is significant better and the same suggest that the business has appropriate sources of funds for

the purpose of undertaking the financial plan effectively. It can be further argued that the

liquidity of the family is extremely well as the same estimate is above the ideal level. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

liquidity ratio of the family also shows the currents assets is significantly more than the current

liabilities which suggest that the business has financial strength and the family can effectively

cover its expenses for a given period of time provided the liquidity estimates are maintained by

the business.

The current ratio also shows the ability of the family to meet the current expenses and

obligation and the estimate which is computed for Allen Family is appropriate.

Debt Ratios

Total Debt ratio = Total debt / Total assets

= 120000/245950

= 0.49 or 49%

The total debt figure is shown to be 49% of the total asset figure as per the computations

which are shown in the above figure. The debt figure is shown to be high which suggest that the

family depends to a certain degree on the application of debt capital for financing the activities

and requirements of the family in pursuance of the goals. Allen Family is shown to have

significant amount of debts which is almost equal in terms of percentage to the assets of the

family.

Investment Ratios

The investment ratios are computed on the basis of the investments which are made by

the family in various insurances and the same is assessed whether the same is appropriate or not.

Investing to Net Income after Deductions ratio = Cash flow available for investing / Net income

after deductions

The above is shown to establish as relationship between the cash flow from investing

activities and net income which can be computed for the Family. The ratio analysis shows the

liquidity ratio of the family also shows the currents assets is significantly more than the current

liabilities which suggest that the business has financial strength and the family can effectively

cover its expenses for a given period of time provided the liquidity estimates are maintained by

the business.

The current ratio also shows the ability of the family to meet the current expenses and

obligation and the estimate which is computed for Allen Family is appropriate.

Debt Ratios

Total Debt ratio = Total debt / Total assets

= 120000/245950

= 0.49 or 49%

The total debt figure is shown to be 49% of the total asset figure as per the computations

which are shown in the above figure. The debt figure is shown to be high which suggest that the

family depends to a certain degree on the application of debt capital for financing the activities

and requirements of the family in pursuance of the goals. Allen Family is shown to have

significant amount of debts which is almost equal in terms of percentage to the assets of the

family.

Investment Ratios

The investment ratios are computed on the basis of the investments which are made by

the family in various insurances and the same is assessed whether the same is appropriate or not.

Investing to Net Income after Deductions ratio = Cash flow available for investing / Net income

after deductions

The above is shown to establish as relationship between the cash flow from investing

activities and net income which can be computed for the Family. The ratio analysis shows the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

Allen’s have the ability to cover their short- and long-term obligations, a large amount of debt

capacity, and perhaps too much invested in liquid assets with too little return. The liquidity ratios

which is computed for the family is favourable and therefore can cover all obligations. The

family uses too much debt capital which is also clear from the ratio analysis which is computed

for the family.

Tax Planning

Greg have made certain investments in funds which would be providing the family with tax

benefits. Greg Has investments in pension plan which is provided by the employer of his business

but also has an RRSP and 10 years government bonds which would count as investments which

have made by the family and therefore would be subjected to tax deductions. The case shows that

Sharon has not made any investments in RRSP funds and most of the investments have been made

by Greg. The family would be eligible for deductions for all consumption expenses and direct

expenses of the family and therefore would be getting tax benefits. In addition to this, the family

can claim deduction for travel expenses which forms an important part of Greg’s work. The couple

has also taken loan during the period for which the employee can claim more deduction from the

total taxable income of the employee.

The Allen Family needs to effectively split their incomes in order to take advantage of tax

benefits and the same strategy is provided below:

Greg needs to pay Sharon for any work which is done by her which can be advisory or

even as a simple book keeping as this would effectively split the income of Greg and would

provide tax advantage during the time of computation of the same.

Allen’s have the ability to cover their short- and long-term obligations, a large amount of debt

capacity, and perhaps too much invested in liquid assets with too little return. The liquidity ratios

which is computed for the family is favourable and therefore can cover all obligations. The

family uses too much debt capital which is also clear from the ratio analysis which is computed

for the family.

Tax Planning

Greg have made certain investments in funds which would be providing the family with tax

benefits. Greg Has investments in pension plan which is provided by the employer of his business

but also has an RRSP and 10 years government bonds which would count as investments which

have made by the family and therefore would be subjected to tax deductions. The case shows that

Sharon has not made any investments in RRSP funds and most of the investments have been made

by Greg. The family would be eligible for deductions for all consumption expenses and direct

expenses of the family and therefore would be getting tax benefits. In addition to this, the family

can claim deduction for travel expenses which forms an important part of Greg’s work. The couple

has also taken loan during the period for which the employee can claim more deduction from the

total taxable income of the employee.

The Allen Family needs to effectively split their incomes in order to take advantage of tax

benefits and the same strategy is provided below:

Greg needs to pay Sharon for any work which is done by her which can be advisory or

even as a simple book keeping as this would effectively split the income of Greg and would

provide tax advantage during the time of computation of the same.

8FINANCE

Sharon is also eligible for medical credit as she fall under the category of lower income

group and a lesser amount will be deducted from legitimate medical expenses in arriving at

allowable medical expenses.

The household expenses should be paid by Greg and Sharon should invest her earnings

which would attract lower rate of taxes for the family. The finances of both Greg and

Sharon needs to be kept separately so that they can effectively support this strategy.

The Allen Family also needs to consider strategies which is related to RRSP and the same is

given below in details:

If either has any RRSP carry-forward room, they should maximize their RRSP

contributions which would be beneficial for the business.

Where RRSP and spousal RRSP contributions have been maximized to reduce taxable

income and create income tax splitting during retirement, TFSAs should be used to keep

investment income tax free up to the limits available for each of Greg and Sharon. Any

capital gain on the GHI stock will have to be claimed before it is contributed in-kind to the

RRSP.

In order to ensure tax efficiency, the IMCanadian Equity Fund could be moved out of the

RRSP and GICs swapped in by the Allen Family.

Debt and Cash Management

The debt and cash management need to be effectively carried out by the Allen Family.

The plan of the family is to make the mortgage payment earlier than the due date. The period

which is actually left for the mortgage is 3 years while the family intends to settle the mortgage

within 2 years period. The mortgage was originally taken for an amortization period of 15 years

but the same is being covered for a period of 12 years. The family also has an offer for taking a

Sharon is also eligible for medical credit as she fall under the category of lower income

group and a lesser amount will be deducted from legitimate medical expenses in arriving at

allowable medical expenses.

The household expenses should be paid by Greg and Sharon should invest her earnings

which would attract lower rate of taxes for the family. The finances of both Greg and

Sharon needs to be kept separately so that they can effectively support this strategy.

The Allen Family also needs to consider strategies which is related to RRSP and the same is

given below in details:

If either has any RRSP carry-forward room, they should maximize their RRSP

contributions which would be beneficial for the business.

Where RRSP and spousal RRSP contributions have been maximized to reduce taxable

income and create income tax splitting during retirement, TFSAs should be used to keep

investment income tax free up to the limits available for each of Greg and Sharon. Any

capital gain on the GHI stock will have to be claimed before it is contributed in-kind to the

RRSP.

In order to ensure tax efficiency, the IMCanadian Equity Fund could be moved out of the

RRSP and GICs swapped in by the Allen Family.

Debt and Cash Management

The debt and cash management need to be effectively carried out by the Allen Family.

The plan of the family is to make the mortgage payment earlier than the due date. The period

which is actually left for the mortgage is 3 years while the family intends to settle the mortgage

within 2 years period. The mortgage was originally taken for an amortization period of 15 years

but the same is being covered for a period of 12 years. The family also has an offer for taking a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

car loan which is offered by the employer of Greg. The car which is being offered on loan is a

second-hand car and the same

Car Loan

The family also intends to take a car loan which is represented in the financial statements

which is prepared for the family. Having a new car is one of the goals which is identified for the

business.

Credit Card Debt

Both Greg and Sharon have credit cards which has a debt and the same attracts interest at

the rate of 19.9%. The case shows that the couple do not use their credit cards most of the times

as they do not like such debts. The strategy which is applied by the couple is appropriate as they

can easily meet their obligations without bearing additional interest on the credit cards which is

being offered.

Cash Management

The cash flow statement for the family is prepared in order to shows the cash inflows and

outflows of the business and how the same can have an impact on the operations of the business.

The family has invested significantly in different kinds of registered and non-registered funds as

presented in the balance of the family. The family still has an amount of $ 15000 for Greg in

Cheque Account while an amount of $ 1800 is shown to be present in the savings account of

Sharon. The couple may use such amounts also for the purpose of investments in some funds. In

case of any emergency Greg can always rely on 5-year locked-in GICs and Canada Savings

Bonds.

Risk Management and Insurance

General Insurance

car loan which is offered by the employer of Greg. The car which is being offered on loan is a

second-hand car and the same

Car Loan

The family also intends to take a car loan which is represented in the financial statements

which is prepared for the family. Having a new car is one of the goals which is identified for the

business.

Credit Card Debt

Both Greg and Sharon have credit cards which has a debt and the same attracts interest at

the rate of 19.9%. The case shows that the couple do not use their credit cards most of the times

as they do not like such debts. The strategy which is applied by the couple is appropriate as they

can easily meet their obligations without bearing additional interest on the credit cards which is

being offered.

Cash Management

The cash flow statement for the family is prepared in order to shows the cash inflows and

outflows of the business and how the same can have an impact on the operations of the business.

The family has invested significantly in different kinds of registered and non-registered funds as

presented in the balance of the family. The family still has an amount of $ 15000 for Greg in

Cheque Account while an amount of $ 1800 is shown to be present in the savings account of

Sharon. The couple may use such amounts also for the purpose of investments in some funds. In

case of any emergency Greg can always rely on 5-year locked-in GICs and Canada Savings

Bonds.

Risk Management and Insurance

General Insurance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

The general insurance coverage of Greg is provided by the employer and the same is

provided to a maximum of three times of Greg’s salary and in addition to this Greg has also

purchased general insurance which is twice as much as his salary. The assumption which can be

made is that the general insurance which is available with Greg is appropriate but the major risk

which can be identified with the same is related to the coverage which it provides and the same

needs to be assessed before any new insurance is purchased. It is also required to be assessed

whether the same can cover Sharon appropriately or not.

Disability Coverage

One of the major risks which is faced by Greg is of accidents due to the nature of work

which is carried out by Greg. The nature of such accidents is so frequent that the employer does

not provide any Disability Coverage. Greg is covered by a insurance package which was purchased

by him, however, it would have been better if the disability co0verage was provided. The

assessment of the policies also does not clearly specify whether Sharon would have covered by

such disability coverage.

Investment Management

One of the major things which needs to be cleared with Greg is that the diversification of

portfolio is to be made appropriately. The portfolio should be shown as one and not as secured

and unsecured securities. Greg also has made investment in Government Bonds which are

providing an interest rate of 6% and has 6 years left for the maturity for the same.

In addition to this, Greg should start trading in stocks which is held by him. As the value

of the stock decrease, it is always the right move to sell of the stock rather than hold the same

with an expectation of rise in the value for the same.

Risk tolerance and investment objectives

The general insurance coverage of Greg is provided by the employer and the same is

provided to a maximum of three times of Greg’s salary and in addition to this Greg has also

purchased general insurance which is twice as much as his salary. The assumption which can be

made is that the general insurance which is available with Greg is appropriate but the major risk

which can be identified with the same is related to the coverage which it provides and the same

needs to be assessed before any new insurance is purchased. It is also required to be assessed

whether the same can cover Sharon appropriately or not.

Disability Coverage

One of the major risks which is faced by Greg is of accidents due to the nature of work

which is carried out by Greg. The nature of such accidents is so frequent that the employer does

not provide any Disability Coverage. Greg is covered by a insurance package which was purchased

by him, however, it would have been better if the disability co0verage was provided. The

assessment of the policies also does not clearly specify whether Sharon would have covered by

such disability coverage.

Investment Management

One of the major things which needs to be cleared with Greg is that the diversification of

portfolio is to be made appropriately. The portfolio should be shown as one and not as secured

and unsecured securities. Greg also has made investment in Government Bonds which are

providing an interest rate of 6% and has 6 years left for the maturity for the same.

In addition to this, Greg should start trading in stocks which is held by him. As the value

of the stock decrease, it is always the right move to sell of the stock rather than hold the same

with an expectation of rise in the value for the same.

Risk tolerance and investment objectives

11FINANCE

There is no direct knowledge of the tolerance of risks for Greg but it can be judged from

the financial position of the family and the net worth which is computed, it can be said that the

family is in a strong position and therefore can take risks and make investments in more equities

in order to enhance the wealth of the family. The retirement age of Greg is also good and

therefore Greg should definitely take more risks.

The case shows that the Allen family can take more risks by investing more in equity but

they are shown to be uncomfortable with the same and therefore, it is up to them as they can

avoid more risky investments.

Retirement Planning

The plan of Greg is to retire at the age of 60 years and he plans to provide for 25 years’

worth income which would be received by the family post retirement. The opinion of Greg is

that the couple needs 60% of the current years for the purpose of making the life after retirement

smoother. The retirement plan has been formulated on the basis of a forecasted life span for both

Greg and Sharon being considered. The major risk would arise if one or both of the outlive their

estimated life span which would result in shortage of money during retirement. This can be

considered as a serious risk to the plans which is formulated by the family.

Estate Planning

The Allen family can undertake the following steps for the purpose of planning for the

estate:

Firstly, they should have wills. Their assumption about the distribution of assets would be

appropriately done if either one or both them die in case of a will. The assets of the

family would be distributed according to the intestate laws of the province they live in

There is no direct knowledge of the tolerance of risks for Greg but it can be judged from

the financial position of the family and the net worth which is computed, it can be said that the

family is in a strong position and therefore can take risks and make investments in more equities

in order to enhance the wealth of the family. The retirement age of Greg is also good and

therefore Greg should definitely take more risks.

The case shows that the Allen family can take more risks by investing more in equity but

they are shown to be uncomfortable with the same and therefore, it is up to them as they can

avoid more risky investments.

Retirement Planning

The plan of Greg is to retire at the age of 60 years and he plans to provide for 25 years’

worth income which would be received by the family post retirement. The opinion of Greg is

that the couple needs 60% of the current years for the purpose of making the life after retirement

smoother. The retirement plan has been formulated on the basis of a forecasted life span for both

Greg and Sharon being considered. The major risk would arise if one or both of the outlive their

estimated life span which would result in shortage of money during retirement. This can be

considered as a serious risk to the plans which is formulated by the family.

Estate Planning

The Allen family can undertake the following steps for the purpose of planning for the

estate:

Firstly, they should have wills. Their assumption about the distribution of assets would be

appropriately done if either one or both them die in case of a will. The assets of the

family would be distributed according to the intestate laws of the province they live in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.