ACC00716 Finance Assignment: Risk and Return Analysis and CAPM

VerifiedAdded on 2023/01/23

|11

|1609

|73

Report

AI Summary

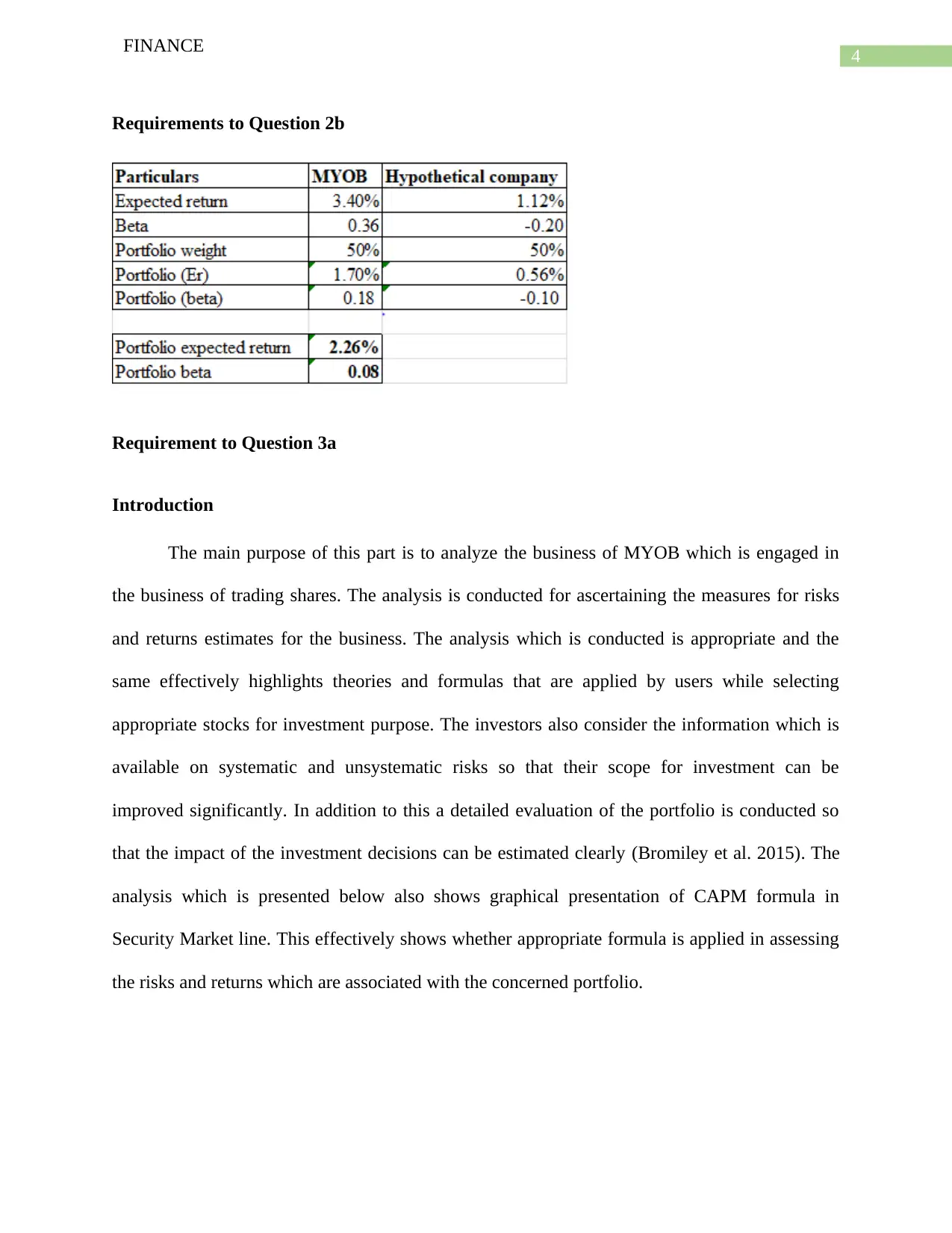

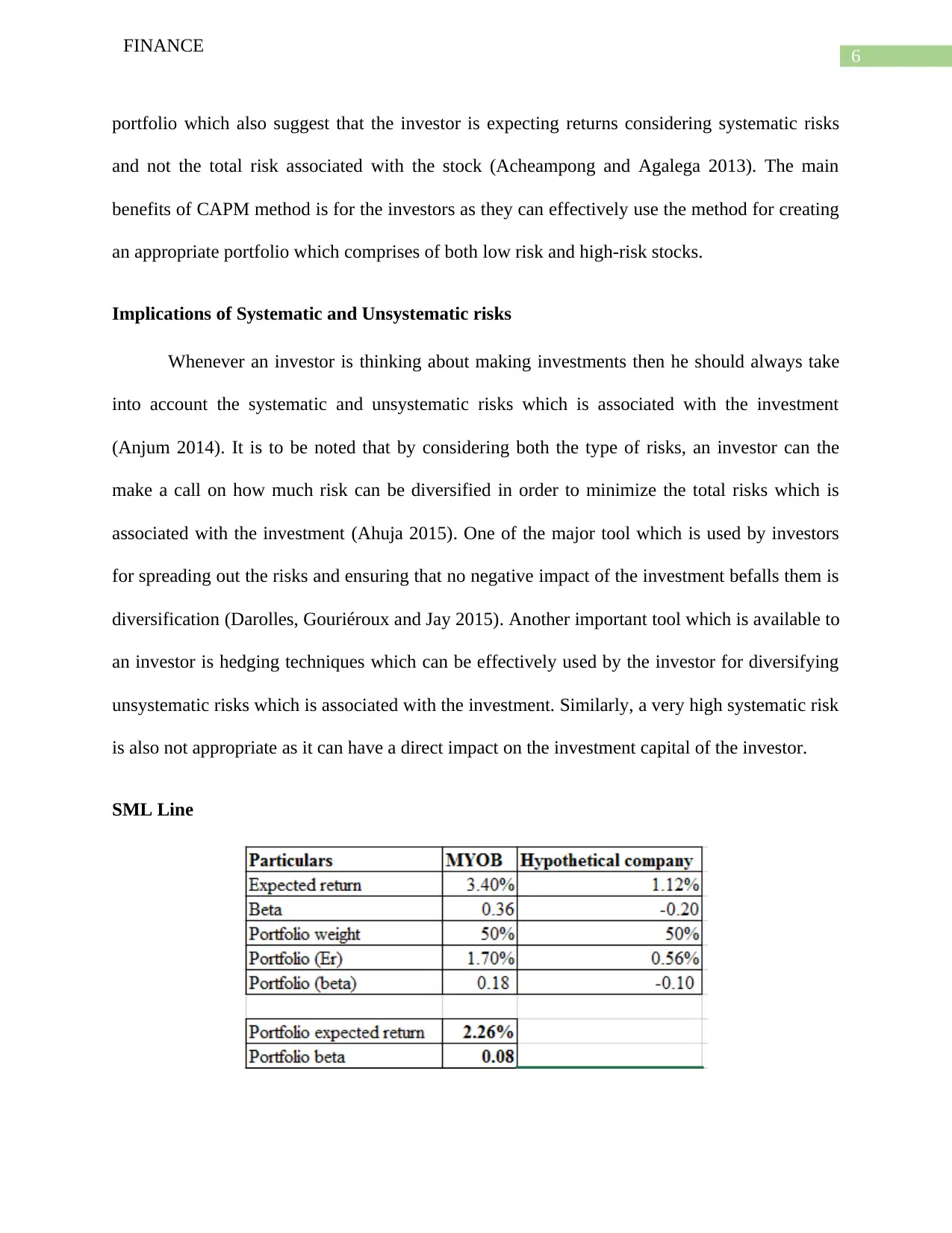

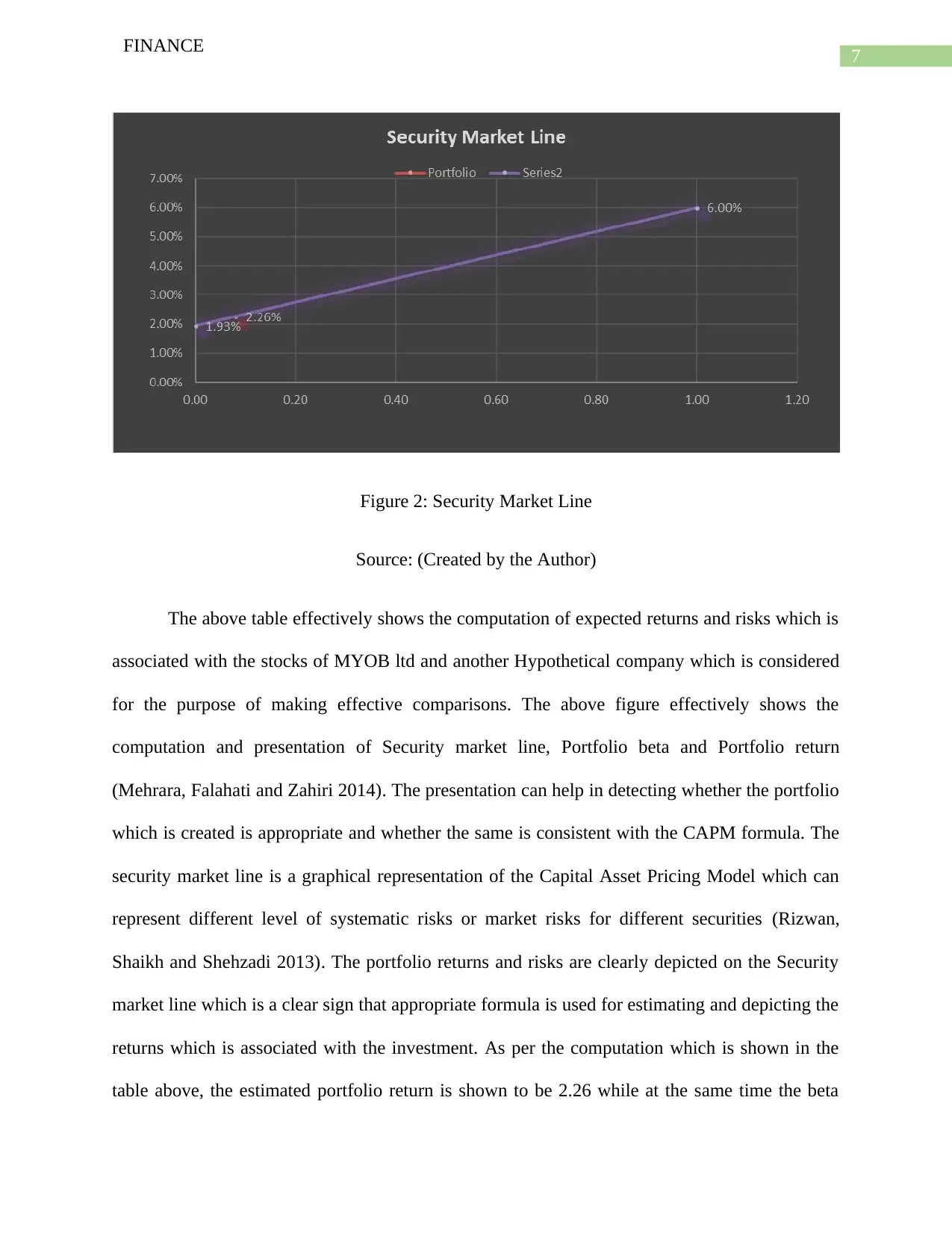

This finance report analyzes the business of MYOB, focusing on risk and return assessment for investment decisions. It applies the Capital Asset Pricing Model (CAPM) to evaluate risks and returns, considering both systematic and unsystematic risks, and includes a graphical representation of the Security Market Line (SML). The report explains the CAPM formula, its application in portfolio creation, and the implications of different types of risks. The analysis aims to determine the relationship between systematic risks and expected returns, assisting investors in making informed decisions. The report provides a detailed evaluation of the portfolio, demonstrating how the CAPM formula and SML can be used to assess the risks and returns associated with an investment portfolio. The conclusion emphasizes the importance of managing risks through portfolio diversification and the use of appropriate financial models like CAPM to optimize investment strategies.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.