Corporate Governance and Liquidity Ratios for BUSINESS

VerifiedAdded on 2021/06/17

|20

|3984

|87

AI Summary

FINANCE FOR BUSINESS FINANCE FOR BUSINESS 19 19 Finance for Business Name of the Student Name of the University Authors Note Course ID Introduction: 2 Description of the Company: 2 Corporate Governance Structure and Ownership: 3 Substantial Shareholdings: 3 Major people involved in the governance of the Firm: 4 Calculations of the Fundamental Ratios: 5 Liquidity Ratios: 5 Financial Leverage Ratios: 6 Efficiency Ratio: 6 Profitability Ratios: 7 Market Value Ratios: 7 Description of Results through

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE FOR BUSINESS

Finance for Business

Name of the Student

Name of the University

Authors Note

Course ID

Finance for Business

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCE FOR BUSINESS

Table of Contents

Introduction:...............................................................................................................................2

Description of the Company:.....................................................................................................2

Corporate Governance Structure and Ownership:.....................................................................3

Substantial Shareholdings:.....................................................................................................3

Major people involved in the governance of the Firm:..........................................................4

Calculations of the Fundamental Ratios:...................................................................................5

Liquidity Ratios:.....................................................................................................................5

Financial Leverage Ratios:.....................................................................................................6

Efficiency Ratio:....................................................................................................................6

Profitability Ratios:................................................................................................................7

Market Value Ratios:.............................................................................................................7

Description of Results through Share Price Movement:........................................................8

Significant factor influencing the share price movement of the company are stated below:....9

Calculations of the Beta values and the anticipated rate of return by employing CAPM:......10

Computation of Beta Values................................................................................................10

Computation of Required Rate of Return:...........................................................................10

Conservative Investment:.....................................................................................................11

Computation of the Weighted Average Cost of Capital:.....................................................12

Implications of higher WACC on the management evaluations of investment prospects:..12

Debt ratio of KYCKR Ltd:.......................................................................................................13

Table of Contents

Introduction:...............................................................................................................................2

Description of the Company:.....................................................................................................2

Corporate Governance Structure and Ownership:.....................................................................3

Substantial Shareholdings:.....................................................................................................3

Major people involved in the governance of the Firm:..........................................................4

Calculations of the Fundamental Ratios:...................................................................................5

Liquidity Ratios:.....................................................................................................................5

Financial Leverage Ratios:.....................................................................................................6

Efficiency Ratio:....................................................................................................................6

Profitability Ratios:................................................................................................................7

Market Value Ratios:.............................................................................................................7

Description of Results through Share Price Movement:........................................................8

Significant factor influencing the share price movement of the company are stated below:....9

Calculations of the Beta values and the anticipated rate of return by employing CAPM:......10

Computation of Beta Values................................................................................................10

Computation of Required Rate of Return:...........................................................................10

Conservative Investment:.....................................................................................................11

Computation of the Weighted Average Cost of Capital:.....................................................12

Implications of higher WACC on the management evaluations of investment prospects:..12

Debt ratio of KYCKR Ltd:.......................................................................................................13

2FINANCE FOR BUSINESS

Dividend Policy:.......................................................................................................................14

Letter of Recommendations:....................................................................................................14

Conclusion:..............................................................................................................................15

Reference list:...........................................................................................................................16

Dividend Policy:.......................................................................................................................14

Letter of Recommendations:....................................................................................................14

Conclusion:..............................................................................................................................15

Reference list:...........................................................................................................................16

3FINANCE FOR BUSINESS

Introduction:

The report is based on understanding the financial performance of the KYCKR Ltd

and providing the necessary financial advice to the investors so that a viability related to

sound investment can be provided. The report would be focusing on the segments of

ownership of the KYCKR Ltd along with a descriptive summary of the overall existence. To

better gauge into the financial performance of the KYCKR Ltd a computation of ratios has

been performed to understand the liquidity, profitability, solvency, market leverage and

gearing of KYCKR Ltd. The movement in the share prices would be reflected with the help

of the graphical description of the results for KYCKR Ltd.

The study would also place emphasis on the significant factors that would be creating

an influence on the share price of the KYCKR Ltd. Additionally, to support the identified

factors of share price movement a weighted average cost of capital will be computed that

would highlight the required the rate of return for KYCKR Ltd. Emphasis would also be

placed on the debt ratio for the KYCKR Ltd to understand whether the company has followed

debt structure in the management of its capital. Analysis of the dividend policy would be

made for KYCKR Ltd and a letter of recommendations would be provided to address the

potential investors regarding the viability of making investment in KYCKR Ltd.

Description of the Company:

KYCKR Ltd is regarded as the worldwide business register that is established in

Waterford, Ireland from the year 2007. KYCKR Ltd is controlled and publicly traded

company on the Australian Securities Exchange (Kyckr 2018). The business of KYCKR Ltd

began with the simple idea of creating a business for the customers that could obtain the

access in real time from several countries across the Europe. Ben Cronin and Robert Leslie

Introduction:

The report is based on understanding the financial performance of the KYCKR Ltd

and providing the necessary financial advice to the investors so that a viability related to

sound investment can be provided. The report would be focusing on the segments of

ownership of the KYCKR Ltd along with a descriptive summary of the overall existence. To

better gauge into the financial performance of the KYCKR Ltd a computation of ratios has

been performed to understand the liquidity, profitability, solvency, market leverage and

gearing of KYCKR Ltd. The movement in the share prices would be reflected with the help

of the graphical description of the results for KYCKR Ltd.

The study would also place emphasis on the significant factors that would be creating

an influence on the share price of the KYCKR Ltd. Additionally, to support the identified

factors of share price movement a weighted average cost of capital will be computed that

would highlight the required the rate of return for KYCKR Ltd. Emphasis would also be

placed on the debt ratio for the KYCKR Ltd to understand whether the company has followed

debt structure in the management of its capital. Analysis of the dividend policy would be

made for KYCKR Ltd and a letter of recommendations would be provided to address the

potential investors regarding the viability of making investment in KYCKR Ltd.

Description of the Company:

KYCKR Ltd is regarded as the worldwide business register that is established in

Waterford, Ireland from the year 2007. KYCKR Ltd is controlled and publicly traded

company on the Australian Securities Exchange (Kyckr 2018). The business of KYCKR Ltd

began with the simple idea of creating a business for the customers that could obtain the

access in real time from several countries across the Europe. Ben Cronin and Robert Leslie

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCE FOR BUSINESS

are regarded as the founder of the KYCKR Ltd with the initial idea of creating a Global

Business Register Limited in the year 2007.

The website of GBDR initially went live for the first time in the year 2009 went about

in eighteen European countries. From thereon, the company rapidly grew and turned out to be

leader in the providing the official live company information to electronically source the

single point admission (Kyckr 2018). The GBDR Direct recognized the rising demand for the

instant access of the real time company information that are sourced from registered business

across the world. The company became the largest authoritative company that searches the

company network that is available online and connects more than 150 business registries

across the world through API or the web portal.

Corporate Governance Structure and Ownership:

Substantial Shareholdings:

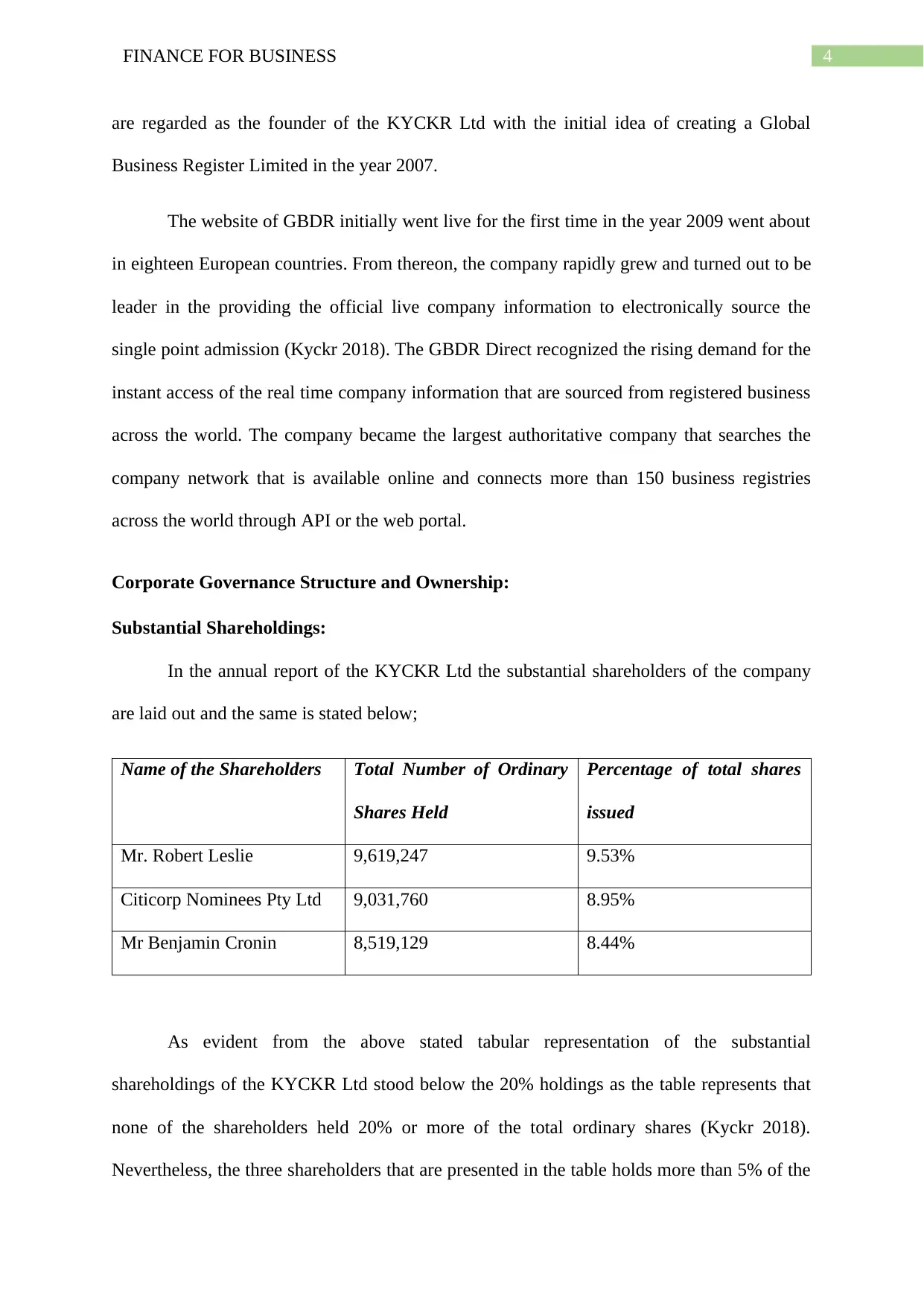

In the annual report of the KYCKR Ltd the substantial shareholders of the company

are laid out and the same is stated below;

Name of the Shareholders Total Number of Ordinary

Shares Held

Percentage of total shares

issued

Mr. Robert Leslie 9,619,247 9.53%

Citicorp Nominees Pty Ltd 9,031,760 8.95%

Mr Benjamin Cronin 8,519,129 8.44%

As evident from the above stated tabular representation of the substantial

shareholdings of the KYCKR Ltd stood below the 20% holdings as the table represents that

none of the shareholders held 20% or more of the total ordinary shares (Kyckr 2018).

Nevertheless, the three shareholders that are presented in the table holds more than 5% of the

are regarded as the founder of the KYCKR Ltd with the initial idea of creating a Global

Business Register Limited in the year 2007.

The website of GBDR initially went live for the first time in the year 2009 went about

in eighteen European countries. From thereon, the company rapidly grew and turned out to be

leader in the providing the official live company information to electronically source the

single point admission (Kyckr 2018). The GBDR Direct recognized the rising demand for the

instant access of the real time company information that are sourced from registered business

across the world. The company became the largest authoritative company that searches the

company network that is available online and connects more than 150 business registries

across the world through API or the web portal.

Corporate Governance Structure and Ownership:

Substantial Shareholdings:

In the annual report of the KYCKR Ltd the substantial shareholders of the company

are laid out and the same is stated below;

Name of the Shareholders Total Number of Ordinary

Shares Held

Percentage of total shares

issued

Mr. Robert Leslie 9,619,247 9.53%

Citicorp Nominees Pty Ltd 9,031,760 8.95%

Mr Benjamin Cronin 8,519,129 8.44%

As evident from the above stated tabular representation of the substantial

shareholdings of the KYCKR Ltd stood below the 20% holdings as the table represents that

none of the shareholders held 20% or more of the total ordinary shares (Kyckr 2018).

Nevertheless, the three shareholders that are presented in the table holds more than 5% of the

5FINANCE FOR BUSINESS

total ordinary shares. This included Mr Robert Leslie that held 9,619,247 number of total

ordinary shares and comprised of 9.53% of the total shares.

The Citicorp Nominees Pty Ltd held 9,031,760 of total ordinary shares and that

constituted 8.95% of the total shares that was issued (Kyckr 2018). Other shareholders

include Mr Benjamin Cronin held 8,519,129 held total number of shares that constituted

8.44% of the total shares. Based on the overall analysis of the substantial shareholdings an

argument can be bought forward by stating that the company cannot be classified as the

family company since none of the shareholders held more than 20% of the substantial shares

in KYCKR Ltd (Kyckr 2018). Additionally, the three substantial shareholders that stood for

the company held greater than 5% of the shares but not higher than 20% of the total shares.

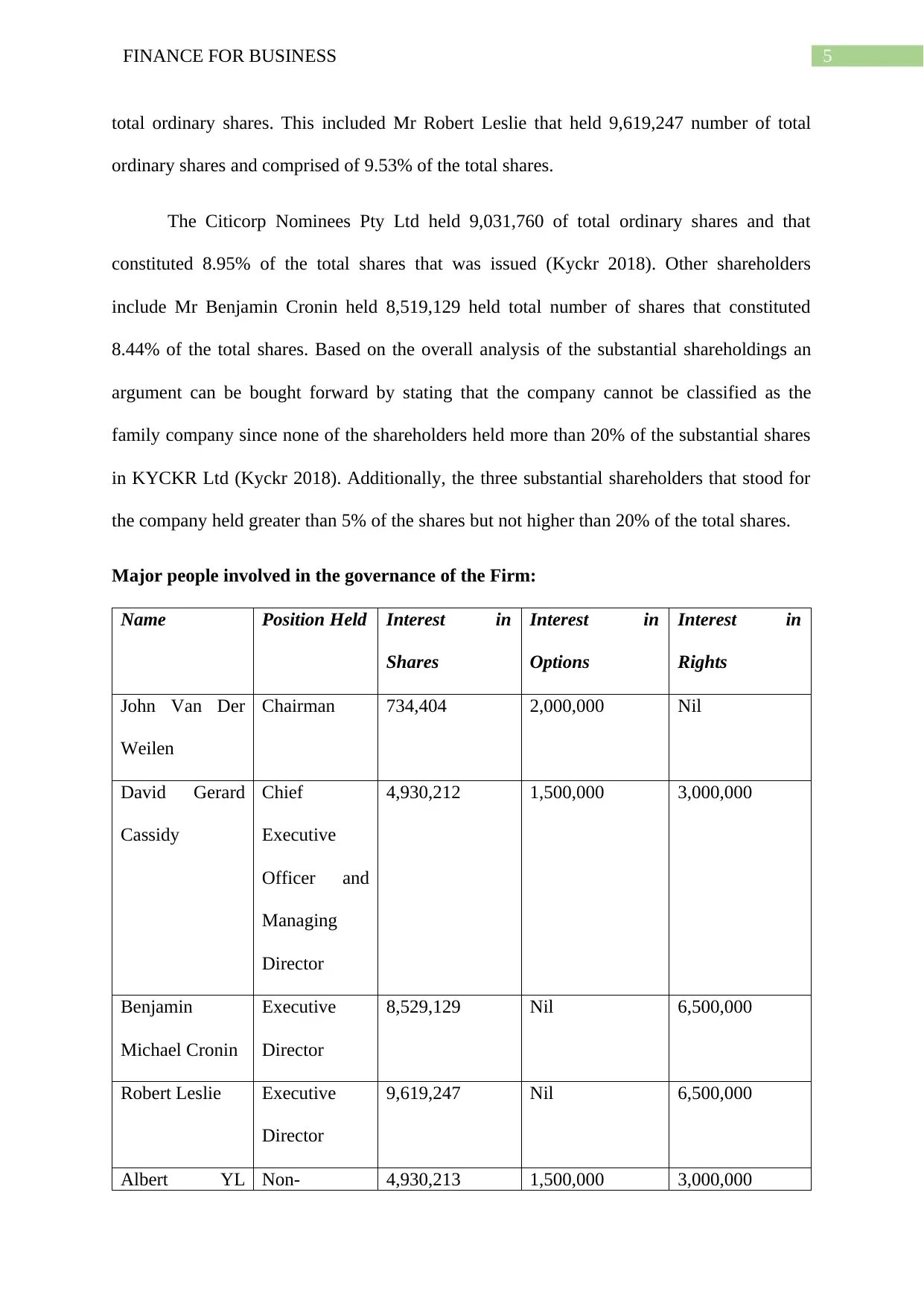

Major people involved in the governance of the Firm:

Name Position Held Interest in

Shares

Interest in

Options

Interest in

Rights

John Van Der

Weilen

Chairman 734,404 2,000,000 Nil

David Gerard

Cassidy

Chief

Executive

Officer and

Managing

Director

4,930,212 1,500,000 3,000,000

Benjamin

Michael Cronin

Executive

Director

8,529,129 Nil 6,500,000

Robert Leslie Executive

Director

9,619,247 Nil 6,500,000

Albert YL Non- 4,930,213 1,500,000 3,000,000

total ordinary shares. This included Mr Robert Leslie that held 9,619,247 number of total

ordinary shares and comprised of 9.53% of the total shares.

The Citicorp Nominees Pty Ltd held 9,031,760 of total ordinary shares and that

constituted 8.95% of the total shares that was issued (Kyckr 2018). Other shareholders

include Mr Benjamin Cronin held 8,519,129 held total number of shares that constituted

8.44% of the total shares. Based on the overall analysis of the substantial shareholdings an

argument can be bought forward by stating that the company cannot be classified as the

family company since none of the shareholders held more than 20% of the substantial shares

in KYCKR Ltd (Kyckr 2018). Additionally, the three substantial shareholders that stood for

the company held greater than 5% of the shares but not higher than 20% of the total shares.

Major people involved in the governance of the Firm:

Name Position Held Interest in

Shares

Interest in

Options

Interest in

Rights

John Van Der

Weilen

Chairman 734,404 2,000,000 Nil

David Gerard

Cassidy

Chief

Executive

Officer and

Managing

Director

4,930,212 1,500,000 3,000,000

Benjamin

Michael Cronin

Executive

Director

8,529,129 Nil 6,500,000

Robert Leslie Executive

Director

9,619,247 Nil 6,500,000

Albert YL Non- 4,930,213 1,500,000 3,000,000

6FINANCE FOR BUSINESS

Wong AM Executive

Director

John Walsh Non-

Executive

Director

300,000 Nil Nil

Patrick Curry

O.B.E

Non-

Executive

Director

Nil 1,000,000 Nil

As evident from the above stated table it can be stated that main people that are

involved in the governance structure of the company does not hold more than 20% of the

shareholdings. An argument can be presented by stating that there is no such presence of

family members in the corporate governance of the company (Kyckr 2018). Additionally,

only Robert Leslie and Benjamin Cronin held more than 5% of the total shareholdings in the

corporate governance of the company with each holding 9.53% and 8.44% of the total

shareholdings.

Calculations of the Fundamental Ratios:

Liquidity Ratios:

Particulars` 2017 2016

$000 $000

Current Assets A 2967672.0 656304.0

Current Liabilities B 469170.0 146585.0

Inventory C Nil Nil

Prepayments & Other Assets D 101268.0 181344.0

Cash & Cash equivalents E 2670859.0 266943.0

Current Ratio F=A/B 6.33 4.48

Quick Ratio G=(A-C-D)/B 6.11 3.24

Cash Ratio H=E/B 5.69 1.82

Wong AM Executive

Director

John Walsh Non-

Executive

Director

300,000 Nil Nil

Patrick Curry

O.B.E

Non-

Executive

Director

Nil 1,000,000 Nil

As evident from the above stated table it can be stated that main people that are

involved in the governance structure of the company does not hold more than 20% of the

shareholdings. An argument can be presented by stating that there is no such presence of

family members in the corporate governance of the company (Kyckr 2018). Additionally,

only Robert Leslie and Benjamin Cronin held more than 5% of the total shareholdings in the

corporate governance of the company with each holding 9.53% and 8.44% of the total

shareholdings.

Calculations of the Fundamental Ratios:

Liquidity Ratios:

Particulars` 2017 2016

$000 $000

Current Assets A 2967672.0 656304.0

Current Liabilities B 469170.0 146585.0

Inventory C Nil Nil

Prepayments & Other Assets D 101268.0 181344.0

Cash & Cash equivalents E 2670859.0 266943.0

Current Ratio F=A/B 6.33 4.48

Quick Ratio G=(A-C-D)/B 6.11 3.24

Cash Ratio H=E/B 5.69 1.82

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR BUSINESS

Table 1: Table highlighting Liquidity Ratios of KYCKR Ltd

(Source: As Created by Author)

Financial Leverage Ratios:

Particulars` 2017 2016

$m $m

Total Assets A 15314948.0 817743.0

Total Equity B 12289456.0 671158.0

Total Liabilities C 3025492.0 146585.0

Debt-to-Equity Ratio D=C/B 0.25 0.22

Debt Ratio E=C/A 0.198 0.179

Equity Ratio F=B/A 0.802 0.821

Table 2: Table highlighting Financial Ratios of KYCKR Ltd

(Source: As Created by Author)

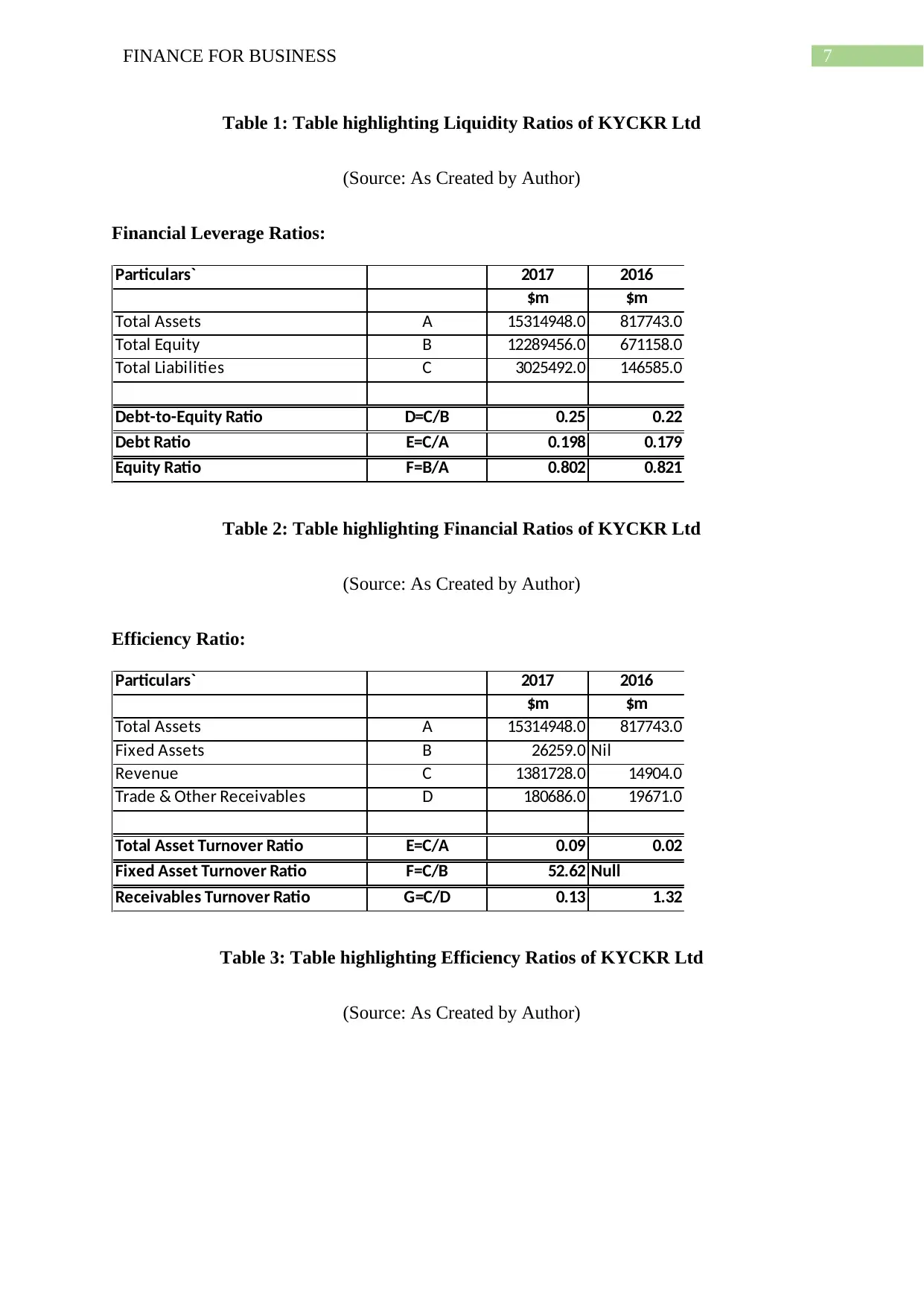

Efficiency Ratio:

Particulars` 2017 2016

$m $m

Total Assets A 15314948.0 817743.0

Fixed Assets B 26259.0 Nil

Revenue C 1381728.0 14904.0

Trade & Other Receivables D 180686.0 19671.0

Total Asset Turnover Ratio E=C/A 0.09 0.02

Fixed Asset Turnover Ratio F=C/B 52.62 Null

Receivables Turnover Ratio G=C/D 0.13 1.32

Table 3: Table highlighting Efficiency Ratios of KYCKR Ltd

(Source: As Created by Author)

Table 1: Table highlighting Liquidity Ratios of KYCKR Ltd

(Source: As Created by Author)

Financial Leverage Ratios:

Particulars` 2017 2016

$m $m

Total Assets A 15314948.0 817743.0

Total Equity B 12289456.0 671158.0

Total Liabilities C 3025492.0 146585.0

Debt-to-Equity Ratio D=C/B 0.25 0.22

Debt Ratio E=C/A 0.198 0.179

Equity Ratio F=B/A 0.802 0.821

Table 2: Table highlighting Financial Ratios of KYCKR Ltd

(Source: As Created by Author)

Efficiency Ratio:

Particulars` 2017 2016

$m $m

Total Assets A 15314948.0 817743.0

Fixed Assets B 26259.0 Nil

Revenue C 1381728.0 14904.0

Trade & Other Receivables D 180686.0 19671.0

Total Asset Turnover Ratio E=C/A 0.09 0.02

Fixed Asset Turnover Ratio F=C/B 52.62 Null

Receivables Turnover Ratio G=C/D 0.13 1.32

Table 3: Table highlighting Efficiency Ratios of KYCKR Ltd

(Source: As Created by Author)

8FINANCE FOR BUSINESS

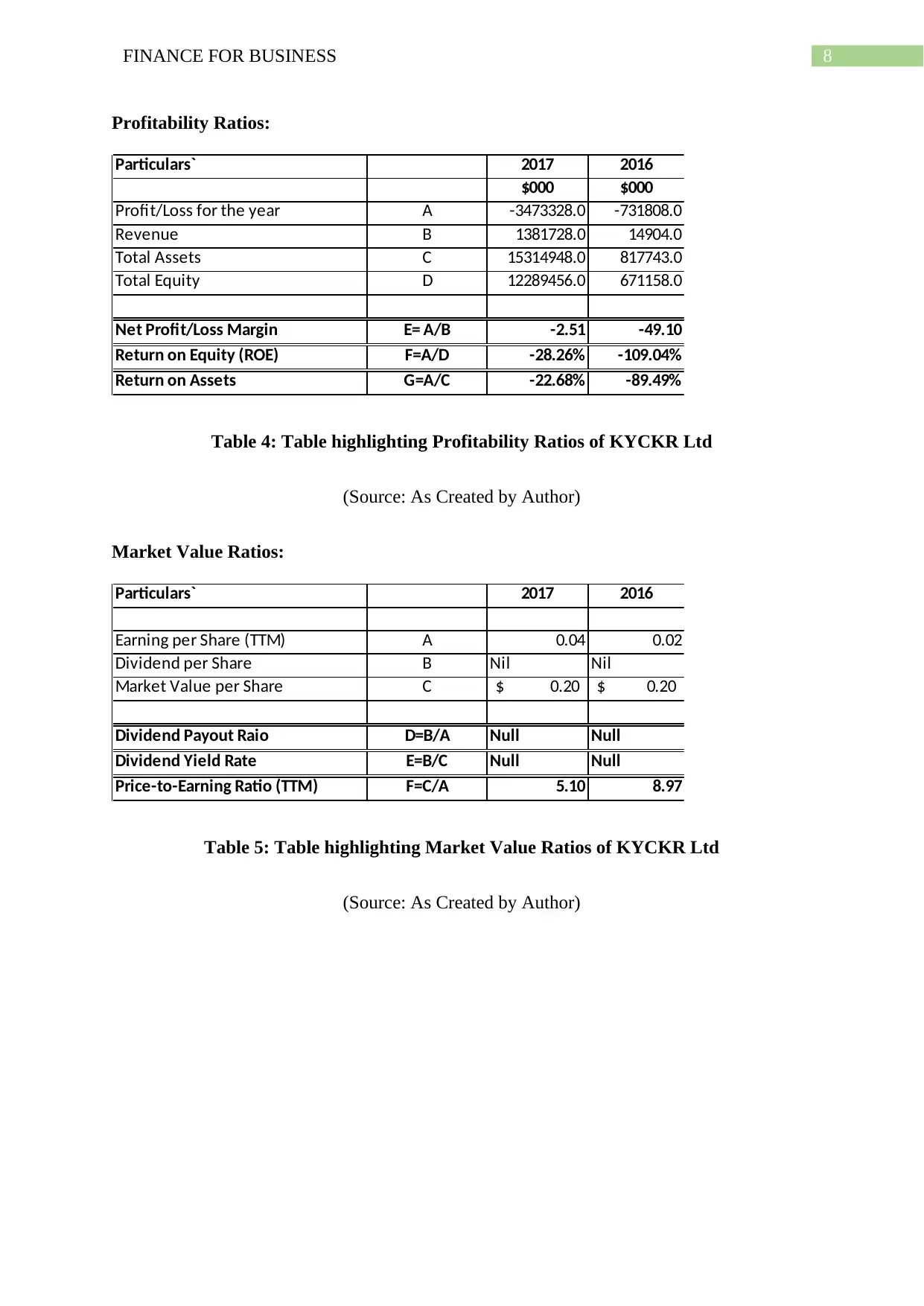

Profitability Ratios:

Particulars` 2017 2016

$000 $000

Profit/Loss for the year A -3473328.0 -731808.0

Revenue B 1381728.0 14904.0

Total Assets C 15314948.0 817743.0

Total Equity D 12289456.0 671158.0

Net Profit/Loss Margin E= A/B -2.51 -49.10

Return on Equity (ROE) F=A/D -28.26% -109.04%

Return on Assets G=A/C -22.68% -89.49%

Table 4: Table highlighting Profitability Ratios of KYCKR Ltd

(Source: As Created by Author)

Market Value Ratios:

Particulars` 2017 2016

Earning per Share (TTM) A 0.04 0.02

Dividend per Share B Nil Nil

Market Value per Share C 0.20$ 0.20$

Dividend Payout Raio D=B/A Null Null

Dividend Yield Rate E=B/C Null Null

Price-to-Earning Ratio (TTM) F=C/A 5.10 8.97

Table 5: Table highlighting Market Value Ratios of KYCKR Ltd

(Source: As Created by Author)

Profitability Ratios:

Particulars` 2017 2016

$000 $000

Profit/Loss for the year A -3473328.0 -731808.0

Revenue B 1381728.0 14904.0

Total Assets C 15314948.0 817743.0

Total Equity D 12289456.0 671158.0

Net Profit/Loss Margin E= A/B -2.51 -49.10

Return on Equity (ROE) F=A/D -28.26% -109.04%

Return on Assets G=A/C -22.68% -89.49%

Table 4: Table highlighting Profitability Ratios of KYCKR Ltd

(Source: As Created by Author)

Market Value Ratios:

Particulars` 2017 2016

Earning per Share (TTM) A 0.04 0.02

Dividend per Share B Nil Nil

Market Value per Share C 0.20$ 0.20$

Dividend Payout Raio D=B/A Null Null

Dividend Yield Rate E=B/C Null Null

Price-to-Earning Ratio (TTM) F=C/A 5.10 8.97

Table 5: Table highlighting Market Value Ratios of KYCKR Ltd

(Source: As Created by Author)

9FINANCE FOR BUSINESS

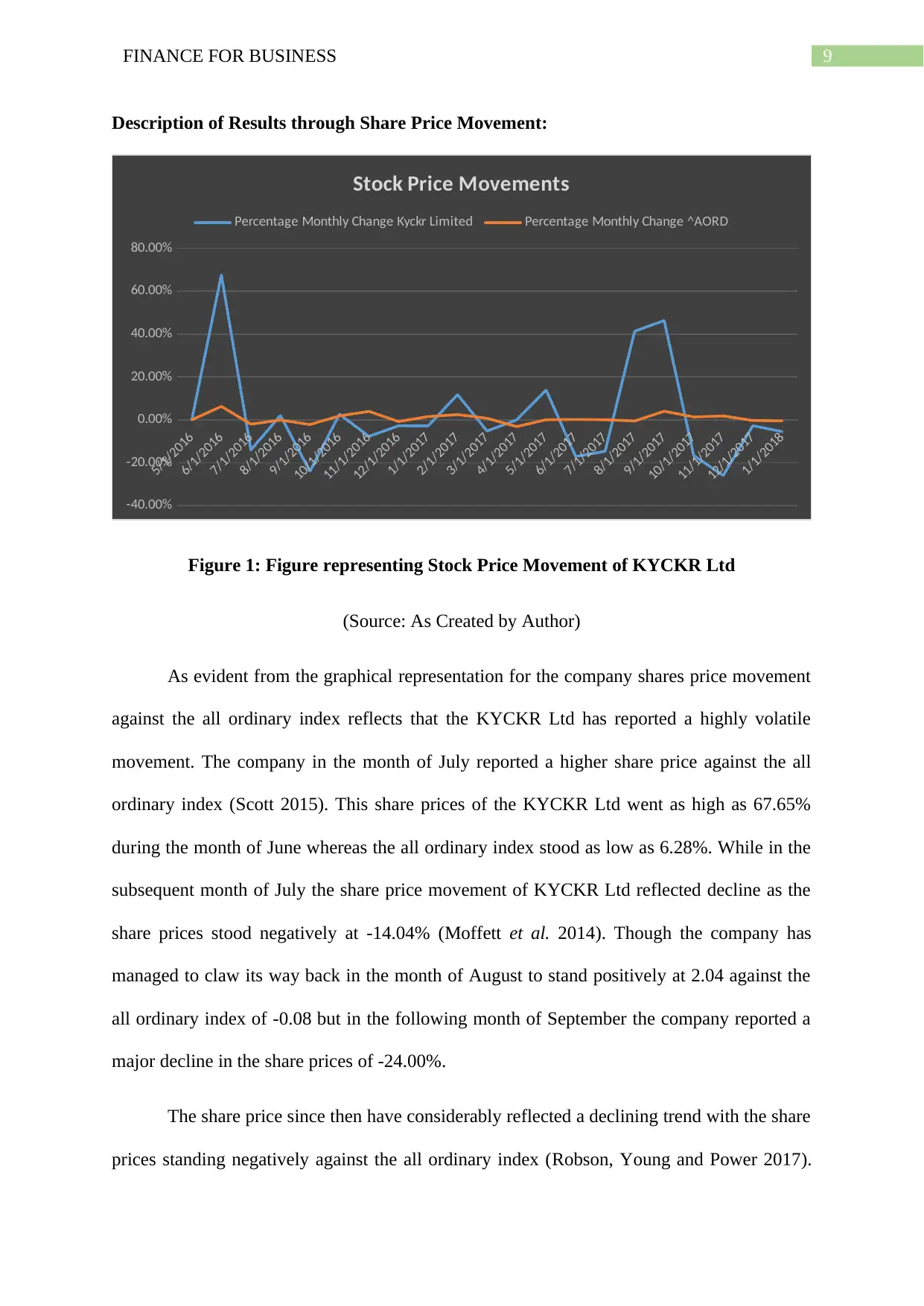

Description of Results through Share Price Movement:

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

1/1/2017

2/1/2017

3/1/2017

4/1/2017

5/1/2017

6/1/2017

7/1/2017

8/1/2017

9/1/2017

10/1/2017

11/1/2017

12/1/2017

1/1/2018

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

Stock Price Movements

Percentage Monthly Change Kyckr Limited Percentage Monthly Change ^AORD

Figure 1: Figure representing Stock Price Movement of KYCKR Ltd

(Source: As Created by Author)

As evident from the graphical representation for the company shares price movement

against the all ordinary index reflects that the KYCKR Ltd has reported a highly volatile

movement. The company in the month of July reported a higher share price against the all

ordinary index (Scott 2015). This share prices of the KYCKR Ltd went as high as 67.65%

during the month of June whereas the all ordinary index stood as low as 6.28%. While in the

subsequent month of July the share price movement of KYCKR Ltd reflected decline as the

share prices stood negatively at -14.04% (Moffett et al. 2014). Though the company has

managed to claw its way back in the month of August to stand positively at 2.04 against the

all ordinary index of -0.08 but in the following month of September the company reported a

major decline in the share prices of -24.00%.

The share price since then have considerably reflected a declining trend with the share

prices standing negatively against the all ordinary index (Robson, Young and Power 2017).

Description of Results through Share Price Movement:

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

1/1/2017

2/1/2017

3/1/2017

4/1/2017

5/1/2017

6/1/2017

7/1/2017

8/1/2017

9/1/2017

10/1/2017

11/1/2017

12/1/2017

1/1/2018

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

Stock Price Movements

Percentage Monthly Change Kyckr Limited Percentage Monthly Change ^AORD

Figure 1: Figure representing Stock Price Movement of KYCKR Ltd

(Source: As Created by Author)

As evident from the graphical representation for the company shares price movement

against the all ordinary index reflects that the KYCKR Ltd has reported a highly volatile

movement. The company in the month of July reported a higher share price against the all

ordinary index (Scott 2015). This share prices of the KYCKR Ltd went as high as 67.65%

during the month of June whereas the all ordinary index stood as low as 6.28%. While in the

subsequent month of July the share price movement of KYCKR Ltd reflected decline as the

share prices stood negatively at -14.04% (Moffett et al. 2014). Though the company has

managed to claw its way back in the month of August to stand positively at 2.04 against the

all ordinary index of -0.08 but in the following month of September the company reported a

major decline in the share prices of -24.00%.

The share price since then have considerably reflected a declining trend with the share

prices standing negatively against the all ordinary index (Robson, Young and Power 2017).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCE FOR BUSINESS

The share prices throughout the course of 2016 stood negatively except in the month of June

where the company reported a highest positive share price movement against the all ordinary

index of 67.55 whereas the company also recorded as low as -24.00% in the month of

September. There is a higher amount of volatility in the share price movement throughout the

financial year of 2016 (Schaltegger and Burritt 2017). Moving to the next financial year of

2017 the share price have reflected more or less the identical volatility as the company

recorded some positive as well as the negative instances of share price movement against the

all ordinary index.

The share price for the KYCKR Ltd in the month of February stood positively at

11.76% while in the following month of March 2017 the share price declined to negatively

stand at 5.26%. Instances obtained in the latter half of the financial year suggest that the share

price movement stood higher against the all ordinary index (Macve 2015). As in the month of

August 2017 the share price of KYCKR Ltd stood positively at 41.38% against the all

ordinary index of -0.54% after recording a low of -17.07% in the previous month of July at -

14.71%. In the subsequent month of September, the share prices increased to stand at 46.34%

while the all ordinary index stood 4.03% (Hoyle, Schaefer and Doupnik 2015). However, in

the later months the declining trend in share prices continued its way.

Significant factor influencing the share price movement of the company are stated

below:

There are certain important factor that govern the share price movement of the

company. This includes the change focus of the company. KYCKR Ltd has uniquely placed

its focus on the business of technology that provides the solution to the people to protect them

against the money laundering and fraud along with tax evasion (Martin and Roychowdhury

2015). The company is trading in the direction of raising the capital and ASX consequently

has granted a trading halt in the preparation of the market entry. This ultimately created a

The share prices throughout the course of 2016 stood negatively except in the month of June

where the company reported a highest positive share price movement against the all ordinary

index of 67.55 whereas the company also recorded as low as -24.00% in the month of

September. There is a higher amount of volatility in the share price movement throughout the

financial year of 2016 (Schaltegger and Burritt 2017). Moving to the next financial year of

2017 the share price have reflected more or less the identical volatility as the company

recorded some positive as well as the negative instances of share price movement against the

all ordinary index.

The share price for the KYCKR Ltd in the month of February stood positively at

11.76% while in the following month of March 2017 the share price declined to negatively

stand at 5.26%. Instances obtained in the latter half of the financial year suggest that the share

price movement stood higher against the all ordinary index (Macve 2015). As in the month of

August 2017 the share price of KYCKR Ltd stood positively at 41.38% against the all

ordinary index of -0.54% after recording a low of -17.07% in the previous month of July at -

14.71%. In the subsequent month of September, the share prices increased to stand at 46.34%

while the all ordinary index stood 4.03% (Hoyle, Schaefer and Doupnik 2015). However, in

the later months the declining trend in share prices continued its way.

Significant factor influencing the share price movement of the company are stated

below:

There are certain important factor that govern the share price movement of the

company. This includes the change focus of the company. KYCKR Ltd has uniquely placed

its focus on the business of technology that provides the solution to the people to protect them

against the money laundering and fraud along with tax evasion (Martin and Roychowdhury

2015). The company is trading in the direction of raising the capital and ASX consequently

has granted a trading halt in the preparation of the market entry. This ultimately created a

11FINANCE FOR BUSINESS

significant impact on the share prices of the company resulting the share prices to fall

negatively against the all ordinary index.

Macroeconomic factors include the currency and the exchange rate fluctuations. The

current financial contribution of the group is largely reliant on the movement in the exchange

rates among the Australian dollar and certain number of overseas currencies (Hoitash and

Hoitash 2017). The exchange rate among the numerous nations fluctuates substantially and

this results in fluctuations that adversely create an impact on the operating results of the

group and the financial position. As a result of this share prices of the company is

considerably impacted.

The industry factors include the market risks as the KYCKR Ltd is exposed to the risk

of currency because of the foreign exchange fluctuations in rate of currency (Henderson et al.

2015). The foreign currency risks originate from the future commercial transactions and the

same that is identified in the financial assets of the KYCKR Ltd. As a result of this there is a

significant movement as well as volatility in the share price movement of KYCKR Ltd.

Calculations of the Beta values and the anticipated rate of return by employing CAPM:

Computation of Beta Values

The calculated amount of beta for the company stood 0.00.

significant impact on the share prices of the company resulting the share prices to fall

negatively against the all ordinary index.

Macroeconomic factors include the currency and the exchange rate fluctuations. The

current financial contribution of the group is largely reliant on the movement in the exchange

rates among the Australian dollar and certain number of overseas currencies (Hoitash and

Hoitash 2017). The exchange rate among the numerous nations fluctuates substantially and

this results in fluctuations that adversely create an impact on the operating results of the

group and the financial position. As a result of this share prices of the company is

considerably impacted.

The industry factors include the market risks as the KYCKR Ltd is exposed to the risk

of currency because of the foreign exchange fluctuations in rate of currency (Henderson et al.

2015). The foreign currency risks originate from the future commercial transactions and the

same that is identified in the financial assets of the KYCKR Ltd. As a result of this there is a

significant movement as well as volatility in the share price movement of KYCKR Ltd.

Calculations of the Beta values and the anticipated rate of return by employing CAPM:

Computation of Beta Values

The calculated amount of beta for the company stood 0.00.

12FINANCE FOR BUSINESS

Computation of Required Rate of Return:

βa 0.00

Risk Free Rate (Rf) 4%

Expected market return of

Emmerson Resources (Rm1) 6%

Required rate of return 4.00%

Table 6: Table representing the Required Rate of Return

(Source: As Created by Author)

As evident from the above stated tabular representation the required rate of return of

the company stood 4.00%.

Conservative Investment:

KYCKR Ltd in the last two financial year reported a significant volatile in price. The

share price of the company been relatively low (Horton 2018). The future cash flow of the

company is poor and this can be primarily reflected on the dividend data as company has not

provided any divided in the past nor there is any plan of providing dividend to its

shareholders in the future. Gauging into the data of the company it can be stated that KYCKR

Ltd is a loss making company and comparatively the share price of the company stands

below Australian internet industry average.

Gauging into the past performance of the company the KYCKR did not reported an

instance of profit making and the company’s yearly average earnings growth stood negative

over the period of five years (Horton 2018). Due to the unavailability of the growth over the

past five year the company has not reported any instances of profit. Findings from the

Computation of Required Rate of Return:

βa 0.00

Risk Free Rate (Rf) 4%

Expected market return of

Emmerson Resources (Rm1) 6%

Required rate of return 4.00%

Table 6: Table representing the Required Rate of Return

(Source: As Created by Author)

As evident from the above stated tabular representation the required rate of return of

the company stood 4.00%.

Conservative Investment:

KYCKR Ltd in the last two financial year reported a significant volatile in price. The

share price of the company been relatively low (Horton 2018). The future cash flow of the

company is poor and this can be primarily reflected on the dividend data as company has not

provided any divided in the past nor there is any plan of providing dividend to its

shareholders in the future. Gauging into the data of the company it can be stated that KYCKR

Ltd is a loss making company and comparatively the share price of the company stands

below Australian internet industry average.

Gauging into the past performance of the company the KYCKR did not reported an

instance of profit making and the company’s yearly average earnings growth stood negative

over the period of five years (Horton 2018). Due to the unavailability of the growth over the

past five year the company has not reported any instances of profit. Findings from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCE FOR BUSINESS

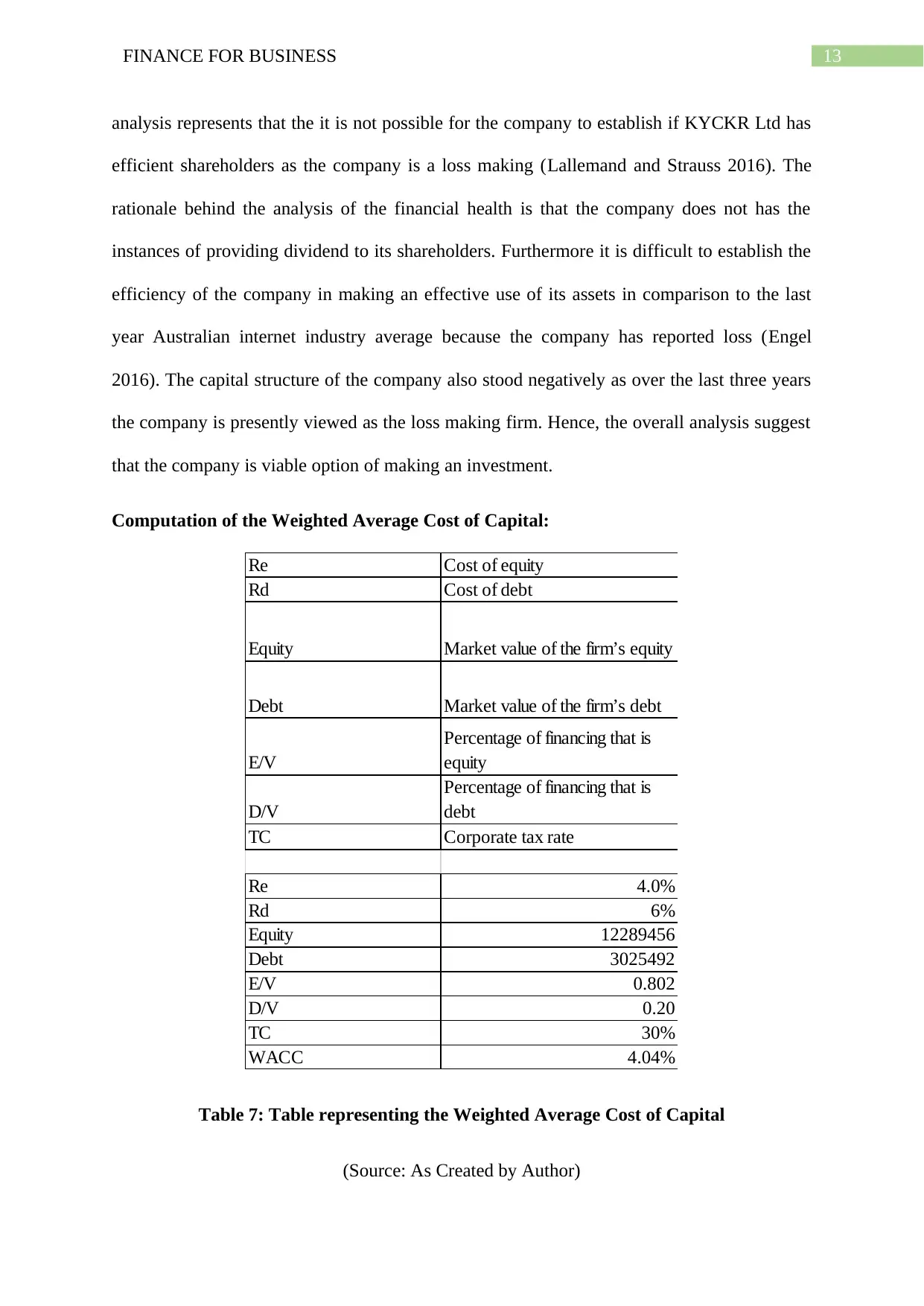

analysis represents that the it is not possible for the company to establish if KYCKR Ltd has

efficient shareholders as the company is a loss making (Lallemand and Strauss 2016). The

rationale behind the analysis of the financial health is that the company does not has the

instances of providing dividend to its shareholders. Furthermore it is difficult to establish the

efficiency of the company in making an effective use of its assets in comparison to the last

year Australian internet industry average because the company has reported loss (Engel

2016). The capital structure of the company also stood negatively as over the last three years

the company is presently viewed as the loss making firm. Hence, the overall analysis suggest

that the company is viable option of making an investment.

Computation of the Weighted Average Cost of Capital:

Re Cost of equity

Rd Cost of debt

Equity Market value of the firm’s equity

Debt Market value of the firm’s debt

E/V

Percentage of financing that is

equity

D/V

Percentage of financing that is

debt

TC Corporate tax rate

Re 4.0%

Rd 6%

Equity 12289456

Debt 3025492

E/V 0.802

D/V 0.20

TC 30%

WACC 4.04%

Table 7: Table representing the Weighted Average Cost of Capital

(Source: As Created by Author)

analysis represents that the it is not possible for the company to establish if KYCKR Ltd has

efficient shareholders as the company is a loss making (Lallemand and Strauss 2016). The

rationale behind the analysis of the financial health is that the company does not has the

instances of providing dividend to its shareholders. Furthermore it is difficult to establish the

efficiency of the company in making an effective use of its assets in comparison to the last

year Australian internet industry average because the company has reported loss (Engel

2016). The capital structure of the company also stood negatively as over the last three years

the company is presently viewed as the loss making firm. Hence, the overall analysis suggest

that the company is viable option of making an investment.

Computation of the Weighted Average Cost of Capital:

Re Cost of equity

Rd Cost of debt

Equity Market value of the firm’s equity

Debt Market value of the firm’s debt

E/V

Percentage of financing that is

equity

D/V

Percentage of financing that is

debt

TC Corporate tax rate

Re 4.0%

Rd 6%

Equity 12289456

Debt 3025492

E/V 0.802

D/V 0.20

TC 30%

WACC 4.04%

Table 7: Table representing the Weighted Average Cost of Capital

(Source: As Created by Author)

14FINANCE FOR BUSINESS

As evident from the above stated tabular representation the weighted average cost of

capital for KYCKR Ltd stood 4.04%.

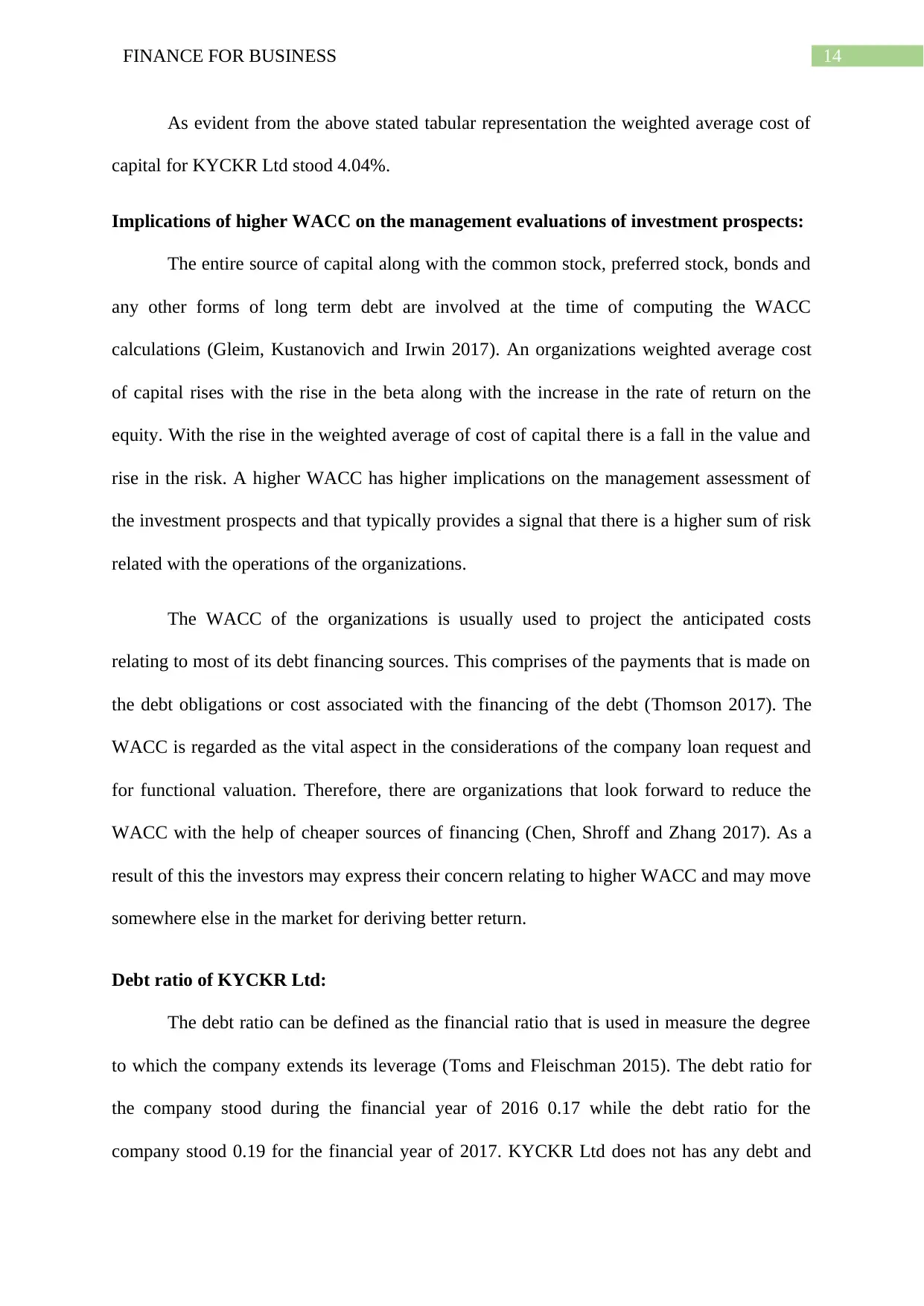

Implications of higher WACC on the management evaluations of investment prospects:

The entire source of capital along with the common stock, preferred stock, bonds and

any other forms of long term debt are involved at the time of computing the WACC

calculations (Gleim, Kustanovich and Irwin 2017). An organizations weighted average cost

of capital rises with the rise in the beta along with the increase in the rate of return on the

equity. With the rise in the weighted average of cost of capital there is a fall in the value and

rise in the risk. A higher WACC has higher implications on the management assessment of

the investment prospects and that typically provides a signal that there is a higher sum of risk

related with the operations of the organizations.

The WACC of the organizations is usually used to project the anticipated costs

relating to most of its debt financing sources. This comprises of the payments that is made on

the debt obligations or cost associated with the financing of the debt (Thomson 2017). The

WACC is regarded as the vital aspect in the considerations of the company loan request and

for functional valuation. Therefore, there are organizations that look forward to reduce the

WACC with the help of cheaper sources of financing (Chen, Shroff and Zhang 2017). As a

result of this the investors may express their concern relating to higher WACC and may move

somewhere else in the market for deriving better return.

Debt ratio of KYCKR Ltd:

The debt ratio can be defined as the financial ratio that is used in measure the degree

to which the company extends its leverage (Toms and Fleischman 2015). The debt ratio for

the company stood during the financial year of 2016 0.17 while the debt ratio for the

company stood 0.19 for the financial year of 2017. KYCKR Ltd does not has any debt and

As evident from the above stated tabular representation the weighted average cost of

capital for KYCKR Ltd stood 4.04%.

Implications of higher WACC on the management evaluations of investment prospects:

The entire source of capital along with the common stock, preferred stock, bonds and

any other forms of long term debt are involved at the time of computing the WACC

calculations (Gleim, Kustanovich and Irwin 2017). An organizations weighted average cost

of capital rises with the rise in the beta along with the increase in the rate of return on the

equity. With the rise in the weighted average of cost of capital there is a fall in the value and

rise in the risk. A higher WACC has higher implications on the management assessment of

the investment prospects and that typically provides a signal that there is a higher sum of risk

related with the operations of the organizations.

The WACC of the organizations is usually used to project the anticipated costs

relating to most of its debt financing sources. This comprises of the payments that is made on

the debt obligations or cost associated with the financing of the debt (Thomson 2017). The

WACC is regarded as the vital aspect in the considerations of the company loan request and

for functional valuation. Therefore, there are organizations that look forward to reduce the

WACC with the help of cheaper sources of financing (Chen, Shroff and Zhang 2017). As a

result of this the investors may express their concern relating to higher WACC and may move

somewhere else in the market for deriving better return.

Debt ratio of KYCKR Ltd:

The debt ratio can be defined as the financial ratio that is used in measure the degree

to which the company extends its leverage (Toms and Fleischman 2015). The debt ratio for

the company stood during the financial year of 2016 0.17 while the debt ratio for the

company stood 0.19 for the financial year of 2017. KYCKR Ltd does not has any debt and

15FINANCE FOR BUSINESS

the company over the past five years have not taken any debt. The capital structure of the

company is efficiently maintained by the directors.

In an attempt to amend their gearing ratio the company has issued to its vendors

46,297,500 of fully paid shares as a consideration of acquisition (Maheshwari 2015). There is

no such changes in the capital structure of the company.

Dividend Policy:

During the financial year of 2017 there were no dividends paid by the KYCKR Ltd to

its shareholder neither did the company recommend or declared present or the earlier

financial year.

Letter of Recommendations:

To Client Company

From Financial Advisory Team

We would like to draw your attention from the above stated analysis that the company

is not suitable for making investment. The share prices of the company over the last 12

months have reported a higher amount of volatility against the all ordinary index. The future

cash flow of KYCKR Ltd appears to be low and the share prices of the company been trading

at a low of A$0.17. The company is a loss making firm and its value is not comparable

against the value of the Australian internet industry average.

The growth of the KYCKR Ltd is also uncertain and with limited availability of the

information the earnings of the company stood relatively lower in comparison to the

Australian internet market. KYCKR Ltd does not generates profits and their yearly average

growth rate has been negative over the period of five years. The company has also not

the company over the past five years have not taken any debt. The capital structure of the

company is efficiently maintained by the directors.

In an attempt to amend their gearing ratio the company has issued to its vendors

46,297,500 of fully paid shares as a consideration of acquisition (Maheshwari 2015). There is

no such changes in the capital structure of the company.

Dividend Policy:

During the financial year of 2017 there were no dividends paid by the KYCKR Ltd to

its shareholder neither did the company recommend or declared present or the earlier

financial year.

Letter of Recommendations:

To Client Company

From Financial Advisory Team

We would like to draw your attention from the above stated analysis that the company

is not suitable for making investment. The share prices of the company over the last 12

months have reported a higher amount of volatility against the all ordinary index. The future

cash flow of KYCKR Ltd appears to be low and the share prices of the company been trading

at a low of A$0.17. The company is a loss making firm and its value is not comparable

against the value of the Australian internet industry average.

The growth of the KYCKR Ltd is also uncertain and with limited availability of the

information the earnings of the company stood relatively lower in comparison to the

Australian internet market. KYCKR Ltd does not generates profits and their yearly average

growth rate has been negative over the period of five years. The company has also not

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16FINANCE FOR BUSINESS

reported dividend payment to its shareholders neither the company recommend in future of

paying any dividend. A recommendations can be drawn by stating that the company is not

suitable for making investment and the investors are request to abstain from making any

investment in the KYCKR Ltd.

We anticipate that the information provided in analysis is helpful in meeting your

anticipation and look forward to provide you service in future.

Thank You

Conclusion:

The report can be concluded by stating that company has been a loss making venture

over the period of five year trend. The share prices of KYCKR Ltd has traded in the ASX as

low as A$ 0.17 and there is no such instances of providing the returns to the shareholders

appear. With the limited availability of the information the efficiency in the areas of return on

assets is not adequate as the company is a loss making venture. On a conclusive note it can be

stated that the company does not provide any dividends to its shareholders and hence it is not

a suitable venture of making an investment for the shareholders.

reported dividend payment to its shareholders neither the company recommend in future of

paying any dividend. A recommendations can be drawn by stating that the company is not

suitable for making investment and the investors are request to abstain from making any

investment in the KYCKR Ltd.

We anticipate that the information provided in analysis is helpful in meeting your

anticipation and look forward to provide you service in future.

Thank You

Conclusion:

The report can be concluded by stating that company has been a loss making venture

over the period of five year trend. The share prices of KYCKR Ltd has traded in the ASX as

low as A$ 0.17 and there is no such instances of providing the returns to the shareholders

appear. With the limited availability of the information the efficiency in the areas of return on

assets is not adequate as the company is a loss making venture. On a conclusive note it can be

stated that the company does not provide any dividends to its shareholders and hence it is not

a suitable venture of making an investment for the shareholders.

17FINANCE FOR BUSINESS

Reference list:

Chen, W., Shroff, P.K. and Zhang, I., 2017. Fair value accounting: Consequences of booking

market-driven goodwill impairment.

Editorial, R. (2018). ${Instrument_CompanyName} ${Instrument_Ric} Quote| Reuters.com.

[online] U.S. Available at: https://www.reuters.com/finance/stocks/overview/KYK.AX

[Accessed 16 May 2018].

Engel, C.J., 2016. A Primer on the Accounting and Reporting Requirements for Not-for-

Profit Organizations. Journal of Public Management Research, 2(1), p.14. Engel, C.J., 2016.

A Primer on the Accounting and Reporting Requirements for Not-for-Profit

Organizations. Journal of Public Management Research, 2(1), p.14.

Finance.yahoo.com. (2018). KYK.AX : Summary for KYCKRLIMIT FPO - Yahoo Finance.

[online] Available at: https://finance.yahoo.com/quote/KYK.AX/ [Accessed 16 May 2018].

Gleim, I.N., Kustanovich, M. and Irwin, G.M., 2017. CPA Review: Financial Accounting &

Reporting. Gleim Publications.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoitash, R. and Hoitash, U., 2017. Measuring accounting reporting complexity with

XBRL. The Accounting Review, 93(1), pp.259-287.

Horton, J., 2018. Advanced Financial Accounting and Reporting: Theory, Practice and

Evidence. Routledge.

Reference list:

Chen, W., Shroff, P.K. and Zhang, I., 2017. Fair value accounting: Consequences of booking

market-driven goodwill impairment.

Editorial, R. (2018). ${Instrument_CompanyName} ${Instrument_Ric} Quote| Reuters.com.

[online] U.S. Available at: https://www.reuters.com/finance/stocks/overview/KYK.AX

[Accessed 16 May 2018].

Engel, C.J., 2016. A Primer on the Accounting and Reporting Requirements for Not-for-

Profit Organizations. Journal of Public Management Research, 2(1), p.14. Engel, C.J., 2016.

A Primer on the Accounting and Reporting Requirements for Not-for-Profit

Organizations. Journal of Public Management Research, 2(1), p.14.

Finance.yahoo.com. (2018). KYK.AX : Summary for KYCKRLIMIT FPO - Yahoo Finance.

[online] Available at: https://finance.yahoo.com/quote/KYK.AX/ [Accessed 16 May 2018].

Gleim, I.N., Kustanovich, M. and Irwin, G.M., 2017. CPA Review: Financial Accounting &

Reporting. Gleim Publications.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoitash, R. and Hoitash, U., 2017. Measuring accounting reporting complexity with

XBRL. The Accounting Review, 93(1), pp.259-287.

Horton, J., 2018. Advanced Financial Accounting and Reporting: Theory, Practice and

Evidence. Routledge.

18FINANCE FOR BUSINESS

Horton, J., 2018. Advanced Financial Accounting and Reporting: Theory, Practice and

Evidence. Routledge.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kyckr. (2018). About Us | Kyckr. [online] Available at: http://www.kyckr.com/about-us/

[Accessed 16 May 2018].

Kyckr. (2018). Corporate Governance | Kyckr. [online] Available at:

http://www.kyckr.com/corporate-governance/ [Accessed 16 May 2018].

Kyckr. (2018). Share Price Charts | Kyckr. [online] Available at:

http://www.kyckr.com/share-price-charts/ [Accessed 16 May 2018].

Lallemand, J. and Strauss, J., 2016. Can We Count on Accounting Fundamentals for Industry

Portfolio Allocation?. Journal of Portfolio Management, 42(4), p.70.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Maheshwari, S., 2015. Fundamentals of Accounting.

Martin, X. and Roychowdhury, S., 2015. Do financial market developments influence

accounting practices? Credit default swaps and borrowers׳ reporting conservatism. Journal

of Accounting and Economics, 59(1), pp.80-104.

Moffett, M.H., Stonehill, A.I. and Eiteman, D.K., 2014. Fundamentals of multinational

finance. Prentice Hall.

Robson, K., Young, J. and Power, M., 2017. Themed section on financial accounting as

social and organizational practice: exploring the work of financial reporting. Accounting,

Organizations and Society, 56, pp.35-37.

Horton, J., 2018. Advanced Financial Accounting and Reporting: Theory, Practice and

Evidence. Routledge.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kyckr. (2018). About Us | Kyckr. [online] Available at: http://www.kyckr.com/about-us/

[Accessed 16 May 2018].

Kyckr. (2018). Corporate Governance | Kyckr. [online] Available at:

http://www.kyckr.com/corporate-governance/ [Accessed 16 May 2018].

Kyckr. (2018). Share Price Charts | Kyckr. [online] Available at:

http://www.kyckr.com/share-price-charts/ [Accessed 16 May 2018].

Lallemand, J. and Strauss, J., 2016. Can We Count on Accounting Fundamentals for Industry

Portfolio Allocation?. Journal of Portfolio Management, 42(4), p.70.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Maheshwari, S., 2015. Fundamentals of Accounting.

Martin, X. and Roychowdhury, S., 2015. Do financial market developments influence

accounting practices? Credit default swaps and borrowers׳ reporting conservatism. Journal

of Accounting and Economics, 59(1), pp.80-104.

Moffett, M.H., Stonehill, A.I. and Eiteman, D.K., 2014. Fundamentals of multinational

finance. Prentice Hall.

Robson, K., Young, J. and Power, M., 2017. Themed section on financial accounting as

social and organizational practice: exploring the work of financial reporting. Accounting,

Organizations and Society, 56, pp.35-37.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19FINANCE FOR BUSINESS

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Thomson, I., 2017, September. Commentary: A theoretical model of stakeholder perceptions

of a new financial reporting system. In Accounting Forum (Vol. 41, No. 3, pp. 277-279).

Elsevier.

Toms, S. and Fleischman, R.K., 2015. Accounting fundamentals and accounting change:

Boulton & Watt and the Springfield Armory. Accounting, organizations and Society, 41,

pp.1-20.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Thomson, I., 2017, September. Commentary: A theoretical model of stakeholder perceptions

of a new financial reporting system. In Accounting Forum (Vol. 41, No. 3, pp. 277-279).

Elsevier.

Toms, S. and Fleischman, R.K., 2015. Accounting fundamentals and accounting change:

Boulton & Watt and the Springfield Armory. Accounting, organizations and Society, 41,

pp.1-20.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.