FINANCE FOR BUSINESS: Financial Statements, Financing & Evaluation

VerifiedAdded on 2022/09/16

|14

|3310

|32

Report

AI Summary

This report, focusing on finance for business, begins with an analysis of financial statements, including a balance sheet, profit and loss statement, and cash flow statement for ABC Pty Ltd. The report then delves into financing options, differentiating between short-term and long-term sources, and exploring the risks and returns associated with each. It examines financing for both start-up firms, such as venture capital, angel investors, and mezzanine financing, and growth firms, with a focus on loans and borrowings. Finally, the report addresses cash flow estimation and project evaluation, including depreciation, EBIT calculations, free cash flow analysis, net present value, and alternative project evaluation measures, providing a comprehensive overview of financial management principles and practices. The report is a valuable resource for students studying finance and business.

Running head: FINANCE FOR BUSINESS

Finance for Business

Name of the Student:

Name of the University:

Author’s Note:

Finance for Business

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR BUSINESS

Table of Contents

Part 1: Financial Statements............................................................................................................2

1.1 Financial Position Statement.................................................................................................2

1.2 Profit and Loss Statement......................................................................................................3

1.3 Cash Flow Statement.............................................................................................................3

Part 2: Financing- Risks and Returns..............................................................................................4

2.1 Potential Sources of Finance for a Business..........................................................................4

2.2 Potential Source of Finance for Start-Up Firms....................................................................6

2.3 Potential Sources of Finance for a Growth Firm...................................................................8

Part 3: Cash flow Estimation and Project Evaluation......................................................................9

3.1 Rate of Diminishing Value Depreciation..............................................................................9

3.2 Firms Additional EBIT Calculations.....................................................................................9

3.3 Free Cash Flow Analysis.....................................................................................................10

3.4 Net Present Value................................................................................................................10

3.5 Alternative Project Evaluation Measures............................................................................10

References......................................................................................................................................11

Table of Contents

Part 1: Financial Statements............................................................................................................2

1.1 Financial Position Statement.................................................................................................2

1.2 Profit and Loss Statement......................................................................................................3

1.3 Cash Flow Statement.............................................................................................................3

Part 2: Financing- Risks and Returns..............................................................................................4

2.1 Potential Sources of Finance for a Business..........................................................................4

2.2 Potential Source of Finance for Start-Up Firms....................................................................6

2.3 Potential Sources of Finance for a Growth Firm...................................................................8

Part 3: Cash flow Estimation and Project Evaluation......................................................................9

3.1 Rate of Diminishing Value Depreciation..............................................................................9

3.2 Firms Additional EBIT Calculations.....................................................................................9

3.3 Free Cash Flow Analysis.....................................................................................................10

3.4 Net Present Value................................................................................................................10

3.5 Alternative Project Evaluation Measures............................................................................10

References......................................................................................................................................11

2FINANCE FOR BUSINESS

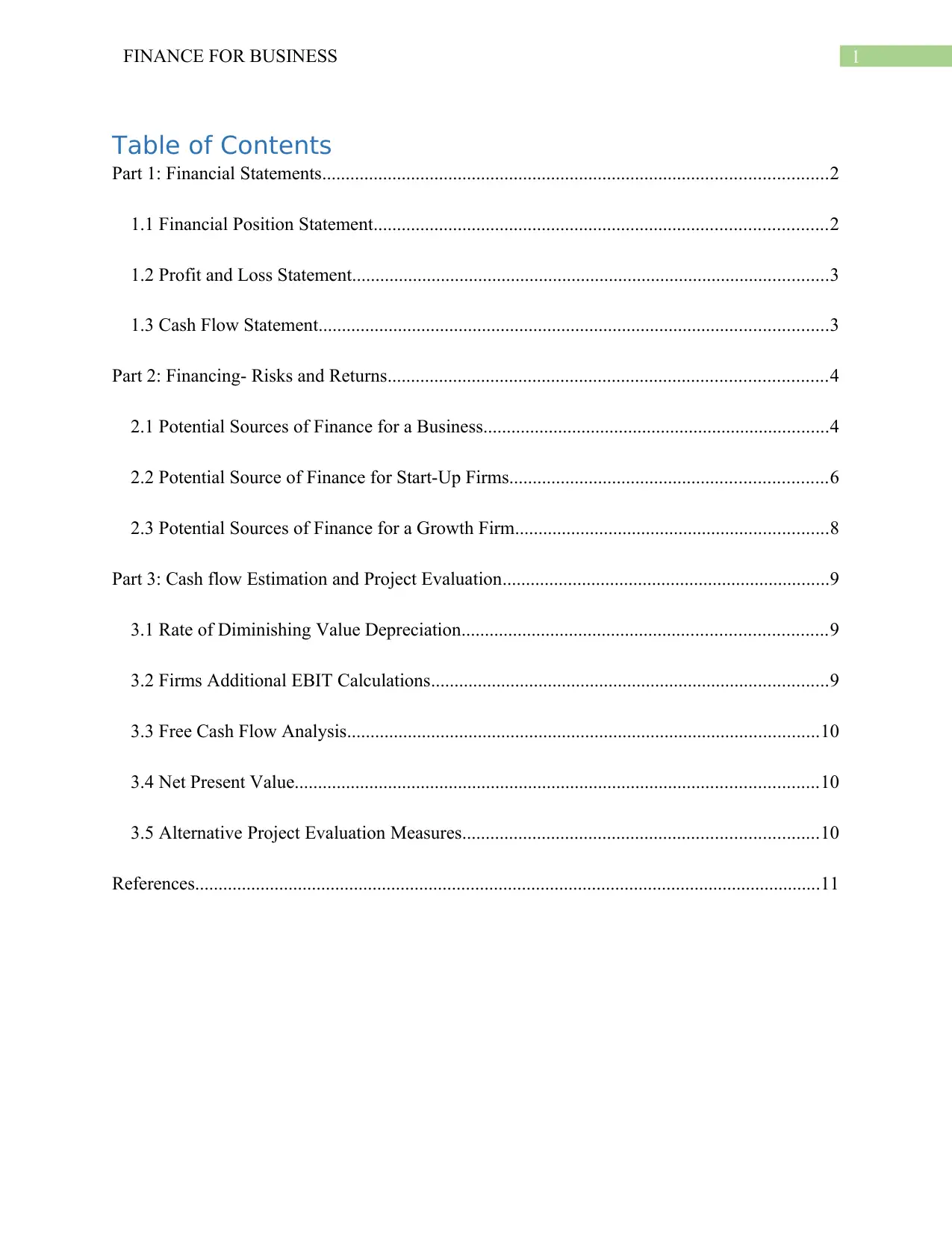

Part 1: Financial Statements

1.1 Financial Position Statement.

Part 1: Financial Statements

Balance Sheet for ABC Pty Ltd as

on30.6.18

Particulars

Amount

($)

Assets

Non-Current Assets

Plant and Equipment 310

Vehicles 235

Land and Building 1210

Total Non-Current

Assets 1755

Current Assets

Cash 200

Accounts Receivable 235

Inventory 370

Total Current Assets 805

Total Assets 2560

Liabilities and Equity

Current Liabilities

Accounts Payable 270

Tax Liability 90

Bank Overdraft 330

Total Current Liabilities 690

Non-Current Liabilities

Bank Loan 320

Corporate Bonds 430

Total Non-Current

Liabilities 750

Total Liabilities 1440

Shareholder's Equity

Preference Shares 260

Ordinary Shares 690

Retained Earnings 170

Total Shareholder’s 1120

Part 1: Financial Statements

1.1 Financial Position Statement.

Part 1: Financial Statements

Balance Sheet for ABC Pty Ltd as

on30.6.18

Particulars

Amount

($)

Assets

Non-Current Assets

Plant and Equipment 310

Vehicles 235

Land and Building 1210

Total Non-Current

Assets 1755

Current Assets

Cash 200

Accounts Receivable 235

Inventory 370

Total Current Assets 805

Total Assets 2560

Liabilities and Equity

Current Liabilities

Accounts Payable 270

Tax Liability 90

Bank Overdraft 330

Total Current Liabilities 690

Non-Current Liabilities

Bank Loan 320

Corporate Bonds 430

Total Non-Current

Liabilities 750

Total Liabilities 1440

Shareholder's Equity

Preference Shares 260

Ordinary Shares 690

Retained Earnings 170

Total Shareholder’s 1120

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR BUSINESS

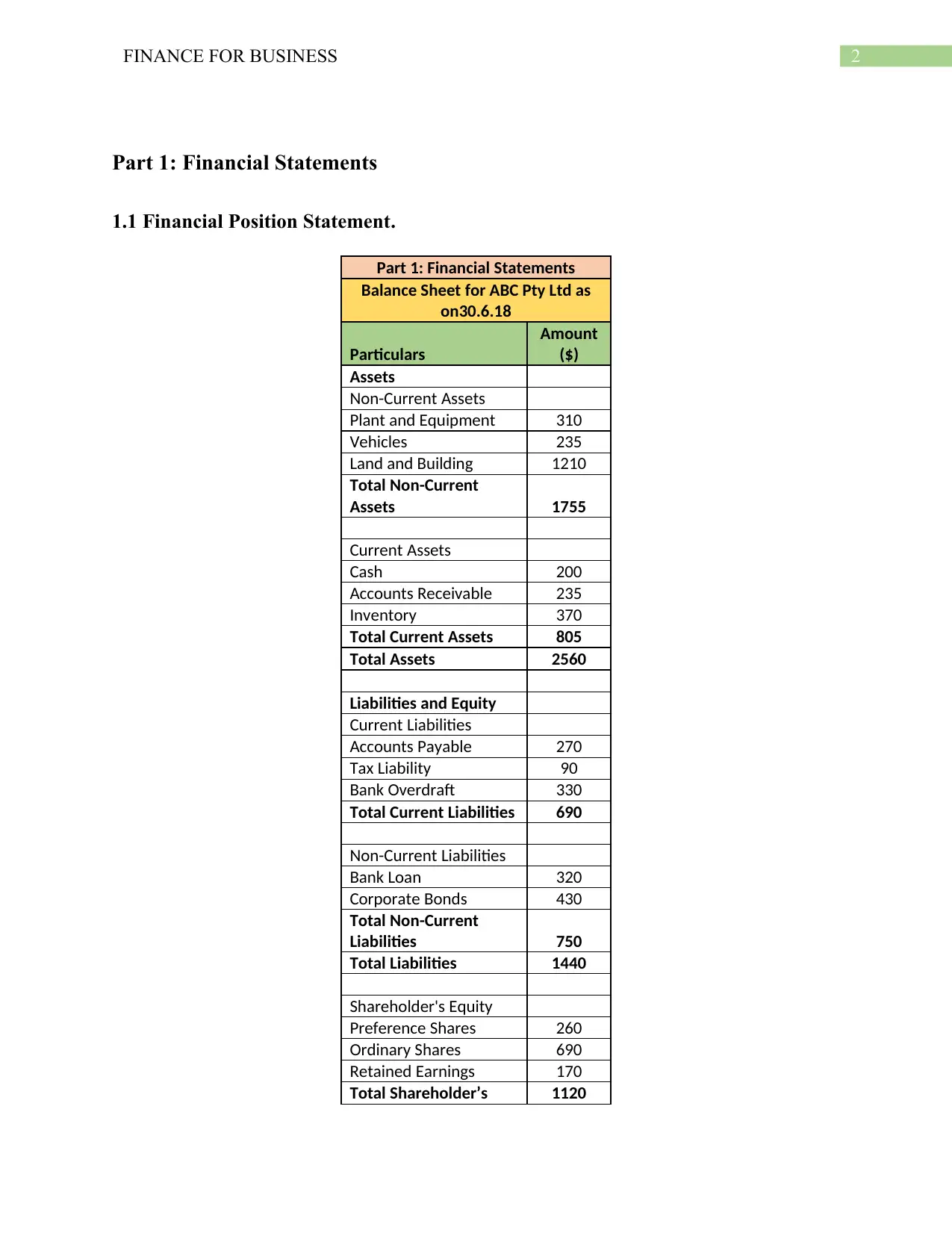

Equity

Total Liabilities and

Equity 2560

1.2 Profit and Loss Statement

Part 1: Financial Statements

Profit and Loss Statement for ABC Pty Ltd as on 30.6.18

Particulars Amount ($) Particulars Amount ($)

Opening Stock 272 Sales 992

Add: Purchases 554 Closing Inventory 257

Less: Wages -117

Gross Profit 540

Total 1249 Total 1249

Interest -27 Gross Profit 540

Utilities -57 Dividend Received 50

Loss from Sale of Machine -10

Rent -82

Net Profit 766

Total 590 Total 590

1.3 Cash Flow Statement

Cash Flow Statement

Particulars Amt. ($)

Cash flow from Operations

Cash Received from Customers 460

Less: Cash Paid to Suppliers -240

Less: Wages Paid -130

Less: Interest Paid -12

Less: Taxes Paid -8

Total Cash Inflow from Operations 70

Cash flow from Investing Activity Amt. ($)

Purchase of Plant and Machinery -350

Proceeds from Sale of Plant and Machinery 80

Total Cash Outflow from Investing Activities -270

Cash flow from Financing Activity Amt. ($)

Proceeds from Issues of New Share 85

Proceeds from Lon-Term Borrowings 155

Equity

Total Liabilities and

Equity 2560

1.2 Profit and Loss Statement

Part 1: Financial Statements

Profit and Loss Statement for ABC Pty Ltd as on 30.6.18

Particulars Amount ($) Particulars Amount ($)

Opening Stock 272 Sales 992

Add: Purchases 554 Closing Inventory 257

Less: Wages -117

Gross Profit 540

Total 1249 Total 1249

Interest -27 Gross Profit 540

Utilities -57 Dividend Received 50

Loss from Sale of Machine -10

Rent -82

Net Profit 766

Total 590 Total 590

1.3 Cash Flow Statement

Cash Flow Statement

Particulars Amt. ($)

Cash flow from Operations

Cash Received from Customers 460

Less: Cash Paid to Suppliers -240

Less: Wages Paid -130

Less: Interest Paid -12

Less: Taxes Paid -8

Total Cash Inflow from Operations 70

Cash flow from Investing Activity Amt. ($)

Purchase of Plant and Machinery -350

Proceeds from Sale of Plant and Machinery 80

Total Cash Outflow from Investing Activities -270

Cash flow from Financing Activity Amt. ($)

Proceeds from Issues of New Share 85

Proceeds from Lon-Term Borrowings 155

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR BUSINESS

Dividend Received 9

Repayment of Long-Term Borrowings -24

Cost of Buying Back Shares -31

Dividend Paid -26

Payment of Finance Lease Liabilities -48

Total Cash flow from Financing Activities 120

Net Cash Increase/(Decrease) for the year -80

Part 2: Financing- Risks and Returns

2.1 Potential Sources of Finance for a Business

The sources of finance for a business for a business can be particularly in the form of

long-term and short term financing sources such as equity, debentures, debts, retained earnings,

term loans, working capital which is currently in the form of excess of current assets over the

current liabilities of the company (Burns and Dewhurst 2016). On the other hand, letter of credit,

euro issue, and short terms loans and bank over drafts are some of the key short-term financing

loans available for the company. The key features and characteristics that the companies should

consider during the time period of financing are primarily as follows:

Time Horizon: In order to select the potential source of finance for the company it is

well important for the company to identify the time horizon for which they would be

undertaking the desired level and amount of finance (Lee, Sameen and Cowling 2015).

The time horizon should be well incorporated in association with the purpose of the

finance for which the company is financing the assets or the investing activities of the

company. In specific if the time horizon for the company is long-term then the company

should be going for equity source of finance or debt finance that can easily fulfill the

requirement of the company (Fraser, Bhaumik and Wright 2015). On the other hand, if

Dividend Received 9

Repayment of Long-Term Borrowings -24

Cost of Buying Back Shares -31

Dividend Paid -26

Payment of Finance Lease Liabilities -48

Total Cash flow from Financing Activities 120

Net Cash Increase/(Decrease) for the year -80

Part 2: Financing- Risks and Returns

2.1 Potential Sources of Finance for a Business

The sources of finance for a business for a business can be particularly in the form of

long-term and short term financing sources such as equity, debentures, debts, retained earnings,

term loans, working capital which is currently in the form of excess of current assets over the

current liabilities of the company (Burns and Dewhurst 2016). On the other hand, letter of credit,

euro issue, and short terms loans and bank over drafts are some of the key short-term financing

loans available for the company. The key features and characteristics that the companies should

consider during the time period of financing are primarily as follows:

Time Horizon: In order to select the potential source of finance for the company it is

well important for the company to identify the time horizon for which they would be

undertaking the desired level and amount of finance (Lee, Sameen and Cowling 2015).

The time horizon should be well incorporated in association with the purpose of the

finance for which the company is financing the assets or the investing activities of the

company. In specific if the time horizon for the company is long-term then the company

should be going for equity source of finance or debt finance that can easily fulfill the

requirement of the company (Fraser, Bhaumik and Wright 2015). On the other hand, if

5FINANCE FOR BUSINESS

the considered time period of investment for the company is currently short-term than the

company should consider short term loans/borrowings in the form of bank loans,

borrowings and bank overdraft facility that the company can avail.

Costs: The costs that are directly associated with the financing purpose of the company

should be well taken into analysis for the company so that the company is well able to

analyze the cost benefit analysis associated with each sources of finance. Equity finance

can be costly for the company on the other hand, debt finance could be cost effective for

the company but the same would be creating a charge on the assets of the company

(Kljucnikov et al., 2016). The actions and implementations taken in perspective to

financing can also be limited due to the debt covenants attached. Thus, the company

should select an optimum mix of various financing sources that is indeed cost effective

and well compatible with the operations of the company (Mason, Botelho and Harrison

2016).

Risks: Risks associated with the company in the form of possible ways where by the

financing sources can create a potential effect on the operations and activities taken by

the company. Borrowings, Debt financing can affect the financial position and the

operations of the company because if the same creates a charge on the assets of the

company where the associated financial risk of the company increases (Mason and

Harrison 2015). The increase in the financial risk can well affect the overall operations of

the company whereby if the company fails to repay interest and principal amount at the

time of due date or maturity the creditors can sue the company and takeover the assets of

the company. On the other hand, there is no such restrictions in equity or preference share

financing.

the considered time period of investment for the company is currently short-term than the

company should consider short term loans/borrowings in the form of bank loans,

borrowings and bank overdraft facility that the company can avail.

Costs: The costs that are directly associated with the financing purpose of the company

should be well taken into analysis for the company so that the company is well able to

analyze the cost benefit analysis associated with each sources of finance. Equity finance

can be costly for the company on the other hand, debt finance could be cost effective for

the company but the same would be creating a charge on the assets of the company

(Kljucnikov et al., 2016). The actions and implementations taken in perspective to

financing can also be limited due to the debt covenants attached. Thus, the company

should select an optimum mix of various financing sources that is indeed cost effective

and well compatible with the operations of the company (Mason, Botelho and Harrison

2016).

Risks: Risks associated with the company in the form of possible ways where by the

financing sources can create a potential effect on the operations and activities taken by

the company. Borrowings, Debt financing can affect the financial position and the

operations of the company because if the same creates a charge on the assets of the

company where the associated financial risk of the company increases (Mason and

Harrison 2015). The increase in the financial risk can well affect the overall operations of

the company whereby if the company fails to repay interest and principal amount at the

time of due date or maturity the creditors can sue the company and takeover the assets of

the company. On the other hand, there is no such restrictions in equity or preference share

financing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR BUSINESS

Purpose: The key purpose of the finance that the company intends to use in the defined

period of analysis should be well taken into consideration. If the associated project or

operations for which the company is associating is risky i.e., the business risk is high then

it is accordingly important for the company to undertake sources of finance that is

considerably less risky for the company.

Impact on Financial Position: The financing sources of the company that the company

is considering should be well considered based on the fact that the same does not impact

the overall financial position of the company. While taxation benefits can be well availed

if the company considers debt financing, but the same might also be not available for the

company if equity and preferences source of finance is considered (Cumming and

Vismara 2017).

The characteristics that were discussed and taken into consideration is important as the

financing sources for the company has been done based on Time Horizon, Liquidity

Requirements, Time horizon, Risks associated, Purpose of Financing and the impact of each

source on the financial position was also taken into consideration. It is very important that the

company considers and takes these factors into account for the purpose of analysis of the

company (Leitch, Welter and Henry 2018).

2.2 Potential Source of Finance for Start-Up Firms

The potential sources of finance for the start-up firms can be primarily done by many

financial institutions and angel investors that ultimately helps the company in financing the

various operational and investment activities undertaken by the company. The list of available

sources of finance that the Start-Up Firm can approach are as follows:

Purpose: The key purpose of the finance that the company intends to use in the defined

period of analysis should be well taken into consideration. If the associated project or

operations for which the company is associating is risky i.e., the business risk is high then

it is accordingly important for the company to undertake sources of finance that is

considerably less risky for the company.

Impact on Financial Position: The financing sources of the company that the company

is considering should be well considered based on the fact that the same does not impact

the overall financial position of the company. While taxation benefits can be well availed

if the company considers debt financing, but the same might also be not available for the

company if equity and preferences source of finance is considered (Cumming and

Vismara 2017).

The characteristics that were discussed and taken into consideration is important as the

financing sources for the company has been done based on Time Horizon, Liquidity

Requirements, Time horizon, Risks associated, Purpose of Financing and the impact of each

source on the financial position was also taken into consideration. It is very important that the

company considers and takes these factors into account for the purpose of analysis of the

company (Leitch, Welter and Henry 2018).

2.2 Potential Source of Finance for Start-Up Firms

The potential sources of finance for the start-up firms can be primarily done by many

financial institutions and angel investors that ultimately helps the company in financing the

various operational and investment activities undertaken by the company. The list of available

sources of finance that the Start-Up Firm can approach are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR BUSINESS

Venture Capital: The corporate financing activity helps the venture capital receive finance

whereby the financial investor invests in the business/start-up for a fresh set of strategic advice

or cash position. Investors of Venture Capital are always on the verge of looking for companies

that can consistently provide them a high growth rate return. Venture Capitalist look for market

capitalistic opportunities for obtaining long-term capital gains of the company. Venture Capital

are trustworthy and have no obligations for repayments (Gambetti and Musso 2017). Venture

Capital are the most optimal source of finance for the company as they have valuable guidance

experience in the field of business start-up assessment and the financial viability of the business.

Exploration of the better available market opportunities can be well done with the help of

venture capitals who will not only be helping in the investment and financing activities but

would also be looking for various ways whereby it can strategies the operations of the company.

Angel Investors: An Angel Investors are high net worth individual investors that provide

adequate funding and financial support for the company in the form of start-up lie for a stake or

the ownership position in the company so that the same can help the company in the financing

support that they require. Angel Investors can be in the form of Entrepreneurs, Family or

Relatives. In addition to the financial support that a company receives from an angel investors

they also provide the start-up companies with critical knowledge of management expertise

(Cassar, Ittner and Cavalluzzo 2015). Financing from the angel investors is comparatively less

risky than taking loans and this stands out to be the key importance for the loan that the start-up

company can have in their financing sources. The Capital needs are adequately meet by the

angels of the company, they also enable the sustainable growth of the company by reinvesting

the return or the profitability generated from the business back to the company. Business

Acumen, Vertical Expertise and Director Services are some of the key portfolio experiences that

Venture Capital: The corporate financing activity helps the venture capital receive finance

whereby the financial investor invests in the business/start-up for a fresh set of strategic advice

or cash position. Investors of Venture Capital are always on the verge of looking for companies

that can consistently provide them a high growth rate return. Venture Capitalist look for market

capitalistic opportunities for obtaining long-term capital gains of the company. Venture Capital

are trustworthy and have no obligations for repayments (Gambetti and Musso 2017). Venture

Capital are the most optimal source of finance for the company as they have valuable guidance

experience in the field of business start-up assessment and the financial viability of the business.

Exploration of the better available market opportunities can be well done with the help of

venture capitals who will not only be helping in the investment and financing activities but

would also be looking for various ways whereby it can strategies the operations of the company.

Angel Investors: An Angel Investors are high net worth individual investors that provide

adequate funding and financial support for the company in the form of start-up lie for a stake or

the ownership position in the company so that the same can help the company in the financing

support that they require. Angel Investors can be in the form of Entrepreneurs, Family or

Relatives. In addition to the financial support that a company receives from an angel investors

they also provide the start-up companies with critical knowledge of management expertise

(Cassar, Ittner and Cavalluzzo 2015). Financing from the angel investors is comparatively less

risky than taking loans and this stands out to be the key importance for the loan that the start-up

company can have in their financing sources. The Capital needs are adequately meet by the

angels of the company, they also enable the sustainable growth of the company by reinvesting

the return or the profitability generated from the business back to the company. Business

Acumen, Vertical Expertise and Director Services are some of the key portfolio experiences that

8FINANCE FOR BUSINESS

an angel investors brings during the financing activity carried out by the company. The angel

investors also allows a four-year time period for the purpose of analysis of the fund growth and

fund analysis where they analyze the ability of the company in effective utilization and growth of

funds for the angel investors (Connolly and Jackman 2017). Wealth creation and sustainable

growth of the organization is the key focus of the angel investors rather than monthly or regular

fees which do create as a burden for the start-up business.

Mezzanine Financing: Mezzanine Fund or Mezzanine Loan does not primarily fall into the

category of a pure debt or pure equity. In other words it can be well explained it is a very high

risk and high reward type of financing that is done by the company that almost fulfills the gaps

between the senior debt and equity that the company owns. The key characteristics of this

finance is that this type of finance is generally subordinate to senior debt but still stands out to be

senior than the equity finance. It also earns a higher yield than the senior debt finance that

accompany generally has in the books. The start-up investor can get the desired amount of loan

from the mezzanine investors for a defined period of time where in it has to provide regular

interest amount associated with the equity finance. They charge a very rate of interest rate in the

form of higher risk and higher return for the capital they provide (Khan 2015).

2.3 Potential Sources of Finance for a Growth Firm

The key potential sources of finance for a growing or expanding firm can be in the various

following ways and the same can be as follows:

Loans and Borrowings: Bank Loans and Credits can be the best sources of finance that the

company can utilize in order to finance the operations of the company. The bank loans and

borrowings done can be primarily in the field of line of credit loans, installment credits, balloon

loans and secured loans. The balloon loans is typically most suitable for a growing or expanding

an angel investors brings during the financing activity carried out by the company. The angel

investors also allows a four-year time period for the purpose of analysis of the fund growth and

fund analysis where they analyze the ability of the company in effective utilization and growth of

funds for the angel investors (Connolly and Jackman 2017). Wealth creation and sustainable

growth of the organization is the key focus of the angel investors rather than monthly or regular

fees which do create as a burden for the start-up business.

Mezzanine Financing: Mezzanine Fund or Mezzanine Loan does not primarily fall into the

category of a pure debt or pure equity. In other words it can be well explained it is a very high

risk and high reward type of financing that is done by the company that almost fulfills the gaps

between the senior debt and equity that the company owns. The key characteristics of this

finance is that this type of finance is generally subordinate to senior debt but still stands out to be

senior than the equity finance. It also earns a higher yield than the senior debt finance that

accompany generally has in the books. The start-up investor can get the desired amount of loan

from the mezzanine investors for a defined period of time where in it has to provide regular

interest amount associated with the equity finance. They charge a very rate of interest rate in the

form of higher risk and higher return for the capital they provide (Khan 2015).

2.3 Potential Sources of Finance for a Growth Firm

The key potential sources of finance for a growing or expanding firm can be in the various

following ways and the same can be as follows:

Loans and Borrowings: Bank Loans and Credits can be the best sources of finance that the

company can utilize in order to finance the operations of the company. The bank loans and

borrowings done can be primarily in the field of line of credit loans, installment credits, balloon

loans and secured loans. The balloon loans is typically most suitable for a growing or expanding

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE FOR BUSINESS

firm where the company currently has to only to pay the interest payment over the defined period

of finance and the exit stage of the loan it pays back the entire principal amount. The balloon

loan does not create any burden on the operations of the company and can be well considered by

growing companies. On the other hand, secured loans and borrowings can also be well taken by

the company for a defined period of time (Leitch, Welter and Henry 2018).

Venture Capital: The venture capital are typically known for backing up companies that are in

the growth or expansion phase of their business. Investors of Venture Capital are always on the

verge of looking for companies that can consistently provide them a high growth rate return.

Venture Capitalist look for market capitalistic opportunities for obtaining long-term capital gains

of the company (Triantis 2018). Venture Capital are trustworthy and have no obligations for

repayments. Venture Capital are the most optimal source of finance for the company as they

have valuable guidance experience in the field of business start-up assessment and the financial

viability of the business (Sidek et al., 2016).

Initial Public Offering: The initial public offering is a common way of raising equity finance by

the general public in exchange of shares for the company. Small or growing companies typically

raise finance with the help of issue of equity or preferences share in the capital market in the

form of Initial Public Offering for the company whereby the company can grow and expands its

operations (Sidek, Mohamad and Nasir 2016).

Part 3: Cash flow Estimation and Project Evaluation

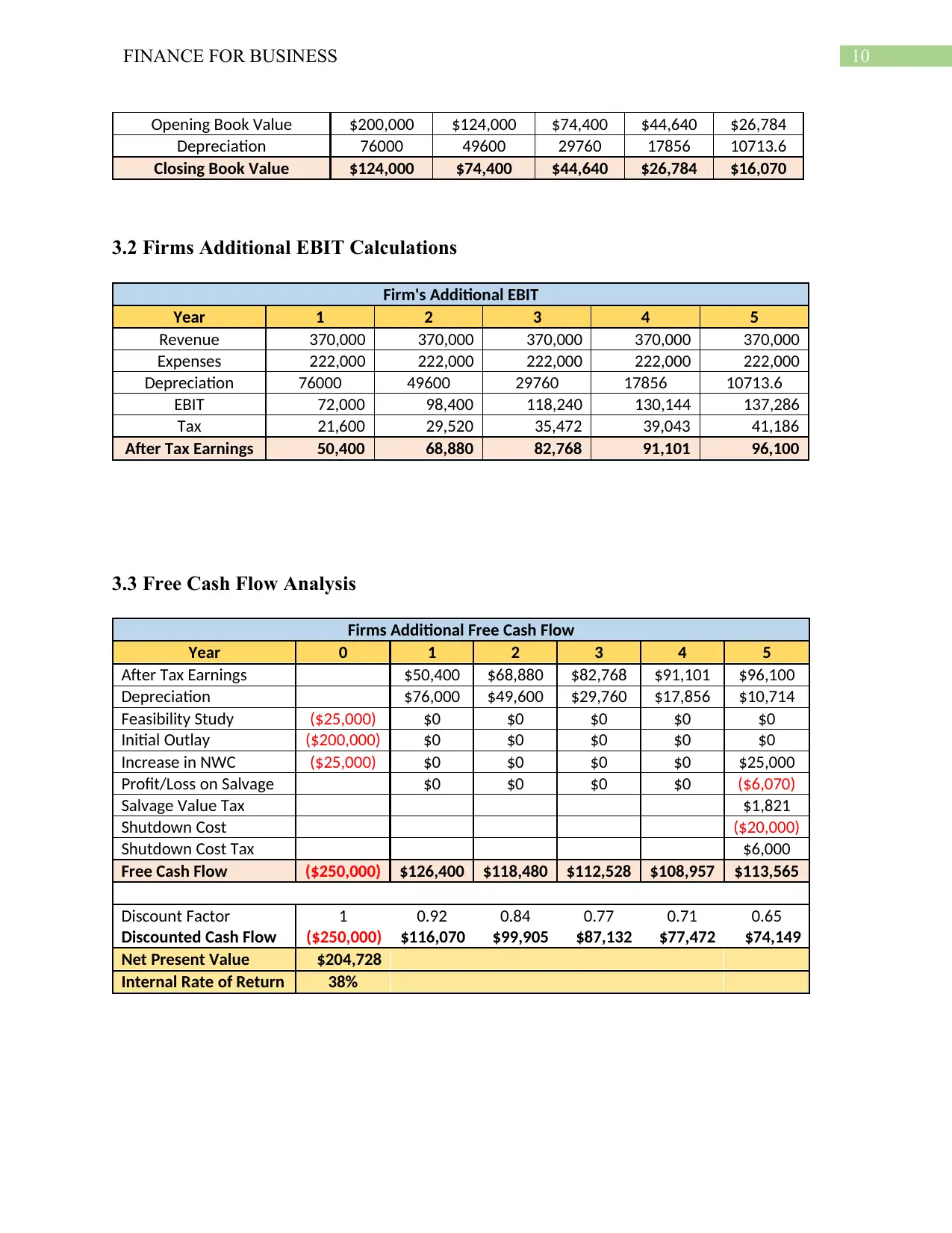

3.1 Rate of Diminishing Value Depreciation

Diminishing Value of Depreciation

Year 1 2 3 4 5

firm where the company currently has to only to pay the interest payment over the defined period

of finance and the exit stage of the loan it pays back the entire principal amount. The balloon

loan does not create any burden on the operations of the company and can be well considered by

growing companies. On the other hand, secured loans and borrowings can also be well taken by

the company for a defined period of time (Leitch, Welter and Henry 2018).

Venture Capital: The venture capital are typically known for backing up companies that are in

the growth or expansion phase of their business. Investors of Venture Capital are always on the

verge of looking for companies that can consistently provide them a high growth rate return.

Venture Capitalist look for market capitalistic opportunities for obtaining long-term capital gains

of the company (Triantis 2018). Venture Capital are trustworthy and have no obligations for

repayments. Venture Capital are the most optimal source of finance for the company as they

have valuable guidance experience in the field of business start-up assessment and the financial

viability of the business (Sidek et al., 2016).

Initial Public Offering: The initial public offering is a common way of raising equity finance by

the general public in exchange of shares for the company. Small or growing companies typically

raise finance with the help of issue of equity or preferences share in the capital market in the

form of Initial Public Offering for the company whereby the company can grow and expands its

operations (Sidek, Mohamad and Nasir 2016).

Part 3: Cash flow Estimation and Project Evaluation

3.1 Rate of Diminishing Value Depreciation

Diminishing Value of Depreciation

Year 1 2 3 4 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR BUSINESS

Opening Book Value $200,000 $124,000 $74,400 $44,640 $26,784

Depreciation 76000 49600 29760 17856 10713.6

Closing Book Value $124,000 $74,400 $44,640 $26,784 $16,070

3.2 Firms Additional EBIT Calculations

Firm's Additional EBIT

Year 1 2 3 4 5

Revenue 370,000 370,000 370,000 370,000 370,000

Expenses 222,000 222,000 222,000 222,000 222,000

Depreciation 76000 49600 29760 17856 10713.6

EBIT 72,000 98,400 118,240 130,144 137,286

Tax 21,600 29,520 35,472 39,043 41,186

After Tax Earnings 50,400 68,880 82,768 91,101 96,100

3.3 Free Cash Flow Analysis

Firms Additional Free Cash Flow

Year 0 1 2 3 4 5

After Tax Earnings $50,400 $68,880 $82,768 $91,101 $96,100

Depreciation $76,000 $49,600 $29,760 $17,856 $10,714

Feasibility Study ($25,000) $0 $0 $0 $0 $0

Initial Outlay ($200,000) $0 $0 $0 $0 $0

Increase in NWC ($25,000) $0 $0 $0 $0 $25,000

Profit/Loss on Salvage $0 $0 $0 $0 ($6,070)

Salvage Value Tax $1,821

Shutdown Cost ($20,000)

Shutdown Cost Tax $6,000

Free Cash Flow ($250,000) $126,400 $118,480 $112,528 $108,957 $113,565

Discount Factor 1 0.92 0.84 0.77 0.71 0.65

Discounted Cash Flow ($250,000) $116,070 $99,905 $87,132 $77,472 $74,149

Net Present Value $204,728

Internal Rate of Return 38%

Opening Book Value $200,000 $124,000 $74,400 $44,640 $26,784

Depreciation 76000 49600 29760 17856 10713.6

Closing Book Value $124,000 $74,400 $44,640 $26,784 $16,070

3.2 Firms Additional EBIT Calculations

Firm's Additional EBIT

Year 1 2 3 4 5

Revenue 370,000 370,000 370,000 370,000 370,000

Expenses 222,000 222,000 222,000 222,000 222,000

Depreciation 76000 49600 29760 17856 10713.6

EBIT 72,000 98,400 118,240 130,144 137,286

Tax 21,600 29,520 35,472 39,043 41,186

After Tax Earnings 50,400 68,880 82,768 91,101 96,100

3.3 Free Cash Flow Analysis

Firms Additional Free Cash Flow

Year 0 1 2 3 4 5

After Tax Earnings $50,400 $68,880 $82,768 $91,101 $96,100

Depreciation $76,000 $49,600 $29,760 $17,856 $10,714

Feasibility Study ($25,000) $0 $0 $0 $0 $0

Initial Outlay ($200,000) $0 $0 $0 $0 $0

Increase in NWC ($25,000) $0 $0 $0 $0 $25,000

Profit/Loss on Salvage $0 $0 $0 $0 ($6,070)

Salvage Value Tax $1,821

Shutdown Cost ($20,000)

Shutdown Cost Tax $6,000

Free Cash Flow ($250,000) $126,400 $118,480 $112,528 $108,957 $113,565

Discount Factor 1 0.92 0.84 0.77 0.71 0.65

Discounted Cash Flow ($250,000) $116,070 $99,905 $87,132 $77,472 $74,149

Net Present Value $204,728

Internal Rate of Return 38%

11FINANCE FOR BUSINESS

3.4 Net Present Value

The net present value for the project was determined to be around $204,728 and the same

states that the project would be creating an wealth greater than the required rate of return which

is around 8.90% for the company. The project can be well accepted based on the profitability

generated from the business (Andersen et al., 2018).

3.5 Alternative Project Evaluation Measures

The key alternative project evaluation measures that the companies should deploy for the

purpose of project evaluation can be the Internal Rate of Return or the IIR method that states the

return for the project in percentage terms. The IRR of the project was determined to be around

38% for the company reflecting the return that the investors would be getting from the project.

3.4 Net Present Value

The net present value for the project was determined to be around $204,728 and the same

states that the project would be creating an wealth greater than the required rate of return which

is around 8.90% for the company. The project can be well accepted based on the profitability

generated from the business (Andersen et al., 2018).

3.5 Alternative Project Evaluation Measures

The key alternative project evaluation measures that the companies should deploy for the

purpose of project evaluation can be the Internal Rate of Return or the IIR method that states the

return for the project in percentage terms. The IRR of the project was determined to be around

38% for the company reflecting the return that the investors would be getting from the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.