Finance for Business: Analysis of Metallic Minerals Company Report

VerifiedAdded on 2020/05/28

|13

|2829

|35

Report

AI Summary

This finance report provides a comprehensive analysis of Metallic Minerals Limited, an Australian bauxite developer. It examines the company's ownership and governance structure, highlighting key individuals and shareholder information. The report delves into the calculation of performance ratios, including return on assets, return on equity, and debt ratios, over a four-year period, providing insights into the company's financial health and operational efficiency. It also explores significant factors influencing the share price, such as mining lease announcements and project developments. Furthermore, the report calculates the beta value and expected rate of return, assessing the investment's risk profile. The weighted average cost of capital is determined, and debt ratios are analyzed. The dividend policy of Metallic Minerals is discussed, along with a letter of recommendation regarding investment potential. The report concludes with a list of references and bibliography, supporting the analysis with credible sources.

Running head: FINANCE FOR BUSINESS

Finance for Business

Name of the university

Name of the student

Authors note

Finance for Business

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCE FOR BUSINESS

Table of Contents

Description of company:..................................................................................................................2

Ownership and governance structure of company:.........................................................................2

Calculation of performance ratios:..................................................................................................3

Significant factors influencing the share price of Metallic Minerals:.............................................6

Calculation of Beta values and expected rate of returns:................................................................6

Weighted average cost of capital:....................................................................................................6

Debt ratios for the past two years:...................................................................................................7

Dividend policy:..............................................................................................................................8

Letter of recommendation:..............................................................................................................8

References and Bibliography list:..................................................................................................10

FINANCE FOR BUSINESS

Table of Contents

Description of company:..................................................................................................................2

Ownership and governance structure of company:.........................................................................2

Calculation of performance ratios:..................................................................................................3

Significant factors influencing the share price of Metallic Minerals:.............................................6

Calculation of Beta values and expected rate of returns:................................................................6

Weighted average cost of capital:....................................................................................................6

Debt ratios for the past two years:...................................................................................................7

Dividend policy:..............................................................................................................................8

Letter of recommendation:..............................................................................................................8

References and Bibliography list:..................................................................................................10

2

FINANCE FOR BUSINESS

Description of company:

Metallic Minerals Limited is a bauxite developer of Australia that has assets based in

Cape York Peninsula of Queensland. Currently, company is concentrating on development and

production of its bauxite assets and is transitioning from exploration of minerals. It would help

organization in fulfilling the goal of becoming a sustainable, successful and profitable bauxite

mine producer. Opportunities to unlock the value from noncore assets are being investigated by

company that will help in generating revenue and increase production efficiency. Some of the

operations that are owned by company involve Urquhart bauxite project, HMS exploration, Cape

York regional bauxite and Urquhart point HMS project (metallicaminerals.com.au, 2018). It has

been indicated by Urquhart bauxite project that there will be potential for delivering strong

financial returns with minimum capital expenditure. Organization has received approval from

Commonwealth and Queensland government for mining lease. It is also seeking approval from

government regarding haul road. Cash reserves of company have been bolstered by availability

of standby credit facility, conversion of options and completion of right issue

(metallicaminerals.com.au, 2018).

Ownership and governance structure of company:

The board of directors of metallic minerals comprised of two non-executive directors,

non-executive chairman and alternate non executive director. There are no substantial

shareholders having higher than 20% of shareholders and the shareholder having higher than 5%

of shareholdings is Jien mining Pty limited. It can be seen that there are no shareholders having

more than 20% of shares and hence it can be concluded that company is a non-family company.

FINANCE FOR BUSINESS

Description of company:

Metallic Minerals Limited is a bauxite developer of Australia that has assets based in

Cape York Peninsula of Queensland. Currently, company is concentrating on development and

production of its bauxite assets and is transitioning from exploration of minerals. It would help

organization in fulfilling the goal of becoming a sustainable, successful and profitable bauxite

mine producer. Opportunities to unlock the value from noncore assets are being investigated by

company that will help in generating revenue and increase production efficiency. Some of the

operations that are owned by company involve Urquhart bauxite project, HMS exploration, Cape

York regional bauxite and Urquhart point HMS project (metallicaminerals.com.au, 2018). It has

been indicated by Urquhart bauxite project that there will be potential for delivering strong

financial returns with minimum capital expenditure. Organization has received approval from

Commonwealth and Queensland government for mining lease. It is also seeking approval from

government regarding haul road. Cash reserves of company have been bolstered by availability

of standby credit facility, conversion of options and completion of right issue

(metallicaminerals.com.au, 2018).

Ownership and governance structure of company:

The board of directors of metallic minerals comprised of two non-executive directors,

non-executive chairman and alternate non executive director. There are no substantial

shareholders having higher than 20% of shareholders and the shareholder having higher than 5%

of shareholdings is Jien mining Pty limited. It can be seen that there are no shareholders having

more than 20% of shares and hence it can be concluded that company is a non-family company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCE FOR BUSINESS

Main people involved in governance firms are non-executive chairman, non executive

director and alternate non executive director.

Chairman of metallic minerals is Mr, Wang ruobing and he is the largest shareholder of

company through its Australian subsidiary. CEO of company is Steve Boulton that has

experience in this position over past fifteen years. Other board members include Peter Turnbull

who is the non-executive director of company and he has enabled development of business on a

global perspective and has considerable experience in commercialization and digital economy.

John Haley is the chief financial officer and company secretary and Simon Slesarewich is chief

executive officer (metallicaminerals.com.au, 2018). It can be seen that surname of substantial

shareholders do not have same surname as that of any members of board of directors. Yes, one

shareholder having highest number of shares is involved in the governance of metallic minerals.

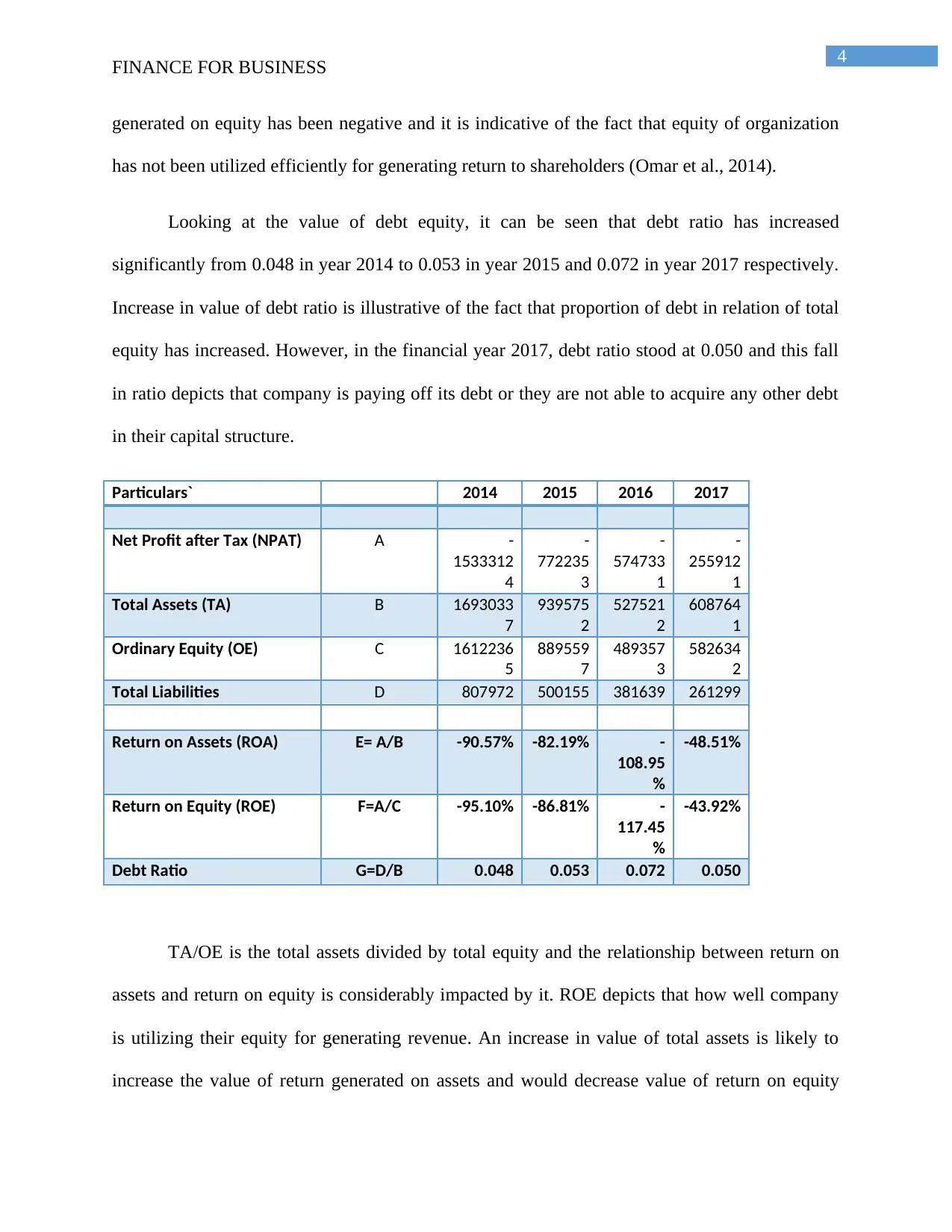

Calculation of performance ratios:

The performance of metallic minerals has been evaluated by computation of key

performance ratios such as return on assets, debt ratio and return on equity. Return on assets for

company for four consecutive years is negative. Value is computed at -90.57% in year 2014 and

this has increased to 108.95% in year 2015 and -48.5% in year 2016 respectively. This negative

value is indicative of the fact that assets are not utilized profitably for generating revenue.

Return on equity for metallic minerals in year 2014 and 2015 stood at -95.10% and -

86.81% respectively. This value has increased significantly in year -117.45% in year 2016 and

has reduced to -43.92% in year 2017. There has been improvement in return generated from

equity in sense of increasing utilization of shareholder equity. However, value of return

FINANCE FOR BUSINESS

Main people involved in governance firms are non-executive chairman, non executive

director and alternate non executive director.

Chairman of metallic minerals is Mr, Wang ruobing and he is the largest shareholder of

company through its Australian subsidiary. CEO of company is Steve Boulton that has

experience in this position over past fifteen years. Other board members include Peter Turnbull

who is the non-executive director of company and he has enabled development of business on a

global perspective and has considerable experience in commercialization and digital economy.

John Haley is the chief financial officer and company secretary and Simon Slesarewich is chief

executive officer (metallicaminerals.com.au, 2018). It can be seen that surname of substantial

shareholders do not have same surname as that of any members of board of directors. Yes, one

shareholder having highest number of shares is involved in the governance of metallic minerals.

Calculation of performance ratios:

The performance of metallic minerals has been evaluated by computation of key

performance ratios such as return on assets, debt ratio and return on equity. Return on assets for

company for four consecutive years is negative. Value is computed at -90.57% in year 2014 and

this has increased to 108.95% in year 2015 and -48.5% in year 2016 respectively. This negative

value is indicative of the fact that assets are not utilized profitably for generating revenue.

Return on equity for metallic minerals in year 2014 and 2015 stood at -95.10% and -

86.81% respectively. This value has increased significantly in year -117.45% in year 2016 and

has reduced to -43.92% in year 2017. There has been improvement in return generated from

equity in sense of increasing utilization of shareholder equity. However, value of return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCE FOR BUSINESS

generated on equity has been negative and it is indicative of the fact that equity of organization

has not been utilized efficiently for generating return to shareholders (Omar et al., 2014).

Looking at the value of debt equity, it can be seen that debt ratio has increased

significantly from 0.048 in year 2014 to 0.053 in year 2015 and 0.072 in year 2017 respectively.

Increase in value of debt ratio is illustrative of the fact that proportion of debt in relation of total

equity has increased. However, in the financial year 2017, debt ratio stood at 0.050 and this fall

in ratio depicts that company is paying off its debt or they are not able to acquire any other debt

in their capital structure.

Particulars` 2014 2015 2016 2017

Net Profit after Tax (NPAT) A -

1533312

4

-

772235

3

-

574733

1

-

255912

1

Total Assets (TA) B 1693033

7

939575

2

527521

2

608764

1

Ordinary Equity (OE) C 1612236

5

889559

7

489357

3

582634

2

Total Liabilities D 807972 500155 381639 261299

Return on Assets (ROA) E= A/B -90.57% -82.19% -

108.95

%

-48.51%

Return on Equity (ROE) F=A/C -95.10% -86.81% -

117.45

%

-43.92%

Debt Ratio G=D/B 0.048 0.053 0.072 0.050

TA/OE is the total assets divided by total equity and the relationship between return on

assets and return on equity is considerably impacted by it. ROE depicts that how well company

is utilizing their equity for generating revenue. An increase in value of total assets is likely to

increase the value of return generated on assets and would decrease value of return on equity

FINANCE FOR BUSINESS

generated on equity has been negative and it is indicative of the fact that equity of organization

has not been utilized efficiently for generating return to shareholders (Omar et al., 2014).

Looking at the value of debt equity, it can be seen that debt ratio has increased

significantly from 0.048 in year 2014 to 0.053 in year 2015 and 0.072 in year 2017 respectively.

Increase in value of debt ratio is illustrative of the fact that proportion of debt in relation of total

equity has increased. However, in the financial year 2017, debt ratio stood at 0.050 and this fall

in ratio depicts that company is paying off its debt or they are not able to acquire any other debt

in their capital structure.

Particulars` 2014 2015 2016 2017

Net Profit after Tax (NPAT) A -

1533312

4

-

772235

3

-

574733

1

-

255912

1

Total Assets (TA) B 1693033

7

939575

2

527521

2

608764

1

Ordinary Equity (OE) C 1612236

5

889559

7

489357

3

582634

2

Total Liabilities D 807972 500155 381639 261299

Return on Assets (ROA) E= A/B -90.57% -82.19% -

108.95

%

-48.51%

Return on Equity (ROE) F=A/C -95.10% -86.81% -

117.45

%

-43.92%

Debt Ratio G=D/B 0.048 0.053 0.072 0.050

TA/OE is the total assets divided by total equity and the relationship between return on

assets and return on equity is considerably impacted by it. ROE depicts that how well company

is utilizing their equity for generating revenue. An increase in value of total assets is likely to

increase the value of return generated on assets and would decrease value of return on equity

5

FINANCE FOR BUSINESS

provided there is an increase in profit generated by company (Renneboog & Szilagyi, 2015). If

the company generates negative profits, then the impact on ROA and ROE would be negative.

ROA is greater than ROE because the value of total assets is more than value of ordinary

equities. Throughout the years of analysis, value of assets has exceeded value of equities;

however, their individual value has been declining.

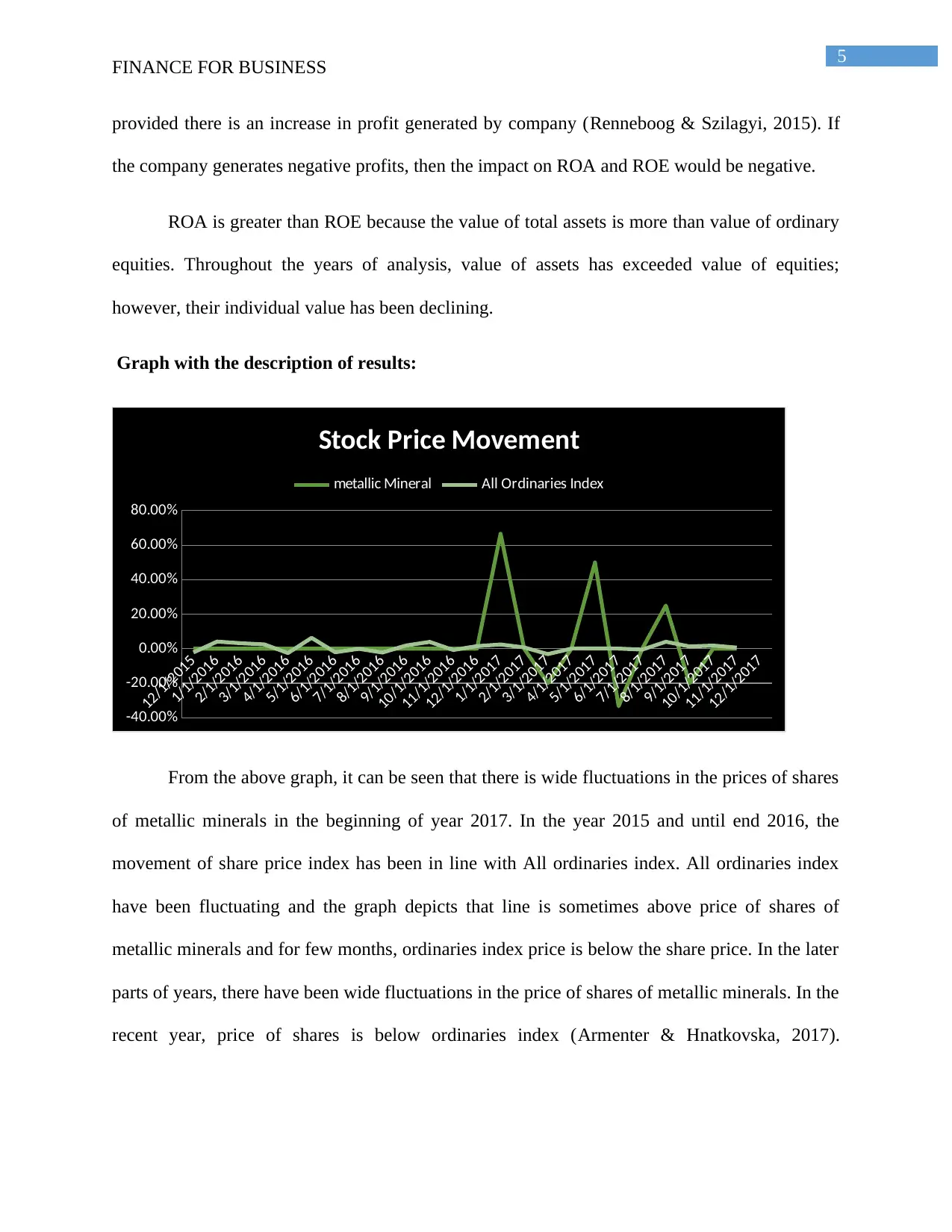

Graph with the description of results:

12/1/2015

1/1/2016

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

1/1/2017

2/1/2017

3/1/2017

4/1/2017

5/1/2017

6/1/2017

7/1/2017

8/1/2017

9/1/2017

10/1/2017

11/1/2017

12/1/2017

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

Stock Price Movement

metallic Mineral All Ordinaries Index

From the above graph, it can be seen that there is wide fluctuations in the prices of shares

of metallic minerals in the beginning of year 2017. In the year 2015 and until end 2016, the

movement of share price index has been in line with All ordinaries index. All ordinaries index

have been fluctuating and the graph depicts that line is sometimes above price of shares of

metallic minerals and for few months, ordinaries index price is below the share price. In the later

parts of years, there have been wide fluctuations in the price of shares of metallic minerals. In the

recent year, price of shares is below ordinaries index (Armenter & Hnatkovska, 2017).

FINANCE FOR BUSINESS

provided there is an increase in profit generated by company (Renneboog & Szilagyi, 2015). If

the company generates negative profits, then the impact on ROA and ROE would be negative.

ROA is greater than ROE because the value of total assets is more than value of ordinary

equities. Throughout the years of analysis, value of assets has exceeded value of equities;

however, their individual value has been declining.

Graph with the description of results:

12/1/2015

1/1/2016

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

1/1/2017

2/1/2017

3/1/2017

4/1/2017

5/1/2017

6/1/2017

7/1/2017

8/1/2017

9/1/2017

10/1/2017

11/1/2017

12/1/2017

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

Stock Price Movement

metallic Mineral All Ordinaries Index

From the above graph, it can be seen that there is wide fluctuations in the prices of shares

of metallic minerals in the beginning of year 2017. In the year 2015 and until end 2016, the

movement of share price index has been in line with All ordinaries index. All ordinaries index

have been fluctuating and the graph depicts that line is sometimes above price of shares of

metallic minerals and for few months, ordinaries index price is below the share price. In the later

parts of years, there have been wide fluctuations in the price of shares of metallic minerals. In the

recent year, price of shares is below ordinaries index (Armenter & Hnatkovska, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCE FOR BUSINESS

Therefore, in recent years, there has been much wider volatility in share price and in the

beginning year, share price line is closely related.

Significant factors influencing the share price of Metallic Minerals:

Share price of Metallic minerals is influenced by the announcement made by company

regarding grant of mining lease by the State government. Development of Urquhart bauxite has

been done by imposition of development and conditions. The appointment of haulage and mining

contractors are done in the project of bauxite and the project is fully funded. Some of the projects

is being evaluated by company for the acquisition purpose. Australian mine shares are expected

to be granted to metallic minerals on the completion of definitive feasibility study is also likely

to influence share price (Faccio & Xu, 2015). Therefore, the share price of organization has the

likelihood of impacting by their strategically decisions.

Calculation of Beta values and expected rate of returns:

Particulars Amount

Beta of the company A 1.15

Risk Free Rate B 4%

Market Risk Premium C 6%

Required Rate of

Return

D=B+[Ax(C-

B)]

6.30%

The investment of company is determined by the value of beta and beta value being 1.15

indicates that investment strategy is aggressive. Value of beta is higher and it depicts that there is

higher volatility along with higher return and higher risks. Investors who are risk averse would

not like to make investment in this company.

FINANCE FOR BUSINESS

Therefore, in recent years, there has been much wider volatility in share price and in the

beginning year, share price line is closely related.

Significant factors influencing the share price of Metallic Minerals:

Share price of Metallic minerals is influenced by the announcement made by company

regarding grant of mining lease by the State government. Development of Urquhart bauxite has

been done by imposition of development and conditions. The appointment of haulage and mining

contractors are done in the project of bauxite and the project is fully funded. Some of the projects

is being evaluated by company for the acquisition purpose. Australian mine shares are expected

to be granted to metallic minerals on the completion of definitive feasibility study is also likely

to influence share price (Faccio & Xu, 2015). Therefore, the share price of organization has the

likelihood of impacting by their strategically decisions.

Calculation of Beta values and expected rate of returns:

Particulars Amount

Beta of the company A 1.15

Risk Free Rate B 4%

Market Risk Premium C 6%

Required Rate of

Return

D=B+[Ax(C-

B)]

6.30%

The investment of company is determined by the value of beta and beta value being 1.15

indicates that investment strategy is aggressive. Value of beta is higher and it depicts that there is

higher volatility along with higher return and higher risks. Investors who are risk averse would

not like to make investment in this company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCE FOR BUSINESS

Weighted average cost of capital:

Particulars Amount

Weightag

e Cost Return Rate

Tax

Rate WACC

Total Long Term Debt 0 0.00% 0

0.000000000

%

30.00

% 0.00%

Total Equity 5826342 100.00% 6.30% 6.30%

TOTAL 5826342 100% 6.30%

It can be seen that there is no long-term debt attributable to company in the current year

and hence cost of equity will be equal to weighted average cost of capital. Therefore, WACC is

same of cost of equity of 6.30%.

WACC is the composite cost of capital that is used by investors in evaluating the project

undertaken by company. This particular measure helps in forming estimation about

organization’s expected cost. Computation of capital budgeting is the discount rate used by

company. Whether company should undertake any project is terms of risk of compensation and

return generated. Higher risks are generated by higher value of WACC and for undertaking

additional amount of risks, investors should be provided with higher return (Hamza & Hassan,

2017).

Debt ratios for the past two years:

Debt ratios for the past two years of Metallic minerals stood at 0.072 and 0.050 for

financial year 2016 and 2017 respectively. There has not been any stability in value of dividend

and in the current situation; the capital structure of organization cannot be evaluated using the

value of total equity (Graham and Sathye, 2017). It is so because company is incurring loss year

after year and the company cannot seek any further long-term borrowing.

FINANCE FOR BUSINESS

Weighted average cost of capital:

Particulars Amount

Weightag

e Cost Return Rate

Tax

Rate WACC

Total Long Term Debt 0 0.00% 0

0.000000000

%

30.00

% 0.00%

Total Equity 5826342 100.00% 6.30% 6.30%

TOTAL 5826342 100% 6.30%

It can be seen that there is no long-term debt attributable to company in the current year

and hence cost of equity will be equal to weighted average cost of capital. Therefore, WACC is

same of cost of equity of 6.30%.

WACC is the composite cost of capital that is used by investors in evaluating the project

undertaken by company. This particular measure helps in forming estimation about

organization’s expected cost. Computation of capital budgeting is the discount rate used by

company. Whether company should undertake any project is terms of risk of compensation and

return generated. Higher risks are generated by higher value of WACC and for undertaking

additional amount of risks, investors should be provided with higher return (Hamza & Hassan,

2017).

Debt ratios for the past two years:

Debt ratios for the past two years of Metallic minerals stood at 0.072 and 0.050 for

financial year 2016 and 2017 respectively. There has not been any stability in value of dividend

and in the current situation; the capital structure of organization cannot be evaluated using the

value of total equity (Graham and Sathye, 2017). It is so because company is incurring loss year

after year and the company cannot seek any further long-term borrowing.

8

FINANCE FOR BUSINESS

Dividend policy:

Dividend policy of Metallic minerals has been implemented in accordance with

Corporation Act and as per rules that are listed on Australian stock exchange. Payment of

dividend to shareholder have incorporated the guidelines and this ensures that share price of

metallic mineral will be traded fairly. Payment of dividend has not been recognized in the

financial statement for the year ending 30th June, 2017. As per the dividend policy of company,

ordinary shareholders are entitled to participate in dividend payments. Company for avoiding

any kind of compliance issues does principles prescribing the implementation of dividend policy

(Chittenden and Derregia, 2015).

Letter of recommendation:

Dear XYZ

Queensland

Australia

Respected Sir,

I would like to give an opinion of making investments in shares of metallic minerals after

conducting a detailed analysis and evaluation of company in terms of their capital, debt structure,

financial leverage and share price. From the computation of ratios, it can be inferred that both

return on assets and return on equity is negative and this is indicative of the fact that organization

are not able to efficiently utilize their underlying assets and shareholders’ equity. Debt ratio has

decreased in recent year because of decline in total value of liabilities. This depicts that liabilities

are being paid and there is no further acquisition of long-term borrowing. Moreover, metallic

minerals is generating year on year loss and this is not favorable for investors willing to make

FINANCE FOR BUSINESS

Dividend policy:

Dividend policy of Metallic minerals has been implemented in accordance with

Corporation Act and as per rules that are listed on Australian stock exchange. Payment of

dividend to shareholder have incorporated the guidelines and this ensures that share price of

metallic mineral will be traded fairly. Payment of dividend has not been recognized in the

financial statement for the year ending 30th June, 2017. As per the dividend policy of company,

ordinary shareholders are entitled to participate in dividend payments. Company for avoiding

any kind of compliance issues does principles prescribing the implementation of dividend policy

(Chittenden and Derregia, 2015).

Letter of recommendation:

Dear XYZ

Queensland

Australia

Respected Sir,

I would like to give an opinion of making investments in shares of metallic minerals after

conducting a detailed analysis and evaluation of company in terms of their capital, debt structure,

financial leverage and share price. From the computation of ratios, it can be inferred that both

return on assets and return on equity is negative and this is indicative of the fact that organization

are not able to efficiently utilize their underlying assets and shareholders’ equity. Debt ratio has

decreased in recent year because of decline in total value of liabilities. This depicts that liabilities

are being paid and there is no further acquisition of long-term borrowing. Moreover, metallic

minerals is generating year on year loss and this is not favorable for investors willing to make

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCE FOR BUSINESS

investment in this company (Minnis & Sutherland, 2017). Furthermore, share price of company

has been highly volatile from 0.03 in year 2015 to end of year 2017. Therefore, investing in

stocks of Metallic mineral would be risky and thereby it has the possibility of not generating

favorable to investors in recent years.

Therefore, as part of recommendation to XYZ, investment in this company should be

avoided and currently they should not involve shares of this company into their portfolio of

investment.

Thanking you,

LMN

Investment Company

FINANCE FOR BUSINESS

investment in this company (Minnis & Sutherland, 2017). Furthermore, share price of company

has been highly volatile from 0.03 in year 2015 to end of year 2017. Therefore, investing in

stocks of Metallic mineral would be risky and thereby it has the possibility of not generating

favorable to investors in recent years.

Therefore, as part of recommendation to XYZ, investment in this company should be

avoided and currently they should not involve shares of this company into their portfolio of

investment.

Thanking you,

LMN

Investment Company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCE FOR BUSINESS

References and Bibliography list:

Armenter, R., & Hnatkovska, V. (2017). Taxes and capital structure: Understanding firms’

savings. Journal of Monetary Economics, 87, 13-33.

Breuer, W., Rieger, M. O., & Soypak, K. C. (2014). The behavioral foundations of corporate

dividend policy a cross-country analysis. Journal of Banking & Finance, 42, 247-265.

Cao, M., Chychyla, R., & Stewart, T. (2015). Big Data analytics in financial statement audits.

Accounting Horizons, 29(2), 423-429.

Chittenden, F. and Derregia, M., 2015. Uncertainty, irreversibility and the use of ‘rules of

thumb’in capital budgeting. The British Accounting Review, 47(3), pp.225-236.

Faccio, M., & Xu, J. (2015). Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), 277-300.

Graham, P.J. and Sathye, M., 2017. Does National Culture Impact Capital Budgeting Systems?.

Australasian Accounting Business & Finance Journal, 11(2).

Hamza, S. M., & Hassan, Z. (2017). IMPACT OF DIVIDEND POLICY ON SHAREHOLDERS

WEALTH: A COMPARATIVE STUDY AMONG DIVIDEND PAYING AND NON-

PAYING TECHNOLOGY BASED FIRM’S IN USA. International Journal of

Information, Business and Management, 9(3), 1

Jagongo, A. O., & Mutswenje, V. S. (2014). A survey of the factors influencing investment

decisions: the case of individual investors at the NSE.

Mbabazize, P.M. and Daniel, T., 2014. Capital Budgeting Practices In Developing Countries: A

Case Of Rwanda. Research journali’s Journal of Finance vol. 2 No 3 Hal. 34, 38.

FINANCE FOR BUSINESS

References and Bibliography list:

Armenter, R., & Hnatkovska, V. (2017). Taxes and capital structure: Understanding firms’

savings. Journal of Monetary Economics, 87, 13-33.

Breuer, W., Rieger, M. O., & Soypak, K. C. (2014). The behavioral foundations of corporate

dividend policy a cross-country analysis. Journal of Banking & Finance, 42, 247-265.

Cao, M., Chychyla, R., & Stewart, T. (2015). Big Data analytics in financial statement audits.

Accounting Horizons, 29(2), 423-429.

Chittenden, F. and Derregia, M., 2015. Uncertainty, irreversibility and the use of ‘rules of

thumb’in capital budgeting. The British Accounting Review, 47(3), pp.225-236.

Faccio, M., & Xu, J. (2015). Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), 277-300.

Graham, P.J. and Sathye, M., 2017. Does National Culture Impact Capital Budgeting Systems?.

Australasian Accounting Business & Finance Journal, 11(2).

Hamza, S. M., & Hassan, Z. (2017). IMPACT OF DIVIDEND POLICY ON SHAREHOLDERS

WEALTH: A COMPARATIVE STUDY AMONG DIVIDEND PAYING AND NON-

PAYING TECHNOLOGY BASED FIRM’S IN USA. International Journal of

Information, Business and Management, 9(3), 1

Jagongo, A. O., & Mutswenje, V. S. (2014). A survey of the factors influencing investment

decisions: the case of individual investors at the NSE.

Mbabazize, P.M. and Daniel, T., 2014. Capital Budgeting Practices In Developing Countries: A

Case Of Rwanda. Research journali’s Journal of Finance vol. 2 No 3 Hal. 34, 38.

11

FINANCE FOR BUSINESS

Metallicaminerals.com.au. (2018). Retrieved 22 January 2018, from

http://www.metallicaminerals.com.au/wp-content/uploads/2016/09/Metallica-Minerals-

Limited-Annual-Financial-Report-30062017.pdf

Michaely, R., & Qian, M. (2016). Stock Liquidity and Dividend Policy: Evidence from a Natural

Experiment.

Minnis, M., & Sutherland, A. (2017). Financial statements as monitoring mechanisms: Evidence

from small commercial loans. Journal of Accounting Research, 55(1), 197-233.

Omar, N., Koya, R. K., Sanusi, Z. M., & Shafie, N. A. (2014). Financial statement fraud: A case

examination using Beneish Model and ratio analysis. International Journal of Trade,

Economics and Finance, 5(2), 184.

Renneboog, L., & Szilagyi, P. G. (2015). How relevant is dividend policy under low shareholder

protection?. Journal of International Financial Markets, Institutions and Money.

Robb, A. M., & Robinson, D. T. (2014). The capital structure decisions of new firms. The

Review of Financial Studies, 27(1), 153-179.

Rossi, M. (2015). The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), 43-56.

Sari, I.U. and Kahraman, C., 2015. Interval type-2 fuzzy capital budgeting. International Journal

of Fuzzy Systems, 17(4), pp.635-646.

Schmidlin, N. (2014). The Art of Company Valuation and Financial Statement Analysis: A value

investor's guide with real-life case studies. John Wiley & Sons

FINANCE FOR BUSINESS

Metallicaminerals.com.au. (2018). Retrieved 22 January 2018, from

http://www.metallicaminerals.com.au/wp-content/uploads/2016/09/Metallica-Minerals-

Limited-Annual-Financial-Report-30062017.pdf

Michaely, R., & Qian, M. (2016). Stock Liquidity and Dividend Policy: Evidence from a Natural

Experiment.

Minnis, M., & Sutherland, A. (2017). Financial statements as monitoring mechanisms: Evidence

from small commercial loans. Journal of Accounting Research, 55(1), 197-233.

Omar, N., Koya, R. K., Sanusi, Z. M., & Shafie, N. A. (2014). Financial statement fraud: A case

examination using Beneish Model and ratio analysis. International Journal of Trade,

Economics and Finance, 5(2), 184.

Renneboog, L., & Szilagyi, P. G. (2015). How relevant is dividend policy under low shareholder

protection?. Journal of International Financial Markets, Institutions and Money.

Robb, A. M., & Robinson, D. T. (2014). The capital structure decisions of new firms. The

Review of Financial Studies, 27(1), 153-179.

Rossi, M. (2015). The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), 43-56.

Sari, I.U. and Kahraman, C., 2015. Interval type-2 fuzzy capital budgeting. International Journal

of Fuzzy Systems, 17(4), pp.635-646.

Schmidlin, N. (2014). The Art of Company Valuation and Financial Statement Analysis: A value

investor's guide with real-life case studies. John Wiley & Sons

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.