Finance for Business: Analysis of Westpac Banking Corporation and Bank of Queensland

VerifiedAdded on 2023/04/23

|18

|4492

|206

AI Summary

This report analyses the profitability and liquidity positions of Westpac Banking Corporation and Bank of Queensland, along with share price movement analysis and recommendation for investment opportunities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE FOR BUSINESS

Finance for Business

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Finance for Business

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCE FOR BUSINESS

Executive Summary:

The current report has focused on the perspective of a foreign institutional investor planning to

invest in the Australian market. Therefore, the two organisations that have been selected for this

assignment operate in the banking sector of Australia. They include Westpac Banking

Corporation and Bank of Queensland. Westpac is observed to be placed in a better position in

terms of profitability position than the Bank of Queensland in the Australian market. In terms of

long-term liquidity or solvency, Westpac is placed in a favourable position in the Australian

banking sector compared to the Bank of Queensland. The composition of capital structure of

Westpac has changed over the three-year period, in which the depth exposure has fallen over the

three-year period, while there has been rise in exposure of equity. Therefore, the investor is

recommended to invest in the shares of Westpac Banking Corporation for maximising the overall

return on investment.

Executive Summary:

The current report has focused on the perspective of a foreign institutional investor planning to

invest in the Australian market. Therefore, the two organisations that have been selected for this

assignment operate in the banking sector of Australia. They include Westpac Banking

Corporation and Bank of Queensland. Westpac is observed to be placed in a better position in

terms of profitability position than the Bank of Queensland in the Australian market. In terms of

long-term liquidity or solvency, Westpac is placed in a favourable position in the Australian

banking sector compared to the Bank of Queensland. The composition of capital structure of

Westpac has changed over the three-year period, in which the depth exposure has fallen over the

three-year period, while there has been rise in exposure of equity. Therefore, the investor is

recommended to invest in the shares of Westpac Banking Corporation for maximising the overall

return on investment.

2FINANCE FOR BUSINESS

Table of Contents

Introduction:....................................................................................................................................3

1. Description of the chosen companies:.........................................................................................3

2. Calculation and comparison of selected performance ratios:......................................................4

3. Share price movement analysis:..................................................................................................8

4. Calculation and analysis of weighted average cost of capital (WACC):...................................10

5. Capital structure policy:.............................................................................................................12

6. Recommendation letter:.............................................................................................................12

Conclusion:....................................................................................................................................13

References and Bibliographies:.....................................................................................................15

Table of Contents

Introduction:....................................................................................................................................3

1. Description of the chosen companies:.........................................................................................3

2. Calculation and comparison of selected performance ratios:......................................................4

3. Share price movement analysis:..................................................................................................8

4. Calculation and analysis of weighted average cost of capital (WACC):...................................10

5. Capital structure policy:.............................................................................................................12

6. Recommendation letter:.............................................................................................................12

Conclusion:....................................................................................................................................13

References and Bibliographies:.....................................................................................................15

3FINANCE FOR BUSINESS

Introduction:

The current report would focus from the perspective of a foreign institutional investor

planning to invest in the Australian market. Therefore, the two organisations that have been

selected for this assignment operate in the banking sector of Australia. They include Westpac

Banking Corporation and Bank of Queensland. The first section of the report would provide an

insight of the business operations of the two banks along with comparative advantages. The

second section would concentrate on analysing and contrasting the profitability and liquidity

positions of the two chosen banks for the past three years by extracting the financial information

from their published annual reports. The next part would emphasise on analysing the share price

movement analysis of the two banks to determine the volatility of their stock prices in the ASX

index. In addition, the weighted average cost of capital of the two companies has been analysed

as well as their capital structures. Based on all the above aspects, recommendation letter would

be provided to the concerned investor regarding the investment opportunities in the two banks.

1. Description of the chosen companies:

Westpac Banking Corporation is involved in providing different financial and banking

services in Australia, New Zealand, the Pacific region and global nations. The bank operates in

five divisions, which include Business Bank, Consumer Bank, Westpac Institutional Bank and

Westpac New Zealand. Moreover, the bank offers particular treasury and banking services,

telephone banking, ATMs, travel centre, margin lending and emergency cash. Furthermore, it is

involved in serving micro, small and medium enterprises, individuals, government customers and

others by providing fund management and capital advisory services, which are the main

comparative advantages of the bank. The bank has been established in 1817 with an employee

base of around 35,029 employees (Westpac.com.au 2019).

Bank of Queensland is one of the leading regional banks in Australia and the local

owner-managers run majority of its branches. The bank focuses on maintaining long-term

customer relationships, which are dependent on mutual understanding and respect. The bank has

above 180 branches in Australia and it has developed easy, simple and understandable banking

products for supporting the financial needs of its customers. These products and services are

rendered to the businesses as well as individuals. It falls under the top 100 Australian firms in

Introduction:

The current report would focus from the perspective of a foreign institutional investor

planning to invest in the Australian market. Therefore, the two organisations that have been

selected for this assignment operate in the banking sector of Australia. They include Westpac

Banking Corporation and Bank of Queensland. The first section of the report would provide an

insight of the business operations of the two banks along with comparative advantages. The

second section would concentrate on analysing and contrasting the profitability and liquidity

positions of the two chosen banks for the past three years by extracting the financial information

from their published annual reports. The next part would emphasise on analysing the share price

movement analysis of the two banks to determine the volatility of their stock prices in the ASX

index. In addition, the weighted average cost of capital of the two companies has been analysed

as well as their capital structures. Based on all the above aspects, recommendation letter would

be provided to the concerned investor regarding the investment opportunities in the two banks.

1. Description of the chosen companies:

Westpac Banking Corporation is involved in providing different financial and banking

services in Australia, New Zealand, the Pacific region and global nations. The bank operates in

five divisions, which include Business Bank, Consumer Bank, Westpac Institutional Bank and

Westpac New Zealand. Moreover, the bank offers particular treasury and banking services,

telephone banking, ATMs, travel centre, margin lending and emergency cash. Furthermore, it is

involved in serving micro, small and medium enterprises, individuals, government customers and

others by providing fund management and capital advisory services, which are the main

comparative advantages of the bank. The bank has been established in 1817 with an employee

base of around 35,029 employees (Westpac.com.au 2019).

Bank of Queensland is one of the leading regional banks in Australia and the local

owner-managers run majority of its branches. The bank focuses on maintaining long-term

customer relationships, which are dependent on mutual understanding and respect. The bank has

above 180 branches in Australia and it has developed easy, simple and understandable banking

products for supporting the financial needs of its customers. These products and services are

rendered to the businesses as well as individuals. It falls under the top 100 Australian firms in

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCE FOR BUSINESS

terms of market capitalisation in ASX, which has assisted the bank in gaining comparative

advantage in the market (Boq.com.au 2019).

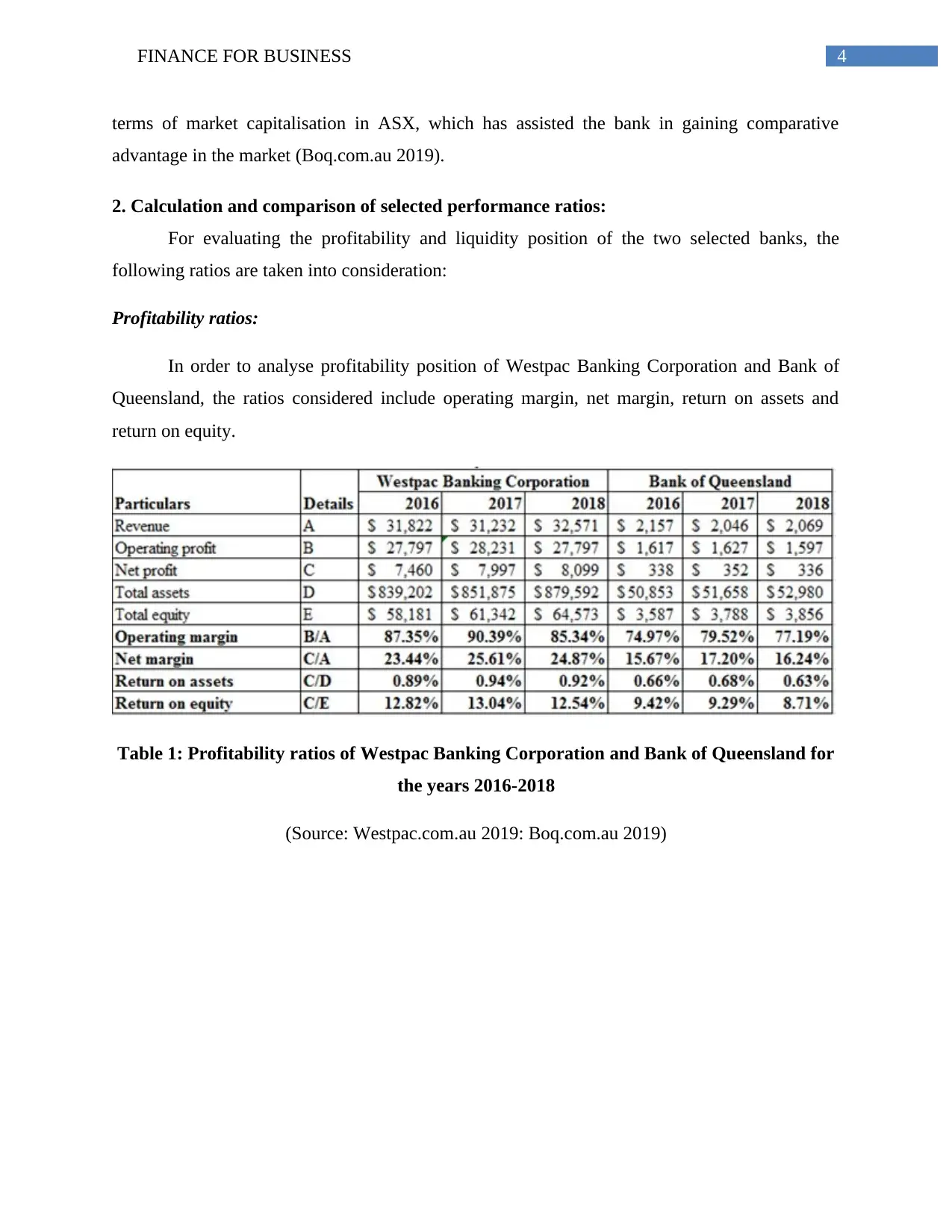

2. Calculation and comparison of selected performance ratios:

For evaluating the profitability and liquidity position of the two selected banks, the

following ratios are taken into consideration:

Profitability ratios:

In order to analyse profitability position of Westpac Banking Corporation and Bank of

Queensland, the ratios considered include operating margin, net margin, return on assets and

return on equity.

Table 1: Profitability ratios of Westpac Banking Corporation and Bank of Queensland for

the years 2016-2018

(Source: Westpac.com.au 2019: Boq.com.au 2019)

terms of market capitalisation in ASX, which has assisted the bank in gaining comparative

advantage in the market (Boq.com.au 2019).

2. Calculation and comparison of selected performance ratios:

For evaluating the profitability and liquidity position of the two selected banks, the

following ratios are taken into consideration:

Profitability ratios:

In order to analyse profitability position of Westpac Banking Corporation and Bank of

Queensland, the ratios considered include operating margin, net margin, return on assets and

return on equity.

Table 1: Profitability ratios of Westpac Banking Corporation and Bank of Queensland for

the years 2016-2018

(Source: Westpac.com.au 2019: Boq.com.au 2019)

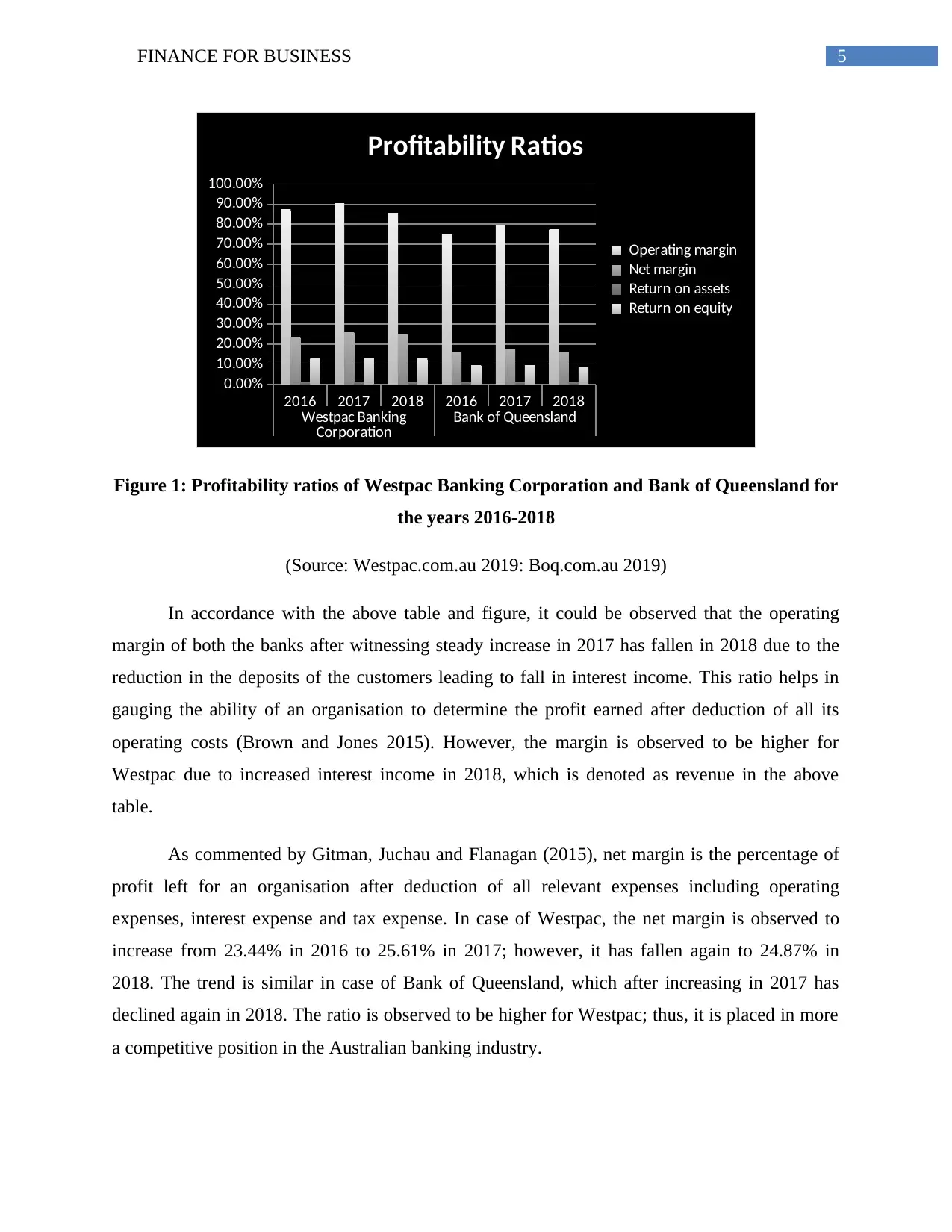

5FINANCE FOR BUSINESS

2016 2017 2018 2016 2017 2018

Westpac Banking

Corporation Bank of Queensland

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Profitability Ratios

Operating margin

Net margin

Return on assets

Return on equity

Figure 1: Profitability ratios of Westpac Banking Corporation and Bank of Queensland for

the years 2016-2018

(Source: Westpac.com.au 2019: Boq.com.au 2019)

In accordance with the above table and figure, it could be observed that the operating

margin of both the banks after witnessing steady increase in 2017 has fallen in 2018 due to the

reduction in the deposits of the customers leading to fall in interest income. This ratio helps in

gauging the ability of an organisation to determine the profit earned after deduction of all its

operating costs (Brown and Jones 2015). However, the margin is observed to be higher for

Westpac due to increased interest income in 2018, which is denoted as revenue in the above

table.

As commented by Gitman, Juchau and Flanagan (2015), net margin is the percentage of

profit left for an organisation after deduction of all relevant expenses including operating

expenses, interest expense and tax expense. In case of Westpac, the net margin is observed to

increase from 23.44% in 2016 to 25.61% in 2017; however, it has fallen again to 24.87% in

2018. The trend is similar in case of Bank of Queensland, which after increasing in 2017 has

declined again in 2018. The ratio is observed to be higher for Westpac; thus, it is placed in more

a competitive position in the Australian banking industry.

2016 2017 2018 2016 2017 2018

Westpac Banking

Corporation Bank of Queensland

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Profitability Ratios

Operating margin

Net margin

Return on assets

Return on equity

Figure 1: Profitability ratios of Westpac Banking Corporation and Bank of Queensland for

the years 2016-2018

(Source: Westpac.com.au 2019: Boq.com.au 2019)

In accordance with the above table and figure, it could be observed that the operating

margin of both the banks after witnessing steady increase in 2017 has fallen in 2018 due to the

reduction in the deposits of the customers leading to fall in interest income. This ratio helps in

gauging the ability of an organisation to determine the profit earned after deduction of all its

operating costs (Brown and Jones 2015). However, the margin is observed to be higher for

Westpac due to increased interest income in 2018, which is denoted as revenue in the above

table.

As commented by Gitman, Juchau and Flanagan (2015), net margin is the percentage of

profit left for an organisation after deduction of all relevant expenses including operating

expenses, interest expense and tax expense. In case of Westpac, the net margin is observed to

increase from 23.44% in 2016 to 25.61% in 2017; however, it has fallen again to 24.87% in

2018. The trend is similar in case of Bank of Queensland, which after increasing in 2017 has

declined again in 2018. The ratio is observed to be higher for Westpac; thus, it is placed in more

a competitive position in the Australian banking industry.

6FINANCE FOR BUSINESS

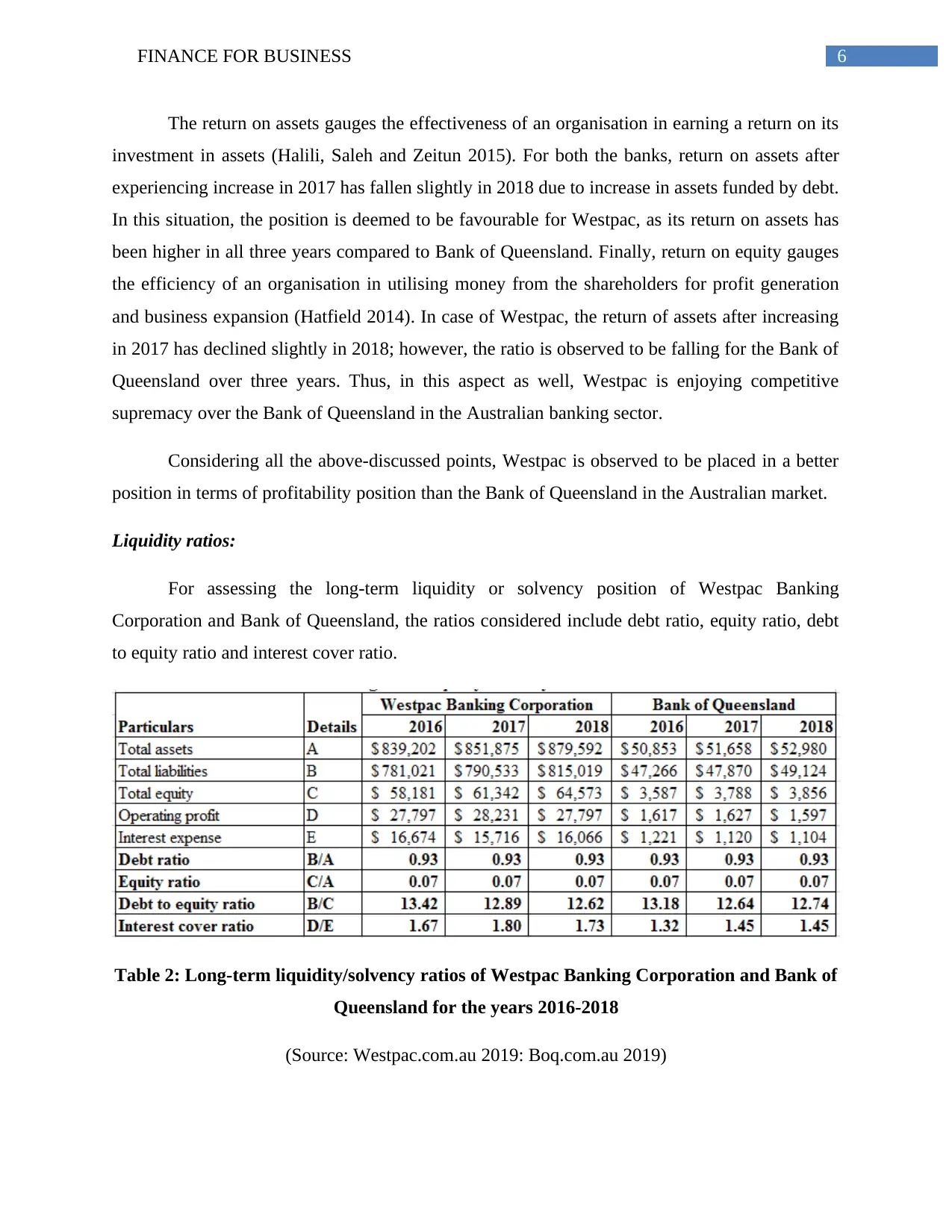

The return on assets gauges the effectiveness of an organisation in earning a return on its

investment in assets (Halili, Saleh and Zeitun 2015). For both the banks, return on assets after

experiencing increase in 2017 has fallen slightly in 2018 due to increase in assets funded by debt.

In this situation, the position is deemed to be favourable for Westpac, as its return on assets has

been higher in all three years compared to Bank of Queensland. Finally, return on equity gauges

the efficiency of an organisation in utilising money from the shareholders for profit generation

and business expansion (Hatfield 2014). In case of Westpac, the return of assets after increasing

in 2017 has declined slightly in 2018; however, the ratio is observed to be falling for the Bank of

Queensland over three years. Thus, in this aspect as well, Westpac is enjoying competitive

supremacy over the Bank of Queensland in the Australian banking sector.

Considering all the above-discussed points, Westpac is observed to be placed in a better

position in terms of profitability position than the Bank of Queensland in the Australian market.

Liquidity ratios:

For assessing the long-term liquidity or solvency position of Westpac Banking

Corporation and Bank of Queensland, the ratios considered include debt ratio, equity ratio, debt

to equity ratio and interest cover ratio.

Table 2: Long-term liquidity/solvency ratios of Westpac Banking Corporation and Bank of

Queensland for the years 2016-2018

(Source: Westpac.com.au 2019: Boq.com.au 2019)

The return on assets gauges the effectiveness of an organisation in earning a return on its

investment in assets (Halili, Saleh and Zeitun 2015). For both the banks, return on assets after

experiencing increase in 2017 has fallen slightly in 2018 due to increase in assets funded by debt.

In this situation, the position is deemed to be favourable for Westpac, as its return on assets has

been higher in all three years compared to Bank of Queensland. Finally, return on equity gauges

the efficiency of an organisation in utilising money from the shareholders for profit generation

and business expansion (Hatfield 2014). In case of Westpac, the return of assets after increasing

in 2017 has declined slightly in 2018; however, the ratio is observed to be falling for the Bank of

Queensland over three years. Thus, in this aspect as well, Westpac is enjoying competitive

supremacy over the Bank of Queensland in the Australian banking sector.

Considering all the above-discussed points, Westpac is observed to be placed in a better

position in terms of profitability position than the Bank of Queensland in the Australian market.

Liquidity ratios:

For assessing the long-term liquidity or solvency position of Westpac Banking

Corporation and Bank of Queensland, the ratios considered include debt ratio, equity ratio, debt

to equity ratio and interest cover ratio.

Table 2: Long-term liquidity/solvency ratios of Westpac Banking Corporation and Bank of

Queensland for the years 2016-2018

(Source: Westpac.com.au 2019: Boq.com.au 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR BUSINESS

2016 2017 2018 2016 2017 2018

Westpac Banking

Corporation Bank of Queensland

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Long-Term Liqudity/Solvency Ratios

Debt ratio

Equity ratio

Debt to equity ratio

Interest cover ratio

Figure 2: Long-term liquidity/solvency ratios of Westpac Banking Corporation and Bank

of Queensland for the years 2016-2018

(Source: Westpac.com.au 2019: Boq.com.au 2019)

Debt ratio is considered as a solvency measure that gauges the proportion of total

liabilities of an organisation as a percentage of total assets (Henderson et al. 2015). It is observed

from the above figure that both banks have same debt ratio of 0.93 in all the three years, which

denote that 93% of the assets of the banks are funded by debt. On the other hand, equity ratio

denotes the percentage of equity out of the total asset base of an organisation (Hirshleifer 2015).

The situation is similar like debt ratio, as 7% of the overall assets of the two banks are funded by

equity.

Debt to equity ratio helps in denoting the proportion of company financing coming from

investors and creditors (Hoyle, Schaefer and Doupnik 2015). This ratio has remained identical

for both the banks, as most of its assets are funded by public deposits and thus, the banks are

prone to increased financial leverage risk. Finally, interest cover ratio helps in denoting the

capability of an organisation to settle off its interest expense with the help of operating profit

(Kaplan and Atkinson 2015). In terms of this ratio, both banks have the ability to clear its interest

expense efficiently due to higher positive operating income; however, the ratio is found to be

slightly higher for Westpac Banking Corporation.

2016 2017 2018 2016 2017 2018

Westpac Banking

Corporation Bank of Queensland

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Long-Term Liqudity/Solvency Ratios

Debt ratio

Equity ratio

Debt to equity ratio

Interest cover ratio

Figure 2: Long-term liquidity/solvency ratios of Westpac Banking Corporation and Bank

of Queensland for the years 2016-2018

(Source: Westpac.com.au 2019: Boq.com.au 2019)

Debt ratio is considered as a solvency measure that gauges the proportion of total

liabilities of an organisation as a percentage of total assets (Henderson et al. 2015). It is observed

from the above figure that both banks have same debt ratio of 0.93 in all the three years, which

denote that 93% of the assets of the banks are funded by debt. On the other hand, equity ratio

denotes the percentage of equity out of the total asset base of an organisation (Hirshleifer 2015).

The situation is similar like debt ratio, as 7% of the overall assets of the two banks are funded by

equity.

Debt to equity ratio helps in denoting the proportion of company financing coming from

investors and creditors (Hoyle, Schaefer and Doupnik 2015). This ratio has remained identical

for both the banks, as most of its assets are funded by public deposits and thus, the banks are

prone to increased financial leverage risk. Finally, interest cover ratio helps in denoting the

capability of an organisation to settle off its interest expense with the help of operating profit

(Kaplan and Atkinson 2015). In terms of this ratio, both banks have the ability to clear its interest

expense efficiently due to higher positive operating income; however, the ratio is found to be

slightly higher for Westpac Banking Corporation.

8FINANCE FOR BUSINESS

Therefore, in terms of long-term liquidity or solvency, Westpac is placed in a favourable

position in the Australian banking sector compared to the Bank of Queensland.

3. Share price movement analysis:

0

5

10

15

20

25

30

35

40

0

1000

2000

3000

4000

5000

6000

7000

Westpac and All Ordinaries Index

Westpac Close All Ordinaries Index

Figure 3: Monthly share price movements of Westpac Banking Corporation in comparison

to All Ordinaries Index for the years 2016-2018

(Source: Au.finance.yahoo.com 2019)

The above figure mainly assists in representing the monthly share price movements of

Westpac Banking Corporation compared to the All Ordinaries Index for three-year period

starting from 2016 to 2018. The analysis directly points out the fact that the entire performance

of Westpac has been declining over the three years. Along with this, the share price of the bank

has failed to complement the rise in share price of the All Ordinaries Index, in which the index

has increased exponentially, while the share price of Westpac has fallen; thus, depicting between

negative correlation between the share price of the bank and the index. The price action of

Westpac has indicated an unfavourable trend, which is expected to fall further in future and thus

would minimise the overall return on investment for the investors. The correlation between the

share price of Westpac and All Ordinaries Index is observed to be -0.211, which indicates that if

Therefore, in terms of long-term liquidity or solvency, Westpac is placed in a favourable

position in the Australian banking sector compared to the Bank of Queensland.

3. Share price movement analysis:

0

5

10

15

20

25

30

35

40

0

1000

2000

3000

4000

5000

6000

7000

Westpac and All Ordinaries Index

Westpac Close All Ordinaries Index

Figure 3: Monthly share price movements of Westpac Banking Corporation in comparison

to All Ordinaries Index for the years 2016-2018

(Source: Au.finance.yahoo.com 2019)

The above figure mainly assists in representing the monthly share price movements of

Westpac Banking Corporation compared to the All Ordinaries Index for three-year period

starting from 2016 to 2018. The analysis directly points out the fact that the entire performance

of Westpac has been declining over the three years. Along with this, the share price of the bank

has failed to complement the rise in share price of the All Ordinaries Index, in which the index

has increased exponentially, while the share price of Westpac has fallen; thus, depicting between

negative correlation between the share price of the bank and the index. The price action of

Westpac has indicated an unfavourable trend, which is expected to fall further in future and thus

would minimise the overall return on investment for the investors. The correlation between the

share price of Westpac and All Ordinaries Index is observed to be -0.211, which indicates that if

9FINANCE FOR BUSINESS

the share price of the index rises, there would be fall in the stock price of Westpac Banking

Corporation and vice-versa.

1/01/2016

1/03/2016

1/05/2016

1/07/2016

1/09/2016

1/11/2016

1/01/2017

1/03/2017

1/05/2017

1/07/2017

1/09/2017

1/11/2017

1/01/2018

1/03/2018

1/05/2018

1/07/2018

1/09/2018

1/11/2018

0

2

4

6

8

10

12

14

16

0

1000

2000

3000

4000

5000

6000

7000

Bank of Queensland and All Ordinaries Index

Bank of Queensland Close All Ordinaries Index

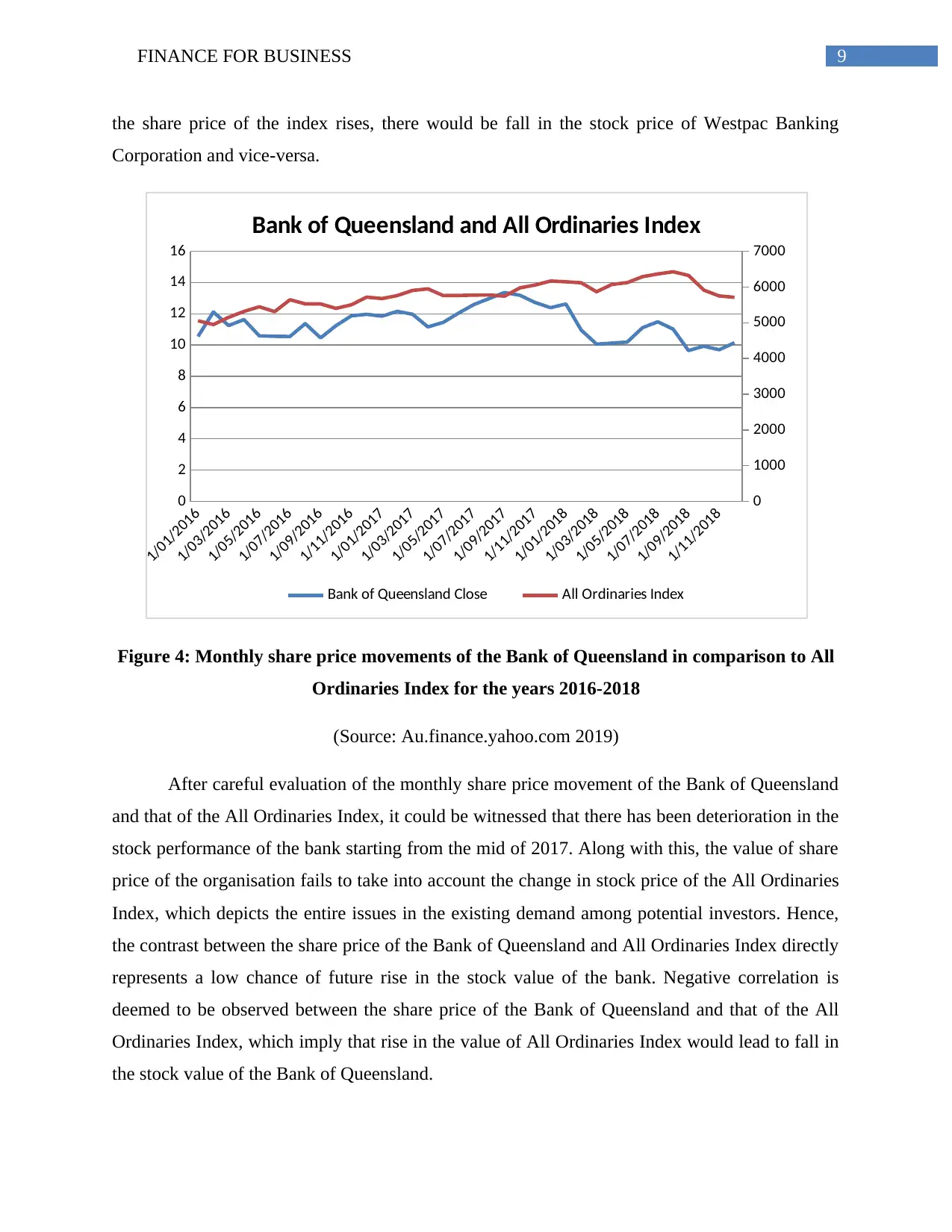

Figure 4: Monthly share price movements of the Bank of Queensland in comparison to All

Ordinaries Index for the years 2016-2018

(Source: Au.finance.yahoo.com 2019)

After careful evaluation of the monthly share price movement of the Bank of Queensland

and that of the All Ordinaries Index, it could be witnessed that there has been deterioration in the

stock performance of the bank starting from the mid of 2017. Along with this, the value of share

price of the organisation fails to take into account the change in stock price of the All Ordinaries

Index, which depicts the entire issues in the existing demand among potential investors. Hence,

the contrast between the share price of the Bank of Queensland and All Ordinaries Index directly

represents a low chance of future rise in the stock value of the bank. Negative correlation is

deemed to be observed between the share price of the Bank of Queensland and that of the All

Ordinaries Index, which imply that rise in the value of All Ordinaries Index would lead to fall in

the stock value of the Bank of Queensland.

the share price of the index rises, there would be fall in the stock price of Westpac Banking

Corporation and vice-versa.

1/01/2016

1/03/2016

1/05/2016

1/07/2016

1/09/2016

1/11/2016

1/01/2017

1/03/2017

1/05/2017

1/07/2017

1/09/2017

1/11/2017

1/01/2018

1/03/2018

1/05/2018

1/07/2018

1/09/2018

1/11/2018

0

2

4

6

8

10

12

14

16

0

1000

2000

3000

4000

5000

6000

7000

Bank of Queensland and All Ordinaries Index

Bank of Queensland Close All Ordinaries Index

Figure 4: Monthly share price movements of the Bank of Queensland in comparison to All

Ordinaries Index for the years 2016-2018

(Source: Au.finance.yahoo.com 2019)

After careful evaluation of the monthly share price movement of the Bank of Queensland

and that of the All Ordinaries Index, it could be witnessed that there has been deterioration in the

stock performance of the bank starting from the mid of 2017. Along with this, the value of share

price of the organisation fails to take into account the change in stock price of the All Ordinaries

Index, which depicts the entire issues in the existing demand among potential investors. Hence,

the contrast between the share price of the Bank of Queensland and All Ordinaries Index directly

represents a low chance of future rise in the stock value of the bank. Negative correlation is

deemed to be observed between the share price of the Bank of Queensland and that of the All

Ordinaries Index, which imply that rise in the value of All Ordinaries Index would lead to fall in

the stock value of the Bank of Queensland.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCE FOR BUSINESS

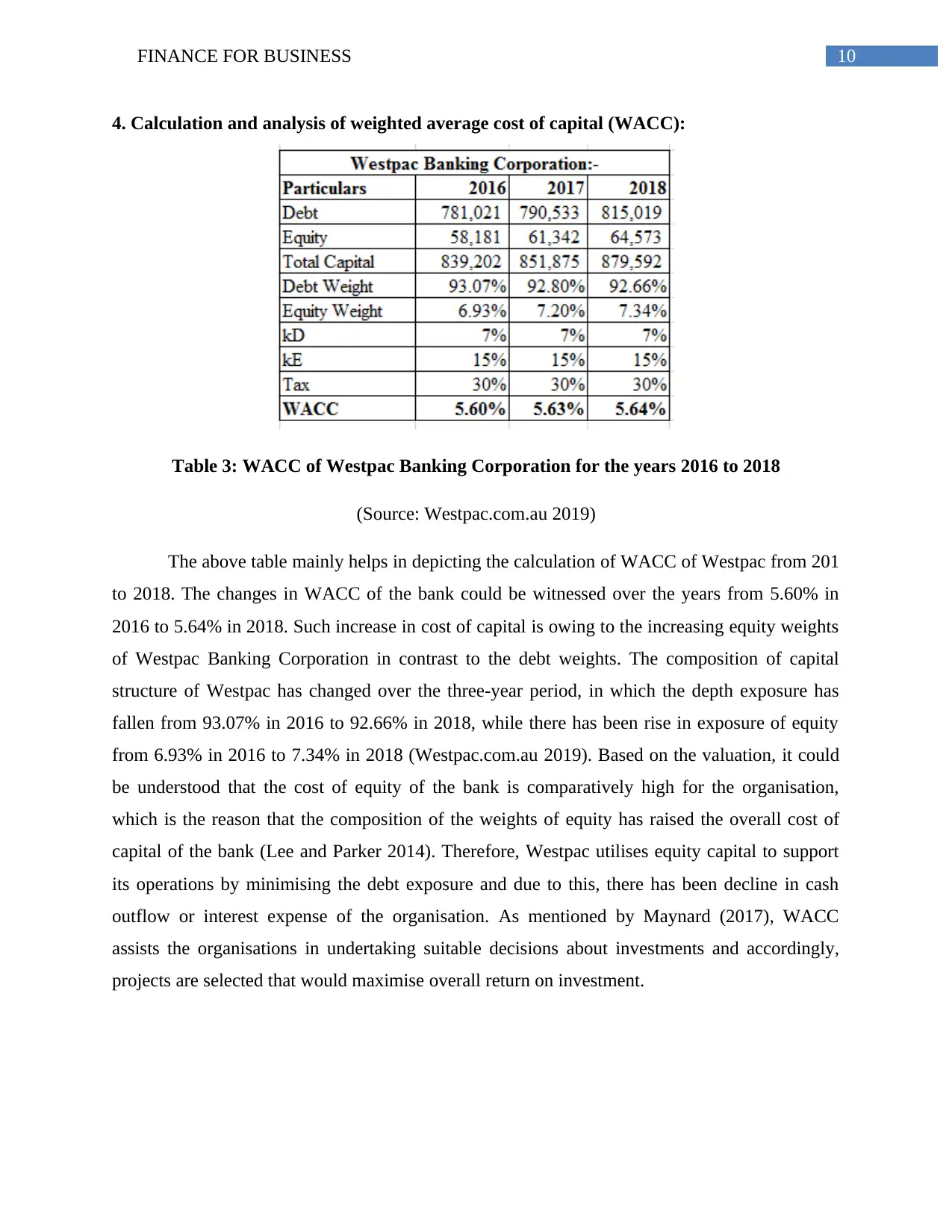

4. Calculation and analysis of weighted average cost of capital (WACC):

Table 3: WACC of Westpac Banking Corporation for the years 2016 to 2018

(Source: Westpac.com.au 2019)

The above table mainly helps in depicting the calculation of WACC of Westpac from 201

to 2018. The changes in WACC of the bank could be witnessed over the years from 5.60% in

2016 to 5.64% in 2018. Such increase in cost of capital is owing to the increasing equity weights

of Westpac Banking Corporation in contrast to the debt weights. The composition of capital

structure of Westpac has changed over the three-year period, in which the depth exposure has

fallen from 93.07% in 2016 to 92.66% in 2018, while there has been rise in exposure of equity

from 6.93% in 2016 to 7.34% in 2018 (Westpac.com.au 2019). Based on the valuation, it could

be understood that the cost of equity of the bank is comparatively high for the organisation,

which is the reason that the composition of the weights of equity has raised the overall cost of

capital of the bank (Lee and Parker 2014). Therefore, Westpac utilises equity capital to support

its operations by minimising the debt exposure and due to this, there has been decline in cash

outflow or interest expense of the organisation. As mentioned by Maynard (2017), WACC

assists the organisations in undertaking suitable decisions about investments and accordingly,

projects are selected that would maximise overall return on investment.

4. Calculation and analysis of weighted average cost of capital (WACC):

Table 3: WACC of Westpac Banking Corporation for the years 2016 to 2018

(Source: Westpac.com.au 2019)

The above table mainly helps in depicting the calculation of WACC of Westpac from 201

to 2018. The changes in WACC of the bank could be witnessed over the years from 5.60% in

2016 to 5.64% in 2018. Such increase in cost of capital is owing to the increasing equity weights

of Westpac Banking Corporation in contrast to the debt weights. The composition of capital

structure of Westpac has changed over the three-year period, in which the depth exposure has

fallen from 93.07% in 2016 to 92.66% in 2018, while there has been rise in exposure of equity

from 6.93% in 2016 to 7.34% in 2018 (Westpac.com.au 2019). Based on the valuation, it could

be understood that the cost of equity of the bank is comparatively high for the organisation,

which is the reason that the composition of the weights of equity has raised the overall cost of

capital of the bank (Lee and Parker 2014). Therefore, Westpac utilises equity capital to support

its operations by minimising the debt exposure and due to this, there has been decline in cash

outflow or interest expense of the organisation. As mentioned by Maynard (2017), WACC

assists the organisations in undertaking suitable decisions about investments and accordingly,

projects are selected that would maximise overall return on investment.

11FINANCE FOR BUSINESS

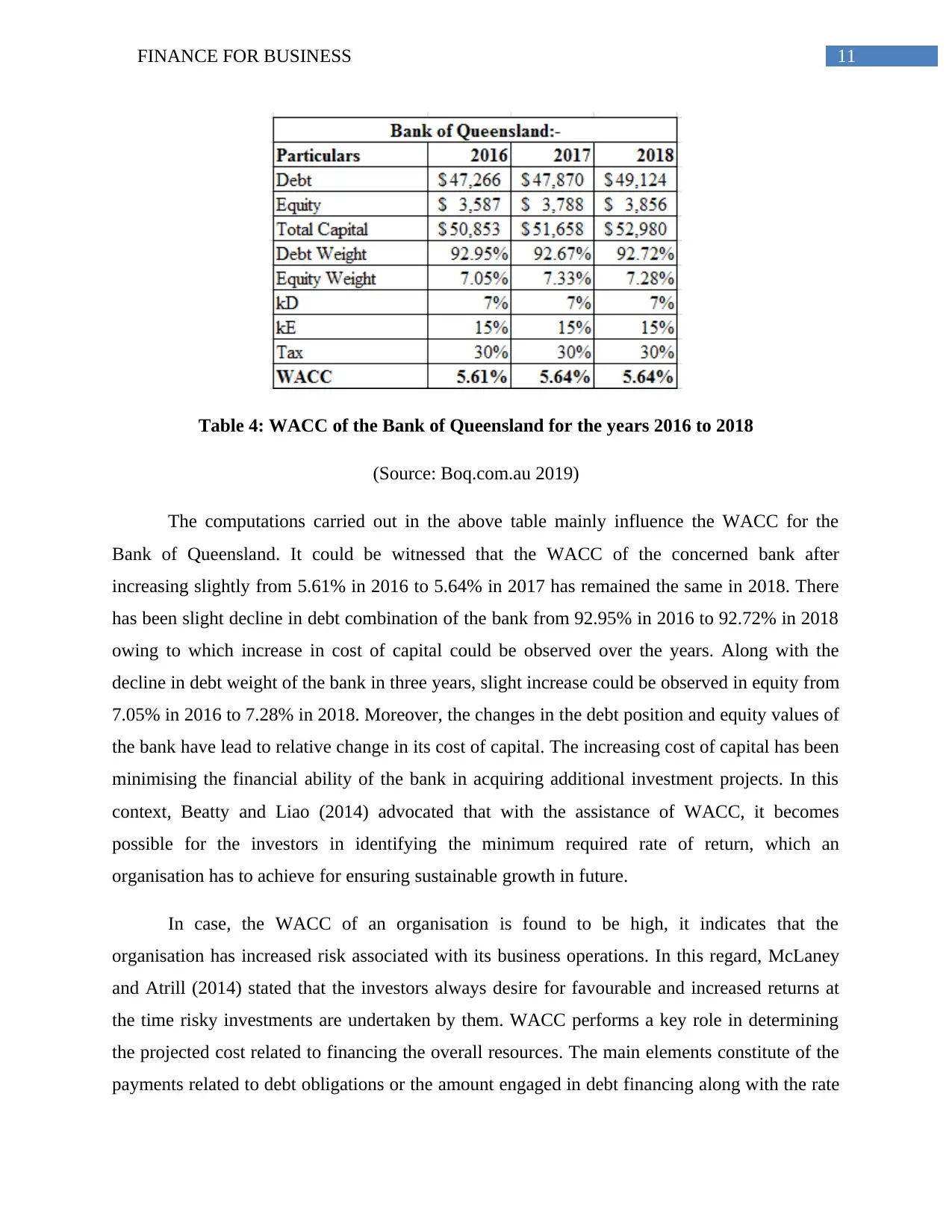

Table 4: WACC of the Bank of Queensland for the years 2016 to 2018

(Source: Boq.com.au 2019)

The computations carried out in the above table mainly influence the WACC for the

Bank of Queensland. It could be witnessed that the WACC of the concerned bank after

increasing slightly from 5.61% in 2016 to 5.64% in 2017 has remained the same in 2018. There

has been slight decline in debt combination of the bank from 92.95% in 2016 to 92.72% in 2018

owing to which increase in cost of capital could be observed over the years. Along with the

decline in debt weight of the bank in three years, slight increase could be observed in equity from

7.05% in 2016 to 7.28% in 2018. Moreover, the changes in the debt position and equity values of

the bank have lead to relative change in its cost of capital. The increasing cost of capital has been

minimising the financial ability of the bank in acquiring additional investment projects. In this

context, Beatty and Liao (2014) advocated that with the assistance of WACC, it becomes

possible for the investors in identifying the minimum required rate of return, which an

organisation has to achieve for ensuring sustainable growth in future.

In case, the WACC of an organisation is found to be high, it indicates that the

organisation has increased risk associated with its business operations. In this regard, McLaney

and Atrill (2014) stated that the investors always desire for favourable and increased returns at

the time risky investments are undertaken by them. WACC performs a key role in determining

the projected cost related to financing the overall resources. The main elements constitute of the

payments related to debt obligations or the amount engaged in debt financing along with the rate

Table 4: WACC of the Bank of Queensland for the years 2016 to 2018

(Source: Boq.com.au 2019)

The computations carried out in the above table mainly influence the WACC for the

Bank of Queensland. It could be witnessed that the WACC of the concerned bank after

increasing slightly from 5.61% in 2016 to 5.64% in 2017 has remained the same in 2018. There

has been slight decline in debt combination of the bank from 92.95% in 2016 to 92.72% in 2018

owing to which increase in cost of capital could be observed over the years. Along with the

decline in debt weight of the bank in three years, slight increase could be observed in equity from

7.05% in 2016 to 7.28% in 2018. Moreover, the changes in the debt position and equity values of

the bank have lead to relative change in its cost of capital. The increasing cost of capital has been

minimising the financial ability of the bank in acquiring additional investment projects. In this

context, Beatty and Liao (2014) advocated that with the assistance of WACC, it becomes

possible for the investors in identifying the minimum required rate of return, which an

organisation has to achieve for ensuring sustainable growth in future.

In case, the WACC of an organisation is found to be high, it indicates that the

organisation has increased risk associated with its business operations. In this regard, McLaney

and Atrill (2014) stated that the investors always desire for favourable and increased returns at

the time risky investments are undertaken by them. WACC performs a key role in determining

the projected cost related to financing the overall resources. The main elements constitute of the

payments related to debt obligations or the amount engaged in debt financing along with the rate

12FINANCE FOR BUSINESS

of return (McLean and Zhao 2014). This is deemed to be important for the management

ownership as well as cost involved in equity funding.

5. Capital structure policy:

The capital structure policy of Westpac Banking Corporation could be identified from the

long-term liquidity section, which implies that the bank earns adequate profit that helps in

covering up its interest expenses. The bank has raised its overall equity exposure by minimising

the overall composition of debt. As a result, debt ratio is observed to fall over the years for the

bank. On the contrary, slight increase in equity ratio could be observed over the years for the

bank, which has resulted in increased weighted average cost of capital. Finally, the interest cover

ratio is above 1, which indicates that the bank has stable capital position and the interest

payments would be lower compared to its earnings before interest and taxes.

In case of the Bank of Queensland, both positive and negative attributes could be

observed in its capital structure position. Since it is a bank, it is quite obvious that the debt to

equity ratio would be extremely high. However, a slight minimisation in debt to equity ratio is

considered as a positive attribute, while the increase in interest cover ratio is deemed to be

favourable for the bank as well. Due to the fall in debt weight of the bank, the interest cover ratio

represents has increased coupled with fall in interest payments. Along with this, the operating

income of the bank has risen over the years.

Therefore, it could be stated that both the banks have increased financial leverage, since

the debt weights are considerably high. Moreover, the issuance of mew equity shares would not

have adequate negative effects on the capital structure combination of the two banks.

6. Recommendation letter:

To,

The Investor

Date: 25/01/2019

Subject: Letter of recommendation

of return (McLean and Zhao 2014). This is deemed to be important for the management

ownership as well as cost involved in equity funding.

5. Capital structure policy:

The capital structure policy of Westpac Banking Corporation could be identified from the

long-term liquidity section, which implies that the bank earns adequate profit that helps in

covering up its interest expenses. The bank has raised its overall equity exposure by minimising

the overall composition of debt. As a result, debt ratio is observed to fall over the years for the

bank. On the contrary, slight increase in equity ratio could be observed over the years for the

bank, which has resulted in increased weighted average cost of capital. Finally, the interest cover

ratio is above 1, which indicates that the bank has stable capital position and the interest

payments would be lower compared to its earnings before interest and taxes.

In case of the Bank of Queensland, both positive and negative attributes could be

observed in its capital structure position. Since it is a bank, it is quite obvious that the debt to

equity ratio would be extremely high. However, a slight minimisation in debt to equity ratio is

considered as a positive attribute, while the increase in interest cover ratio is deemed to be

favourable for the bank as well. Due to the fall in debt weight of the bank, the interest cover ratio

represents has increased coupled with fall in interest payments. Along with this, the operating

income of the bank has risen over the years.

Therefore, it could be stated that both the banks have increased financial leverage, since

the debt weights are considerably high. Moreover, the issuance of mew equity shares would not

have adequate negative effects on the capital structure combination of the two banks.

6. Recommendation letter:

To,

The Investor

Date: 25/01/2019

Subject: Letter of recommendation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCE FOR BUSINESS

After taking into account the financial performance, stock price performance, weighted

average cost of capital, capital structure and leverage position of Westpac Banking Corporation

and the Bank of Queensland, the former option seems to be feasible for the concerned investor.

The Australian banking sector is deemed to be experiencing increased profits over the years,

which would assist in providing increased level of return to the shareholders and the investors.

Westpac Banking Corporation is selected, since its financial performance has improved more

compared to that of the Bank of Queensland. Positive attributes could be found more in the

profitability and liquidity aspects of Westpac compared to the Bank of Queensland. This is

because Westpac in comparison to the Bank of Queensland has ensured favourable financial

growth in the accounting periods. As a result, it has assisted in undertaking sound investment

decision of choosing an appropriate investment option generating greater returns in the long-run.

The stock price performance of Westpac is not adequate compared to the All Ordinaries Index,

as negative correlation could be found between the index performance and the stock performance

of Westpac. The situation is deemed to be similar for the Bank of Queensland, as its stock

performance is negatively correlated with the performance of the index.

The capital structure of both the banks is found to be funded by debt and thus, it implies

that the financial leverage risk is high for both. In this aspect, Westpac Banking Corporation is

deemed to be more capable than the Bank of Queensland in covering its interest expense with the

help of operating income. Thus, it could be stated that choosing Westpac Banking Corporation

would be the better alternative from the perspective of the investors, since it would increase the

relevant portfolio returns related to the investment of the concerned investor.

Conclusion:

From the above discussion, it has been analysed that Westpac is observed to be placed in

a better position in terms of profitability position than the Bank of Queensland in the Australian

market. In terms of long-term liquidity or solvency, Westpac is placed in a favourable position in

the Australian banking sector compared to the Bank of Queensland. The composition of capital

structure of Westpac has changed over the three-year period, in which the depth exposure has

fallen over the three-year period, while there has been rise in exposure of equity. Based on the

valuation, it could be understood that the cost of equity of the bank is comparatively high for the

organisation, which is the reason that the composition of the weights of equity has raised the

After taking into account the financial performance, stock price performance, weighted

average cost of capital, capital structure and leverage position of Westpac Banking Corporation

and the Bank of Queensland, the former option seems to be feasible for the concerned investor.

The Australian banking sector is deemed to be experiencing increased profits over the years,

which would assist in providing increased level of return to the shareholders and the investors.

Westpac Banking Corporation is selected, since its financial performance has improved more

compared to that of the Bank of Queensland. Positive attributes could be found more in the

profitability and liquidity aspects of Westpac compared to the Bank of Queensland. This is

because Westpac in comparison to the Bank of Queensland has ensured favourable financial

growth in the accounting periods. As a result, it has assisted in undertaking sound investment

decision of choosing an appropriate investment option generating greater returns in the long-run.

The stock price performance of Westpac is not adequate compared to the All Ordinaries Index,

as negative correlation could be found between the index performance and the stock performance

of Westpac. The situation is deemed to be similar for the Bank of Queensland, as its stock

performance is negatively correlated with the performance of the index.

The capital structure of both the banks is found to be funded by debt and thus, it implies

that the financial leverage risk is high for both. In this aspect, Westpac Banking Corporation is

deemed to be more capable than the Bank of Queensland in covering its interest expense with the

help of operating income. Thus, it could be stated that choosing Westpac Banking Corporation

would be the better alternative from the perspective of the investors, since it would increase the

relevant portfolio returns related to the investment of the concerned investor.

Conclusion:

From the above discussion, it has been analysed that Westpac is observed to be placed in

a better position in terms of profitability position than the Bank of Queensland in the Australian

market. In terms of long-term liquidity or solvency, Westpac is placed in a favourable position in

the Australian banking sector compared to the Bank of Queensland. The composition of capital

structure of Westpac has changed over the three-year period, in which the depth exposure has

fallen over the three-year period, while there has been rise in exposure of equity. Based on the

valuation, it could be understood that the cost of equity of the bank is comparatively high for the

organisation, which is the reason that the composition of the weights of equity has raised the

14FINANCE FOR BUSINESS

overall cost of capital of the bank. In case of the Bank of Queensland, both positive and negative

attributes could be observed in its capital structure position. Since it is a bank, it is quite obvious

that the debt to equity ratio would be extremely high. However, a slight minimisation in debt to

equity ratio is considered as a positive attribute, while the increase in interest cover ratio is

deemed to be favourable for the bank as well. Therefore, the investor is recommended to invest

in the shares of Westpac Banking Corporation for maximising the overall return on investment.

overall cost of capital of the bank. In case of the Bank of Queensland, both positive and negative

attributes could be observed in its capital structure position. Since it is a bank, it is quite obvious

that the debt to equity ratio would be extremely high. However, a slight minimisation in debt to

equity ratio is considered as a positive attribute, while the increase in interest cover ratio is

deemed to be favourable for the bank as well. Therefore, the investor is recommended to invest

in the shares of Westpac Banking Corporation for maximising the overall return on investment.

15FINANCE FOR BUSINESS

References and Bibliographies:

Au.finance.yahoo.com., 2019. [online] Available at:

https://au.finance.yahoo.com/quote/BOQ.AX/history/ [Accessed 25 Jan. 2019].

Au.finance.yahoo.com., 2019. [online] Available at:

https://au.finance.yahoo.com/quote/WBC.AX/history/ [Accessed 25 Jan. 2019].

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Boq.com.au., 2019. About us | Bank of Queensland. [online] Available at:

https://www.boq.com.au/About-us [Accessed 25 Jan. 2019].

Boq.com.au., 2019. Annual Reports | Bank of Queensland. [online] Available at:

https://www.boq.com.au/Shareholder-centre/financial-information/Annual-Report [Accessed 25

Jan. 2019].

Brown, R. and Jones, M., 2015. Mapping and exploring the topography of contemporary

financial accounting research. The British Accounting Review, 47(3), pp.237-261.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Halili, E., Saleh, A. and Zeitun, R., 2015. Governance and Long-Term Operating Performance of

Family and Non-Family Firms in Australia. Studies in Economics and Finance, 32(4), pp.398-

421.

Hatfield, H.R., 2014. Accounting: Its Principles and Some ofits Problems. In The Development

of Accounting Theory (RLE Accounting) (pp. 21-29). Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hirshleifer, D., 2015. Behavioral finance. Annual Review of Financial Economics, 7, pp.133-

159.

References and Bibliographies:

Au.finance.yahoo.com., 2019. [online] Available at:

https://au.finance.yahoo.com/quote/BOQ.AX/history/ [Accessed 25 Jan. 2019].

Au.finance.yahoo.com., 2019. [online] Available at:

https://au.finance.yahoo.com/quote/WBC.AX/history/ [Accessed 25 Jan. 2019].

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Boq.com.au., 2019. About us | Bank of Queensland. [online] Available at:

https://www.boq.com.au/About-us [Accessed 25 Jan. 2019].

Boq.com.au., 2019. Annual Reports | Bank of Queensland. [online] Available at:

https://www.boq.com.au/Shareholder-centre/financial-information/Annual-Report [Accessed 25

Jan. 2019].

Brown, R. and Jones, M., 2015. Mapping and exploring the topography of contemporary

financial accounting research. The British Accounting Review, 47(3), pp.237-261.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Halili, E., Saleh, A. and Zeitun, R., 2015. Governance and Long-Term Operating Performance of

Family and Non-Family Firms in Australia. Studies in Economics and Finance, 32(4), pp.398-

421.

Hatfield, H.R., 2014. Accounting: Its Principles and Some ofits Problems. In The Development

of Accounting Theory (RLE Accounting) (pp. 21-29). Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hirshleifer, D., 2015. Behavioral finance. Annual Review of Financial Economics, 7, pp.133-

159.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16FINANCE FOR BUSINESS

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Lee, T.A. and Parker, R.H. eds., 2014. Evolution of Corporate Financial Reporting (RLE

Accounting). Routledge.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

McLaney, E.J. and Atrill, P., 2014. Accounting and finance: An introduction. Pearson.

McLean, R.D. and Zhao, M., 2014. The business cycle, investor sentiment, and costly external

finance. The Journal of Finance, 69(3), pp.1377-1409.

Narayanaswamy, R., 2017. Financial Accounting: A Managerial Perspective. PHI Learning Pvt.

Ltd..

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Titman, S., Martin, T., Keown, A.J., Martin, J.D, 2016. Financial Management: principles and

applications, 7th Edition. Pearson Education, Melbourne, Australia.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Westpac.com.au., 2019. Annual reports | Westpac. [online] Available at:

https://www.westpac.com.au/about-westpac/investor-centre/financial-information/annual-

reports/ [Accessed 25 Jan. 2019].

Westpac.com.au., 2019. Westpac - Personal, Business and Corporate Banking. [online]

Available at: https://www.westpac.com.au/ [Accessed 25 Jan. 2019].

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Lee, T.A. and Parker, R.H. eds., 2014. Evolution of Corporate Financial Reporting (RLE

Accounting). Routledge.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

McLaney, E.J. and Atrill, P., 2014. Accounting and finance: An introduction. Pearson.

McLean, R.D. and Zhao, M., 2014. The business cycle, investor sentiment, and costly external

finance. The Journal of Finance, 69(3), pp.1377-1409.

Narayanaswamy, R., 2017. Financial Accounting: A Managerial Perspective. PHI Learning Pvt.

Ltd..

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Titman, S., Martin, T., Keown, A.J., Martin, J.D, 2016. Financial Management: principles and

applications, 7th Edition. Pearson Education, Melbourne, Australia.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Westpac.com.au., 2019. Annual reports | Westpac. [online] Available at:

https://www.westpac.com.au/about-westpac/investor-centre/financial-information/annual-

reports/ [Accessed 25 Jan. 2019].

Westpac.com.au., 2019. Westpac - Personal, Business and Corporate Banking. [online]

Available at: https://www.westpac.com.au/ [Accessed 25 Jan. 2019].

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons.

17FINANCE FOR BUSINESS

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.