HI5002 Finance for Business Company Performance Analysis

VerifiedAdded on 2022/10/10

|8

|739

|101

Project

AI Summary

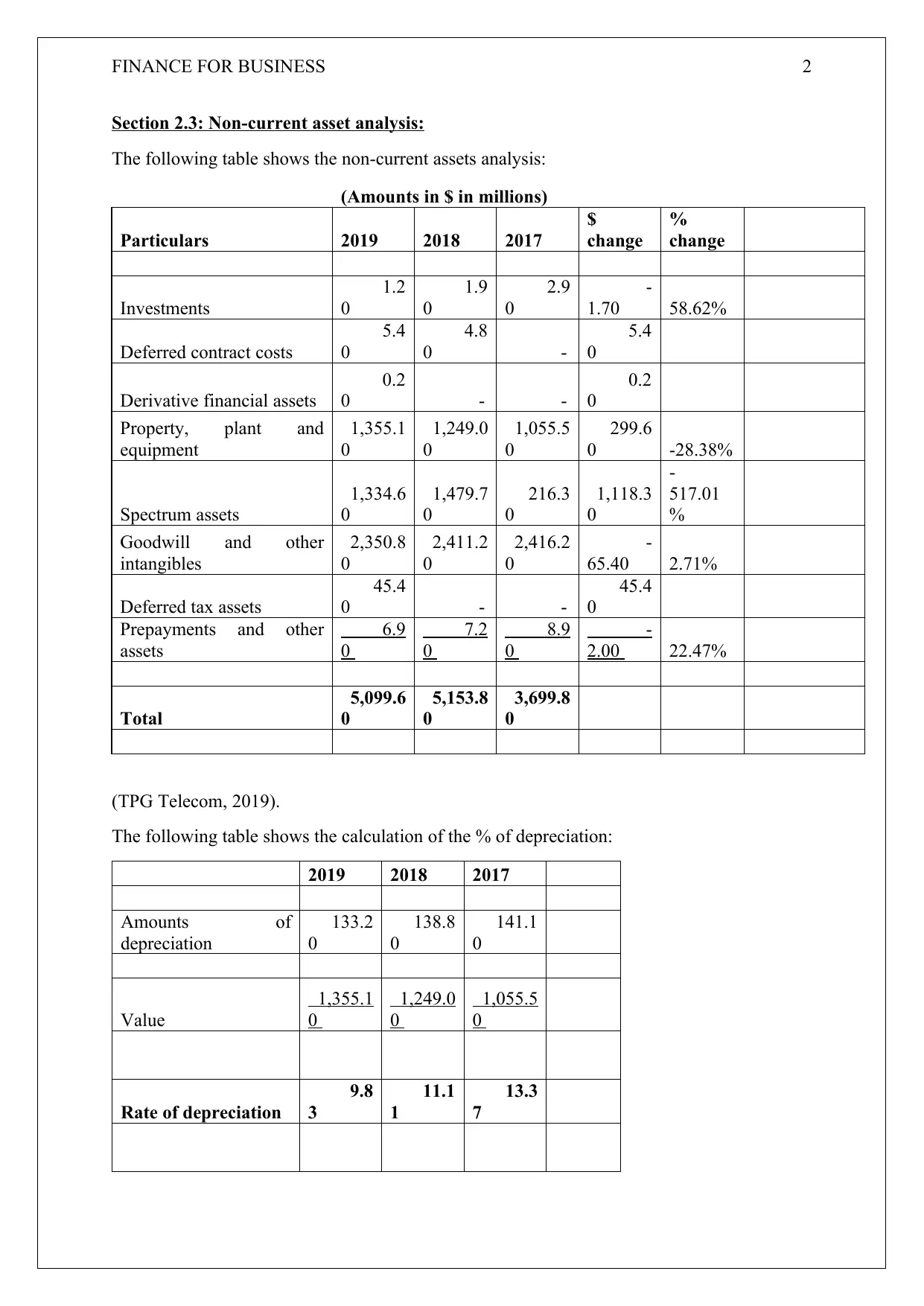

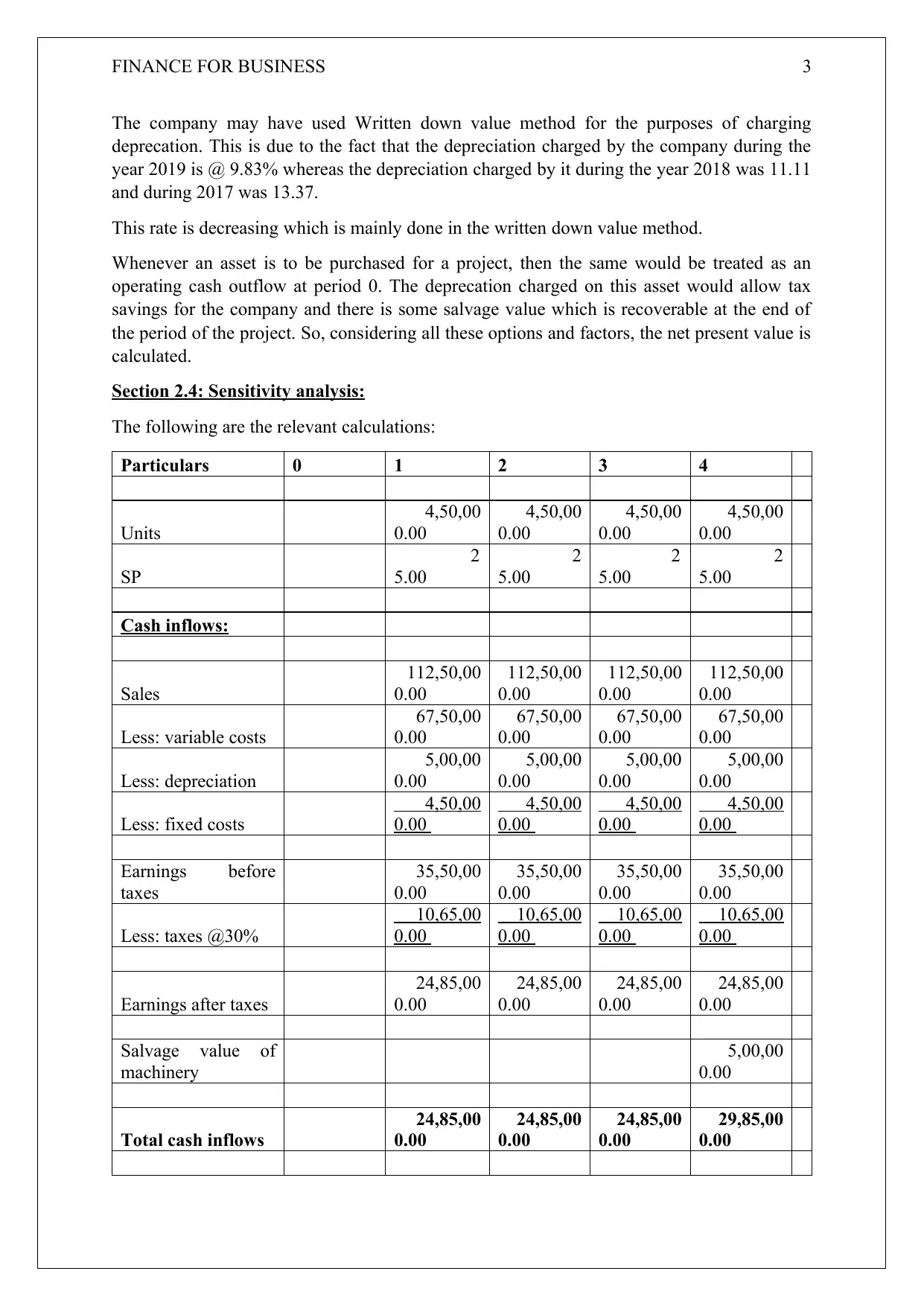

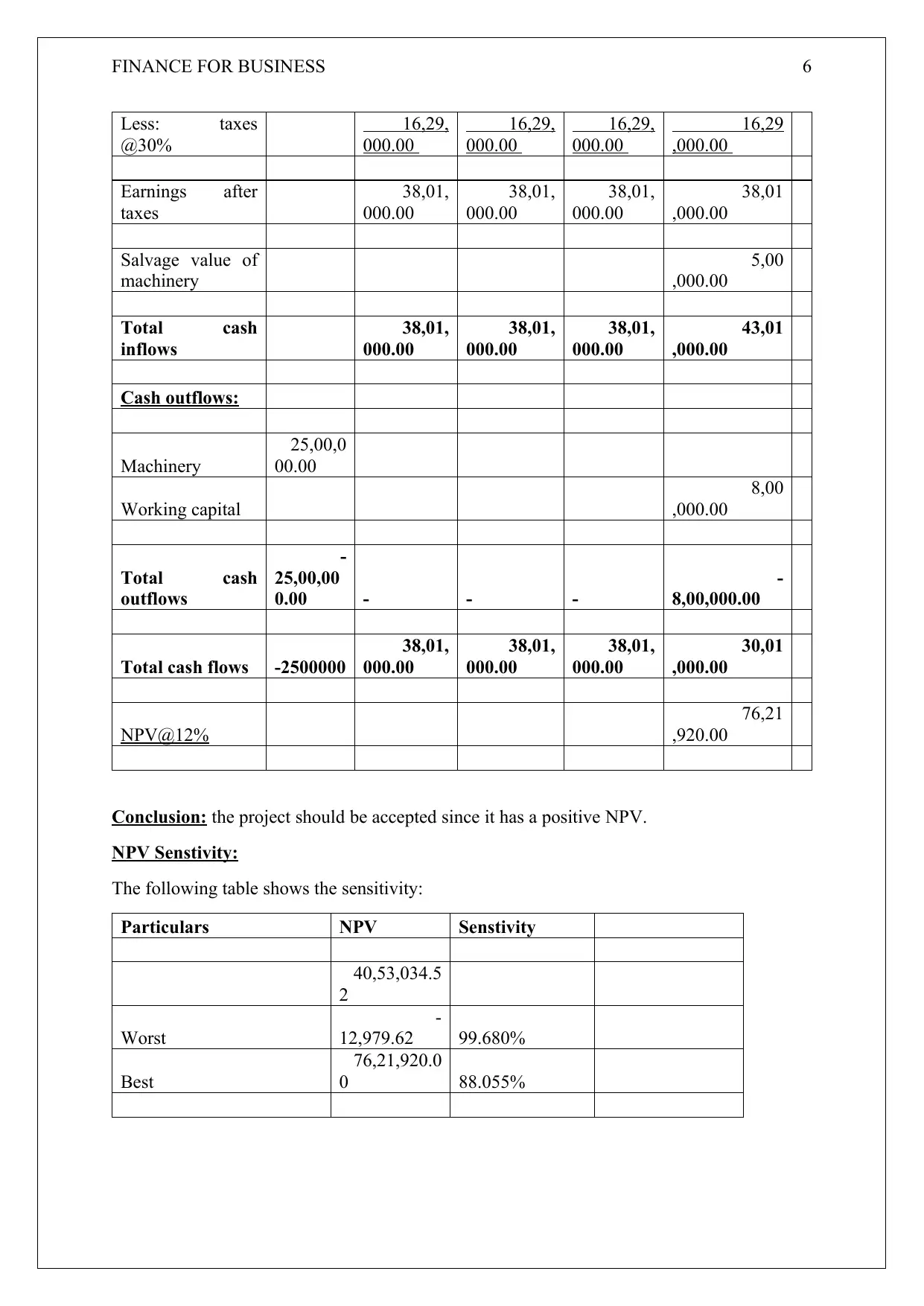

This finance project analyzes the financial performance of TPG Telecom. The analysis includes a review of non-current assets, focusing on investments, property, plant, and equipment, spectrum assets, and goodwill. The project also calculates the rate of depreciation and discusses the written-down value method. Furthermore, the project performs a sensitivity analysis, calculating Net Present Value (NPV) under best-case, worst-case, and base-case scenarios. The analysis includes detailed cash flow calculations and concludes with an assessment of the project's viability based on the NPV results. The project uses data from TPG Telecom's financial reports for the years 2017-2019.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.