Finance for Business – Masters Project: Cash Flow and NPV Analysis

VerifiedAdded on 2020/04/07

FINANCE FOR BUSINESS – MASTERS

Finance for business – Masters

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

FINANCE FOR BUSINESS – MASTERS

Table of Contents

1. Detecting the relevant accounts that need to be omitted from the list of Exhibit 3:..............3

2. Mentioning the calculation for the incremental cash flow table for most likely situation:....3

3. Calculating the NPV, internal rate of return (IRR) and profitability index (PI) for the

overall project:...........................................................................................................................5

4. Portraying the sensitivity analysis for best case and worst case scenario mentioned in

exhibit 1:.....................................................................................................................................6

5. Calculating the expected sales, standard deviation and coefficient variance from different

situations:.................................................................................................................................10

6. Increasing the annual sales by minimal value:.....................................................................10

7. Mentioning the reason behind using high discount rate when the inflation rate is at 3%:. .17

8. Mentioning the recommendation for the production of 10-in and 12-in Pipe to the

organisation:.............................................................................................................................18

Reference and Bibliography:....................................................................................................19

FINANCE FOR BUSINESS – MASTERS

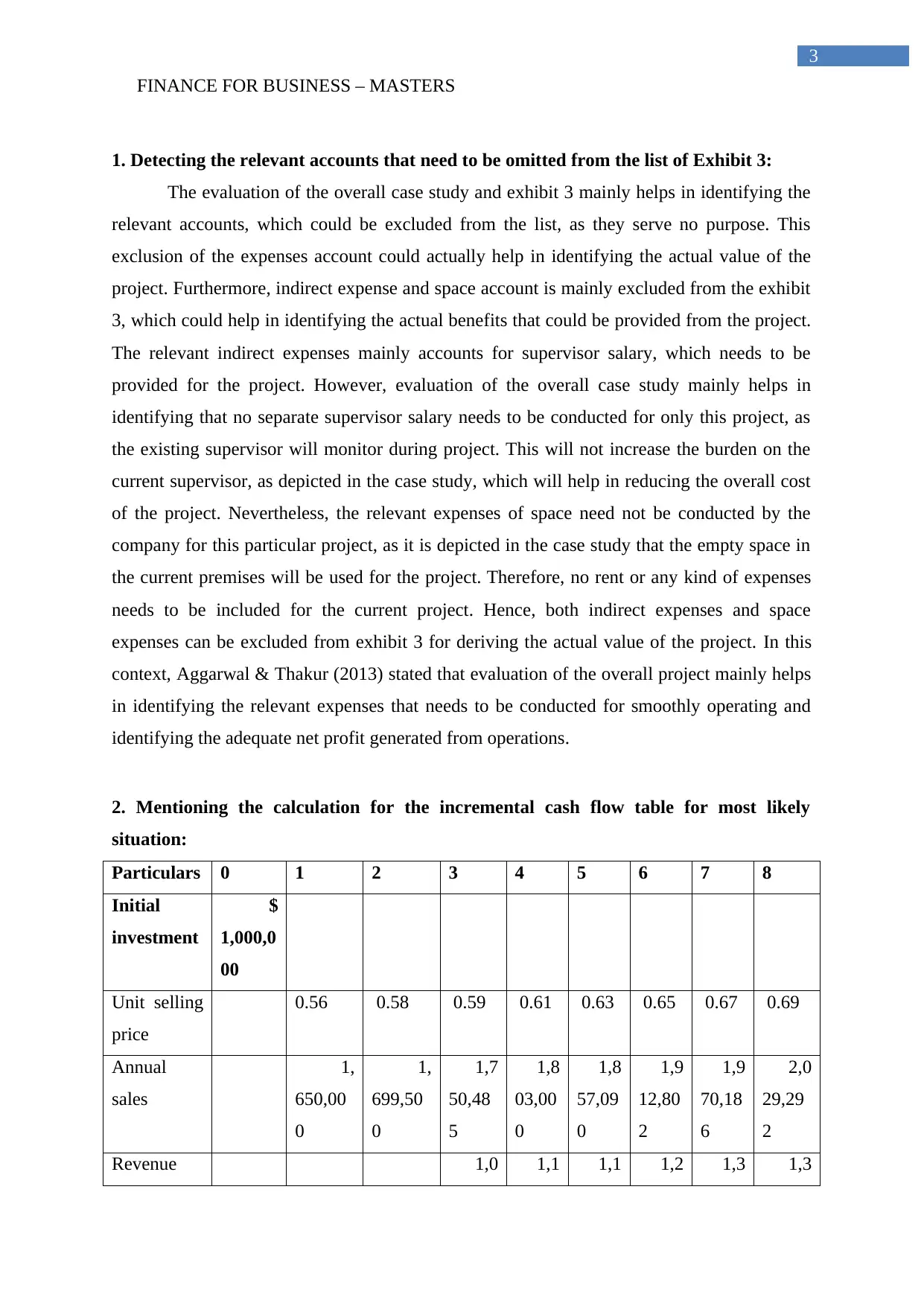

1. Detecting the relevant accounts that need to be omitted from the list of Exhibit 3:

The evaluation of the overall case study and exhibit 3 mainly helps in identifying the

relevant accounts, which could be excluded from the list, as they serve no purpose. This

exclusion of the expenses account could actually help in identifying the actual value of the

project. Furthermore, indirect expense and space account is mainly excluded from the exhibit

3, which could help in identifying the actual benefits that could be provided from the project.

The relevant indirect expenses mainly accounts for supervisor salary, which needs to be

provided for the project. However, evaluation of the overall case study mainly helps in

identifying that no separate supervisor salary needs to be conducted for only this project, as

the existing supervisor will monitor during project. This will not increase the burden on the

current supervisor, as depicted in the case study, which will help in reducing the overall cost

of the project. Nevertheless, the relevant expenses of space need not be conducted by the

company for this particular project, as it is depicted in the case study that the empty space in

the current premises will be used for the project. Therefore, no rent or any kind of expenses

needs to be included for the current project. Hence, both indirect expenses and space

expenses can be excluded from exhibit 3 for deriving the actual value of the project. In this

context, Aggarwal & Thakur (2013) stated that evaluation of the overall project mainly helps

in identifying the relevant expenses that needs to be conducted for smoothly operating and

identifying the adequate net profit generated from operations.

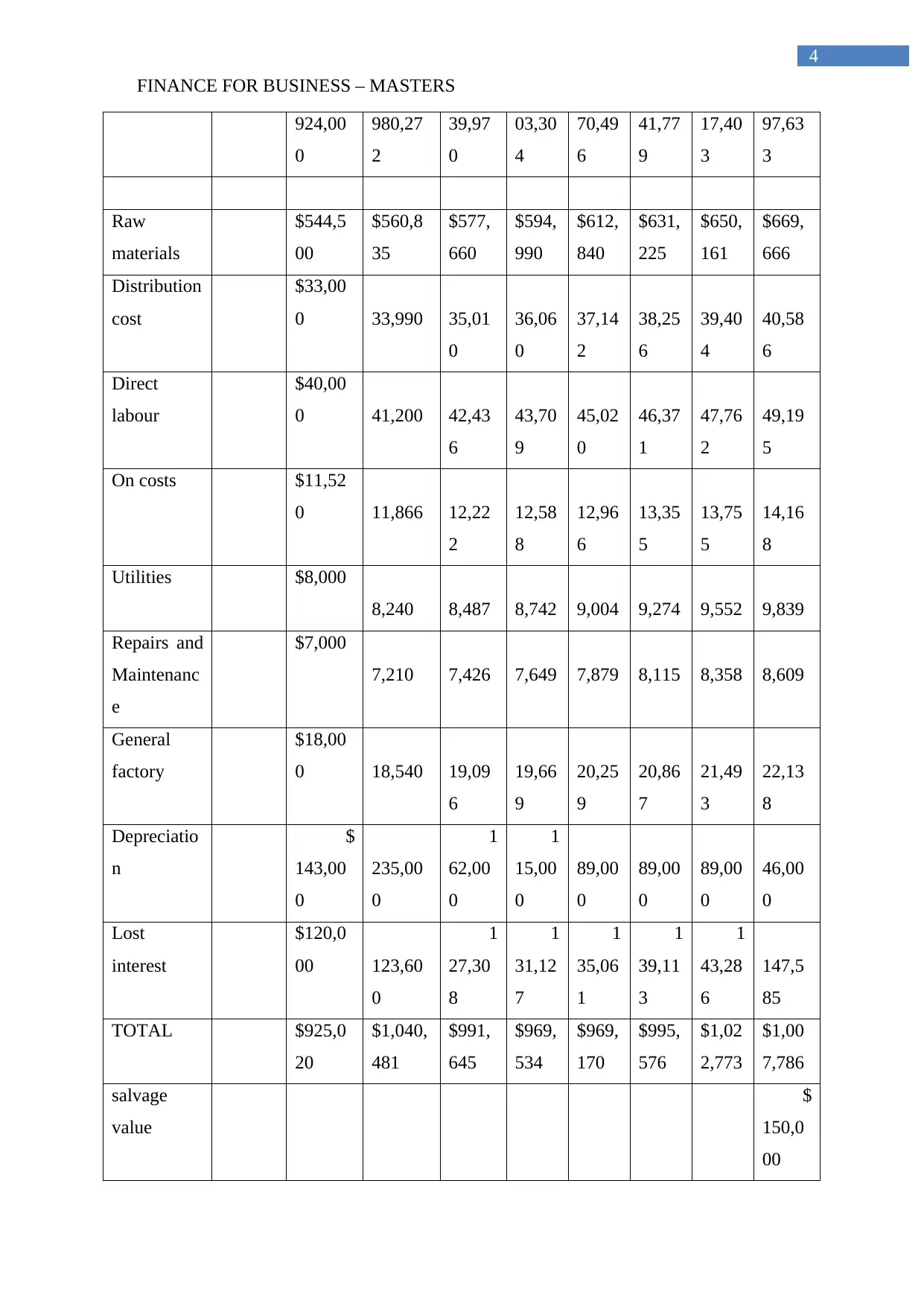

2. Mentioning the calculation for the incremental cash flow table for most likely

situation:

Particulars 0 1 2 3 4 5 6 7 8

Initial

investment

$

1,000,0

00

Unit selling

price

0.56 0.58 0.59 0.61 0.63 0.65 0.67 0.69

Annual

sales

1,

650,00

0

1,

699,50

0

1,7

50,48

5

1,8

03,00

0

1,8

57,09

0

1,9

12,80

2

1,9

70,18

6

2,0

29,29

2

Revenue 1,0 1,1 1,1 1,2 1,3 1,3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS – MASTERS

924,00

0

980,27

2

39,97

0

03,30

4

70,49

6

41,77

9

17,40

3

97,63

3

Raw

materials

$544,5

00

$560,8

35

$577,

660

$594,

990

$612,

840

$631,

225

$650,

161

$669,

666

Distribution

cost

$33,00

0 33,990 35,01

0

36,06

0

37,14

2

38,25

6

39,40

4

40,58

6

Direct

labour

$40,00

0 41,200 42,43

6

43,70

9

45,02

0

46,37

1

47,76

2

49,19

5

On costs $11,52

0 11,866 12,22

2

12,58

8

12,96

6

13,35

5

13,75

5

14,16

8

Utilities $8,000

8,240 8,487 8,742 9,004 9,274 9,552 9,839

Repairs and

Maintenanc

e

$7,000

7,210 7,426 7,649 7,879 8,115 8,358 8,609

General

factory

$18,00

0 18,540 19,09

6

19,66

9

20,25

9

20,86

7

21,49

3

22,13

8

Depreciatio

n

$

143,00

0

235,00

0

1

62,00

0

1

15,00

0

89,00

0

89,00

0

89,00

0

46,00

0

Lost

interest

$120,0

00 123,60

0

1

27,30

8

1

31,12

7

1

35,06

1

1

39,11

3

1

43,28

6

147,5

85

TOTAL $925,0

20

$1,040,

481

$991,

645

$969,

534

$969,

170

$995,

576

$1,02

2,773

$1,00

7,786

salvage

value

$

150,0

00

Paraphrase This Document

FINANCE FOR BUSINESS – MASTERS

PBT

(1,020) (60,209

)

48,32

5

1

33,77

0

2

01,32

5

2

46,20

3

2

94,63

0

539,8

47

Tax

- - 14,49

8

40,13

1

60,39

8

73,86

1

88,38

9

161,9

54

PAT

(1,020) (60,209

)

33,82

8

93,63

9

1

40,92

8

1

72,34

2

2

06,24

1

377,8

93

Net Cash

flow

$

(1,000,

000)

141,98

0

174,79

1

1

95,82

8

2

08,63

9

2

29,92

8

2

61,34

2

2

95,24

1

423,8

93

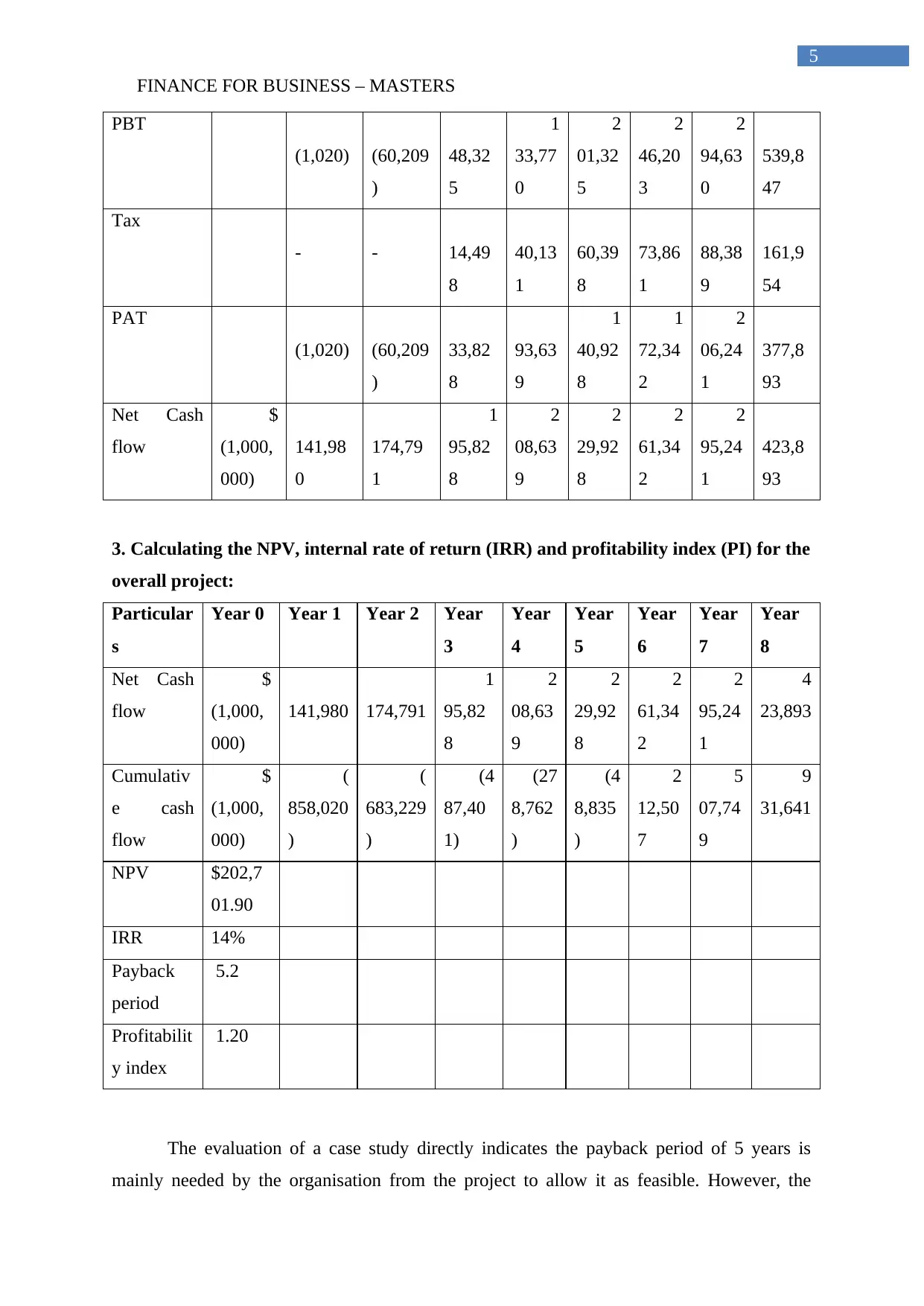

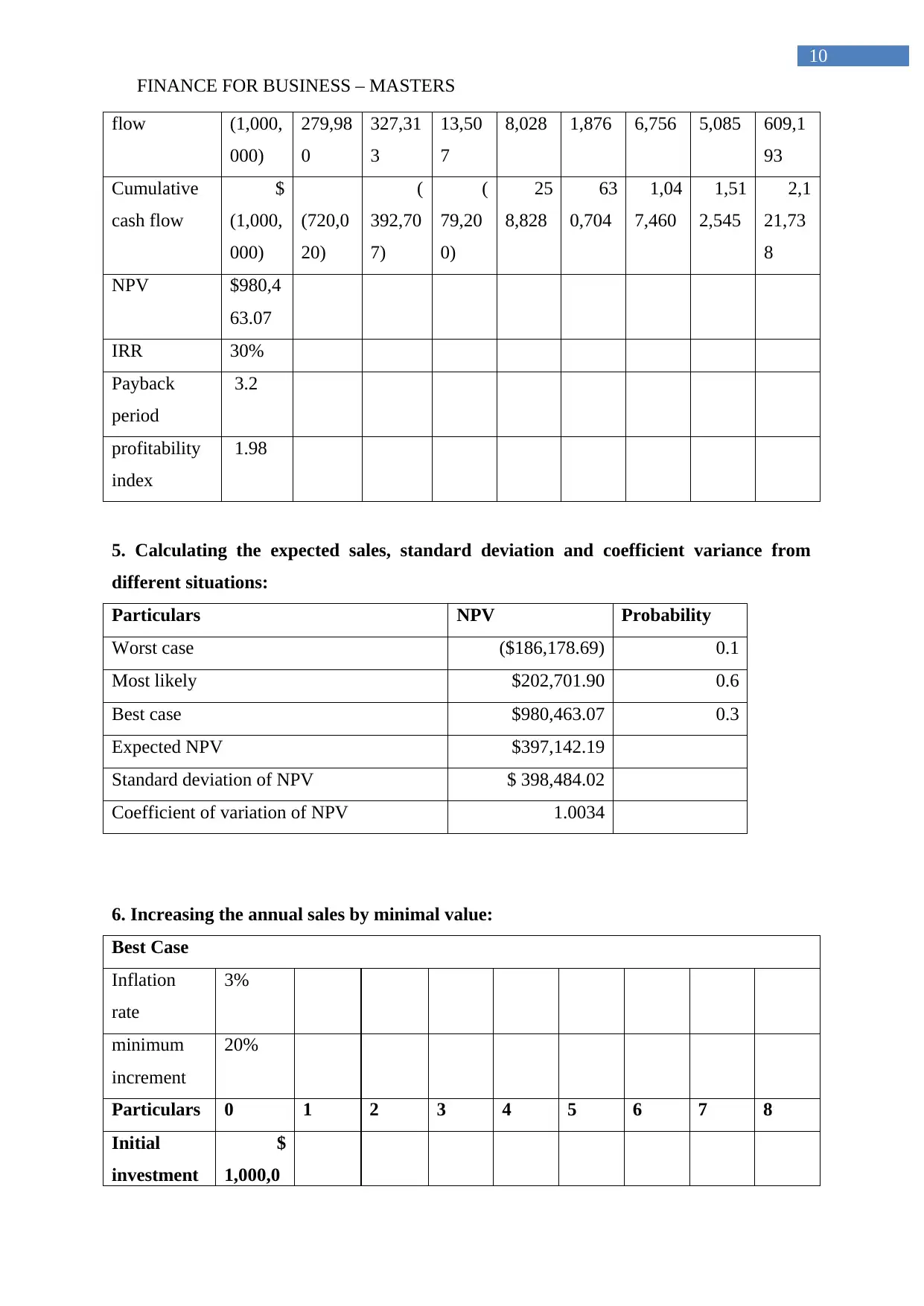

3. Calculating the NPV, internal rate of return (IRR) and profitability index (PI) for the

overall project:

Particular

s

Year 0 Year 1 Year 2 Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Net Cash

flow

$

(1,000,

000)

141,980 174,791

1

95,82

8

2

08,63

9

2

29,92

8

2

61,34

2

2

95,24

1

4

23,893

Cumulativ

e cash

flow

$

(1,000,

000)

(

858,020

)

(

683,229

)

(4

87,40

1)

(27

8,762

)

(4

8,835

)

2

12,50

7

5

07,74

9

9

31,641

NPV $202,7

01.90

IRR 14%

Payback

period

5.2

Profitabilit

y index

1.20

The evaluation of a case study directly indicates the payback period of 5 years is

mainly needed by the organisation from the project to allow it as feasible. However, the

FINANCE FOR BUSINESS – MASTERS

overall project has a payback period of 5.2 years, which is a relatively higher than the actual

criteria of the organisation. This non-fulfilment of the specific payback period could directly

force the organisation to reject the overall project. Nevertheless, the profitability index

directly indicates a value of 1.20, which directly states relevant profits that could be incurred

from the project. Moreover, the NPV of the project is $202,701.90, while the IRR is 14%,

which directly indicates the overall viability of the project. Awojobi & Jenkins (2016) stated

that use of adequate investment appraisal techniques could eventually allow the organisation

to identify the relevant viability of the investment and the adequate returns which could be

provided after completion of the project.

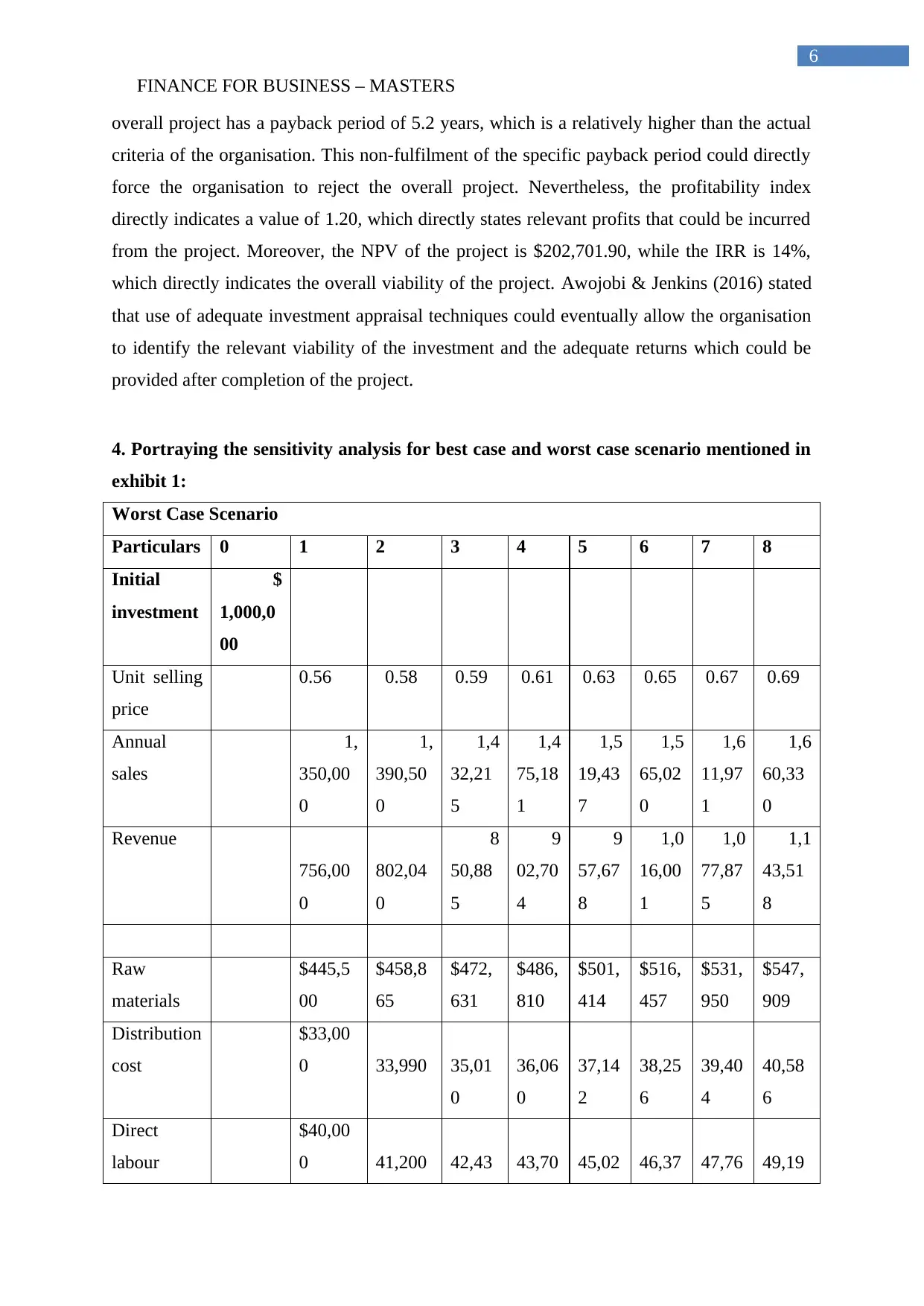

4. Portraying the sensitivity analysis for best case and worst case scenario mentioned in

exhibit 1:

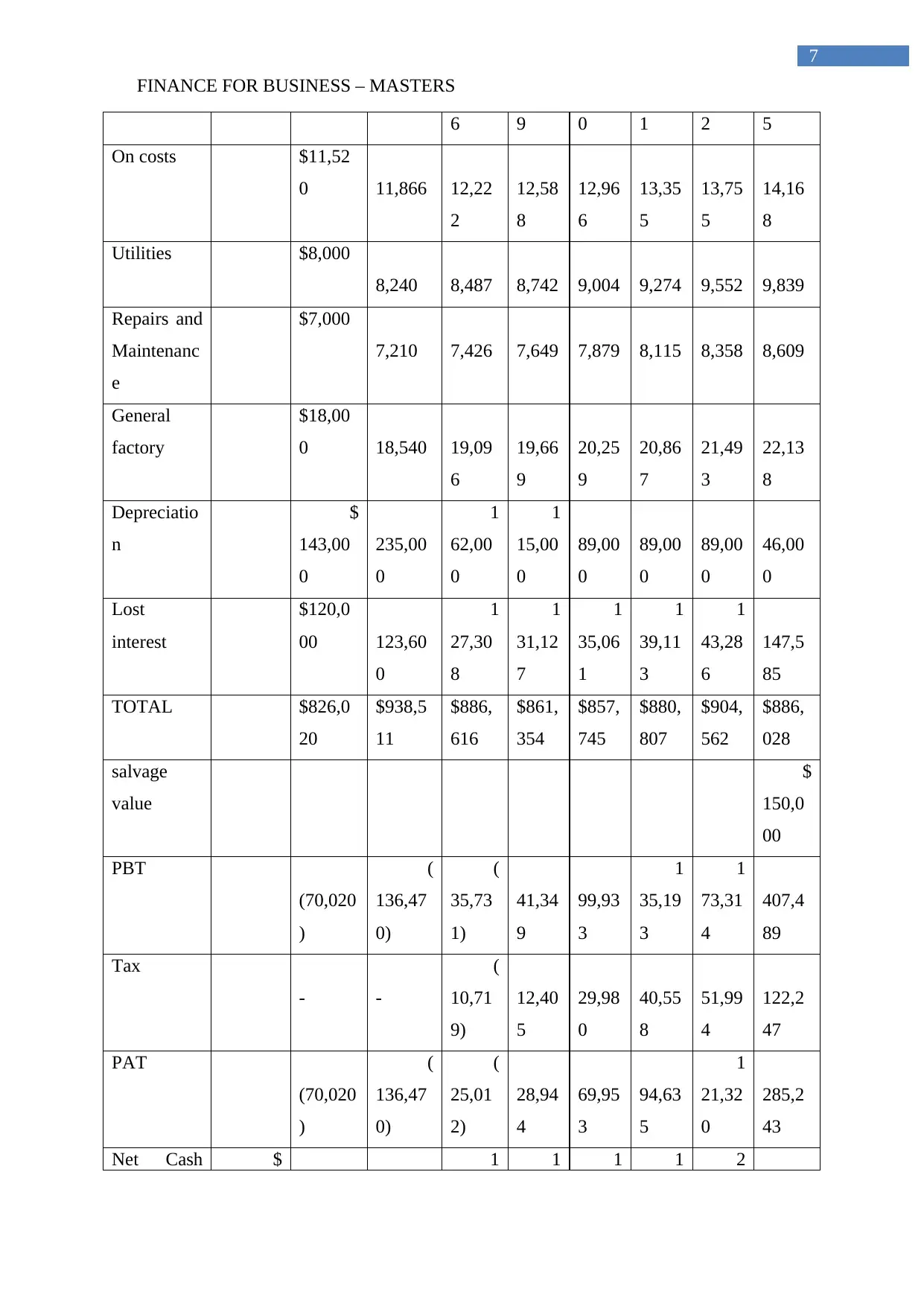

Worst Case Scenario

Particulars 0 1 2 3 4 5 6 7 8

Initial

investment

$

1,000,0

00

Unit selling

price

0.56 0.58 0.59 0.61 0.63 0.65 0.67 0.69

Annual

sales

1,

350,00

0

1,

390,50

0

1,4

32,21

5

1,4

75,18

1

1,5

19,43

7

1,5

65,02

0

1,6

11,97

1

1,6

60,33

0

Revenue

756,00

0

802,04

0

8

50,88

5

9

02,70

4

9

57,67

8

1,0

16,00

1

1,0

77,87

5

1,1

43,51

8

Raw

materials

$445,5

00

$458,8

65

$472,

631

$486,

810

$501,

414

$516,

457

$531,

950

$547,

909

Distribution

cost

$33,00

0 33,990 35,01

0

36,06

0

37,14

2

38,25

6

39,40

4

40,58

6

Direct

labour

$40,00

0 41,200 42,43 43,70 45,02 46,37 47,76 49,19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS – MASTERS

6 9 0 1 2 5

On costs $11,52

0 11,866 12,22

2

12,58

8

12,96

6

13,35

5

13,75

5

14,16

8

Utilities $8,000

8,240 8,487 8,742 9,004 9,274 9,552 9,839

Repairs and

Maintenanc

e

$7,000

7,210 7,426 7,649 7,879 8,115 8,358 8,609

General

factory

$18,00

0 18,540 19,09

6

19,66

9

20,25

9

20,86

7

21,49

3

22,13

8

Depreciatio

n

$

143,00

0

235,00

0

1

62,00

0

1

15,00

0

89,00

0

89,00

0

89,00

0

46,00

0

Lost

interest

$120,0

00 123,60

0

1

27,30

8

1

31,12

7

1

35,06

1

1

39,11

3

1

43,28

6

147,5

85

TOTAL $826,0

20

$938,5

11

$886,

616

$861,

354

$857,

745

$880,

807

$904,

562

$886,

028

salvage

value

$

150,0

00

PBT

(70,020

)

(

136,47

0)

(

35,73

1)

41,34

9

99,93

3

1

35,19

3

1

73,31

4

407,4

89

Tax

- -

(

10,71

9)

12,40

5

29,98

0

40,55

8

51,99

4

122,2

47

PAT

(70,020

)

(

136,47

0)

(

25,01

2)

28,94

4

69,95

3

94,63

5

1

21,32

0

285,2

43

Net Cash $ 1 1 1 1 2

Paraphrase This Document

FINANCE FOR BUSINESS – MASTERS

flow (1,000,0

00)

72,980 98,530 36,98

8

43,94

4

58,95

3

83,63

5

10,32

0

331,2

43

Cumulative

cash flow

$

(1,000,0

00)

(

927,02

0)

(

828,49

0)

(6

91,50

2)

(54

7,558

)

(38

8,604

)

(20

4,969

)

5,350 336,5

93

NPV ($186,1

78.69)

IRR 6%

Payback

period 7.0

profitability

index 0.81

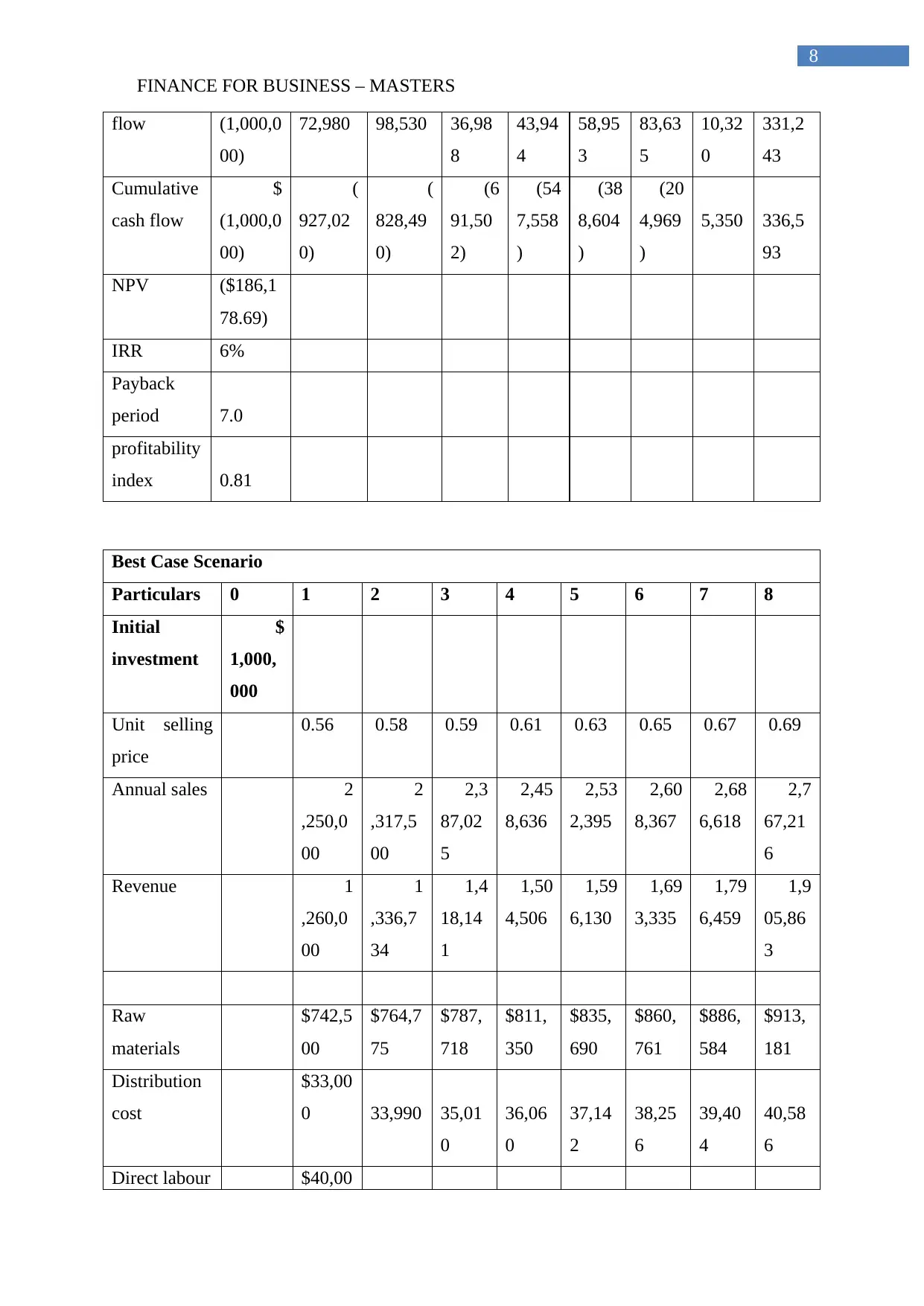

Best Case Scenario

Particulars 0 1 2 3 4 5 6 7 8

Initial

investment

$

1,000,

000

Unit selling

price

0.56 0.58 0.59 0.61 0.63 0.65 0.67 0.69

Annual sales 2

,250,0

00

2

,317,5

00

2,3

87,02

5

2,45

8,636

2,53

2,395

2,60

8,367

2,68

6,618

2,7

67,21

6

Revenue 1

,260,0

00

1

,336,7

34

1,4

18,14

1

1,50

4,506

1,59

6,130

1,69

3,335

1,79

6,459

1,9

05,86

3

Raw

materials

$742,5

00

$764,7

75

$787,

718

$811,

350

$835,

690

$860,

761

$886,

584

$913,

181

Distribution

cost

$33,00

0 33,990 35,01

0

36,06

0

37,14

2

38,25

6

39,40

4

40,58

6

Direct labour $40,00

FINANCE FOR BUSINESS – MASTERS

0 41,200 42,43

6

43,70

9

45,02

0

46,37

1

47,76

2

49,19

5

On costs $11,52

0 11,866 12,22

2

12,58

8

12,96

6

13,35

5

13,75

5

14,16

8

Utilities $8,000

8,240 8,487 8,742 9,004 9,274 9,552 9,839

Repairs and

Maintenance

$7,000

7,210 7,426 7,649 7,879 8,115 8,358 8,609

General

factory

$18,00

0 18,540 19,09

6

19,66

9

20,25

9

20,86

7

21,49

3

22,13

8

Depreciation $

143,00

0

235,00

0

1

62,00

0

11

5,000 89,00

0

89,00

0

89,00

0

46,00

0

Lost interest $120,0

00 123,60

0

1

27,30

8

13

1,127

13

5,061

13

9,113

14

3,286 147,5

85

TOTAL $1,123

,020

$1,244

,421

$1,20

1,703

$1,18

5,894

$1,19

2,021

$1,22

5,112

$1,25

9,195

$1,25

1,301

salvage value $

150,0

00

PBT

136,98

0

92,313

2

16,43

8

31

8,612

40

4,109

46

8,223

53

7,264 804,5

62

Tax

- - 64,93

1

95,58

3

12

1,233

14

0,467

16

1,179 241,3

69

PAT

136,98

0

92,313

1

51,50

7

22

3,028

28

2,876

32

7,756

37

6,085 563,1

93

Net Cash $ 3 33 37 41 46

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS – MASTERS

flow (1,000,

000)

279,98

0

327,31

3

13,50

7

8,028 1,876 6,756 5,085 609,1

93

Cumulative

cash flow

$

(1,000,

000)

(720,0

20)

(

392,70

7)

(

79,20

0)

25

8,828

63

0,704

1,04

7,460

1,51

2,545

2,1

21,73

8

NPV $980,4

63.07

IRR 30%

Payback

period

3.2

profitability

index

1.98

5. Calculating the expected sales, standard deviation and coefficient variance from

different situations:

Particulars NPV Probability

Worst case ($186,178.69) 0.1

Most likely $202,701.90 0.6

Best case $980,463.07 0.3

Expected NPV $397,142.19

Standard deviation of NPV $ 398,484.02

Coefficient of variation of NPV 1.0034

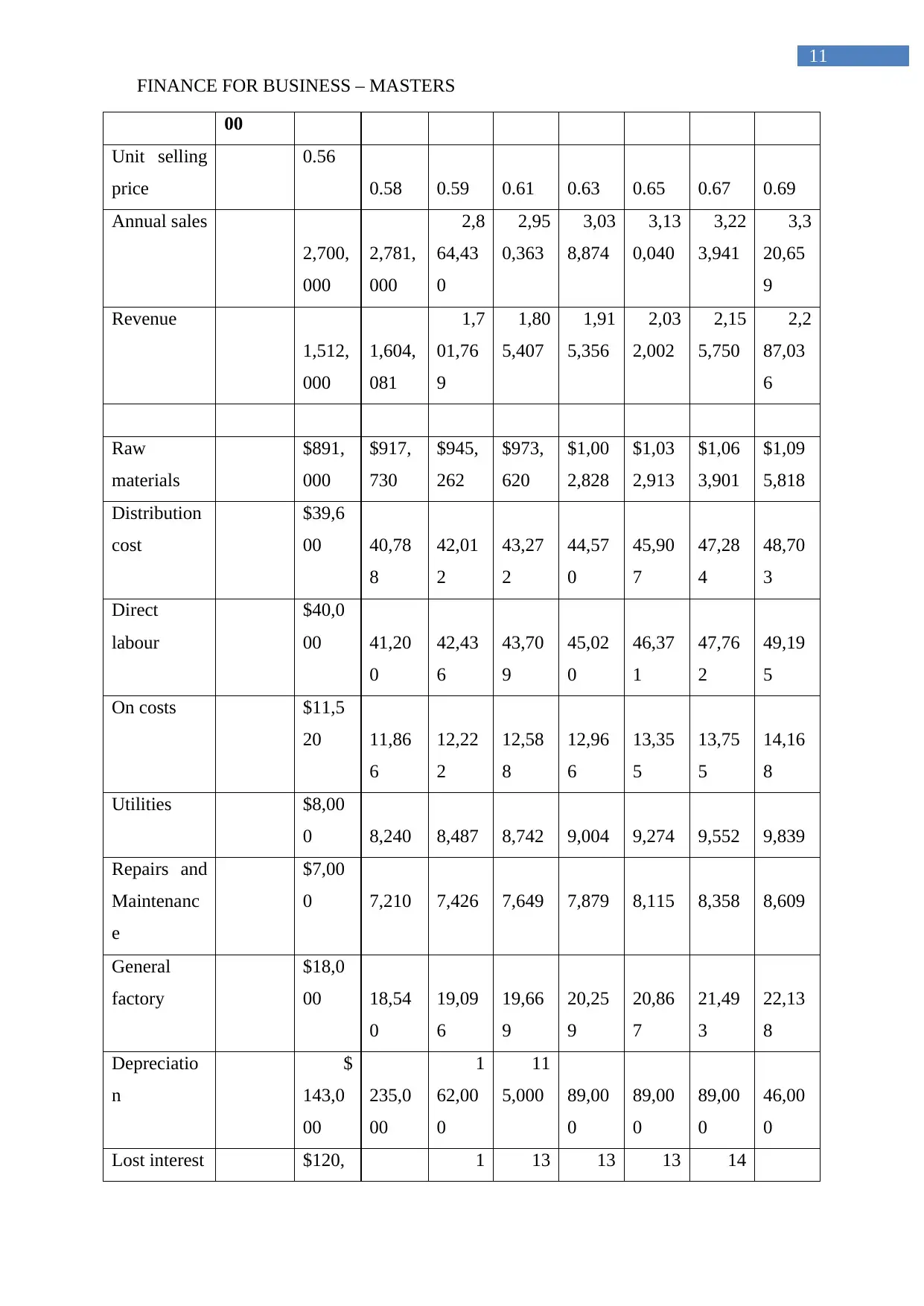

6. Increasing the annual sales by minimal value:

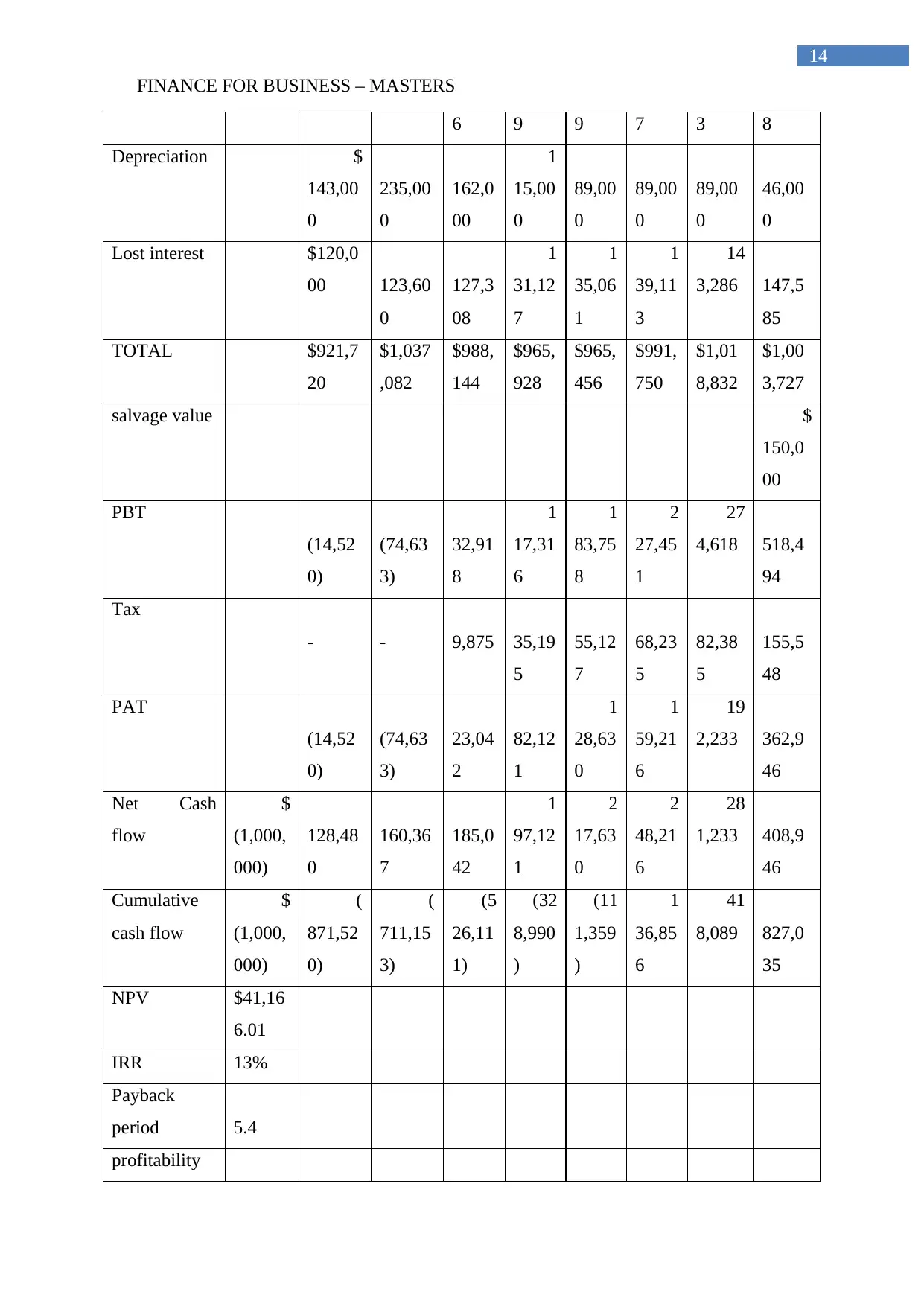

Best Case

Inflation

rate

3%

minimum

increment

20%

Particulars 0 1 2 3 4 5 6 7 8

Initial

investment

$

1,000,0

Paraphrase This Document

FINANCE FOR BUSINESS – MASTERS

00

Unit selling

price

0.56

0.58 0.59 0.61 0.63 0.65 0.67 0.69

Annual sales

2,700,

000

2,781,

000

2,8

64,43

0

2,95

0,363

3,03

8,874

3,13

0,040

3,22

3,941

3,3

20,65

9

Revenue

1,512,

000

1,604,

081

1,7

01,76

9

1,80

5,407

1,91

5,356

2,03

2,002

2,15

5,750

2,2

87,03

6

Raw

materials

$891,

000

$917,

730

$945,

262

$973,

620

$1,00

2,828

$1,03

2,913

$1,06

3,901

$1,09

5,818

Distribution

cost

$39,6

00 40,78

8

42,01

2

43,27

2

44,57

0

45,90

7

47,28

4

48,70

3

Direct

labour

$40,0

00 41,20

0

42,43

6

43,70

9

45,02

0

46,37

1

47,76

2

49,19

5

On costs $11,5

20 11,86

6

12,22

2

12,58

8

12,96

6

13,35

5

13,75

5

14,16

8

Utilities $8,00

0 8,240 8,487 8,742 9,004 9,274 9,552 9,839

Repairs and

Maintenanc

e

$7,00

0 7,210 7,426 7,649 7,879 8,115 8,358 8,609

General

factory

$18,0

00 18,54

0

19,09

6

19,66

9

20,25

9

20,86

7

21,49

3

22,13

8

Depreciatio

n

$

143,0

00

235,0

00

1

62,00

0

11

5,000 89,00

0

89,00

0

89,00

0

46,00

0

Lost interest $120, 1 13 13 13 14

FINANCE FOR BUSINESS – MASTERS

000 123,6

00

27,30

8

1,127 5,061 9,113 3,286 147,5

85

TOTAL $1,27

8,120

$1,40

4,174

$1,36

6,249

$1,35

5,376

$1,36

6,588

$1,40

4,915

$1,44

4,393

$1,44

2,054

salvage

value

$

150,0

00

PBT

233,8

80

199,9

07

3

35,52

1

45

0,031

54

8,769

62

7,086

71

1,358 994,9

81

Tax

- -

1

00,65

6

13

5,009

16

4,631

18

8,126

21

3,407 298,4

94

PAT

233,8

80

199,9

07

2

34,86

4

31

5,022

38

4,138

43

8,960

49

7,950 696,4

87

Net Cash

flow

$

(1,000,

000)

376,8

80

434,9

07

3

96,86

4

43

0,022

47

3,138

52

7,960

58

6,950 742,4

87

Cumulative

cash flow

$

(1,000,

000)

(623,1

20)

(188,2

13)

2

08,65

2

63

8,673

1,11

1,811

1,63

9,772

2,22

6,722

2,9

69,20

9

NPV $1,340,

309.13

IRR 41%

Payback

period 2.5

profitability

index 2.34

Worst Case

Inflation rate 3%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS – MASTERS

minimum

increment

20%

Particulars 0 1 2 3 4 5 6 7 8

Initial

investment

$

1,000,0

00

Unit selling

price

0.56

0.58 0.59 0.61 0.63 0.65 0.67 0.69

Annual sales 1

,620,0

00

1

,668,6

00

1,7

18,65

8

1,7

70,21

8

1,8

23,32

4

1,8

78,02

4

1,93

4,365

1,9

92,39

6

Revenue

907,20

0

962,44

8

1,0

21,06

2

1,0

83,24

4

1,1

49,21

4

1,2

19,20

1

1,29

3,450

1,3

72,22

1

Raw

materials

$534,6

00

$550,6

38

$567,

157

$584,

172

$601,

697

$619,

748

$638,

340

$657,

491

Distribution

cost

$39,60

0 40,788 42,01

2

43,27

2

44,57

0

45,90

7

47,28

4

48,70

3

Direct labour $40,00

0 41,200 42,43

6

43,70

9

45,02

0

46,37

1

47,76

2

49,19

5

On costs $11,52

0 11,866 12,22

2

12,58

8

12,96

6

13,35

5

13,75

5

14,16

8

Utilities $8,000

8,240 8,487 8,742 9,004 9,274 9,552 9,839

Repairs and

Maintenance

$7,000

7,210 7,426 7,649 7,879 8,115 8,358 8,609

General

factory

$18,00

0 18,540 19,09 19,66 20,25 20,86 21,49 22,13

Paraphrase This Document

FINANCE FOR BUSINESS – MASTERS

6 9 9 7 3 8

Depreciation $

143,00

0

235,00

0

162,0

00

1

15,00

0

89,00

0

89,00

0

89,00

0

46,00

0

Lost interest $120,0

00 123,60

0

127,3

08

1

31,12

7

1

35,06

1

1

39,11

3

14

3,286 147,5

85

TOTAL $921,7

20

$1,037

,082

$988,

144

$965,

928

$965,

456

$991,

750

$1,01

8,832

$1,00

3,727

salvage value $

150,0

00

PBT

(14,52

0)

(74,63

3)

32,91

8

1

17,31

6

1

83,75

8

2

27,45

1

27

4,618 518,4

94

Tax

- - 9,875 35,19

5

55,12

7

68,23

5

82,38

5

155,5

48

PAT

(14,52

0)

(74,63

3)

23,04

2

82,12

1

1

28,63

0

1

59,21

6

19

2,233 362,9

46

Net Cash

flow

$

(1,000,

000)

128,48

0

160,36

7

185,0

42

1

97,12

1

2

17,63

0

2

48,21

6

28

1,233 408,9

46

Cumulative

cash flow

$

(1,000,

000)

(

871,52

0)

(

711,15

3)

(5

26,11

1)

(32

8,990

)

(11

1,359

)

1

36,85

6

41

8,089 827,0

35

NPV $41,16

6.01

IRR 13%

Payback

period 5.4

profitability

FINANCE FOR BUSINESS – MASTERS

index 1.04

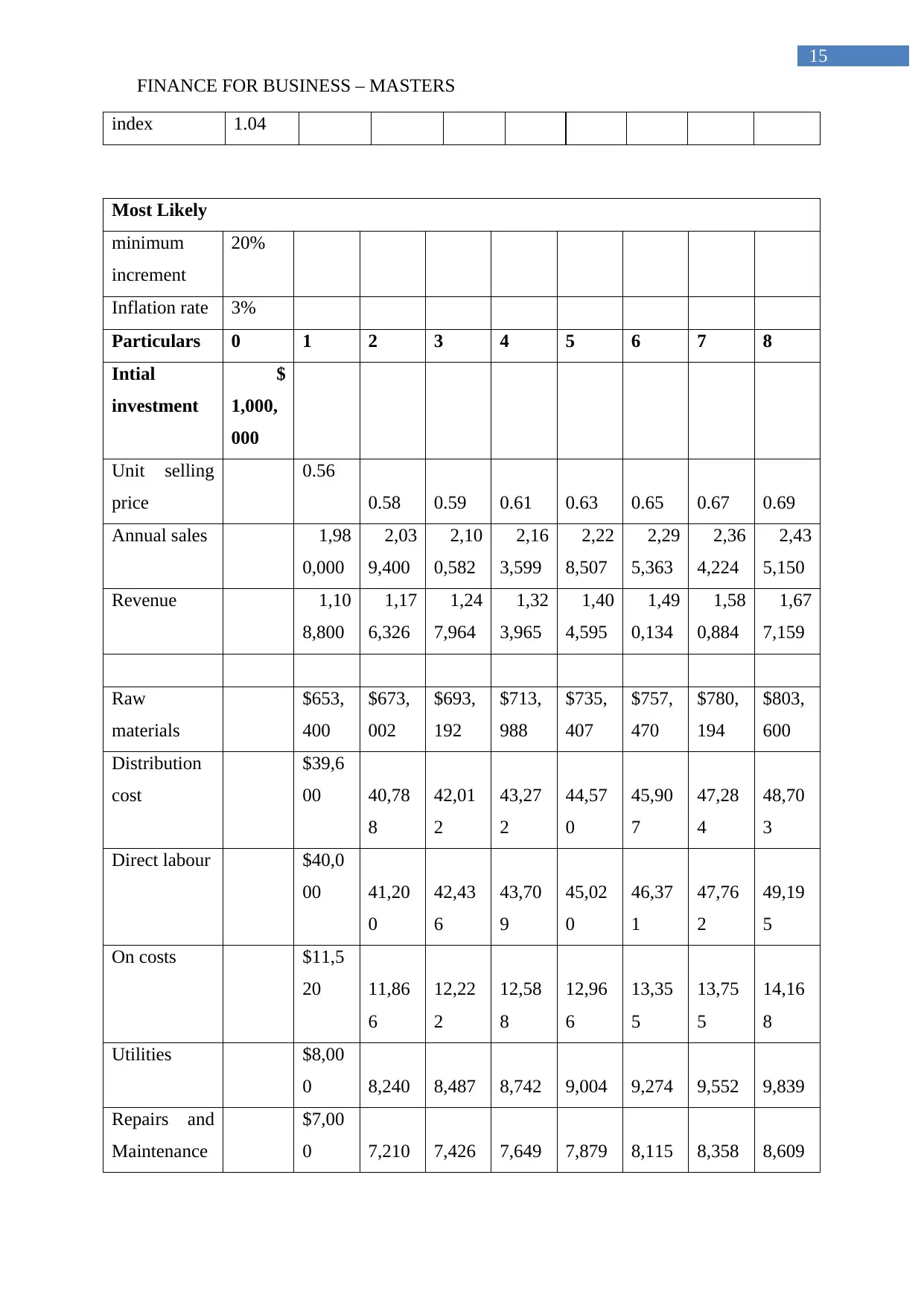

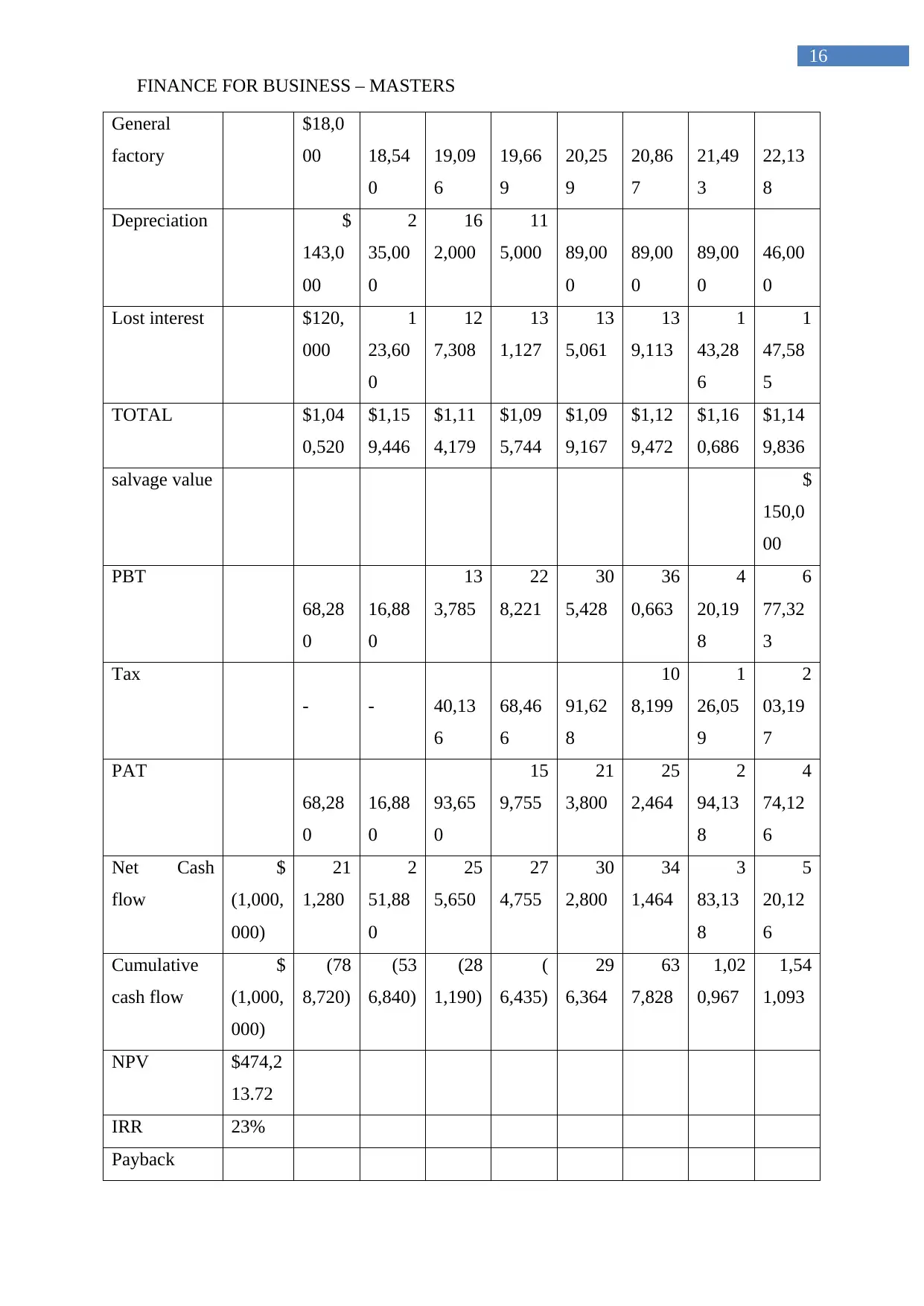

Most Likely

minimum

increment

20%

Inflation rate 3%

Particulars 0 1 2 3 4 5 6 7 8

Intial

investment

$

1,000,

000

Unit selling

price

0.56

0.58 0.59 0.61 0.63 0.65 0.67 0.69

Annual sales 1,98

0,000

2,03

9,400

2,10

0,582

2,16

3,599

2,22

8,507

2,29

5,363

2,36

4,224

2,43

5,150

Revenue 1,10

8,800

1,17

6,326

1,24

7,964

1,32

3,965

1,40

4,595

1,49

0,134

1,58

0,884

1,67

7,159

Raw

materials

$653,

400

$673,

002

$693,

192

$713,

988

$735,

407

$757,

470

$780,

194

$803,

600

Distribution

cost

$39,6

00 40,78

8

42,01

2

43,27

2

44,57

0

45,90

7

47,28

4

48,70

3

Direct labour $40,0

00 41,20

0

42,43

6

43,70

9

45,02

0

46,37

1

47,76

2

49,19

5

On costs $11,5

20 11,86

6

12,22

2

12,58

8

12,96

6

13,35

5

13,75

5

14,16

8

Utilities $8,00

0 8,240 8,487 8,742 9,004 9,274 9,552 9,839

Repairs and

Maintenance

$7,00

0 7,210 7,426 7,649 7,879 8,115 8,358 8,609

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS – MASTERS

General

factory

$18,0

00 18,54

0

19,09

6

19,66

9

20,25

9

20,86

7

21,49

3

22,13

8

Depreciation $

143,0

00

2

35,00

0

16

2,000

11

5,000 89,00

0

89,00

0

89,00

0

46,00

0

Lost interest $120,

000

1

23,60

0

12

7,308

13

1,127

13

5,061

13

9,113

1

43,28

6

1

47,58

5

TOTAL $1,04

0,520

$1,15

9,446

$1,11

4,179

$1,09

5,744

$1,09

9,167

$1,12

9,472

$1,16

0,686

$1,14

9,836

salvage value $

150,0

00

PBT

68,28

0

16,88

0

13

3,785

22

8,221

30

5,428

36

0,663

4

20,19

8

6

77,32

3

Tax

- - 40,13

6

68,46

6

91,62

8

10

8,199

1

26,05

9

2

03,19

7

PAT

68,28

0

16,88

0

93,65

0

15

9,755

21

3,800

25

2,464

2

94,13

8

4

74,12

6

Net Cash

flow

$

(1,000,

000)

21

1,280

2

51,88

0

25

5,650

27

4,755

30

2,800

34

1,464

3

83,13

8

5

20,12

6

Cumulative

cash flow

$

(1,000,

000)

(78

8,720)

(53

6,840)

(28

1,190)

(

6,435)

29

6,364

63

7,828

1,02

0,967

1,54

1,093

NPV $474,2

13.72

IRR 23%

Payback

Paraphrase This Document

FINANCE FOR BUSINESS – MASTERS

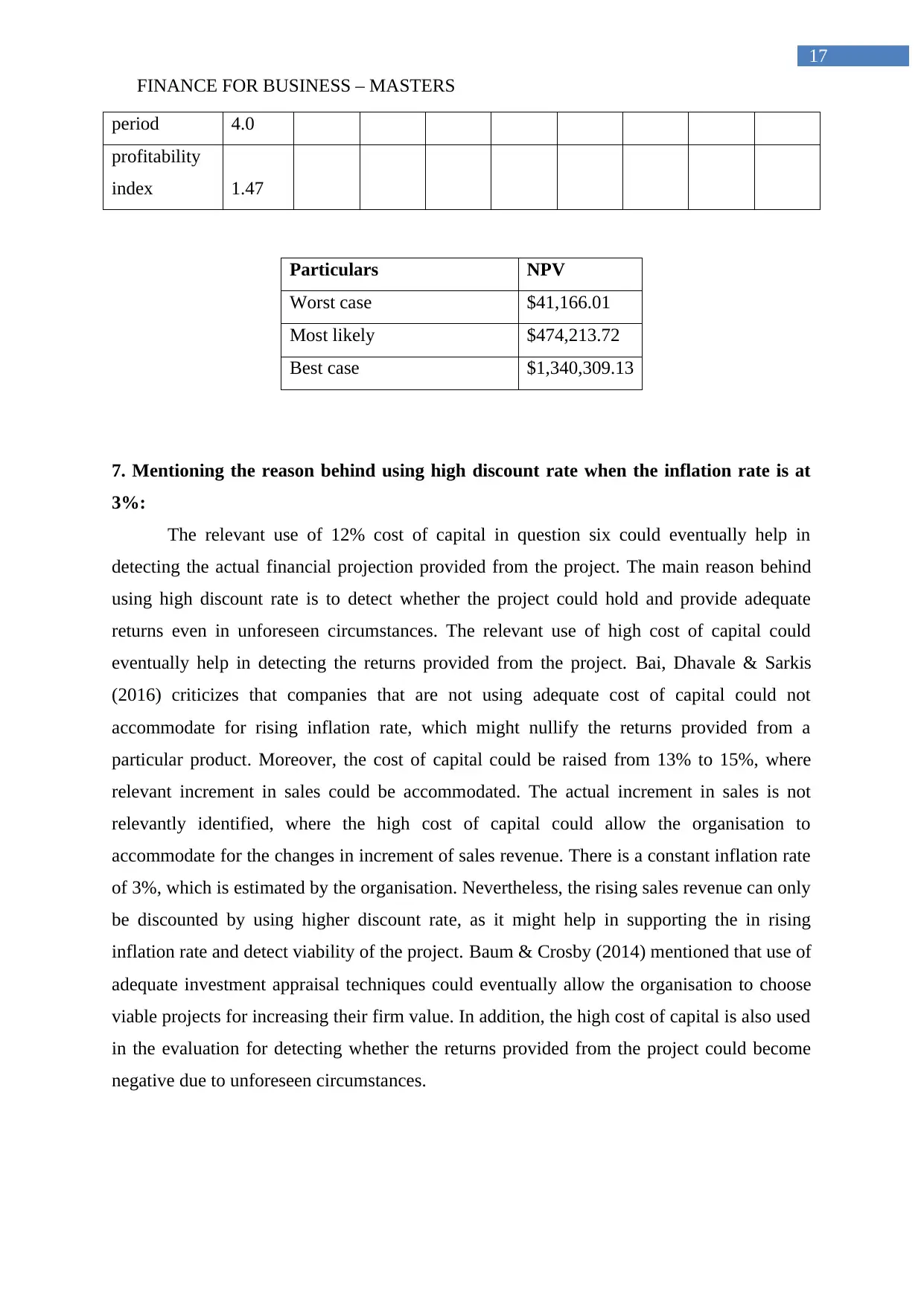

period 4.0

profitability

index 1.47

Particulars NPV

Worst case $41,166.01

Most likely $474,213.72

Best case $1,340,309.13

7. Mentioning the reason behind using high discount rate when the inflation rate is at

3%:

The relevant use of 12% cost of capital in question six could eventually help in

detecting the actual financial projection provided from the project. The main reason behind

using high discount rate is to detect whether the project could hold and provide adequate

returns even in unforeseen circumstances. The relevant use of high cost of capital could

eventually help in detecting the returns provided from the project. Bai, Dhavale & Sarkis

(2016) criticizes that companies that are not using adequate cost of capital could not

accommodate for rising inflation rate, which might nullify the returns provided from a

particular product. Moreover, the cost of capital could be raised from 13% to 15%, where

relevant increment in sales could be accommodated. The actual increment in sales is not

relevantly identified, where the high cost of capital could allow the organisation to

accommodate for the changes in increment of sales revenue. There is a constant inflation rate

of 3%, which is estimated by the organisation. Nevertheless, the rising sales revenue can only

be discounted by using higher discount rate, as it might help in supporting the in rising

inflation rate and detect viability of the project. Baum & Crosby (2014) mentioned that use of

adequate investment appraisal techniques could eventually allow the organisation to choose

viable projects for increasing their firm value. In addition, the high cost of capital is also used

in the evaluation for detecting whether the returns provided from the project could become

negative due to unforeseen circumstances.

FINANCE FOR BUSINESS – MASTERS

8. Mentioning the recommendation for the production of 10-in and 12-in Pipe to the

organisation:

From the evaluation of all the relevant calculation conducted above, it could be

identified that the overall project portrays a viable approach, which could help in generating

adequate revenue for the company. Moreover, the production of 10-in and 12-in Pipe is

actually feasible under all the three situations when sales revenue or increased by 20%. This

adequate increment in revenue could eventually help in generating the required returns which

could allow the organisation to increase their firm value in future. Nevertheless, the returns

provided directly indicate that the project is viable option for the company, which might help

in increasing both demand and revenue for the product. However, the evaluation of the

project under normal circumstances mainly supports only two situations most likely and best

case scenario, which provide adequate returns from investment. Moreover, the worst case

scenario provides the negative NPV, which indicates that the project will not be viable if

worst case scenario occurs (Bueno, Vassallo & Cheung, 2015). This could directly indicate

that relevant returns provided from the project can increase the risk and reduce return of the

company. Therefore under normal circumstances if the revenue does not increase after

producing 10-in and 12-in Pipe in the factory premises then the project has relevant risk from

investment. Adequate evaluation of it conducted the expected sales, standard deviation, and

Coefficient of variance is calculated. The relevant expected sales is $397,142.19 with a

standard deviation of $ 398,484.02 and Coefficient of variance of 1.0034.directly indicates

that the organisation could commence with the project, as it might provide higher returns

from investment.

Hence, from the evaluation of different calculations conducted in the above tables it

could be identified that overall project for producing 10-in and 12-in Pipe in the premises of

the organisation is a viable approach, which could provide higher returns from investment.

Moreover, the relevant production of 10-in and 12-in Pipe could also boost the current

products, which is being produced by the organisation. This could eventually help in boosting

the revenues of the total products produced by the organisation. Therefore, it is advisable for

organisation 2 comments with the current project, which might help any increasing its

customer base and revenue in future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS – MASTERS

Reference and Bibliography:

Aggarwal, A., & Thakur, G. S. M. (2013). Techniques of performance appraisal-a

review. International Journal of Engineering and Advanced Technology

(IJEAT), 2(3), 2249-8958.

Awojobi, O., & Jenkins, G. P. (2016). Managing the cost overrun risks of hydroelectric dams:

An application of reference class forecasting techniques. Renewable and Sustainable

Energy Reviews, 63, 19-32.

Bai, C., Dhavale, D., & Sarkis, J. (2016). Complex investment decisions using rough set and

fuzzy c-means: an example of investment in green supply chains. European journal of

operational research, 248(2), 507-521.

Baum, A. E., & Crosby, N. (2014). Property investment appraisal. John Wiley & Sons.

Bueno, P. C., Vassallo, J. M., & Cheung, K. (2015). Sustainability assessment of transport

infrastructure projects: a review of existing tools and methods. Transport

Reviews, 35(5), 622-649.

Burns, R., & Walker, J. (2015). Capital budgeting surveys: the future is now.

Byett, A. J., Laird, J., Stroombergen, A., & Trodd, S. (2015). Assessing new approaches to

estimating the economic impact of transport interventions using the gross value added

approach (No. 566).

Crosby, N., & Henneberry, J. (2016). Financialisation, the valuation of investment property

and the urban built environment in the UK. Urban Studies, 53(7), 1424-1441.

Dittrich, R., Wreford, A., & Moran, D. (2016). A survey of decision-making approaches for

climate change adaptation: Are robust methods the way forward?. Ecological

Economics, 122, 79-89.

Eliasson, J., & Börjesson, M. (2014). On timetable assumptions in railway investment

appraisal. Transport Policy, 36, 118-126.

Fu, Y., Xiong, H., Ge, Y., Yao, Z., Zheng, Y., & Zhou, Z. H. (2014, August). Exploiting

geographic dependencies for real estate appraisal: a mutual perspective of ranking and

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.