Financial Analysis of Caltex Australia: Profitability, Efficiency, and Cash Management

VerifiedAdded on 2022/11/14

|23

|3898

|463

AI Summary

This report analyzes the financial performance of Caltex Australia through ratio analysis, cash management, sensitivity, dividend payout, systematic and unsystematic risks. It provides recommendations for institutional investors based on the findings.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Finance for business - Masters

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Abstract

This report has been undertaken to examine the financial performance of selected ASX

listed entity, that is, Caltex Australia. The financial performance as examined through the use of

analysis of ratios, cash management, sensitivity, dividend payout, systematic and unsystematic

risks ahs reflected that the company is presently not in a high state of growth and development, It

has weak profitability, cash management and efficiency position and therefore an investor need

to examine the future financial performance before taking any significant investment decision.

2

This report has been undertaken to examine the financial performance of selected ASX

listed entity, that is, Caltex Australia. The financial performance as examined through the use of

analysis of ratios, cash management, sensitivity, dividend payout, systematic and unsystematic

risks ahs reflected that the company is presently not in a high state of growth and development, It

has weak profitability, cash management and efficiency position and therefore an investor need

to examine the future financial performance before taking any significant investment decision.

2

Contents

Abstract............................................................................................................................................2

1. Introduction..................................................................................................................................4

2. Financial Analysis of Caltex Australia........................................................................................4

2.1: Description of the Company.................................................................................................4

2.2: Use of Ratio Analysis to evaluate the financial performance of Caltex Australia...............5

2.3: Cash Management Analysis...............................................................................................10

Part 2.4: Application of capital budgeting and sensitivity analysis...........................................11

2.5 Identification and Discussion of Systematic and Un-systematic Risk Impacting the

Performance of Caltex Australia...............................................................................................16

Unsystematic Risk.....................................................................................................................16

Systematic Risks........................................................................................................................17

Part 2.6: Calculation of dividend payout ratio and identification of dividend policy of Caltex

Australia Limited.......................................................................................................................19

3. Recommendation Letter.............................................................................................................21

4. Conclusion.................................................................................................................................22

References......................................................................................................................................23

3

Abstract............................................................................................................................................2

1. Introduction..................................................................................................................................4

2. Financial Analysis of Caltex Australia........................................................................................4

2.1: Description of the Company.................................................................................................4

2.2: Use of Ratio Analysis to evaluate the financial performance of Caltex Australia...............5

2.3: Cash Management Analysis...............................................................................................10

Part 2.4: Application of capital budgeting and sensitivity analysis...........................................11

2.5 Identification and Discussion of Systematic and Un-systematic Risk Impacting the

Performance of Caltex Australia...............................................................................................16

Unsystematic Risk.....................................................................................................................16

Systematic Risks........................................................................................................................17

Part 2.6: Calculation of dividend payout ratio and identification of dividend policy of Caltex

Australia Limited.......................................................................................................................19

3. Recommendation Letter.............................................................................................................21

4. Conclusion.................................................................................................................................22

References......................................................................................................................................23

3

1. Introduction

The purpose of the present report is to develop an understanding of the methods used in

conducting financial analysis of a selected listed company within ASX. The financial analysis

has been performed through evaluation of the financial statements of the selected company. The

overall financial evaluation of the selected company is done for proving suggestions to

institutional investors for investing within the Australian market. The recommendations provided

through report will assist the investors to take correct investment decision based on the financial

outcomes of the company.

The ASX listed entity selected for financial evaluation purpose is Caltex Australia, a

transport based fuel supplier and convenience retailer of Australia. The report, in this context,

has performed financial analysis of the selected company through the use of ratio analysis,

evaluation of its cash management, performing sensitivity analysis, identifications of the

systematic and unsystematic risks and examination of its dividend policy. The recommendation

letter is provided to the institutional investors on the basis of overall evaluation conducted and

lastly the findings obtained are summarized in the conclusion section of the report.

2. Financial Analysis of Caltex Australia

2.1: Description of the Company

Caltex Australia Limited is a recognized Australian based Transport Company involved

in providing fuel and operates convenience stores across Australia. The core activities of the

company consist of purchasing, distributing and marketing of petroleum based products and also

operating its convenience stories. It is an ASX listed entity that has attained a leading position in

meeting the fuel needs within Australia. It has developed a flexible supply chain that has enabled

it to develop high quality fuel products to its diverse number of customer segments such as retail,

mining, agriculture, aviation, marine and automotive sector. In addition to this, it is also

recognized to be prominent convenience retailers within the country. It is only fuel and

convenience retailing company of Australia that is listed on the ASX. It has attained a unique

position among the refiner and marketers in Australia on the basis of carrying out its operations

4

The purpose of the present report is to develop an understanding of the methods used in

conducting financial analysis of a selected listed company within ASX. The financial analysis

has been performed through evaluation of the financial statements of the selected company. The

overall financial evaluation of the selected company is done for proving suggestions to

institutional investors for investing within the Australian market. The recommendations provided

through report will assist the investors to take correct investment decision based on the financial

outcomes of the company.

The ASX listed entity selected for financial evaluation purpose is Caltex Australia, a

transport based fuel supplier and convenience retailer of Australia. The report, in this context,

has performed financial analysis of the selected company through the use of ratio analysis,

evaluation of its cash management, performing sensitivity analysis, identifications of the

systematic and unsystematic risks and examination of its dividend policy. The recommendation

letter is provided to the institutional investors on the basis of overall evaluation conducted and

lastly the findings obtained are summarized in the conclusion section of the report.

2. Financial Analysis of Caltex Australia

2.1: Description of the Company

Caltex Australia Limited is a recognized Australian based Transport Company involved

in providing fuel and operates convenience stores across Australia. The core activities of the

company consist of purchasing, distributing and marketing of petroleum based products and also

operating its convenience stories. It is an ASX listed entity that has attained a leading position in

meeting the fuel needs within Australia. It has developed a flexible supply chain that has enabled

it to develop high quality fuel products to its diverse number of customer segments such as retail,

mining, agriculture, aviation, marine and automotive sector. In addition to this, it is also

recognized to be prominent convenience retailers within the country. It is only fuel and

convenience retailing company of Australia that is listed on the ASX. It has attained a unique

position among the refiner and marketers in Australia on the basis of carrying out its operations

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

in an independent manner and all the decision-taking is with management and the Board (Caltex

Australia: Our Company, 2019).

2.2: Use of Ratio Analysis to evaluate the financial performance of Caltex Australia

Profitability Ratios of Caltex Australia

Financial Data of Caltex Australia for calculation of Profitability Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Operating profit

$

811,350.00

$

934,953.00

$

930,497.00

$

819,969.00

Net profit after tax

$

522,621.00

$

610,480.00

$

620,752.00

$

561,590.00

Net Sales

$

19,926,546.00

$

17,933,201.00

$

16,285,810.00

$

21,731,342.00

Shareholder's equity

$

2,787,805.00

$

2,810,215.00

$

3,107,901.00

$

3,389,064.00

Average shareholder's

equity

$

2,799,010.00

$

2,959,058.00

$

3,248,482.50

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Profitability Ratio of Caltex Australia

Ratios Formula 2016 2017 2018

5

Australia: Our Company, 2019).

2.2: Use of Ratio Analysis to evaluate the financial performance of Caltex Australia

Profitability Ratios of Caltex Australia

Financial Data of Caltex Australia for calculation of Profitability Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Operating profit

$

811,350.00

$

934,953.00

$

930,497.00

$

819,969.00

Net profit after tax

$

522,621.00

$

610,480.00

$

620,752.00

$

561,590.00

Net Sales

$

19,926,546.00

$

17,933,201.00

$

16,285,810.00

$

21,731,342.00

Shareholder's equity

$

2,787,805.00

$

2,810,215.00

$

3,107,901.00

$

3,389,064.00

Average shareholder's

equity

$

2,799,010.00

$

2,959,058.00

$

3,248,482.50

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Profitability Ratio of Caltex Australia

Ratios Formula 2016 2017 2018

5

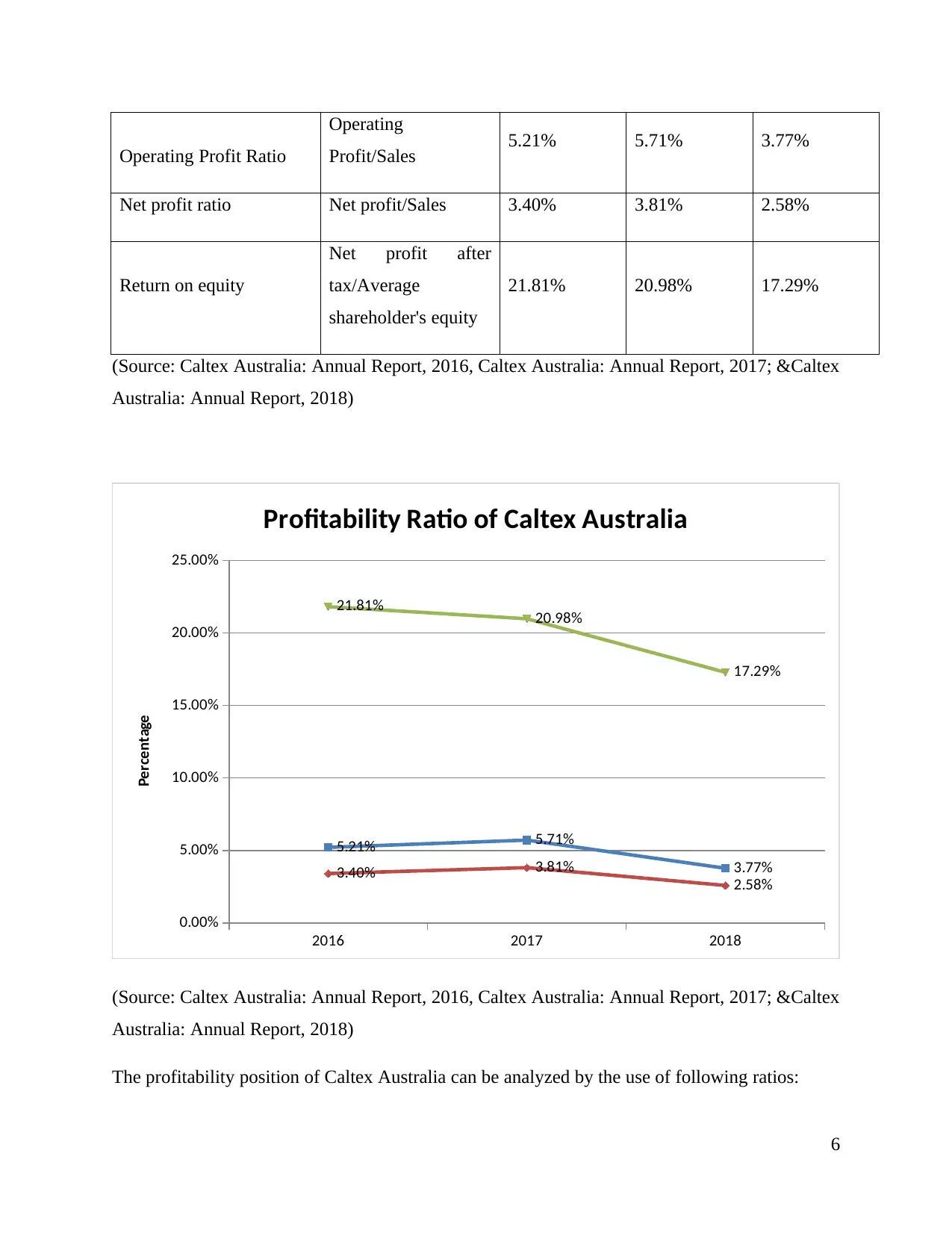

Operating Profit Ratio

Operating

Profit/Sales 5.21% 5.71% 3.77%

Net profit ratio Net profit/Sales 3.40% 3.81% 2.58%

Return on equity

Net profit after

tax/Average

shareholder's equity

21.81% 20.98% 17.29%

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017; &Caltex

Australia: Annual Report, 2018)

2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

5.21% 5.71%

3.77%3.40% 3.81%

2.58%

21.81% 20.98%

17.29%

Profitability Ratio of Caltex Australia

Percentage

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017; &Caltex

Australia: Annual Report, 2018)

The profitability position of Caltex Australia can be analyzed by the use of following ratios:

6

Operating

Profit/Sales 5.21% 5.71% 3.77%

Net profit ratio Net profit/Sales 3.40% 3.81% 2.58%

Return on equity

Net profit after

tax/Average

shareholder's equity

21.81% 20.98% 17.29%

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017; &Caltex

Australia: Annual Report, 2018)

2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

5.21% 5.71%

3.77%3.40% 3.81%

2.58%

21.81% 20.98%

17.29%

Profitability Ratio of Caltex Australia

Percentage

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017; &Caltex

Australia: Annual Report, 2018)

The profitability position of Caltex Australia can be analyzed by the use of following ratios:

6

Operating Profit Ratio: The Operating Profit ratio indicates the profit from operating

Activities attributable towards per $ of net Sales. Caltex Australia’s operating Profit has

an upward trend from 2016 to 2017 but in 2018 it has a downward trend as operating

profit ratio comes to 3.77% from 5.71%. If we analyses the data the reason behind a low

operating profit as compared to 2017’s operating profit is increase in selling and

distribution expenses. Net sales in 2018 is increased as compared to previous years so as

other expenses, but Caltex Australia had to spent a higher amount on selling and

distribution expenses. It may be due to new competitors in market, or availability of

substitutes in market resulting in a low operating profit (Krantz, 2016).

Net Profit Ratio: Net Profit Ratio Measures the net profit attributable towards per $ of

Net Sales. However Net profit ratio is also increased from 3.40% (2016) to 3.81 %( 2017)

but then it went down to 2.58% in 2018. The reason behind the downward trend in year

2017 to year 2018 is the same as of the operating profit ratio. Because Caltex Australia

has a low finance cost and a high share of profit/loss from other entities as compared to

2017. Company had to spend money on Selling and distribution of its products due to

competitors and substitutes available in market (Reilly and Brown, 2011).

Return on Equity: ROE states the rate of return realized by company on its equity

investment. Here also an upward trend is noticed in year 2016 to year 2017 but then there

is a downward trend in year 2017 to 2018. However the downward trend is not because

of increase in equity (Moles and Kidwekk, 2011). But it can be said that Caltex Australia

has lower finance cost as compared to 2017 that shows that it has repaid its debt resulting

in a lower profit as well as company has created reserves in 2018 which was not there in

2017 or can say has a negative balance in 2017. Thus Caltex Australia has a low return on

equity 17.29% as compared to 2017 of 20.98%.

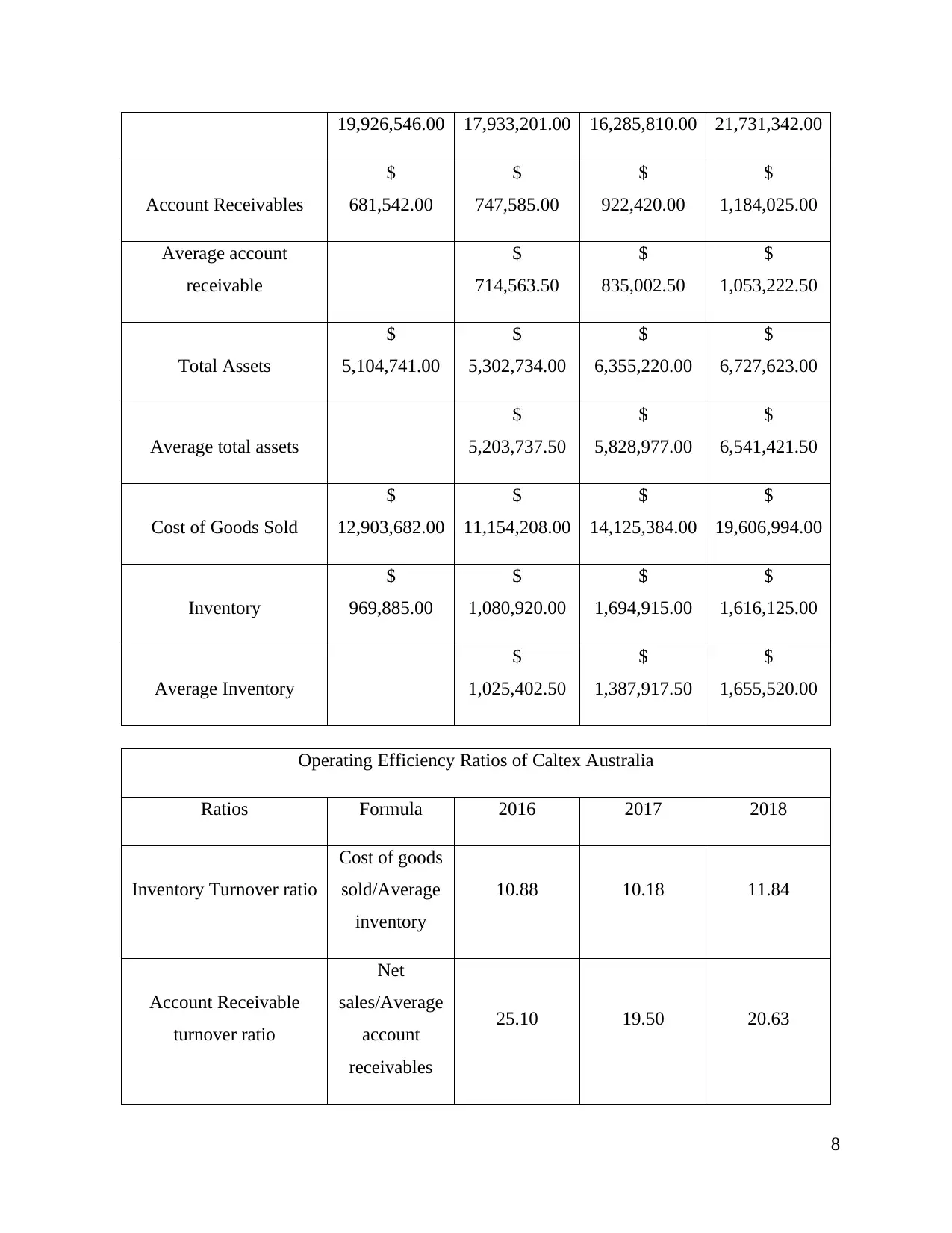

Operating Efficiency Ratios

Financial Data of Caltex Australia for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales $ $ $ $

7

Activities attributable towards per $ of net Sales. Caltex Australia’s operating Profit has

an upward trend from 2016 to 2017 but in 2018 it has a downward trend as operating

profit ratio comes to 3.77% from 5.71%. If we analyses the data the reason behind a low

operating profit as compared to 2017’s operating profit is increase in selling and

distribution expenses. Net sales in 2018 is increased as compared to previous years so as

other expenses, but Caltex Australia had to spent a higher amount on selling and

distribution expenses. It may be due to new competitors in market, or availability of

substitutes in market resulting in a low operating profit (Krantz, 2016).

Net Profit Ratio: Net Profit Ratio Measures the net profit attributable towards per $ of

Net Sales. However Net profit ratio is also increased from 3.40% (2016) to 3.81 %( 2017)

but then it went down to 2.58% in 2018. The reason behind the downward trend in year

2017 to year 2018 is the same as of the operating profit ratio. Because Caltex Australia

has a low finance cost and a high share of profit/loss from other entities as compared to

2017. Company had to spend money on Selling and distribution of its products due to

competitors and substitutes available in market (Reilly and Brown, 2011).

Return on Equity: ROE states the rate of return realized by company on its equity

investment. Here also an upward trend is noticed in year 2016 to year 2017 but then there

is a downward trend in year 2017 to 2018. However the downward trend is not because

of increase in equity (Moles and Kidwekk, 2011). But it can be said that Caltex Australia

has lower finance cost as compared to 2017 that shows that it has repaid its debt resulting

in a lower profit as well as company has created reserves in 2018 which was not there in

2017 or can say has a negative balance in 2017. Thus Caltex Australia has a low return on

equity 17.29% as compared to 2017 of 20.98%.

Operating Efficiency Ratios

Financial Data of Caltex Australia for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales $ $ $ $

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19,926,546.00 17,933,201.00 16,285,810.00 21,731,342.00

Account Receivables

$

681,542.00

$

747,585.00

$

922,420.00

$

1,184,025.00

Average account

receivable

$

714,563.50

$

835,002.50

$

1,053,222.50

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Cost of Goods Sold

$

12,903,682.00

$

11,154,208.00

$

14,125,384.00

$

19,606,994.00

Inventory

$

969,885.00

$

1,080,920.00

$

1,694,915.00

$

1,616,125.00

Average Inventory

$

1,025,402.50

$

1,387,917.50

$

1,655,520.00

Operating Efficiency Ratios of Caltex Australia

Ratios Formula 2016 2017 2018

Inventory Turnover ratio

Cost of goods

sold/Average

inventory

10.88 10.18 11.84

Account Receivable

turnover ratio

Net

sales/Average

account

receivables

25.10 19.50 20.63

8

Account Receivables

$

681,542.00

$

747,585.00

$

922,420.00

$

1,184,025.00

Average account

receivable

$

714,563.50

$

835,002.50

$

1,053,222.50

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Cost of Goods Sold

$

12,903,682.00

$

11,154,208.00

$

14,125,384.00

$

19,606,994.00

Inventory

$

969,885.00

$

1,080,920.00

$

1,694,915.00

$

1,616,125.00

Average Inventory

$

1,025,402.50

$

1,387,917.50

$

1,655,520.00

Operating Efficiency Ratios of Caltex Australia

Ratios Formula 2016 2017 2018

Inventory Turnover ratio

Cost of goods

sold/Average

inventory

10.88 10.18 11.84

Account Receivable

turnover ratio

Net

sales/Average

account

receivables

25.10 19.50 20.63

8

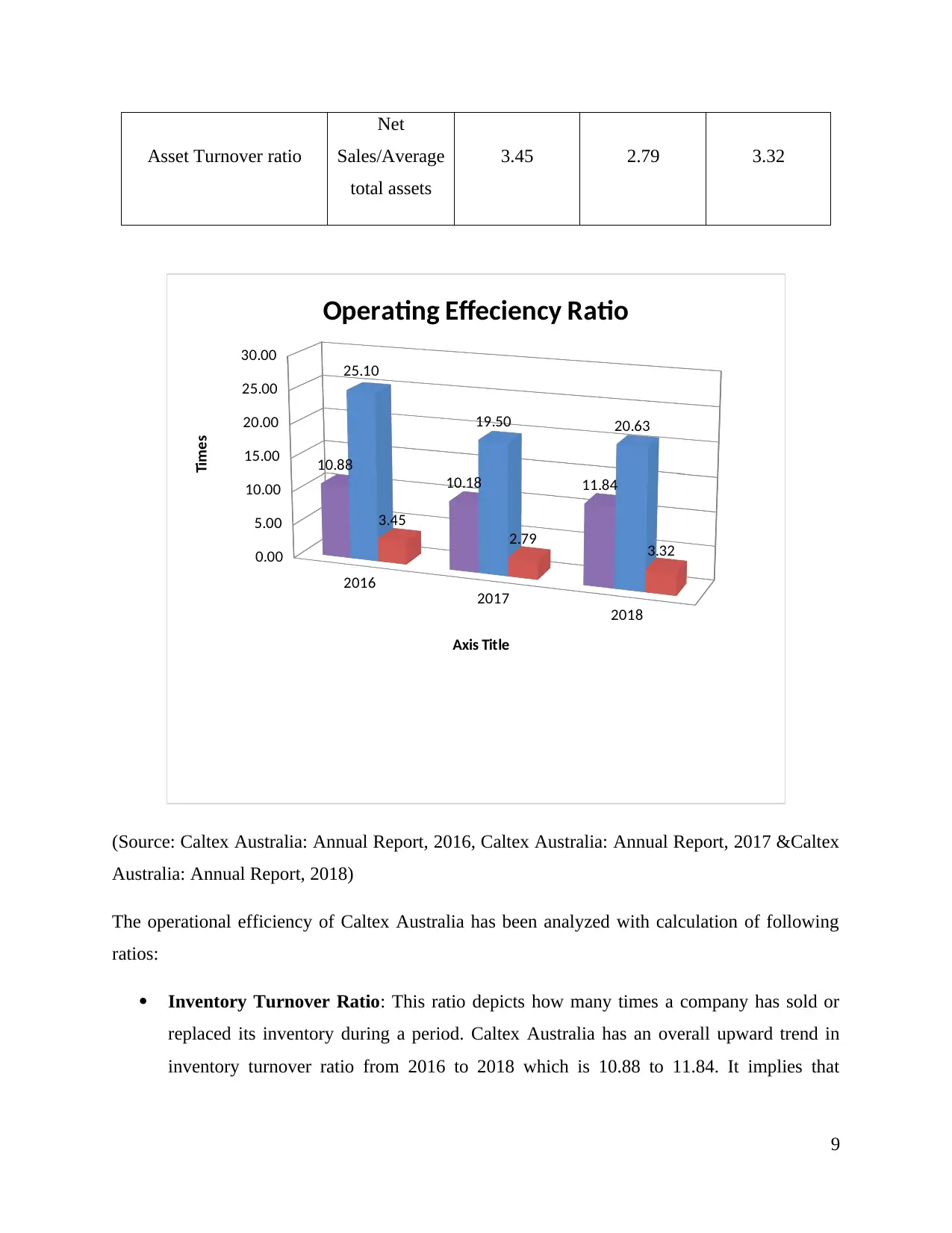

Asset Turnover ratio

Net

Sales/Average

total assets

3.45 2.79 3.32

2016

2017

2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

10.88

10.18 11.84

25.10

19.50 20.63

3.45

2.79 3.32

Operating Effeciency Ratio

Axis Title

Times

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017 &Caltex

Australia: Annual Report, 2018)

The operational efficiency of Caltex Australia has been analyzed with calculation of following

ratios:

Inventory Turnover Ratio: This ratio depicts how many times a company has sold or

replaced its inventory during a period. Caltex Australia has an overall upward trend in

inventory turnover ratio from 2016 to 2018 which is 10.88 to 11.84. It implies that

9

Net

Sales/Average

total assets

3.45 2.79 3.32

2016

2017

2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

10.88

10.18 11.84

25.10

19.50 20.63

3.45

2.79 3.32

Operating Effeciency Ratio

Axis Title

Times

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017 &Caltex

Australia: Annual Report, 2018)

The operational efficiency of Caltex Australia has been analyzed with calculation of following

ratios:

Inventory Turnover Ratio: This ratio depicts how many times a company has sold or

replaced its inventory during a period. Caltex Australia has an overall upward trend in

inventory turnover ratio from 2016 to 2018 which is 10.88 to 11.84. It implies that

9

company is very good at replacing its inventory regularly which will result in low cost of

holding and storage and improve its profitability in long run (Bragg, 2010).

Account Receivable Ratio: Account Receivable ratio depicts number of times a

company can realize payment from its average debtors in a year. If we look into the chart

we notice a downward trend but actually company is improving its efficiency. In 2016

this ratio was 25.10 times which comes to 19.50 times in 2017 but in 2018 company has

efficiently collected its debtors and it comes to 20.63. In 2017 the downward trend is

noticed because of loss of $14 million and in 2018 its $12 million.

Asset Turnover Ratio: This ratio shows company’s ability to best use of its assets to

generate revenue. A downward trend is noticed in past three years (2016-2018) which

may be due to the abnormal loss company has faced in 2017 and 2018. But overall

company is improving its efficiency and using its resources at its best to generate revenue

(Feldman and Libman, 2011).

2.3: Cash Management Analysis

Marketable securities are regarded as the liquid instruments of the company that can be

quickly transferred into cash for meeting the current financial obligations. The liquidity of

marketable securities is due to the fact that they possess the maturity of less than a year and

therefore can be quickly transferred into cash for meeting the financial obligations (Gibson,

2011). As analyzed form the balance sheet of Caltex Australia, the current assets of the company

includes cash and cash equivalents and receivables as marketable securities that presents the

assets that can be quickly transferred into cash. The cash and cash equivalents of the company

has depicted a decline over the past three financial years from 2016-2018 as analyzed from the

financial reports of the company over the selected time period. The cash and cash equivalents

have decreased from 116,606 to 6,142 over the selected financial period. On the other hand, its

account receivables have depicted a large increase over the selected time period as reflected in

the current assets of the company within its balance sheet. It has largely increased from 554,769

to 1,184,025 over the selected financial period (Caltex Australia: Annual Reports, 2019). These

means that the company need to quickly realize its accounts receivable for improving the future

cash flow position as it is holding less cash equivalents. The decrease in the cash equivalents can

results in causing a liquidity risk within the company due to its inability to meet the current

10

holding and storage and improve its profitability in long run (Bragg, 2010).

Account Receivable Ratio: Account Receivable ratio depicts number of times a

company can realize payment from its average debtors in a year. If we look into the chart

we notice a downward trend but actually company is improving its efficiency. In 2016

this ratio was 25.10 times which comes to 19.50 times in 2017 but in 2018 company has

efficiently collected its debtors and it comes to 20.63. In 2017 the downward trend is

noticed because of loss of $14 million and in 2018 its $12 million.

Asset Turnover Ratio: This ratio shows company’s ability to best use of its assets to

generate revenue. A downward trend is noticed in past three years (2016-2018) which

may be due to the abnormal loss company has faced in 2017 and 2018. But overall

company is improving its efficiency and using its resources at its best to generate revenue

(Feldman and Libman, 2011).

2.3: Cash Management Analysis

Marketable securities are regarded as the liquid instruments of the company that can be

quickly transferred into cash for meeting the current financial obligations. The liquidity of

marketable securities is due to the fact that they possess the maturity of less than a year and

therefore can be quickly transferred into cash for meeting the financial obligations (Gibson,

2011). As analyzed form the balance sheet of Caltex Australia, the current assets of the company

includes cash and cash equivalents and receivables as marketable securities that presents the

assets that can be quickly transferred into cash. The cash and cash equivalents of the company

has depicted a decline over the past three financial years from 2016-2018 as analyzed from the

financial reports of the company over the selected time period. The cash and cash equivalents

have decreased from 116,606 to 6,142 over the selected financial period. On the other hand, its

account receivables have depicted a large increase over the selected time period as reflected in

the current assets of the company within its balance sheet. It has largely increased from 554,769

to 1,184,025 over the selected financial period (Caltex Australia: Annual Reports, 2019). These

means that the company need to quickly realize its accounts receivable for improving the future

cash flow position as it is holding less cash equivalents. The decrease in the cash equivalents can

results in causing a liquidity risk within the company due to its inability to meet the current

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

obligations. The cash realized from its accounts receivables can provide large assistance to the

company in meeting its future financial obligations (Brigham and Michael, 2013).

Part 2.4: Application of capital budgeting and sensitivity analysis

Project Life 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per

year 450,000.00$

Initial Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Data Given

11

company in meeting its future financial obligations (Brigham and Michael, 2013).

Part 2.4: Application of capital budgeting and sensitivity analysis

Project Life 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per

year 450,000.00$

Initial Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Data Given

11

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

Statement of Cash flows

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,605,000.00$ 0.909 1,459,090.909$

2 1,605,000.00$ 0.826 1,326,446.281$

3 1,605,000.00$ 0.751 1,205,860.255$

4 2,405,000.00$ 0.683 1,642,647.360$

NPV 3,034,044.806$

Project NPV when there is no change in value drivers

12

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

Statement of Cash flows

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,605,000.00$ 0.909 1,459,090.909$

2 1,605,000.00$ 0.826 1,326,446.281$

3 1,605,000.00$ 0.751 1,205,860.255$

4 2,405,000.00$ 0.683 1,642,647.360$

NPV 3,034,044.806$

Project NPV when there is no change in value drivers

12

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Cash Inflows

Selling Units 270000 270000 270000 270000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,240,000.00$ 3,240,000.00$ 3,240,000.00$ 3,240,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 3,990,000.00$ 3,990,000.00$ 3,990,000.00$ 3,990,000.00$

Cash flows before tax 1,410,000.00$ 1,410,000.00$ 1,410,000.00$ 1,410,000.00$

Less: Tax @ 30% 423,000.00$ 423,000.00$ 423,000.00$ 423,000.00$

Cash Flows after tax 987,000.00$ 987,000.00$ 987,000.00$ 987,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 2,237,000.00$

Statement of Cash flows when Unit sales decrease by 10%

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,437,000.00$ 0.909 1,306,363.636$

2 1,437,000.00$ 0.826 1,187,603.306$

3 1,437,000.00$ 0.751 1,079,639.369$

4 2,237,000.00$ 0.683 1,527,901.100$

NPV 2,501,507.411$

Project NPV when Unit sales decrease by 10%

13

Cash Inflows

Selling Units 270000 270000 270000 270000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,240,000.00$ 3,240,000.00$ 3,240,000.00$ 3,240,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 3,990,000.00$ 3,990,000.00$ 3,990,000.00$ 3,990,000.00$

Cash flows before tax 1,410,000.00$ 1,410,000.00$ 1,410,000.00$ 1,410,000.00$

Less: Tax @ 30% 423,000.00$ 423,000.00$ 423,000.00$ 423,000.00$

Cash Flows after tax 987,000.00$ 987,000.00$ 987,000.00$ 987,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 2,237,000.00$

Statement of Cash flows when Unit sales decrease by 10%

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,437,000.00$ 0.909 1,306,363.636$

2 1,437,000.00$ 0.826 1,187,603.306$

3 1,437,000.00$ 0.751 1,079,639.369$

4 2,237,000.00$ 0.683 1,527,901.100$

NPV 2,501,507.411$

Project NPV when Unit sales decrease by 10%

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,050,000.00$ 1,050,000.00$ 1,050,000.00$ 1,050,000.00$

Less: Tax @ 30% 315,000.00$ 315,000.00$ 315,000.00$ 315,000.00$

Cash Flows after tax 735,000.00$ 735,000.00$ 735,000.00$ 735,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,185,000.00$ 1,185,000.00$ 1,185,000.00$ 1,185,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,185,000.00$ 1,185,000.00$ 1,185,000.00$ 1,985,000.00$

Statement of Cash flows when Price per unit decreases by 10%

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,185,000.00$ 0.909 1,077,272.727$

2 1,185,000.00$ 0.826 979,338.843$

3 1,185,000.00$ 0.751 890,308.039$

4 1,985,000.00$ 0.683 1,355,781.709$

NPV 1,702,701.318$

Project NPV when Price per unit decreases by 10%

14

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,050,000.00$ 1,050,000.00$ 1,050,000.00$ 1,050,000.00$

Less: Tax @ 30% 315,000.00$ 315,000.00$ 315,000.00$ 315,000.00$

Cash Flows after tax 735,000.00$ 735,000.00$ 735,000.00$ 735,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,185,000.00$ 1,185,000.00$ 1,185,000.00$ 1,185,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,185,000.00$ 1,185,000.00$ 1,185,000.00$ 1,985,000.00$

Statement of Cash flows when Price per unit decreases by 10%

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,185,000.00$ 0.909 1,077,272.727$

2 1,185,000.00$ 0.826 979,338.843$

3 1,185,000.00$ 0.751 890,308.039$

4 1,985,000.00$ 0.683 1,355,781.709$

NPV 1,702,701.318$

Project NPV when Price per unit decreases by 10%

14

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,960,000.00$ 3,960,000.00$ 3,960,000.00$ 3,960,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,710,000.00$ 4,710,000.00$ 4,710,000.00$ 4,710,000.00$

Cash flows before tax 690,000.00$ 690,000.00$ 690,000.00$ 690,000.00$

Less: Tax @ 30% 207,000.00$ 207,000.00$ 207,000.00$ 207,000.00$

Cash Flows after tax 483,000.00$ 483,000.00$ 483,000.00$ 483,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 933,000.00$ 933,000.00$ 933,000.00$ 933,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 933,000.00$ 933,000.00$ 933,000.00$ 1,733,000.00$

Statement of Cash flows when Variable cost per unit increases 10%

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 933,000.00$ 0.909 848,181.818$

2 933,000.00$ 0.826 771,074.380$

3 933,000.00$ 0.751 700,976.709$

4 1,733,000.00$ 0.683 1,183,662.318$

NPV 903,895.226$

Project NPV when Variable cost per unit increases 10%

15

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,960,000.00$ 3,960,000.00$ 3,960,000.00$ 3,960,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,710,000.00$ 4,710,000.00$ 4,710,000.00$ 4,710,000.00$

Cash flows before tax 690,000.00$ 690,000.00$ 690,000.00$ 690,000.00$

Less: Tax @ 30% 207,000.00$ 207,000.00$ 207,000.00$ 207,000.00$

Cash Flows after tax 483,000.00$ 483,000.00$ 483,000.00$ 483,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 933,000.00$ 933,000.00$ 933,000.00$ 933,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 933,000.00$ 933,000.00$ 933,000.00$ 1,733,000.00$

Statement of Cash flows when Variable cost per unit increases 10%

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 933,000.00$ 0.909 848,181.818$

2 933,000.00$ 0.826 771,074.380$

3 933,000.00$ 0.751 700,976.709$

4 1,733,000.00$ 0.683 1,183,662.318$

NPV 903,895.226$

Project NPV when Variable cost per unit increases 10%

15

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,960,000.00$ 3,960,000.00$ 3,960,000.00$ 3,960,000.00$

Fixed Cost 330,000.00$ 330,000.00$ 330,000.00$ 330,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,740,000.00$ 4,740,000.00$ 4,740,000.00$ 4,740,000.00$

Cash flows before tax 660,000.00$ 660,000.00$ 660,000.00$ 660,000.00$

Less: Tax @ 30% 198,000.00$ 198,000.00$ 198,000.00$ 198,000.00$

Cash Flows after tax 462,000.00$ 462,000.00$ 462,000.00$ 462,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 912,000.00$ 912,000.00$ 912,000.00$ 912,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 912,000.00$ 912,000.00$ 912,000.00$ 1,712,000.00$

Statement of Cash flows when Cash fixed cost per year increases by 10%

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 912,000.00$ 0.909 829,090.909$

2 912,000.00$ 0.826 753,719.008$

3 912,000.00$ 0.751 685,199.098$

4 1,712,000.00$ 0.683 1,169,319.036$

NPV 837,328.051$

Project NPV when Cash fixed cost per year increases by 10%

2.5 Identification and Discussion of Systematic and Un-systematic Risk Impacting the

Performance of Caltex Australia

Unsystematic Risk

The unsystematic risks are regarded as the risks that are inherent within a company due to

nature of its operations or industry sector. It is known as diversifiable risk as it can be reduced

through diversification. The unsystematic risks that are associated with the operational activities

of Caltex Australia are described below:

16

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,960,000.00$ 3,960,000.00$ 3,960,000.00$ 3,960,000.00$

Fixed Cost 330,000.00$ 330,000.00$ 330,000.00$ 330,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,740,000.00$ 4,740,000.00$ 4,740,000.00$ 4,740,000.00$

Cash flows before tax 660,000.00$ 660,000.00$ 660,000.00$ 660,000.00$

Less: Tax @ 30% 198,000.00$ 198,000.00$ 198,000.00$ 198,000.00$

Cash Flows after tax 462,000.00$ 462,000.00$ 462,000.00$ 462,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 912,000.00$ 912,000.00$ 912,000.00$ 912,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 912,000.00$ 912,000.00$ 912,000.00$ 1,712,000.00$

Statement of Cash flows when Cash fixed cost per year increases by 10%

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 912,000.00$ 0.909 829,090.909$

2 912,000.00$ 0.826 753,719.008$

3 912,000.00$ 0.751 685,199.098$

4 1,712,000.00$ 0.683 1,169,319.036$

NPV 837,328.051$

Project NPV when Cash fixed cost per year increases by 10%

2.5 Identification and Discussion of Systematic and Un-systematic Risk Impacting the

Performance of Caltex Australia

Unsystematic Risk

The unsystematic risks are regarded as the risks that are inherent within a company due to

nature of its operations or industry sector. It is known as diversifiable risk as it can be reduced

through diversification. The unsystematic risks that are associated with the operational activities

of Caltex Australia are described below:

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Operational Risk

The business operations of Caltex are associated with the risks of external threat that can

result in disrupting the information technology system of the company. The company operations

are heavily reliant on IT systems and therefore systems error can result in causing a threat to

continuing of its operations. In addition to this, the occurrence of any type of hazard can result in

causing injury or damage to its property result in ceasing of its operations or causing financial

losses. Caltex in this context has implemented the use of an integrated management system for

mitigating the risks related to safety and environmental threats (Caltex Australia: Annual

Reports, 2019).

Competitive Risk

Caltex conducts its operations in a highly competitive environment and therefore its

continued growth can be negatively impacted by new entrants and inability to meet the customer

expectations of quality and price. The company has implemented the use of various strategies for

mitigating the competitive risks such as reducing costs for increasing its profitability margin and

enhancing the operational efficiency to foster its sustainable growth.

Environmental Risks

The environmental risks can occur due to the exposure of the company to spillover and

other such incidents that can occur during transportations of its petroleum products. As such, the

company has implemented the use of rigid operating standards and policies for ensuring

compliance with the environmental laws and regulations to prevent the occurrence of any such

incident (Caltex Australia: Annual Reports, 2019).

Systematic Risks

These are the market risks that can impact the performance of a company due to volatility

within the marketplace. The risks are un-diversifiable and cannot be reduced by a company by

the use of diversification strategy (Zimmerman and Yahya-Zadeh, 2011). The systematic risks

associated with Caltex Australia have been described as follows:

Commodity Price Risk

17

The business operations of Caltex are associated with the risks of external threat that can

result in disrupting the information technology system of the company. The company operations

are heavily reliant on IT systems and therefore systems error can result in causing a threat to

continuing of its operations. In addition to this, the occurrence of any type of hazard can result in

causing injury or damage to its property result in ceasing of its operations or causing financial

losses. Caltex in this context has implemented the use of an integrated management system for

mitigating the risks related to safety and environmental threats (Caltex Australia: Annual

Reports, 2019).

Competitive Risk

Caltex conducts its operations in a highly competitive environment and therefore its

continued growth can be negatively impacted by new entrants and inability to meet the customer

expectations of quality and price. The company has implemented the use of various strategies for

mitigating the competitive risks such as reducing costs for increasing its profitability margin and

enhancing the operational efficiency to foster its sustainable growth.

Environmental Risks

The environmental risks can occur due to the exposure of the company to spillover and

other such incidents that can occur during transportations of its petroleum products. As such, the

company has implemented the use of rigid operating standards and policies for ensuring

compliance with the environmental laws and regulations to prevent the occurrence of any such

incident (Caltex Australia: Annual Reports, 2019).

Systematic Risks

These are the market risks that can impact the performance of a company due to volatility

within the marketplace. The risks are un-diversifiable and cannot be reduced by a company by

the use of diversification strategy (Zimmerman and Yahya-Zadeh, 2011). The systematic risks

associated with Caltex Australia have been described as follows:

Commodity Price Risk

17

The company is highly exposed to the risks of adverse price movement in the sector of

crude oil and finished product which can influence its sales and purchasing financial

transactions. As such, this type of risk can have a direct impact on the cash flows and earning

potential of the company. The company has implemented the use of derivative contracts for

managing its exposure towards commodity price risks.

Foreign Exchange Risk

The company is also highly exposed to the risks associated with the fluctuations in the

foreign exchange rates. The company purchases its crude oil products in USD and sells them at

AUD and therefore the changes within the exchange rate between AUD and USD can have a

direct impact on the earning potential and cash flows of the company. The company seeks to

manage the foreign exchange risk with the use of financial instruments such as forwards, swaps

and options that can be used to manage the foreign currency exposure.

Liquidity Risk

The company is also exposed to high liquidity risk due to its credit sales and use of debt

facilities. It is essential for the company adequately manage its liquidity risk through maintaining

sufficient cash flows by adequate management of its capital structure. The cash flow forecasts

done by the finance managers help in accessing the degree of access to debt and equity markets.

This helps in estimating the position of future cash flows and therefore managing the liquidity

risk.

Credit Risk

The credit risk represents to the loss that could be faced by the company in the condition of

counterparty failing to meet the contractual terms. The primary credit risk is related with the

trade receivables’ of the company. Caltex Board has developed and implemented an adequate

policy for managing and diversification of the credit risk related with Caltex by conducting

financial transactions with large number of customers across variety of industries (Caltex

Australia: Annual Reports, 2019).

18

crude oil and finished product which can influence its sales and purchasing financial

transactions. As such, this type of risk can have a direct impact on the cash flows and earning

potential of the company. The company has implemented the use of derivative contracts for

managing its exposure towards commodity price risks.

Foreign Exchange Risk

The company is also highly exposed to the risks associated with the fluctuations in the

foreign exchange rates. The company purchases its crude oil products in USD and sells them at

AUD and therefore the changes within the exchange rate between AUD and USD can have a

direct impact on the earning potential and cash flows of the company. The company seeks to

manage the foreign exchange risk with the use of financial instruments such as forwards, swaps

and options that can be used to manage the foreign currency exposure.

Liquidity Risk

The company is also exposed to high liquidity risk due to its credit sales and use of debt

facilities. It is essential for the company adequately manage its liquidity risk through maintaining

sufficient cash flows by adequate management of its capital structure. The cash flow forecasts

done by the finance managers help in accessing the degree of access to debt and equity markets.

This helps in estimating the position of future cash flows and therefore managing the liquidity

risk.

Credit Risk

The credit risk represents to the loss that could be faced by the company in the condition of

counterparty failing to meet the contractual terms. The primary credit risk is related with the

trade receivables’ of the company. Caltex Board has developed and implemented an adequate

policy for managing and diversification of the credit risk related with Caltex by conducting

financial transactions with large number of customers across variety of industries (Caltex

Australia: Annual Reports, 2019).

18

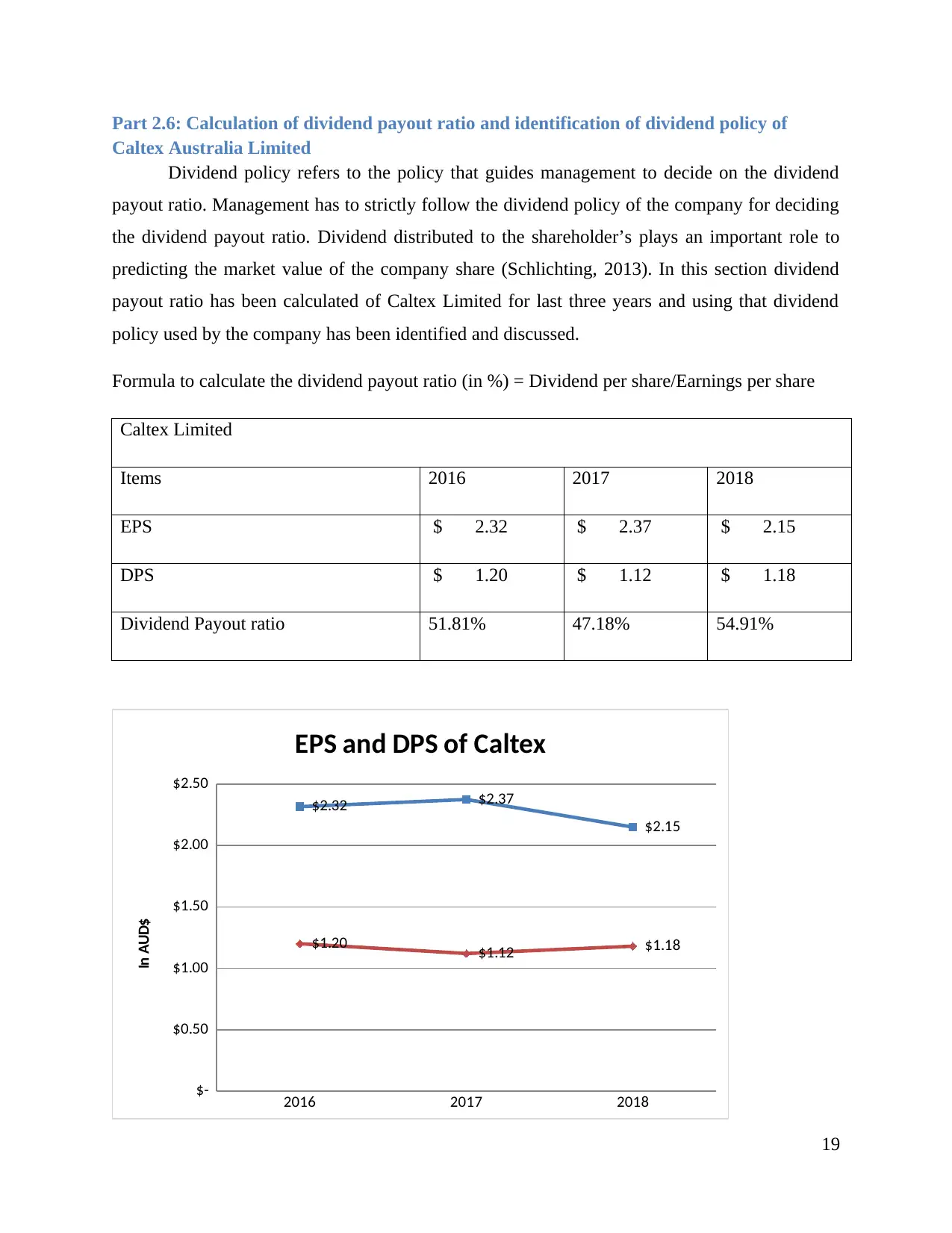

Part 2.6: Calculation of dividend payout ratio and identification of dividend policy of

Caltex Australia Limited

Dividend policy refers to the policy that guides management to decide on the dividend

payout ratio. Management has to strictly follow the dividend policy of the company for deciding

the dividend payout ratio. Dividend distributed to the shareholder’s plays an important role to

predicting the market value of the company share (Schlichting, 2013). In this section dividend

payout ratio has been calculated of Caltex Limited for last three years and using that dividend

policy used by the company has been identified and discussed.

Formula to calculate the dividend payout ratio (in %) = Dividend per share/Earnings per share

Caltex Limited

Items 2016 2017 2018

EPS $ 2.32 $ 2.37 $ 2.15

DPS $ 1.20 $ 1.12 $ 1.18

Dividend Payout ratio 51.81% 47.18% 54.91%

2016 2017 2018

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$2.32 $2.37

$2.15

$1.20 $1.12 $1.18

EPS and DPS of Caltex

In AUD$

19

Caltex Australia Limited

Dividend policy refers to the policy that guides management to decide on the dividend

payout ratio. Management has to strictly follow the dividend policy of the company for deciding

the dividend payout ratio. Dividend distributed to the shareholder’s plays an important role to

predicting the market value of the company share (Schlichting, 2013). In this section dividend

payout ratio has been calculated of Caltex Limited for last three years and using that dividend

policy used by the company has been identified and discussed.

Formula to calculate the dividend payout ratio (in %) = Dividend per share/Earnings per share

Caltex Limited

Items 2016 2017 2018

EPS $ 2.32 $ 2.37 $ 2.15

DPS $ 1.20 $ 1.12 $ 1.18

Dividend Payout ratio 51.81% 47.18% 54.91%

2016 2017 2018

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$2.32 $2.37

$2.15

$1.20 $1.12 $1.18

EPS and DPS of Caltex

In AUD$

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2016 2017 2018

42.00%

44.00%

46.00%

48.00%

50.00%

52.00%

54.00%

56.00%

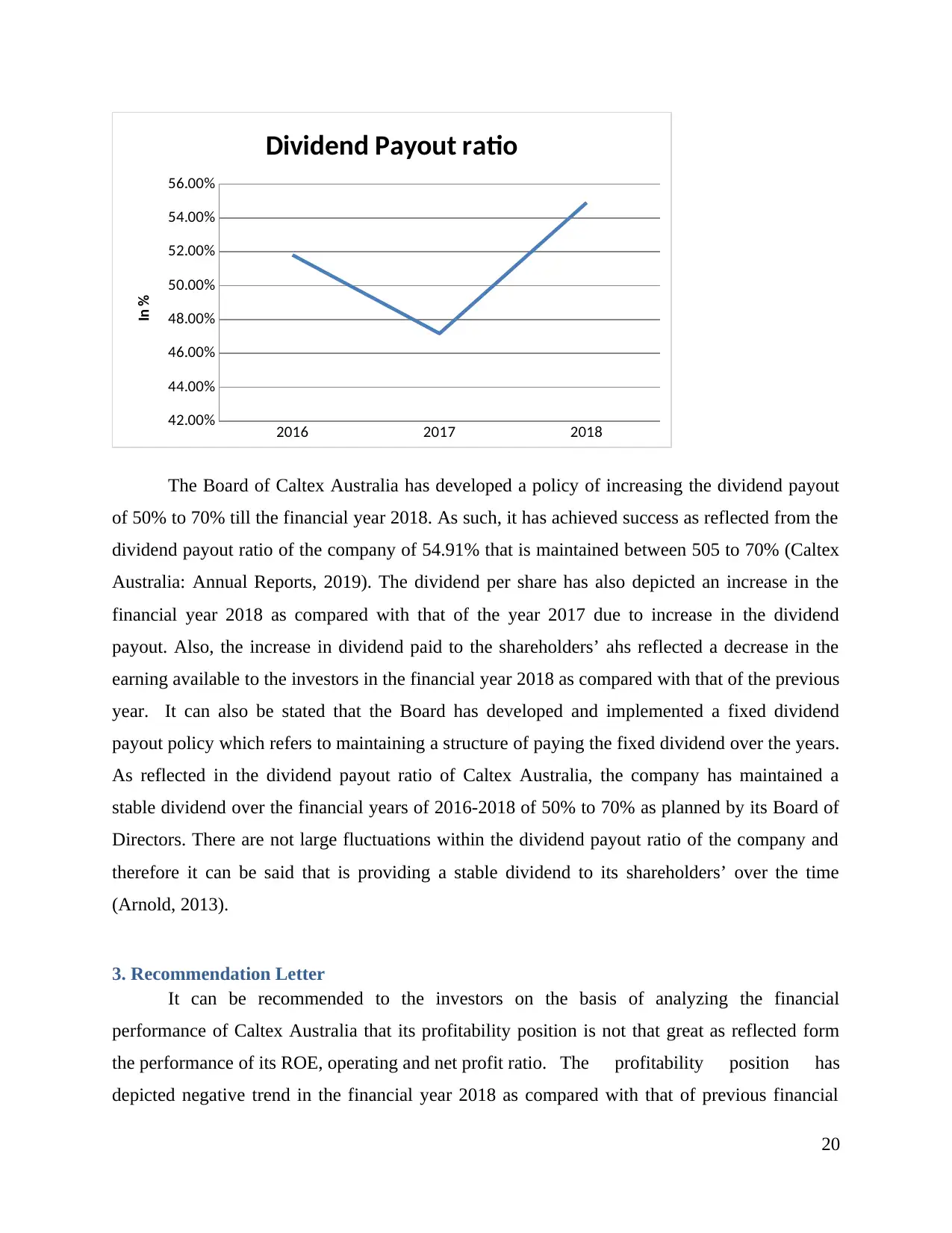

Dividend Payout ratio

In %

The Board of Caltex Australia has developed a policy of increasing the dividend payout

of 50% to 70% till the financial year 2018. As such, it has achieved success as reflected from the

dividend payout ratio of the company of 54.91% that is maintained between 505 to 70% (Caltex

Australia: Annual Reports, 2019). The dividend per share has also depicted an increase in the

financial year 2018 as compared with that of the year 2017 due to increase in the dividend

payout. Also, the increase in dividend paid to the shareholders’ ahs reflected a decrease in the

earning available to the investors in the financial year 2018 as compared with that of the previous

year. It can also be stated that the Board has developed and implemented a fixed dividend

payout policy which refers to maintaining a structure of paying the fixed dividend over the years.

As reflected in the dividend payout ratio of Caltex Australia, the company has maintained a

stable dividend over the financial years of 2016-2018 of 50% to 70% as planned by its Board of

Directors. There are not large fluctuations within the dividend payout ratio of the company and

therefore it can be said that is providing a stable dividend to its shareholders’ over the time

(Arnold, 2013).

3. Recommendation Letter

It can be recommended to the investors on the basis of analyzing the financial

performance of Caltex Australia that its profitability position is not that great as reflected form

the performance of its ROE, operating and net profit ratio. The profitability position has

depicted negative trend in the financial year 2018 as compared with that of previous financial

20

42.00%

44.00%

46.00%

48.00%

50.00%

52.00%

54.00%

56.00%

Dividend Payout ratio

In %

The Board of Caltex Australia has developed a policy of increasing the dividend payout

of 50% to 70% till the financial year 2018. As such, it has achieved success as reflected from the

dividend payout ratio of the company of 54.91% that is maintained between 505 to 70% (Caltex

Australia: Annual Reports, 2019). The dividend per share has also depicted an increase in the

financial year 2018 as compared with that of the year 2017 due to increase in the dividend

payout. Also, the increase in dividend paid to the shareholders’ ahs reflected a decrease in the

earning available to the investors in the financial year 2018 as compared with that of the previous

year. It can also be stated that the Board has developed and implemented a fixed dividend

payout policy which refers to maintaining a structure of paying the fixed dividend over the years.

As reflected in the dividend payout ratio of Caltex Australia, the company has maintained a

stable dividend over the financial years of 2016-2018 of 50% to 70% as planned by its Board of

Directors. There are not large fluctuations within the dividend payout ratio of the company and

therefore it can be said that is providing a stable dividend to its shareholders’ over the time

(Arnold, 2013).

3. Recommendation Letter

It can be recommended to the investors on the basis of analyzing the financial

performance of Caltex Australia that its profitability position is not that great as reflected form

the performance of its ROE, operating and net profit ratio. The profitability position has

depicted negative trend in the financial year 2018 as compared with that of previous financial

20

years of 2016 and 2017. The efficiency of the company has improved in the year 2018 as

compared to the previous years due to its improvement in the efficiency to collect cash from the

debtors and also converting the inventory to sales. However, the company is still improving its

operational efficiency and its profitability position also and therefore there exists some doubt

regarding its future growth prospects of the company (Damodaran, 2011).

The dividend payout ratio has also reflected an increase over the selected time period of

2016-2018 which depicts that it is emphasizing on increasing the dividend provided to the

owners as per its policy of achieving the dividends to come within the range of 50

% to 70%. The increase in divided per share of the company is consequently leading to decline in

the earning per share mainly due to less available earnings to the investors. This also reflects that

the company financial position is not so attractive for the investors to realize larger returns from

the company (Davies and Crawford, 2011). It is taking measures to improve its operational

performance and profitability position but yet a potential investor is recommended to hold back

the shares for some period of time. This is because the analysis of the financial performance of

the company in subsequent years should be undertaken before taking financial decision of

investment (Baker and Powell, 2009).

4. Conclusion

The above report has inferred that the use of ratio analysis and other method such as cash

management, sensitivity analysis and examination of dividend policy and the associated business

risk can help in determining the future growth prospects of a company. The financial

performance evaluated of the company Caltex Australia through the use of above technique has

proved to be largely effective in providing recommendation to an institutional investor regarding

investing within the company. The ratio analysis has examined the profitability and operational

efficiency of the company which depicts that it is profit position and efficiency position need to

be improved in the coming years. Also, it needs to improve its cash management and earnings

per share to provide large returns to the investors and marinating an adequate flow of cash within

the company. The investors are recommended to hold back the shares within the company and

examine it future financial performance before taking any significant investment decision.

21

compared to the previous years due to its improvement in the efficiency to collect cash from the

debtors and also converting the inventory to sales. However, the company is still improving its

operational efficiency and its profitability position also and therefore there exists some doubt

regarding its future growth prospects of the company (Damodaran, 2011).

The dividend payout ratio has also reflected an increase over the selected time period of

2016-2018 which depicts that it is emphasizing on increasing the dividend provided to the

owners as per its policy of achieving the dividends to come within the range of 50

% to 70%. The increase in divided per share of the company is consequently leading to decline in

the earning per share mainly due to less available earnings to the investors. This also reflects that

the company financial position is not so attractive for the investors to realize larger returns from

the company (Davies and Crawford, 2011). It is taking measures to improve its operational

performance and profitability position but yet a potential investor is recommended to hold back

the shares for some period of time. This is because the analysis of the financial performance of

the company in subsequent years should be undertaken before taking financial decision of

investment (Baker and Powell, 2009).

4. Conclusion

The above report has inferred that the use of ratio analysis and other method such as cash

management, sensitivity analysis and examination of dividend policy and the associated business

risk can help in determining the future growth prospects of a company. The financial

performance evaluated of the company Caltex Australia through the use of above technique has

proved to be largely effective in providing recommendation to an institutional investor regarding

investing within the company. The ratio analysis has examined the profitability and operational

efficiency of the company which depicts that it is profit position and efficiency position need to

be improved in the coming years. Also, it needs to improve its cash management and earnings

per share to provide large returns to the investors and marinating an adequate flow of cash within

the company. The investors are recommended to hold back the shares within the company and

examine it future financial performance before taking any significant investment decision.

21

References

Arnold, G. 2013. Corporate financial management. USA: Pearson Higher Ed.

Baker, K. and Powell, G. 2009. Understanding Financial Management: A Practical Guide. USA:

John Wiley & Sons.

Bragg, S. 2010. Business Ratios and Formulas: A Comprehensive Guide. US: John Wiley &

Sons.

Brigham, F., and Michael, C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Caltex Australia. 2019. Annual Reports. [Online]. Available at: https://www.caltex.com.au/our-

company/investor-centre/annual-reports-and-reviews [Accessed on: 29 May 2019].

Caltex Australia. 2019. Our Company. [Online]. Available at: https://www.caltex.com.au/our-

company [Accessed on: 29 May 2019].

Damodaran, A. 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. and Crawford, I. 2011. Business accounting and finance. USA: Pearson.

Feldman, M. and Libman, L. 2011. Crash Course in Accounting and Financial Statement

Analysis. USA: John Wiley & Sons.

Gibson, C. 2011. Financial Reporting and Analysis: Using Financial Accounting Information.

Australia: Cengage Learning.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. And Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Reilly.F.K. and Brown.K.C. 2011. Investment analysis & portfolio management. UK: South

western Cengage learning.

Schlichting, T. 2013. Fundamental Analysis, Behavioral Finance and Technical Analysis on the

Stock Market. Australia: GRIN Verlag.

22

Arnold, G. 2013. Corporate financial management. USA: Pearson Higher Ed.

Baker, K. and Powell, G. 2009. Understanding Financial Management: A Practical Guide. USA:

John Wiley & Sons.

Bragg, S. 2010. Business Ratios and Formulas: A Comprehensive Guide. US: John Wiley &

Sons.

Brigham, F., and Michael, C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Caltex Australia. 2019. Annual Reports. [Online]. Available at: https://www.caltex.com.au/our-

company/investor-centre/annual-reports-and-reviews [Accessed on: 29 May 2019].

Caltex Australia. 2019. Our Company. [Online]. Available at: https://www.caltex.com.au/our-

company [Accessed on: 29 May 2019].

Damodaran, A. 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. and Crawford, I. 2011. Business accounting and finance. USA: Pearson.

Feldman, M. and Libman, L. 2011. Crash Course in Accounting and Financial Statement

Analysis. USA: John Wiley & Sons.

Gibson, C. 2011. Financial Reporting and Analysis: Using Financial Accounting Information.

Australia: Cengage Learning.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. And Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Reilly.F.K. and Brown.K.C. 2011. Investment analysis & portfolio management. UK: South

western Cengage learning.

Schlichting, T. 2013. Fundamental Analysis, Behavioral Finance and Technical Analysis on the

Stock Market. Australia: GRIN Verlag.

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Zimmerman, J.L. and Yahya-Zadeh, M. 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

23

control. Issues in Accounting Education, 26(1), pp.258-259.

23

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.