Financial Analysis of Croc's Diner: Profit and Loss, Ratios

VerifiedAdded on 2022/12/30

|11

|2153

|42

Report

AI Summary

This report presents a comprehensive financial analysis of Croc's Diner, including the preparation of a profit and loss statement and balance sheet for the year ended June 30, 2001. It delves into cost definitions and classifications, differentiating between fixed, variable, and semi-variable costs, as well as marginal and opportunity costs. The report defines ratios and their application as performance management tools, encompassing various ratio classes such as liquidity, activity, leverage, performance, and valuation ratios. A detailed computation of profitability and liquidity ratios is provided, evaluating the business's return on assets, net profit margin, gross profit margin, return on capital employed, return on equity, current ratio, and liquid ratio. Based on the ratio analysis, recommendations for performance improvement are offered, emphasizing the importance of managing business expenses to enhance profitability. The analysis demonstrates the importance of financial planning and management in enhancing the efficiency and productivity of a business.

Finance for Hospitality,

Tourism and Events

Tourism and Events

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Preparation of profit and loss statement of Croc's Diner for the year ended 30th June 2001:....1

Balance sheet of Croc's Diner for the year ended 30th June 2001:.............................................2

Commenting on performance of business with utilisation of ratio analysis:...............................2

TASK 2............................................................................................................................................2

Defining costs:.............................................................................................................................2

Identification and evaluation of different types of costs along with their behaviour:.................3

Defining ratios:............................................................................................................................4

Ratio as a tool of performance management including factors of benchmarking:......................4

Stating five different classes of ratios:.........................................................................................4

Computation of ratios:.................................................................................................................4

Recommendations for performance improvement:.....................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Preparation of profit and loss statement of Croc's Diner for the year ended 30th June 2001:....1

Balance sheet of Croc's Diner for the year ended 30th June 2001:.............................................2

Commenting on performance of business with utilisation of ratio analysis:...............................2

TASK 2............................................................................................................................................2

Defining costs:.............................................................................................................................2

Identification and evaluation of different types of costs along with their behaviour:.................3

Defining ratios:............................................................................................................................4

Ratio as a tool of performance management including factors of benchmarking:......................4

Stating five different classes of ratios:.........................................................................................4

Computation of ratios:.................................................................................................................4

Recommendations for performance improvement:.....................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

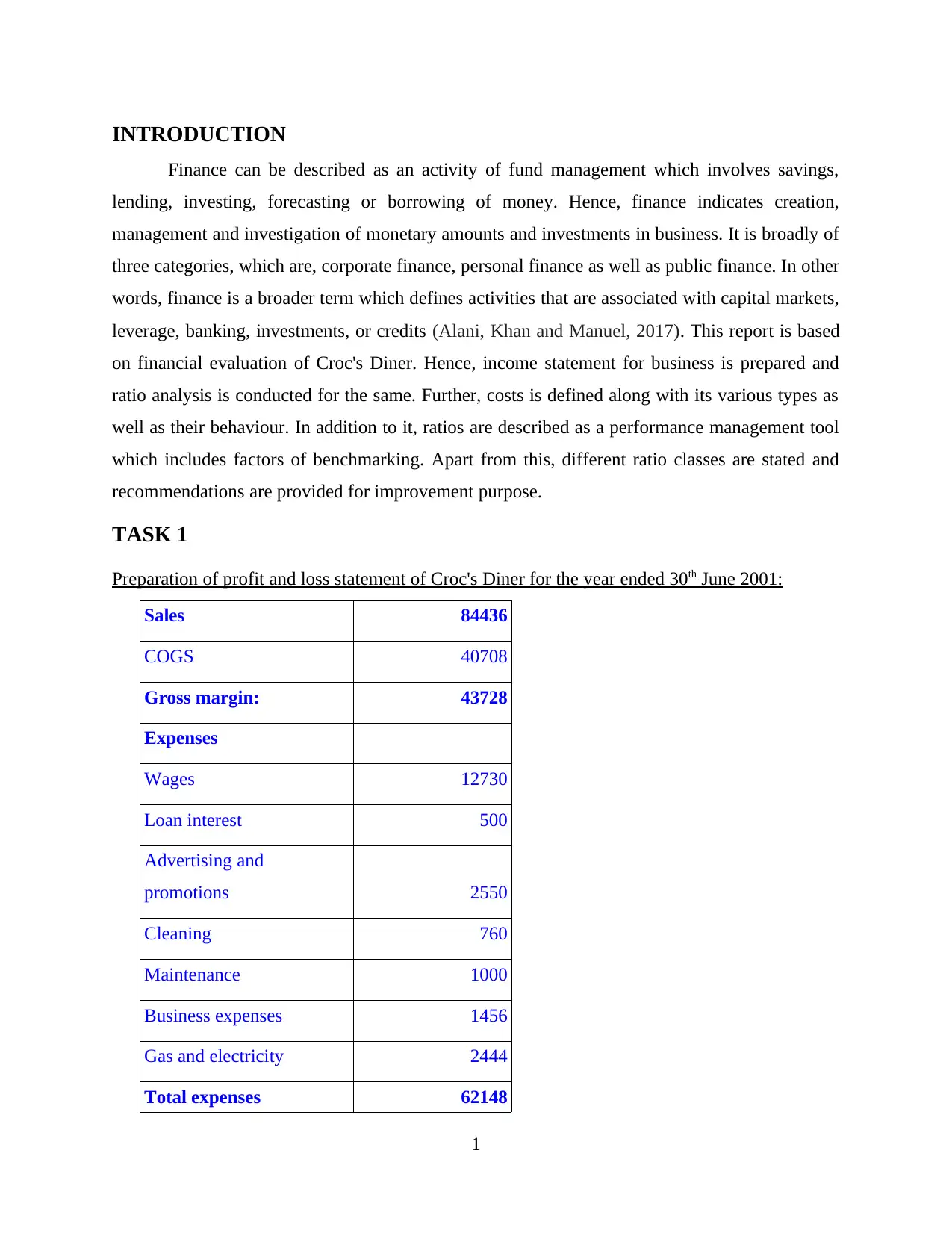

INTRODUCTION

Finance can be described as an activity of fund management which involves savings,

lending, investing, forecasting or borrowing of money. Hence, finance indicates creation,

management and investigation of monetary amounts and investments in business. It is broadly of

three categories, which are, corporate finance, personal finance as well as public finance. In other

words, finance is a broader term which defines activities that are associated with capital markets,

leverage, banking, investments, or credits (Alani, Khan and Manuel, 2017). This report is based

on financial evaluation of Croc's Diner. Hence, income statement for business is prepared and

ratio analysis is conducted for the same. Further, costs is defined along with its various types as

well as their behaviour. In addition to it, ratios are described as a performance management tool

which includes factors of benchmarking. Apart from this, different ratio classes are stated and

recommendations are provided for improvement purpose.

TASK 1

Preparation of profit and loss statement of Croc's Diner for the year ended 30th June 2001:

Sales 84436

COGS 40708

Gross margin: 43728

Expenses

Wages 12730

Loan interest 500

Advertising and

promotions 2550

Cleaning 760

Maintenance 1000

Business expenses 1456

Gas and electricity 2444

Total expenses 62148

1

Finance can be described as an activity of fund management which involves savings,

lending, investing, forecasting or borrowing of money. Hence, finance indicates creation,

management and investigation of monetary amounts and investments in business. It is broadly of

three categories, which are, corporate finance, personal finance as well as public finance. In other

words, finance is a broader term which defines activities that are associated with capital markets,

leverage, banking, investments, or credits (Alani, Khan and Manuel, 2017). This report is based

on financial evaluation of Croc's Diner. Hence, income statement for business is prepared and

ratio analysis is conducted for the same. Further, costs is defined along with its various types as

well as their behaviour. In addition to it, ratios are described as a performance management tool

which includes factors of benchmarking. Apart from this, different ratio classes are stated and

recommendations are provided for improvement purpose.

TASK 1

Preparation of profit and loss statement of Croc's Diner for the year ended 30th June 2001:

Sales 84436

COGS 40708

Gross margin: 43728

Expenses

Wages 12730

Loan interest 500

Advertising and

promotions 2550

Cleaning 760

Maintenance 1000

Business expenses 1456

Gas and electricity 2444

Total expenses 62148

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit before tax 22288

Tax expense 1640

Net profit after tax 20648

Balance sheet of Croc's Diner for the year ended 30th June 2001:

Fixed assets

Furniture and equipments 8800

Lease hold premises 20000

Total fixed assets 28800

Current assets

Inventory 720

Debtors 150

Cash in hand 890

Bank balance 4567

Total current assets 6327

Total assets 35127

Current liability

Creditors 4000

Total current liabilities 4000

Finance by/ Equity

Capital 16979 (less: drawings

11000) 5979

Surplus 20648

2

Tax expense 1640

Net profit after tax 20648

Balance sheet of Croc's Diner for the year ended 30th June 2001:

Fixed assets

Furniture and equipments 8800

Lease hold premises 20000

Total fixed assets 28800

Current assets

Inventory 720

Debtors 150

Cash in hand 890

Bank balance 4567

Total current assets 6327

Total assets 35127

Current liability

Creditors 4000

Total current liabilities 4000

Finance by/ Equity

Capital 16979 (less: drawings

11000) 5979

Surplus 20648

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

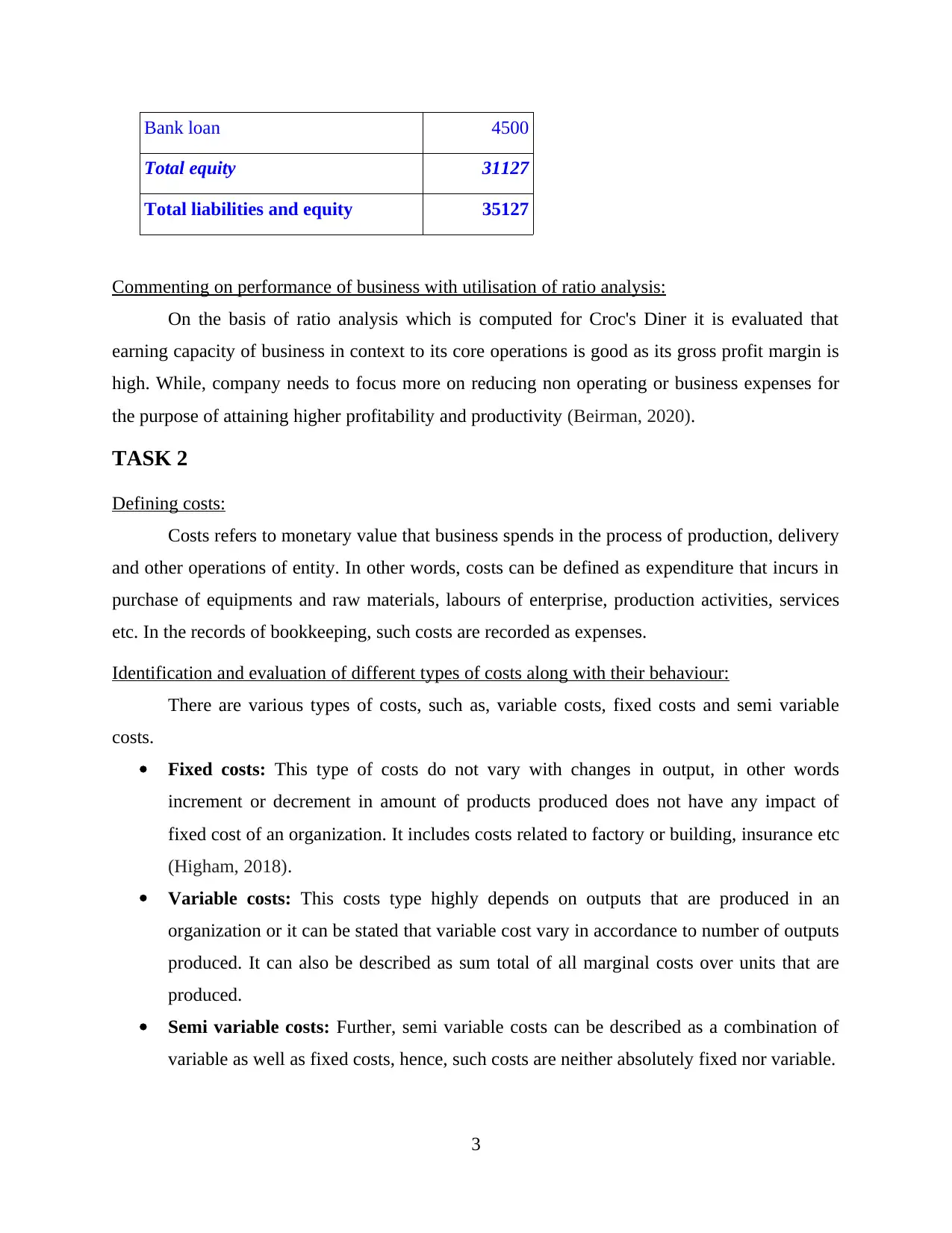

Bank loan 4500

Total equity 31127

Total liabilities and equity 35127

Commenting on performance of business with utilisation of ratio analysis:

On the basis of ratio analysis which is computed for Croc's Diner it is evaluated that

earning capacity of business in context to its core operations is good as its gross profit margin is

high. While, company needs to focus more on reducing non operating or business expenses for

the purpose of attaining higher profitability and productivity (Beirman, 2020).

TASK 2

Defining costs:

Costs refers to monetary value that business spends in the process of production, delivery

and other operations of entity. In other words, costs can be defined as expenditure that incurs in

purchase of equipments and raw materials, labours of enterprise, production activities, services

etc. In the records of bookkeeping, such costs are recorded as expenses.

Identification and evaluation of different types of costs along with their behaviour:

There are various types of costs, such as, variable costs, fixed costs and semi variable

costs.

Fixed costs: This type of costs do not vary with changes in output, in other words

increment or decrement in amount of products produced does not have any impact of

fixed cost of an organization. It includes costs related to factory or building, insurance etc

(Higham, 2018).

Variable costs: This costs type highly depends on outputs that are produced in an

organization or it can be stated that variable cost vary in accordance to number of outputs

produced. It can also be described as sum total of all marginal costs over units that are

produced.

Semi variable costs: Further, semi variable costs can be described as a combination of

variable as well as fixed costs, hence, such costs are neither absolutely fixed nor variable.

3

Total equity 31127

Total liabilities and equity 35127

Commenting on performance of business with utilisation of ratio analysis:

On the basis of ratio analysis which is computed for Croc's Diner it is evaluated that

earning capacity of business in context to its core operations is good as its gross profit margin is

high. While, company needs to focus more on reducing non operating or business expenses for

the purpose of attaining higher profitability and productivity (Beirman, 2020).

TASK 2

Defining costs:

Costs refers to monetary value that business spends in the process of production, delivery

and other operations of entity. In other words, costs can be defined as expenditure that incurs in

purchase of equipments and raw materials, labours of enterprise, production activities, services

etc. In the records of bookkeeping, such costs are recorded as expenses.

Identification and evaluation of different types of costs along with their behaviour:

There are various types of costs, such as, variable costs, fixed costs and semi variable

costs.

Fixed costs: This type of costs do not vary with changes in output, in other words

increment or decrement in amount of products produced does not have any impact of

fixed cost of an organization. It includes costs related to factory or building, insurance etc

(Higham, 2018).

Variable costs: This costs type highly depends on outputs that are produced in an

organization or it can be stated that variable cost vary in accordance to number of outputs

produced. It can also be described as sum total of all marginal costs over units that are

produced.

Semi variable costs: Further, semi variable costs can be described as a combination of

variable as well as fixed costs, hence, such costs are neither absolutely fixed nor variable.

3

Marginal costs: This type of costs can be explained as expenditure incurred in

production of one additional unit of output. Hence, marginal costs indicates change or

variations in total costs of business which arises when quantity or unit that is produced in

increased by an additional unit. Therefore, it states expenditure that is incorporated in an

enterprise in order to produce next unit.

Opportunity costs Such type of costs refers to cost of next best alternative. Hence,

opportunity costs indicates potential benefit of business which is missed out in order of

choosing an alternative over other. It is not represented in financial reports of business.

Explicit costs: It refers to costs which is directly paid by firm. Hence, explicit costs can

be described as quantifiable or identifiable operating expenses of an organization. For

example, payment of wages (Menicucci, 2018).

Implicit costs: It indicates that costs which represents opportunity costs of business. It is

also called as implied or imputed costs. It defines expenses of resources which is owned

by an organization that can be utilised for some another purpose.

Defining ratios:

Ratio can be defined as a quantitative technique of analysing performance of company.

Reason is that ratio analysis provides clear insight to management of an organization about

operational efficiency, liquidity position as well as profitability status of business. Ratio analysis

helps is analysing financial status of company by interpreting its information related to finance

(Sainaghi, Phillips and Zavarrone, 2017).

Ratio as a tool of performance management including factors of benchmarking:

Ratio analysis is a reliable tool which enables managers to analyse financial information

of an enterprise. Application of technique of ratio analysis helps managers in evaluating

performance of business on the basis of internal benchmarks or goals. This performance

management tool enables interpretation of actual financial status of entity as well as ensures

identification of weak points or loop holes, by eliminating it organization can gain higher

sustainability or success.

Stating five different classes of ratios:

Ratios are of different classes which are described below:

4

production of one additional unit of output. Hence, marginal costs indicates change or

variations in total costs of business which arises when quantity or unit that is produced in

increased by an additional unit. Therefore, it states expenditure that is incorporated in an

enterprise in order to produce next unit.

Opportunity costs Such type of costs refers to cost of next best alternative. Hence,

opportunity costs indicates potential benefit of business which is missed out in order of

choosing an alternative over other. It is not represented in financial reports of business.

Explicit costs: It refers to costs which is directly paid by firm. Hence, explicit costs can

be described as quantifiable or identifiable operating expenses of an organization. For

example, payment of wages (Menicucci, 2018).

Implicit costs: It indicates that costs which represents opportunity costs of business. It is

also called as implied or imputed costs. It defines expenses of resources which is owned

by an organization that can be utilised for some another purpose.

Defining ratios:

Ratio can be defined as a quantitative technique of analysing performance of company.

Reason is that ratio analysis provides clear insight to management of an organization about

operational efficiency, liquidity position as well as profitability status of business. Ratio analysis

helps is analysing financial status of company by interpreting its information related to finance

(Sainaghi, Phillips and Zavarrone, 2017).

Ratio as a tool of performance management including factors of benchmarking:

Ratio analysis is a reliable tool which enables managers to analyse financial information

of an enterprise. Application of technique of ratio analysis helps managers in evaluating

performance of business on the basis of internal benchmarks or goals. This performance

management tool enables interpretation of actual financial status of entity as well as ensures

identification of weak points or loop holes, by eliminating it organization can gain higher

sustainability or success.

Stating five different classes of ratios:

Ratios are of different classes which are described below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Liquidity ratios: It is a demonstration of ability of business for paying debts or other

short term obligations. It involves computation of current ratio, quick ratio, cash ratio etc.

Activity ratios: Computation of activity class of ratio describes efficiency of business

operations. It indicates utilisation of company's assets for the purpose of generating sales

in involves inventory turnover, receivables or payables turnover etc.

Leverage ratios: Solvency or leverage class of ratio is an analysis of paying capacity of

an organization in context to its long term debt (Navarro-Galera and et.al., 2016).

Performance ratios: Analysis of performance ratios enables computation of profit

generating capacity of an enterprise.

Valuation ratios: This class of ratio analysis provides outline about share price of

company. In other words, valuation ratio represent relationship among market value and

book value of an organization.

Computation of ratios:

Profitability ratios:

Return on total assets: It measures ability of company in generating profit from its total

assets.

Formula= Net profit before interest/ total assets *100

Particulars Amount

Net profit before interest 22788

Total assets 35127

Result 0.65

On the basis of above ratio it can be interpreted that return on total assets of business is

0.65 which states that organization is adequately efficient in generating revenue from its total

assets.

Working note:

Net profit before interest = Net profit before tax + interest

= 22288+500 = 22788

Net profit margin: It is a computation of net profit generated by an organization in

relevance to net sales.

Formula= Net profit before interest/sales*100

5

short term obligations. It involves computation of current ratio, quick ratio, cash ratio etc.

Activity ratios: Computation of activity class of ratio describes efficiency of business

operations. It indicates utilisation of company's assets for the purpose of generating sales

in involves inventory turnover, receivables or payables turnover etc.

Leverage ratios: Solvency or leverage class of ratio is an analysis of paying capacity of

an organization in context to its long term debt (Navarro-Galera and et.al., 2016).

Performance ratios: Analysis of performance ratios enables computation of profit

generating capacity of an enterprise.

Valuation ratios: This class of ratio analysis provides outline about share price of

company. In other words, valuation ratio represent relationship among market value and

book value of an organization.

Computation of ratios:

Profitability ratios:

Return on total assets: It measures ability of company in generating profit from its total

assets.

Formula= Net profit before interest/ total assets *100

Particulars Amount

Net profit before interest 22788

Total assets 35127

Result 0.65

On the basis of above ratio it can be interpreted that return on total assets of business is

0.65 which states that organization is adequately efficient in generating revenue from its total

assets.

Working note:

Net profit before interest = Net profit before tax + interest

= 22288+500 = 22788

Net profit margin: It is a computation of net profit generated by an organization in

relevance to net sales.

Formula= Net profit before interest/sales*100

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

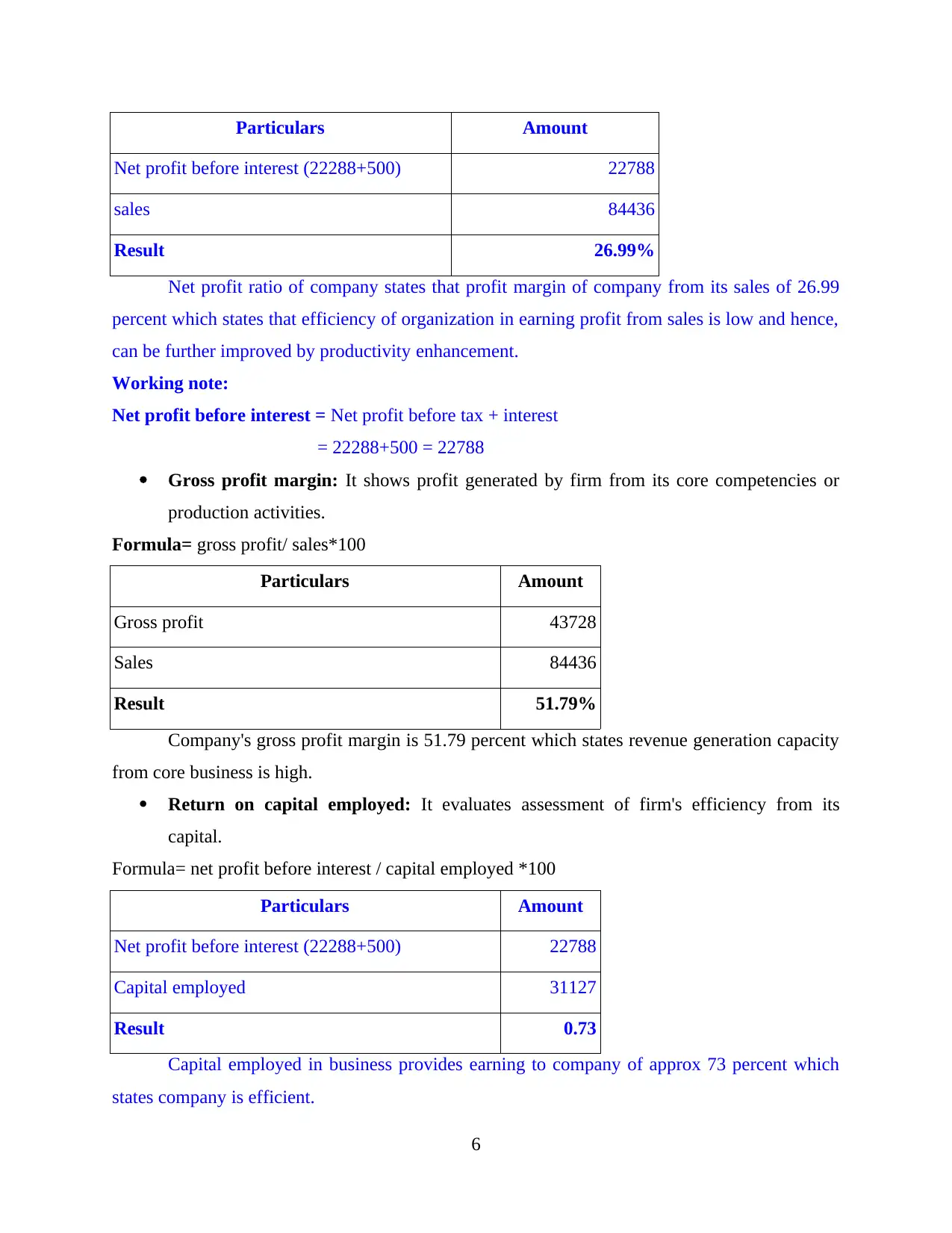

Particulars Amount

Net profit before interest (22288+500) 22788

sales 84436

Result 26.99%

Net profit ratio of company states that profit margin of company from its sales of 26.99

percent which states that efficiency of organization in earning profit from sales is low and hence,

can be further improved by productivity enhancement.

Working note:

Net profit before interest = Net profit before tax + interest

= 22288+500 = 22788

Gross profit margin: It shows profit generated by firm from its core competencies or

production activities.

Formula= gross profit/ sales*100

Particulars Amount

Gross profit 43728

Sales 84436

Result 51.79%

Company's gross profit margin is 51.79 percent which states revenue generation capacity

from core business is high.

Return on capital employed: It evaluates assessment of firm's efficiency from its

capital.

Formula= net profit before interest / capital employed *100

Particulars Amount

Net profit before interest (22288+500) 22788

Capital employed 31127

Result 0.73

Capital employed in business provides earning to company of approx 73 percent which

states company is efficient.

6

Net profit before interest (22288+500) 22788

sales 84436

Result 26.99%

Net profit ratio of company states that profit margin of company from its sales of 26.99

percent which states that efficiency of organization in earning profit from sales is low and hence,

can be further improved by productivity enhancement.

Working note:

Net profit before interest = Net profit before tax + interest

= 22288+500 = 22788

Gross profit margin: It shows profit generated by firm from its core competencies or

production activities.

Formula= gross profit/ sales*100

Particulars Amount

Gross profit 43728

Sales 84436

Result 51.79%

Company's gross profit margin is 51.79 percent which states revenue generation capacity

from core business is high.

Return on capital employed: It evaluates assessment of firm's efficiency from its

capital.

Formula= net profit before interest / capital employed *100

Particulars Amount

Net profit before interest (22288+500) 22788

Capital employed 31127

Result 0.73

Capital employed in business provides earning to company of approx 73 percent which

states company is efficient.

6

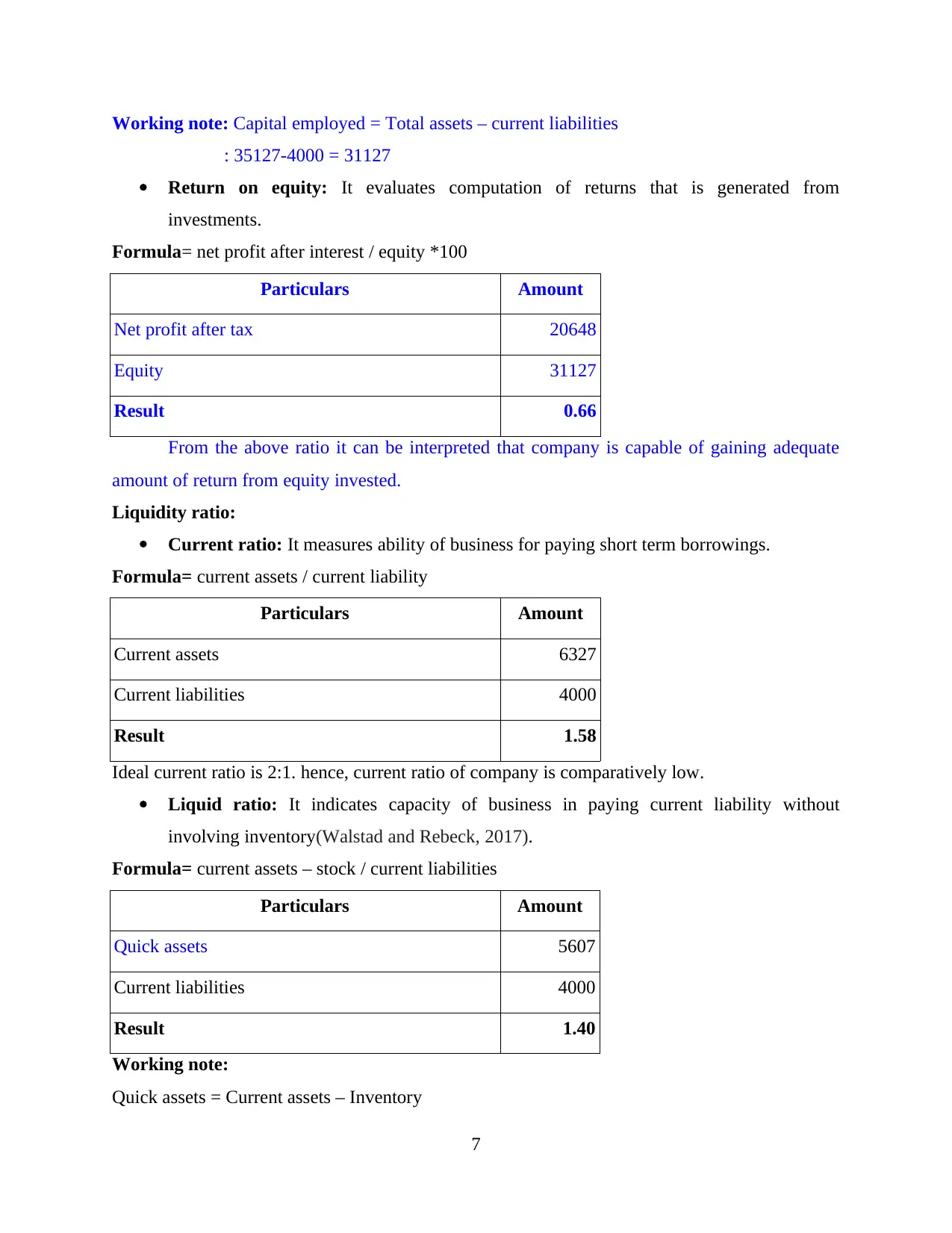

Working note: Capital employed = Total assets – current liabilities

: 35127-4000 = 31127

Return on equity: It evaluates computation of returns that is generated from

investments.

Formula= net profit after interest / equity *100

Particulars Amount

Net profit after tax 20648

Equity 31127

Result 0.66

From the above ratio it can be interpreted that company is capable of gaining adequate

amount of return from equity invested.

Liquidity ratio:

Current ratio: It measures ability of business for paying short term borrowings.

Formula= current assets / current liability

Particulars Amount

Current assets 6327

Current liabilities 4000

Result 1.58

Ideal current ratio is 2:1. hence, current ratio of company is comparatively low.

Liquid ratio: It indicates capacity of business in paying current liability without

involving inventory(Walstad and Rebeck, 2017).

Formula= current assets – stock / current liabilities

Particulars Amount

Quick assets 5607

Current liabilities 4000

Result 1.40

Working note:

Quick assets = Current assets – Inventory

7

: 35127-4000 = 31127

Return on equity: It evaluates computation of returns that is generated from

investments.

Formula= net profit after interest / equity *100

Particulars Amount

Net profit after tax 20648

Equity 31127

Result 0.66

From the above ratio it can be interpreted that company is capable of gaining adequate

amount of return from equity invested.

Liquidity ratio:

Current ratio: It measures ability of business for paying short term borrowings.

Formula= current assets / current liability

Particulars Amount

Current assets 6327

Current liabilities 4000

Result 1.58

Ideal current ratio is 2:1. hence, current ratio of company is comparatively low.

Liquid ratio: It indicates capacity of business in paying current liability without

involving inventory(Walstad and Rebeck, 2017).

Formula= current assets – stock / current liabilities

Particulars Amount

Quick assets 5607

Current liabilities 4000

Result 1.40

Working note:

Quick assets = Current assets – Inventory

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 6327-720 = 5607

From the above liquid or quick ratio it is estimated that liquidity position of an

organization is less.

Recommendations for performance improvement:

From the above ratio analysis it is estimated that company is required to focus on in profit

earning. Hence, business expenses should be lowered so that profitability can be improved.

CONCLUSION

Above report concludes that It helps of management team of an organization to

adequately plan and manage financials for the purpose of gaining higher efficiency and

productivity. Ratio analysis can be described as a useful tool of management which enhances

understanding of financial results and hence serves as a key indicator for performance of an

organization.

8

From the above liquid or quick ratio it is estimated that liquidity position of an

organization is less.

Recommendations for performance improvement:

From the above ratio analysis it is estimated that company is required to focus on in profit

earning. Hence, business expenses should be lowered so that profitability can be improved.

CONCLUSION

Above report concludes that It helps of management team of an organization to

adequately plan and manage financials for the purpose of gaining higher efficiency and

productivity. Ratio analysis can be described as a useful tool of management which enhances

understanding of financial results and hence serves as a key indicator for performance of an

organization.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Alani, F., Khan, F. R. and Manuel, D., 2017. Need for Professionalism and Quality Service of

the Tourist Guides in Oman. International Journal of Tourism & Hospitality Reviews.

4(1). pp. 20-29.

Beirman, D., 2020. Restoring tourism destinations in crisis: A strategic marketing approach.

Routledge.

Higham, J., 2018. Sport tourism development. Channel view publications.

Menicucci, E., 2018. The influence of firm characteristics on profitability. International Journal

of Contemporary Hospitality Management.

Navarro-Galera, A., and et.al., 2016. Measuring the financial sustainability and its influential

factors in local governments. Applied Economics. 48(41). pp. 3961-3975.

Sainaghi, R., Phillips, P. and Zavarrone, E., 2017. Performance measurement in tourism firms: A

content analytical meta-approach. Tourism Management. 59. pp. 36-56.

Walstad, W. B. and Rebeck, K., 2017. The test of financial literacy: Development and

measurement characteristics. The Journal of Economic Education. 48(2). pp. 113-122.

9

Books and Journals:

Alani, F., Khan, F. R. and Manuel, D., 2017. Need for Professionalism and Quality Service of

the Tourist Guides in Oman. International Journal of Tourism & Hospitality Reviews.

4(1). pp. 20-29.

Beirman, D., 2020. Restoring tourism destinations in crisis: A strategic marketing approach.

Routledge.

Higham, J., 2018. Sport tourism development. Channel view publications.

Menicucci, E., 2018. The influence of firm characteristics on profitability. International Journal

of Contemporary Hospitality Management.

Navarro-Galera, A., and et.al., 2016. Measuring the financial sustainability and its influential

factors in local governments. Applied Economics. 48(41). pp. 3961-3975.

Sainaghi, R., Phillips, P. and Zavarrone, E., 2017. Performance measurement in tourism firms: A

content analytical meta-approach. Tourism Management. 59. pp. 36-56.

Walstad, W. B. and Rebeck, K., 2017. The test of financial literacy: Development and

measurement characteristics. The Journal of Economic Education. 48(2). pp. 113-122.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.