Finance for Managers: Financial Ratio Analysis of Two Companies

VerifiedAdded on 2021/02/19

|14

|4260

|252

Report

AI Summary

This report provides a comparative financial analysis of ASOS Plc and Boohoo Group Plc, focusing on key financial ratios to assess their performance and financial health. The analysis includes calculations and interpretations of current ratio, acid test ratio, debtor days, creditor days, operating profit margin, net profit margin, return on assets, and return on capital employed for both companies. The report highlights the importance of these ratios for investment decisions, discussing the strengths and weaknesses of each company based on their financial metrics. It also addresses the limitations of financial ratio analysis, such as the impact of different accounting methods and external factors. The report concludes with recommendations for investors, emphasizing the need for a comprehensive understanding of financial ratios in the context of the companies' specific industries and market conditions.

Finance for Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Content

INTRODUCTION......................................................................................................................................3

MAIN BODY.............................................................................................................................................3

PART A.......................................................................................................................................................3

Financial Ratios and key areas to be considered from the point of view of investment............................3

PART B.....................................................................................................................................................11

Appropriateness of pricing method for achieving strategic financial objectives................................11

CONCLUSION........................................................................................................................................12

RECOMMENDATIONS..........................................................................................................................12

REFERENCES.........................................................................................................................................14

INTRODUCTION......................................................................................................................................3

MAIN BODY.............................................................................................................................................3

PART A.......................................................................................................................................................3

Financial Ratios and key areas to be considered from the point of view of investment............................3

PART B.....................................................................................................................................................11

Appropriateness of pricing method for achieving strategic financial objectives................................11

CONCLUSION........................................................................................................................................12

RECOMMENDATIONS..........................................................................................................................12

REFERENCES.........................................................................................................................................14

INTRODUCTION

Financial report is a concise summary of business operations and accounting transaction which has

taken place for a specific accounting period. Financial statements prepared by every company plays a

crucial role for every investor as well as stakeholders in their decision making process. The report is

based on ASOS Plc which is a British online fashion and cosmetic retailer. This company is engaged in

clothing business and provides facility of online shopping. Also, report will discuss about Boohoo

Group Plc, providing services related to fashion and clothing retail business. The report will provide

comparative analysis with the help of financial ratios and their interpretation between two companies

named ASOS Plc and Boohoo Group Plc.

MAIN BODY

PART A

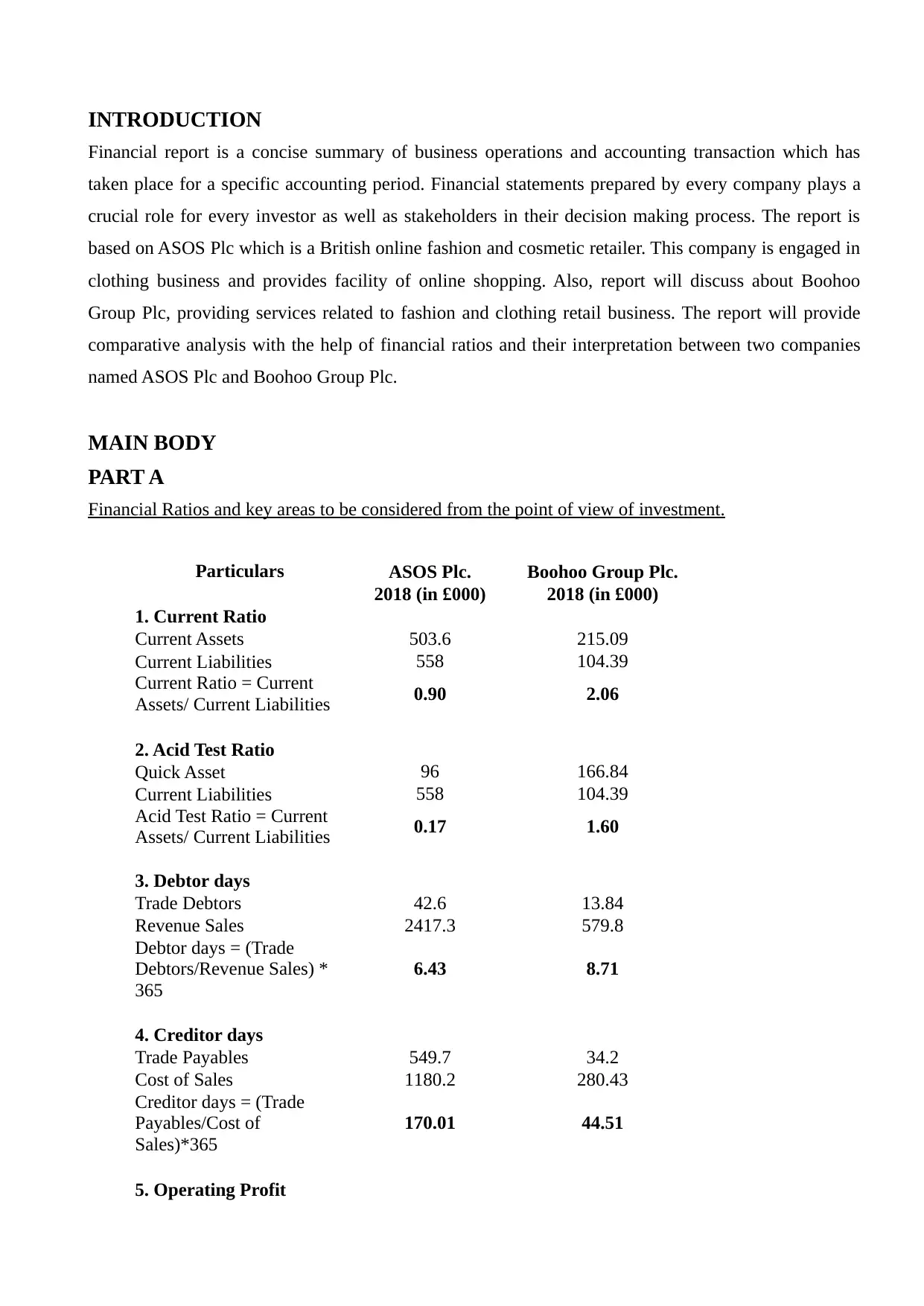

Financial Ratios and key areas to be considered from the point of view of investment.

Particulars ASOS Plc. Boohoo Group Plc.

2018 (in £000) 2018 (in £000)

1. Current Ratio

Current Assets 503.6 215.09

Current Liabilities 558 104.39

Current Ratio = Current

Assets/ Current Liabilities 0.90 2.06

2. Acid Test Ratio

Quick Asset 96 166.84

Current Liabilities 558 104.39

Acid Test Ratio = Current

Assets/ Current Liabilities 0.17 1.60

3. Debtor days

Trade Debtors 42.6 13.84

Revenue Sales 2417.3 579.8

Debtor days = (Trade

Debtors/Revenue Sales) *

365

6.43 8.71

4. Creditor days

Trade Payables 549.7 34.2

Cost of Sales 1180.2 280.43

Creditor days = (Trade

Payables/Cost of

Sales)*365

170.01 44.51

5. Operating Profit

Financial report is a concise summary of business operations and accounting transaction which has

taken place for a specific accounting period. Financial statements prepared by every company plays a

crucial role for every investor as well as stakeholders in their decision making process. The report is

based on ASOS Plc which is a British online fashion and cosmetic retailer. This company is engaged in

clothing business and provides facility of online shopping. Also, report will discuss about Boohoo

Group Plc, providing services related to fashion and clothing retail business. The report will provide

comparative analysis with the help of financial ratios and their interpretation between two companies

named ASOS Plc and Boohoo Group Plc.

MAIN BODY

PART A

Financial Ratios and key areas to be considered from the point of view of investment.

Particulars ASOS Plc. Boohoo Group Plc.

2018 (in £000) 2018 (in £000)

1. Current Ratio

Current Assets 503.6 215.09

Current Liabilities 558 104.39

Current Ratio = Current

Assets/ Current Liabilities 0.90 2.06

2. Acid Test Ratio

Quick Asset 96 166.84

Current Liabilities 558 104.39

Acid Test Ratio = Current

Assets/ Current Liabilities 0.17 1.60

3. Debtor days

Trade Debtors 42.6 13.84

Revenue Sales 2417.3 579.8

Debtor days = (Trade

Debtors/Revenue Sales) *

365

6.43 8.71

4. Creditor days

Trade Payables 549.7 34.2

Cost of Sales 1180.2 280.43

Creditor days = (Trade

Payables/Cost of

Sales)*365

170.01 44.51

5. Operating Profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Margin

Operating Profit 101.9 43

Total Revenue 2417.3 579.8

Operating Profit Margin =

(Operating Profit /Total

Revenue)*100

4.22 7.42

6. Net Profit Margin

Net Profit 82.4 32

Net sales 2417.3 579.8

Net Profit Margin = (Net

Profit/ Net sales)*100 3.41 5.52

7. Return on Assets

Net Income 82.4 32

Total Assets 1007 326.89

Return on Assets = Net

Income/ Total Assets 0.08 0.10

8. Return on Capital

Employed

Net Operating Profit 82.4 32

Total Assets 1007 326.89

Current Liabilities 558 104.39

Total Assets – Current

Liabilities 449 222.5

Return on Capital

Employed = Net Operating

Profit/ (Total Assets –

Current Liabilities)

0.18 0.14

(Source: ASOS ANNUAL Report, 2018)

Financial ratio provides a deep insight about the financial position as well as performance level

of the company in relation with financial perspective. For making investment in any company or

business firm, investor should make proper analysis of company's financial position as well as its

liquidity position. Before making any decision related to investing of money or funds, investor should

make correct interpretation of the available financials and thus proceed further. The above table has

provided a comparison along with interpretation on the basis of financial ratio of two companies named

ASOS Plc. And Boohoo Group Plc.

1. Current Ratio – This financial ratio defines the liquidity position of the company. With the

help of this ratio, it can be ascertained that whether the company has made use of its available

business assets as well as resources of short term nature effectively for meeting its business

obligation. ASOS Plc. Is having a current ratio of 0.90 which is a matter of concern for the

Operating Profit 101.9 43

Total Revenue 2417.3 579.8

Operating Profit Margin =

(Operating Profit /Total

Revenue)*100

4.22 7.42

6. Net Profit Margin

Net Profit 82.4 32

Net sales 2417.3 579.8

Net Profit Margin = (Net

Profit/ Net sales)*100 3.41 5.52

7. Return on Assets

Net Income 82.4 32

Total Assets 1007 326.89

Return on Assets = Net

Income/ Total Assets 0.08 0.10

8. Return on Capital

Employed

Net Operating Profit 82.4 32

Total Assets 1007 326.89

Current Liabilities 558 104.39

Total Assets – Current

Liabilities 449 222.5

Return on Capital

Employed = Net Operating

Profit/ (Total Assets –

Current Liabilities)

0.18 0.14

(Source: ASOS ANNUAL Report, 2018)

Financial ratio provides a deep insight about the financial position as well as performance level

of the company in relation with financial perspective. For making investment in any company or

business firm, investor should make proper analysis of company's financial position as well as its

liquidity position. Before making any decision related to investing of money or funds, investor should

make correct interpretation of the available financials and thus proceed further. The above table has

provided a comparison along with interpretation on the basis of financial ratio of two companies named

ASOS Plc. And Boohoo Group Plc.

1. Current Ratio – This financial ratio defines the liquidity position of the company. With the

help of this ratio, it can be ascertained that whether the company has made use of its available

business assets as well as resources of short term nature effectively for meeting its business

obligation. ASOS Plc. Is having a current ratio of 0.90 which is a matter of concern for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company as it is not able to meet its upcoming business obligation in near future. On the other

hand, Boohoo Group is having 2.06 as current ratio which means that company's business

operations on day to day basis will not get affected by any problem in working capital cycle.

2. Acid Test Ratio – This ratio is also known as Quick ratio which depicts about the strength as

well as liquidity position of the company on the basis of financial aspect. 0.17 & 1.60 is the

value of ratio determined for ASOS Plc and Boohoo Group Plc. For calculating this ratio,

inventories of the company are not included in the calculation of the current asset value

(Berková, Adamová and Nývltová, 2017). This ratio helps in assessing how liquid and solvent

the company is in meeting its business obligations.

3. Debtor days – With the help of this financial ratio, the company can evaluate the average time

period in which the company is able to collect its debt amount due from customers. This ratio

defines how easily and fast the company is able to get back its money against the credit sales

made to its customer. For ASOS Plc, in an average 6.43 or 6 days company will receive its due

payment & a period of 8.71 or 9 days will take in which Boohoo will be able to collects its

receivable. The company should always focus on reducing the debtor period for carrying on its

business operations.

4. Creditor days – This period provides details about the average time period in which the

company will pay off all its debt obligations which are due to all its creditors as well as

suppliers. Also, known as accounts payable period, company should always focus on increasing

its creditors period as it will help the company in remaining liquid and ensures proper

availability of cash. ASOS Plc is having 170.01 creditor period which is considered good on

part of liquidity as well as solvency terms whereas Boohoo Group is 44.51 as its creditors

period which states that company can have to face liquidity or shortage of cash in near future

for carrying on its business operations.

5. Operating Profit Margin – This ratio helps in assessing the operational efficiency as well as

effectiveness of the business. It determines the amount of profit which is left after meeting all

the business expenses and variable cost expenses in form of wages, raw material etc. The

operating profit margin for ASOS Plc is 4.22 and for Boohoo it is 7.42. For investor it is better

to take a view over the behaviour of operating profit ratio of the company. It is having

increasing trend than it is considered as a better option to invest in.

6. Net Profit Margin – It is the amount of profit or a part of revenue which is left after deducting

all the business expenses from the sales made by the business for a specific period of time. 3.41

& 5.52 is the amount of net profit which both the company has made after meeting all its

expenses.

7. Return on Assets – This term of financial ratio define how effectively the company is using its

hand, Boohoo Group is having 2.06 as current ratio which means that company's business

operations on day to day basis will not get affected by any problem in working capital cycle.

2. Acid Test Ratio – This ratio is also known as Quick ratio which depicts about the strength as

well as liquidity position of the company on the basis of financial aspect. 0.17 & 1.60 is the

value of ratio determined for ASOS Plc and Boohoo Group Plc. For calculating this ratio,

inventories of the company are not included in the calculation of the current asset value

(Berková, Adamová and Nývltová, 2017). This ratio helps in assessing how liquid and solvent

the company is in meeting its business obligations.

3. Debtor days – With the help of this financial ratio, the company can evaluate the average time

period in which the company is able to collect its debt amount due from customers. This ratio

defines how easily and fast the company is able to get back its money against the credit sales

made to its customer. For ASOS Plc, in an average 6.43 or 6 days company will receive its due

payment & a period of 8.71 or 9 days will take in which Boohoo will be able to collects its

receivable. The company should always focus on reducing the debtor period for carrying on its

business operations.

4. Creditor days – This period provides details about the average time period in which the

company will pay off all its debt obligations which are due to all its creditors as well as

suppliers. Also, known as accounts payable period, company should always focus on increasing

its creditors period as it will help the company in remaining liquid and ensures proper

availability of cash. ASOS Plc is having 170.01 creditor period which is considered good on

part of liquidity as well as solvency terms whereas Boohoo Group is 44.51 as its creditors

period which states that company can have to face liquidity or shortage of cash in near future

for carrying on its business operations.

5. Operating Profit Margin – This ratio helps in assessing the operational efficiency as well as

effectiveness of the business. It determines the amount of profit which is left after meeting all

the business expenses and variable cost expenses in form of wages, raw material etc. The

operating profit margin for ASOS Plc is 4.22 and for Boohoo it is 7.42. For investor it is better

to take a view over the behaviour of operating profit ratio of the company. It is having

increasing trend than it is considered as a better option to invest in.

6. Net Profit Margin – It is the amount of profit or a part of revenue which is left after deducting

all the business expenses from the sales made by the business for a specific period of time. 3.41

& 5.52 is the amount of net profit which both the company has made after meeting all its

expenses.

7. Return on Assets – This term of financial ratio define how effectively the company is using its

assets as well as other resources for earning more profit. This ratio provides detail about the

effectiveness of business in making use of its assets with the objective of high profitability and

improving business performance as well. ASOS Plc is earning a return of 0.08 on its assets &

Boohoo Group is making a return of 0.10 from utilizing its business assets.

8. Return on Capital employed – This ratio reveals amount of profit or revenue made by the

company in comparison with the amount of its shareholder equity. This ratio defines how

effectively the company has makes use of its equity capital for generating more profit. The

return earned by ASOS Plc on its equity is 0.18 and 0.14 by Boohoo Group Plc.

For completion of this report two companies has been selected named as ASOS Plc and Boohoo

Group Plc. Both the companies are operating in the same sector and are giving competition to each

other. In case of ASOS Plc., the company is operating in the field of retail business especially in

fashion and cosmetic products. Also, the company is conducting its business operations with the help of

online marketing i.e. online shopping. It is having its online business with over 850 brands dealing in

196 countries. Currently the company is employing 4386 number of employees and having revenue of

around £2.4 billion (ASOS ANNUAL Report, 2018). On the other hand, Boohoo Group Plc is a UK

based retail company engaged in the online business of fashion. The specialization of this company is

its own brand fashion clothing with more than 36,000 products. The company is having revenue of

£580 million with 2175 number of employees.

For making proper comparison between these two companies following ratios has been determined:

Ratios ASOS Plc Boohoo Group Plc

Current Ratio 0.90 2.06

Acid Test Ratio 0.17 1.60

Debtor days 6.43 8.71

Creditor days 170.01 44.51

Operating Profit Margin 4.22 7.42

Net Profit Margin 3.41 5.52

Return on Assets 0.08 0.10

Return on Capital employed 0.18 0.14

In case of analysis of sector specific company, following are the impact on the uses of financial ratio:

1. Different companies uses different accounting methods and standards for making their financial

statements and reports, as a result of it becomes difficult to make comparative analysis between

both the companies (Le, H. L. and Tran, 2018).

2. In case of non sector specific company, analysis of financial ratio is difficult because both the

effectiveness of business in making use of its assets with the objective of high profitability and

improving business performance as well. ASOS Plc is earning a return of 0.08 on its assets &

Boohoo Group is making a return of 0.10 from utilizing its business assets.

8. Return on Capital employed – This ratio reveals amount of profit or revenue made by the

company in comparison with the amount of its shareholder equity. This ratio defines how

effectively the company has makes use of its equity capital for generating more profit. The

return earned by ASOS Plc on its equity is 0.18 and 0.14 by Boohoo Group Plc.

For completion of this report two companies has been selected named as ASOS Plc and Boohoo

Group Plc. Both the companies are operating in the same sector and are giving competition to each

other. In case of ASOS Plc., the company is operating in the field of retail business especially in

fashion and cosmetic products. Also, the company is conducting its business operations with the help of

online marketing i.e. online shopping. It is having its online business with over 850 brands dealing in

196 countries. Currently the company is employing 4386 number of employees and having revenue of

around £2.4 billion (ASOS ANNUAL Report, 2018). On the other hand, Boohoo Group Plc is a UK

based retail company engaged in the online business of fashion. The specialization of this company is

its own brand fashion clothing with more than 36,000 products. The company is having revenue of

£580 million with 2175 number of employees.

For making proper comparison between these two companies following ratios has been determined:

Ratios ASOS Plc Boohoo Group Plc

Current Ratio 0.90 2.06

Acid Test Ratio 0.17 1.60

Debtor days 6.43 8.71

Creditor days 170.01 44.51

Operating Profit Margin 4.22 7.42

Net Profit Margin 3.41 5.52

Return on Assets 0.08 0.10

Return on Capital employed 0.18 0.14

In case of analysis of sector specific company, following are the impact on the uses of financial ratio:

1. Different companies uses different accounting methods and standards for making their financial

statements and reports, as a result of it becomes difficult to make comparative analysis between

both the companies (Le, H. L. and Tran, 2018).

2. In case of non sector specific company, analysis of financial ratio is difficult because both the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

companies are dealing different business operations and thus different accounting principles and

standards will be applicable to them making it irrelevant to make comparison between both.

3. For example – in case of banking companies their financial statements doesn't provide deep

insight about sales, revenue and other business operations which other company's financials

makes. Thus, it is sometime impossible to make profitability analysis of these banking company

thereby making it difficult to make effective investment decision.

Though financial ratios are considered as one of the best measures for making investment

decision but on the flip side it has some limitations as well which has to be taken into consideration

before making any crucial financial and investment related decision. Following are the limitation of

financial ratio which are as follows:

1. Companies of different sector has to face different environmental conditions such as market

forces, regulations, policies, taxation law which influences the working of business. Because of

these factors, it is very difficult to make accurate comparison between two companies from

different industry base. This can lead to misleading in terms of interpretation of financial ratio

(LIGOCKÁ, 2019).

2. Most of the time different accounting polices, standards and methods are used by companies for

making valuation of its business transaction such as assets, inventory etc. For example for

valuing the total inventory level of the business, one company adopts FIFO method while

another prefer LIFO one. Thus, because of different methodologies used by companies, it is

difficult to make proper comparison on the basis of ratio.

3. Financial ratio of the company is calculated on the basis of accounting as well as financial

information as provided by its financial statements. The accounting information provided in this

financials are subject to many deficiencies, errors, mistakes or manipulation made at the time of

recording of accounting and other business transactions. Because of this factor, it is difficult to

make correct and reliable interpretation.

4. The main focus of ratio analysis is on explaining the relationship between past information

whereas investors or end users have concern about the current as well as future business

information.

Different companies tries to perform at their best in comparison with its rivalry firm in different

manner so as to seek competitive advantage in the market. For improving the overall business

performance level, it is very essential on part of the management of the company to formulate sound

and effective business strategies and plans.

Affordable pricing strategies – By charging fair and affordable price for its products and services, a

standards will be applicable to them making it irrelevant to make comparison between both.

3. For example – in case of banking companies their financial statements doesn't provide deep

insight about sales, revenue and other business operations which other company's financials

makes. Thus, it is sometime impossible to make profitability analysis of these banking company

thereby making it difficult to make effective investment decision.

Though financial ratios are considered as one of the best measures for making investment

decision but on the flip side it has some limitations as well which has to be taken into consideration

before making any crucial financial and investment related decision. Following are the limitation of

financial ratio which are as follows:

1. Companies of different sector has to face different environmental conditions such as market

forces, regulations, policies, taxation law which influences the working of business. Because of

these factors, it is very difficult to make accurate comparison between two companies from

different industry base. This can lead to misleading in terms of interpretation of financial ratio

(LIGOCKÁ, 2019).

2. Most of the time different accounting polices, standards and methods are used by companies for

making valuation of its business transaction such as assets, inventory etc. For example for

valuing the total inventory level of the business, one company adopts FIFO method while

another prefer LIFO one. Thus, because of different methodologies used by companies, it is

difficult to make proper comparison on the basis of ratio.

3. Financial ratio of the company is calculated on the basis of accounting as well as financial

information as provided by its financial statements. The accounting information provided in this

financials are subject to many deficiencies, errors, mistakes or manipulation made at the time of

recording of accounting and other business transactions. Because of this factor, it is difficult to

make correct and reliable interpretation.

4. The main focus of ratio analysis is on explaining the relationship between past information

whereas investors or end users have concern about the current as well as future business

information.

Different companies tries to perform at their best in comparison with its rivalry firm in different

manner so as to seek competitive advantage in the market. For improving the overall business

performance level, it is very essential on part of the management of the company to formulate sound

and effective business strategies and plans.

Affordable pricing strategies – By charging fair and affordable price for its products and services, a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company can improves its market profit as well as customer base. Company should assess the pricing

strategies which its competitor firms has been used for making profits for long time.

Improving its marketing strategy – It is very important on part of every business organisation to have

strong and effective marketing and promotional business activities (Zietlow and et.al., 2018). With

better and innovative marketing skill and strategies, a company can attract large number of customers

and thus earn earn profitability.

Implementing better strategies for promoting of its products and services – With the help of

various business tools such as Bench marking and Balance scorecard, a company can make comparison

of its own business performance with the best profit making companies of the same sector industry.

Adoption of business strategies, plans which rivalry and profit making companies are using should be

done for increasing the overall sales of the company (Fields, 2016).

Conducting of research and development process – For determining the current market trends and

demand forces, it is very essential on the part of every business organisation to conduct research,

survey activities. This will help the company in assessing the taste and preferences of customer in the

market and thus can carry on its production function accordingly. It will also help the company in

improving its operational efficiency of business.

Better business strategies and plans – A company should always focus on framing of sound and

effective business strategies and plans in line with its objectives and goals. It is very important to

implement new and improved business operations in a cost effective manner with focus on

maximization of profit margin.

Risk and opportunities faced by companies are as follows:

ASOS Plc.

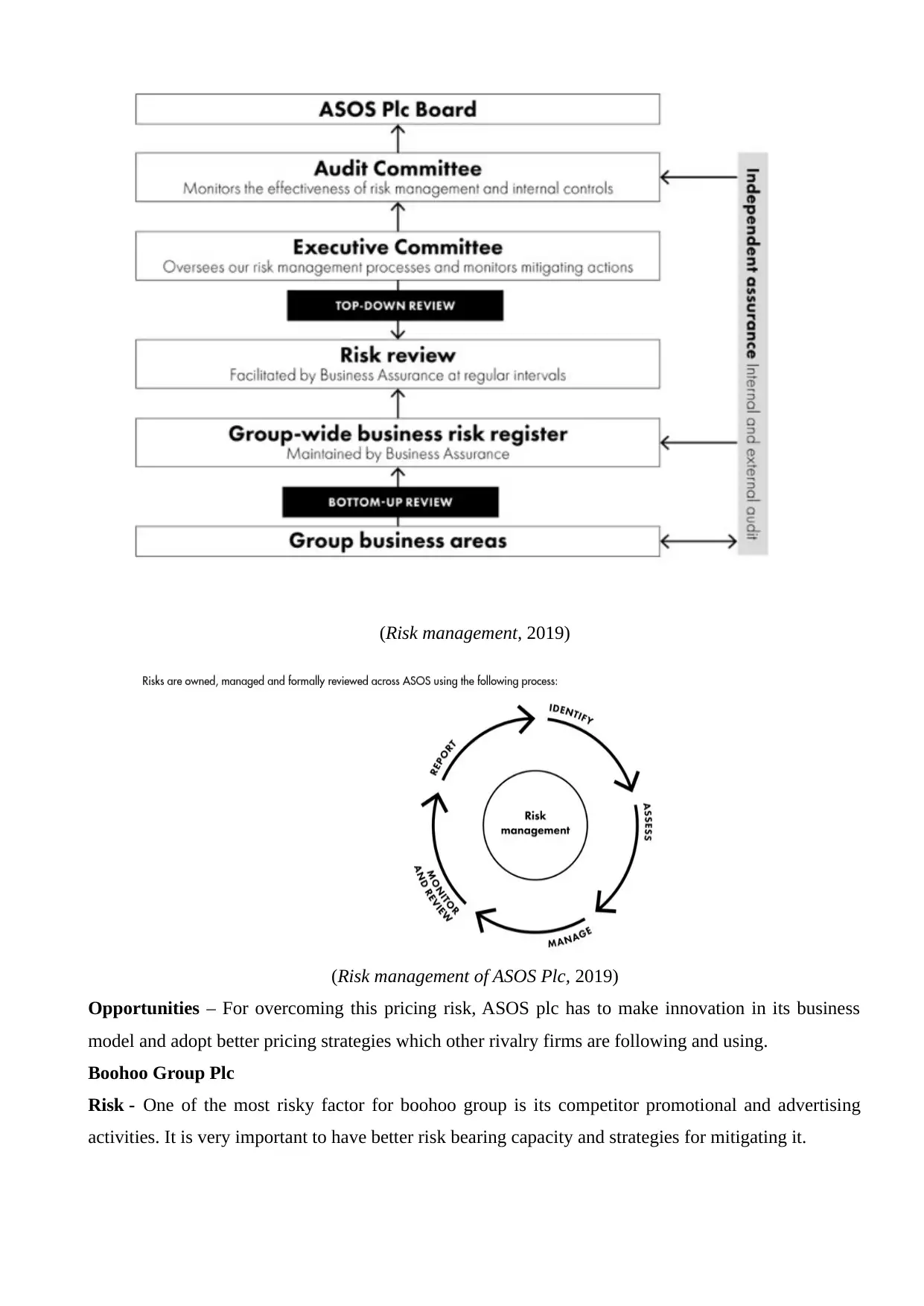

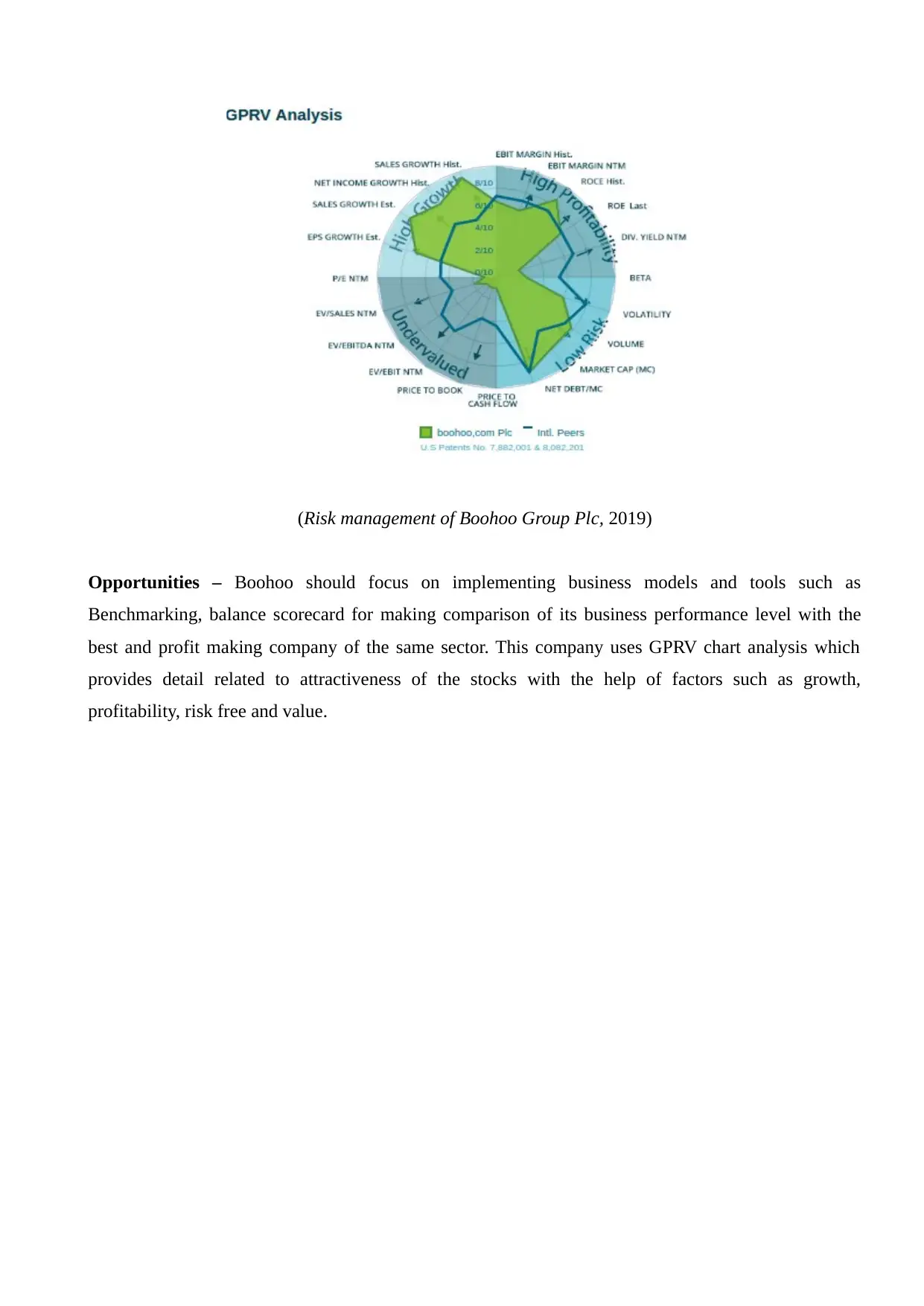

Risk – Risk faced by ASOS plc is related to high competition prevailing in the current market. Many

competitive firm are also their as a result of which the profit margin of ASOS plc is decreasing. The

main risk faced is related to pricing for which company has framed following steps and process:

strategies which its competitor firms has been used for making profits for long time.

Improving its marketing strategy – It is very important on part of every business organisation to have

strong and effective marketing and promotional business activities (Zietlow and et.al., 2018). With

better and innovative marketing skill and strategies, a company can attract large number of customers

and thus earn earn profitability.

Implementing better strategies for promoting of its products and services – With the help of

various business tools such as Bench marking and Balance scorecard, a company can make comparison

of its own business performance with the best profit making companies of the same sector industry.

Adoption of business strategies, plans which rivalry and profit making companies are using should be

done for increasing the overall sales of the company (Fields, 2016).

Conducting of research and development process – For determining the current market trends and

demand forces, it is very essential on the part of every business organisation to conduct research,

survey activities. This will help the company in assessing the taste and preferences of customer in the

market and thus can carry on its production function accordingly. It will also help the company in

improving its operational efficiency of business.

Better business strategies and plans – A company should always focus on framing of sound and

effective business strategies and plans in line with its objectives and goals. It is very important to

implement new and improved business operations in a cost effective manner with focus on

maximization of profit margin.

Risk and opportunities faced by companies are as follows:

ASOS Plc.

Risk – Risk faced by ASOS plc is related to high competition prevailing in the current market. Many

competitive firm are also their as a result of which the profit margin of ASOS plc is decreasing. The

main risk faced is related to pricing for which company has framed following steps and process:

(Risk management, 2019)

(Risk management of ASOS Plc, 2019)

Opportunities – For overcoming this pricing risk, ASOS plc has to make innovation in its business

model and adopt better pricing strategies which other rivalry firms are following and using.

Boohoo Group Plc

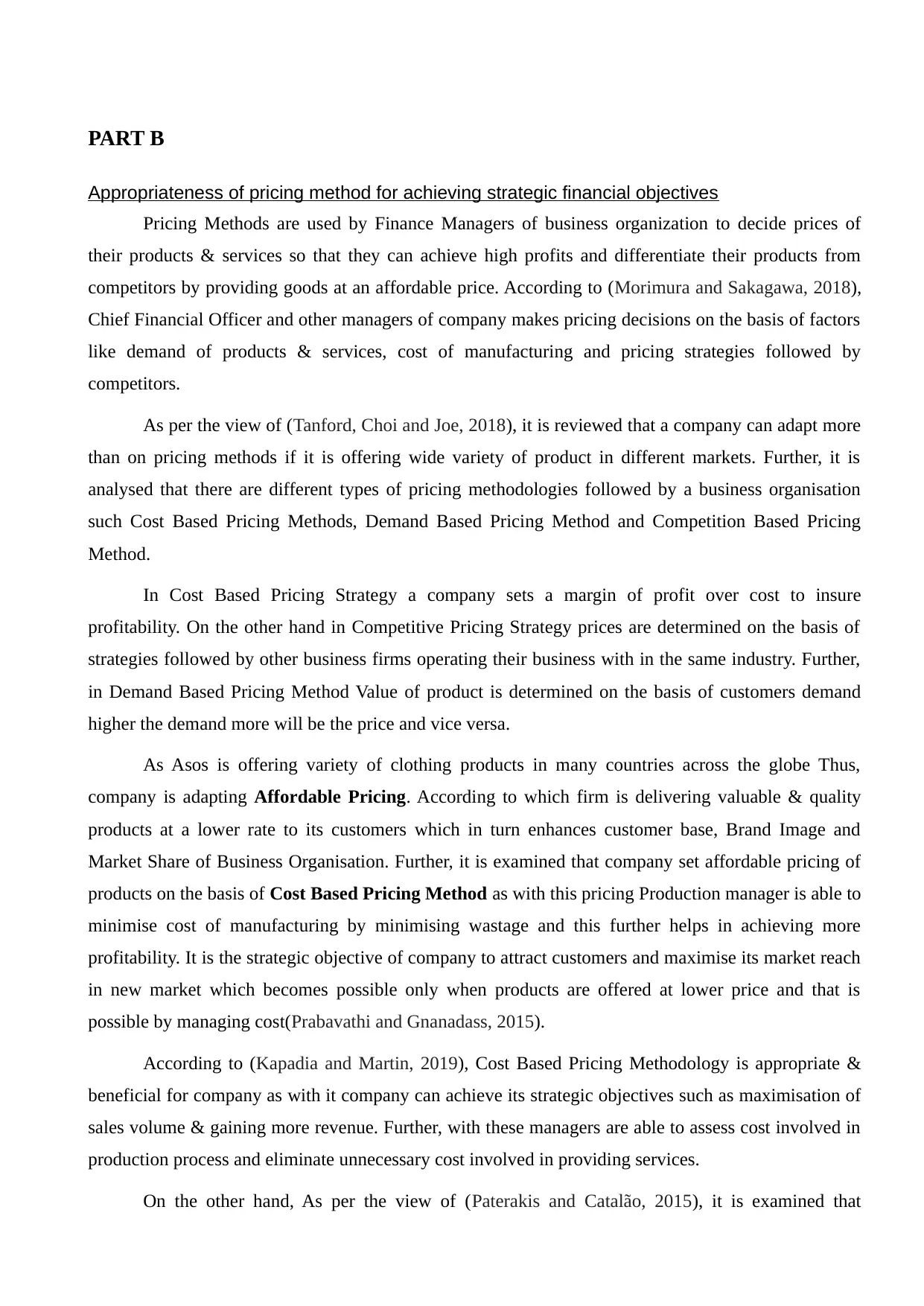

Risk - One of the most risky factor for boohoo group is its competitor promotional and advertising

activities. It is very important to have better risk bearing capacity and strategies for mitigating it.

(Risk management of ASOS Plc, 2019)

Opportunities – For overcoming this pricing risk, ASOS plc has to make innovation in its business

model and adopt better pricing strategies which other rivalry firms are following and using.

Boohoo Group Plc

Risk - One of the most risky factor for boohoo group is its competitor promotional and advertising

activities. It is very important to have better risk bearing capacity and strategies for mitigating it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Risk management of Boohoo Group Plc, 2019)

Opportunities – Boohoo should focus on implementing business models and tools such as

Benchmarking, balance scorecard for making comparison of its business performance level with the

best and profit making company of the same sector. This company uses GPRV chart analysis which

provides detail related to attractiveness of the stocks with the help of factors such as growth,

profitability, risk free and value.

Opportunities – Boohoo should focus on implementing business models and tools such as

Benchmarking, balance scorecard for making comparison of its business performance level with the

best and profit making company of the same sector. This company uses GPRV chart analysis which

provides detail related to attractiveness of the stocks with the help of factors such as growth,

profitability, risk free and value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

Appropriateness of pricing method for achieving strategic financial objectives

Pricing Methods are used by Finance Managers of business organization to decide prices of

their products & services so that they can achieve high profits and differentiate their products from

competitors by providing goods at an affordable price. According to (Morimura and Sakagawa, 2018),

Chief Financial Officer and other managers of company makes pricing decisions on the basis of factors

like demand of products & services, cost of manufacturing and pricing strategies followed by

competitors.

As per the view of (Tanford, Choi and Joe, 2018), it is reviewed that a company can adapt more

than on pricing methods if it is offering wide variety of product in different markets. Further, it is

analysed that there are different types of pricing methodologies followed by a business organisation

such Cost Based Pricing Methods, Demand Based Pricing Method and Competition Based Pricing

Method.

In Cost Based Pricing Strategy a company sets a margin of profit over cost to insure

profitability. On the other hand in Competitive Pricing Strategy prices are determined on the basis of

strategies followed by other business firms operating their business with in the same industry. Further,

in Demand Based Pricing Method Value of product is determined on the basis of customers demand

higher the demand more will be the price and vice versa.

As Asos is offering variety of clothing products in many countries across the globe Thus,

company is adapting Affordable Pricing. According to which firm is delivering valuable & quality

products at a lower rate to its customers which in turn enhances customer base, Brand Image and

Market Share of Business Organisation. Further, it is examined that company set affordable pricing of

products on the basis of Cost Based Pricing Method as with this pricing Production manager is able to

minimise cost of manufacturing by minimising wastage and this further helps in achieving more

profitability. It is the strategic objective of company to attract customers and maximise its market reach

in new market which becomes possible only when products are offered at lower price and that is

possible by managing cost(Prabavathi and Gnanadass, 2015).

According to (Kapadia and Martin, 2019), Cost Based Pricing Methodology is appropriate &

beneficial for company as with it company can achieve its strategic objectives such as maximisation of

sales volume & gaining more revenue. Further, with these managers are able to assess cost involved in

production process and eliminate unnecessary cost involved in providing services.

On the other hand, As per the view of (Paterakis and Catalão, 2015), it is examined that

Appropriateness of pricing method for achieving strategic financial objectives

Pricing Methods are used by Finance Managers of business organization to decide prices of

their products & services so that they can achieve high profits and differentiate their products from

competitors by providing goods at an affordable price. According to (Morimura and Sakagawa, 2018),

Chief Financial Officer and other managers of company makes pricing decisions on the basis of factors

like demand of products & services, cost of manufacturing and pricing strategies followed by

competitors.

As per the view of (Tanford, Choi and Joe, 2018), it is reviewed that a company can adapt more

than on pricing methods if it is offering wide variety of product in different markets. Further, it is

analysed that there are different types of pricing methodologies followed by a business organisation

such Cost Based Pricing Methods, Demand Based Pricing Method and Competition Based Pricing

Method.

In Cost Based Pricing Strategy a company sets a margin of profit over cost to insure

profitability. On the other hand in Competitive Pricing Strategy prices are determined on the basis of

strategies followed by other business firms operating their business with in the same industry. Further,

in Demand Based Pricing Method Value of product is determined on the basis of customers demand

higher the demand more will be the price and vice versa.

As Asos is offering variety of clothing products in many countries across the globe Thus,

company is adapting Affordable Pricing. According to which firm is delivering valuable & quality

products at a lower rate to its customers which in turn enhances customer base, Brand Image and

Market Share of Business Organisation. Further, it is examined that company set affordable pricing of

products on the basis of Cost Based Pricing Method as with this pricing Production manager is able to

minimise cost of manufacturing by minimising wastage and this further helps in achieving more

profitability. It is the strategic objective of company to attract customers and maximise its market reach

in new market which becomes possible only when products are offered at lower price and that is

possible by managing cost(Prabavathi and Gnanadass, 2015).

According to (Kapadia and Martin, 2019), Cost Based Pricing Methodology is appropriate &

beneficial for company as with it company can achieve its strategic objectives such as maximisation of

sales volume & gaining more revenue. Further, with these managers are able to assess cost involved in

production process and eliminate unnecessary cost involved in providing services.

On the other hand, As per the view of (Paterakis and Catalão, 2015), it is examined that

Competition Based Pricing is more appropriate for Asos Plc as it is an International Retail company

and Competition in retail sector is increasing day by day thus, it is beneficial for finance manager of

company to follow Competitive Pricing because if firm sets prices of products in accordance with

strategies followed by other companies than it is able to formulate effective pricing which influence

customers to purchase products from Asos Plc only.

Further, it is reviewed that this method increases profits of Asos Plc which in turn maximises

shareholders value with that more shareholders show their interest in investing in shares of company.

This in turn helps company in achieving its strategic objective of maximising value of its share capital

under UK Stock Exchange. Further, Asos Plc can also achieve its objective of maximising Market

Share if company is able to offer better products at a price which is attractive than other competitors.

Company is also using Zonal Based Pricing according to different geographical area.

Thus, it is evaluated that both Cost Based Pricing Method & Competitive Pricing Methods are

suitable for Asos Plc.

CONCLUSION

From the above report it can be concluded that, by having sound financial management in the company

it will help in proper an effective allocation of funds and business resources. The report has discussed

how with the help of financial ratio, a comparative analysis can be made between two companies. This

analysis thus can be helpful for investors in making better and correct interpretation about the financial

as well as liquidity position of the company.

RECOMMENDATIONS

It is recommended to both the companies to follow better accounting standards and policies at the time

of preparation of its own financial statements and reports. Also, proper compliance should be made by

company related to disclosure of all the material information in its financials so that it can provide

better interpretation to its investor.

and Competition in retail sector is increasing day by day thus, it is beneficial for finance manager of

company to follow Competitive Pricing because if firm sets prices of products in accordance with

strategies followed by other companies than it is able to formulate effective pricing which influence

customers to purchase products from Asos Plc only.

Further, it is reviewed that this method increases profits of Asos Plc which in turn maximises

shareholders value with that more shareholders show their interest in investing in shares of company.

This in turn helps company in achieving its strategic objective of maximising value of its share capital

under UK Stock Exchange. Further, Asos Plc can also achieve its objective of maximising Market

Share if company is able to offer better products at a price which is attractive than other competitors.

Company is also using Zonal Based Pricing according to different geographical area.

Thus, it is evaluated that both Cost Based Pricing Method & Competitive Pricing Methods are

suitable for Asos Plc.

CONCLUSION

From the above report it can be concluded that, by having sound financial management in the company

it will help in proper an effective allocation of funds and business resources. The report has discussed

how with the help of financial ratio, a comparative analysis can be made between two companies. This

analysis thus can be helpful for investors in making better and correct interpretation about the financial

as well as liquidity position of the company.

RECOMMENDATIONS

It is recommended to both the companies to follow better accounting standards and policies at the time

of preparation of its own financial statements and reports. Also, proper compliance should be made by

company related to disclosure of all the material information in its financials so that it can provide

better interpretation to its investor.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.